The COVID-19 pandemic showed the strength of broadband networks in the United States, yet it also underscored that all Americans need — and deserve — better access to the economic, educational, health care, and civic opportunities that have moved increasingly online.

Fortunately, closing the rural broadband gap has gained bipartisan support and is a priority for both Congress and the White House. President Joe Biden’s American Jobs Plan calls for $100 billion in federal funding to bring high-speed broadband coverage to 100% of Americans, including those living in rural areas that have been left behind. Data collected by the Federal Communications Commission (FCC) indicates that nearly 5% of the U.S. population does not have access to fixed broadband service that provides a minimum of 25 megabits per second (Mbps) download and 3 Mbps upload — the so-called “25/3” standard the FCC currently uses as the definition for “broadband.”

The light touch regulatory approach in the U.S. has encouraged substantial private investment for broadband networks in both urban and suburban areas of the country. Over the past quarter century, the broadband industry has invested almost $2 trillion to build infrastructure that brings broadband access to nearly 96% of Americans. This is commendable progress and unparalleled innovation, but it is simply not enough when more than 14.5 million Americans are unable to access high-speed internet (25/3 Mbps) at home, and more than 11 million of those people live in rural areas.

This paper examines past achievements and failures to close the rural broadband gap and proposes pragmatic changes to ensure that future attempts to connect rural America are poised for success.

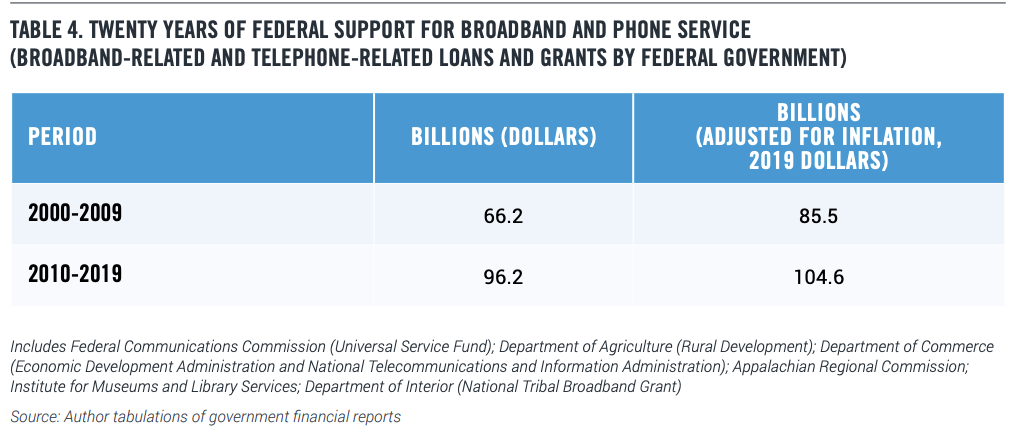

As policymakers work toward a solution, history tells a cautionary tale about how easy it can be for federal funding to be misspent in ways that do not appreciably contribute to enhancing rural broadband access and closing the digital divide. By our count, the federal government has spent $105 billion on broadband- and telephone-related initiatives from 2010 through 2019, on top of $86 billion from 2000 to 2009. (These figures include both grants and loans and are reported in 2019 dollars).

Where did this federal money go? Some of it went toward expanding access and closing the rural broadband gap and achieved measurable success. In particular, the Connect America Fund Phase II (CAF II) and Rural Digital Opportunity Fund (RDOF) reverse auctions conducted by the FCC in 2018 and 2020 allowed providers to bid for the right to provide subsidized broadband service to unserved locations at the lowest cost to the government. The reverse auctions were troubled in some important respects, as this paper will discuss, but hold the potential to extend broadband service to rural areas if revamped. However, overall progress has been slow and does not appear commensurate with the substantial federal funding over the past two decades, especially in unserved rural areas of the country where the cost of broadband deployment is especially high.

The problems with past funding efforts fall into three categories:

The pandemic demonstrated the growing and immediate importance of every American having access to sufficient internet speeds for work, school, health care, and social activities. President Biden and Congress seem ready to provide a sizable pot of money to bridge the digital divide gap. But no matter how many billions of dollars are allocated, history shows that the money can be spent unwisely if policymakers are not careful.

This paper will dive deeper into the challenges with previous funding programs, what has worked, and where the challenges remain. While the focus of this paper is on access and not affordability, it’s important to note that only 2.6% of personal consumer spending went to “communications services” — a basket including all consumer outlays on cable and satellite television, video and audio streaming, wired and wireless phone service, and internet service — in 2020 and fell by 3% from 2007 to 2020. At the same time, internet service providers (ISPs) have set up programs to make broadband more affordable to low-income families, which have successfully brought millions of previously unconnected Americans online.

All of this suggests we may have found a proper balance between affordability and investment, notwithstanding the apparent gap in access for rural communities. We recommend three pragmatic principles for ensuring that the rural broadband access gap is closed.

We have a once in a lifetime opportunity to finally connect all of rural America, but only if we don’t repeat the mistakes of the past. The funding for broadband after the financial crisis of 2008-2009 was supposed to close the rural accessibility gap, but the programs were mismanaged and spread out over far too many unrelated purposes. It is time to bring broadband to all of the unserved people across America and to reach the president’s target of 100% connectivity. By following this pragmatic roadmap, we can finally achieve this goal.

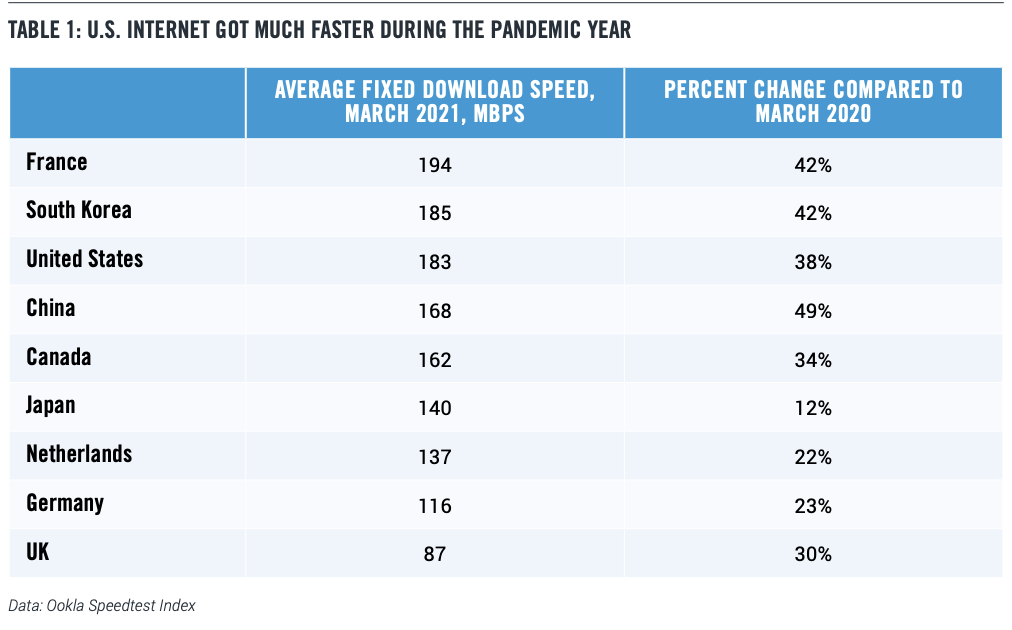

The COVID-19 pandemic has shown the strength of broadband networks in the United States. Faced with an unprecedented shift to virtual work, education, and entertainment, the nation’s broadband networks barely shrugged in handling the dramatic increase in use. Download speeds dipped very slightly at the beginning of the pandemic, then quickly rebounded. Meanwhile, the decline in download speeds in major European countries was much deeper, lasted longer, and required government officials to step in and ask YouTube, Netflix, and other streaming services to downgrade their content to prevent the internet from breaking.

Moreover, the speed of the U.S. broadband network continued to rise during the pandemic year. Average fixed broadband download speeds rose by 38% between March 2020 and March 2021, according to Ookla data. As Table 1 shows, the U.S. is clearly in the top tier of major countries based on average download speed and performance improvements, along with South Korea, China and France, and well ahead of Japan, Netherlands, Germany and the United Kingdom.

The successful and resilient performance shown by U.S. broadband networks both in the early stages of the pandemic and the year that followed was a direct result of the substantial private investment made by the U.S. broadband industry over the past quarter century. From 1996 to 2019, the broadband industry invested $1.78 trillion to build infrastructure that brings broadband access to nearly 96% of Americans.

The triumph of this private investment should remove and relieve any lingering doubts as to the relative merits of the U.S. light-touch approach to broadband regulation over the more heavily regulated, utility-style common carrier approach favored in Europe. Indeed, OECD figures show that U.S. telecommunications investment per capita in 2018 was more than twice that of Europe.

The substantial discrepancy in investment per capita can be traced to the markedly different broadband network investment incentives that have existed for some time. In the United States, ISPs own their networks and have an incentive to invest, whereas Europe has pursued the “leased access” path where transmission lines are leased at heavily regulated rates, thereby reducing the incentives for wireline incumbents to further invest in their networks for fear of not getting a sufficient investment return. The success of U.S. broadband networks during the current COVID-19 crisis is clear and worthy of the praise it has garnered from all sides. As the Broadband Internet Technical Advisory Group wrote in an April 2021 report, “available data suggests that the internet has performed well during the pandemic … and is a testament to the importance of continued investment in robust Internet infrastructure in all parts of the ecosystem.” The report went on to note that “ISPs reacted to the sudden demand increase by rapidly adding extraordinary amounts of new capacity and pledging to Keep Americans Connected.”

In 2020 the FCC also ran the Rural Digital Opportunity Fund (“RDOF”) reverse auction, which allocated $9.2 billion to 180 bidders over 10 years to provide broadband to 5.2 million locations, at an average bid of $177 per location per year. That’s the average amount of public support that providers will get if they provide the level of broadband that they bid for. Of course, the public support covers only part of the cost of rural broadband, with private sector providers in particular drawing on private funding to make up the difference.

RDOF followed in the heels of the FCC’s first broadband reverse auction (CAF II). CAF II allocated $1.49 billion over 10 years to 103 bidders to provide access to over 700,000 locations. That’s an average of $209 per year per location in public support. Reverse auctions like RDOF and CAF II have potential for funding network build-out in rural areas, with some important changes that we discuss later.

When the FCC unveiled the National Broadband Plan in 2010, it identified broadband as “the great infrastructure challenge of the early 21st century.” How well have we met that challenge so far?

The plan set the National Broadband Availability Target at “[a]ctual download speeds of at least 4 Mbps and actual upload speeds of at least 1 Mbps.” While this seems excruciatingly slow today, that target was mostly in line at the time with similar national targets in countries such as France, Germany, and the United Kingdom. The FCC estimated that 14 million people, or 4.5% of the population, did not “have access to terrestrial broadband infrastructure capable of meeting the National Broadband Availability Target.” As the plan said:

…it is unlikely that private investment alone will fill the broadband availability gap. The question, then, is how much public support will be required to fill the gap … An FCC analysis finds that the level of additional funding required is approximately $24 billion (present value in 2010 dollars)

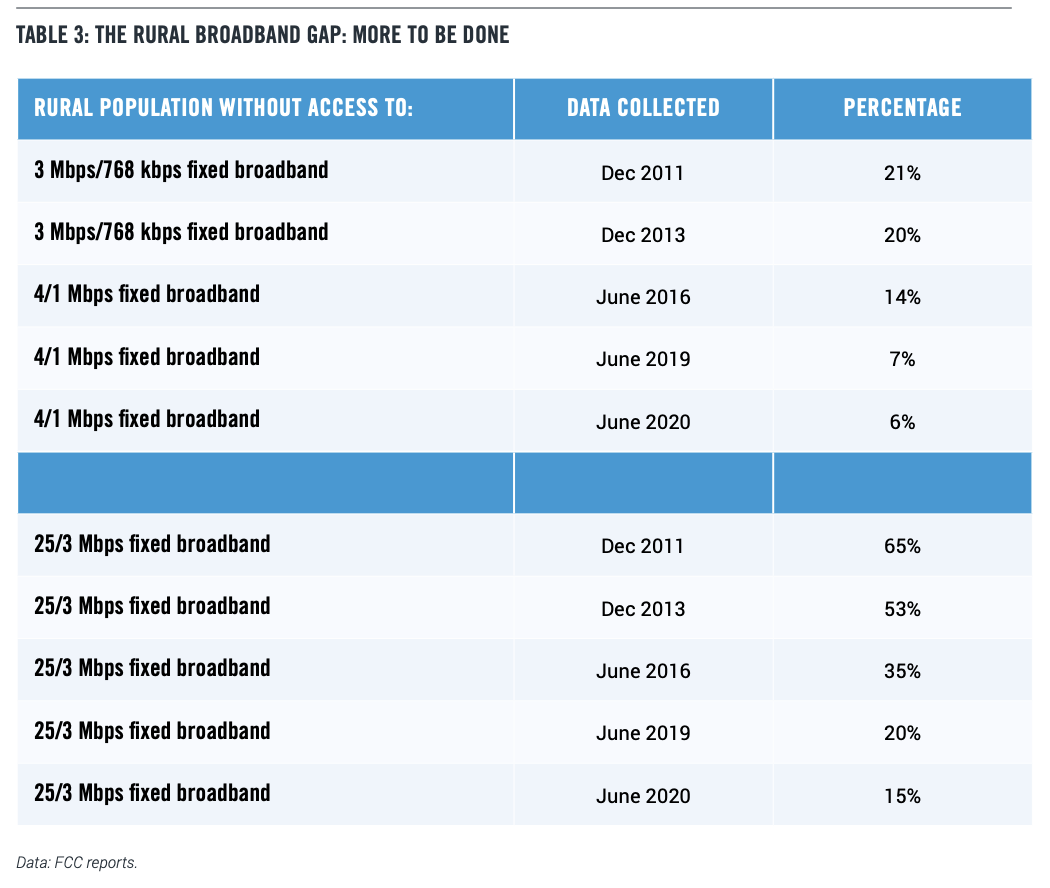

Today, 1.8% of the population does not have access to 4/1 terrestrial broadband, mostly in rural areas. This represents a bare minimum for emails.

The 2010 broadband plan also had a 10-year goal that “[a]t least 100 million U.S. homes should have affordable access to actual download speeds of at least 100 megabits per second and actual upload speeds of at least 50 megabits per second.” Today, there are roughly 130 million households in the U.S. and roughly 92% of Americans have access to 100/10 service according to June 2020 broadband deployment data. So, the download speed goal from 10 years ago has been met. These gains were made mainly through private investment. Presentations to the FCC in 2010 cited $350 billion as the estimated cost of giving every American household access to 100 Mbps service, which was virtually non-existent at that point.

This paper focuses on issues of access, not affordability. Still, it is worth noting that this mass deployment of broadband has not broken the bank for American households. Since the business cycle peak of 2007, internet access has been getting cheaper relative to most other goods and services, according to the Bureau of Economic Analysis. From 2007 to 2020, the price of internet access only rose by 4% (Table 2). US Telecom reports that the price of the most popular tier of broadband service fell by 20% from 2015 to 2020, while offering almost 16% faster service. By contrast, the overall price index for consumer spending on goods and services rose by 22% over the same stretch, while the price of eating out at restaurants rose by 43%.

We also analyzed the changing price and spending for what we call “communications services” — a broad basket including all consumer outlays on internet access, cable, and satellite television, video and audio streaming, and wired and wireless phone service. This broad basket illuminates not just the price of broadband but the way that broadband is used to enable other services.

We found that the price of communications services fell by 3% from 2007 to 2020. Moreover, we calculate that only 2.6% of personal consumer spending went to “communications services” in 2020. That’s equal to the average since 2000, with no sign of an upward trend. People are aware of how much they spend on broadband, but they forget about the long distance and local telephone bills that they used to pay.

The average, of course, doesn’t tell us about what low-income families are spending. However, major ISPs have set up programs to make broadband more affordable to low-income families, which have successfully brought millions of previously unconnected Americans online. According to an April 2021 study from BroadbandNow, 77% of Americans have access to low-priced wired broadband plans, up from 50% a year earlier.

This paper focuses on the persistent rural broadband access gap.23 While almost everyone has access to 4/1 broadband service, as Table 3 shows, the FCC’s 2020 Broadband Progress Report identifies 25/3 broadband as the target level for broadband services. That is sufficient, for example, to enable a Zoom connection for group video calls, according to the company’s published requirements.

However, by that goal, 15% of rural Americans still do not have access to sufficient broadband — a significant gap. Moreover, as discussed later in this paper, this figure almost certainly underestimates the percentage of rural Americans that are unserved by broadband.

Why the rural broadband gap? Despite the declining cost of broadband and robust competition, fixed broadband remains out of reach for many rural Americans, due largely to the economic costs and engineering challenges involved with connecting remote areas. Fewer potential customers within reach of each mile of new infrastructure means less potential revenue over time to pay back the upfront cost of the infrastructure investment.24 Indeed, deploying a robust broadband network over the wide expanse of rural areas requires not only the substantial costs to deploy wires over long distance, but the increased costs for those wires to attach to, and in many cases to replace, exponentially more poles as compared to a smaller and more densely populated urban environment.

The United States is far less dense than a country like South Korea, which is less than half the size of Minnesota with 10 times as many people. That is why connecting everyone in South Korea is easier than in the United States.

But low average density is not the only issue. The United States also has the disadvantage of a very spread-out population — many rural areas with low but significant populations. By contrast, countries like Australia and Canada have low average density, but their populations are very concentrated, making them easier to serve. In Australia, 90% of the population live in 4% of the land, concentrated on the coasts. In Canada, 90% of the population live in 3% of the land. By contrast, in the United States, 90% of the population is spread out over 31% of the land area.25 That’s a whole different engineering challenge.

As a result of these geographic and demographic characteristics in the United States, the economic margin for error for rural broadband is small for providers and the potential return on an investment is challenging. Significantly, broadband providers who build in rural areas cannot expect 25 years of technology stability and protected markets. Broadband speeds have been a moving target. What was acceptable in 2010 is no longer acceptable today. Broadband providers must upgrade their systems at substantial cost to stay current with technology, thereby further narrowing the margin for error.

Moreover, fixed broadband providers in rural areas face competition from alternative technologies such as mobile broadband, fixed wireless, and satellite internet. One can debate endlessly the degree to which a mobile connection is a full substitute for fixed broadband but that’s not the point. People who mostly use a limited number of applications such as email, e-commerce, and social networks may choose to only spend on their smartphone subscriptions, which eats away at potential revenues for fixed broadband providers, yet another reduction in the razor thin margin for error to deploy rural broadband.

Given the economics of broadband deployment, it’s clear that public subsidies have and will continue to play a critical role to make broadband infrastructure economically viable in many rural areas of the country. To date, substantial federal resources have been devoted to deploying rural broadband. For this paper, we undertook a detailed look at how much federal agencies have spent on broadband and telephone-related initiatives over the past 20 years. (We count federal spending on telephone service in the total because the earliest broadband efforts focused on DSL (digital subscriber line), which ran over ordinary telephone lines).

Our analysis shows the federal government has spent $104.6 billion on broadband- and telephone-related initiatives from 2010 to 2019 (Table 4). That’s on top of $85.5 billion spent from 2000 to 2009. These totals include both grants and loans, and are reported in 2019 dollars.

The biggest sum has come from the FCC, including the agency’s Universal Service Fund (USF) program. Funding for the USF program does not come from general tax revenues, but from telecommunications service provider contributions, the cost of which is typically passed through to consumers. The USF provided support through four programs: the High Cost program (now known as the Connect America Fund), which supports the extension of advanced communications networks to rural, insular, and high-cost areas; the E-rate program, which helps rural and urban schools and libraries obtain affordable telecommunications services and broadband; the Lifeline program, which supports low-income users; and the Rural Health Care Program, which provides funding to eligible rural health care providers for telecommunications and broadband services.

In addition to the USF, the federal government has launched multiple initiatives intended to increase broadband availability and usage, including massive efforts from the Departments of Agriculture and Commerce, and small independent agencies like the Appalachian Regional Commission and the Institute for Museum and Library Services.

Why hasn’t this federal expenditure been enough? Why hasn’t the rural broadband gap closed more as a result of this massive funding? While the substantial investment by the federal government demonstrates and confirms the importance policy makers have placed on broadband connectivity throughout the United States, including rural areas, the high level of, and long-standing, federal support has not delivered the universal connectivity many hoped for and expected. Indeed, most of these federal rural broadband initiatives cannot even provide a specific number as to how many previously unconnected homes were connected during the initiative.

It’s clear in retrospect that much of the money was not correctly targeted. Let’s consider, in particular, the American Recovery and Reinvestment Act (ARRA) of 2009. Like the postpandemic infrastructure proposal, ARRA used a major economic downturn as a springboard to solving the rural broadband problem.

ARRA included more than $7 billion intended to expand access to broadband in rural areas — $4.7 billion to the National Telecommunications and Information Administration (NTIA) for the Broadband Technology Opportunities Program (BTOP) and $2.5 billion to the Rural Utilities Service (RUS) at the Department of Agriculture for the Broadband Initiative Program (BIP).26

BIP missed its mark in a number of ways. In January 2011, the RUS administrator provided a report to Congress that said the program would connect nearly 7 million rural Americans.27 But “RUS admits it’s not going to provide better service to the 7 million residents it once touted; instead, the number is in the hundreds of thousands,” according to a 2015 Politico investigation.28

BIP also mishandled hundreds of millions of dollars in funding intended to connect rural Americans. The Politico investigation concluded 42 broadband infrastructure projects RUS initially awarded were canceled, rescinding more than $300 million in loans and grants. The cancellations meant as many as 430,000 residents in rural areas did not benefit from new or improved connections. Politico also found around 150 of the total 297 BIP projects had not drawn down their awarded funds as of the July 2015 investigation, leaving $277 million in potential investment that could be clawed back by Congress.

Where RUS did fund projects, they were unable to tell who they actually served. Politico noted:

In May (2015), the agency reported it has delivered new or improved services to 213,000 households and more than 15,000 businesses. But RUS, as it collected that data from awardees, never asked whether those residents live in unserved, neglected rural towns, or areas that had some broadband access before the Recovery Act.

Indeed, “RUS does not track subscribership by rural area,” a 2014 Government Accountability Office (GAO) report recognized, concluding “RUS has not shown how the approximately $3 billion in funds awarded to BIP projects have affected broadband availability.”29

A broader criticism leveled not just at BIP but at RUS as an agency is that RUS often awarded projects outside of rural areas. An April 2011 study analyzed three projects subsidized by BIP that received a total of $231.7 million in support and found “RUS’ history of funding duplicative service has continued under BIP “with [m]ore than 85% of households in the three project areas … already (being) passed by existing cable broadband, DSL and/or fixed wireless broadband providers.”30 A September 2005 audit by the Office of the Inspector General at the USDA (before the creation of BIP) found that due to RUS’s ambiguous definition of what constituted a rural area, “the agency has issued over $103.4 million in loans to 64 communities near large cities.”31 The audit also found RUS approved $137.4 million in loans despite borrowers’ applications being incomplete or inaccurate, $59.3 million in approved grants and loans not to have been spent, and $30.4 million in loans being in default due to inadequate servicing.

BTOP, the other major broadband program funded by ARRA, shows what happens when a federal subsidy suffers from too many goals, beyond connecting unserved rural households. The single most expensive infrastructure project funded by BTOP was $155 million towards improving the Los Angeles public safety communications systems.32 That may have been a worthwhile project, but Los Angeles is not an unserved rural community.

Two other expensive infrastructure projects funded by BTOP were connecting “community anchor institutions” like schools and hospitals in West Virginia and Maryland with fiber. Once again, these may have been very worthwhile projects, but they explicitly were not designed to build out broadband connections to unserved households. “I was disappointed in the impact that the infusion of $126 million had,” the West Virginia state secretary of commerce told a reporter in 2017. “I would have thought it would have had more impact than it did.”33

Beyond BIP and BTOP, other broadband funding initiatives spent federal money on building networks that didn’t add to rural connectivity. For example, in 2012, the Department of Commerce’s Economic Development Administration (EDA) gave a grant of $2.1 million to San Leandro, California, a middle-income suburb of San Francisco, to build a fiber optic network, even though the Bay Area is probably one of the most wired regions in the world.

In 2017 the EDA gave $1.9 million to the City of Eugene in Lane County (Oregon), home of the University of Oregon, to fund the installation of fiber-optic cable in Eugene’s Central Business District area. True, the rural residents of Lane County might have needed some broadband assistance, with 52% not having access to 25/3 fixed broadband in 2017.34 But overbuilding in the center city did nothing to help them. That same government money could have been used to provide broadband to 2,000 rural households who don’t have it now.35

As we have just seen, the United States has far too much experience with programs that are supposed to deliver better broadband to rural areas but fail to reach their objective. In this section we will consider in more depth the specific reasons why these efforts did not succeed. In particular, we can identify three categories of problems with previous broadband funding initiatives:

It is clear from the history of past broadband programs that running broadband to unserved rural areas is expensive, while building additional networks in urban or suburban areas is much cheaper. As a result, the first step in closing the rural broadband gap is to make sure that money is getting to where it is needed most and not overbuilding areas which have service already.

Currently fixed broadband providers file Form 477 twice a year, which consists of a list of census blocks where the provider offers service to at least one location. This data forms the basis of the broadband deployment reports that the FCC issues annually, and the rural broadband coverage estimates cited earlier in this paper.

But Form 477 does not give a full picture of unserved areas, since just because one location is served doesn’t imply anything about the rest of the census block. Indeed, some studies conclude that the true number of unserved Americans is twice the official figure.36

For this reason, in August 2019, the FCC launched a new process called Digital Opportunity Data Collection (DODC) for collecting more granular data on broadband coverage.37 DODC includes requirements for fixed broadband providers to submit geospatial polygon coverage maps like mobile operators do depicting the areas where they offer service, a public map reflecting where fixed broadband is and is not available, and a crowdsourcing portal allowing consumers and governments to submit input on the accuracy of the data.

In March 2020, the bipartisan Broadband Deployment Accuracy and Technological Availability (DATA) Act was signed into law.38 Congress put aside $65 million for broadband mapping as part of December’s COVID-19 relief bill. The FCC set up a Broadband Data Task Force to coordinate the agency’s mapping efforts.39

With geospatial polygon maps, broadband operators will submit where they either supply or could supply service within a reasonable time, providing more detailed, granular data on broadband coverage. Such shapefile mapping will provide more accurate information about which areas are truly unserved, which in turn will prevent overbuilding and ensure that limited taxpayer resources are targeted to closing the gap for those who have lacked access to broadband for too long.

Better mapping will make it easier to identify which locations and areas are “unserved” — that is, don’t have access to the minimum target level of broadband. Currently under the RDOF program, an “unserved area” is a census block where no service provider is offering a fixed voice service and a broadband service with speeds of at least 25/3 Mbps (download/ upload), and no service provider has committed to offer such service under another federal or state broadband subsidy program.40 As noted above, as mapping gets more granular, the number of unserved locations will likely increase.

But the concept of an “underserved” area is much more ambiguous and troubling. For example, under RDOF, the FCC defined an “underserved” area as a census block that is only partially served by the target broadband service. That’s straightforward. But other organizations use the term “underserved” to mean less than two providers at the target service level. For example, the Wisconsin Public Service Commission defines an “underserved” area as a census block

… that is served by fewer than 2 broadband service providers, or an area that an applicant has demonstrated in its application is underserved.41

A 2020 Pew report on state broadband programs defined an “underserved area” as having:

… internet service at speeds higher than those that are defined as unserved but lower than those that have broadband service as defined by the state program.42

This vague definition simply means that state government sets two target levels, with the idea of encouraging areas to shoot for the higher one.

It seems innocuous to specify a stretch goal. But in reality, “underserved” becomes a way of justifying spending scarce federal funds in urban and suburban areas that already have broadband service, as opposed to rural areas that are actually unserved. For example, suppose that an “underserved” area was to be defined as one with less than two providers with service of at least 100 Mbps. Suddenly 42% of the population would live in “underserved” census blocks, including 33% of the urban population. The consequence is that the U.S. will have taken on a much more expensive task, and rural areas with no broadband service would once again be competing for funds with urban areas which already have broadband service.

To put it another way, the “underserved” concept encourages overbuilding of existing networks. Competition is a plus if it arises naturally. But if building an additional network in an urban area draws government funds away from rural areas without any service, then it moves us further from 100% coverage.

One important case of the overbuilding problem is the question of municipal broadband networks in areas that already have existing broadband networks. The American Jobs Plan, proposed by President Biden, specifically called for “lifting barriers that prevent municipally-owned or affiliated providers and rural electric co-ops from competing on an even playing field with private providers.”

This is not the right place to consider the broad plusses and minuses of municipal broadband. Nevertheless, there is no evidence that municipal broadband networks outperform private networks. A 2019 paper from the Technology Policy Institute found no empirical support for positive effects of municipal broadband on employment or broadband subscription rates.43 Moreover, municipal broadband systems do not necessarily offer lower rates than private providers. For example, as of early 2021, a 1,000 Mbps broadband connection from publiclyowned Greenlight Community Broadband in Wilson (NC) cost $99.95 per month. In the nearby city of Raleigh, AT&T offered a 1,000 Mbps broadband connection at a promotional rate of $60/month and a regular rate of $60 per month.

If the federal government has a limited pot of money to fund broadband construction, it should go to connecting unserved rural areas, rather than subsidizing municipal networks that overbuild existing private networks. Municipalities have limited funding capacity and a multitude of potential uses, including roads and highways, airports (if applicable), and water systems. Charles City, Iowa, for example, was unable to raise the money in 2020 for a municipal fiber broadband system, putting the project on indefinite hold.44

Sometimes what seems like a small problem can turn out to be a big one. Logically speaking, the easiest way to bring broadband to many rural households is by stringing the new connection along existing utility poles. Indeed, all comers must have access to the same set of poles, no matter who they are owned by, in order to provide critical services such as electricity, telephone, video, and now broadband service.

However, problematic behavior by rent-seeking pole owners makes the already difficult economics of rural broadband even worse. The owners of those poles — frequently the local electric and phone companies — can impose excessive non-recurring and recurring costs on broadband providers, which directly reduces their ability to deploy more broadband. Non-recurring costs include something called “complex make-ready” requirements where pole owners require broadband providers to bear the entire cost of replacing the poles they own. Recurring costs include the rental rates that “attachers” pay to maintain on-going access to poles year after year. Depending on who owns the poles and how they are regulated, these rates can vary dramatically.

Regulation is patchwork and inconsistent. Some poles — those owned by investor owned utilities and incumbent telephone companies — are regulated at the federal level or at the state level while other poles — owned by municipalities and electric cooperatives — are regulated at the state or local level or not at all.45 In addition, poles owned by the approximately 165 southeastern electric cooperatives and municipally-owned utilities supervised by the Tennessee Valley Authority are regulated completely separately from all other poles.46

On top of the inconsistent approach to pole regulation, this infrastructure is aging and is not being maintained, updated, and replaced in a manner to ensure that we reach our goal of closing the digital divide for deployment of broadband to unserved rural areas. As a result, the time and expense required to replace aging poles and to pay attachment fees is a significant obstacle to broadband deployment in unserved areas. As noted in an NCTA filing to the FCC in 2020:

… in one major broadband construction project that has included (to date) over five thousand miles of new rural plant, Charter has encountered situations in which as many as one out of every twelve poles needs to be replaced, with the average replaced pole already several decades into its service life. In a major expansion to over 57,000 rural homes and small businesses, pole replacement costs alone have accounted for approximately 25% of the total cost of construction (including applications, surveys, permitting, labor, and material).47

NCTA further noted that “[u]tilities frequently treat deployment projects by broadband providers as opportunities to shift the utilities’ own inevitable infrastructure upgrade costs onto third parties.” The result is that broadband providers are effectively financing utility investors.

The FCC’s response to the NCTA petition in January 2021 made it clear that “it is unreasonable and inconsistent … for utilities to impose the entire cost of a pole replacement on a requesting attacher when the attacher is not the sole cause of the pole replacement.”48 Still, that ruling leaves questions open. The issue of how pole replacement costs are divided is especially important at a time when the federal government is likely about to lay out large sums to provide broadband to unserved rural areas. The more federal broadband subsidies that are diverted into paying for replacing utility poles, the more expensive closing the rural broadband gap will be. Pole replacement costs need to be allocated more fairly between pole attachers and pole owners if we are going to close the rural broadband gap once and for all.

The impact of recurring pole attachment fees on broadband deployment projects has been hotly debated. The National Rural Electric Cooperative Association (NRECA) has argued that pole attachment rental rates are not an important barrier to rural broadband deployment, accounting for only “a fraction of the overall cost to build broadband systems in rural areas.”49 Meanwhile the NCTA has argued that the rates pole owners charge to access the poles are “often excessive and can stop a broadband provider from being able to provide service to an area that lacks it.”50

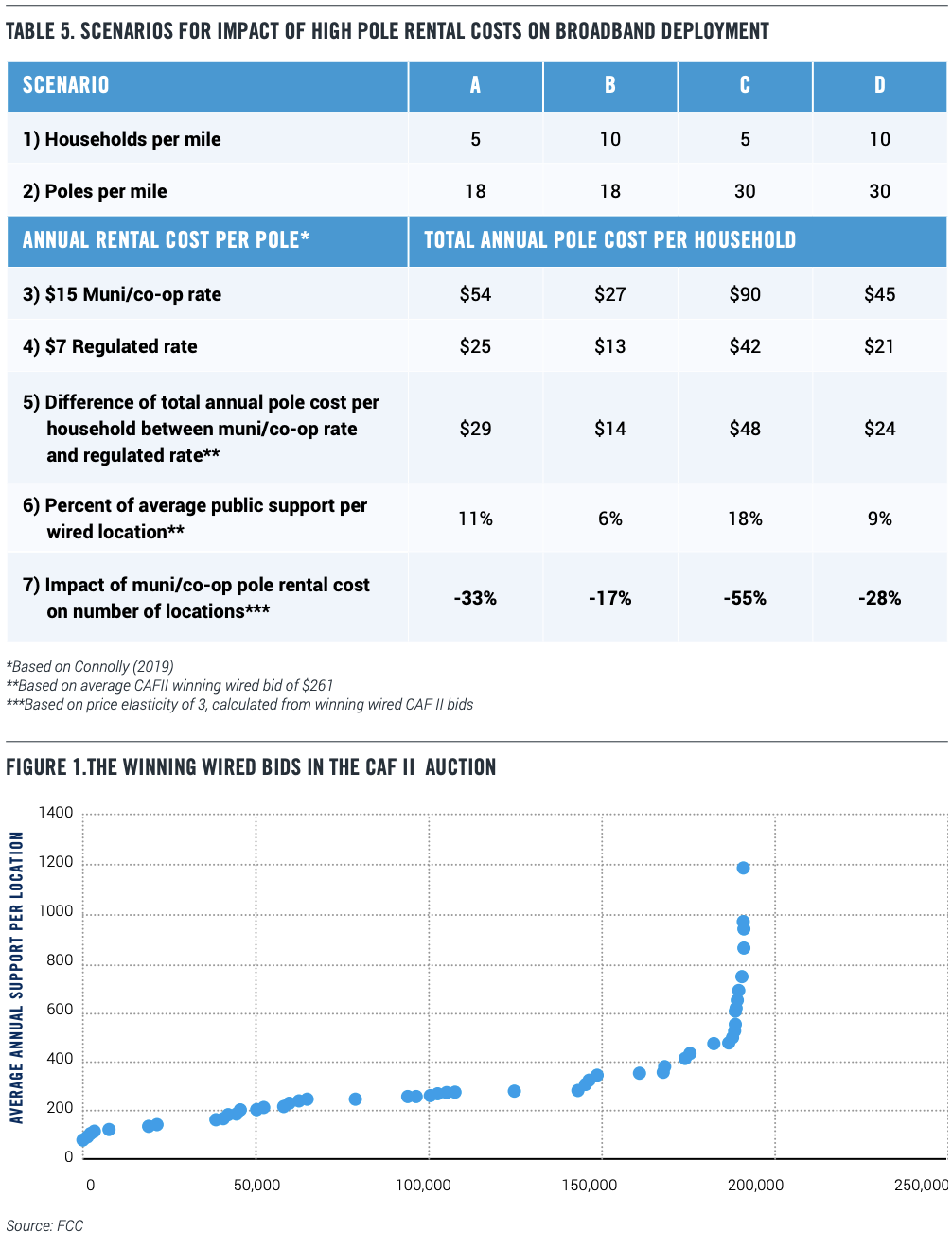

To shed light on this debate, we can look at the results from the 2018 CAF II reverse auction. In both cases, each winning bid represents the broadband provider’s public assessment of how much public support it needs per location to make the proposed deployment economically feasible over the next ten years.

We can then compare the estimated cost of pole attachment fees per location with the size of the public support required for broadband deployment. That is the correct comparison, because it tells us how much of public support is being absorbed by the pole owners. In addition, the auction results allow us to estimate the “elasticity” of broadband deployment relative to pole attachment costs.

Based on the published numbers, we calculate that the average winning bid for wired broadband locations in the CAF II auction was $261 per location per year. That is, each bidder, on average, required $261 in support each year for each wired location to make the build-out worthwhile. (As this paper is being written, winners of the RDOF auction have not yet submitted enough information to determine which ones will be using wired technologies).

How does the cost of pole attachments affect these bids? It depends on the number of households per mile, the number of poles per mile, and the price elasticity of broadband deployment relative to public support per location. Table 5 lays out four scenarios, depending on different typical values of households and poles per mile for rural situations. The two values of rental cost per pole is drawn from a 2019 paper.51 The lower value corresponds to FCC-regulated poles, and the higher value corresponds to poles owned by cooperatives and municipal utilities, which are not regulated by the FCC.

Line (5) calculates the difference in total annual pole cost per household for the muni/co-op rate and the regulated rate, for each scenario. Line (6) shows that difference as a percentage of the average public support for winning wired bids. So, depending on the scenario, the higher pole rates charged by co-ops and municipal utilities absorb, on average, 6% to 18% of public support for rural broadband.

How much does that affect deployment? Figure 1 below plots the average annual support per location for the winning wired bids in the CAF II auction against the cumulative number of locations reached. (We omit the non-wired bids because they don’t depend on the cost of poles in the same way).

We see that the curve is quite flat around the average bid of $261, implying that bidders in the aggregate are behaving as if they are sensitive to the level of public subsidy or support. Indeed, a 10% change in net public support per location translates into a 30% change in the number of locations served.52

This calculation enables us to estimate the impact of higher pole attachment rates on broadband deployment. Depending on the scenario, the higher fees charged by co-ops and municipal utilities can reduce broadband deployment by 17% to 55%.

What’s happening is that the fragile economics of rural broadband is, at the margin, very responsive to increases in recurring charges. The data from the auction appears to be telling us that there is a very narrow window between the cost of rural broadband and what rural Americans are willing to pay — and excessively high pole charges push providers out of that window.

This analysis illustrates that high pole attachment charges effectively function as a tax that siphons away money that would have otherwise gone to building out more broadband to more locations in rural America. The tax can be levied because municipal and cooperative electric and phone utilities have unsupervised control over their poles and can therefore extract rents.

Too often, broadband funding programs keep out, or strongly discourage, the very providers that could most effectively close the broadband gap. The FCC’s Universal Service program and its pivot to funding broadband is particularly instructive.53

With the advent of the internet, the FCC’s Universal Service mandate was expanded from voice only to include broadband. The agency tried several different approaches before settling on distributing funding via a reverse auction, where providers would bid for 10 years of public subsidy to build out broadband to specified locations.

However, even with these incremental successes in closing the rural broadband gap, there’s a fundamental problem with the Universal Service funding mechanism — it was designed for last century’s voice-centric world. This is perhaps best illustrated with the program’s “Eligible Telecommunications Carrier” (ETC) requirement — a threshold requirement for a carrier receiving support under the High Cost and Lifeline Support programs. The ETC requirement was borne out of the 1996 Telecommunications Act. At the time, an obligation to serve everyone made sense in a heavily regulated telecom world but was hard to square with the competition that Congress sought to generate in the Act.

The solution was to create the ETC designation.54 Only an ETC can receive Universal Service Fund support in the High Cost and Lifeline programs from the government for a given area. In exchange, the ETC for that area has sole responsibility and obligation as the telephone carrier of last resort.

The ETC designation is essentially composed of two sets of rules: the federal rules, found in Section 214(e) of the Act, and the state rules, which differ in each state and create a patchwork of regulations. Under the Act, the FCC is responsible for broadly defining federal universal service programs and the overall rules for ETCs. States designate providers as ETCs for a particular territory or “study area,” and states have the authority to apply additional requirements and create additional state universal service programs.

This can subject a provider to extremely burdensome regulation that differs state-bystate. State regulations cover topics as diverse as billing format and frequency, complaints, construction, customer notifications, deposits, interconnection, late fees, marketing, network outages, advertising, privacy, record retention, reporting, and accounting standards.

Most notably, ETCs cannot relinquish their voice provider-of-last-resort responsibilities without permission from the state. That permission will ordinarily not be given unless there is another ETC in the same area. A provider that accepts an ETC designation in an area with an existing ETC may find itself involuntarily becoming the voice provider of last resort if the original ETC chooses to relinquish its status.

In other words, the lure of ETC status conceals an expensive “poison pill” with potentially unlimited responsibilities which could be quite onerous, especially in a rural area. This could rationally deter broadband providers, especially large ones operating in multiple states, from seeking out FCC universal service funding to build out high-cost broadband in outlying rural areas. But how important is it in practice? Perhaps the ETC is a vestigial category that has no real effect?

To examine this question, we took advantage of a natural experiment: the CAF II auction required winners to get an ETC designation in order to collect the support funds. As a result, a whole group of winning bidders were going to states within a very short period to get ETC approval, allowing us to observe how different states handle the approval process. In some cases, the same bidders were applying to different states, so we had a direct comparison.

We examined state public utility commission proceedings and found that 26 states adopted an “aggressive” approach towards ETC approval of these potential rural broadband providers. We identified three characteristics of an aggressive ETC approval process.

In terms of the first requirement, various states have their own rules that apply to ETC applications, such as “cream-skimming” rules in South Carolina and Wisconsin that determine the size of the territory that the ETC can request. This requirement can be waived at the choice of the utility commission, but it still represents another hoop that the carrier must jump through.

The provider-of-last-resort responsibility was explicitly referenced in multiple states. One provider, Tri-County (Tri-Co) asked the Pennsylvania Public Utility Commission (PPUC) for authorization as an ETC after winning support from the CAF II auction. The PPUC’s order granting the request made sure to emphasize the potentially unlimited nature of the obligations.

… if all other ETCs in Tri-Co’s particular designated service area relinquish their ETC designations, Tri-Co, as the competitive ETC, may be required to ensure that all customers served by the relinquishing carriers in their respective designated service areas will continue to be served.

In Indiana, Marshall County Fiber (MCF)’s application for ETC status was subject to the same explicit requirement.55 The Indiana Utility Regulatory Commission granted the application subject to several conditions: … as an ETC serving areas known to be unserved or underserved, MCF must respond to Commission inquiries regarding its ability to serve customers in the event

… an ETC serving the same designated service area or portions thereof seeks relinquishment of its obligations as an ETC … MCF committed to offer the services that are supported by the federal universal service support mechanisms.

The 26 states with aggressive ETC policies account for 58% of rural Americans without sufficient broadband.

It is not a coincidence that large providers have been mostly unwilling to bid for support in new areas, since the benefits of Universal Service support may be easily outweighed by the prospect of a burdensome and expensive ETC application process in multiple states that leads to being involuntarily trapped as a provider of last resort. This could make the economic margins for deploying rural broadband thinner still, or evaporate completely, thereby discouraging a larger provider’s rural broadband buildout that might have been fully realized with government funding.

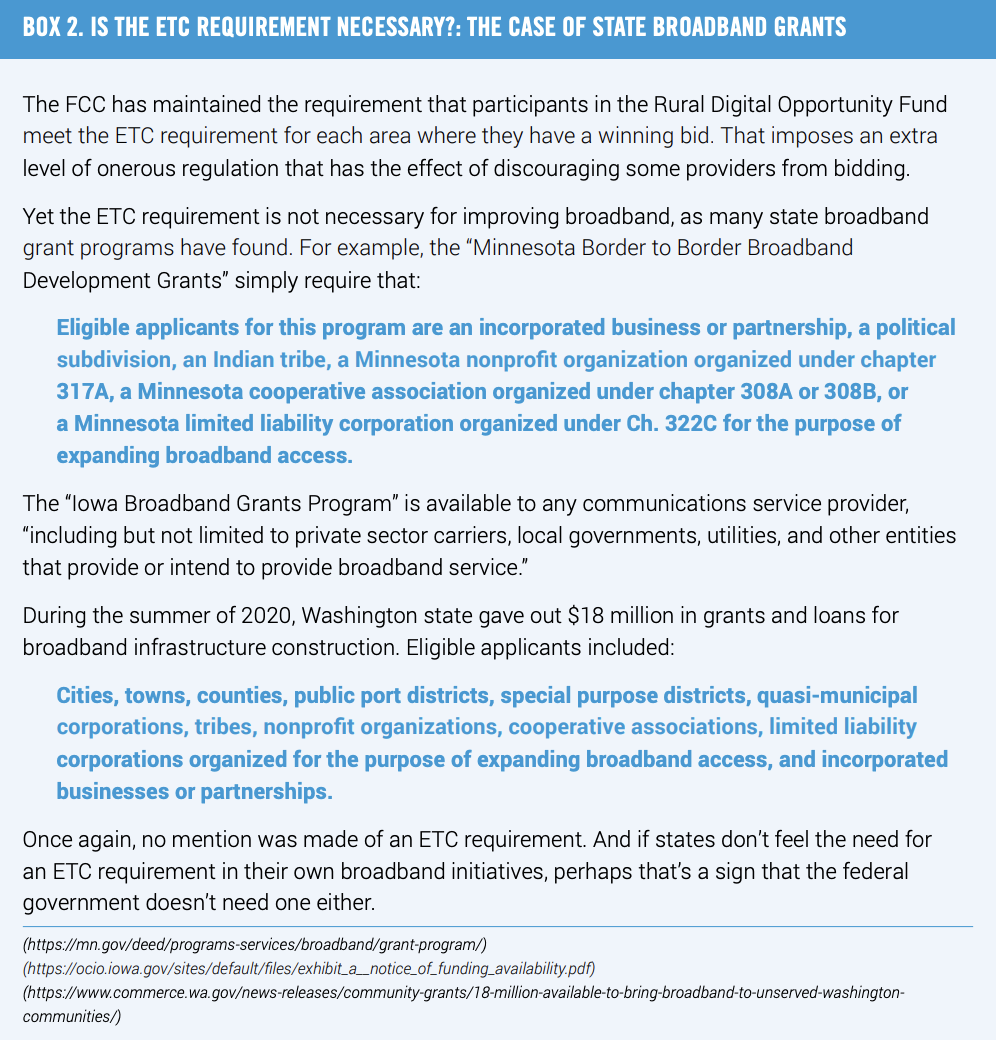

Significantly, ETC designations relate to telephone service only and do not include regulatory requirements for broadband. This shows that such a regulation makes no sense for programs focused on bringing broadband to areas that already have phone service (Box 2). Eliminating the ETC requirement will not undermine the FCC’s goals, all of which can be addressed more effectively with rules and requirements related to the broadband service that will be deployed.

Here’s what we know. Rural broadband is essential for preventing the permanent stagnation of rural areas. We have made remarkable progress connecting rural America. But gaps remain, and the ongoing pandemic has only brought the consequences of those gaps into sharper focus. Without broadband connections, rural residents won’t be able to participate in the economic, political, cultural, and social life of America. Rural businesses won’t be able to take advantage of the technologies and market opportunities that suburban and urban businesses take for granted. And rural students will continually be at a disadvantage compared to their counterparts.

Moreover, without sufficient broadband, rural areas won’t be able to attract people and businesses from other parts of the country. Cheap real estate and low density can be a big draw to many Americans who now lead a high cost, urban existence — if they can stay connected to the rest of the world at the same time.

But rural broadband — for the very same reasons that make rural areas attractive as places to live — is an investment with a slim margin for error, or no margin at all. A low density of households means that building expensive infrastructure and charging reasonable prices is a tough combination. That makes government support essential.

The American Jobs Plan proposes $100 billion for broadband. Whether Congress ends up approving that figure or something smaller, the same questions remain: How to avoid the mistakes of the past, where a myriad of programs squandered resources on overbuilding without closing the rural broadband gap.

No matter how many billions of dollars are allocated, history shows that the money can be spent unwisely if we are not careful. The FCC has shown that reverse auctions like CAF II and RDOF, suitably improved, are a good starting point for getting providers to bid for the lowest amount of public support that they need. Better mapping, too, is essential for making sure that unserved communities get the broadband that they need.

The key step is to decide on the priorities. Some people are concerned with funding alternatives to existing systems. Other people are worried about broadband adoption rates, especially among low-income households. However, the economic evidence shows that the average share of household budgets going to communications services has been flat, not rising, and that the price of internet access has fallen compared to other goods and services. That suggests we may have found a good balance between affordability and investment.

Getting rural locations connected to fast broadband that supports uses like online education and telehealth is essential. Connecting the unconnected should be a priority. Moreover, we want our policies to be pro-competitive rather than protecting incumbents.

From that perspective, a pragmatic agenda has three parts:

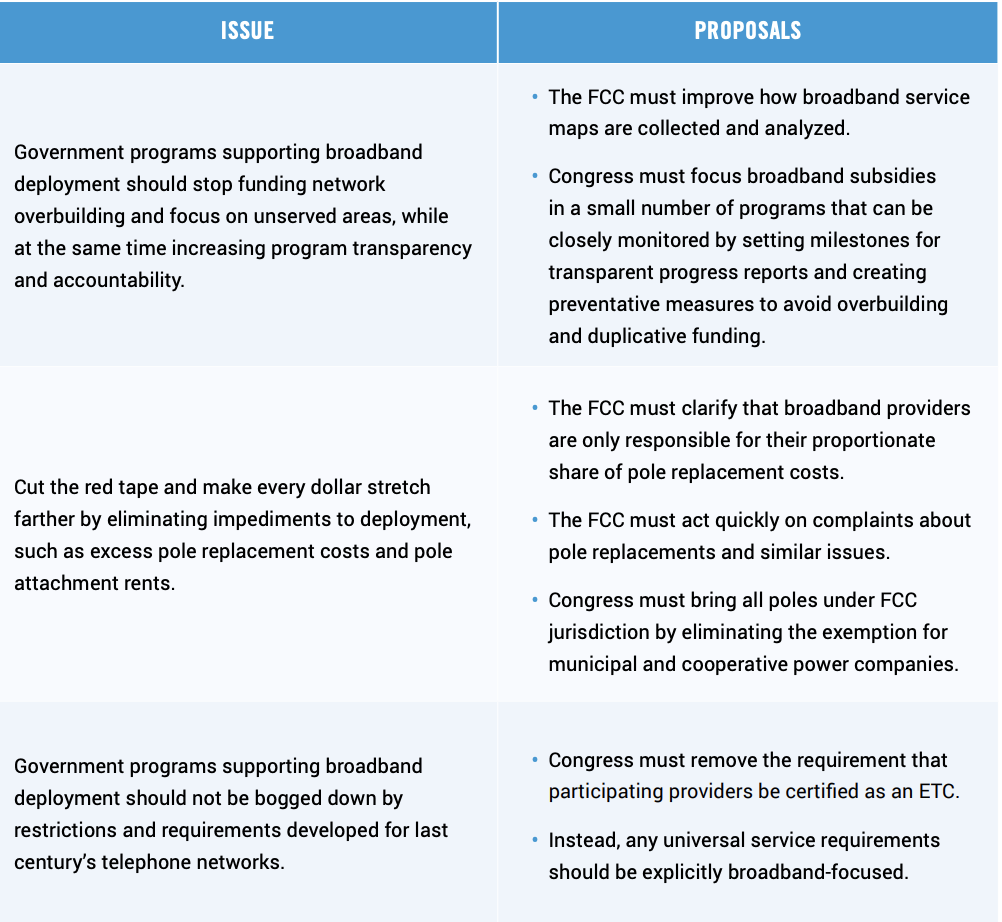

It is essential to focus on truly unserved markets to stretch the taxpayer’s dollar further. Funding duplicative systems with government subsidies in areas already served by commercial networks or in dense areas that are commercially viable takes away funds that could have been used to extend rural networks.

Similarly, the government should be careful about setting an excessively high standard for communities eligible to receive broadband subsidies. “Future-proofing” sounds like a great idea, but every time the standard for acceptable broadband is raised, more urban and suburban households are counted as “unserved.” As a result, the limited pot of broadband subsidies is spread more widely, and less is available for expensive rural connections.

To accomplish these ends, Congress should focus broadband subsidies in a relatively small number of programs that can be closely monitored. When money is spent, it should include milestones for transparent reporting of progress, like the FCC’s RDOF program, and should be careful to avoid overbuilding and duplicative funding.

Deployment of broadband to rural areas is expensive and inconsistent regulations create impediments and increase those deployment costs. Especially when a large pot of government subsidies is involved, different groups have an incentive to slow the process down and try to get a bigger slice of the pie.

One important example: A key to rural deployment is attaching broadband infrastructure to existing poles. However, excessive rent seeking behavior from pole owners — to recover pole replacement costs and attachment charges — is driving up the cost of rural broadband deployment, thereby limiting the number of rural households that can be served in any buildout.

Steps should be taken to streamline these processes to speed rural broadband deployment, bring pole costs in line with actual costs and make every dollar of both private and public funding stretch farther. The FCC needs to go beyond its January 2021 Declaratory Ruling and clarify that broadband providers are only responsible for their proportionate share of the pole replacement cost (e.g., if a pole would need to be replaced after 20 years and it is 18 years old, a broadband provider should only pay for 2/20ths of the cost). In addition, the FCC needs to act quickly on complaints about pole replacement issues, permitting issues and the like. These can languish for years delaying or preventing build out.

At the same time, the FCC can’t do it all, since municipal and cooperative owned poles are exempted from federal regulation of pole attachments. If broadband deployment is a national priority, Congress should act to bring all poles under FCC jurisdiction by eliminating the exemption when it funds the next round of broadband investment.

Even as federal broadband programs try to move rural areas into the 21st century, they still impose anachronistic 20th century requirements on participants. The clearest and most obvious example is the backward-looking rule that winning RDOF bidders meet the requirement to be certified as an “Eligible Telecommunications Carrier” for the locations that they receive public support for. The ETC designation was introduced in the 1996 Telecommunications Act, in an age of voice-only telecommunications networks and it carries with it certain Title II voice obligations that make no sense when the purpose of the funding is to bring broadband to areas without it. In fact, the areas that are being funded already have telephone service provided by an ETC.

This ETC requirement is a major obstacle for many companies and limits funding to providers that either have historically obtained the designation, or those providers that are willing to engage in the time-consuming and resource intensive process to obtain the designation and then comply with the onerous patchwork of state regulations that it requires.

State regulation that is not appropriate to apply to broadband services that are national — and global — in nature. We are continuing to apply legacy telephone regulations when we are trying to solve a broadband divide. It does not make sense and has slowed efforts to address this issue. The ETC requirement limits participation by providers that are otherwise well-positioned for this work and even if some providers do participate it adds unnecessary costs and requirements that do nothing to build broadband. If we are going to close the rural broadband gap, we need to get these providers onto the playing field.

So, when Congress funds the next round of broadband subsidies, the requirement that participating providers be certified as an ETC should be removed. Instead, any universal service requirements should be explicitly broadband-focused, which is in fact the point.

Our proposals are not magic bullets that will suddenly cure the rural broadband problem. But they will ensure that the money that is spent will go to where it belongs, rather than being diverted to other goals.

Devoting government resources to overbuild or upgrade existing robust networks in these areas will take away those finite government resources from those areas of the country that lack any broadband connection at all. The rural/urban divide will only be widened, not narrowed or closed for good.

Nor does it make sense for Washington to fund what the private sector is already moving to accomplish, invest in, and deploy on its own.

Infrastructure proposals should be laser-focused on connecting those areas of the country lacking any broadband access. Past experience with broadband funding has shown that will be the only way to connect 100% of the country once and for all.

This paper demonstrates that tremendous government resources have already been directed towards the problem, but the gap persists. We cannot afford to ignore the lessons of the past. The roadmap laid out in this paper will help ensure we succeed.