On Wednesday, the House Subcommittee on Antitrust will hear testimony from the CEOs of Amazon, Google, Facebook, and Apple. Throughout the long pandemic shutdown, Big Tech has supplied the products and services that allow many Americans to keep working remotely and to stay in touch with family and friends while socially distancing. Our connectedness is one of the few bright spots in this ordeal. It’s an odd moment for lawmakers to be expending energy on castigating America’s most innovative and globally competitive companies, simply because they are big.

However, critics of the tech giants have labeled them “monopolies” and increasingly advocate for regulators to break them up. With that in mind, here are 10 myths about Big Tech and antitrust you should be aware of before tuning in to the hearing.

There is a difference between the layperson’s use of “monopoly” and the technical meaning of the term. In casual commentary, “monopoly” is often used interchangeably with “large” or “dominant” when describing a company. But the term has a much more precise legal definition, and future court cases will hinge on its technical rather than colloquial meaning. According to DOJ guidelines, a company has monopolized a market when it has “maintained a market share in excess of two-thirds for a significant period and market conditions (for example, barriers to entry) are such that the firm’s market share is unlikely to be eroded in the near future.” The tech companies are not above that threshold:

Amazon is actually a surging competitor in digital advertising, and has an estimated 10% market share this year. It is deeply ironic that multiple Big Tech companies have been accused of monopolizing the advertising market at the same time. In reality, the largest player — Google — has less than a third of the market. The second largest — Facebook — has less than a quarter of the market. And Amazon is nipping at their heels.

Critics of Big Tech often try to define arbitrarily narrow markets to show a market share in excess of two thirds. That’s why you’ll hear that Google has “89-93%” of the US digital search advertising market or a large share of the “US digital display advertising market” or the “US digital video advertising market.” What these critics fail to show is why these should be distinct antitrust product markets. Advertisers maximize return on investment. If prices increase in one advertising channel, they likely substitute that spending to other channels. If anything, the simultaneous rise of digital advertising and fall of print advertising — while other advertising channels have remained flat — suggests that “US digital advertising” might be too narrow of a market. It seems that advertisers are substituting digital advertising for print advertising. A good rule of thumb in antitrust is that the more adjectives someone tries to use to define a market, the less likely it has any relation to economic reality.

It’s also important to remember that in digital markets users often multi-home, meaning they use multiple services in the same market. For example, the average person has nine social media accounts. Take a look at your phone. How many messaging apps do you have? How many social media apps do you have? What about email? Does one company really have a monopoly on how you communicate with your friends, family, and coworkers? Does one company have a monopoly on the entertainment you consume? The answer for most people is no.

Next, let’s look at consumer harm. According to DOJ guidelines, an antitrust enforcer must show that a company has used its monopoly power to “harm society by making output lower, prices higher, and innovation less than would be the case in a competitive market.” But prices in digital markets have been falling (or at zero) for years.

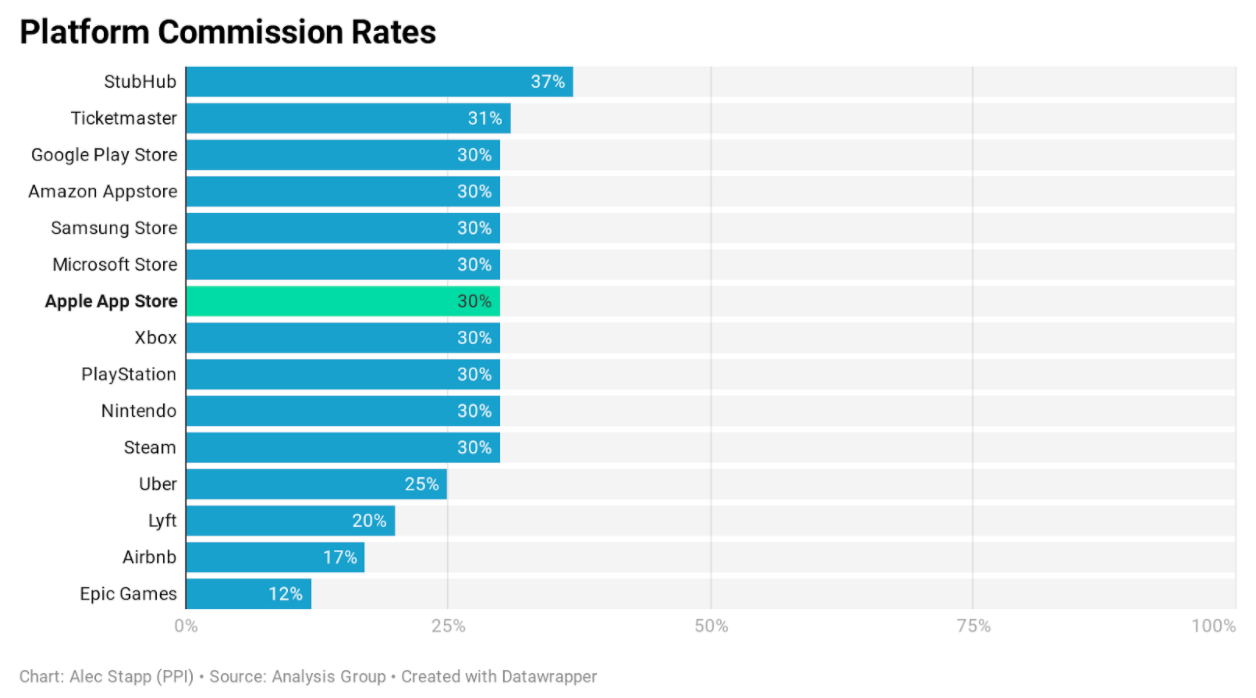

Apple’s 30% App Store “tax” is actually the going rate for platform commissions (and once you account for the revenue generated by free apps, effective app store commission rates are in the range of 4-7%).

While the prices for these services are low or even zero, consumers value them a great deal. Research has shown that, on average, consumers value search engines at $17,530 per year, email at $8,414 per year, digital maps at $3,648 per year, and social media at $322 per year. Again, the price to access these services is typically zero.

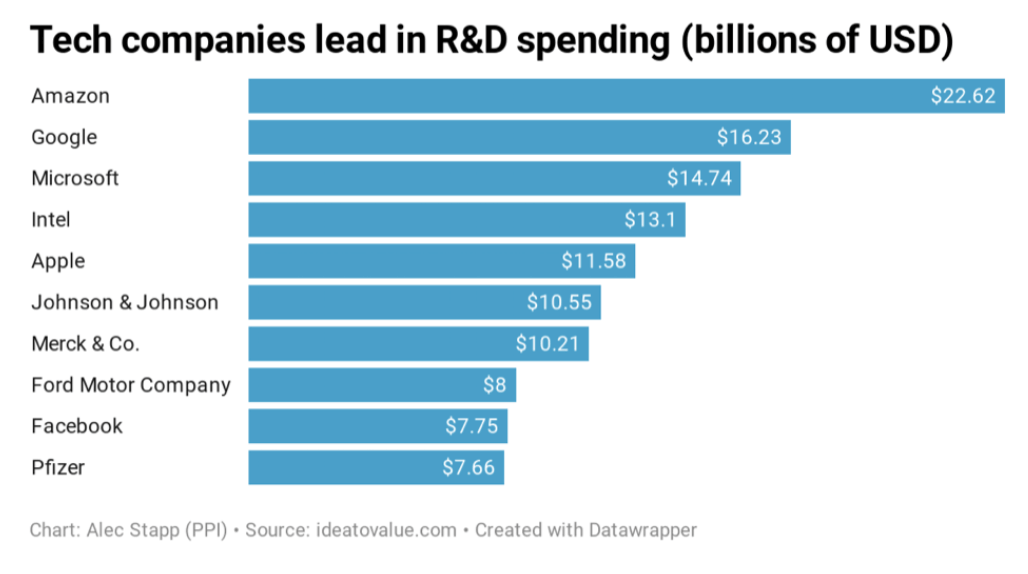

But what about innovation? It’s a hard thing to measure directly. One proxy variable we can look at is spending on research and development (R&D). A complacent incumbent harvesting monopoly rents tends not to invest much in the future. By contrast, in a competitive marketplace, even the dominant firms are nervous they will be unseated by nascent or potential competitors. To prevent that from happening, they invest in the next generation of technology that will benefit consumers.

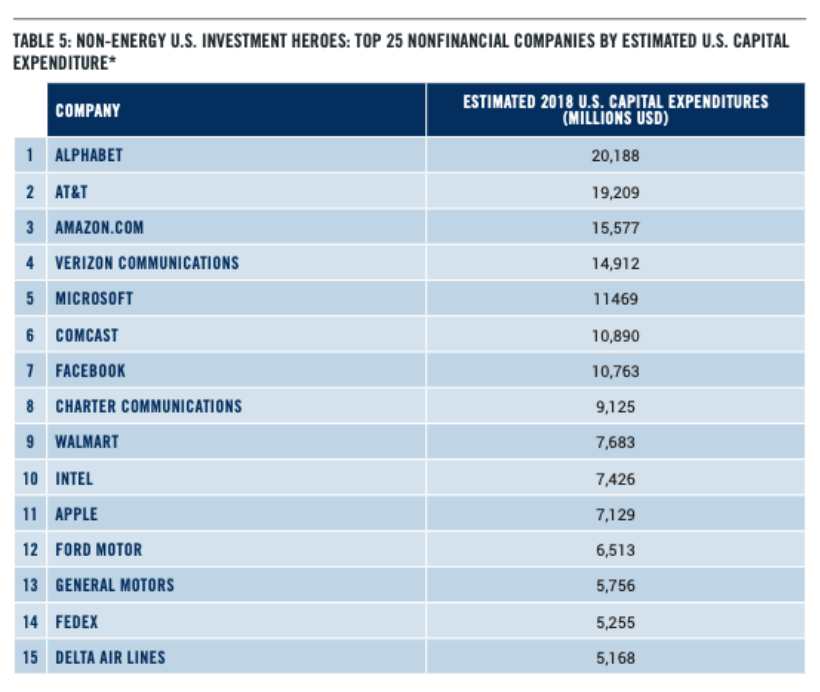

Another metric that’s worth looking at is capital expenditures. The line of reasoning here is similar: a monopolist secure in its market position would rather distribute profits to shareholders than make risky investments. Here again, the tech companies lead the country in spending in this category, according to the Investment Heroes report by Michael Mandel and Elliott Long at PPI.

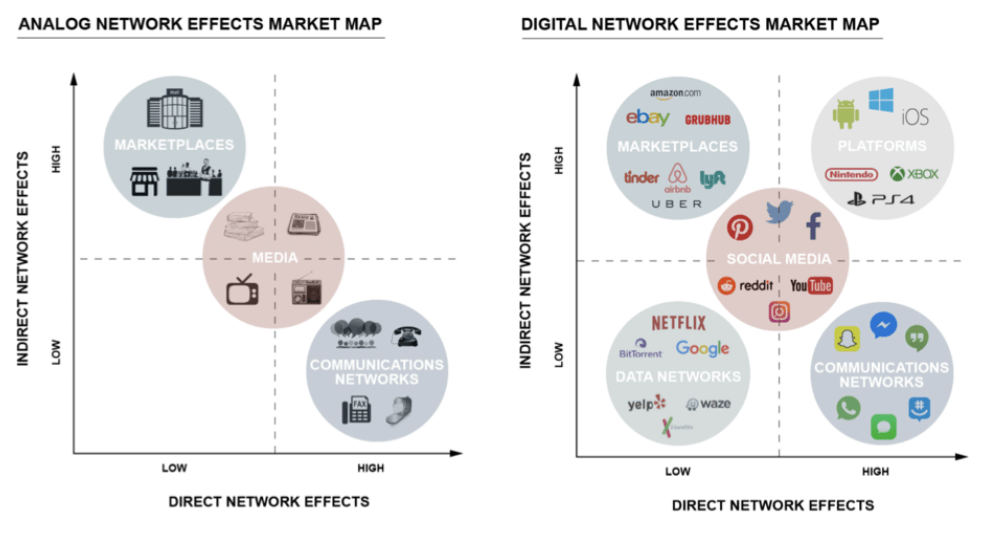

Critics claim that digital markets are different because they have network effects. Network effects are when a service becomes more valuable to each individual user as more users join the network. Telephones are a classic example. A telephone is only valuable insofar as there are other people who also own telephones. A similar dynamic exists for many tech platforms. There are also “indirect” network effects, where one group of customers cares about how many people are in another, distinct group of customers.

For example, operating systems such as iOS and Android need to cater to two different groups — smartphone users and app developers. Smartphone users want to use operating systems that have a lot of apps. App developers want to develop apps for operating systems that have a lot of users. It’s a virtuous cycle. And if there are high switching costs for users or if there are large platform-specific investments that developers need to make, then the equilibrium number of competitors in the market might be only one or two firms.

There are three important facts about network effects to keep in mind. First, network effects are nothing new. As shown in the chart above, many legacy markets have network effects, including fax machines, newspapers, television, shopping malls, and even nightclubs. Second, while network effects can be a source of market power, they can also create large consumer benefits. Breaking up incumbent networks would also destroy these benefits along with dispersing market power, as users lose the positive spillovers from having everyone on the same platform. Lastly, network effects also work in reverse. If a large network begins to lose users, it can quickly unravel as the service becomes less valuable to the remaining users.

Some Big Tech critics believe the companies create a “kill zone” around their businesses. The hypothesis is that the Big Five are so dominant in their respective markets, no venture capitalists will fund startups to compete with them. Over time, as the tech giants grow and branch out into new markets, we should expect the startup ecosystem to shrivel up and die. This theory is contradicted by numerous prominent examples, including Shopify competing successfully with Amazon and TikTok with Facebook.

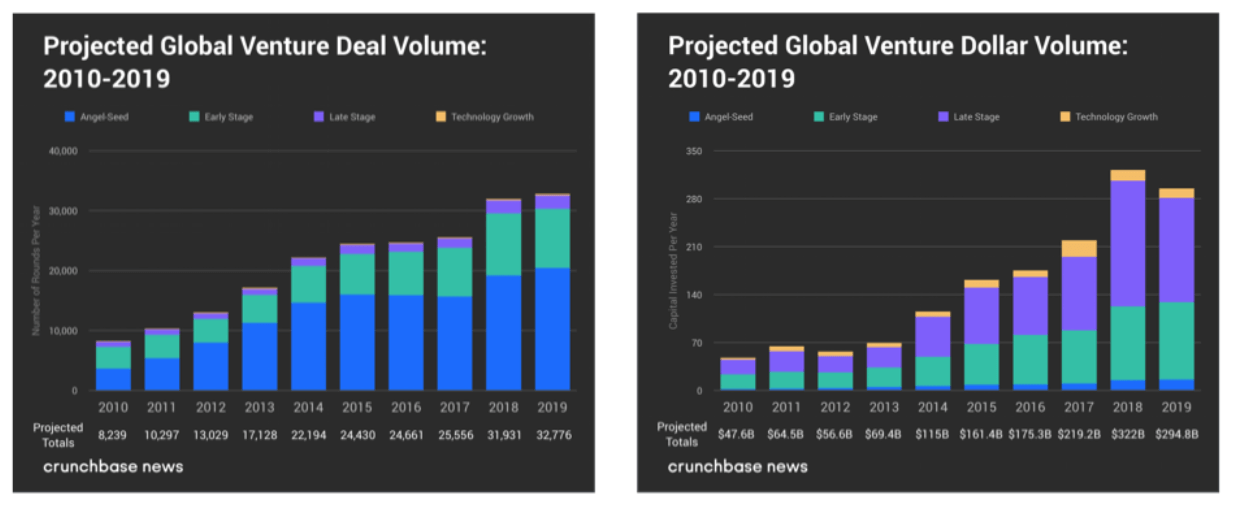

The data on the overall venture capital investment tells a different story. The number of venture capital deals in 2019 reached an all time high of 32,776. The total dollar value of those deals was just slightly off the all time high set in 2018. It seems more likely that startups will die from suffocating on cash than thirsting for liquidity (every Sotbank unicorn investment comes to mind).

And while there is some evidence that venture capitalists are slightly less likely to invest in startups directly competing in a core market for tech giants, this story from Will Rinehart about Google’s founding shows that competition from startups often starts in one narrow market and expands from there:

Google faced a similar environment when it was trying to get off the ground in the late 1990s. Ram Shriram, one of the earliest investors in Google, recently recalled that “I went up and down Sand Hill and could not get a single VC to get a check at the time. The reason? They said search was taken.” Michael Moritz, another early investor in Google, confirmed Shriram’s sentiment and continued by explaining that, “Companies start off with a very narrow focus, and they do one small thing very well, and then they become the best at it, and then they gradually expand.”

As startups get bigger and search for new opportunities for growth, they might increasingly cast their eyes on the cash flows currently enjoyed by Big Tech.

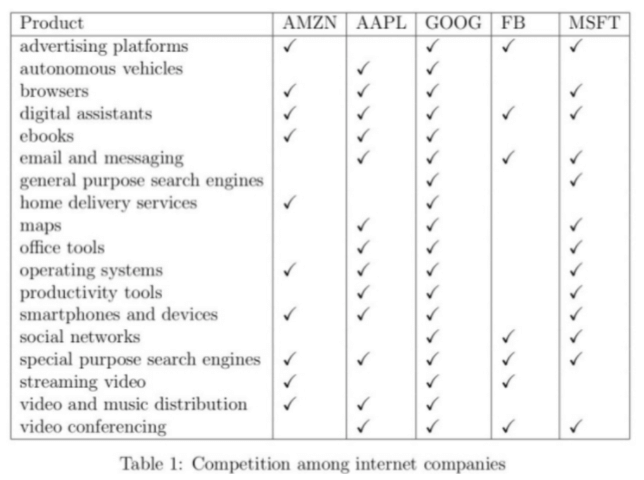

An underrated source of competition for the tech giants is each other. While each of the Big Five has its core area of strength, they are constantly making incursions on each other’s territory and jockeying for position. As the table shows, for every product or service, there are at least two Big Tech companies offering a competing service (and in many markets it’s four companies). The latest example of this: Google lowered its commission fees to zero on products sold via the ‘Buy on Google’ checkout option and started allowing retailers to use third-party payment and order management services like Shopify. All in the pursuit of challenging Amazon in e-commerce.

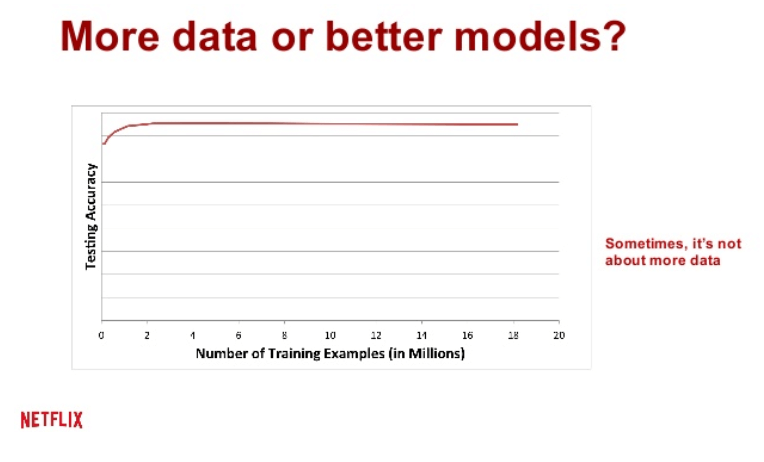

People like to say that “data is a barrier to entry.” But the barrier is much smaller than many think. When data is used as an input for an algorithm, it shows rapidly diminishing returns, as the charts collected in a presentation by Google’s Hal Varian demonstrate. The initial training data is hugely valuable for increasing an algorithm’s accuracy. But as you increase the dataset by a fixed amount each time, the improvements steadily decline (because new data is only helpful insofar as it’s differentiated from the existing dataset).

As the chart above shows, using a real world case of a machine learning algorithm in production at Netflix, adding more than 2 million training examples had very little to no effect. That means the key differentiator is often the quality of the model, not the quantity of data used to train it. And how do you engineer a better model? By hiring top-level machine learning scientists. In the end, the binding constraint is still the humans.

As I’ve written previously, data is not “the new oil.” Data is not like a commodity. It is more akin to a public good — non-rivalrous and non-excludable. For example, if you tell someone your birthday — a discrete piece of personal data — you can’t exclude them from sharing it with other people. And by telling them you have not diminished some finite supply of “birthday tellings.” That piece of information can be shared over and over. And since data is a quasi-public good, that means it is likely underprovided by the market. Private companies can’t capture the full benefits of investing in collecting, processing, and using data. If anything, policymakers should be concerned with how they can promote the safe sharing of more data rather than less (by making it more excludable).

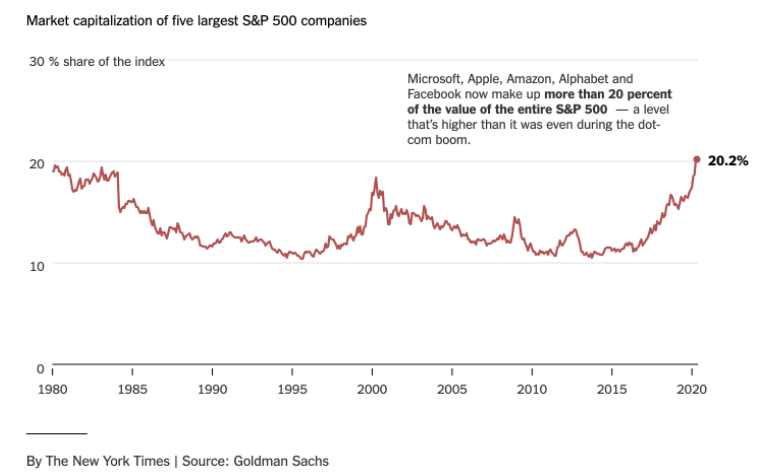

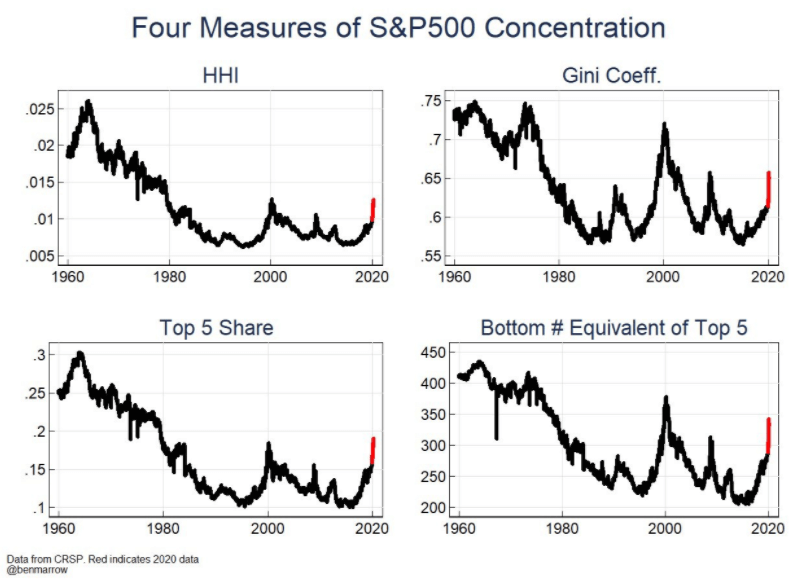

The New York Times and the Financial Times have published articles recently sounding the alarm about the rising concentration in public markets, as measured by the share of the S&P 500 accounted for by the five largest companies in the index (currently Microsoft, Apple, Amazon, Google, and Facebook). The takeaway from these pieces is that concentration is at an all-time high and that it’s unsustainable. But the charts that accompany these articles always seem to start around 1980. What happens if you extend them back further to get more historical context?

As you can see, concentration in the 1960s and 1970s was much higher than it is today. It was normal for the top 5 largest companies to account for more than 20% of the S&P 500, and they even exceeded 30% around 1965. The current level of concentration is not a historical outlier.

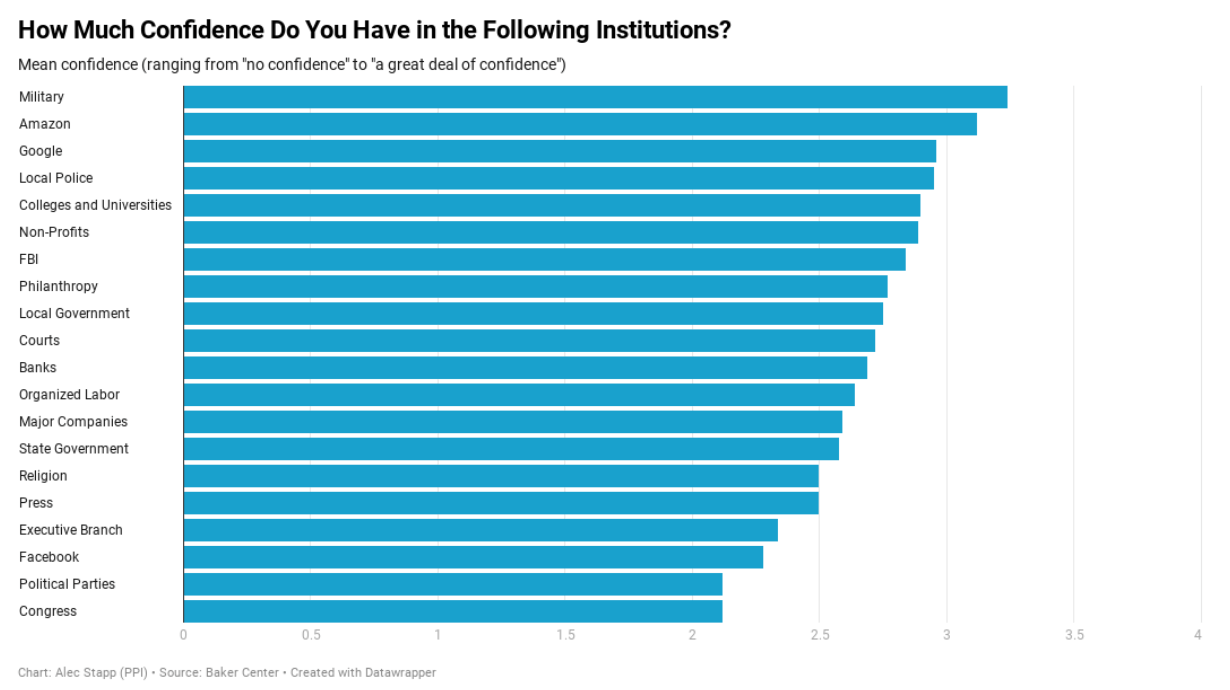

In survey after survey, Americans say they approve of the tech companies, trust them more than companies in other industries, and don’t think politicians should prioritize regulating them more. According to a survey from The Verge, 91% of Americans have a favorable view of Amazon; 90% have a favorable view of Google. According to a poll by the National Research Group, 9 in 10 Americans have a better appreciation for tech during the pandemic. As shown in the chart below, when Georgetown University surveyed Americans on which institutions they had the most confidence in, Amazon and Google ranked second and third respectively, only behind the military. The institution Americans have the least confidence in? Congress.

Some critics have claimed that Big Tech engages in “killer acquisitions” and anticompetitive mergers intended to acquire and maintain a monopoly position in the market. This NYT article points out that Google has made 270 acquisitions and Facebook has made 92 acquisitions. The large numbers are supposed to be taken as prima facie evidence of a competition problem. But many of these acquisitions are really just “acqui-hires,” or when one company purchases another for its engineering talent rather than its proprietary technology. As Ben Thompson points out, these exits act as a safety net that encourages entrepreneurs to be more risky in their ventures: “[I[t might have been easier to simply apply for a job at Google or Facebook, but being handed one because you worked for a failed startup reduces the risk of going to work for that startup in the first place.”

Acquisitions are also an essential part of a healthy startup ecosystem. Startups generally have two methods for achieving liquidity for their shareholders: IPOs or acquisitions. According to the latest data from Orrick and Crunchbase, between 2010 and 2018 there were 21,844 acquisitions of tech startups for a total deal value of $1.193 trillion. By comparison, according to data compiled by Jay R. Ritter, a professor at the University of Florida, there were 331 tech IPOs for a total market capitalization of $649.6 billion over the same period. Those liquidity events reward investors and employees for taking risks and incentivize the next round of startup financing.

But the main problem with labeling past acquisitions “anticompetitive” — even if they were reviewed by antitrust authorities and explicitly approved at the time — is hindsight bias. Because Instagram now has more than a billion users and is arguably a more valuable asset to Facebook than its legacy social network, critics are implicitly claiming that Instagram would have experienced the same success as an independent company. In other words, its success was a foregone conclusion.

Nothing could further from the truth. A cursory review of the historical record makes it clear how much doubt there was at the time about the wisdom of acquiring a photo-filtering app for $1 billion. Instagram had just 30 million users and zero revenue. The company had raised money at a $500 million valuation the day before Zuckerberg made the $1 billion offer. On late night TV, Jon Stewart joked about the acquisition: “A billion dollars of money? For a thing that kind of ruins your pictures? The only Instagram worth a billion dollars would be an app that instantly gets you a gram.”

A CNET article by Molly Wood titled “Facebook buys Instagram…but for what?” had this conclusion:

I still feel like there are more questions than answers to why this price tag makes sense. I hope Facebook isn’t getting distracted by hipster buzz or the photo-sharing bubble, especially at a time when its business decisions need to be as sound as possible to shore up future investor confidence. Don’t spend those billions before you’ve got them, guys.

The same is true for other Big Tech acquisitions. When it comes to a prospective merger, the tech companies are damned if they do, damned if they don’t. If it fails, people call it a “killer acquisition.” If it succeeds, people say the company took out a future competitor.

One of the biggest misnomers in the antitrust discourse is that people presume all monopolies are illegal. According to the FTC,

[I]t is not illegal for a company to have a monopoly, to charge “high prices,” or to try to achieve a monopoly position by what might be viewed by some as particularly aggressive methods. The law is violated only if the company tries to maintain or acquire a monopoly through unreasonable methods. For the courts, a key factor in determining what is unreasonable is whether the practice has a legitimate business justification.

Of course, based on the evidence presented earlier, it is far from clear that the tech companies have even a legal monopoly in any antitrust product market, let alone an illegal monopoly acquired via exclusionary conduct. But it is self-evidently true that the Big Five have been wildly successful and have become dominant in their respective core areas. Upon reviewing the totality of the evidence, the more likely explanation for their size is that they’ve created some of the best products in the market and are more efficient at delivering what consumers want than their competitors.

Given the facts of the market, why would Congress choose to hold a hearing about Big Tech and antitrust at a time like this? Antitrust regulators have been serving as effective watchdogs of actual anti-competitive conduct and should continue to do so in the future. There may be room for behavioral remedies in tech that strike a better balance without blowing up our most valuable and innovative companies. But, of course, that requires more focus on the boring procedural work of careful antitrust analysis — and that doesn’t make good TV.