Online platforms face an increasingly complex regulatory environment in the European Union. Altering their business models to comply with EU regulation while simultaneously experiencing intense scrutiny from competition authorities, American tech companies are being pushed to evaluate their profitability in Europe. Yet, proposals circulating within the EU are seeking to capitalize on this profitability by taxing these same companies to subsidize broadband infrastructure expansion.

While the sector is currently engaging in high levels of investment and enjoying consistent revenue growth, the notion that any industry can withstand significant taxation on top of mounting regulatory compliance costs threatens both the jobs created by the sector and the promise of future investment. These are circumstances that the European telecommunications industry knows well. With amassed regulation corresponding to relatively weak revenue growth over time, EU telcos have struggled to invest in the development of new high speed network technology such as 5G at the same rate as their counterparts in the United States and China. As high-capacity networks become the norm for consumers who rely on data-heavy services like streaming high-quality video and video conferencing tools, Europe risks being left behind in the next era of technological innovation. Though plagued with its own set of problems such as the ongoing debate over net neutrality, the U.S. telecommunications industry has managed to sustain a high level of investment, resulting in widespread 5G infrastructure and connectivity. Concurrently, European telcos have faced weak revenue growth and difficulty translating the demand for online services into a demand for new subscriptions.

Despite the apparent lag, the European Union’s “Plan for the Digital Decade” has set the goals that by 2030 every home in Europe will have Gigabit connectivity and every populated area of Europe will have access to 5G service. While this sounds like a great leap forward in digital expansion, the reality is that each of these goals presents a massive capital investment challenge to European telecommunications companies. Aware of this funding gap, the governments of France, Italy, and Spain released a joint paper in August 2022 calling on the European Commission to craft legislation requiring large online platforms pay a “fair share” of network infrastructure in Europe. EU regulators and industry groups such as the European Telecommunications Network Operators’ Association have echoed this proposal, with the idea being that the growth of these online platforms is dependent on the quality of network infrastructure. They make the claim that “over-the-top” (OTT) companies such as Google and Netflix need improved networks because of the data-intensive nature of their content and should thus contribute to the cost.

But there are regulatory factors preventing European telecommunications companies from accruing the revenue needed for significant network infrastructure investment which additional regulation will not solve. A recent letter signed by 13 European telecom CEOs points out the harm that EU price regulation causes to the competitive market for telecom services, 4 and major operators such as Vodafone have been vocal in their calls for market consolidation to support the scale needed for companies to invest in network expansion. In light of this, those calling for similar action against the tech sector should evaluate whether an additional tax in the face of strict competition guidelines and increasing regulatory hurdles will result in more network investment in the long run, or similarly impair the ability of the tech sector to contribute. This report offers a comparative analysis of the performance of the U.S. and European telecommunications industries, focusing specifically on their ability to achieve widespread high-speed network connectivity to examine the relationship between capacity for investment and heavy regulation. It finds that U.S. companies generally have had greater success in terms of connectivity and services speeds while Europe’s emphasis on low consumer prices may have resulted in underinvestment in its telecommunications sector. It recommends that for Europe to realize its full potential in terms of future technological innovation, the EU must adjust its regulatory policies to acknowledge the trade-off between low prices and investment, avoiding overregulation of high investment industries and supporting a sustainable digital transition for EU’s telecommunications industry.

Over the last decade there has been a global shift in consumer preferences from a reliance on voice-enabled communication to more data-driven internet services such as online messaging and video-calling. The consequence has been a shift in profitability from telecommunications operators to companies which operate internet platforms.

This trend is evident when looking at the percentage of profit held by telecom companies and internet platforms over time. Combining the telecom and internet sector, the global industry had a cumulative profit of $251 billion in 2014. Of this, 74% was profit by telecom companies, leaving the remaining 26% as the profit made my internet platforms. Just five years later, the cumulative profit remained similar at $260 billion, but internet companies now accounted for 60% of the profit.

However, when looking at the telecom industry with a more regional lens, this loss in revenue may not be equally distributed across all telecommunications markets. Though they face similar challenges, there’s a difference in capital investment and subsequent levels of connectivity when comparing the United States and Europe.

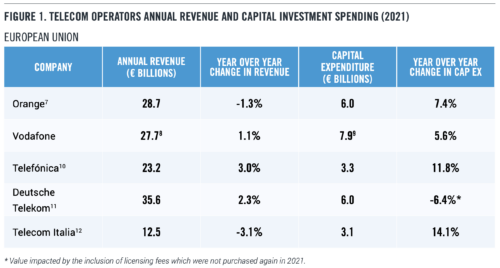

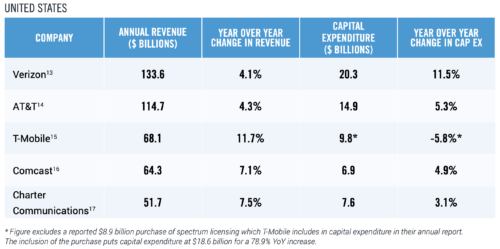

Telecommunications is a capital-intensive industry which requires continuous investment to maintain and develop efficient networks able to meet the challenges of rapidly evolving technology. With the struggle to reach new consumers looming over these companies, revenue growth is slow across the industry. However, while a handful of top European telcos experienced negative revenue growth in 2021, top American telecom operators grew a minimum of 4% — with T-Mobile’s U.S. division experiencing growth of almost three times that.

Figure 1 displays five of the top telecom operators by annual revenue in the European Union and United States, as well as their 2021 capital expenditure. Displayed are only the revenue and expenditures of these companies as they relate to telecommunications — excluding other lines of business. This data is reflective only of the company’s activity within the United States and EU member states and thus does not encompass global operations. Discrepancies such as the inclusion of spectrum licensing fees and inclusion of small amounts of overseas data may be present based on a company’s methods of reporting.

Despite the wavering profitability of the telecom business model globally, American companies are experiencing higher rates of revenue growth and therefore have the wherewithal to boost their capital spending on broadband. Many companies’ annual reports note that a significant amount of this expenditure is being directed to the expansion of 5G networks in the U.S., increasing American capacity for data intensive services. European consumers are not benefitting from the same level of investment in high-capacity networks, and European telecom operators are not experiencing the revenue growth required to catch up.

The heightened need for investment in network infrastructure comes as global online traffic increased roughly 60% in 202018— tasking the telecom industry with ensuring not only widespread connectivity but that their networks have the bandwidth for high levels of consumer use. European networks were not prepared for the surge in online activity, making bandwidth comparatively scarce. As a result, in 2020 the EU called on streaming platforms to lower the quality of their video streaming services to reduce the bandwidth needed to bring video to consumers. In response, platforms such as Netflix and YouTube lowered the quality of video offered to consumers in certain European countries, lightening bandwidth needed to use their services to free capacity for other users.

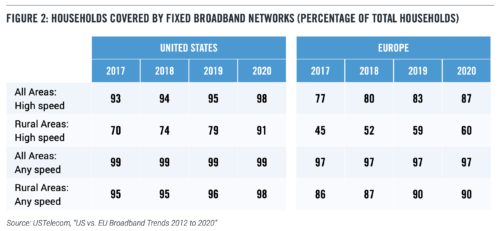

But bandwidth has not been the only challenge. The EU also trails behind the United States when it comes to levels of coverage. Though by 2020 Europe had begun to match the U.S. on the percentage of households covered by broadband networks, there are still disparities in levels of rural and high-speed coverage. The following figure considers connection to be “high speed” if it allows download speeds above 30 Mbps. In the U.S. in 2020, 98% of all households were covered by high-speed broadband, while in Europe only 87% percent of households had access to the same speeds. This is largely driven by the lack of high-speed connection in rural areas of Europe.

When it comes to internet connection speeds, America holds a substantial lead. Median download speeds in the United States more than quadrupled in the period between 2017 and 2020, when download speed grew by 157.7% year over year. Europe’s median speed also increased with a year over year growth rate of 76.2%, but this still left them lagging substantially behind. In 2021, the U.S. median of 83 Mbps was more than double the EU’s median of 38 Mbps. Only four European cities (Copenhagen, Stockholm, Bern, and Budapest) had reported median download speeds faster than the nationwide median reported stateside in 2021.

The United States has also pushed deployment of advanced networks, including fiber optics, at a higher rate than in Europe (see Figure 2). In general, American consumers are more likely to opt into internet subscriptions with higher service speeds. A study by USTelecom found that in 2020, 55% of connected U.S. households had subscriptions with speeds reaching at least 100 Mbps, while only 34% of connected European households had subscriptions capable the same speeds. Whatever the reasons for this wide performance gap, it’s clear that the United States proved better able to support surging demand for online services and commerce during the pandemic.

One metric by which the European telecom industry has the upper hand is prices paid by consumers for internet services. A study by New America’s Open Technology Institute found that in 2020, the average monthly cost of internet service in Europe was $44.71, compared to $68.38 in the United States.

During a period of global inflation there is considerable value in the EU’s prioritization of maintaining low costs to consumers who are juggling rising prices across other sectors. In the context of analysis of the sustainability of the telecommunications industry, however, is important to take account of the trade-offs associated with low prices. European telcos exhibit lower revenue growth, lower levels of capital investment and lower rates of high-speed connectivity than their U.S. counterparts. As Figure 2 shows, the United States also has a significantly higher proportion of rural households with access to high-speed broadband. Rural broadband comes at a high cost to the network operator. As companies expand coverage into less dense areas, the average cost per potential customer rises. Sparsely populated areas don’t provide companies with the return on investment through user fees needed to cover the cost of that network expansion. This generates pressures for both government subsidies and price hikes. Rural regions often also present geographic challenges, both in terms of remote locations and rough terrain for laying cables, further raising the cost to companies.

Prices in the European Union are also lower because of more aggressive regulatory intervention. Europe has maintained a stricter approach to competition policy in the telecommunications industry, contributing to the lower prices when compared to the more consolidated American sector. Additionally, regulations like the EU’s “roam like at home” policy, which requires telcos based in one country to provide service across borders within the European Union at no additional charge, also keep prices down — protecting consumers from predatory behavior by companies overcharging for roaming fees but at the expense of the profits firms need to make robust investments in high-speed networks.

With the newfound prominence of data services, the telecommunications industry has largely looked to rising demand for 5G to fill the hole in revenue created by consumer preferences shifting away from traditional telephone lines and voice traffic. 5G technology is integral to business innovations such as driverless cars, virtual reality-based platforms like the Metaverse, the development of more integrated smart cities, and other Internet of Things applications. But many of these products are in their infancy, meaning that for consumers who would be accessing 5G networks from smartphones, which operate just as effectively on lower capacity networks, the benefits of 5G are relatively intangible. Without consumer need for these networks, the incentive for companies to invest the capital required for widespread deployment is low.

Still, European companies have joined their international counterparts in deploying 5G technology in preparation for that next wave of consumer tech products. The industry association GSMA estimated that as of May 2022, 34 out of 50 European countries had some level of 5G deployment and 92 of 173 operators in the region launched 5G networks. However, even though there are networks available in most countries, only 2.5% of all online connections in Europe were 5G connections in 2021. When compared to other leading economies such as the United States, where 5G accounted for 14.2% of connections, and China, where 5G accounted for 28%, this demonstrates a significant lag in deployment and consumer adoption. This is a trend which is also reflected in the types of hardware being purchased by consumers. The majority of smartphones purchased in Europe are 5G enabled, but 5G smartphones accounting for 60% of smartphone sales in Europe adoption still falls behind the 73% of smartphone sales in North America.

Advocates for 5G expansion tout its potential to support much higher speeds, superior network reliability, and negligible latency. But consumer tech products like smartphones aren’t going to operate much differently between 4G and 5G networks — leaving the appeal of 5G dependent on the promise of future technology. Telecom companies have invested in these networks nonetheless but, without an influx of products on the market which rely on it, the demand is unlikely to translate into the revenue needed for more network expansion. When you add the premium price operators would have to charge to improve their networks, consumers may not consider it a good deal. This is why analysts expect business adoption to be the main driver of 5G demand, though the lag in consumer adoption compared to the United States and China is concerning for the immediate financial state of the European telecom industry.

A 2022 report by MTN Consulting found that investment by global telecom operators as a proportion of their total revenues peaked at 17.3% in 2021, driven by 5G network deployments. However, because of the low return on 5G investment, this proportion is expected to decline in coming years. In any case, telecom investment alone doesn’t give us a full picture of the size and extent of broadband infrastructure in Europe or the United States. Six American companies — Meta, Google, Apple, Amazon, Microsoft, and Netflix — currently account for 56% of all global data traffic between both fixed and mobile networks.

They are considered “over-the-top” or OTT platforms because they are companies reliant on the internet to deliver their products to consumers, in contrast to content mediums such as cable and broadcast. Each of these companies offers highly data-intensive products such as streaming, putting significant strain on areas where the coverage does not offer sufficient bandwidth to run these services.

This is the rationale for the notion that over-the-top platforms are free riders on the telecom investments that allow them to reach their users. However, contrary to over-the-top moniker, these platforms have also made significant global investments in the underlying infrastructure required to support their services. The aforementioned six American companies invested a cumulative $137.3 billion globally in 2021, including $58.2 billion from Amazon 31, 24.6 billion from Google, and $24.2 billion from Microsoft. Included in these figures are investments into the construction of data centers, subsea cables, and network edge locations — all which store and transmit the data traffic that European networks are currently struggling to support.

These investments have been largely focused on supporting the creation and expansion of a cohesive global internet. For example, a partnership between Microsoft, Facebook, and Telxius, a Spanish telecom infrastructure company, finished construction of a transatlantic cable in 2017 connecting the U.S. to Spain with the capability to transmitting up to 160 terabits of data per second. Additionally, Google has least 15 subsea cable projects underway around the world, totaling over 10,000 miles of submarine cable. Outside of the EU and U.S., the company has announced $1 billion in investment to support network expansion in Africa in 2021.

Each of these cables can cost several hundred million dollars apiece, signaling that capital investment by these companies is both large and growing as more of these types of projects are announced. Combined, it is estimated that the subsea cable projects by American OTT platforms contributed to an increase in global data transmission capacity by 41% in 2020.

As they seek to extend the efficiency and accessibility of their products to new customer bases, OTT platforms are expected to increase their capital expenditure from an average of 26.4% of their revenues over the past five years to more than 37% over the next half-decade. That means OTTs likely will be the main driver behind global network infrastructure investment moving forward.

Another overlooked aspect of network infrastructure is the construction of global data centers and network edge locations. Data centers are facilities crucial to storing, processing, and disseminating data and applications over the internet or through the cloud, and network edge locations are facilities geographically distributed to efficiently deliver content to nearby end-users. These are vital investments for over-the-top platforms which, while relying on telecom networks to reach users, need physical locations to support global data transmission.

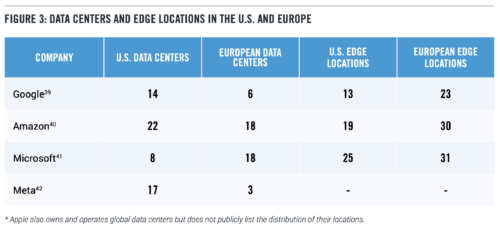

Five of the six big U.S. tech platforms (Netflix is the exception) the EU identifies as bandwidth hogs own and operate their own data centers and edge locations with both U.S. and European presence, as shown in Figure 3, highlighting the investment made to the larger network. Without construction of their own centers, companies outsource to third party content delivery networks to store and transmit data over the cloud. Netflix, for example, largely relies on Amazon’s AWS network for data storage and computing.

Although wireless prices have largely been flat in both European and American markets, U.S. telcos have been able to invest more in 5G and other high-speed network expansion. While some of this investment gap may be explained by lower prices and varying consumer interest in paying for high-capacity networks, the difference in regulatory strategies also is likely at play.

The EU has prioritized the lowest possible price to consumers through rigorous enforcement of competition law to discourage consolidation as well as caps on the prices paid for certain services. In contrast, U.S. policymakers have emphasized investment in high-capacity networks and rural broadband. Though favorable to consumers, it is difficult to see how the EU can sustain its strategy of price-focused regulation and still meet its aggressive connectivity targets for the next decade.

Enforcement of Competition Law Telecommunications networks present a unique challenge when it comes to competition law. Barriers to entry for new telecom operators are high given the capital needed to compete with established networks.

Because the cost of entry is so high, large companies utilize economies of scale to expand and maintain massive networks.

The United States and Europe tackle this challenge in different ways. The U.S. telecommunications market tend to be dominated by a few massive players. European countries aim at forming more localized markets with multiple providers, with regulations that ensure high levels of cooperation between companies to maintain a single coherent network.

High levels of competition help to keep consumer prices low. But as the U.S. case shows, a more consolidated market may allow for the economies of scale required to invest in areas where the return on investment is very low — allowing for higher quality service to rural communities.

This is not to say that the American model is ideal. Too many areas of the United States are served by only one provider, leaving consumers without the ability to shop for prices or consumer-friendly contracts. But for there to be substantial competition in more remote areas of the country, there either needs to be an influx of small telecom operators building rural networks — unlikely given the extremely low return on investment of expanding networks into sparsely populated places — or more large companies which can serve remote areas. This is the logic behind a federal judge’s approval of the merger between T-Mobile and Sprint in 2020. The judge reasoned that the combined company would be better equipped to compete with established industry giants Verizon and AT&T. Thus, despite the market becoming more consolidated, the merger would bring a new player to the top of the market putting pressure on incumbent companies in terms of service quality and price.

In contrast, the EU has been far stricter about the size of telecommunications companies, preventing consolidation and instead encouraging network sharing between operators. As a result, the European telecom market is highly fragmented with most countries hosting as many as four mobile operators, many of which are wary of making significant investment in 5G without clear signals that they will see a profitable return. This has prompted companies such as Vodafone and Orange to call for consolidation, claiming that overcrowding in European markets is making it difficult to invest and that network providers do not currently have the financial capacity to pay for the infrastructure needed to develop 5G technology

Europe’s fragmented broadband market necessitates a complex array of network sharing agreements between operators to ensure that their services work throughout the country. EU regulators have been clear in the goal that European consumers should have seamless access to data and voice services when traveling within the EU, requiring companies to negotiate with one another to ensure that their customers will have service in areas of the continent not covered by their own networks. In order for these agreements to be acceptable under EU antitrust law, they must ensure that they’re not reducing incentives for competition in deployment of infrastructure, putting an additional burden on companies which are struggling to achieve the scale needed to expand. It is for these reasons that CEOs of European companies such as Telefonica, Vodafone, and Norway’s Telenor have said that consolidation is necessary because current price wars and low margins are limiting funds available for 5G deployment. Critics of the movement for consolidation cite the likelihood that it will result in higher prices.

In the U.S., the government spends billions annually to expand access to affordable internet service. Its efforts are mainly directed at subsidizing private companies to offer discount prices to low-income households. The pandemic-induced transition to online school and work in 2020 provided fresh impetus for these programs. In 2021, the Bipartisan Infrastructure Law allocated $65 billion broadband infrastructure deployment and affordability programs, including $401 million to provide access to high-speed internet for 31,000 rural residents and businesses in 11 states. Other programs such as the Affordable Connectivity Program are targeted specifically at long-term affordability for low-income households with a discount of $30 per month for internet service plans.

European funding for such projects differs on a country-by-country basis, but there are also initiatives being spearheaded at the EU level. The EU’s targets for the “Digital Decade” detail a series of initiatives for member states between 2021 and 2030. In addition to the ambitious connectivity targets, Brussels envisions a broader digital transformation in which at least of 80% of the population have digital skills and 75% of EU companies utilize the Cloud or other data services. As previously mentioned, under this plan the EU hopes to have Gigabit connectivity for everyone in Europe and 5G connectivity in all populated locations. To finance these goals, the EU suggests that member states allocate 20% of their funding from the Recovery and Resilience Facility — an EU program meant to finance reform and recovery post-pandemic — to the digital transition.

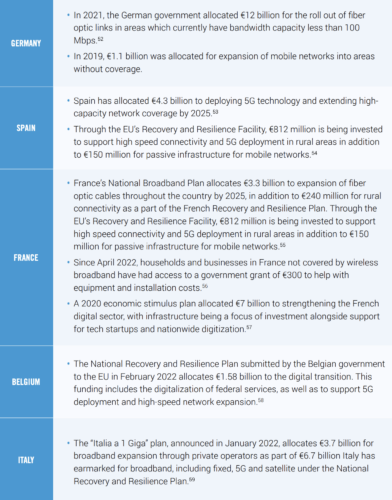

In addition to funding from the EU, member countries have put varying levels of public investment into expansion of fixed and mobile networks. While not a comprehensive list, the table below provides examples of the funding initiatives taken on by a handful of European countries since 2021.

While the U.S. government has negotiated with private network providers to lower prices of internet service for low-income Americans and implemented programs to give benefits for these households to front the costs, capping the prices that telecom operators can charge for given services without subsidy is a policy that is uniquely European.

Potentially the most consequential example of this is the EU’s “roam-like-at-home” policy, which allows customers with EU service plans to travel within the EU without additional charges for data roaming. In addition to requiring no charge to the consumer for crossing national borders, companies are required to ensure that data usage is available abroad at the same capacity and speed as the consumer would be paying domestically, with any additional surcharges for surpassing that data usage at €2 per GB of data. It would be infeasible for companies to have network infrastructure everywhere in the EU to meet the requirements of this policy, so it is made possible through network sharing. European telecom operators must enter agreements with other companies so that their customers can access other networks. This can be a costly process for telecom companies so, in the interest of supporting the sustainability of this policy for the telecom operators, wholesale caps are in place to provide a maximum amount that a visited operator may charge for the use of its network in order to provide roaming services.

The problems associated with this policy from a business standpoint are intuitive. By capping roaming fees, the EU limits telecom profits. On top of that lid on profits, companies are not allowed to charge one another more than the wholesale cap. If a company’s costs are at or above the cap, it loses money whenever its customers travel within the EU.

In addition to caps on roaming charges, in 2019 the European Parliament approved a rule to control the prices of intra-EU communication, capping cross-border phone charges at 19 cents per minute for calls and 6 cents per text message. Its purpose is to lower costs to consumers and bolster competitiveness for EU businesses, which will pay less for telecom services. However, for EU telecom operators forced to offer services with a lower profit margin, the net result is less global competitiveness.

There is no question that this is a beneficial policy for consumers in the short term, but the long-term impact is that such policies will disincentivize investment into Europe, ultimately hurting the individual who is having to consume other products at a lower quality than others around the world because of a lack of bandwidth and might not have access to future data-heavy services without network updates. Disincentivizing investment in Europe also pushes European telecom providers to bring their capital investment elsewhere. Vodafone has been in the Indian market since 2007 and continues to invest heavily in expansion in the region, working on bringing 5G to India. Similarly, as shown in Section I, T-Mobile in the United States is now much larger in terms of both revenue and capital investment than their parent company and European line of business, Deutsche Telekom.

The United States and the European Union have vastly different telecommunications sectors in terms of market structure, regulation, and operating capacity. Though these differing approaches have worked in the past, the recent influx in demand for bandwidth has exposed cracks in the European system which differ from those in the United States.

As Europe’s example shows, heavily regulated industries tend to invest less. In deciding how to move forward with goals for connectivity and digitalization, the trade-off between low prices to consumers must be weighed with the telecom operator’s propensity to invest such that the industry is not crippled by inability to achieve sufficient scale for network expansion.

This trade-off must also be weighed in the case imposing a fee on internet platforms. While over-the-top internet platforms are currently experiencing high growth, the mentality that they are therefore too big to fail and can withstand heavy regulation and taxation is an oversimplification of the market. This is a heightened risk given the other regulatory activities affecting the tech industry in Europe such as the Digital Markets Act passed in July 2022, which identifies many of these same companies as “gatekeepers” for purposes of competition law, further regulating their ability to profit in European markets. When an entity is taxed, it will also invest less. To add responsibility for network expansion to a growing list of recent EU regulations on leading American online platforms puts strain on an industry which currently engages in enormous capital expenditure, altering the incentive for them to continue to operate and invest within the EU.

With China and the United States leading the way for 5G and high-capacity networks, now is the time for Europe to strengthen its own networks to compete in the next era of technological innovation. As we move toward products that require higher data traffic there is a demonstrated need for updates to global network infrastructure. This will require global cooperation and investment, both from the telecom sector and the OTT platforms which are investing in ways to connect the international internet ecosystem in ways which are not necessarily covered by telecommunications companies. For a successful push toward global digitization, governments must recognize and support this private investment such that European innovation isn’t left behind.