Jacoby, who is based in Kyiv, talked about the mood there, after almost three years of war in the country. “People are tired,” she said, “and that word doesn’t quite even capture it. Kyiv is far from the front, and life goes on in Kyiv. People go to restaurants and bars, and do live their lives, but just about everybody knows or is related to somebody who’s fighting, and indeed, most have casualties in their circle of a family or acquaintances. And the war is coming increasingly to Kyiv and to the west of the country because of the intensified missile and drone strikes.”

Democrats are out of touch and disconnected from working class voters of all races, genders, and backgrounds. That isn’t exactly breaking news. It is obvious. For many of us in the industrial Midwest, this has been like watching a decades-long train wreck in slow motion. Many of us have been screaming this from the rooftops, and no one, and I mean no one, in Washington wanted to listen. Now here we are with a brand new Trump presidency and an even further damaged Democratic brand. My suggestion as a first step on the road to recovery: Move the Democratic National Committee headquarters out of Washington, D.C. to Youngstown, Ohio.

Democrats need to get the hell out of the D.C. bubble. It’s killed our party. Force the overpaid consultants and contractors who give really bad advice to get immersed into the culture of an old mill town trying to make its way in the new economy. Make them and the staffers who work for the DNC drink coffee, eat lunch and dinner, drink beer, bowl, play bocce, go to concerts and watch sports with normal everyday working people. And they should spend their time mostly listening—not talking or tweeting.

The Democrats have, whether we like it or not, become an arrogant, preachy, coastal, inside-the-beltway, Twitter Party. We’ve become an organization of loosely tied, self interested groups who make a lot of money pitching outrage so they can raise more money for their own self preservation. Then, if any fellow Democrat has an honest, fact based disagreement, they scream and yell and call you corrupt.

It’s pretty pathetic. Our party has no clear unifying vision for America. The Party has taken extreme positions that are not connected to reality generally and do not resonate with the sensibilities of working class voters. We’ve lost touch with the hopes and dreams of everyday Americans. And we won’t reconnect with those hopes and dreams by having all of our operatives living and working just blocks from the stupid echo chamber that has become Washington, D.C.

Many states’ standardized test scores mislead the public about whether students have mastered the lessons taught at their grade level. In other words, scores some states label as ‘proficient’ doesn’t match the knowledge the nation’s top experts in student assessment say children should attain by their age.

Wisconsin now joins their ranks.

In June, with nary a public hearing, Jill Underly’s Department of Public Instruction (DPI) unilaterally watered down Wisconsin’s achievement standards. Without input from the governor, legislators, parents, or assessment experts, DPI lowered the “cut” scores for the state’s annual Forward exam.

Not surprisingly, Underly’s new performance standards manifested as a mirage on the Forward exam scores released earlier this fall:

In 2023, 39% of Wisconsin students tested proficient in reading; in 2024, 51% did.

In 2023, 41% were proficient in math; in 2024, DPI claims 53% are.

That’s a 12% jump in both subjects in one year – extremely unusual, even when students get intensive academic remediation.

On this episode of RAS Reports, Curtis Valentine, the Co-Director of PPI’s Reinventing America’s Schools Project, and Naomi Shelton, CEO of the National Charter Collaborative, sit down with Ronald Falls Jr., a member of the Board of Trustees at Stillman College.

The group discusses Stillman’s charter school partnership, as well as the crucial role HBCUs can play in K-12 education as charter authorizers.

After a pandemic-induced recession and several years of high inflation, many Americans are pessimistic about both their own personal finances and the overall economy. Unfortunately, the incoming Trump administration will likely bring more economic turbulence, with sweeping policy promises that could cause economic growth and employment to drop, while reigniting high inflation. Americans without robust savings are especially vulnerable in such turbulent times.

One of the most unnecessary contributors to inflation over the past four years was an excess of deficit-financed stimulus spending. But Trump and Congressional Republicans appear likely to repeat the mistake of their predecessors by extending and possibly expanding upon the tax cuts they enacted in Trump’s first term — which would cost more than $4 trillion over 10 years — without offsetting most of the cost. Furthermore, while the tax cuts’ largest benefits will disproportionately flow to wealthy Americans, the inflation they could cause would be borne primarily by working-class Americans who consume more of their household income than their upper-income peers.

As both a candidate and as president-elect, Trump has promised several other policy shifts that would wreak havoc on American households’ financial stability. For example, Trump promised throughout his campaign to impose a 10-20% tariff on every imported good, with at least a 60% tariff on Chinese goods. More recently, Trump also threatened a 25% tariff on Canada and Mexico, two of our largest trade partners. If implemented, these proposals would lower most Americans’ incomes by thousands of dollars, as importers pass the cost onto consumers through higher prices for everyday items.

If enacted, these policies and the many others Trump has advocated for, such as mass deportations, would send shockwaves through the economy. One prediction from the Peterson Institute for International Economics suggests severe consequences for Americans: Prices could skyrocket as much as 28% above the baseline prediction, gross domestic product could be $6.4 trillion lower, and employment would fall in exporting industries such as agriculture and manufacturing. While other estimates may be smaller, they all point to disastrous consequences for American households if Trump succeeds in enacting the economic agenda he campaigned on.

Households without savings to rely upon will be especially vulnerable to these economic disruptions. Emergency savings can not only provide a crucial financial cushion during unexpected events such as job loss but can also reduce reliance upon debt when a household’s costs rise faster than its income. Yet the past few years of inflation have taken a toll on American households, with 65% of adults in a Federal Reserve survey published earlier this year saying price increases have worsened their financial situation. One consequence of higher prices is that it becomes harder to adequately save for emergencies: According to the same survey, 46% of Americans surveyed did not have emergency savings to cover three months of expenses, up from 41% in 2021. Another recent survey by Blackrock found that more than one in four Americans lack any form of easily accessible savings to draw from during a crisis.

Donald Trump’s voting base is especially at risk: Blackrock’s survey found that 36% of rural households, which backed Trump by a 28-point margin, had no form of emergency savings — one of the highest of any demographic group. But these communities will also be among the hardest hit by Trump’s economic policies: The trade wars caused by his across-the-board tariffs will not only raise the prices they pay on consumer goods, but hit export-reliant industries that are important for rural economies, such as agriculture. As other countries respond with retaliatory tariffs, the industry will suffer as American products become substantially less competitive overseas.

Ideally, policymakers should avoid pursuing policies that will cause economic uncertainty or chaos. But in any case, they should pursue policies that promote financial capability to help vulnerable households weather whatever turbulent times lie ahead. PPI will be highlighting some potential policies that could advance these objectives in the next year.

On Wednesday, outgoing Senate Majority Chuck Schumer announced his intention to bring the House-passed “Social Security Fairness Act” up for a vote before the end of the year. While the bill may sound good and have some admirable goals, passing it now as written would undermine the future of Social Security. It would be both political malpractice and bad governance for Democrats to rush this bill into law as their final act before handing control of the White House and U.S. Senate to the GOP in January.

Social Security is currently built around two core principles. The first is that workers should receive benefits based on what they paid into the program. Although this principle is heavily strained today, as workers have not paid enough in Social Security payroll taxes to cover the cost of benefits for many years now, benefits are calculated based on the average wages upon which workers paid payroll taxes over their careers. The second principle is that the benefit formula is progressive, meaning workers with lower lifetime incomes receive a greater benefit relative to the money they earned (and paid into the program) compared to higher earners.

At issue are two provisions, known as the windfall elimination provisions (WEP) and government pension offset (GPO), that attempt to enforce these principles fairly for people who spend part of their career working for state and local governments in jobs that offer pension benefits in lieu of Social Security. Earnings from these jobs are considered “uncovered,” which means workers don’t have to pay payroll taxes on the income, but those earnings also aren’t taken into account for Social Security’s benefit formula. WEP and GPO are intended to prevent someone who consistently earned a $100,000 annual salary over a career that was split evenly between covered and uncovered jobs — and thus would be treated by the benefit formula as if they received a $50,000 over their whole career — from getting a higher return on their payroll-tax contributions than someone who consistently earned $60,000 in covered employment.

As President Biden “runs through the tape” in his last weeks in office, he should take a few minutes to approve U.S. Steel’s purchase by Japanese firm Nippon Steel. Doing so would have myriad benefits and virtually no costs. The merger would help America’s heavy industry, support a core U.S. international alliance, and promote fair competition and supply for steel users in the United States. Approving the merger is, basically, the right thing to do.

Nippon Steel’s bid to purchase U.S. steel succeeded in late 2023. That is, at least as far as the money, the terms, and the agreement of U.S. Steel’s management and Board of Directors. The two companies agreed on a $14 billion deal that would bring new blue-chip Japanese technology and capital to a fading U.S. industrial icon and help preserve metal production in Pennsylvania.

Nonetheless, the Nippon-U.S. Steel merger has proved controversial. Fears about foreign ownership of a major American metals producer quickly generated opposition from both the Biden administration and the incoming Trump administration. The issues have also divided the United Steelworkers union, with union leadership opposing the deal while many Pennsylvania members support it.

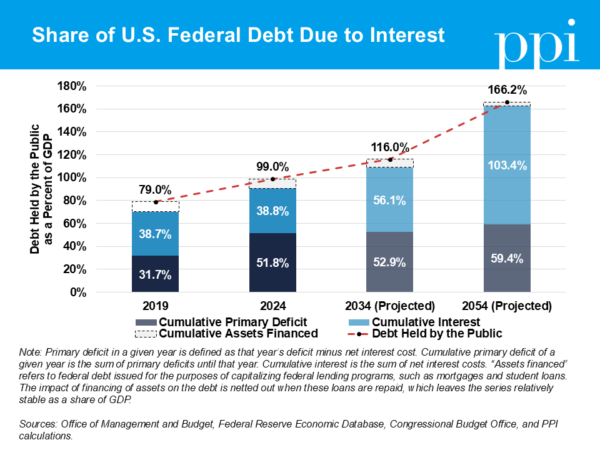

Over the course of the Biden administration, the federal government borrowed more than $5 trillion to pay for programs it did not have the tax revenue to finance. Under current law, the Congressional Budget Office projects these primary deficits — the difference between non-interest spending and tax revenue — to total $7.4 trillion over the next decade.

Financing government spending with deficits is not inherently bad. In fact, it is often necessary to support the economy temporarily during widely recognized emergencies such as wars or recessions. When the crisis subsides, the government can raise taxes or reduce spending to compensate, and the debt is either repaid or at least shrinks as a share of the economy. Debt can also be a useful tool to make investments that will grow our economy over the long-term, such as funding scientific research that lays the foundation for technological progress.

But most federal debt isn’t taken out for these productive purposes. Before the COVID-19 pandemic, more than half of the national debt could be attributed to the cumulative cost of interest payments. This means that most of our debt wasn’t used to finance tangible benefits like providing public goods, uplifting the poor, or subsidizing long-term investments. Instead, it was borrowed just to pay the cost of past debt.

Although it might appear that the share of debt attributable to interest has since shrunk, this is an artifact from the unusual surge of borrowing to finance temporary programs following the COVID-19 pandemic. As the federal government begins paying interest on the debt accumulated over the past four years, and then pays interest on the debt used to pay for future interest payments, cumulative interest payments will snowball to the point where they again make up the majority of debt within the next decade.

The problem will only get worse as time goes on if current law remains unchanged. Over the next 30 years, cumulative interest payments are projected to grow twice as fast as gross domestic product. At the end of that window, the amount of money spent financing past debts will exceed the total value of all goods and services produced by our economy each year.

When we borrow, we are making a transfer from future taxpayers to current ones. By continuing to neglect the long-term cost of debt, we are setting our future selves and subsequent generations for a snowballing debt burden, most of which will not even have been used to buy anything other than time for politicians to procrastinate.

Despite the nation’s deteriorating fiscal health, President-elect Trump and his Republican allies in Congress want to accumulate even more debt. Their top fiscal policy priority for next year — fully extending the expiring provisions of the 2017 Tax Cuts and Jobs Act without offsetting the cost — would increase primary deficits by $5.2 trillion over the next 10 years alone. Implementing all of Trump’s proposals from his 2024 presidential campaign, including tax cuts on income from tips, overtime pay, and social security payments, could add as much as $13.5 trillion to primary deficits over the coming decade.

If there is one key takeaway from this analysis, it is that when policymakers pass unfunded tax cuts today, future taxpayers will be stuck with a debt burden that is many times the cost of the tax cuts themselves. When each dollar of debt we undertake is unlikely to be repaid soon, it comes with a far higher cost of interest. This should set the standard for what’s worth borrowing for higher, not lower.

President-elect Donald Trump believes Americans have given him an “unprecedented and powerful mandate to govern.” Like so much of what he says, this claim blurs the line between hyperbole and fantasy. His Nov. 5 victory was solid, but no landslide.

Trump won just under half the popular vote, only 1.6% more than Vice President Kamala Harris received. With a public disapproval rating of 50%, he is the least popular presidential winner in modern times.

It’s certainly possible to look at Trump’s return to power as reflecting the new norm in U.S. elections of small and unstable majorities. Since Barack Obama’s departure, U.S. voters have tossed out the incumbents in one “change” election after another.

But such an interpretation might tempt Democrats, who were shut out of power in Congress as well as the White House, to do little but wait for their chance two and four years hence. That would be a colossal mistake.

Instead, Democrats must face a hard truth: their coalition is inexorably shrinking as non-college voters continue to defect. It’s time for honest answers to three vexing questions:

How did they lose again to the deeply flawed Trump? Does their loss signal a U.S. political realignment? And why are Democrats — and indeed center-left parties across Europe — alienating the working-class voters they once championed?

The sweep of Trump’s victory — both demographically and geographically — came as a shock. He shaved his losing margins in Democratic regions and made large gains among Democratic-leaning voter groups — young voters, Blacks, and especially Latinos.

Despite spending a half-billion dollars more than Trump, Harris won not one of the seven battleground states. In the brief time allotted her (107 days), she ran a competent campaign but could not avoid being sucked into the undertow of President Biden’s unpopularity.

Tactics aside, however, the defeat highlighted Democrats’ strategic political failure under Biden-Harris to stop hemorrhaging working-class voters.

Biden talked incessantly about fighting for working people, but his policies did not align with their interests.

Instead, he and his advisors fell victim to the fallacy of “deliverism” — the notion that passing big, multitrillion-dollar bills in Washington would impress working families and show them the “system” at last was working for them.

Instead, they got blindsided by inflation. Forty percent of these voters identified the high cost of living as their top concern. Economists differ as to its causes, but working-class voters link inflation to high government spending.

Immigration ranked second for these voters. Here again, they blamed the Biden administration for liberalizing asylum policy and presiding over a surge of over 7 million illegal migrants over the past four years. In fact, on almost all the key issues except for abortion, non-college voters expressed far higher levels of trust in Republicans than Democrats. They also were more likely to say Democrats had moved too far to the left than Republicans had to the right.

The aftershocks of Trump’s victory and U.S. voters’ rightward shift are felt across the Atlantic. Like his populist-right counterparts in Europe, Trump is riding a working-class revolt against governing elites. First confined to white Americans without college degrees, it’s now spreading to the non-white working class.

In fact, social class, now defined chiefly by education level, is replacing race and ethnicity as America’s deepest political fault line.

Since the high-water mark of Barack Obama’s presidency, Democrats have experienced a 30-point drop in non-white working-class support. That’s shattered a cherished progressive myth that “voters of color” think and vote alike along reliably Democratic lines. Harris improved on Biden’s 2020 performance with only one group — white college graduates. Yet that only underscored the strange inversion of America’s partisan loyalties: Democrats have become the party of the highly educated and professionals, while Republicans represent a multiethnic working class.

For the first time in memory, Harris won Americans making more than $100,000, while Trump won those making less than $50,000.The blue-collar exodus from the Democratic Party has been decades in the making. It won’t be fixed by minor tweaks. Democrats need to make dramatic course correction to head off a U.S. political realignment around a new populist right majority.

Voters without college degrees constitute roughly two-thirds of the U.S. electorate. Mathematically, there’s no way to build durable governing majorities with college-educated voters alone.

Morally, if Democrats hope to resume their historical role as the “party of the people,” they’ll need to reflect the mainstream values of middle-class America rather than the rarefied “luxury beliefs” of upper-class elites.

According to a post-election analysis by More in Common, Americans overwhelmingly believe that Democrats care more about advancing progressive social causes than the economic interests of average working families.

Asked to describe the party’s highest priorities, they picked “LGBT/transgender policy” second, after abortion. Actually, Democrats, like all other voter groups, picked the cost of living first, followed by health care and abortion. Transgender issues were 13th on their priority list.

Why are public perceptions so skewed? A big reason is that U.S. political discourse is mainly driven by progressive activists and right-wing populists. This leads members of both parties to assume the other party holds more extreme views that it actually does.

The outsized influence of progressive activists associates Democrats with a raft of unpopular positions on race/gender, immigration, crime and education. Trump exploited that to devastating effect against Harris.

The most lethal attack ad of the presidential campaign was a clip from a 2019 interview in which Harris explains her support for publicly-funded sex change surgery for prisoners, including detained immigrants. The kicker: “Kamala is for they/them; President Trump is for you.”

After watching the ad, 2.7% of voters shifted to Trump. That’s a stunning result. And even if most Democrats hold more moderate views on culturally fraught issues, they pay the opportunity costs that come with the progressive left’s fixation on race, gender, police brutality, fossil abolitionism and other “social justice” issues. The amount of time Democrats spend talking about such issues diverts their focus from the kitchen table struggles of working-class families.

It is the kitchen table struggles of working-class families that now need to become the fixation for Democrats. PPI has been working with Deborah Mattinson, most recently director of strategy to U.K. Labour leader and now Prime Minister Keir Starmer, to understand how those crucial voters experienced the U.S. election. In this report, PPI presents insight and analysis of the election, and draws on our learning from the center-left around the world to set out the way ahead for Democrats.

Only by re-connecting with the working-class Americans we have lost, and providing them with a credible alternative for change, can we hope to win the next Presidential election. That work has to start now.

WASHINGTON — As the cost of higher education continues to rise, students and families are turning to Advanced Placement (AP) and International Baccalaureate (IB) programs to reduce tuition expenses and graduate sooner. However, despite the increasing popularity of these programs — over 5.2 million AP exams were taken in 2023 — a new analysis from the Progressive Policy Institute (PPI) reveals that many colleges and universities are imposing restrictive policies on how AP and IB credits are applied, making it harder for students to save both time and money.

A new PPI report, “Diminishing Credit II: How Colleges and Universities Restrict the Use of AP and IB Towards Earning a Degree in Less Than Four Years”, authored by PPI Senior Fellow Paul Weinstein Jr., dives deeper into these trends. The report highlights how institutions limit the value of pre-college coursework through measures such as capping the total credits allowed, raising minimum exam score thresholds, and making credit policies opaque and difficult to navigate. These restrictions force students to take more courses than necessary, prolonging their time to degree completion and inflating the overall cost of a college education.

The report is a follow-up to PPI’s groundbreaking 2016 study and reveals that colleges are increasingly reducing the value of pre-college coursework, worsening the student debt crisis. Key findings include:

Credit Caps: Half of the surveyed institutions cap the number of AP and IB credits students can apply toward graduation.

Minimum Score Inflation: The percentage of top schools requiring a minimum AP score of 4 or higher has grown, with some elite institutions only accepting scores of 5.

Opaque Policies: Many colleges bury or omit information about their AP/IB credit policies, leaving students in the dark until after enrollment.

“Colleges and universities are creating unnecessary obstacles for students striving to graduate early and reduce tuition costs,” said Weinstein. “By capping credits, raising score requirements, and limiting transparency around AP and IB policies, these institutions are driving up the cost of a degree and forcing families to shoulder even greater financial burdens. It’s time for policymakers and colleges to remove these barriers and deliver on the promise of affordable, accessible higher education for all students.”

The report recommends reforms to make credit policies more transparent and equitable, including:

A national database detailing AP and IB credit policies for all colleges

Mandating that colleges provide detailed credit assessments to admitted students before enrollment

Limiting caps on AP/IB credits to one year of coursework

Expanding access to AP and IB programs in underserved schools

The findings are especially timely given the Biden administration’s focus on reducing student loan debt. While President Biden has made strides to address the financial burden of student loans, such as his executive order to cancel up to $20,000 of student debt for many borrowers, PPI maintains that these measures are not enough to tackle the root cause of the crisis: skyrocketing tuition costs.

Instead of relying on costly and potentially inequitable debt forgiveness programs, PPI emphasizes the need for colleges and universities to lower costs and allow students to capitalize on pre-college achievements like AP and IB coursework. These steps would provide a more sustainable and equitable path forward by ensuring that families can reduce the cost of higher education upfront rather than retroactively addressing debt burdens.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visitingprogressivepolicy.org.Find an expertat PPI andfollow uson Twitter.

In 2016, the Progressive Policy Institute (PPI) released an analysis of school policies regarding Advanced Placement (AP) credit. Despite being one of the few ways students could seek to graduate in fewer than four years, we discovered that the vast majority of the nation’s top schools restricted students from applying AP coursework toward degree credits. Unfortunately, despite strong evidence that successfully completed AP courses meet the standards of achievement expected by colleges and universities, the situation has deteriorated significantly as more schools seek to protect their revenue streams.

Furthermore, schools have significantly diminished the value of other college-level coursework completed before matriculation. For example, U.S. universities and colleges limit the amount of course credit awarded to students who have completed coursework through the International Baccalaureate (IB) curriculum, which is increasingly offered throughout the country. PPI’s study shows that IB credit was typically denied at the same rate as credit as AP.

Today, more students than ever enroll in AP courses and exams. In 2023, 5.2 million AP exams were taken by high school students, up from 1.6 million in 2002. A study from the College Board, which owns AP, shows that 738,698 students, or 21.7% of students in the class of 2023, scored at least a 3, more than 2 points higher than the class of 2013.

Although still small by comparison to the reach of AP (almost 23,000 high schools offer AP courses), 900 high schools in America now offer the IB diploma. This number has risen considerably since 1971, when the first IB program was taught in a U.S. school. The granting of credit for AP and IB is one of the few ways students can reduce the cost of attending college. Presently, the average cost of attending a private, nonprofit college or university is $38,421, and $15,868 for a public university.

Students who successfully complete AP or IB courses in high school could graduate in some cases either one year or one semester early, saving them anywhere between 12.5% to 25% of the total cost of the degree.

Students have other tools that help them graduate college at a lower cost. According to the National Center for Education Statistics, between 20% to 50% of new university students have transferred from community college. But as students move between community college and four-year programs, many find it very difficult to navigate the system of credit transfers and agreements.

Furthermore, students looking for information on credits for AP or IB work (and courses completed at community colleges as well), often have to wait until they arrive on campus and have paid their first tuition installment. Many schools have made it increasingly difficult to figure out how much AP or IB credit will be awarded before stepping on campus. Many institutions are leaving that decision to academic departments. And more and more schools are offering only waivers on introductory courses in lieu of course credit.

For too long students have been at the mercy of college administrators — forced to pay higher tuition bills and fees for things that should be free — transcripts, tickets for graduation, etc. Policymakers need to help level the playing field by using the government’s bargaining power (the federal government is the largest source of financial aid and provides billions in research grants to colleges and universities) to negotiate lower prices and force schools to accept coursework completed elsewhere. An important step to help students get through college faster and, therefore, at a lower cost is to ensure they get credit for successfully completing college-level work before matriculating.

Diana Moss has spent the last 25 years advocating for a centrist, consumer- and economics-based antitrust policy. Recently, as Vice President and Director of Competition Policy at the Progressive Policy Institute (PPI), she has been particularly active, publishing several papers, intending, to my read, to revive an antitrust agenda focused on enforcement that matters to consumers’ pocket-book issues. She sat down with the Rethinking Antirust Podcast to discuss.

“Many Gen Z teens don’t feel career ready. What if we made students aware of all of the many options available to them early on, starting in middle school (or even sooner)?”

That’s the challenge for K-12 career education presented by the authors of a report entitled Success Redefined issued by American Student Assistance and Jobs for the Future. The report is based on a Morning Consult poll of over 1,100 high school graduates who opted not to go to college directly after high school.

Nearly one out of three non-college youth (32%) reports a lack confidence in knowing the steps to take to transition into a post-high school career and further education. Two out of three (64%) who did not take career pathway programs say they would have considered pathway programs if they knew more about them.

The barriers to not pursuing pathway programs include a lack of encouragement from those at school to explore them. The preferred sources of information for the post-high school plans of non-college youth were searching the web (87%) and watching online videos (81%).

WASHINGTON — High prices for essential goods and services force consumers to make tough choices about what to buy, where to live, and even what bills to pay. Anger around high prices and the high cost of living played a major role in the 2024 presidential election. Disillusionment with the “Bidenomics” agenda fueled a sense of disenfranchisement. Namely, the struggle to afford the necessities that account for most of consumers’ budgets were de-prioritized in favor of proposals to pay off college student loans, green the economy at substantial cost, and other policies that do not ease financial burdens for working class Americans.

Today, the Progressive Policy Institute (PPI) released a new report, “Can Antitrust Be Doing More to Protect Consumers?,” authored by Diana L. Moss, Vice President and Director of Competition Policy at PPI.Market power is an important contributor to higher prices in critical sectors that make up the bulk of consumer spending. The report unpacks evidence of high market concentration, flagging productivity, market power “bottlenecks,” and lackluster merger control in critical sectors such as housing, transportation, food, insurance, and health care.

“PPI’s findings highlight the need to rethink antitrust priorities to more directly and effectively protect consumers,” said Moss. “We know that antitrust enforcers make hard choices about what cases they pursue. But our analysis shows that enforcement could be doing a better job of championing the interests of consumers. We propose that enforcers prioritize sectors where high prices hit consumers hard in their pocketbooks and drive up their already high cost of living.”

PPI’s analysis highlights the vital role of antitrust — especially stronger and more coordinated merger enforcement — in key sectors that account for the bulk of consumer spending. The report suggests several priorities that would sharpen antitrust priorities and bring it into closer touch with consumers, including:

The U.S. antitrust agencies should stop “splitting up” merger reviews for transactions in different parts of the food and health care supply chains. Oversight of all consolidation in these sectors should be assigned to one agency to ensure that competitive dynamics along a supply chain are fully accou

The antitrust agencies should revisit policy to approve virtually all retail grocery mergers subject to divestitures. Failed divestitures have unfairly transferred the burden of anticompetitive mergers to consumers through higher food prices. Reversing this damage will require concerted policy action moving forward.

The antitrust agencies should consider the impact of harmful consolidation and business practices on the stability and resiliency of supply chains. Consolidation in “intermediary” markets that are prone to market power bottlenecks have not been adequately addressed.

Agencies should organize public workshops to deepen their understanding of changes in business models, supply chains, and bargaining power in major consumer-facing supply chains over time.

“Competition is the lifeblood of a healthy market system,” said Moss. “To ensure it thrives, and consumers reap the benefits of competition. We should reevaluate antitrust priorities to provide more direct and effective relief in sectors that have the most impact on their budgets.”

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org. Find an expert at PPI and follow us on Twitter.

###

Media Contact: Ian O’Keefe – iokeefe@ppionline.org

FACT: 29 Haitian garment factories exported 300 million clothing articles to the U.S. last year.

THE NUMBERS: Haitian GDP (2023) –

Total

$19.6 billion

Remittances from abroad

$3.9 billion

HOPE/HELP exports

$0.8 billion

WHAT THEY MEAN:

In the holiday season, as we’re supposed to think at least a bit about those with less, here’s a useful last job for Congress: extend the U.S.’ three small ‘trade preference’ programs — acronyms “GSP,” “AGOA,” and HOPE/HELP” — for lower-income countries.

As an introduction, here’s an October piece from the International Labor Organization’s “Better Work” office in Port-au-Prince, worriedly entitled “Battling the Odds”. The ILO officers summarize the state of Haitian garment production and employment as follows:

“Throughout 2023 and the first half of 2024, Haiti has faced escalating crises, taking a toll on the nation’s socio-economic health. Gang-related violence is profoundly impacting daily life, with effects spilling over into the labour market, livelihoods and the well-being of workers. The garment industry has been seriously affected. Better Work Haiti’s most recent report delves into the data, revealing a troubling decline in operational factories, with one permanent and two temporary closures. The industry has seen a significant reduction in the workforce, with employment falling from 42,500 to 33,857 in just a few months, a loss of over 8,600 jobs.”

As they were writing up their report in September, “Better Work” was overseeing 29 Haitian garment factories in a handful of industrial parks — Port-au-Prince, Cap Haitien, Ouanaminthe — serving as guarantors for health and safety, wage and benefit, and other labor standards in lieu of a functioning labor ministry. Last year these factories produced about 300 million garments for American retailers and brands — mostly T-shirts, with some tracksuits, pullovers, and sweatshirts as well. Over the past decade, these factories have earned about $1 billion a year in export revenue, with 2023 shipments a bit lower at $800 million.

The figure, a bit more than 1% of American clothing imports, is about 5% of Haitian GDP. To draw an intellectually shaky but illustrative parallel to the American economy, by BEA’s GDP-By-Industry data, you could combine the GDP shares of U.S. automotive manufacturers and dealerships (1.9%), energy production and refining (1.7%), film and music (0.4%), and air transport (0.6%) to get a similar share. At a personal level, the ILO-regulated apparel jobs as of 2021 (mostly women, often with on-site clinics) made up about a tenth of Haiti’s regular, hourly-wage-paying jobs. Statistics have been scarce since then, but even with falling factory employment the share of formal labor may have been higher earlier this year.

As the ILO’s comment suggests, Haiti’s protracted political crisis has damaged but so far not broken these businesses and their workers. For most of this year, Better Work’s factories were shipping about 800,000 clothing articles to the U.S. daily via the 40-hour boat ride to the Port of Miami, together earning about $50 million a month.

The factories persist because of a special trade program — HOPE/HELP, suitably upbeat acronyms for “Haitian Hemispheric Opportunity through Partnership Encouragement”, and “Haitian Economic Lift Program” — created 20 years ago. This waives the pricy 16.5% tariff a cotton T-shirt normally gets, and has unusually simple and easy rules for the sorts of fabric factories can use to make the shirt. Last authorized in 2015, HOPE/HELP is scheduled to end in September next year. So each week the uncertainty about its future prospects grows, and the prospect of its end appears already to be pulling business away. As the ILO’s staffers were writing up their report, one of their factories had shut, and the other two were temporarily closed. This week, only 13 factories appear to be open and producing. So the already substantial worries facing the seamstresses and their employers are growing rapidly more intense.

Now back to Congress, in this session’s last days. Haiti relies more heavily than any other country in the world on American ‘trade preference’ support. Haiti’s is an exceptional case in which loss of trade preference could spark a national economic crisis as well as well as harm to the workers. But an exceptional case, HOPE/HELP isn’t alone. The 24-year-old benefit for Africa, the “African Growth and Opportunity Act” — frequently termed the “cornerstone” of U.S.-African economic relations — is also set to expire next year, and the broader “Generalized System of Preferences” has been in a sort of legal limbo since 2020, with renewal serially frustrated by intense arguments over what we see as relatively minor differences in the wording of eligibility criteria, and then by ‘hostage-taking’ on unrelated topics. Putting off renewal until next year is full of risk: a new Congress with new members unfamiliar with the programs, along with typically slow agency nominations, both make timely renewal hard to imagine and outright lapse fully possible.

These three programs represent a small share of U.S. trade flows: $29 billion in imports in 2023, about 0.9% of the $3.1 trillion in total U.S. imports, and well below the $80 billion from Ireland or the $53 billion from Switzerland. Despite this modest total, HOPE/HELP, AGOA, and GSP remain of great importance to Port-au-Prince’s anxious seamstresses as they “battle the odds” against them — and (via AGOA) to their garment-industry sisters in Maseru, Antanarivo, and Nairobi, and (via GSP) to tuna cannery workers in Honiara, jewelry-makers in Yerevan, and tannery guys in Asuncion. For Congress, a few minutes’ work for the less fortunate, before the Members go home for their own Christmas holidays, would be time well spent.

Miami-based Haitian Times on remittances from expatriates — construction workers, restaurant dishwashers, professionals — as a second economic lifeline.

And what do “jobs,” “unemployment,” and similar terms mean in this context? World Bank databases say that Haiti’s labor force is about 5.2 million people — 45% in agriculture, 55% urban — with an unemployment rate of 15.7%. These figures suggest totals of 760,000 unemployed workers and 4.3 million with “jobs.” “Unemployment,” though, is a labor-market term invented in the 1880s and designed for wealthy countries in which most workers are in wage-paying jobs subject to national laws and taxes. The term, or at least its commonly understood American definition, doesn’t suit least-developed country realities in general, let alone in crisis. An actual on-the-ground WB report from 2021 guesses that even before the breakdown of government in 2022, 86% of “employed” Haitian workers, or about 4 million people, were in the “informal sector” — that is, doing irregular work in seasonal harvesting, maid and gardening work, day-labor on construction sites, and so on. These would be spottily paid, and not subject to minimum wage or occupational health and safety laws. This implies that about 500,000 Haitian jobs, such as those in the garment industry — 60,000 at the time, fewer now — offer safety inspection, minimum wage laws, and so on. The World Bank’s background on Haiti’s pre-COVID, pre-“gang era” private-sector economy.

ABOUT ED

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank ProgressiveEconomy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

Consumers and the dollars they spend are the backbone of the U.S. economy. For the last several years, consumers have grown frustrated by high prices for basic necessities like housing, food, and health care. Anger around rising prices and a high cost of living played a major role in the 2024 U.S. presidential election. Disillusionment with the “Bidenomics” agenda fueled a sense of disenfranchisement. Namely, consumers’ struggle to afford necessities was put on the back burner in favor of proposals that would benefit elite demographics, not working-class voters.

High prices in consumer-facing sectors that account for the vast bulk of spending are driven by a number of factors: inflation, economic scarcity, opportunistic price gouging, and market power wielded by powerful firms. This report by the Progressive Policy Institute (PPI) takes up the problem of market power, or the ability of powerful firms — rather than competition — to control prices.

To head off the skeptics, disentangling the role of market power from other drivers of high prices is unnecessary. There is substantial evidence that sectors that have an outsized impact on consumers’ pocketbooks lack robust competition. This results, in part, from decades of consolidation, sluggish growth in productivity, and some bottlenecked supply chains that contribute to high consumer prices.

This report asks if antitrust could be doing a better job of protecting consumers. Analysis of a number of key trends over the last 15 years indicates that the answer is “yes.” Indeed, by many measures, antitrust has lost touch with consumers. This finding is especially relevant with the changing of the antitrust guard from the Biden to Trump administrations. With little common bipartisan ground on a “populist” antitrust agenda, a scaling back or scrapping of the Neo-Brandeisian movement’s influence at the U.S. antitrust agencies is likely. This does not necessarily mean, however, that antitrust enforcement will decline in vigor.

The Biden antitrust enforcers focused on extending the reach of antitrust from traditional law enforcement to solve broader economic, political, and social problems; introducing new standards; and taming market power in the digital sector. This retooling of antitrust appeared in many ways to be tone deaf to the pleas of Americans besieged by high prices and living costs resulting from harmful consolidation and business practices. Moreover, it likely came at the expense of enforcement that more directly protects consumers’ pocketbooks.

PPI’s analysis breaks down major factors that highlight the importance of antitrust priorities focused on directly protecting consumers from the effect of market power on raising prices and their cost of living. It looks at flagging productivity in the top five sectors in which consumers spend 75% of their budgets. The analysis exposes high concentration and market power “bottlenecks” that supercharge high prices to consumers and destabilize critical supply chains, such as in health care and food. The analysis also finds lackluster merger enforcement — the most important tool for controlling consolidation that can drive up prices — in the top five consumer-facing sectors over the last 15 years.

The report concludes with policy recommendations. These range from reshuffling merger review responsibilities at the DOJ and FTC, to junking policies for approving harmful mergers subject to ineffective remedies. Other recommendations focus on how the agencies should consider the impact of market power on the stability and resiliency of critical supply chains, and call for the agencies to get up the learning curve on strengthening enforcement in consumer-facing sectors.