Bloomberg recently ran an article about the impact of Amazon fulfillment centers on warehouse wages. The story’s point was simple: “A Bloomberg analysis of government labor statistics reveals that in community after community where Amazon sets up shop, warehouse wages tend to fall.”

A bit of background here: The once-sleepy warehousing industry, which was nobody’s idea of a growth sector, used to be the equivalent of serviceable shoes. Companies would put up warehouses to store parts that were heading to domestic factories, and to store finished products that were on their way from domestic manufacturers to retailers and business purchasers. Later, as U.S. factories closed, warehouses held mountains of imports from China and other countries.

Prior to the ecommerce era, the whole notion of a governor or mayor proclaiming “We need another warehouse as a source of good jobs!” was laughable. Indeed, warehousing in most counties was a tiny source of jobs, often too small to be measured and reported by the Bureau of Labor Statistics.

But the ecommerce boom has supercharged the warehousing industry. Most eCommerce fulfillment centers are counted as warehouses by the BLS, but as I wrote in my 2017 report, these fulfillment centers “bear the same relationship to ordinary warehouses as jet planes bear to bicycles. Whereas an ordinary retail warehouse is a stopping place for bulk shipments on the way to stores, a fulfillment center dynamically responds to orders from individual customers, integrating many different vendors.”

Thus, the Bloomberg story is covering an important topic, as I told the reporter. And given my long history as chief economist and economics writer at BusinessWeek (in its pre-Bloomberg days), I strongly support journalistic organizations doing data-driven reporting. It’s the right way to go.

But based on my own analysis, I strongly disagree with the conclusions in the story. More broadly, I’m concerned with the need to put data into context.

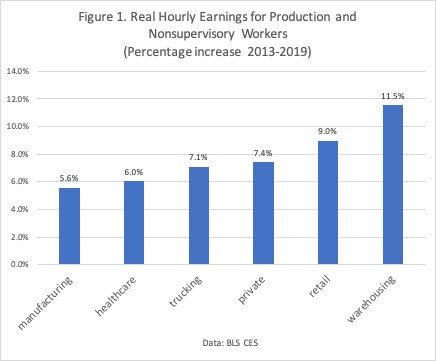

Let’s start by taking a closer look at BLS data for wages for production and nonsupervisory workers in the warehousing industry, which are the floor workers that we actually care about. Rather than falling, as the story implies, hourly earnings for production and nonsupervisory workers in the warehousing industry, adjusted for inflation, have risen by 11.5% in the “e-commerce era” (2013-2019). (details available on request). That’s a far bigger gain than other major sectors, including retail, manufacturing and healthcare (Figure 1).

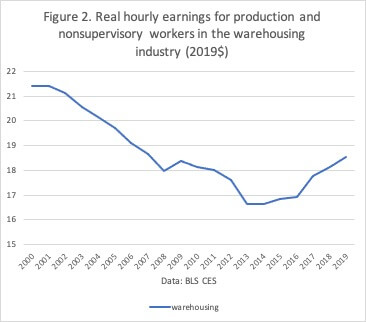

To put this in context, this increase in real wages for production and nonsupervisory workers—who make up almost 90 percent of the employees in the “warehousing and storage” industry (NAICS 493)—comes after many years of declining real wages in an industry that was moribund and stagnant before it was transformed by the coming of ecommerce (Figure 2)

Why do these figures paint a very different picture than the Bloomberg article? One key difference comes from the limitations of the particular wage measure that Bloomberg used, average weekly wages from the Quarterly Census of Employment and Wages (QCEW). I will discuss here some of the strengths and weakness of the QCEW wage measure that the Bloomberg article uses.

Second, the Bloomberg piece misses the broader context of the ongoing transformation of consumer distribution, which has integrated retail, warehousing, and delivery in a way that was never possible before. Ecommerce uses technology to create jobs, boost productivity, and raise pay by shifting workers from low-paid brick-and-mortar retail jobs to much better paid ecommerce fulfillment jobs. I will discuss this broader point as well.

We start with a description of the wage measure used by the Bloomberg article. The QCEW collects data on employment and wage payments on a detailed industry and county basis. It enables economists to say, for example, that there were 898 employees in the warehousing industry in Mercer County (NJ) in 2013, rising to 6115 employees in 2019. (Mercer County is the location of the Robbinsville (NJ) Amazon facility featured in the Bloomberg story). The QCEW data also reports that wage payments to warehousing workers in Mercer County rose from $46,223,000 in 2013 to $222,356,000 in 2019, and that average weekly wage fell from $990 to $699 per week.

What do we make of this decline in average weekly wages? The QCEW data are very useful, if handled with care. But the QCEW has limitations. First, there is no information on hours of work on a county and industry level, so average weekly wages can rise or fall as workers work more or fewer hours per week. If there are more part-time workers, average weekly wages can fall, even if hourly wages stay the same.

Second, the lack of QCEW data on hours of work by industry and county means that hourly earnings cannot be calculated from the QCEW data without making additional assumptions. (For example, the Bloomberg article appears to report hourly earnings for warehousing workers in Mercer County, saying that “Six years ago, before the company opened a giant fulfillment center in Robbinsville, New Jersey, warehouse workers made $24 an hour on average, according to BLS data. Last year the average hourly wage slipped to $17.50.” I could be wrong, but it appears to me that this calculation was done by assuming that average hours worked per week in the warehousing industry in Mercer County did not change after Amazon opened its facility. If so, the Bloomberg piece should have reported that assumption.).

Third, QCEW weekly wages can change as the composition of the workforce changes. For example, if the composition of warehouses shift towards relatively fewer high-paid managers and relatively more nonsupervisory workers, that could lower average weekly wages even if the wages for the nonsupervisory workers was actually rising.

A simple example will make that point. Suppose that we start off with a sleepy little warehouse with 1 manager earning $1200 per week and 1 “picker and packer” earning $600 per week. Then the average weekly pay for the entire operations is $900 per week. Now suppose that the operation expands to hire 7 more “picker and packer” and in order to attract the new workers their pay is raised to $660 per week. Then the average weekly pay falls to $720 per week, even though pay for individual workers has increased (Calculations available upon request).

A related point is that average weekly wages in the QCEW data can rise if younger and lower-paid workers are laid off. So in the example above, if the single picker and packer was laid off, leaving only the manager, the weekly wage at the “warehouse” would go from $900 to $1200. My analysis of the BLS county-level data (details available on request) shows a negative correlation between job growth and weekly wage growth in warehousing over the time period 2007 to 2019.. Indeed, many of the counties with the biggest wage growth in warehousing also have shrinking warehouse employment. Meanwhile, fast-growth counties, whether they have an Amazon facility or not, show relatively slow warehousing wage growth on average.

Fourth, the QCEW is sensitive to the form of compensation. Employer payments for benefits such as health care and retirement contributions are not generally counted as part of QCEW wages (though some states do count 401k contributions). So if there is a shift towards employers who pay better benefits, that does not show up in the QCEW wages.

In addition, most stock options are generally not counted as part of QCEW pay until they are exercised and become taxable income. Similarly, restricted stock units (RSU) are generally not counted as part of QCEW pay until they vest and become taxable.

This last point, while wonky, is relevant for analyzing Amazon pay in particular. According to press reports, many Amazon fulfillment center workers received restricted stock units during the years covered by the Bloomberg study. According to one source, Amazon RSUs vest at 5% after one year, another 15% after two years, another 40% after three years, and the final 40% after four years. For example, a big chunk of compensation paid to an Amazon fulfillment center worker in 2014 would not show up in the QCEW data until 2017 and 2018. That would artificially depress the initial reported wages when a new fulfillment center opens, especially given the rise in Amazon stock prices.

To further complicate matters, when Amazon raised its minimum wage to $15 in 2018, it also changed the form of its compensation package for fulfillment center workers, including phasing out RSUs. These changes make it very difficult to interpret the recent QCEW wage figures. My best guess is reported weekly wages in warehousing are significantly underestimated, but coming up with a quantitative figure would require an in-depth analysis of the Amazon pay package, which I have not done, as well as an estimate of worker churn.

The BLS offers alternative sources of pay data. The Current Employment Statistics program asks a sample of businesses to report wages and hours by industry, with an additional category of production and nonsupervisory employees. These figures, which do *not* include annual bonuses, were reported in Figures 1 and 2. As noted, they show strong growth in real hourly earnings for production and nonsupervisory workers in the warehousing industry. The caveat is that they do not reflect changes in the annual bonus structure of the industry.

Another source of pay data is the Occupational Employment Statistics (OES) program, which offers detailed data on pay for occupations in different industries and locations. The OES enables us to compare “apples to apples,” matching up the same occupations in different industries. In particular , laborers and material movers, who make up about 45% of the warehousing workforce, average $16.19 per hour in the warehousing industry. That’s more than workers in the same occupation make in manufacturing ($15.78) or the private sector as a whole ($14.64), as shown in Figure 3.

Taking these numbers on face value suggests that laborers and material movers can do better in the warehousing industry than in the rest of the economy, which is probably the right comparison to make. Note, interestingly enough, that the overall wage in warehousing is lower than manufacturing or private, pulled down by a lower white-collar wage. However, as before, the key caveat is that these figures do not include annual bonuses, exercised stock options or tuition repayments. So the lower wages for white-collar workers should be taken with a grain of salt.

| Figure 3. 2019 average hourly pay, dollars per hour (OES) | |||

| Warehousing | Manufacturing | Private sector | |

| All occupations | 19.77 | 26.09 | 25.20 |

| Management Occupations | 52.65 | 65.11 | 60.26 |

| Business and financial operations | 31.99 | 36.92 | 37.92 |

| Computer and mathematical occupations | 33.56 | 49.38 | 45.88 |

| Office and Administrative Support | 19.62 | 20.91 | 19.46 |

| Installation, Maintenance, and Repair | 24.82 | 25.98 | 23.95 |

| Transportation and material moving occupations | 17.96 | 17.58 | 18.01 |

| Laborers and material movers | 16.19 | 15.78 | 14.64 |

| Packers and Packagers, Hand | 15.01 | 13.94 | 13.30 |

| Data: BLS (OES) | |||

But that’s enough about the wonky dive into the data. Now let’s consider the broader question about how to best measure the impact on the labor market of the ongoing transformation of the retail, warehousing, and delivery industries.

Conventional retailing—especially big box retailing—turned the store into the warehouse, and consumers into pickers and packers. Clothes, electronics, and building materials were stacked to the ceiling, as buyers roamed the “miles of aisles.” Households had to drive to stores and effectively be their own delivery services. In return, they could get everything they needed in one place.

E-commerce flips the equation. The picking and packing function is done by ecommerce fulfillment workers, saving household time and creating jobs. These jobs are clearly better paid than the typical jobs in the brick-and-mortar retail sector, by about 30 percent.

Even during the pandemic, the jobs generated in electronic shopping, ecommerce fulfillment and delivery either more than or almost compensates for the jobs lost in brick-and-mortar retail, depending on the month. For example, if we compare October 2019 to October 2020, brick-and-mortar lost 269,000 full-time-equivalent (FTE) jobs while ecommerce industries (NAICS 4541, 492, and 493) gained 295,000 FTE jobs, for a net plus.

Even as the new consumer distribution sector—retail, warehousing, and delivery–uses technology to improve productivity, it’s generating new higher-paying jobs. From October 2019 to October 2020, average hourly earnings in the combined retail, warehousing, and delivery sector rose by 5.2 percent, far above the rate of inflation and beating the average private sector wage growth of 4.4 percent (by this time I don’t need to remind you of the multiple caveats).

What about the labor market in Mercer County, home of the Robbinsville (NJ) fulfillment center featured in the Bloomberg story? It turns out that looking at the broader consumer distribution sector–compromising retail, warehousing and couriers and messengers (local delivery)–gives a very different picture than simply focusing on warehousing (Figure 4).

Over the 2013-2019 period Mercer County employment in the consumer distribution sector—comprising retail, warehousing and couriers and messengers (local delivery) expanded by 25%, almost double the rate in the rest of the private sector (Figure 4). That’s all coming from warehousing, and it’s unalloyed good news for Mercer County workers, because they have access to many more job opportunities.

Similarly, total wage payments in the consumer distribution sector expanded by 42%, also much faster than the rest of the labor market. That’s good news for the local economy, and tax revenues.

And wage growth in the consumer distribution sector was somewhat faster than the rest of the labor market, as workers were hired in warehousing jobs that paid significantly more than brick-and-mortar retail in the county. These figures suggest that Mercer County’s workers and local economy benefited from the transformation of the consumer distribution sector (once again, all caveats apply).

| Figure 4. Mercer County (NJ), percentage change, 2013-2019 | ||

| Consumer distribution* | private sector minus consumer distribution | |

| Jobs | 25.1% | 13.0% |

| Total wage payments | 42.4% | 27.5% |

| Average weekly wages | 13.8% | 12.8% |

| *Retail, warehousing, couriers and messengers | ||

| Data: BLS QCEW | ||

I’m going to stop this overly-long blog post here. The bottom line is that the Bloomberg story tackled an interesting and important question, but if reporters do data-driven stories, they need to be more sensitive to the strengths and weaknesses of the underlying data. Interrogate the data as they would interrogate a source, rather than taking it for granted. Let the readers know where the assumptions are and the problems are. Give them alternative perspectives and context.