The House of Representatives is set to vote next week on President Biden’s bipartisan infrastructure bill. At stake is not just a stronger U.S. economy, but whether we still have a functioning democracy.

In normal times, this bill wouldn’t be controversial. Almost no one disputes the need for a major infusion of public investment in modernizing America’s transportation, water and other common goods that undergird U.S. economic innovation and competitiveness. That’s why the bill breezed through an otherwise polarized Senate on a 60-30 vote in August.

In the House, however, progressives are threatening to torpedo the bill unless they get a simultaneous vote on a “reconciliation” bill that would spend trillions more on social and climate programs. Critics have assailed this tactic as political hostage-taking, but it’s more like a murder-suicide pact, since progressives want a big infrastructure bill too.

But they’re apparently willing to sacrifice the infrastructure upgrade to gain political leverage over the growing ranks of moderate Democrats who, although they support many elements of the massive reconciliation bill, are balking at its $3.5 trillion price tag.

The shape of inflation over the past year isn’t what you might expect. The table below pulls out the change in price for selected goods and services from July 2020 to July 2021, based on BEA personal consumption expenditure (PCE) data (we explain below why we use BEA rather than BLS data).

The overall price level for personal consumption expenditures rose by 4.2% over the past year. (that’s the bold line in the middle of the table). Well-reported contributors to inflation include car rentals (+74%) and purchases of used vehicles (+37%), both spectacularly large pandemic-related increases that no one expects to continue. Other price increases are clearly related to the disruptions of supply chains: Furniture (9%), televisions (10%), and major appliances (12%).

But then there are some price increases that are not so obviously related to the pandemic, and maybe sticky. The price of financial services is up 5%, driven in part by pension funds (12%) and financial service charges, fees, and commissions (+9%). The latter category includes portfolio management and investment advice services, where prices have risen 17% over the past year. That’s disturbing given the importance of the financial system.

Meanwhile some goods and services showed much slower than average price increases. For example, the price of beer only rose by 2.1% from July 2020 to July 2021, about half the overall inflation rate, and lower than the 2.6% increase in the price of food purchased for off-premises consumption.

The price of rental tenant-occupied nonfarm housing rose only 1.9%. That’s the lowest rental inflation rate in decades, with the exception of 2008-09 financial crisis and its aftermath.

Finally, there is the price of telecom and broadband services, which only rose 0.5% over the past year. To calculate this figure, we built a price index that combined wireless and wired telephone, cable and satellite television, internet access, and video and audio streaming, taking into account shifts in spending patterns as consumers adapt to new technological choices.

Change in personal consumption expenditure prices (July 2020-July 2021)

Spectator sports

-4.6%

Prescription drugs

-2.5%

Personal care products

-0.5%

Insurance

-0.2%

Recreational books

0.1%

Household cleaning products

0.3%

Telecom and broadband*

0.5%

Legal services

0.6%

Education services

0.8%

Rental of tenant-occupied nonfarm housing

1.9%

Beer

2.1%

Nursing homes

2.3%

Imputed rental of owner-occupied nonfarm housing

2.4%

Pets and related products

2.4%

Newspapers and periodicals

2.5%

Educational books

2.6%

Food purchased for off-premises consumption

2.6%

Hospitals

2.9%

Physician services

3.4%

Accounting and other business services

3.7%

Veterinary and other services for pets

4.1%

Personal consumption expenditures

4.2%

Hairdressing salons and personal grooming establishments

4.8%

Financial services

5.0%

Social assistance

5.0%

Meats and poultry

5.4%

Repair of household appliances

6.1%

Fresh milk

6.2%

Museums and libraries

6.2%

Meals at limited service eating places

6.6%

Electricity and gas

7.0%

Nonpostal delivery services

7.7%

Furniture

8.8%

Financial service charges, fees, and commissions

9.2%

Televisions

9.9%

Pension funds

12.2%

Major household appliances

12.3%

Moving, storage, and freight services

13.3%

Portfolio management and investment advice services

16.6%

Air transportation

19.7%

Net purchases of used motor vehicles

36.5%

Motor vehicle rental

73.5%

*Includes wireless and wired telephone; cable and satellite television; internet access; video and audio streaming

Data: BEA

Note: The BLS publishes the Consumer Price Index (CPI) for various goods and services, while the BEA publishes a set of price indices connected with Personal Consumption Expenditure (PCE) data. Both are useful, but the Federal Reserve tends to give somewhat more weight to the PCE inflation rate because it accounts better for changes in spending patterns. Similarly, using the PCE gives us an opportunity to construct a price index for the telecom and broadband sector that has a chance of capturing some of the rapid changes in the sector.

As Democrats shape the reconciliation package, Congressional leaders must work to earn voter trust on jobs, debt and support for private enterprise

The Progressive Policy Institute (PPI) recently commissioned a national survey by Expedition Strategies of public attitudes in battleground 44 House districts and eight states likely to have competitive Senate races next year. This second report focuses on how these pivotal voters compare the two parties on jobs and the economy, tax and fiscal policy, and innovation, entrepreneurship and competition.

“Our findings provide crucial context for today’s debate – both between the parties and between the pragmatic and left wings of the Democratic Party – over the size, cost and financing of President Biden’s ambitious Build Back Better plans,” said PPI President Will Marshall.

“The good news is that battleground voters trust Biden and the Democrats more to improve the economy and deliver tax fairness,” he added. “But there are warning signs here on job creation, deficits and paying for public investment that Democrats should heed as they shape their big reconciliation package.”

The full memo on this exclusive polling can be found here. Here are some of the key takeaways:

Battleground voters trust President Biden (53%- 47%) and Congressional Democrats (52%-48%) more than Republicans to “improve the economy.”

They overwhelmingly believe that Republicans stand more for the wealthy (74%) and favor special interests (63%), while Democrats are seen as representing the poor (72%).

Although they want Biden to succeed, voters divide evenly on which party “knows how to create good jobs” and lean toward the GOP as the party that “knows how to strengthen the economy (52-48).

Republicans appear to have a structural advantage on helping companies be more innovative, working to create private sector jobs, strengthening the economy, and helping U.S. firms win the competition with China for economic and technological leadership.

Two-thirds of battleground voters say they are concerned that Democrats are too anti-business. This includes 73% of Independents and even 42% of Democrats.

Possibly as a result, voters are more likely to credit the GOP as the party striving to create private sector jobs (54-46).

Voters lean strongly toward the Democratic position on tax fairness, saying their top goal for tax policy is “making sure the wealthy and companies pay more in taxes.”

Voters also side with Democrats in supporting additional IRS funding to crack down on tax cheats and evaders.

Battleground voters favor more public investment to improve the economy over cutting taxes and regulations by a solid margin, 58-42. Republican supply side nostrums aren’t getting traction.

On the economy, voters say jobs, growth and rewarding work are more important goals than addressing inequality and fairness. Only 10% said “promoting fairness” should be the most important goal.

Battleground district and state voters rank deficits and debt as their second highest economic concern. By 88-12, they say the national debt is a “serious problem.” Independents, undecideds, and Hispanic voters strongly express this view.

By 80-20, voters say they are worried about the mounting debt burden on the young and working families. They also express strong concerns about inflation (74-26).

Voters are slightly more inclined to blame Democrats than Republicans for running up public debt (32-28). Similarly, they trust Republicans more than Democrats (32-28) to get the debt under control, but a plurality (40%) say they trust neither party.

These voters favor (53-47) taxing gains from capital and labor at the same level. However, they oppose capital gains hikes when they are presented as a way to finance public investment in infrastructure and child tax credits (54% opposed).

Last week, PPI released the first report on the poll, which focused on voter attitudes towards President Biden’s infrastructure plan and the social investment package Democrats hope to pass using the reconciliation process.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

As House Democrats start work today on a massive, $3.5 trillion reconciliation bill, a new Expedition Strategies poll offers timely insights into how a pivotal group of voters view President Biden’s ambitious “Build Back Better” agenda.

The findings suggest Biden and Congressional Democrats should focus public attention on the broad economic benefits of the reconciliation bill rather than social equity and be flexible about the ultimate size and cost of the spending package.

Commissioned by the Progressive Policy Institute, the poll surveyed voters in 44 battleground House Districts and eight states likely to have competitive Senate races in next year’s midterm elections. “What happens in these critical swing districts and states will determine whether Democrats can enlarge their slender House and Senate majorities or yield control to the Republicans,” said PPI President Will Marshall.

“There’s encouraging news for President Biden and the Democrats here, but also grounds for proceeding cautiously on the reconciliation spending package,” he added. “Battleground voters are worried about piling up debt on young working families.”

This report, the first of a series based on this extensive poll’s findings, can be found here. Here are some key takeaways:

Battleground voters overwhelmingly (73-27) support the president’s bipartisan infrastructure bill. Even more (83-17) approve of his determination to work with Republicans to get it done, and 85% say it’s a “major investment” in strengthening the U.S. economy.

These voters also favor Biden’s proposed “human infrastructure” or social investment package, but by a much narrower margin, 54-46.

In general, these voters respond more favorably to arguments that the package will create jobs and economic opportunity and reward work than to arguments that it’s necessary to reduce economic inequality.”

Battleground district and state voters rank deficits and debt as their second highest economic concern. By 88-12, they say the national debt is a “serious problem.”

These voters favor paying for these initiatives with a mix of tax hikes and public borrowing rather than just adding them to the deficit. By a solid 57-43 margin, they favor increasing taxes on the wealthy and corporations to pay for new public investments. Two-thirds of voters believe inherited income should be taxed at the same or higher rate than earned income.

Republican supply side nostrums may be losing their potency. A variety of Democratic arguments that offer an activist economic alternative are more appealing to these voters than the traditional Republican mantra of cutting taxes and regulation.

However, Democrats should be wary of claims that these voters will reward “bold” action on spending. When asked if the federal government should make investments but be careful about how much spending and the national debt increases or make bold and significant new investments and address the impact on the debt later, 63% say to be careful while just 20% say be bold and worry about the debt later.

In a warning to Democrats, three-in-four (73%) voters say they are concerned that “Democrats in Congress want to spend too much money without paying for it.” In addition, 74% said they are worried that these bills may lead to inflation.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

When Congressional Democrats began the legislative process to enact President Biden’s Build Back Better agenda last month, Sen. Bernie Sanders insisted on adding a costly expansion of Medicare benefits to the bill. But a new report from the program’s trustees makes clear that this expansion would be unwise: Medicare is already expensive and growing faster than the revenues needed to finance it, resulting in unsustainable deficits. Before Washington considers adding benefits that would further increase costs, it must find a way to pay for the promises it’s already made. Otherwise, critical public investments in young Americans and working families in greater need could be crowded out.

As part of the American Rescue Plan (ARP) they passed in March, Democrats increased the maximum child tax credit (CTC) parents can claim in 2021 for each of their children under 18 years old to $3,000, or $3,600 for each child under age six, and made the full value of the credit available to families with no income for the first time ever. The expansion lifted three million children out of poverty in its first month alone, which will improve their educational, health and economic outcomes throughout their lives if the policy is continued.

Democrats have made extending this policy a centerpiece of their $3.5 trillion Build Back Better agenda. But despite its success, Democrats are only proposing to extend the expanded CTC through 2025 at the latest because the annual cost of continuing the current expansion will roughly double after related policies from the GOP’s 2017 tax law expire. Fortunately, they can resolve this problem making those related policies permanent.

The GOP tax law temporarily doubled the maximum CTC to $2,000 and made more high-income parents eligible for the credit as part of a broader effort to consolidate family tax benefits. Previously, parents could claim a CTC worth up to $1,000 for each of their children, and all households could reduce their taxable income by $4,050 for each “personal exemption” they claimed for themselves and their dependents.

Taxpayers could also choose to either deduct the cost of specific expenses from their taxable income or claim a “standard deduction” that was the same for everyone. The GOP tax law temporarily repealed personal exemptions but increased the CTC (which replaced exemptions for children), doubled the standard deduction (which replaced exemptions for taxpayers themselves) and created a $500 non-refundable credit for non-child dependents.

To keep their bill from adding to the deficit after 10 years, which would have prohibited them from passing it via the filibuster-proof “reconciliation” process, Republicans scheduled these, and many of their bill’s other provisions, to expire after 2025. Those expirations are what would make a formal score of the cost of the Democrats’ CTC expansion spike after that year.

The official scorekeepers at the Joint Committee on Taxation and Congressional Budget Office score the fiscal impact of all proposals over a 10-year window relative to their “current law baseline,” or the levels of spending and revenues that would occur if Congress did not pass any new laws. Since the GOP tax law scheduled the CTC to shrink after 2025, the gap between the Democrats’ proposed spending levels and current law would grow. The expiration would add roughly $530 billion to the expansion’s 10-fiscal year cost. Should the Democrats’ expanded CTC be made permanent, families in 2026 would be eligible for both the enlarged CTC and the larger per-child exemption that existed in 2017, meaning the tax benefit per child would be even greater than it is today.

Rather than create an unintended bonus benefit that raises the CTC expansion’s cost, Democrats should simply make the changes to personal exemptions and the standard deduction permanent. Based on figures from the Tax Foundation, PPI estimates that permanently repealing personal exemptions while retaining the increased standard deduction and credit for dependents not eligible for the CTC would reduce the net cost of the Democrats’ CTC expansion by more than $100 billion each year after 2025.

As a result, Democrats may need only about $800 billion in additional offsets over the 10-year window to make the current CTC permanent (and even less if they are willing to consider a slightly smaller expansion). Although this figure could be a slight underestimate, since the Office of Management and Budget projects the CTC expansion would cost roughly 10 percent more than Tax Foundation does, the cost of this package is still likely to be only around half the $1.6 trillion cost of making the expanded CTC permanent on its own.

Making these reforms permanent would not only help pay for the CTC expansion but also give Democrats ownership of one of the few progressive components of the GOP’s tax law. The CTC expansion is more progressive than exemptions for dependents because credits directly reduce a taxpayer’s final liability, while exemptions lower their taxable income, which gives a bigger benefit to those in high tax brackets than those in low brackets. Meanwhile, the increased standard deduction only benefits households that do not itemize their deductions, which are disproportionately low- and middle-income households. Making this progressive benefit consolidation permanent now would prevent Republicans from using the continuation of middle-class tax cuts as a vehicle to enact more tax cuts for the rich in 2025.

Democrats do not want their most consequential anti-poverty policy in a generation to expire less than four years from now. When polls show that a majority of voters support the current CTC expansion but are skeptical of continuing it post-pandemic, lawmakers cannot necessarily count on their successors to keep a temporary extension from expiring. Rather than jeopardizing these important benefits to circumvent budget scoring rules, Democrats should protect their policy achievement and help pay for it by extending other family tax provisions in place today along with it.

Brendan McDermott is a fiscal policy analyst at the Progressive Policy Institute’s Center for Funding America’s Future.

Join the Progressive Policy Institute for a high-level international briefing and dialogue on the status of and reception to a GlobalMinimumTax in the U.S. Congress.

This hour-long event will feature Beth Bell, Staff Director of the Subcommittee on Select Revenue Measures on the House of Representative’s Ways and Means Committee.

Attendees are asked to share their perspectives and thoughts on the GlobalMinimumTax.

When: Tuesday, August 31, 2021

11:00AM EDT / 5:00PM CEST

Featuring:

Beth Bell

Staff Director, Subcommittee on Select Revenue Measures | Ways and Means Committee, U.S, House of Representatives

Moderated by:

Michael Mandel, Chief Economic Strategist, PPI

This event is closed to the press and by invitation only.

What would a new middle class look like? And which industries are leading the way?

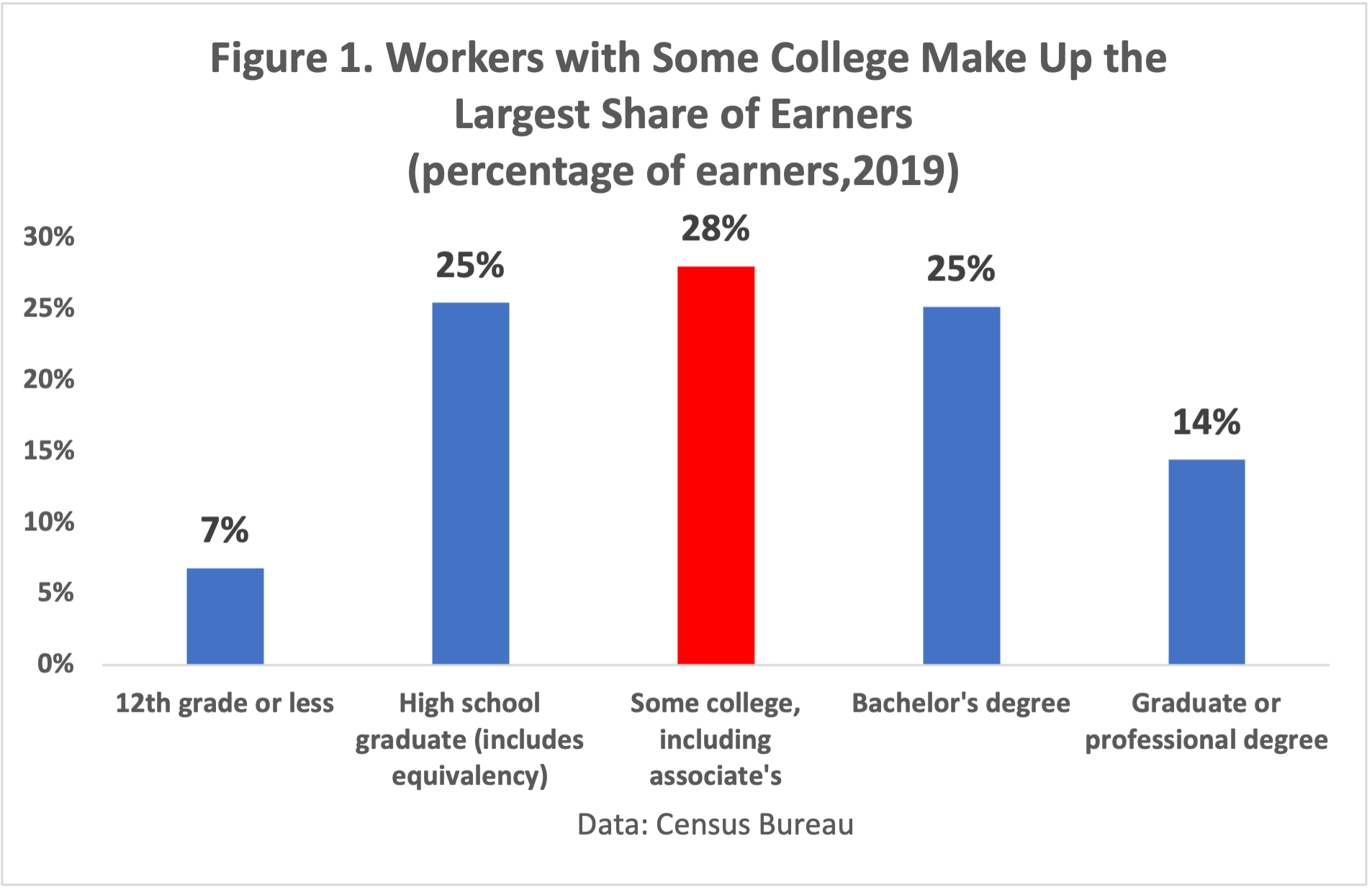

We actually know who is missing from the middle class. More than one-quarter of American workers have some college (including an associate’s degree), but no bachelor’s degree. These are the people at the middle of the education distribution, and the single largest group (Figure 1) — but they are also the people who been betrayed by the transformations of the American economy in recent years. They invested time and often took on debt to go to school, and discovered that employers did not want to pay them.

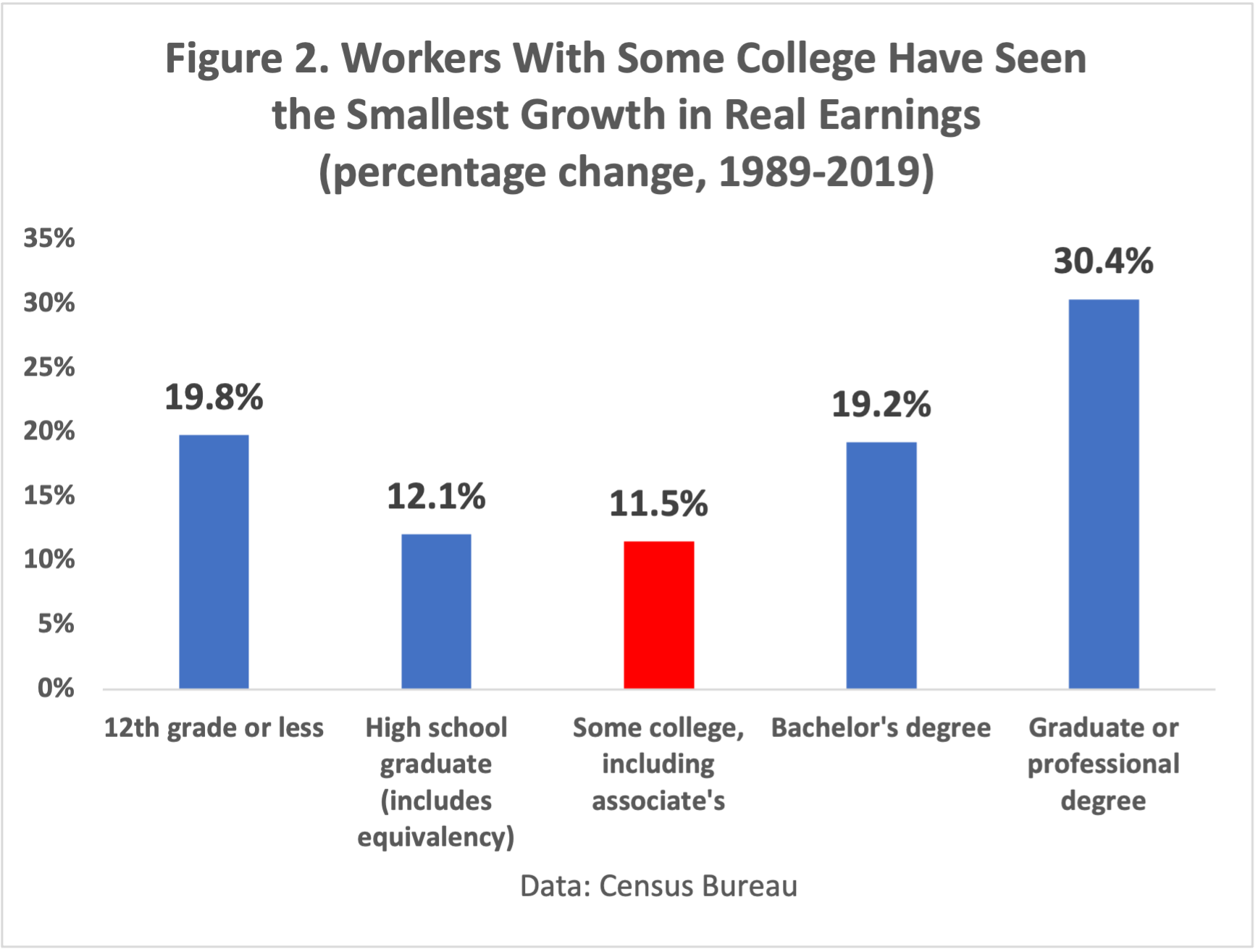

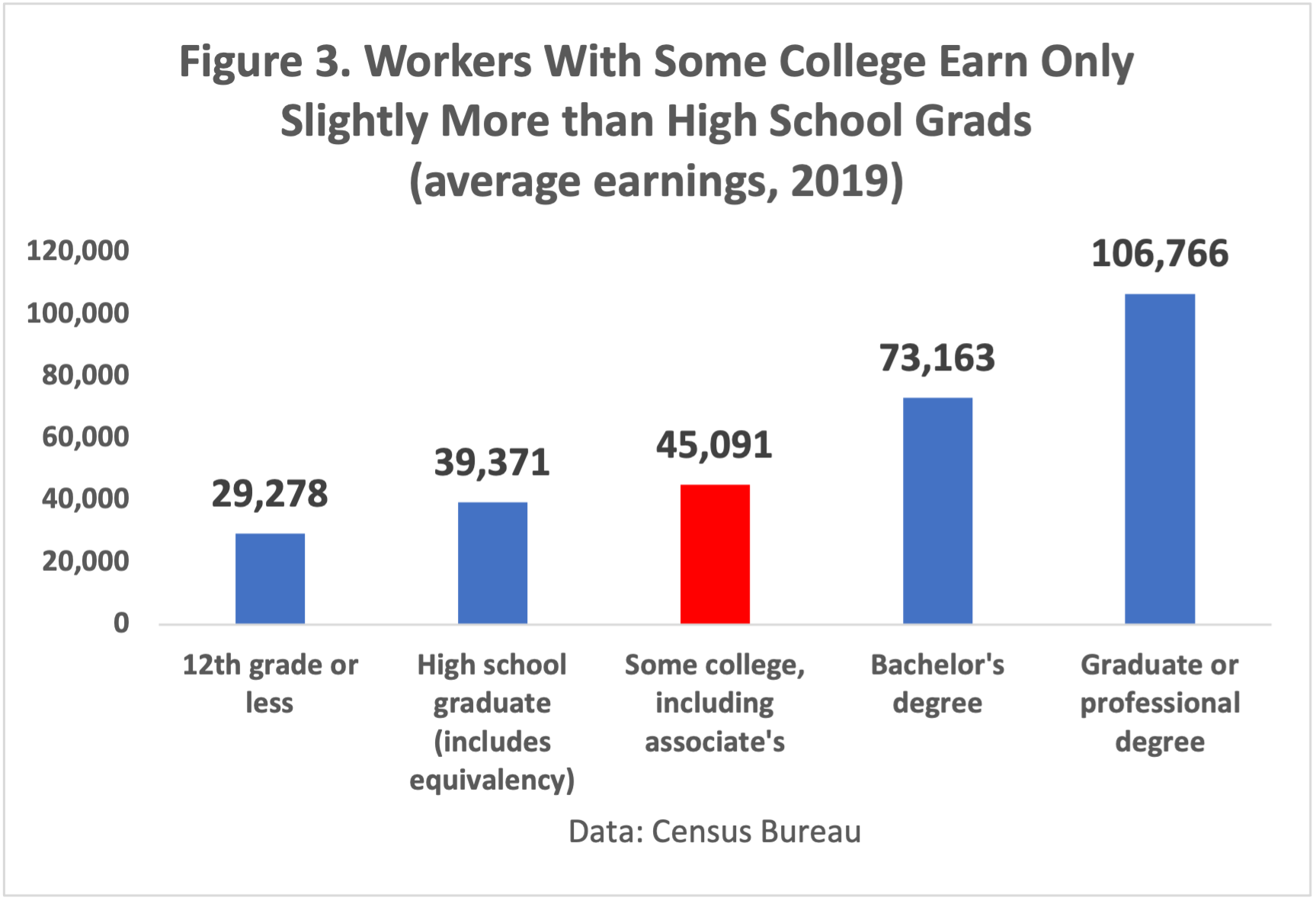

Over the past 30 years, workers with some college have seen their real earnings rise by less than 12%, slower than every other group including workers with only a high school diploma (Figure 2), As of 2019, the average person with some college but no bachelor’s earned only $45,000, just $6,000 more than the average high school graduate. By comparison, the average person with a bachelor’s degree but no advanced degree earned $73,000 (Figure 3). That’s a huge payoff for the bachelor’s degree, but much, much less for some college.

In America, having a “middle” education does not mean earning a “middle” income or being part of the “middle” class. There’s a hole in the middle of the income distribution, and it’s hurting Americans.

But over the past few years, a surge in tech/ecommerce employment has begun filling in the middle. As of 2019, tech/ecommerce companies employed 1.8 million American workers with some college, in occupations like computer support specialists and network and computer system administrators. (That figure is based on our tabulations of the March 2020 Annual Social and Economic Supplement to the Current Population Survey, covering 2019 earnings and employment).

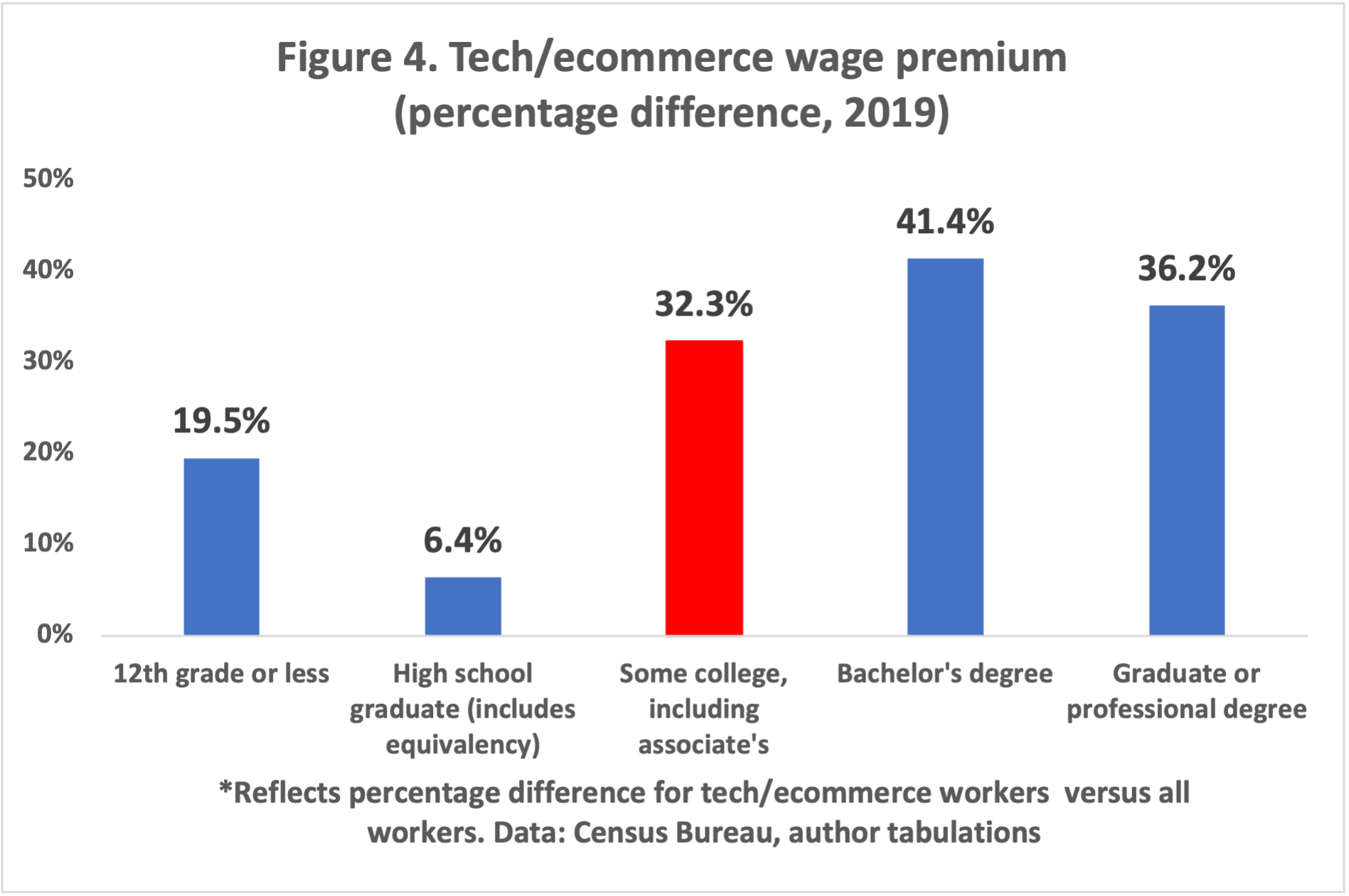

Moreover, tech/ecommerce workers with some college are paid more, on average, than workers with comparable education are getting elsewhere in the economy. The tech/ecommerce wage premium is 32% for workers with some college (Figure 4). Overall, tech/ecommerce workers with some college earned almost $60,000 in 2019.

Now, part of this tech/ecommerce premium is a composition effect. Tech/ecommerce workers skew more male than the overall population, and since men on average get paid more, that shows up as higher average wages. However, even when we take gender into account, the tech/ecommerce wage premium shrinks for workers with some college but does not disappear. Men with some college make 23% more in tech/ecommerce, on average, then comparable men with the same education. Women with some college make 20% more in the tech/ecommerce sector. That’s an important benefit of working in the tech/ecommerce sector.

For examples of the tech/ecommerce wage premium for workers with some college, a comparison to health care pay is instructive. Two-thirds of emergency medical technicians and paramedics have some college but no bachelor’s. Their median full-time weekly pay in 2019 was $912. Similarly, 60% of dental hygienists have some college but no bachelor’s, and their median full-time weekly pay was $1,094. By comparison, the median full time weekly pay for network and computer systems administrators, a tech occupation with a significant portion of workers with some college, was $1,447.

Geographically, the growth of tech/ecommerce jobs has been spread out around the country, much like manufacturing was. California is still at the top of the list with 291,000 new tech/ecommerce jobs created between 2016 and 2020, but other states with strong job creation include Florida, Ohio, Georgia, and Illinois (see table below, based on QCEW data for all education groups).

The problem of the missing middle did not spring up overnight, and it won’t disappear right away. But based on these trends, it may be time for young people to shift their aspirations away from healthcare occupations to the growing tech/ecommerce sector. That shift may alleviate some of the economic frustration and struggles that have become part of the political landscape.

Increase in tech/ecommerce jobs, 2016-2020, thousands

This week, the Innovation Frontier Project, a project of the Progressive Policy Institute (PPI), released a new report from Claudia Persico, an economist and leading environmental and health policy expert, on how exposure to pollution and lead negatively impacts the American workforce and economy.

“Lead and other environmental pollutants are not only causing a public health crisis, but they are hurting the productive capacity of the American people. Children who might otherwise have grown up to invent a new supercomputer or to cure a disease are having their brain function impaired at an early age by these pollutants,” said Caleb Watney, Director of Innovation Policy at PPI.

As outlined in this must-read new report, exposure to pollutants can cause cognitive impairments, behavioral issues, and lower test scores among children. Over a lifetime, these deficits in human capital accrue through lower educational attainment, wages, and productivity. The prevalence of pollution exposure is a significant obstacle to improving health, education, and economic growth in the United States.

Persico argues Congress, the White House, and state governments should use a variety of strategies to target pollution remediation for communities that disproportionately live and attend school near pollution sites, or live near high-risk sites, or live in older homes with pipes and paint that release lead into the air and drinking water. Persico suggests regulators act quickly to:

Raise Clean Air Act standards to close racial gaps in pollution exposure

Change zoning laws to keep children, schools, and daycares away from toxic sites

Accelerate cleanup of Superfund, Toxic Release Inventory, and other toxic sites.

Remediate homes with flaking lead paint to reduce blood lead levels in children

Increase lead screenings for children and use results to target homes for remediation

Use infrastructure spending to replace HVAC systems in schools and lead pipes in homes

Based in Washington, D.C. and housed in the Progressive Policy Institute, the Innovation Frontier Project explores the role of public policy in science, technology and innovation. The project is managed by Jack Karsten. Learn more by visiting innovationfrontier.org.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

As Congress makes progress on a bipartisan infrastructure deal, Democrats turn their attention to the sizable $3.5 trillion reconciliation package. The bill includes major pieces of President Biden’s Build Back Better platform and the American Families and Jobs Plans. Some moderate Democrats have voiced concerns about the size and scope of the package—foretelling of difficult negotiations ahead.

As lawmakers begin those discussions, however, we should not forget about a group that doesn’t get a seat at the table for policy debates: the United States’ more than 73 million children. The reconciliation package should prioritize investments in kids, not just to equalize our relatively low rates of spending on youth, but because doing so has huge shared benefits and among the highest rates of return for any social investment.

Senate Democrats have promised that both the $579 billion Bipartisan Infrastructure Framework and the $3.5 trillion budget blueprint they are advancing this week will be “fully paid for.” While there’s a case for borrowing to finance the most pro-growth infrastructure investments when interest rates are low, lawmakers’ commitment to fiscal discipline is reassuring at a time when the national debt is at record levels and inflation concerns are heating up. But signs are emerging that lawmakers will struggle to keep that promise as they flesh out the details. The upcoming budget resolution is an important opportunity to begin developing clearer financing plans and safeguards to uphold the agreements.

President Joe Biden initially proposed tax increases on corporations and wealthy households that would raise roughly $3.3 trillion in new revenue over the next 10 years to finance his American Jobs and Families Plans. That revenue would almost be enough to pay for the $3.5 trillion in new spending agreed to by Senate Democratic leadership last week, but several key lawmakers have already called for reducing the scope of those tax hikes.

Meanwhile, on the spending side, the budget agreement incorporates provisions — such as a costly Medicare expansion — that weren’t included in either the Jobs or Families Plan. Negotiators have said they will keep the bill’s sticker price under $3.5 trillion by setting the duration of some programs, including an expansion of the Child Tax Credit, to arbitrarily expire after a few years. But this move would be nothing more than a gimmick: The Committee for a Responsible Federal Budget estimates the package could cost up to $5.5 trillion over the coming decade if lawmakers allowed all the policies slated for inclusion in the budget blueprint to become permanent (as is clearly their ultimate intention).

Similar problems with fuzzy accounting plague the Bipartisan Infrastructure Framework. For example, negotiators have said they will pay for $70 billion of spending by cutting fraud from unemployment benefits even though the Congressional Budget Office estimates that overpayments over the next decade will be less than half that amount. The framework also counts offsets such as selling the strategic petroleum reserve, which may need to be bought back at a higher price, and sales of spectrum that have already occurred or would occur under current law. The situation worsened over the weekend when Republicans demanded that increased funding to help the IRS collect unpaid taxes — one of the few legitimate sources of real revenue included in the bipartisan deal — be dropped from the package. .

Some economists and politicians would argue that the policies in these packages don’t need to be paid for because they are public investments in the future. On the one hand, it makes sense to borrow from future generations to pay for investments they will benefit from, particularly when interest rates are low. But on the other, the federal government is currently on track to spend roughly $8 trillion more on programs that aren’t public investment than it will collect in taxes over the next decade, and some of the policies under discussion would further add to that category of spending. Interest rates are also likely to rise between now and when the money in these bills is actually spent. Even if lawmakers are content to borrow $4 trillion for public investment, they should pair it with $4 trillion of revenue to reduce the “consumption deficit” that no responsible leader can defend.

Deficit spending, even for worthwhile long-term investments, could also have negative short- and medium-term consequences if it occurs at a time when the economy is overheating. Much of the $2 trillion spent on the American Rescue Plan earlier this year was necessary to help our economy recover from the pandemic recession, but it has also likely contributed to higher-than-expected inflation. Although most economists believe these recent spikes are likely transitory, nobody can know for sure until later this year or early next. Lawmakers should therefore be wary of committing to a massive new spending bill in the near future before having a plausible plan for how to pay for it.

The Senate will soon vote on a budget resolution that includes instructions telling Congressional committees how much their policies can add to the deficit in a reconciliation bill (the legislative vehicle that will allow Democrats to pass their $3.5 trillion agreement without any Republican votes). Even though lawmakers could pass a reconciliation bill that increases the deficit by less than the amount allowed by the budget resolution, neither the American Rescue Plan nor the 2017 Trump tax cuts left anything on the table.

Therefore, if Congress is serious about paying for the upcoming spending bills, it should safeguard the agreement by passing a budget resolution that instructs the reconciliation process not to increase total budget deficits at all (there could still be some modest deficit-spending in a bipartisan infrastructure bill). Lawmakers must also eschew timing gimmicks that hide the true cost of the policies they are enacting and create uncertainty for working families who may plan their lives around new programs. A broader menu of revenue options, such as a carbon tax, inheritance tax, or progressive consumption tax, should be on the table to cover the costs of these policies. And if lawmakers cannot get consensus on a revenue package big enough to cover their spending ambitions, they should prioritize the most pro-growth public investments and cut what they are unwilling to pay for.

The $3.5 trillion budget blueprint unveiled earlier this week by Senate Democrats would fund many policies from President Joe Biden’s American Jobs and Families Plans not covered by the $579 billion Bipartisan Infrastructure Framework. But among many worthwhile public investments is a new proposal that should give lawmakers pause: a costly expansion of Medicare paid for entirely by young Americans. Although lawmakers should be open to thoughtful improvements to Medicare, any changes must be financed in a way that is fair to Americans of all ages.

There are two possible changes to Medicare that Sen. Bernie Sanders, I-Vt., the chairman of the Senate Budget Committee, wants to include in the next major spending bill. The first proposal is to offer vision, dental, and hearing services not currently covered by Medicare at no additional cost to beneficiaries. The second proposal is to give Americans ages 60-64 the option to enroll in Medicare with the same premiums and benefits currently available to those over age 65 (which are heavily subsidized by income and payroll taxes paid by younger workers).

The problem with these proposals is that Medicare is already struggling to pay for the current suite of benefits it offers. Medicare Part A, which offers hospital insurance that is supposed to be fully funded by payroll taxes, will face a 10% budget shortfall five years from now. The amount of general revenue needed to subsidize Medicare Parts B and D, which cover physician services and prescription drug benefits, is projected to nearly double as a percent of gross domestic product over the next 20 years. These costs will impose a significant burden on young Americans, either by crowding out investments in their future or requiring them to pay higher taxes than current retirees did when they were in the workforce.

Giving today’s seniors, who have collectively enjoyed greater gains in income and wealth than younger Americans, a suite of new benefits they didn’t finance over their working lives or in retirement would only compound the intergenerational inequity built into current policy. That’s especially true if the Senate blueprint foregoes some investments in clean energy or child welfare, such as a permanent expansion of the Child Tax Credit, to make room for this costly expansion of Medicare.

There are better alternatives. Americans ages 60-64 could be allowed to buy into Medicare at a premium that covers the full cost of their coverage rather than the heavily subsidized one currently paid by people aged 65 and over. This option would still be cheaper for most beneficiaries than private insurance because Medicare is able to negotiate lower prices for services than private insurers. Any new vision, dental, or hearing benefits should have a significant share of the cost covered by income-based premiums and co-pays, as is currently the case for Parts B and D. A broad-based consumption tax that is paid by all consumers regardless of age could also help finance benefits in a way that doesn’t place the burden on anyone generation. Lawmakers should also consider pairing or preceding any benefit expansion with measures to close the existing financial shortfall in Medicare, such as the bipartisan TRUST Act.

For too long, Washington has allowed the growth of retirement programs to crowd out critical public investments in infrastructure, education, and scientific research. The new budget agreement is a once-in-a-generation opportunity to right this intergenerational wrong. It would be shameful for lawmakers to choose affluent retirees over working families yet again. Any expansion of Medicare should require some contribution by those who would benefit, or it should be dropped from the budget agreement altogether.

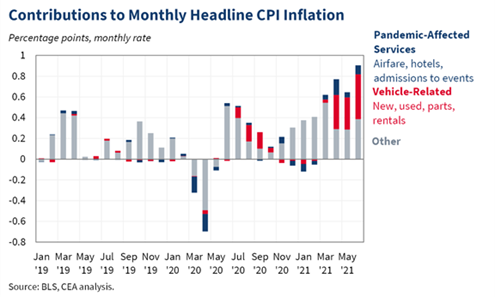

Today, the Labor Department released a new batch of inflation data for the year ending in June. The headline number for the consumer price index has sparked panic in some quarters, as year-over-year inflation is now at 5.4%, the highest annual rate since 2008.

While this backward-looking measure is currently above its recent historical average, there is little cause for concern based on market forecasts of future inflation. Medium-term inflation expectations remain well-anchored, as bond prices show an expected average rate of inflation of 2.2% between 5 and 10 years from today.

This is a very clear market signal that inflation pressures are transitory and will abate as supply chain issues caused by the pandemic work themselves out. Notably, motor vehicles represented 60% of the month-over-month inflation increase in June. As the global semiconductor shortage ebbs, we can expect motor vehicle inflation to return to its historical average.

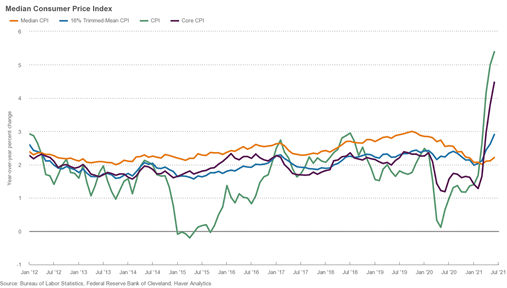

Another way to strip out the most volatile sectors of the economy and get a clearer picture of where inflation is heading is to look at median CPI, which includes only the middle changing item in the CPI’s basket of goods and services. In contrast to headline CPI, median CPI remains stable at 2.2% year-over-year. In the chart below you can see that CPI is more volatile than median CPI, and historically it has reverted toward median CPI after short deviations.

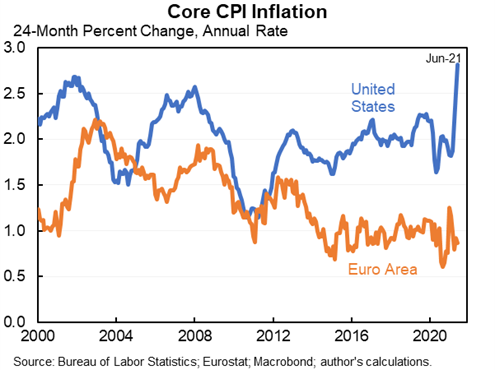

Lastly, year-over-year inflation numbers remain plagued by base effects, as the economy was depressed in June 2020 due to the poor handling of the pandemic by the Trump administration. Looking at two-year core inflation numbers shows that inflation is still within its historical range at 2.8%. This number is entirely consistent with the Federal Reserve’s average inflation targeting framework, which targets 2% average inflation over the business cycle with short periods of above average inflation making up for periods of below average inflation.

While there is not yet much reason to panic about long-run inflation, there are still things policymakers can do today to decrease the risk of inflation expectations becoming unmoored. For the first time in decades, we have sufficient demand in the economy to support rapid growth. Now we just need supply side investments and reforms to make sure that demand turns into real growth rather than increased inflation. Three items immediately spring to mind for policymakers to work on.

First, Congress should double down on its efforts to pass a bipartisan infrastructure package. While it may seem odd to spend more money to tamp down inflation, infrastructure spending is a special kind of spending. It’s an investment in the future productivity of our economy.

Second, the administration needs to follow through on many of the commitments it made last week in its executive order on promoting competition. Sectors like health care have been driving a disproportionate share of inflation in recent years. Encouraging more competition in that sector and others will have a disinflationary effect. Similarly, policymakers should avoid an unforced error by inadvertently harming sectors like tech and e-commerce, which have been holding down inflation in recent years.

Third, the Biden administration should begin to roll back tariffs implemented during the Trump presidency. These are taxes ultimately borne by American consumers and they raise the input costs for American manufacturers, making them less competitive in global markets.

The Mosaic Economic Project application process is now open for the September 2021 Women Changing Policy workshop, scheduled for September 13-15, 2021.

“The Women Changing Policy workshop is an opportunity for diverse women with expertise in economics and technology to hone the skills needed to communicate their work and ideas to policy makers and the media,” said Crystal Swann, Mosaic Economic Project Lead and PPI Senior Fellow. “Through our interactive format, participants get hands-on experience learning the ins and outs of Washington politics and on how to become a go-to policy expert. And it’s a chance to expand their networks.”

This is the third Women Changing Policy workshop. Previous workshops have included candid conversations with influencers in public policy, including leaders and representatives from the United States Congress, the media, and other experts from the policymaking ecosystem.

We encourage women with expertise in economics, finance, technology, telecom and corporate governance to apply. Applicants should be well established in their careers – be it at a corporation, academic institution or NGO–and looking for opportunities to grow their influence on critical issues, from the wealth gap to infrastructure to health care. The Mosaic Economic Project aims to bring new voices to the policy arena. To that end, we value diversity in applicants. This workshop will be held virtually, and the deadline to apply is August 31, 2021.

The Mosaic Economic Project is a network of diverse women in fields of economics and technology. Mosaic programming provides coaching on presenting skills and focuses on connecting and advocating for cohort participants’ to engage in public policy debates, with a particular focus on engaging Congress and the media.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

For the firms that adopt them, artificial intelligence (AI) systems can offer revolutionary new products, increase productivity, raise wages, and expand consumer convenience.[1] But there are open questions about how well the ecosystem of small and medium-sized enterprises (SMEs) across the United States is prepared to adopt these new technologies. While AI systems offer some hope of narrowing the recent productivity gap between small and large firms, that can only happen if the technologies actually diffuse throughout the economy.

While some large firms in the U.S. are on the cutting edge of global AI adoption, the challenge for policymakers now is to help these technologies diffuse across the rest of the economy. To realize the full productivity potential of the U.S., AI tools need to be available to 89% of U.S. firms that have fewer than 20 employees and the 98% that have fewer than 100.[2] An AI-enabled productivity boost would be particularly timely as SMEs are recovering from the effects of the ongoing COVID-19 crisis.

The report discusses the promise for AI systems to increase productivity among U.S. SMEs, the current barriers to AI uptake, and policy tools that may be useful in managing the risks of AI while maximizing the benefits. In short: there is a wide range of policy levers that the U.S. can use to proactively provide the underlying digital and data infrastructure that will make it easier for SMEs to take the leap in adopting AI tools. Much of this infrastructure operates as a type of public good that will likely be underprovided by the market without public support.

Benefits of AI adoption:

The central case for AI adoption is that human cognition is limited in a variety of ways, most notably in time and processing power. Software tools can improve decision-making by increasing the speed and consistency with which decisions can be made, while also allowing more decisions to be planned out ahead of time in the event of various contingencies. Under this broad framework, we can think about “AI” as being a broad suite of technologies that are designed to automate or augment aspects of human decision-making.

While many of AI’s most eye-catching use cases will likely remain the preserve of large platforms, the technology also holds tremendous promise for SMEs. The adoption of third-party AI systems will notably enable SMEs to streamline mundane (but often costly) tasks such as marketing, customer relationship management, pre- and post-sales discussions with consumers, and Search Engine Optimization (SEO). These systems can provide a lifeline for SMEs who are overwhelmed by the many challenges of running a business, and they can expand the number of businesses that are eligible for certain financial supports. For example, AI tools can be used to improve the accuracy of credit risk underwriting models and using alternative data sources and a streamlined process, they can make it easier for SMEs to take out loans they otherwise might not qualify for under traditional methods. Along similar lines, research shows that AI-driven robotics have (and will continue) to boost the productivity of SMEs in the manufacturing industry.

Importantly, this upcoming wave of AI technology can help SMEs catch up with larger, international firms because it can democratize the benefits of large information technology (IT) investments that superstar firms have been seeing over the last decade.

The economist James Bessen has argued that the top 5% of firms in many industries have been increasingly pulling away from the rest of the field because they’ve made large investments in proprietary IT systems. Their smaller rivals struggle to develop their own systems because they lack the necessary scale to hire a large stable of in-house technical talent. Amazon, for example, has a team of 10,000 employees working to improve their Alexa and Echo systems.

While AI tools can’t fully reverse this trend, they can help shrink the gap when embedded into Software as a Service (SaaS) platforms that smaller firms can make use of without the same level of investment. Essentially, through general-purpose AI tools, SMEs can have access to a host of productivity enhancements that these proprietary IT systems offer, but at a price point that is economical for SMEs. By shrinking this productivity gap, smaller firms can begin to compete in earnest while differentiating from large firms through improved customer service and greater product diversity. This will give a large leg up to SMEs who adopt these AI systems and help them better compete with large global incumbent firms.

Consider a firm like Keelvar Systems, which uses advanced sourcing automation to help businesses rapidly shift supply chains around the globe in the event of disruptions or delays. Essentially, it replaces or augments the work that a large supply chain and sourcing office would do within a firm. By using their service, or others like it, SMEs have the ability to benefit from similar levels of sophistication in their supply chain management without having employees spend hundreds of hours on tedious tasks or maintaining expensive proprietary IT systems.

There are firms like Legal Robot that have created a series of tools to help small businesses access legal services that would otherwise require a small army of in-house lawyers. With their service, SMEs can use smart contract templates based on their industry, receive instant contract analysis to make sure they are receiving fair terms and can automate certain aspects of compliance with laws like the GDPR.

Likewise, companies like Bold360 have helped SMEs improve their customer service experiences by offering a variety of AI-powered-chatbots and tools. Many basic customer concerns about products or delivery can be handled by these basic chatbots, freeing up human customer representatives to focus their time on the hard or advanced cases. Again, the pattern here is there is a service that large, multinational companies have been investing billions of dollars to create proprietary versions of, and now the customizability of AI is helping this service become more accessible to SMEs.

What are the barriers to AI adoption for SMEs in the U.S. and what can policymakers do to help create a welcoming environment?

Data investment as a public good

Depending on the context, data can often have the same traits as other public goods. First, it is non-rival—the marginal cost of producing a new copy of a piece of data is zero. Stated differently, multiple individuals can use the same dataset at almost no additional cost. The second important trait is that data is hard to exclude. Consider this report. Once it has been posted online, it is difficult to prevent people from accessing and sharing it as they see fit. This is one of the reasons why copyright infringement is so hard to stamp out.

Oversimplifying, these two features can lead to two opposite problems. On the one hand, economic agents might underinvest in public goods, absent government-created appropriability mechanisms (such as patent and copyright protection). Conversely, public goods tend to be underutilized (at least from a static point of view). Any price that enables economic agents to recoup their investments in a public good will be above the good’s “socially optimal” marginal cost of zero. Public good policies thus involve a tradeoff between incentives to create and incentives to disseminate. For example, patents give inventors the exclusive right to make, use and sell their invention; but inventors must disclose their inventions, and these fall into the public domain after twenty years.

What does this mean for data and artificial intelligence? If policymakers think that data is an essential input for cutting-edge AI, then they should question whether obstacles currently prevent firms from investing in data generation or disseminating their data.

While policies in this space involve significant tradeoffs, some offer much higher returns to social welfare. For instance, to the extent policymakers believe existing datasets are being underutilized, purchasing private entities’ data (through voluntary exchanges) and placing it in public data trusts would be a better policy than imposing data sharing obligations (which could undermine firms incentive to produce data in the first place). This is akin to the idea of government patent buyouts.

Of particular interest for policymakers, however, is the fact that some SMEs are sitting on top of data flows that are not being fully utilized because it is expensive to make data usable and these datasets may not be very valuable in isolation. As an example, industry-level manufacturing data might be quite valuable to all firms in a sector, but the dataflows from one SME are much less valuable. The U.S. could align incentives by providing investment funds to quantify various aspects of business flows and then submit them to public data trusts, which could be accessible for use by all firms in the industry. This would essentially be treating valuable dataflows as a type of public infrastructure that needs government investment to be fully realized.

This kind of public investment can happen not only through incentives for private firms but through the public sector as well. Governments at all levels (state, local, and national) have valuable dataflows regarding infrastructure development, the organization of public transportation, and general macro-level economic data that can be turned into open datasets for public and commercial use. Particularly on the national level, the U.S. should consider investment in IT infrastructure that can coordinate the submission of open datasets on the state and local level.

Indeed, if key scientific or commercial datasets do not yet exist, the public sector may be best positioned to create them in the first place as a type of digital infrastructure provision. One notable structure that may help in this regard is the idea of a Focused Research Organization, which would provide a team of researchers with an ambitious budget and a nimble organizational structure with the specific goal of creating new public datasets or toolkits over a set time period.

Provide regulatory certainty

For SMEs deciding whether to invest in adopting AI tools, regulatory and compliance costs can be a significant deterrent. Policymakers should recognize that regulation is often more burdensome for small firms that generally have less ability to shoulder compliance costs. Especially in industries with low marginal costs, such as the tech sector, larger firms can spread fixed compliance costs across more consumers, giving them a competitive edge over smaller rivals. Regulation can thus act as a powerful barrier to entry. For instance, a study found that the European experiment with GDPR led to a 17% increase in industry concentration among technology vendors that provide support services to websites.

This is not to say that additional regulation is, or is not, necessary in the first place. Indeed, there are a host of malicious or unintentional harms that can occur from improperly calibrated AI systems. Regulation can be a powerful tool to prevent these harms and, when well-balanced, can promote greater trust in the overall ecosystem. But potential regulation should follow sound policymaking principles that reduce the regulatory burden imposed on firms, notably by making regulation easy to understand, risk based, and low-cost to comply with.

In the U.S. there is to date no overriding national AI regulation. Instead, each sectoral regulator (i.e. Federal Aviation Administration, Security and Exchange Commission, Federal Trade Commission, etc.) has been steadily increasing their oversight over the use of algorithms and software in their specific area. This is likely an appropriate approach, as the kinds of risks and tradeoffs at play are going to be very different in healthcare or financial decision-making when compared to consumer applications. As this approach develops, it would be prudent to develop a risk-based framework that allows for more scrutiny of algorithmic decision-making in sensitive areas while giving SMEs confidence to invest in low-risk areas with the knowledge they will not later take on large compliance costs.

However, regulation over data protection has been far more segmented and piecemeal. And the state-by-state patchwork of rules that has developed can be a significant deterrent for SMEs when considering whether to invest in the use of certain AI tools. Policymakers should consider an overriding national privacy law that would be able to set standard rules of the road over the protection of data in all 50 states so that U.S. SMEs can invest with confidence.

Finally, U.S. policymakers should consider aggregating all this information through the creation of a dedicated AI regulatory website that provides a toolkit of resources for SMEs about the benefits of AI adoption for their business, the potential obligations and roadblocks that they need to be aware of, and best practices for cybersecurity hygiene and data sharing.

Expand the AI talent pool

A lack of skilled talent is one of the biggest barriers to AI adoption as the technical skills required to build or adapt AI models are in short supply. In the U.S., especially, smaller companies struggle to compete with the high salaries paid out by large tech firms for top-end machine learning engineers and data scientists.

In broad strokes, this skills shortage can be alleviated in two ways: through upskilling the domestic population and by improving immigration pathways for global talent.

To upskill the domestic population, one relatively simple lever would be to pay some portion of the costs of individuals and businesses who wish to upskill. In the U.S., a portion of a worker’s retraining costs may be written off as a business expense so long as the worker is having their productivity improved in a role they currently occupy. But this expense is not tax deductible if the proposed training would enable them to take on a new role or trade.

For example, if a small manufacturing firm has technically competent IT staff who wish to attend a specialized training course on using machine vision systems in a warehouse environment, this expense would not currently be deductible as it would enable them to take on a new role within the company. This inadvertently creates an incentive to spend more on capital productivity investments than labor productivity investments. Addressing this imbalance would incentivize more firms to invest in worker retraining and help speed the creation of an AI workforce in the U.S.

Secondly, the U.S. needs to urgently address the shortcomings in the U.S. immigration system which make it more difficult for startups to compete with large incumbents on the basis of talent. Approximately 79% of the graduate students in computer science (and related subfields) studying in the U.S. are international students, which means a large majority of potential AI workers U.S. firms may look to recruit must operate through the immigration system. The cost, complexity, and length of this process inevitably favors large, incumbent firms who can afford to navigate the regulatory maze of procuring an H-1B or related work visa.

A recent NBER paper showed in detail the myriad ways in which access to international talent is important for startup success. Utilizing the random nature of the H-1B lottery system, the paper compared startups that randomly received a higher percentage of their visa applications approved to those who did not. The random nature of the H-1B lottery makes an ideal policy experiment because it allows for a clean test in which other potentially confounding variables are controlled for. The study found that a one standard deviation increase in the likelihood of successfully sponsoring an H-1B visa correlated with a 10% increase in the likelihood of receiving external funding, a 20% increase in the likelihood of a successful exit, a 23% increase in successful Initial Public Offering, and a 4.8% increase in the number of patents filed by the startup.

Policymakers could begin to counter this effect by waiving immigration fees for firms of a certain size and by streamlining the application process.

Further, policymakers should look to create a statutory startup visa so that international entrepreneurs have a viable pathway into the U.S. to launch firms of their own. According to research by Michael Roacha and John Skrentny, international STEM PhD students are just as likely to report wanting to work for or launch their own firm as native-born students, but the difficulty of our immigration system pushes them towards working at large incumbent firms.

Using these two levers of upskilling and immigration reform, the U.S. should increase the supply of AI talent available to SMEs or to launch SMEs themselves and thereby spur the adoption of AI adoption.

Conclusion

Artificial intelligence systems hold great potential to streamline the costs of doing business in a modern economy, particularly for SMEs. The last 20 years of the information technology revolution have helped large, established firms reach the cutting edge of productivity while smaller firms have been left behind. But general-purpose AI tools now provide an opportunity for SMEs to take advantage of many of these IT advancements at a cost and a scale that is feasible for them. Policymakers should attempt to proactively build out the digital infrastructure that will make it easier for SMEs to take the leap in adapting AI tools.

Summary of policy recommendations:

Data investment as a public good:

Where appropriate, align incentives for the private sector to contribute industry-level SME data to public and private data trusts that could be used by everyone.

Invest in making more government datasets open to the public.

Fund Focused Research Organizations or similar groups with the explicit goal of creating new scientific and commercial public datasets.

Provide regulatory certainty:

Clarify existing regulations and the obligations that SMEs must meet when utilizing a new AI tool.

Encourage the development of a risk-based framework that allows for more stringent regulation of sensitive applications while giving certainty to SMEs on investment in low-risk applications.

Pass an overriding national privacy law so that SMEs aren’t deterred from investing by a patchwork of differing state-by-state laws.

Consider the creation of a new SME regulatory website that provides informational resources to SMEs about the benefits of AI adoption for their business and the potential roadblocks that they need to be aware of.

Expand the AI talent pool

Encourage upskilling of the U.S. population by making worker retraining deductible as a business expense.

Reevaluate U.S. immigration pathways to make them more attractive for international technical talent.

Streamline the immigration application process and waive fees for firms below a certain size to make it easier for SMEs to compete for technical talent.

[1] This report is an adaptation of an earlier paper coauthored with Dirk Auer titled “Encouraging AI Adoption in the EU”.

[2] Annual Survey of Entrepreneurs – Characteristics of Businesses: 2016 Tables, United States Census Bureau

President Biden’s American Jobs Plan proposed to spend $300 billion on rebuilding America’s manufacturing sector. The funds would be distributed through a variety of channels, including $50 billion in semiconductor manufacturing and research, $50 billion for a new office to fund investments to support production of critical goods. Biden also called for the creation of a “new financing program to support debt and equity investments for manufacturing to strengthen the resilience of America’s supply chains.”

The US Innovation and Competition Act of 2021, which passed the Senate in early June, also highlights pro-manufacturing polices. These include funding for semiconductor manufacturing and research, money for regional technology hubs, and the creation of the position of Chief Manufacturing Officer in the White House to coordinate the nation’s manufacturing policies.

We believe that these plans are a big step in the right direction, and applaud the President’s and the Senate’s focus on manufacturing. But the nation’s policy framework for manufacturing needs more explicit emphasis on digitization of physical production, which is the only way that American manufacturers can compete over the long run and create new jobs. In addition, the 2017 Tax Cuts and Jobs Act (TCJA) introduced an odd quirk into the business tax code that will make it more expensive for some manufacturers to borrow. That quirk needs to be fixed.

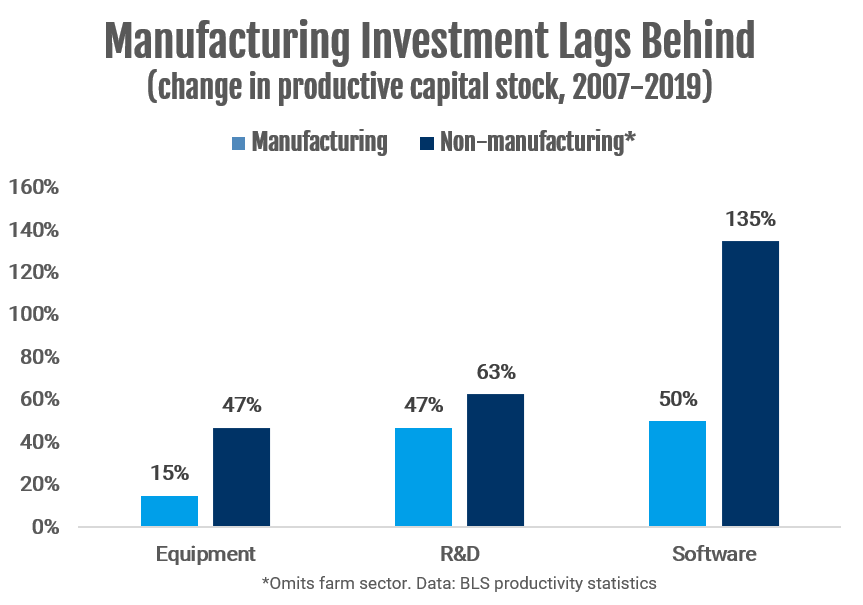

First, we review the facts about manufacturing investment. Government figures show that domestic investment by manufacturers has been lagging the rest of the economy by a substantial margin. During the last business cycle—which started in 2007 and ended in 2019—the productive stock of equipment rose by 15% in the manufacturing sector, far less than the 47% increase in the rest of the non-farm business sector (see chart below). (Equipment includes everything from industrial machinery to trucks to computers and communications gear bought by manufacturers).

This weakness in factory investment undermines the usual argument that manufacturing workers have been mainly displaced by automation. Certainly automation has been progressing, but if capital investment in robots and the like were the main cause of job loss, the investment surge in equipment would have been much bigger. The White House 100-day supply chain review points out that “many SME manufacturers are underinvesting in new technology to increase their productivity.” Contrast this with the warehousing industry (including fulfillment centers) where the productive stock of equipment rose by 91% from 2007 to 2019, even as employment soared.

Moreover, manufacturers have been lagging in software and R&D investment as well. The productive stock of software in the manufacturing sector rose by 50 percent from 2007 to 2019, compared to a 135 percent increase in the non-manufacturing sector. The productive stock of research and development rose by 47 percent in the manufacturing sector, compared to a 63 percent increase in the non-manufacturing sector.

The investment picture gets even worse when we look at specific industries within manufacturing. Consider the computer and electronics products industry, which includes semiconductor manufacturing. The productive stock of equipment in this industry did not grow at all from 2007 to 2019, and similarly for the stock of software. In other words, the computer and electronics product industry, including semiconductors, had no net investment in equipment and software over this 12-year stretch. This may help explain why government action to boost semiconductor manufacturing investment is necessary now.

Similarly, capital investment in the motor vehicle industry has been lagging. The 22 percent increase in the productive stock of equipment (including robots) is above the norm for manufacturing, but well behind the average for the nonmanufacturing sector. And investment in motor vehicle R&D, while still strong in absolute terms, has barely kept up with the industry’s need to shift to electric vehicles. Once again, the investment data helps us identify manufacturing sectors that need help in competing with China.

We note that the manufacturing sector is responsible for the entire slowdown in equipment investment compared to the 1990s. That shows how important it is that the U.S. address the issue of weakness in investment in manufacturing.

So what can we do? Biden’s manufacturing plan and the Competition and Innovation Act passed by the Senate are both heading in the right direction, but they could be improved with an overarching vision. As PPI has noted in several reports, we need the American manufacturing industry to invest in digitization—not just robots on the factory floor, but manufacturing platforms that make it easier for American startups to join global supply chains. The Biden Administration should think in terms of an Internet of Goods, where manufacturers plug into a network of companies that are linked digitally. The Biden manufacturing initiative should build on existing platforms such as Xometry and Fictiv to connect smaller suppliers.

The other big issue is funding. Manufacturing requires large capital investments, so borrowing costs are always a consideration. Unfortunately, in an example of the law of unforeseen consequences, key provisions of the 2017 TCJA are about to make it much more expensive for manufacturers and other capital-heavy businesses to fund their investments, even before any potential increase in the corporate income tax rate.

First, the TCJA permitted full expensing for investments in short-lived assets such as machinery and equipment. However, the “bonus depreciation” will begin phasing out in 2023 and will be eliminated by 2027. That will make it more expensive for manufacturing investment.

Second, the TCJA reduced the amount of interest expenses that most businesses could deduct from 50 percent to 30 percent of a business’s “earnings before interest, taxes, depreciation, and amortization” (EBITDA). Because of the pandemic, the CARES Act temporarily relaxed this restriction for 2020, but it comes back into effect for 2021.

Third, as of 2022, the TCJA further reduces the tax deductibility of interest to 30 percent of business “earnings before interest and tax” (EBIT). The difference between EBIT and EIBTDA is depreciation and amortization, which can be enormous for asset-heavy manufacturers. This 2022 shift, as embodied in current law, will have the effect of reducing the amount of interest that a manufacturer or other investment-heavy company can deduct.

To understand the magnitude of this change, consider American Axle & Manufacturing, a leading automotive supplier that did $4.7 billion in sales in 2020. The company’s EBITDA was $720 million, and depreciation and amortization was $522 million. That means EBIT was only $188 million (Note: These numbers are all drawn from the company’s public 10K, with no contact with the company).

In 2020 American Axle paid $212 million in interest. Under the TCJA rules that apply to 2021, it would all be deductible, since $212 million is less than 30 percent of $720 million. Under the TCJA rules that apply to 2022 and after, assuming that all numbers remain the same, only $56 million of the interest payment will be deductible. Future borrowing will take the same hit.

When the TCJA was passed, the increased restrictions on the deductibility of interest seemed appealing to many policymakers for several reasons. First, it reduced the bias in the tax code toward debt financing. Second, it discouraged excess borrowing by companies. Third, it raised money and helped balance out the cost of cutting corporate income tax rates.

However, the increased restrictions are likely to disproportionately affect manufacturers, who as a whole paid $96 billion and $90 billion in interest in 2018 and 2019 respectively, more than any other sector of the economy except real estate (who could opt out of the new requirements). The impact of this provision on companies like American Axle will be even greater if interest rates rise, as seems likely.

Given the acknowledged importance of manufacturing, it might make sense for lawmakers to consider extending the provision of the CARES Act that relaxes the limitations on interest expense deductions to avoid imposing another financial burden on the U.S. manufacturing sector. This would also cover the coming shift to EBIT. Such a move might be especially appropriate if the current provisions of the tax law that phase out bonus depreciation stay in effect. If we care about domestic factory investment, it seems like a mistake to make it more expensive for manufacturers to borrow even while the depreciation rules become more restrictive.