It’s become conventional wisdom that corporate America has fallen victim to myopia and short-termism. Companies are spending billions buying back stock that could have gone to innovation and investment. Corporate executives have compensation packages tied to stock prices, which focuses their attention on quarterly earnings rather than long-term growth. Investors want immediate results, rather than building for the future. Whatever the merits of the short-termism thesis, America’s weakness in capital spending is all too real. The Progressive Policy Institute first noted the “business investment drought” in 2010 and 2011.

Indeed, we started our “Investment Heroes” annual ranking in 2012 precisely to highlight those companies that were investing heavily in the United States. Jason Furman, head of President Obama’s Council of Economic Advisors, gave the keynote talk at a 2015 PPI conference on “Reviving Private Investment” and highlighted how the private investment drought undercuts U.S. productivity growth and, therefore, income gains.

This report continues the annual Investment Heroes ranking again this year by identifying those U.S. companies resisting short-termism and making long-term domestic investments in buildings, equipment, and software.5 We call these companies “Investment Heroes” because their capital spending is helping raise productivity and wages across the country. Further, we use our “Investment Heroes” analysis to help understand the potential causes of the current short-term mentality and discuss some policy options for reversing it.

I’d like to draw your attention to this extraordinary essay by President Obama in The Economist. It stands out for two reasons. First, it provides what has been sorely missing from the bizarre 2016 presidential race – a progressive roadmap for restoring America’s economic dynamism.

Both documents reject populist claims that the U.S. economy is a “disaster” or a game hopelessly rigged by Wall Street or billionaires and focus instead on the main driver of meager wage gains and growing inequality – slumping productivity growth. As the President notes, one reason for the slowdown is lagging private investment – a problem PPI also has been highlighting in multiple studies of the nation’s “investment drought.”

We also agree with many of the President’s key prescriptions for putting America back on a high-growth path. To highlight just a few:

Pro-growth tax reform, including lowering business taxes and closing special interest loopholes.

Expanding U.S. exports and passing the Trans-Pacific Partnership to strengthen global trade rules.

Lowering college costs, not just expanding education subsidies.

Making work pay by expanding tax credits for low-income workers.

Why is all this important? Because despite all the rhetoric about “inclusive growth,” in this election, we’re hearing a lot more about distributing existing wealth than creating new wealth. To speak to the hopes and aspirations of working families, Democrats need to balance that equation.

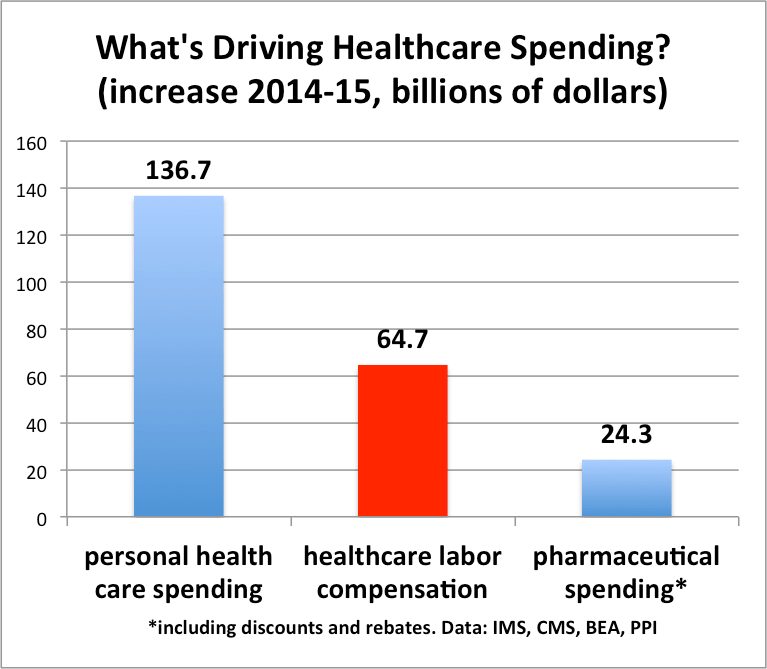

According to PPI estimates, rising labor costs accounted for almost $65 billion in added health care costs in 2015, or 47 percent of the total increase in personal health care spending (as reported by the latest projections from the actuaries at the Centers for Medicare and Medicaid). By contrast, IMS reports that net spending on prescription drugs rose by only $24 billion in 2015, or 18 percent of the rise in personal health care spending.

This result, which updates our previously published data for 2014, fights the prevailing narrative that healthcare spending is primarily driven by rising drug prices.. Instead, the big increase in labor compensation in 2015 is mainly being impelled by the rapid growth of health care employment. The number of workers in the nation’s hospitals, physician offices, and nursing homes increased by 429,000 in 2015, compared to an annual average of 226,000 for the previous 5 years.

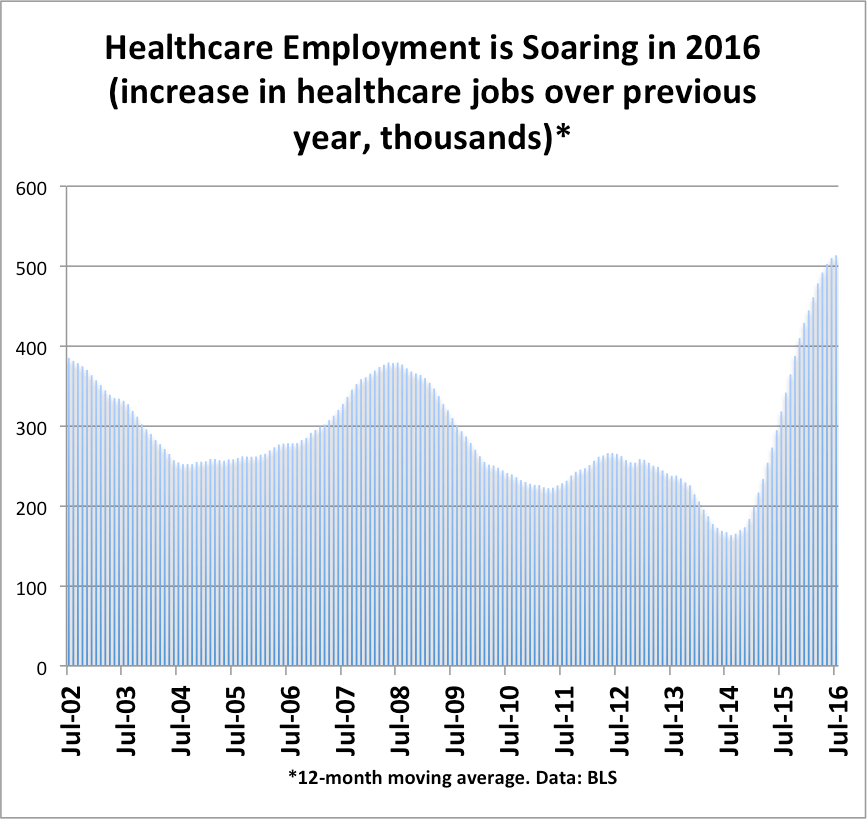

Unfortunately, this trend of rapidly rising healthcare employment driving overall spending appears to have accelerated in 2016. Healthcare employment in the 12 months ending July 2016 was more than 500,000 above its year earlier level, suggesting that healthcare labor costs will surge even more in 2016.

Meanwhile data from the BEA seem to show the pace of pharmaceutical spending slowing in 2016. Consumer spending on prescription drugs in August 2016 was 4.3% over a year earlier, less than half as fast as in 2015. There’s no guarantee that this slower pace will continue for the rest of 2016, but so far it’s a good sign.

The FCC chose to ‘delete‘ (their word) discussion of its “set-top box rule” from today’s meeting. As we wrote two weeks ago, the FCC’s proposed rule appeared to put the commission in the position of rewriting copyright law and setting up a licensing board for apps. The licensing board for apps is particularly disturbing, because it represents an entirely new layer of regulation on an innovative sector that has produced more than 1.6 million jobs in the US alone.

But we’re left with a headscratcher. The truth is that no one–including members of Congress–really knows at this point what Chairman Tom Wheeler and the FCC commission are thinking, or how the FCC has modified its plan. Rather than having to guess, we favor transparency–the FCC should announce its current proposal, and give an opportunity for public comment, meaningful review by Congress, and real economic analysis of the rule’s impact on jobs and innovation. That’s the right way to move forward.

When Americans think of trade, we tend to focus on large, world-leading multinationals. We usually don’t think of a small food exporter like Pacific Valley Foods, which started in a couple’s home office, or of The Pro’s Closet, an online global reseller of used biking gear founded by a pro cyclist. But, like these businesses, 98 percent of U.S. exporters are actually small and medium-sized enterprises (SMEs), and these smaller traders account for over one-third of U.S. exports.

SMEs that export are also economic powerhouses—they hire more employees, pay higher wages, and are more resilient and productive than their non-exporting counterparts. And, since only about five percent of American SMEs currently export, the United States has significant untapped potential to drive growth and support good jobs by increasing small business trade.

In a previous issue brief, we explained how the Trans-Pacific Partnership agreement (TPP) would boost U.S. small business exports by clearing away significant foreign trade barriers and by mandating reforms that would make exporting fairer, faster, cheaper, and more certain for America’s smaller firms.

Does the Federal Communications Commission (FCC) have the authority to rewrite copyright law and license apps? This Thursday the Senate Commerce Committee will hold an oversight hearing for the FCC, giving the committee members the opportunity to ask FCC Chairman Tom Wheeler this very relevant question.

Wheeler has proposed a plan by which payTV operators will be required to offer their shows through an app, which can be used on any device. The goal of this plan is to wean consumers off set-top boxes and home television sets, and encourage them to watch their favorite shows on their phones or tablets.

In the process, however, Wheeler is also mandating that the copyright holders for movies and television shows can no longer control where their material appears. That dramatically changes established copyright law, which gives copyright holders effectively unlimited discretion over how and where to sell and distribute their content.

Moreover, the FCC would set up a licensing board to certify the apps, setting an unfortunate precedent where any app that provided video content could presumably come under government control about how and where it could provide that content (or else it would be easy to circumvent the FCC’s rules). In effect, the FCC is setting itself up as the gatekeeper of the App Economy, which has been a tremendous job producer so far for the United States.

Do they promote the creation of new artistic works?

Do they allow creators and authors to benefit from their artistic endeavors?

Do they stimulate jobs and economic growth?

There is no evidence that the FCC did any economic analysis of these copyright metrics to justify its proposal. Moreover, app licensing by the government could dramatically slow down the rate of innovation in apps

PPI is in favor of competition in the set-top box market, including the delivery of content through apps. But the FCC’s attempt to squeeze out set-top boxes by rewriting copyright rules and licensing apps has the potential to have wide-reaching negative economic consequences.

The introduction of the iPhone in 2007 created a profound new economic force. There are now nearly 2 billion smartphone users worldwide, an unprecedented rate of adoption for a new technology. Equally important, Apple’s unveiling of the App Store in July 2008 ignited a global App Economy boom. This revolutionary concept enabled software developers to write mobile applications from anywhere in the world, with the ability to sell and distribute them globally.

Anti-trade populists are hell-bent on locking Democrats into a future of rigid opposition to trade deals like the Trans-Pacific Partnership. They recently failed in efforts to include a plank in the Democratic Party Platform that would have committed Democrats to the decidedly undemocratic principle of never, ever agreeing even to bring TPP to a vote—either in this Congress or any future one. Now, they are back, pressuring Democratic candidates and Members to go on record against TPP—a key priority for President Obama—and any vote on TPP in the lame duck session of Congress.

Pro-growth progressives should stand up and fight this ill-conceived attempt to make dogmatic opposition to trade agreements a new political loyalty test. The last thing America needs is a Democratic version of the Republicans’ infamous Norquist Pledge on taxes, which has paralyzed Washington’s ability to compromise and make sound fiscal policy.

Killing TPP would deprive policy makers of a potent tool for stimulating jobs and growth, and for augmenting American influence and leadership in the Pacific East. Make no mistake: blanket hostility to trade agreements is a formula for slow growth, lagging innovation and a fatal loss of U.S. economic dynamism.

All around the world we are seeing the rise of the App Economy—jobs, companies, and economic growth created by the production and distribution of mobile applications (“apps”) that run on smartphones. Since the introduction of the iPhone in 2007, the App Economy has grown from nothing to a powerful economic force that rivals existing industries.

In this paper, we examine the production and distribution of mobile apps as a source of growth and job creation for Mexico. We find that Mexico had over 225,000 App Economy jobs as of March 2016. What’s more, Mexico’s connectivity with the global economy, particularly the United States, gives the country the potential to add many more App Economy jobs in the near future.

Mexico has long benefited from strong relationships with its global trading partners and has been an enthusiastic supporter of the proposed Trans-Pacific Partnership agreement. An important next step for Mexico is to seize the opportunities provided by the new economy, realizing its potential for creating new export markets. Trade is now much more than just traditional goods and services—it is also digital goods, such as mobile apps.

Mexico is also benefiting from a relatively stable economy in a time of volatility in the region. Mexico has managed to register slow but steady growth rates over the past few years. For 2015, Mexico showed annual growth of 2.5 percent, while the overall Latin American economy contracted by 0.3 percent. As the global economy stabilizes and Mexico continues its steady growth amongst a region plagued with uncertainty, the country can further strength its position as an economic leader in Latin America.

As we’ve repeatedly said, innovation creates jobs, not destroys them. But we’ve also recently pointed out that government has been lagging private sector spending on R&D, and that’s one reason why productivity growth and job creation has been weak. Moreover, PPI’s Will Marshall recently wrote that the Democrats have to resolve their economic identity crisis.

So it was good news when in today’s speech in Michigan, Hillary Clinton said:

And we’re going to … recommit to scientific research that can create entire new industries.

She’s been getting increasingly powerful on this point. On her website, her “Jobs Plan for Millennials” contains the paragraph (our bold):

Support scientific research and technological innovation. We must ensure that America remains at the forefront of scientific and technological innovation in the 21st century. We will make bold new investments in scientific research, which will create entirely new industries and the good-paying jobs of the future. Together, we can achieve bold research goals, like preventing, effectively treating, and making an Alzheimer’s cure possible by 2025. And we will pursue public policies that spur technological innovation and support young entrepreneurs. Hillary believes that by supporting young entrepreneurs in all types of communities, we can catalyze innovation hubs across the country, encourage millennial talent and capital to invest in their communities, and build thriving local economies.

By contrast, a Google search of Trump’s website shows no appearances of the term “scientific research.” The outline of Trump’s economic vision on his website does not contain the words ‘technology’ or ‘innovation’. We wonder if Trump understands that his favorite outlet, Twitter, was only invented in 2006.

Donald Trump’s travesty of a presidential campaign is forcing Republicans to ask themselves some hard questions: Does party loyalty outweigh the risks of putting a self-infatuated political ignoramus in the White House? Do they hate Hillary Clinton more than they love their country?

No doubt Democrats are enjoying the GOP’s agonizing moment of truth, but their party also faces a big strategic choice. Will Democrats wage the fall campaign as pro-growth progressives or as angry populists?

PPI was among the first organizations to highlight the business investment drought, starting in 2010 and 2011, way before it became commonly accepted (see here and here). And our “Investment Heroes” annual ranking was started in 2012 precisely to contrast the companies that were investing heavily in the United States with the many others that chose to pare back. So the issue of short-term business thinking is no stranger to us.

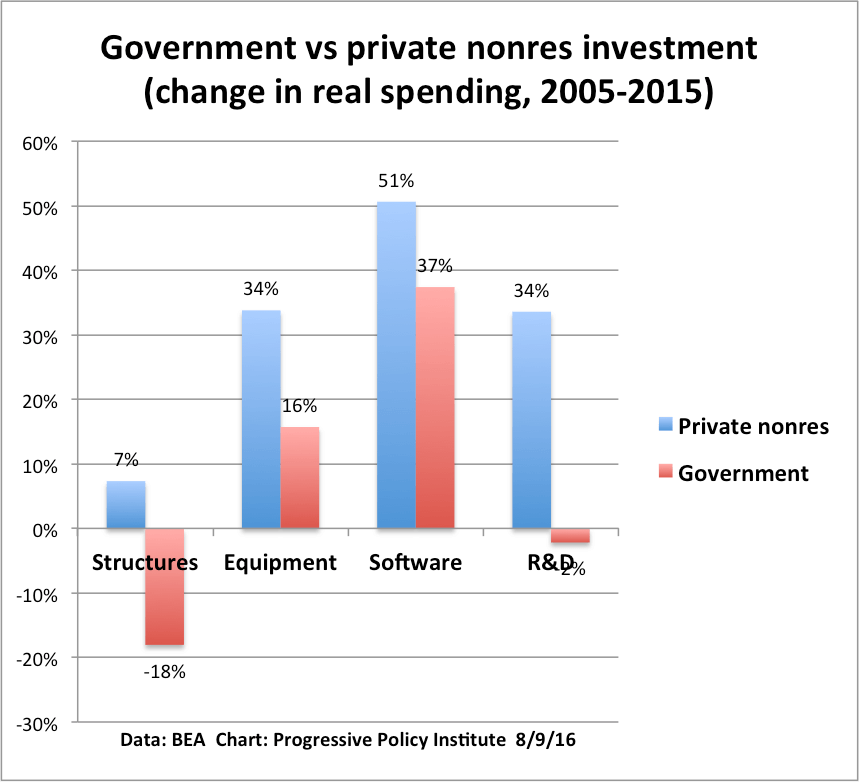

But we were pondering the recent annual revision from the Bureau of Economic Analysis, and noticed something very interesting: By some objective measures, government is more guilty of short-term thinking than business is.

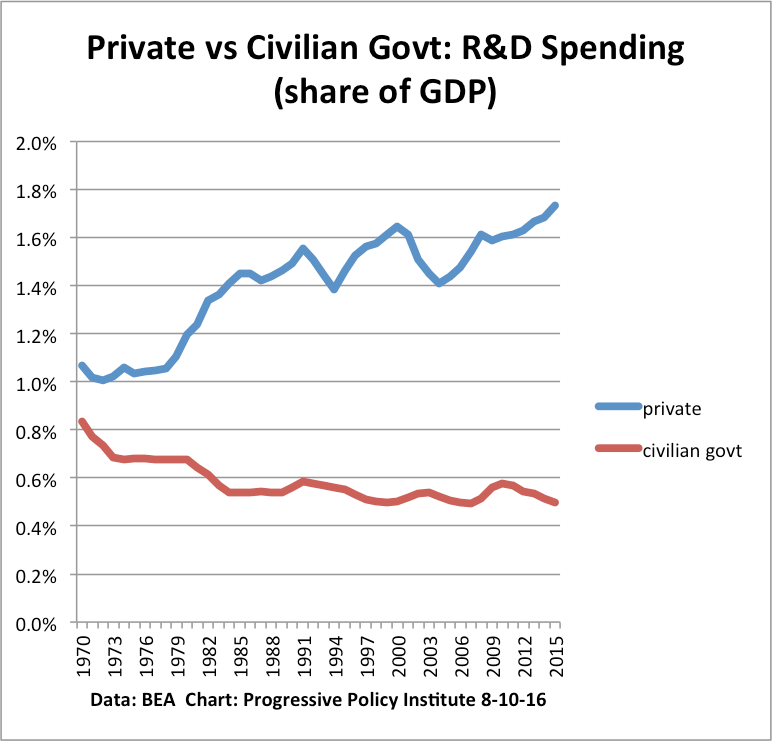

For example, one of the key measures of short-term vs long-term thinking is how much money is being invested in research and development. We found that over the past ten years R&D spending by the private sector has increased by 34%, in real terms. By comparison, real R&D spending by government at all levels has decreased by 2% (see chart below). This decline is mostly driven by defense R&D. But even if we just restrict ourselves to civilian R&D (federal state and local), the real gain in government R&D spending since 2005 is only 12%, far below the private sector increase.*

The gap between private sector and government investment in software is large, but not as large as for R&D. Since 2005, the private sector has increased its investment in software by 51% in real terms, compared to only 37% for government. Similarly, growth in real equipment expenditures by the private sector outpaced the government sector by a wide margin.

Finally, we come to structures. The private sector, despite the recession, has managed to somewhat expand its real spending on long-lived structures over the past ten years. Meanwhile, real government spending on structures–especially infrastructure–has tanked. Real government outlays for highways and streets is down 21% from 2005 to 2014.

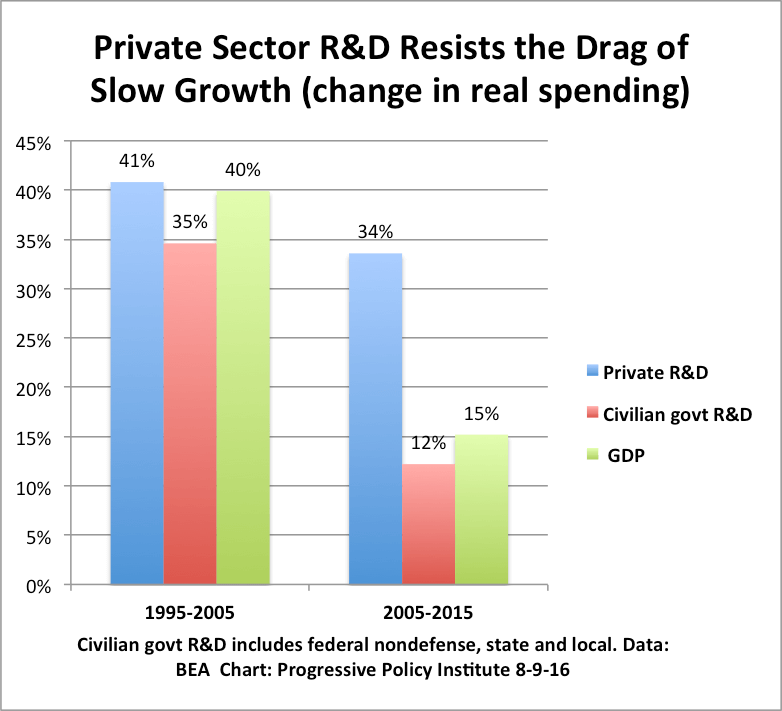

Now let’s focus down a bit more on R&D, which is one clear measure of long-term thinking. From 1995 to 2005, private R&D spending, civilian government R&D spending, and GDP all grew at roughly the same rate, adjusted for inflation. For example, over that period real GDP rose by 40%, and real private R&D spending rose by 41%.

But over the past ten years, the pattern is far different. GDP growth slowed sharply, from 40% to 15%, and so did the growth of civilian govt R&D. But private R&D spending barely took a pause, dropping only to 34%. In other words, the private sector continued to boost spending on R&D at more than twice the rate of the rate of GDP growth.

Finally, we can compare private sector R&D with civilian govt R&D, as a share of GDP, over the past 45 years. It turns that private sector R&D is at 45-year high, as a share of GDP, while civilian govt R&D spending is near a 45-year low.

So what conclusion can we come to? Clearly there is a business investment drought in many parts of the economy, as we have written repeatedly. But private sector R&D growth–a true measure of long-term thinking–has held up surprisingly well over the past decade, despite slow GDP growth. Meanwhile, civilian govt spending on R&D has slowed more or less in tandem with the overall economy. Government spending on structures–including physical infrastructure–has simply collapsed

So if policymakers are worried about short-term thinking holding back US growth, they might find it easier and faster to boost government spending on R&D and infrastructure, rather than crafting complex policies to affect private sector decision making.

*Data from OMB shows that nondefense federal outlays for R&D rose by 3.5% from FY2005 to FY 2015.

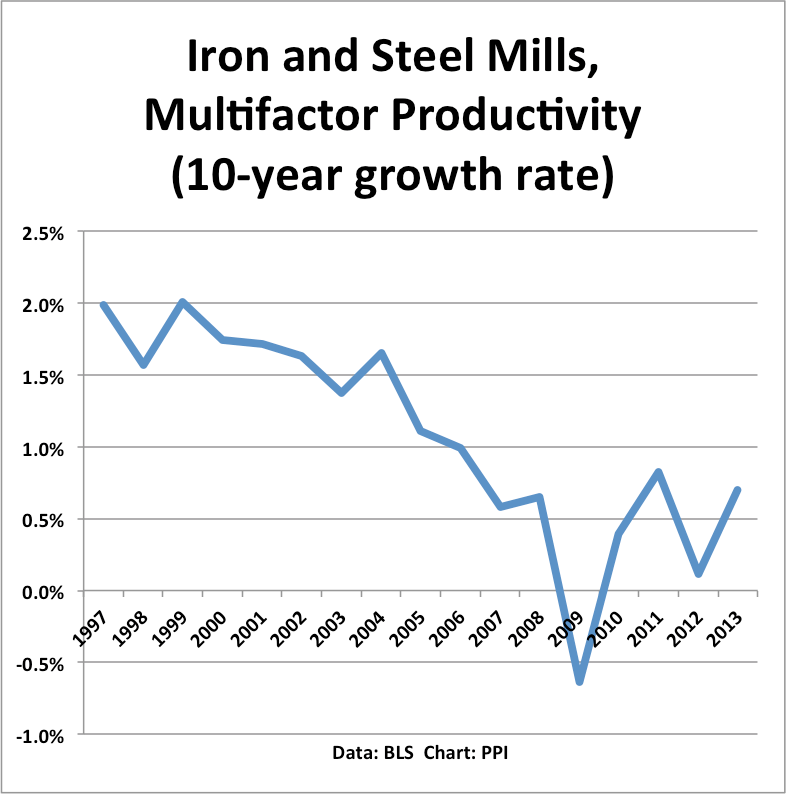

Yes, the productivity slump has hit the iron and steel mill industry as well.

Robert Samuelson wrote a long piece in the WaPo about productivity growth in the steel industry, arguing that “…[p]roductivity (a.k.a., efficiency) has increased dramatically.” His main source was a very careful academic study by Allan Collard-Wexler of Duke University and Jan De Loecker of Princeton University.

However, that study only used data up to 2002. Since then, multifactor productivity growth in the iron and steel mill industry has cratered, according to data from the Bureau of Labor Statistics (‘multifactor productivity’ growth, also called ‘total factor productivity’ growth, adjusts for use of capital, materials, energy, and purchased services. )

The chart below shows the growth rate of multifactor productivity was 2 percent annually in the 10 years ending in 1999. Then it slumped sharply. In the 10 years ending 2007–before the financial crisis–the average annual multifactor productivity gain was an excruciatingly slow 0.6%. That’s about where it is today.

Now, iron and steel mills are only a part of the steel industry. What’s happened to productivity growth in the primary metal industry, which also includes companies that buy steel and make it into steel products, foundries, and makers of non-ferrous metals such as aluminum and copper?

Nothing good, I’m afraid. In the 20 years between 1994 and 2014, multifactor productivity in the primary metal industry rose by only 1.7% in total. That averages out to an annual rate of less than 0.1%. In other words, any productivity gains in iron and steel mills since 1994 were swallowed up in the rest of the primary metal industry.

This is actually the central puzzle that economists have to unravel. Why has multifactor productivity growth been so slow across much of manufacturing over the past 20 years? (see the data here). Without significant productivity growth, it’s tough to produce rising wages or to compete against low-cost countries.

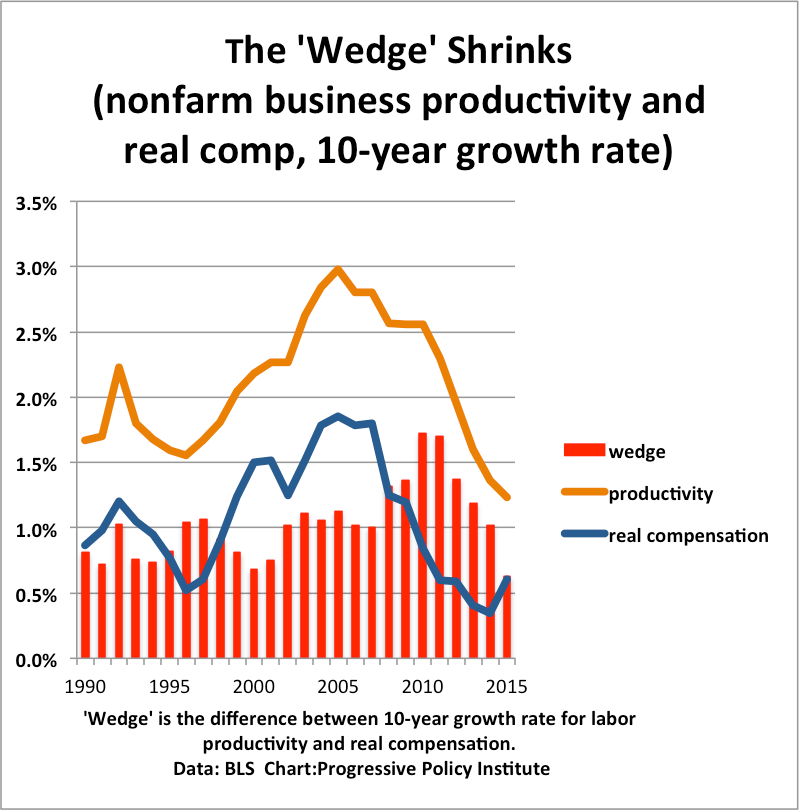

The ‘wedge’ between productivity growth and average real compensation growth has shrunk to the lowest level in at least fifteen years.* That’s because productivity growth is slowing, not because real compensation growth is accelerating significantly.

The top line is the ten-year growth rate of nonfarm business productivity, based on data reported by the Bureau of Labor Statistics. The bottom line is the ten-year growth rate of real labor compensation. The vertical lines represent the’wedge’–the difference between productivity growth and compensation growth.

What we see is that the wedge is 0.6 percentage points, the smallest difference between productivity growth and compensation growth in at least 15 years. To put it a different way, the slowdown of real compensation growth is very closely tied to the collapse of productivity growth.

This data does not mean there is no inequality problem. Because these figures report average compensation growth, they do not reflect increased inequality between workers, or the difference between median and average workers. However, they do imply that the problems facing American workers today have at least as much to do with weak productivity growth as with rising inequality.

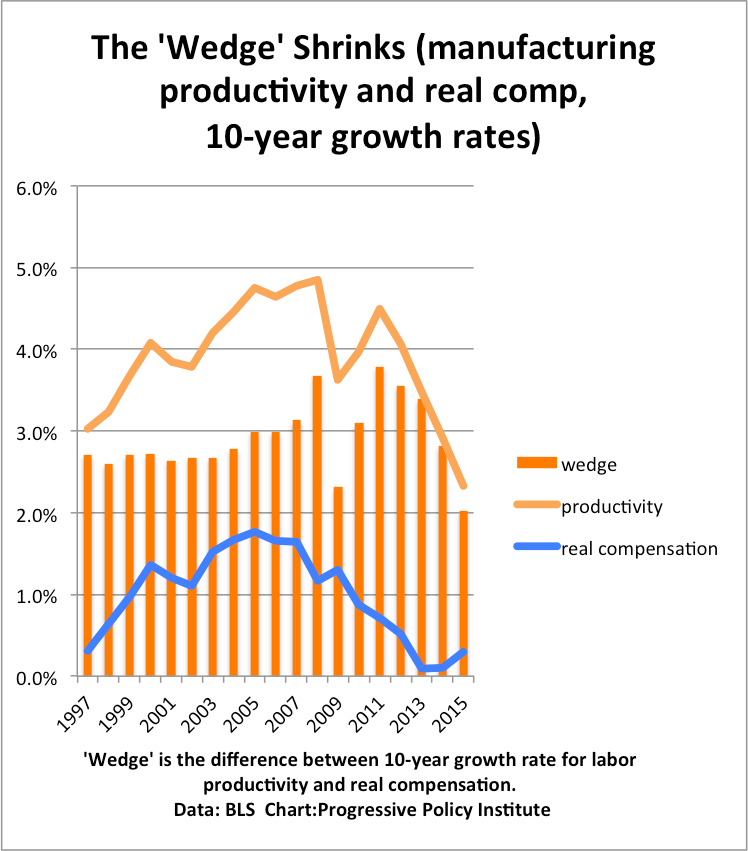

We see the exact same pattern in the manufacturing data, only more so. The growth rate of manufacturing productivity peaked in the mid-2000s, along with the growth of real compensation in manufacturing. Since then, productivity growth has collapsed by 2.4 percentage points, while real compensation growth has dropped by 1.5%. So even within the goods-producing sector, the extreme weakness in compensation growth is driven by the decline in productivity growth.

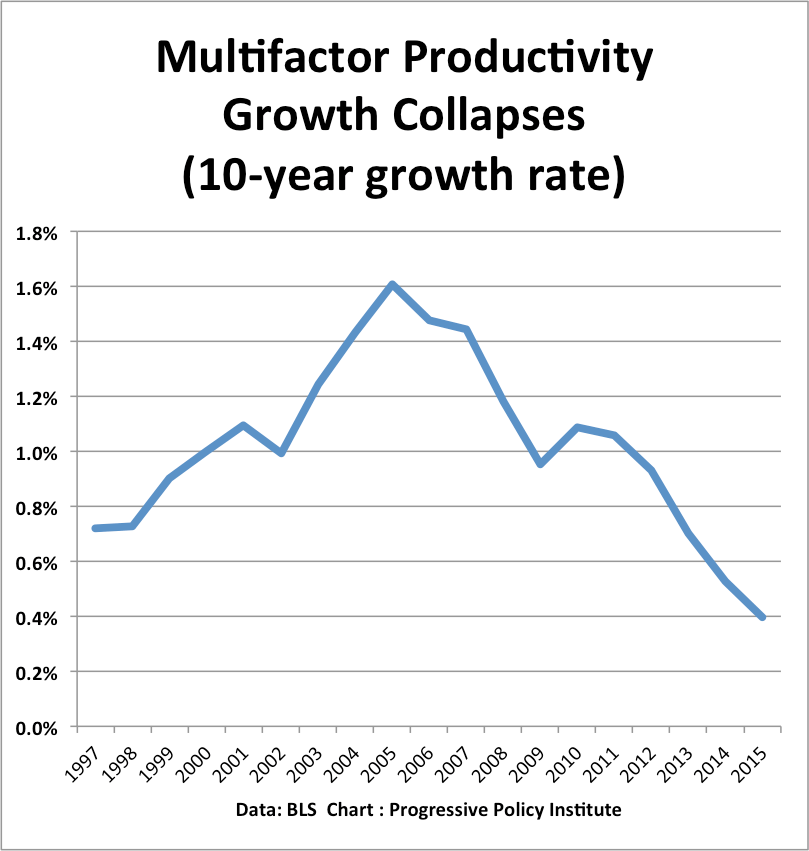

If we look at the 10-year growth rate of multifactor productivity, the importance of slowing productivity growth becomes even more vivid. Multifactor productivity growth in some sense represents the “innovation” component of growth. It measures the ‘vibrancy’ of an economy–the ability to get out more than we put in by being smarter.

We see that multifactor productivity growth has collapsed to only 0.4% annually, well below the 0.7% growth in the 10 years before 1997. Indeed, as a recent blog item showed, many manufacturing industries have negative multifactor productivity growth since 1994. When the pie is shrinking, it can’t be cut in a way to make everyone happy.

Addressing the inequality problem is important. But Americans can’t prosper unless we fix the productivity problem as well.

*This discussion abstracts from a very wide range of substantive and technical issues, including: the difference between median and average workers; the correct measure of compensation; the best deflator to use, etc. A good review of some of these issues can be found here, though I disagree with some of the conclusions. In addition, I believe that productivity growth figures should be treated with some wariness, given the inability of statisticians to do a good job tracking global supply chains in goods, services, and data. Having said all that, there is little doubt that productivity growth has slumped sharply, not just in the US but across the developed world.

After the Republican fear-fest in Cleveland, watching the Democrats in Philadelphia last week was like stepping out of the Dark Ages into the Enlightenment. Donald Trump may have no use for facts, civility or rational argument, but these things still seem to matter to Democrats.

There was, however, a big exception to the rule: trade. Riding a wave of populist wrath, Democrats demonized President Obama’s Trans-Pacific Partnership (TPP) as a gift to the 1% and mortal threat to U.S. workers. It’s a bogus claim, and one that has them sounding a lot like, well, Trump.

TPP is a linchpin of Obama’s strategic goal of “rebalancing” U.S. power and diplomacy. It would combine the U.S. and 11 Pacific nations in a vast free-trade zone that would act as a counterweight to China’s enormous economic might. If the pact goes down, so will our influence in the region, leaving Beijing to call the shots.

The division between the trade skeptics and the trade supporters in the Democratic Party is on stark display at this week’s convention in Philadelphia. The Progressive Policy Institute favors smart, high-standard trade agreements, as PPI president Will Marshall and senior fellow Ed Gerwin recently wrote.

Yet both trade skeptics and supporters can agree on one critical point: The government must do more, much more, to provide American manufacturers, especially small ones, with the tools they need to compete successfully against foreign rivals on global and domestic markets. If American manufacturers can compete more successfully, that will lead to more jobs for Americans.

A good first step: The International Trade Commission, the Bureau of Labor Statistics, and the Department of Commerce should jointly lead a government-wide project to do a “competitiveness audit“ of the U.S. economy, as PPI wrote in a previous policy brief, “How a Competitiveness Audit Can Create Jobs”. This competitiveness audit would compare the price of a wide variety of US-made products with the price of similar imported products, based on functionality and quality. The audit would cover the full range of manufacturing industries, from communications equipment to furniture to chemicals to machinery. So, for example, the audit would compare the producer price of a piece of household furniture produced in the United States versus the import price of a similar piece produced in China.

The competitiveness audit is likely to show a big gap between US-made and import prices for some products. But other products are likely to have a small and perhaps shrinking gap, making them prime targets for expansion of US production.

Armed with this information, American manufacturers will be able to target markets where the United States has a competitive advantage. Small companies, especially, will benefit from information produced by the competitiveness audit, since they don’t have access to the global networks that their bigger counterparts do.

The competitiveness audit can also stimulate the formation of new manufacturing businesses by pointing out market opportunities to potential entrepreneurs. People who want to start a new manufacturing business in Ohio, say, will be able to use the competitiveness audit to attract funding.

In addition, mayors and other local officials would be able to use the results of the national competitiveness audit to help direct their economic development efforts. Right now, they are simply shooting blind, without adequate information about where the US has a competitive edge.

Surprisingly, the government currently does not collect or publish data comparing prices of domestic and imported products. That’s an egregious hole. Filling that hole would not only help manufacturers, but would also help economists resolve some big issues about the impact of trade on the economy.

No matter where you fall on the trade question, a competitiveness audit makes sense: If we want to see a revival of manufacturing employment, we have to provide small manufacturers and local officials with the information they need to make good decisions.

Reference

Michael Mandel and Diana Carew , “How a Competitiveness Audit Can Help Create Jobs,” Progressive Policy Institute, November 2011. https://progressivefix.com/wp-content/uploads/2011/11/11.2011-Mandel-Carew_How-A-Competitiveness-Audit-Can-Help-Create-Jobs.pdf