Mike Konczal’s inequality post as a guest blogger for Ezra is getting a bit of attention in the blogosphere. Konczal jumps off of an interesting post by Jamelle Bouie to argue that contrary to those who argue that “inequality isn’t so bad,” the unhealthy nature of the cheaper food that is purchased by the poor negates the fact that the poor face a lower inflation rate. Since he suggests I (and Will Wilkinson) think that “inequality isn’t so bad,” I wanted to correct a misconception that Konczal has about the argument of economist Christian Broda that he is responding to. Broda’s actual argument really doesn’t have anything to do with how healthy the things purchased by the poor are.

Here’s Konczal:

One argument that has become popular recently is that the increase in income inequality isn’t quite as bad because both the rich and the poor have different ‘inflation’ rates — the prices at which goods increase for the rich have been increasing much faster than the prices at which goods have been increasing for the poor. So even though the poor or median person hasn’t had any wage growth, he has much more purchasing power because of this effect.

This isn’t quite the argument that has become popular recently. What fans of the Broda research argue (i.e., what Broda and his colleagues argue) is that the apparent increase in income inequality may overstate the actual increase in inequality because the poor appear to have a lower inflation rate than the rich. If true, then it’s not that “the poor or median person hasn’t had any wage growth,” it’s that they have had wage growth because of their lower inflation rate — and the wage growth has been big enough that it has kept the ratio of rich-to-poor incomes roughly constant.

Think of it this way. Broda and his colleagues find that the prices of what the poor buy (that is, “price” when the satisfaction derived, or utility, is held constant) have risen less than the prices of what the rich buy. That’s because when prices of related goods change, the poor are more likely to switch to cheaper goods, all the while maintaining their overall level of satisfaction with their purchases. If it becomes cheaper to maintain a constant level of satisfaction, then one’s wages have effectively grown. So poor consumers may switch from Green Giant frozen veggies to generics when the latter go on sale, or they might buy their frozen veggies at the chain a couple of neighborhoods over rather than the local grocery store when the latter’s prices go up. Rich consumers, on the other hand, may be relatively unlikely to stop buying Whole Foods vegetables when the plebian chain’s prices are cut. They may not switch to generics as those products become cheaper relative to those on offer at the farmer’s market.

It’s not that we should be excited about how great the generic frozen veggies bought by the poor are compared with the Whole Foods produce. It’s that we should be excited that the poor are either more willing or more able to economize to maintain a constant lifestyle than the rich are, and so inflation eats into their quality of life to a lesser extent than it does among the rich, holding in check other forces that would increase inequality.

Now, Broda’s research is based on purchases of a limited number of commodities and over a limited number of years, but if his findings extend to other goods and services and to earlier periods (which he believes they do), then the implication is that inequality between the poor and the well-off — though not necessarily the richest of the rich — has not grown. We can still worry about the quality of the food purchased by the poor and their health outcomes, but that’s a story about poverty and deprivation, not about inequality or growth in inequality.

An army of census takers has begun knocking on doors all across the country, following up on the 48 million households who didn’t send in very user-friendly forms in spite of a ubiquitous media campaign. There must a better, cheaper and even safer way to do this.

There is. People should be able to respond online.

In 2000, the government quietly experimented with a limited online option and it was very successful, as noted in a 2008 report by ITIF’s Daniel Castro. The online option was not publicized, but a few savvy citizens (.07 percent of respondents) discovered the link on the U.S. Census Bureau’s website and 94 percent of them said they liked it.

Ten years is several generations in Internet time. Less than five percent of Americans had broadband connections at home in 2000. Today, an estimated 68 percent take advantage of broadband access, and that percentage grows by six to eight percent each year. To be sure, there are many without access to computers and still others who would prefer not to respond online. Still, with so many more of us online daily and with the short form the Census Bureau used this year, it is reasonable to think we would have a high participation rate and could end up with a more accurate count. Canada, Australia, Singapore and Norway are using the Internet to collect data. We should, too.

Regrettably, back in 2008, the Census Bureau nixed the idea of an Internet-based data collection for 2010 mainly for three not very compelling reasons -– that it would not necessarily increase the response rate, that the entire undertaking could be wrecked by security problems and that it was too expensive. Given how much of life has migrated online, these objections seem a little flimsy in 2010.

First, no one claims using the Internet-based approach will boost overall participation. The Census Bureau quite correctly cited data from other countries that have adopted an online system. But it might help individuals respond more thoroughly and accurately. Besides, higher participation isn’t the only reason for using the Internet. It is easier and more conducive to the online habits of an increasing number of Americans.

Second, while security concerns such as denial of service attacks, “phishing” (where fraudulent sites pose as legitimate sites to extract sensitive information from people), or the use of spyware to steal data are legitimate, they are not sufficient to completely scrap an online count. For one thing, the risks from a denial of service attack are minimal in a non-time-sensitive project like the census — if the website is unavailable, respondents would simply check back later. The concerns about unscrupulous operators and hackers are part of life online and security experts have gotten pretty good at protecting consumers and citizens. ITIF estimates that 25 years after the first dot-com, the global economy is larger by $1.5 trillion a year thanks to the commercial Internet. The Internal Revenue Service says roughly 100 million of the 140 million tax returns filed this year were done so electronically. That’s a lot of personal data and money floating around and most of it is secure, so long as people are attentive to instructions and wary of possible fraud. There may be no such thing as a 100 percent secure system (on the Internet or in the real world) but that is no reason to put off going online with the census.

Third, but perhaps most important, is cost. The census is not cheap. The cost for the education effort, forms, workers and other activities adds up to $14.5 billion, according to the bureau. In 2008, there was a much-publicized and costly kerfuffle over the bureau’s problems with hand-held devices. The decision to scrap them rather than figure out how to use them effectively may have cost taxpayers $3 billion needlessly.

Aside from that snafu, the agency observed in 2008 that it would be hard to predict online usage and the number of paper forms that would be needed, and that there would be considerable startup costs for an online system. But an analysis by ITIF in February 2008 estimated that even with an online response rate of just 10 percent, the savings could have added up to $28 million — more than enough to cover the $22.5 million the Census Bureau estimated would be needed to implement an Internet-based system.

The bottom line is that there will always be challenges shifting an undertaking as massive as the decennial census from paper to electronic mode. But the Census Bureau, and all other government agencies for that matter, should be creating ways to overcome these challenges and not be fearful of being overcome by them. It is hard to think of anything that could be done more smoothly than the census with the smart use of information technology. That’s 20/20 hindsight for 2010 and foresight for 2020.

How to tell a good climate bill from a bad one? This series will guide you through the main issues that are likely to arise in the coming weeks as the Senate takes on climate change. In previous posts, we looked at the crucial and the merely important issues that factor in the climate debate. In this post we highlight issues that matter for climate policy, but will not necessarily make or break it. (To read the other posts in the series, click here.)

So far, we’ve established the absolutely critical aspects needed to make credible climate policy and identified the important features that would make that policy effective. Now we will focus on issues that aren’t quite on the same level, negotiable elements that could still have a meaningful role in determining the long-term viability and effectiveness of a domestic emissions mitigation program. These issues — specifically, price controls and the international implications of U.S. legislation — could become a big part of the political discussion.

Category III Issues: Negotiable Elements of Climate Policy

#1: Price controls: offsets and collars

An uncontrollably rising carbon price is a nightmare scenario for regulated firms and consumers, so industry groups have made a priority of getting robust price controls into climate legislation. Price controls generally take three different forms: banking and borrowing, offsets and price collars. Because banking and borrowing has such a strong effect on the emissions reduction path, we included them in our last post. Here we’ll focus on the two other strong cost containment mechanisms.

a) Offsets

If you’ve been paying attention to the debate over the past two years, you’ve likely heard something about offsets. They are one of the most controversial aspects of climate legislation. Environmentalists are suspicious of them and industry can’t live without them.

What exactly are offsets? As we mentioned in a previous post, carbon is a stock pollutant, meaning that we only care about its total accumulation in the atmosphere. If you keep adding carbon to the system, but remove an equal amount at the same time, it is just as good as no longer adding carbon at all. This is the underlying principle of offsets — firms that pay to remove greenhouse gases from the atmosphere (or keep them from entering in the first place) can receive the same credit they would get if they reduced their own emissions.

For example, with offsets in a cap-and-trade system, a utility that needs to reduce its carbon emissions by 20 million tons need not do so only through emissions cuts from its operations. It could reduce its own emissions by 15 million tons, then receive offset credits through financing a reforestation project and an agricultural methane reduction project that combined would lead to emissions reductions of five million tons, allowing the company to meet its target.

Here is a quick list of different kinds of offsets that might count under climate legislation:

Forestry: Forests absorb CO2 through natural respiration processes and store it in plant tissue and soil. When deforestation occurs, that stored carbon is released into the atmosphere, contributing to emissions. Deforestation and forest degradation count for around 15 percent of global CO2 emissions. Projects that reforest — increasing carbon sequestration — or reduce deforestation and forest degradation are growing increasingly popular in voluntary carbon markets and may facilitate significant savings. Some models have speculated that international forest offsets can account for 25 percent of emissions mitigation by 2020.

Agriculture: The agricultural sector accounts for six percent of U.S. emissions, but agricultural emissions will probably not be covered by a carbon price due to the complexity of measuring emissions from agricultural practices and the power of the farm lobby in Washington. The important gases from agriculture are methane emissions from large-scale cattle operations and manure management, and nitrous oxide emissions from fertilizer applications and soil management. Offset projects that capture renegade methane emissions or reduce nitrous oxide releases through better soil management will likely be the most widespread offsets available from the agriculture sector.

Renewable energy/energy efficiency: Projects that supplant dirty energy sources with cleaner sources or improve efficiency in energy production or end-use can also be eligible for offset credit. For example, a firm looking for cheap reductions could finance the development of a renewable energy project and receive credit for the emissions reduced when the renewable energy displaces conventional dirty energy. Additionally, projects that increase the efficiency of energy usage in buildings or facilities can count as offsets. These projects are a major component of the Clean Development Mechanism (CDM), which was established by the Kyoto Protocol. Using the CDM, developed countries can sponsor projects in developing countries and receive emissions reduction credit.

Waste management: The decay of garbage in the nation’s thousands of landfills represents the second largest source of U.S. methane emissions behind cattle operations. Methane flaring, a process that captures and burns these emissions, converting methane into CO2, is considered an offset, as CO2 has a lower global warming potential than methane. Combusting methane for energy generation may also generate offset credits.

Fugitive mine emissions: As with landfills, capturing fugitive methane emissions from coal mines presents an opportunity for offsets and may also have benefits in terms of miner safety.

While all of these offsets options are currently available in voluntary offset markets and allowed by regional cap-and-trade schemes like RGGI, they may not all be eligible for credit under federal regulation. Waxman-Markey does not count renewable energy, energy efficiency, waste management and coal emissions as offsets. Cantwell-Collins does not allow offsets in its trading system, but it does permit such projects to be paid for from its Clean Energy Reinvestment Trust.

Many offsets will be cheaper than actual emissions reductions, making them an important means of price control. This is especially true for international forest offsets — the EPA analysis of Waxman-Markey contended that allowance prices would be 96 percent higher without them. That said, Greenpeace and other environmental groups have firmly planted their flag in the anti-offset camp, and there are a number of issues that would need some serious policy attention in order to make forest offsets credible in the U.S. market.

There are four major requirements to making offsets a robust tool. First, they must be additional — that is, projects should only be considered offsets if the specific practice would not have happened anyway. Second, offsets should have permanence — projects are only useful if they are not quickly undone (an offset for planting a tree is of little value if it is rapidly cut down). Third, offsets should be verifiable — there must be some way to confirm that projects are doing what they claim (for forests, this can be very difficult). Finally, offset programs should address leakage — they should not simply shift emission-generating activities somewhere else. These are all valid concerns, and all four will have to be addressed for offsets to be a credible part of climate policy.

Potential hang-ups for offsets will likely involve politicians’ hesitations to send large sums of money overseas, the reliability and veracity of offset credits, the number of offsets allowed for use by regulated firms and the type of offsets available from domestic sources. Despite the misgivings of some policymakers and commentators, offsets will figure prominently in domestic legislation. Waxman-Markey included two billion tons worth of offsets annually, a significant proportion of overall U.S. emissions, the same amount as in the Kerry-Boxer bill introduced in the Senate last fall. Instead of spending time and energy railing against them, policy discussions should instead focus on setting up institutions to fix the problems listed above.

b) Price collars

More than anything else, firms want some certainty when it comes to climate regulations. Planning capital investments over the long-term will be significantly affected by carbon prices, and the more predictable the changes over time, the better firms can plan ahead. Moreover, sudden system shocks in the form of extreme drops or increases in prices can be very expensive and detract from the efficacy of cap-and-trade markets.

To protect the system and reduce price uncertainty, policy-makers are looking to use a price collar in the allowance market. A price collar is a way to define a general price path by restricting how much the price can rise or fall. Price collars work by establishing a price floor — under which the allowance price can never drop — and a price ceiling — above which the price will not rise. It is a simple mechanism in concept, and can provide a lot of certainty for regulated parties and market participants. The price floor and ceiling should be spaced far enough apart to accommodate market dynamics and rise at some rate to match the general rise in allowance prices.

When allowance prices hit the floor, they simply remain at that price until trading forces the price to rise again. Things get more complicated when they hit the ceiling, however. There are two options to bring down the price, depending on if you employ a hard collar or a soft collar. A hard collar releases additional allowances into the system until the price drops, regardless of how many it takes to do so. By contrast, a soft collar uses a strategic reserve of set-aside allowances to reduce the price below the ceiling. The difference between the two is a matter of emissions certainty. A soft collar maintains the overall emissions cap by taking some out of the system at the beginning, much like a rainy day fund, whereas a hard collar just dumps allowances into the market until the price changes. Firms may favor a hard collar because it provides more price certainty, but people concerned about overall emissions will prefer a soft collar.

#2: International aspects

If and when Congress does pass climate legislation, its impact will reach far beyond our borders. The international implications of domestic climate policy are extensive, and while they do not play a huge role in the political discourse, they have sway over some notable policy choices.

a) International negotiations

The Conference of Parties (COP) 15 in Copenhagen in December 2009 was advertised as a chance for the U.S. to reclaim its place at the world leader and innovator on environmental issues. The U.S. was able to do that only partially, and that was due largely to the extraordinary personal diplomacy of President Obama. U.S. negotiators had little to work with, bringing with them no official legislation to show other nations while trying to broker a deal that could pass Senate muster. Without a signed bill, the 2010 COP in Cancun this coming November will probably turn out similarly; nations will bicker and haggle and eventually end up not making any kind of serious commitment sans U.S. leadership. The EU does not have the sway to move a global climate deal forward, while other major emitters like China and India don’t have the incentive to act.

That’s not to say international negotiations will not have some influence on the shape of U.S. legislation. At Copenhagen, the U.S. committed to provide $30 billion from 2010 to 2012 to developing countries for mitigation, adaptation, technology transfer and other assistance. Additionally, the conference agreed to establish an annual $100 billion fund — of which the U.S. is expected to give roughly $20 billion — for developing countries for the same uses. Some of this funding will likely be partitioned from current programs, but it will certainly not be enough. Revenues from carbon markets established by climate legislation — as well as allowance allocations — will likely provide the most reliable source of international funds. The tradeoff is that every dollar spent on helping other nations adjust to climate change is one that can’t be used domestically. Though it won’t dominate the debate over any climate bill, the use of carbon revenues for international financing could end up having a real impact.

b) Competitiveness and leakage

Certain industries with intrinsically large carbon footprints, such as cement, steel and paper pulp, are particularly sensitive to carbon prices. These industries are concerned that paying for their sizable emissions will reduce their overall output, leading to job cuts and smaller profit margins. Moreover, they worry that a U.S. carbon price will lead to a shift in production to other countries that do not have similar regulatory burdens. When firms leave for other countries that don’t have a climate policy, it could lead to higher overall global emissions, a phenomenon known as leakage.

There are a couple of solutions to these problems. First, to help protect industries at home, climate policy can include rebates to industries — either in the form of cash or extra tradeable allowances — based on their output to help them adjust to the new reality of a price on carbon. Second (and more controversial), the federal government can establish border adjustments, slapping taxes on imports competing with vulnerable domestic industries. Essentially tariffs, such levies would put goods from countries without a climate policy on the same level as those from the U.S. Border adjustments can make for tricky politics, though. When the Waxman-Markey bill passed the House in 2009, President Obama openly criticized the inclusion of such measures. When the debate picked up in the Senate, however, 10 Midwestern senators stated they would not back any climate legislation that did not support manufacturing interests with some kind of border provision. Even if some compromise allows border adjustment to find its way into climate legislation, there’s a chance it would not be allowed under WTO agreements.

The Bottom Line

Last post, we reviewed important aspects of climate policy. In this post, we surveyed two areas that have value in generating good policy, but are negotiable in terms of their importance:

Is there a price collar? Are offsets allowed?

What is the effect of the proposal on international climate issues? How will it affect negotiations and commitments? How does it attempt to protect trade-vulnerable industries?

In our next and final post, we will focus on the issues that make little contribution to good climate policy — or might even be counterproductive.

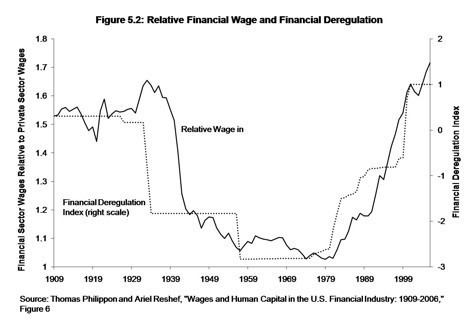

James Kwak, coauthor of the new financial crisis book 13 Bankers, recently sought to explain his thesis “in 4 pictures.” And impressive pictures they are. But I’ve been particularly struck by one of them — this chart, from a paper by economists Thomas Philippon and Ariell Reshef, showing the close correspondence between deregulation trends on the one hand and the ratio of financial sector wages to private sector wages on the other. My reaction to the chart was essentially, Huh. Those trend lines look like the basic income inequality trend line.

But to my knowledge, no one has really made this point since the chart has circulated widely. Certainly no one has tried to illustrate it.

Maybe people just lack my whiz-bang PowerPoint and Excel skills, or maybe I’ve actually had an Original Thought. But take a look at the chart I created, which overlays a trend line showing the share of income received by the top one percent (the black line) on top of the Philippon-Reshef chart. The trend line comes from the widely cited work of economists Thomas Piketty and Emmanuel Saez, who used IRS data to look at the incomes of the very rich:

I’ve argued before that I think the Piketty-Saez top-share trend line overstates the recent rise in income inequality, but I don’t see much reason to doubt the basic U-shape of the trend since the Great Depression. For all of the consensus around the basic inequality trend, there’s surprisingly little agreement or understanding as to why it looks the way it does (a major theme of Paul Krugman’s Conscience of a Liberal). Could it really be as simple as the extent of financial regulation? Every analyst bone in my body says this is too easy, but…but….

Of course, saying it’s all financial regulation trends isn’t necessarily inconsistent with Krugman-esque arguments that it’s all about changes in cultural acceptance of inequality. Maybe financial regulation flows from public attitudes about inequality.

I know you’re not supposed to tout your own work on blogs, but for this, my inaugural post for Progressive Fix, I can’t resist.

When PPI established its New Economy Task Force 11 years ago, its first product was a pamphlet entitled “Rules of the Road: Governing Principles for the New Economy.” In Internet time, 11 years is a lifetime. But that short but powerful statement still holds up — and, I would argue, is just as relevant today as it was in 1999. This seems as good a time as any to revisit what we said and take stock of how far — or not — we’ve come.

The pamphlet started off with this statement:

The U.S. economy has undergone a profound structural transformation in the last decade and a half. The information technology revolution has expanded well beyond the cutting-edge high-tech sector. It has shaken the very foundations of the old industrial and occupational order, redefined the rules of entrepreneurship and competition, and created an increasingly global marketplace for a myriad of new goods and services.

I would venture to say that it’s even truer today than when we first wrote it. The introduction went on to state:

Yet while economic reality is fundamentally changing, much of our public policy framework remains rooted in the past. This mismatch between public policy and economic reality is not sustainable. … On one side of the political spectrum, policymakers advocate across-the-board tax cuts, a dramatically reduced role for government, and elimination of social regulations. … On the other side of the political spectrum, policymakers advocate increased spending on top-down social programs geared toward income redistribution, coupled with a focus on command-and-control regulation through bureaucratic institutions, ignoring just how entrepreneurial, fast moving, and flexible our economy has become. Furthermore, resistance from both ends of the political spectrum to open trade, global integration, and technological and organizational change threatens to slow the economic changes that hold great potential to yield higher standards of living for American workers

After 11 years, while some progress has been made, all too often policy-makers still view economic and technology challenges through either of these lenses. And those resistant to change, whether groups advocating for strict regulations on “network neutrality” and “Internet privacy,” or restrictions on globalization and trade, continue to be active, if not more so.

How Far Have We Traveled?

The guide offered 10 key rules to policy-makers to encourage an innovation-driven economy. How have we done on those prescriptions? Let’s go down the list:

Rule #1: Spur Innovation to Raise Living Standards

….Because innovation and change are disruptive, they tend to spark strong political demands to insulate affected segments of the economy and slow down economic change. Such demands, while understandable, inherently deny opportunities to less politically powerful interests in the guise of “protecting” those with clout. As a result, to effectively promote growth in the New Economy, government must facilitate, rather than resist, the processes of economic change and modernization as these changes create new opportunities and increased incomes for all Americans.

Unfortunately, the urge to protect the status quo is powerful, as Washington still shows little appetite for upsetting it by enabling or promoting innovation.

Rule #2: Expand the Winners’ Circle

Ensuring that the benefits of innovation and change are spread broadly will require that all Americans, including those not yet engaged in or benefitting from the New Economy, have access to the tools and resources they need to get ahead and stay ahead.

We’ve made some progress here, not the least of which was expanding health care coverage to more Americans (though the effects of reform won’t be felt for years). But more needs to be done, particularly in areas like unemployment insurance reform and better access to lifelong learning.

Rule #3: Invest in Knowledge and Skills

To spur innovation and equip citizens to win in the New Economy, government should invest more in the knowledge infrastructure of the 21st century: world class education, training and life-long learning, science, technology, technology standards, and other intangible public goods. These are the essential drivers of economic progress today.

Not many in Washington would disagree. But it’s a different matter altogether to muster the political will to increase investments in these areas, particularly when it means cutting old economy spending, such as agricultural subsidies.

Rule #4: Grow the Net

The Internet is a critical component of the emerging digital economy. …The information technology revolution is transforming virtually all industries and is central to increased economic efficiency and productivity, higher standards of living, and greater personal empowerment.

Governments must avoid policies and regulations that would inhibit the growth of the Internet or slow progress by protecting business interests threatened by the digitization of the economy. Policymakers should craft a legal and regulatory framework that supports the widespread growth of the Internet and high-speed “broadband” telecommunications, in such areas as taxation, encryption, privacy, digital signatures, telecommunications regulation, and industry regulation (in banking, insurance, and securities, for example).

In some ways Washington has embraced this message. The inclusion of billions of dollars for support for the smart grid, health IT and broadband in the stimulus package was a key step in the right direction. On the other hand, the growing interest in regulating the Internet — such as overly restrictive net neutrality and privacy regulations — suggests that we have gone in the wrong direction.

Rule #5: Let Markets Set Prices

In the old economy, government often regulated prices when national markets were dominated by oligopolies or monopolies. In those cases, the economic costs of government intervention were manageable, and sometimes necessary. But in the new, more competitive global economy, distorted prices are much more likely lead to economically inefficient decisions by consumers and producers and to unfair, politically driven resource allocation. Therefore, in the absence of clear market failures, markets, not governments, should set prices of privately provided goods and services.

It’s still hard for many policy-makers to embrace this rule, but it’s as valid today as it was a decade ago.

Rule #6: Open Regulated Markets to Competition

Economists have long acknowledged that competition keeps prices down. The New Economy creates another critical reason for competition: competition drives innovation, and ultimately provides the greatest benefits to consumers and citizens. Of course, government must continue to provide common-sense health, safety, and environmental regulations. However, government should move away from regulating economic competition among firms and instead promote competition … Through minimalist, yet consistent rules, public policy should also ensure that consumers have the information they need to make educated choices and provide a backstop to protect consumers and citizens from abuse in markets.

Like rule # 5, it’s hard for some policy-makers to resist intervention to regulate competition. We see it most clearly in telecommunications, where some still argue that more government-enforced competition is needed.

Rule #7: Let Competing Technologies Compete

Technological innovation has now become central to addressing a wide range of public policy goals, including better health care, environmental protection, a renewed defense base, improved education and training, and reinvented government. For example, technology provides doctors and patients with state-of- the-art health information systems that improve the quality of care. Similarly, new generations of cleaner technologies can dramatically reduce pollution generated by industrial processes. … We should look for technology-enabled solutions to public problems, but not so that today’s winners are frozen in place at the expense of tomorrow’s innovators.

Amen. While government does need to target technology areas (e.g., clean energy, IT, robotics, etc.), it shouldn’t pick specific technologies within those sectors.

Rule #8: Empower People With Information

In the old economy, information was a scarce resource to which few outside of large corporations and governments had access. In the New Economy, constant innovations in ever-lower-cost information technologies have enabled increasingly ubiquitous access to information, giving individuals greater power to make informed choices. Governments should encourage and take advantage of this trend to address a broad array of public policy questions by ensuring that all Americans have the information they need as consumers and citizens.

Progress on this front: The recently announced National Broadband Plan, for example, takes a number of important steps in this direction.

Rule #9:Demand High-Performance Government

Government should become as fast, responsive, and flexible as the economy and society with which it interacts. The new model of governing should be decentralized, non-bureaucratic, catalytic, results-oriented, and empowering. …

When designing solutions to compelling public concerns, such as reducing industrial pollution or delivering world-class public education, government should hold organizations and individuals accountable for meeting goals, while allowing them flexibility to achieve those goals. In many cases, industry self-regulation can achieve public policy goals in ways that are more flexible and cost effective than traditional command-and-control regulation, while also enabling technological innovation.

Procedurally, governments should use information technologies to fundamentally reengineer government and provide a wide array of services through digital electronic means to increase efficiency, cut costs, and improve service. Digitizing government is the next step in re-engineering government.

Washington may give lip service to #9, but when the rubber hits the road, much is still the same. Perhaps the main area of progress is using IT to transform government, but even here a great deal remains to be done.

Rule #10: Replace Bureaucracies With Networks

In the old economy, bureaucracy was how we addressed many major public policy problems. In the New Economy, we must rely on a host of new public-private partnerships and alliances.

Rather than acting as the sole funder and manager of bureaucratic programs, New Economy governments need to co-invest and collaborate with other organizations — networks of companies, universities, non-profit community organizations, churches, and other civic organizations — to achieve a wide range of public policy goals.

Yet public policy has only begun to explore the potential of bottom-up, decentralized networks assuming the lead role in solving pressing societal problems. Government needs to co-invest in these efforts and foster continuous learning through the sharing of best- practice lessons. Most importantly, the collaborative network model requires government to relax its often overly rigid bureaucratic program controls and instead rely on incentives, information sharing, competition, and accountability to achieve policy goals.

Of the 10 rules, this last one may be the hardest for policy-makers to embrace. The legacy of government bureaucracy and “programs” as the solution to our problems — rather than government-enabled networks — is so deeply held that new approaches are not even considered in many cases.

More than a decade since we first published these rules, it’s clear that many of our prescriptions remain unheeded. Whether or not you embrace the term “New Economy” is not the point. The U.S. economy is fundamentally different than it was two decades ago. To pretend that it hasn’t changed, and to continue ignoring the shifting landscape, will consign us to economic stagnation. That rules of the road issued in 1999 remain relevant today underscores just how little progress was made in the 2000s, and how much work needs to be done to fully bring America into the 21st century. Policy makers and stakeholders from across the political spectrum need to move beyond the talking points from another generation and embrace policies based on today’s realities.

The views expressed here do not necessarily reflect those of the Progressive Policy Institute.

On the heels of a severe recession, with stubbornly high unemployment and a still-sputtering recovery, economists and policy-makers are casting around for something — anything — that might jump-start economic growth and rapid job creation. One place we might expect them to look for ideas is our own economic history: Where have new jobs come from in the past? What is the pattern of recent economic recoveries?

As it turns out, job creation in the American economy comes disproportionately from new and young companies. Sluggish economic times, moreover, can be the cradle of entrepreneurship: Over half of the companies on the Fortune 500 were founded during a recession or bear market. Entrepreneurs are also responsible for introducing a large share of innovations that improve our standard of living.

One would think, then, that the conditions for job creation would be obvious: Avoid steps that would discourage new companies from starting and that would make it as difficult as possible for them to grow. But alas, one would be wrong. In recent weeks, we have seen signs that policy-makers and legislators still have no clue how to solve the jobs dilemma.

An Assault on Startups?

First, Bloomberg BusinessWeekreported last week that the Internal Revenue Service (IRS) is targeting the use of freelancers and “perma-temps” by many firms. At issue is the classification as freelancers of workers who remain on a company’s payroll months and even years, a violation of the tax code. Because such workers offer flexibility and help reduce costs, many companies that use them are young and small. As Nick Schulz pointed out, this “assault” on voluntary work arrangements might not be the best idea when we’re interested in encouraging job creation.

Data from the Census Bureau and Bureau of Labor Statistics indicate that the average size of new firms has been shrinking by about one or two employees for several years. On one hand, that’s a potentially worrisome trend as it suggests a Red Queen effect whereby we need to start more and more new companies just to generate a steady level of jobs. On the other hand, as the BusinessWeek story pointed out, this trend also indicates that more new and young companies are using flexible employment — freelancers, independent contractors, temporary workers — as a way to help boost their chances of survival and growth.

Just last week the CEO of a young firm explained to me how he and his co-founder opened up their office space some time ago to anyone who wanted to come in and write software for them on a temporary basis. Some of those who did became full-time employees, while others ended up starting their own companies in the same office. It’s difficult to predict what effect the IRS action will have on new and young companies, but it seems safe to say that it won’t be the job creation elixir for which policy-makers are searching.

Another recent, admittedly less worrisome development was the appearance in the financial reform bill of some provisions that likely would have suppressed startup activity. One provision required startups that raised funding to register with the Securities and Exchange Commission and then wait four months for review. Another hiked the monetary thresholds for “angel investors” — wealthy individuals who play an increasingly important role in financing new companies — which could have worked to prohibit much startup financing.

The anti-startup and anti-angel provisions have since been watered down, but remain testaments to how easily and quietly we might kill the golden goose in this country. Who sits down and asks, How can I depress entrepreneurship today?

Entrepreneurship Essential to Any Recovery

These recent episodes take place against a backdrop of an apparently anti-startup zeitgeist taking shape. An impressionistic gaze at the landscape reveals an increasing tendency for policy-makers to focus on things large and well-established, even as our economy and society are driven more and more by the new and small.

One indication of this is well-known: The rush to bail out some of the biggest and oldest companies in the economy sent the wrong message to potential entrepreneurs. There was a compelling rationale to the actions to save General Motors and Chrysler, just as there was one to pour money into banks and other financial institutions. But the composite signal was perverse: bigger and older are better. The largest banks in the country now have a bigger market share than they did prior to the recession, and these aren’t necessarily the primary sources of financing for new and young businesses. The zeitgeist was expressed quite succinctly in the BusinessWeek story: “It’s easier and quicker to audit smaller businesses.” So there you go — ease trumps dynamism.

New companies and the jobs and innovations they generate are not silver-bullet solutions. Yet economic recovery surely won’t happen, or be as strong, without them. Entrepreneurship in the U.S. has been remarkably resilient for about 30 years, with a surprisingly steady level and rate of firm formation. While encouraging the formation and growth of more startups is clearly something that would boost economic growth, it’s not entirely clear how we might go about doing that. What is crystal clear, however, is that we could very well succeed in killing entrepreneurship if we don’t pay attention to what goes on in Washington.

The following is an excerpt from a column by Ed Kilgore in today’s New Republic Online:

The first thing you need to understand about Florida’s political climate is that its seemingly endless summer of Boom Times seems to be coming to a close. The vast migration to the state that caused its population to increase over 16 percent since the 2000 census seems to be winding down, and last year, shockingly enough, it actually lost population. The state’s economy is suffering from problems that are deeper than any business cycle: Its 2.7 percent drop in per capita personal income has pushed the state near the bottom of rankings by percent change of personal income data. State government and politics have followed suit, inaugurating a period of unhappy partisan and ideological wrangling with no clear outcome in sight.

Many of the troubles resemble the problems of Florida’s distant political cousins, Arizona and Nevada, both Sunbelt areas with significant retiree populations that have also been hit by an economic triple-whammy of rapidly declining housing values, reduced tourism, and eroded retirement savings. Not surprisingly, all three have developed volatile, toxic political climates this election cycle. (In Nevada, the only politician who is perhaps less popular than the Harry Reid is the Republican governor, Jim Gibbons. In Arizona, the 2008 Republican presidential nominee, John McCain, whom you’d expect to be riding high along with the GOP’s national renaissance, is scrambling to the right to survive a primary challenge by a defeated former congressman and radio talk show host, J.D. Hayworth.)

In addition, Florida has certainly suffered from the global economic slump because it is a major magnet for foreign investment. It also shares some of the structural problems of its otherwise very different Southern neighbors, particularly chronic underinvestment in public education. And when it comes to the fiscal and political consequences of a bad economy, Florida is one of just a handful of states with no personal income tax, which has made property-tax rates on steadily decreasing real estate values a red-hot issue (a billion-dollar deal that allowed the Seminole Indian tribe to expand its gambling operations was one of the only things that allowed legislators to balance the latest state budget).

So the question is, what does this mean for Charlie Crist, the erratic and heavily-tanned governor who is throwing the calculations of both major political parties into chaos? And what does it mean for Democrats, whose electoral future continues to depend, in part, on the whims of Florida’s diverse and fickle voters?

We’ve heard a lot of doom and gloom on environmental topics recently, with progressives providing dark statistics about escalating carbon levels and conservative rebutting with stormy predictions of economic eclipse.

But Earth Day is supposed to be a feel-good day. And, as Thomas Friedman argued yesterday, when you start winning, everything becomes easier. That’s why President Obama’s victory on health care helped led National Security Advisor Jim Jones’ to declare that “America is back” on the world stage.

So it’s fitting that Vice President Joe Biden yesterday announced just under a half-billion dollars worth of stimulus monies for efficiency retrofits. In a little over a year, the administration has won a surprising number of victories in the push to mine “negawatts” through efficiency. Where we were slouching toward disaster through the laissez-faire, do-nothing inertia of the prior administration, we are now plowing toward a brighter, cleaner horizon.

Among other highlights, Biden announced that $20 million will be distributed to cities in the southeastern states of Alabama, Florida, Georgia, North Carolina, Louisiana, South Carolina, Tennessee and Virginia to dramatically increase the effectiveness of retrofits across the region. The new programs will use a pay-for-performance approach to finance affordable, accessible programs for both small and large residential, commercial and public buildings. But that’s just one of dozens of programs spread through Boulder to Camden, Cincinnati to Seattle.

What’s not to like? These projects pay for themselves. They work with local and state governments to quickly upgrade buildings. They employ local workers and are the quintessence of “shovel-ready.” And perhaps most importantly, they showcase in very public ways the powerful nexus of public works and progressive policy. These are wins — and, hopefully, preludes to victory this summer, as the administration and Congress turn to the effort to price carbon.

As the Senate turns to financial reform this week, the big question is whether any Republicans will join in, or whether the party will stick to its new political doctrine of Maximum Feasible Obstruction.

This doctrine is predicated on the idea that Barack Obama, elected with nearly 53 percent of the vote, is a dangerous radical bent on extinguishing American liberties and importing Euro-style social democracy. It’s an idea so crazy on its face that many progressives are convinced that racism must lurk behind it.

Maybe, but some conservatives also convinced themselves that Bill Clinton maintained a secret airport in Arkansas to import narcotics from Central America. The right’s feral attacks on Clinton led a sympathetic Toni Morrison to dub him in a figurative sense “America’s first black president.”

Whether or not race is a factor, Republicans have evidently calculated that there is no political cost in withholding cooperation from Obama, at least on domestic issues. That may have been true of health care, which lost public support as the debate wore on. But fixing Wall Street is another matter.

The Pew Center for Research reported yesterday that Americans overwhelmingly favor (by 61-31) reform of financial rules, even as they evince growing skepticism of government activism. It’s pretty clear the public takes a “never again” stance toward bailing out Wall Street bankers, speculators and bonus babies.

That’s why Mitch McConnell, the GOP Senate leader, latched onto the theme that the bill crafted by Sen. Chris Dodd (D-CT) would actually make future bailouts more likely. President Obama blasted that “cynical and deceptive assertion” over the weekend, and McConnell yesterday seemed to back down.

Still, Democrats need Republican votes to bring a bill to the floor. The Washington Postreports this morning that Democrats are targeting Sens. Olympia Snowe and Susan Collins of Maine and Bob Corker of Tennessee. Bucking his party’s sullenly oppositionist temper, Corker has worked constructively with Sen. Mark Warner (D-VA) to offer sensible improvements to the Dodd bill.

That bill is snagged on GOP opposition to a new regulatory body, to be independent but lodged in the Federal Reserve, that would protect consumers of credit cards, mortgages and other loans from deceptive or predatory practices. Dodd has signaled a willingness to compromise on another controversial provision, an industry-financed $50 billion fund to liquidate bankrupt firms. And the New York Times reports today financial sector lobbyists have lavished contributions on members of the Agriculture Committee, which is grappling with a key provision to regulate derivatives.

During the health care debate, Republicans did not appear to be moved by the plight of Americans with no medical insurance. But financial reform involves something Republicans traditionally care deeply about – money. Where are the sobersided conservatives of yesteryear, who understood that the safety and soundness of our financial system is fundamental to America’s economic health? Striking the right balance between regulation and innovation, security and risk, is an urgent national priority that ought to engage responsible leaders in both parties.

If Republicans aren’t willing to set aside reflexive partisanship long enough to stand up for American capitalism, we really are in a world of political hurt.

Public trust in the federal government, Congress and the political parties is scraping rock bottom, the Pew Research Center reports today. The findings don’t invalidate what President Obama and the Democrats have done over the past year, but they do underscore the need for a new direction.

According to Pew’s Andrew Kohut, only 22 percent of Americans trust the government in Washington to do the right thing. Anger at Washington has intensified and, most important for progressives, the public seems to be souring on activist government. “…[T]he general public now wants government reform and a growing number want its power curtailed,” he says. The important exception is regulation of Wall Street, which Americans continue to favor by nearly 2-1.

Obama’s first year was dominated by the economic emergency and the Herculean task of passing a landmark health care reform. The administration had no choice but to spend prodigiously to prevent a general financial collapse and pump up a stricken economy. If you think the polls look bad now, imagine how much worse they’d be had Obama failed to take decisive action on the economic front.

The health care push may have been the domestic equivalent of a war of choice, in that Obama could theoretically have deferred it until the economy recovered. But it was the right choice for a president with large reserves of political good will, and for a Democratic Party finally given undivided control of the federal government and a mandate to tackle big problems.

There’s no denying the rising public backlash against government intervention and spending, though it probably has as much to do with lingering economic anxieties as what Obama and the Democrats have been doing. In any case, public sentiment for a smaller federal government has risen, while Democrats’ favorable ratings have tumbled 21 points to 38 percent, about the same as the GOP’s, says Pew. At the same time, the poll also shows that voters aren’t hobgoblins of consistency. Even as they complain about the influence of special interests, 56 percent also say government does not do enough to help average Americans.

Progressives shouldn’t lose too much sleep over the Tea Partiers, who are hardcore conservatives and extreme libertarians. But independents are another question. The Pew study confirms the trend of recent elections, which saw independents from Virginia, New Jersey and Massachusetts abandon Obama’s winning 2008 coalition. This portends a difficult midterm election for Democrats, since independents seem highly motivated to turn out in November and, according to Kohut, express strong preferences for Republican candidates in their district.

What can progressives do to staunch the defection of independent voters? They should pass financial reforms, reduce home foreclosures and get as much of the bailout money back as possible. But the main emphasis for the rest of the year should be on stimulating economic innovation and growth. They should pay particular attention to relieving regulatory burdens on entrepreneurs and new enterprises – including onerous paperwork requirements in the new health care law — which are the primary generators of new jobs.

Progressives also must lay the groundwork for serious deficit reduction and entitlement reform next year as unemployment subsides. The Obama administration should press hard on health reform’s new cost containment measures, and produce concrete plans for closing Social Security’s funding gap. It’s vital for them to show they can discipline federal spending, not just raise taxes.

Here the administration can learn from Bill Clinton’s experience. He too faced an electorate worried about public spending and deficits, and skeptical about suspicious of bureaucratic overreach. He not only produced budget surpluses (a feat Obama won’t be able to duplicate), but also gave priority to downsizing and “reinventing” the federal government.

Obama doesn’t need to echo Clinton’s assertion that “the era of big government is over.” But in this next phase of his presidency, he needs to be as ambitious in reforming government as he was last year in expanding government.

Americans are increasingly alarmed by the nation’s massive deficits. Yet according to a new CNN poll, 60 percent favor making the Bush tax cuts permanent, instead of letting them expire this year. This doesn’t compute. If President Obama is to make any headway in restoring fiscal discipline in Washington, he will have to inject a note of realism into the debate over taxes and spending.

Here’s the blunt truth: the federal government faces a huge revenue hole – too big to be closed by spending cuts alone. Spending last year reached an astonishing 26 percent of national output, while revenues fell to 15 percent. Full economic recovery is expected to cut that yawning tax gap of 11 percent roughly in half.

Getting federal deficits down to a sustainable level – say 3 percent a year – will require both spending cuts and tax hikes. The president’s deficit-reduction commission will have to look hard at entitlement spending, but we will also need a sweeping overhaul of our tax system to solve our fiscal crisis.

Extending all the Bush tax cuts, of course, will only dig us in deeper. The Congressional Budget Office estimates that extending them through 2017 would cost $1.9 trillion. That doesn’t include the costs of servicing a bigger national debt, or the cost of adjusting the alternative minimum tax so it doesn’t offset the cuts.

Obama pledged during the campaign to keep the Bush cuts for households making under $200,000 a year. He will either have to break that very expensive promise, or turn to other possible revenue sources. What are the options?

The first, and most attractive, is to go after the hundreds of billions of tax subsidies that range from specific industry tax breaks to broader provisions – like the health care exclusion and mortgage interest deduction – that benefit all taxpayers. This is the essence of an intriguing bill crafted by Sens. Ron Wyden (D-OR) and Judd Gregg (R-N.H.), which would broaden the tax base by eliminating all itemized deductions except for mortgage interest and charitable deductions.

Another option is to look for new revenue sources. The best would be a charge on carbon, which would raise revenue, boost clean energy investment and protect the earth’s climate all in one fell swoop. The emerging Senate climate and energy compromise, engineered by Sens. Kerry (D-MA), Graham (R-S.C.) and Lieberman (I-CT), would cap carbon emissions, but it appears that the revenues would be rebated to the public. This approach would blunt Republican charges that putting a price on carbon is tantamount to raising taxes in a weak economy, but it wouldn’t close our revenue gap.

That’s why there’s rising interest in a value-added tax (VAT). Paul Volcker, the éminence grise of high finance, floated the idea recently. It’s also been endorsed by leading progressive thinkers like Isabel Sawhill and Henry Aaron of the Brookings Institution. A VAT has traditionally been seen as a harbinger of European-level taxes, but Sawhill believes it may be the only way to finance health care. She adds:

In the end, any tax increase will be a heavy lift in a country that seems allergic to paying its bills. But it will have to happen sooner or later and sooner would be much better. As Larry Summers once noted, Republicans don’t like value-added taxes because they are a revenue machine and Democrats don’t like them because they are regressive. We will get a VAT when Democrats realize they are a revenue machine and Republicans realize that they are regressive.

A recent post highlighted the importance of new and young companies to job creation in the U.S., implicitly raising an important question for policy makers: How can we increase the number of startups? Assuming it can be done, such an increase would not solve all of the economic challenges facing this country, but it would certainly help. New companies not only create millions of jobs across all sectors of the economy — they also introduce product and process innovations, boosting overall productivity.

Saying startups are important is one thing, of course; actually designing policies to increase their number is something else entirely. Before making any recommendations, for example, we need to know more about the universe of startups. Are they more prominent in some sectors than others? Does the impact of new companies differ across sectors or geographic regions? Should policy focus on encouraging more new firms, or on enhancing the growth of those already in existence? How would any such policies affect established companies, large and small?

Policymaking around entrepreneurship is evidently not clear-cut as there is still quite a bit we do not understand regarding startups. In the coming weeks we will try to explore these questions and illuminate the world of startups for policymakers. We’ll start with the lowest-hanging fruit of all, though one that may seem like poison to some in Washington: immigration.

It’s commonly accepted that the United States is a nation of immigrants, settled and populated by those fleeing persecution, seeking commercial opportunities in a new land or looking for a fresh start. We have always recognized the important contributions of immigrants to the U.S. economy, from entrepreneurs like Samuel Slater (textile mills) to Andrew Carnegie (steel) to Andy Bechtolsheim (Sun Microsystems) to the laborers and workers who built this country with their hands.

Recently, researchers have begun to paint a broader picture of the economic role of immigrant entrepreneurs. For example, Vivek Wadhwa and his research team have found that, from 1995 to 2006, fully one-quarter of new technology and engineering companies in the U.S. were founded by immigrants. In Silicon Valley, the figure was one-half. These firms constitute only a sliver of all companies, yet contribute an outstanding number of jobs and innovations to the economy.

It makes sense, then, that if we are seeking to increase the number of new companies started each year in the U.S., we might look to immigrants. It turns out that Sens. John Kerry (D-MA) and Richard Lugar (R-IN) are thinking precisely along these lines, introducing the StartUp Visa Act (PDF) in the Senate. This bill would grant a two-year visa to immigrant entrepreneurs who are able to raise $250,000 from an American investor and can create at least five jobs in two years. Without question, such a visa is a good idea and this legislation hopefully paves the way for future actions that would reduce the pecuniary threshold and focus more on job creation.

Quite naturally, however, the promotion of immigrant entrepreneurs arouses suspicion among those on the right who harbor nativist views, and those on the left who perceive progressive immigration policies as a threat to American labor. Such views take the precisely wrong perspective: immigration, as we have seen, is a core American value. Immigrant entrepreneurs, moreover, come to the U.S. to make jobs for Americans, not take them.

Further, many of those who promote immigration as a way to boost economic growth narrowly focus on “high-skilled” entrepreneurs, those who might start technology companies. Clearly, as Wadhwa’s research indicates, such companies are important to American innovation. But we exclude non-technology entrepreneurs at our peril — every new company, including those founded by immigrants, represents pursuit of the American dream. By closing our borders to immigrants in general or welcoming only those with certain skills, we leave out many who will start new firms in other industries. If not in the United States, they will go elsewhere to start their companies and create jobs.

Entrepreneurs are implicit in Emma Lazarus’ poem: “Give me your tired, your poor/Your huddled masses yearning to breathe free.” Entrepreneurs start from nothing and work endlessly to build their companies, expressing their individual freedom through commerce. Why should we want to exclude them from the home of entrepreneurial capitalism?

A distinct sense of unease permeates the traditional spirit of American optimism. The unemployment rate appears stuck at 9.7 percent, and many project that it will fall to around only eight percent by 2012 and to perhaps five percent by the middle of the decade. Disquiet over jobs is joined by a vague fear that the U.S. has lost its edge in innovation: our companies are losing ground to emerging market competitors and our students are falling behind their peers in other countries. In a recent post, Michael Mandel put these two concerns together, saying our jobs crisis is simultaneously an innovation crisis.

In response, a common impulse in Washington has been to call on the federal government to somehow solve both problems together, whether by creating “green” jobs, directing more money into research and development, or, most distressingly, provoking a trade war with China. Yet the real solution to both crises — the way to create more jobs and innovation — is right in front of us: startups. As New York Times columnist Thomas Friedman wrote recently: “Good-paying jobs don’t come from bailouts. They come from startups.”

Americans start new companies at one of the highest rates in the world, a pace that has been consistent for nearly 30 years. This steady stream of new companies was responsible for nearly all net job creation over that period of time, and many of those startups introduced new innovations into the economy, whether personal computers (Apple), productivity-enhancing software (Microsoft), 24-hour news (CNN), biotechnology (Genentech) or web browsers (Netscape).

The empirical evidence on the importance of startups is compelling, but not everyone is buying it. Responding to Friedman, for example, Dean Baker wrote:

Friedman’s conclusion about the special importance of new firms is utter nonsense. The claim that most net new jobs came from new firms conceals the fact that existing firms added tens of millions of jobs in this 25-year-period. Of course existing firms also lost tens of millions of jobs. We can say that the net job creation for existing firms was zero, but if we did not have an environment that was conducive for the job adders to grow (how many jobs did Microsoft, Apple, and Intel create after their first 5 years of existence?), then existing firms would have lost tens of millions more jobs.

There are basically two ways to look at job creation in the economy: gross and net. Large existing companies hire thousands of people each year, but they also see thousands of people leave. Gross job inflows and outflows in the American economy are enormous, an indicator of the ongoing reallocation of resources that drives economic growth. At the end of the day, however, if we want to keep pace with an expanding labor force (new entrants) and a changing economy (the rise and fall of sectors and companies), what matters is net job creation. It would be little consolation if we had 100 people looking for jobs, and large company ABC hired those 100 people but also fired 100 different people.

Many people prefer the (ostensible) comfort of big, established companies to the unpredictability of startups. Sure enough, while new companies create thousands of jobs each year, they also destroy thousands of jobs, whether through their effect on existing firms or through failure. (Roughly a third of new firms close in their first two years.) But these firms are important, too, in that they provide one of the few sources for big companies to draw on in adding jobs: in many cases a big company can only add net jobs by acquiring a new firm.

In addition to jobs, startups are an important source of innovation for the economy, responsible for a disproportionate share of breakthroughs. Big companies inevitably become locked into a cycle of quarterly earnings and long-term investments, leaving little room to pursue fringe ideas. Startups have the freedom to explore ideas at the frontier and succeed (or fail) in commercializing them.

This is not to say that large, established companies are unimportant. Far from it — the U.S. economy derives important strength from the symbiosis between startups and big firms. But if policy drifts too far in protecting big companies (whether through bailouts or certain types of regulation), it could suppress the number of startups. Just as importantly, should policymakers choose to focus on promoting entrepreneurship, it’s not clear that we can pick and choose certain sectors. The high-technology companies mentioned above garner much of the attention, but we see plenty of new firms emerge from seemingly mundane sectors such as retail and restaurants. We should reserve judgment on the types of startups we wish to see: every new company represents a source of renewal for the economy.

None of this means that startups represent the saving grace of the American economy; there is no silver bullet solution, to be sure. But, just as plainly, economic recovery will not happen without them. To begin creating our economic future, we need to start more new companies.

It’s considered gospel truth in many conservative circles that the American Recovery and Reinvestment Act of 2009, a.k.a. the “economic stimulus package,” was just a porkfest aimed at buying votes or rewarding Democratic constitutencies at the expense of good, virtuous taxpayers and their grandchirren. In support of this hypothesis, Veronique de Rugy of George Mason University’s Mercatus Center, and a regular contributor to conservative and libertarian magazines and web sites, recently wrote a “study” designed to show that ARRA dollars went disproportionately to districts represented by Democrats and/or that voted for Obama in 2008, regardless of their actual economic needs. De Rugy helpfully touted her study at National Review’s The Corner yesterday, for the edification of those who look to that blog for talking points.

Looks like she should probably have kept the paper to herself. Nate Silver of 538.com took a look at it, and pretty much demolished it today.

Turns out that de Rugy didn’t notice, or didn’t mention, that most of the “Democratic districts” that show up in her study as the top recipients of ARRA dollars happen to contain state capitals. Thus, ARRA spending designed to benefit states as a whole (the Medicaid super-match, school improvement incentives, state infrastructure grants, the state “flexibility” funds, etc.) are attributed by her to individual districts. She also ignored economic indicators showing poverty and local unemployment, which may or may not be correlated with Democratic voting habits, but which certainly indicate actual need.

I hear through the grapevine that de Rugy plans to respond to Nate’s demolition job at some point. If she manages to climb out of this crater, I’ll certainly be impressed.

The larger point, though, is that without Nate’s intervention (and perhaps even after it), conservatives would be gleefully citing de Rugy’s bottom line “findings” as “proof” that ARRA was what they always said it was. She is, after all, an academic thinker, and her “study” is impressive-looking, with lots of footnotes and scatter plot charts. I’m not saying that conservatives are alone in conducting this sort of skewed and deeply flawed “research,” or in citing it without examination. But that doesn’t excuse it for even a moment, particularly when the “researcher” is out there circulating the stuff as agitprop for the chattering classes before the ink is even dry.

Longtime political reporter Tom Edsall has a long and fascinating piece of analysis up at The Atlantic on the present and future shape of the two major party coalitions. While none of the data he discusses is terribly surprising, he does suggest some real internal problems with the emerging Republican coalition, which is increasingly made of up married white folks, but includes those who are “haves” only because they “have” government benefits that are perceived as vulnerable to budgetary competition from “have-nots”:

It’s entirely possible that, if the deficit forces continued zero-sum calculations, the definition of the center-right coalition of “haves” will be expanded beyond its original boundaries, stretching past the wealthy, the managerial and business class, the gun owners, the anti-taxers, the home schoolers, the property rights-ers, the Western ranchers, Christian evangelicals, and the self-employed to begin to include members of what conservative operative Grover Norquist called the “takings” coalition — men or women who get federal benefits. A Republican Party hungry for victory would welcome as new members Social Security and Medicare recipients — “takers” who simultaneously consider themselves part of the universe of “haves” and of Norquist’s “leave us alone coalition.”

Add in people who are self-consciously dependent on federal defense spending, and you can see how a Republican coalition of public- and private-sector “haves” could be formidable if not terribly stable.

Demographic trends, though, are very dangerous for the GOP, as this Edsall nugget shows:

While there is no doubt that the increase in the number of racial and ethnic minority voters works to the advantage of the liberal coalition, white voters remain a wild card. In 2008, whites made up 74 percent of the electorate, and McCain carried them 55-43. There are precedents for much higher Republican margins: in 1972, Nixon carried 67 percent of the white vote, and in 1984 Reagan won 64 percent. Conversely, Bill Clinton only lost the white vote by one percentage point to George H. W. Bush in 1992. The one clear conclusion to draw from these figures is that if the GOP is unwilling to make major policy shifts, especially on immigration reform, a crucial issue to many Hispanics, the party will have to drive its margins among white voters back up to the Nixon-Reagan levels.

If anything, the current pressure on the GOP from its rank-and-file, including the Tea Party Movement, is in the opposite direction from any position on immigration policy that could attract Hispanics. So there will be a strong temptation on the Right for indulging heavily in what might be called White Identity Politics. In light of Edsall’s insight on the “haves” in the GOP coalition who are dependent on government spending, White Identity Politics could involve racially tinged distinctions between the “deserved” government benefits received by white middle-class retirees and the “undeserved” government benefits received or sought by poorer or darker folk. That’s a dynamic that’s already been abundantly apparent in the Republican assault on health reform.

Looks like today’s political turbulence will be with us for quite a while, particularly if relatively high unemployment and budget deficits persist, accentuating the zero-sum politics of group competition that Edsall sees in the data.

A little over a week ago, I praised Sen. Bob Corker (R-TN) for working with Sen. Mark Warner (D-VA) to come up with some bipartisan improvements to the financial regulatory reform package that Senate Banking Committee Chair Chris Dodd (D-CT) is looking to get through the Senate in time for Memorial Day. I may have spoken too soon. Corker said yesterday:

“I couldn’t support the bill in its current form,” Mr. Corker said in an interview with The Wall Street Journal. “I am absolutely not throwing in the towel. I have no plans to support the current legislation. I hope we’ll get back to the negotiating table.”

This is, of course, a familiar tactic. After a year of being actively courted by the administration and Democrats, congressional Republicans claimed they couldn’t support health care reform, but were willing to stall further by espousing an interest in negotiating. But despite Corker’s backing away from a bill that as recently a last week he said he thought was going to pass, it’s worth sticking to the principle of a bill with bipartisan ideas.

The big idea that Warner and Corker worked on was including an autonomous Consumer Financial Protection Agency (CFPA) as part of the Federal Reserve System. While sticking the CFPA in the Fed is an ungainly solution, it does have the benefit of giving the CFPA start-up funding through the Fed’s balance sheet. Additionally, creating a brand-new agency out of the parts of others does have the chance of echoing the struggles the Department of Homeland Security had getting off the ground, a fate a Fed-housed CFPA can avoid.

Senate Democrats shouldn’t bend over backwards and try to pass a flawed bill in the hopes of convincing Republicans to get on board. But neither should they give up on looking for broad-based support for meaningful reform.

Mike Konczal’s inequality post as a guest blogger for Ezra is getting a bit of attention in the blogosphere. Konczal jumps off of an interesting post by Jamelle Bouie to argue that contrary to those who argue that “inequality isn’t so bad,” the unhealthy nature of the cheaper food that is purchased by the poor negates the fact that the poor face a lower inflation rate. Since he suggests I (and Will Wilkinson) think that “inequality isn’t so bad,” I wanted to correct a misconception that Konczal has about the argument of economist Christian Broda that he is responding to. Broda’s actual argument really doesn’t have anything to do with how healthy the things purchased by the poor are.

Mike Konczal’s inequality post as a guest blogger for Ezra is getting a bit of attention in the blogosphere. Konczal jumps off of an interesting post by Jamelle Bouie to argue that contrary to those who argue that “inequality isn’t so bad,” the unhealthy nature of the cheaper food that is purchased by the poor negates the fact that the poor face a lower inflation rate. Since he suggests I (and Will Wilkinson) think that “inequality isn’t so bad,” I wanted to correct a misconception that Konczal has about the argument of economist Christian Broda that he is responding to. Broda’s actual argument really doesn’t have anything to do with how healthy the things purchased by the poor are. An army of census takers has begun knocking on doors all across the country, following up on the 48 million households who didn’t send in very user-friendly forms in spite of a ubiquitous media campaign. There must a better, cheaper and even safer way to do this.

An army of census takers has begun knocking on doors all across the country, following up on the 48 million households who didn’t send in very user-friendly forms in spite of a ubiquitous media campaign. There must a better, cheaper and even safer way to do this. So far, we’ve established the absolutely

So far, we’ve established the absolutely

The first thing you need to understand about Florida’s political climate is that its seemingly endless summer of Boom Times seems to be coming to a close. The vast migration to the state that caused its population to increase over 16 percent since the 2000 census seems to be winding down, and last year, shockingly enough, it actually