The perverse joke at the heart of so-called reality TV is that it is totally fake — full of cartoonish heroes and villains and contrived dramas. Just like pro wrestling, the Trump presidency, and this week’s Republican National Convention.

It was a slickly produced, flag-bedecked exercise in mass delusion. In the squalid, everyday reality of his presidency, Donald Trump is a fumbling, dissembling, chaotic mess of a “leader” whose MO is denying the nation’s most urgent problems and deflecting blame on others for his failure to manage them effectively.

In the spectacle of the last four nights, however, Trump was anointed America’s only hope for salvation. Speaker after speaker extolled a beaming Trump for his “decisive action” against COVID-19, an inversion of reality that would make George Orwell dizzy. In his acceptance speech last night, Trump lauded himself, with characteristic hyperbole, for having ordered an “unprecedented national mobilization” against the “China virus,” even as the United States leads the world in COVID-19 deaths and infections.

The week featured what you would expect from the Trump Party: a Niagara of lies about the fictitious evils stalking America — socialism, anarchy in the streets, a plot to abolish the suburbs, Chinese leaders who deliberately loosed a deadly disease on the world, the betrayal of U.S. workers and assaults on religion and gun rights, etc. — and about Trump’s supposedly heroic, solitary battles on behalf of embattled Americans who still love their country.

The most overtly bigoted president in modern U.S. history trotted out people of color to pay tribute to his color-blind compassion, and Trump shamelessly repeated his risible claim to have done more for Black Americans than any president since Abraham Lincoln.

In cult-like fashion, family members and administration flunkies parroted the Great Leader’s own talking points, such as his easily disproven claim that Trump had built the “greatest economy in world history” before the Chinese bushwacked him with the coronavirus. In the absence of a record of real accomplishments to run on, as Barack Obama said at the Democratic Convention, Trump just “makes stuff up.”

It is a tale of two worlds. In Real World, the COVID scourge continues to inflict massive human suffering and economic costs on the American people. More than 177,000 Americans have died. More than 5.7 million have been infected. These are by far the largest tolls in the world. No wonder the U.S. economy is now a basket case.

More than 22 million jobs were lost in April alone, and many more in March and May, yet only 42% of those jobs have returned. Even with so many jobless Americans waiting to go back to work, job growth has slowed with July employment less than half that of June, and August looking weaker still.

This is the worst job market since the Great Depression. Yet after more than almost nine months, the Trump administration still does not have a coherent or effective national COVID-19 strategy, and Senate Republicans went on vacation rather than pass unemployment extensions for millions of jobless Americans.

But as his convention continues, the president seems to reside in Trump World, a land of alternative facts where everything appears fine. Late last week, Trump called his presidency the “most successful period of time in the history of our country, from every standard” and said his administration has “demonstrated over the last four years the extraordinary gains that are possible.”

Meanwhile, this week heatwaves, wildfires and hurricanes, all made much worse by climate change, are devastating communities and making life unbearable for tens of millions of Americans across the country.

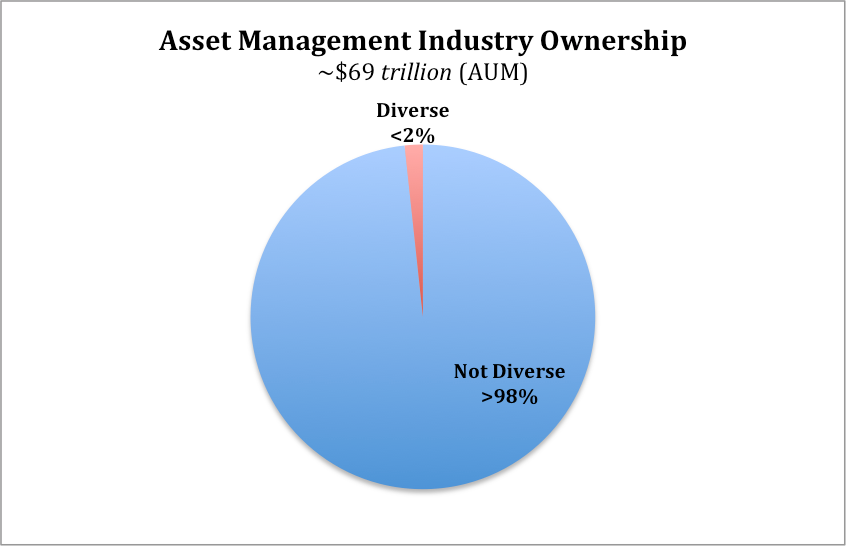

In July 16 the Securities and Exchange Commission (SEC) hosted a discussion on improving diversity and inclusion within the asset management industry.

The SEC doesn’t have a long history of using its powers to focus on diversity, but SEC Chairman Jay Clayton sounded an optimistic note: “We should continue to ask ourselves how we want participation and representation in our markets to evolve, at all levels,” Mr. Clayton said at the meeting.

But government can’t do it alone. To wit- just 69 of 1,367 entities surveyed by the SEC in 2018 completed an assessment of their diversity policies and practices, according to the agency.

Some diversity advocates implored the SEC to increase pressure by declining to meet with firms that ignore its diversity surveys.

While the increase of these discussions by the government is welcome, withholding access to your government is never a good idea.

One chart explains the reason the SEC hosted this discussion

Why is this chart so important? It speaks to opportunity — which is the essential precondition of equality. Simply put, how can we expect investment capital to flow to minority and women entrepreneurs if it’s not flowing through the hands of diverse capital allocators?

Congressional Red Alert: Local governments need help — ASAP

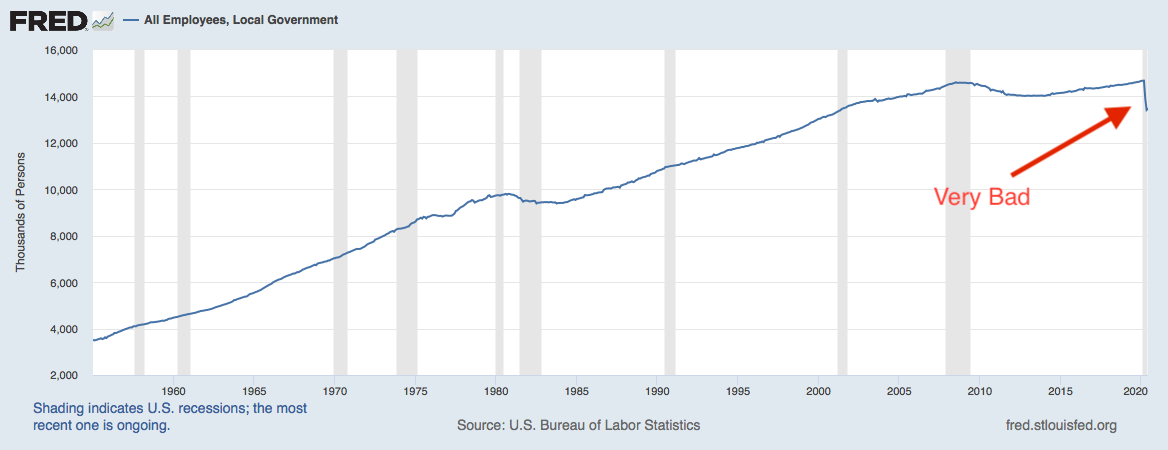

Still not convinced this recession is different? Take a look at this graph from the Federal Reserve of St. Louis:

This chilling drop-off is one of several reasons to get emergency funding directly to states and cities in the next stimulus package. The chart dates back to 1955 and shows that local governments who are hemorrhaging money are shedding jobs at a record pace. (Previous recessions are shaded)

In March 2020, local governments employed nearly 14.7 million people. Two months later that number dropped to 13.4 million with more cuts expected soon. Those job losses moved across various sectors including fire, police, teachers, and frontline healthcare workers.

How Amazon advances clean energy goals, while nurturing innovation and shareholder capital

Amazon announced it has teamed up with We Mean Business, a global non-profit working with business to accelerate the clean energy transition.

This push by Amazon is reflective of a larger trend by cash rich companies and is an important focus by businesses that have significant resources to allocate. If you dig closer, you will find more and more of these proposals have a capital investment component in clean energy technology. From the press release:

Climate Pledge signatories will explore investment opportunities, including through Amazon’s Climate Pledge Fund, in companies whose products and services will facilitate the transition to a zero-carbon economy.

New York uses green infrastructure investment to get its economy back on track

Amid a massive economic crisis on the heels of serving as America’s first Covid-19 epicenter, New York’s Governor Andrew Cuomo has forged ahead with plans for an historic solicitation of renewable energy via offshore wind farms. Combined with a $400 million multi-port public/private infrastructure investment, these actions are key components to get New York State’s economy back on track and progressing towards its mandate to secure 70% of its electricity from renewable sources by 2030.

“During one of the most challenging years New York has ever faced, we remain laser-focused on implementing our nation-leading climate plan and growing our clean energy economy, not only to bring significant economic benefits and jobs to the state, but to quickly attack climate change at its source by reducing our emissions.” Gov. Cuomo said.

Glaring omission in the CARES Act commission highlighted

Thornell, et al, make a pretty convincing case in Barron’s that the oversight commission for the CARES Act as currently constructed, is problematic to help get money needed to the 8.7 million employees of minority-owned businesses, hardest hit since the crisis began and overlooked in previous stimulus packages. Why? There are no minorities on the current commission. The solution according to the authors? Add more members to the commission, and this time- include minorities.

From the piece: “No requests were made of the Treasury Department and Federal Reserve Board to explore the array of economic implications for communities of color or inquire about possible strategies to address them. The Treasury and the Fed wield powerful economic tools to manage the pandemic’s devastation on businesses, workers’ livelihoods, family savings, and consumer confidence.”

Agreed. I highlighted similar inclusive governance challenges in an op-ed for The Hill in April arguing why Biden needs some diversity in key economic cabinet posts that have never been led by a minority.

Meanwhile… “Inside the Klubhouse”

The Institute for Diversity and Ethics In Sport (TIDES) at the University of Central Florida last week released its 2020 Racial and Gender Report Card for the NBA. Commissioner Adam Silver, owners, and players have been longtime leaders on social issues among all mainstream sports, so these results are no surprise:

Case in point from the San Antonio Spurs last week. Coach Gregg Popovich, a 5x Champion, top 3 all time, future hall of fame coach, swapped roles with assistant coach Becky Hammon, who took over head coaching duties for the Spurs against the Milwaukee Bucks.

The outbreak of COVID-19, caused by the novel coronavirus, has created a global market downturn and put the United States on track for its first recession since the 2008 financial crisis. Quarantines, social distancing, and other proactive measures that are necessary to contain the pandemic are already limiting commerce and disrupting global supply chains, essentially ensuring that the U.S. economy will contract for at least some period of time in 2020.1 Policymakers must adopt a combination of thoughtful public health and macroeconomic policy measures that will limit the damage caused by both this and future recessions.

Congress has already taken two strong first steps. On March 6th, President Trump signed legislation that provided $8.3 billion in emergency funding for public health agencies and coronavirus vaccine research.2 Now the U.S. Senate is debating the Families First Coronavirus Response Act: a far more expansive bill carefully crafted by House Democrats to further bolster public health agencies and provide economic support to the people and businesses most likely to be harmed by the disease.3 This bill temporarily increases federal Medicaid and food-security spending, makes coronavirus testing available to patients free of charge, expands unemployment insurance benefits, mandates employees afflicted with the virus be given 14 days of paid sick leave, and creates a refundable tax credit to provide them with up to 12 weeks of additional paid medical leave, among many other things.4

Although these measures were a great start, much more will be needed. For example, the sick-leave mandate – which is essential for discouraging potentially infected employees from spreading the disease to their coworkers – covered just one fifth of workers after concessions were made to win Republican support.5 Many otherwise financially healthy businesses face the threat of going bankrupt as the crisis chokes off their cash flows, further increasing unemployment and perpetuating a vicious cycle of weakening demand.6 Millions of Americans may be unable to make their rent or mortgage payments, causing both homelessness and instability in the financial sector.

The Federal Reserve’s target interest rate has been reduced to zero percent, meaning it has already used its most potent tool for fighting a serious recession.7 But fortunately, low interest rates also make it cheaper than ever for Congress to borrow money to provide needed economic stimulus. Importantly, the current crisis is somewhat different than previous recessions in that most consumer spending will be constrained by limits on opportunities for commerce rather than a lack of money in their bank accounts. It is therefore more important than ever that stimulus money be targeted towards those who are most in need and most likely to spend. At the same time, a stimulus package must be aggressive enough to prevent an economic contagion that spirals into another financial crisis, or worse, a second great depression.

The best way to accomplish this goal is through the expansion of “automatic stabilizers” – policies that cause spending to rise or taxes to fall automatically when the economy contracts. These policies are more responsive to real economic needs because they are unconstrained by the political processes that often slow the passage of discretionary stimulus. Moreover, as the economy recovers, well-designed automatic stabilizers will actually reduce federal budget deficits and help pay back the debt that was used to finance stimulus.8 This proven structure prevents stimulus from being prematurely shut off (as it was following the 2008 financial crisis) and removes fiscal concerns as a political impediment to essential borrowing.9

This report provides a framework for new automatic stabilizers and other measures that will both combat the coronavirus recession and better prepare the United States for others that come after it. The Progressive Policy Institute recommends that policymakers prioritize giving relief to people who either lose their job or are already low-income, since both groups have a higher propensity to spend any money they receive than those who are economically secure. People and businesses should be given increased financial flexibility to inject liquidity into the market and prevent unnecessary bankruptcies during the crisis. The federal government should provide relief to cash-strapped state governments so that they are not forced to cut back their own spending and counteract federal stimulus. Finally, policymakers at all levels of government should cut taxes that discourage consumption, particularly those applied to industries hardest hit by the crisis.

Watching the nation’s political leaders tie themselves in knots over minor changes in gun laws, I can’t help but wonder if America hasn’t become the “pitiful, helpless giant” Richard Nixon warned about decades ago.

Nixon conjured up this arresting image to rally public support for his unpopular plan to invade Cambodia. But it seems more apt today, as Washington fails to stem the growing scourge of mass shootings.

The blunt truth is, the Republican Party is chiefly responsible for this paralysis of national will. Even as our children are slaughtered in classrooms, Republicans shrug and offer nothing more than “thoughts and prayers.” Sorry, they tell us, the U.S. Constitution bars us from taking effective action to protect our children from killers wielding weapons of war.

Read PPI President Will Marshall’s full piece on Medium by clicking here.

If you think your credit report is accurate, there is a good chance you are wrong. According to the Federal Trade Commission (FTC), one in five Americans has a potentially material error in their credit file, and one of the biggest contributors is medical bills—with half of all medical bills containing an error.

In fact, mistakes on credit reports have become so pervasive that around a third of all complaints filed annually to the Consumer Financial Protection Bureau (CFPB) resulted from problems with consumer credit reports.

Credit report errors are a serious threat to the financial well-being of American families. As Senator Elizabeth Warren has noted, “credit reports regularly contain errors that can make it harder for families to access credit, find jobs, and get housing.” And as many consumers know all too well, it’s very difficult to get those errors corrected.” (1)

Under the Fair Credit Reporting Act, the company that furnished the information to the credit bureau must conduct an investigation to verify the information and correct a mistake, if they find one. Unfortunately, consumers who want to try to fix mistakes on their credit report face three daunting obstacles.

First, the system put into place by the credit reporting agencies heavily favors creditors and other data furnishers. Credit bureaus almost exclusively depend on lenders (such as banks, credit unions, credit card providers, and mortgage underwriters).

Consumers contacted the credit reporting agencies approximately eight million times in 2011 to initiate a credit dispute. But only a small fraction of those disputes was resolved internally by credit bureau staff. According to the CFPB, 85 percent of credit report disputes are passed on to data furnishers (the lenders) to investigate and resolve. (2) Unfortunately, in most cases the disputes are then shelved unless the consumer perseveres.

Second, the credit report agencies earn their profits by providing services such as credit checks to the very entities that provide the data used to create the credit reports – banks, mortgage lenders, credit card companies, retailers, and other businesses that provide credit. This creates a serious conflict of interest.

Third, despite several notable efforts to try to empower consumers, trying to correct errors on your credit report is still tedious, confusing, and time consuming.

CREDIT REPAIR ORGANIZATIONS AND COMPANIES

Because the system is rigged against them, many consumers turn to credit counseling agencies or credit repair companies. The dispute system designed to help consumers fix the problem favors the position of the debt collector over the consumer. Specifically, the credit bureau is only legally required to check with the creditor or debt collector and ask them whether they stand by their claim. As long as the creditor says you owe money, the dispute is resolved in their favor. As the National Consumer Law Center concludes: “Credit bureaus have little economic incentive to conduct proper disputes or improve their investigations.” (3)

Credit counseling agencies are typically a free resource from nonprofit financial education organizations that review your finances, debt and credit reports with the goal of teaching you to improve and manage your financial situation.

A credit repair company is a firm that offers to improve your credit in exchange for a fee. Unfortunately, the quality of these firms varies greatly. Some credit repair firms are highly reputable and follow best practices. Unfortunately, a significant cohort of credit repair firms are not good actors and, in some cases, have committed outright fraud. In 2016 the Consumer Financial Protection Bureau (CFPB) stated that “more than half of people who submitted complaints with the CFPB about credit repair chose the issue ‘fraud or scam’ to describe their complaints.”

There are some telltale signs for consumers trying to separate the bad actors from legitimate credit repair firms. Companies should be avoided that:

Demand an upfront payment.

Don’t provide a written agreement that includes cancellation rights for consumers.

Guarantee they’ll raise your credit score or fix an error.

Have multiple complaints against them with the Consumer Financial Protection Bureau or the attorney general’s office in the state where they operate.

Suggest they can remove legitimate negative information.

Offer to create a new credit profile based on a new employer identification number, rather than your Social Security number.

In contrast, responsible credit repair companies not only follow federal and state law but also:

Offer a free consultation

Have a track record and consistently solid reviews from past clients.

Have an attorney on staff.

Are licensed, bonded and insured.

WHAT NEEDS TO CHANGE?

To protect consumers, some policymakers have suggested new regulations to further police the credit repair industry. They note that credit repair firms don’t do anything someone with a bad credit report couldn’t do on their own. Anyone can dispute credit errors on their own behalf. But the Do-It-Yourself approach can be dauntingly complicated and time-consuming for harried families.

In essense, paying for credit repair assistance is really no different than paying an accountant or purchasing software to do your taxes – something 90 percent of Americans do according to the Internal Revenue Service.

It is important to note that there is already existing legislation to regulate the credit repair system. The Credit Repair Organizations Act (CROA) was signed into law in 1996 to protect consumers from the unscrupulous practices commonly used by several credit scammers.

Because of CROA, credit repair organizations are not permitted to misrepresent the services they provide, including guaranteeing the removal of negative credit listings. Credit repair organizations are also not permitted to attempt to create a “new” credit file or advise you to lie about your credit history. The Act also bars companies offering credit repair services from demanding advance payment, gives consumers certain contract cancellation rights as well as the right to sue a credit repair organization that violates CROA. (4)

CROA is a sensible law, and despite criticisms that it does not go far enough in regulating the credit repair industry, the law does provide consumers with protections against bad actors in the credit repair sector without eliminating legitimate credit repair firms. CROA needs strengthening, not in the form of new regulations but rather more effective enforcement.

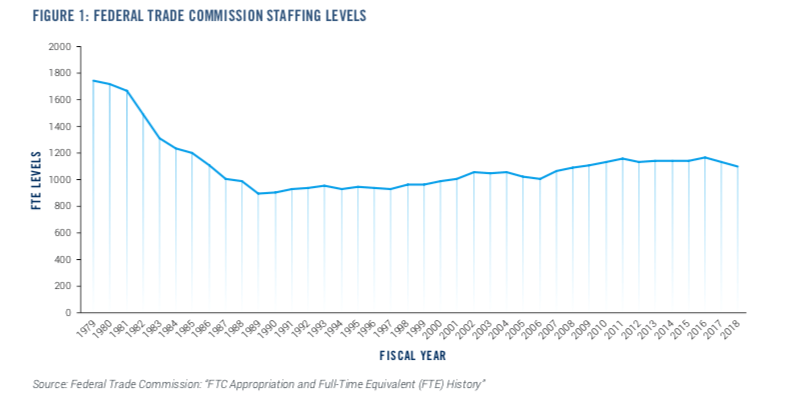

Under CROA, the Federal Trade Commission (FTC) is the primary enforcement body at the federal level. The problem is the FTC is severely underfunded and understaffed. In a Senate hearing last year Commissioner Rebecca Slaughter said the FTC’s staff level is 50 percent below its level at the beginning of the Reagan administration in 1981. Senators Jerry Moran (R-Kan.) and Catherine Cortez Masto (D-Nev.) agreed the FTC needs more resources and is “understaffed.” (5)

As Table 1 confirms, FTC staffing levels dropped dramatically during the 1980s and have never really recovered. Yet, over the same time, the responsibilities of the agency have dramatically changed and expanded. Today the FTC has to address some 2.7 million complaints a year in areas from debt collection, to identify theft, to imposter scams. (6)

Better enforcement of CROA would obviate the need to pile on new rules. Unfortunately, in fact, Congress has added to the FTC’s workload even as its workforce has shrunk. The simplest solution is to provide the FTC with additional resources dedicated to enforcing CROA and protecting consumers from those credit repair companies that have acted fraudulently or in bad faith.

To pay for this increase in supervisors, a small annual fee could be placed on the credit reporting agencies (Equifax, TransUnion, and Experian). To create an incentive for these agencies to be more responsive to consumer complaints about credit reporting agencies, the fee could be lowered or raised in synchronization with the number of consumer complaints about their credit reports.

OTHER REMEDIES

Another approach to fixing the current system is to go to the source of the problem, eliminating some of the causes for the extraordinary amount of errors made by the credit reporting industry. As Aaron Klein of the Brookings Institution has noted, there are three major reasons why credit scores are so inaccurate: “size, speed, and economic incentives of the system.”

One way to change the incentive structure would be to create some consequences for credit rating companies that frequently give lenders inaccurate data about borrowers. Lawmakers could consider legislation that would penalize credit reporting agency error rates above a certain level. Klein’s approach would use a random sample method (5 to 10 percent of complaints) to review credit rating firms’ performance. Another approach would be to grade the credit bureaus on their error and response rates.

CONCLUSION

While it is tempting to lump all credit repair firms into the same basket, many of these firms act in good faith and follow CROA to the letter of the law. Yet there is no doubt that a significant number of these companies are misleading consumers and sometimes acting fraudulently. If lawmakers really want to crack down on these bad actors, however, the first step should be strengthening enforcement of existing law.

Otherwise, spawning new laws and regulations would likely enmesh all credit repair firms in new layers of regulatory complexity and compliance burdens, making it even harder for consumers to detect and correct errors on their credit reports. In CROA we have the consumer protection law we need, now it’s time to focus on oversight and enforcement.

As the idea of “free college” gains popularity, Virginia and Iowa are instead focused on career and technical education.

In the midst of record low unemployment, many states are nonetheless struggling with ongoing skills gaps — shortages of workers with the right skills for in-demand jobs.

At the start of 2019, according to the Department of Labor, as many as 7.3 million jobs remained unfilled. These included a substantial number of “middle-skill” jobs requiring some schooling beyond high school but not a four-year degree. They were in fields such as health care, IT, welding and truck driving. The American Trucking Associations, for instance, reported a shortage of 50,000 drivers in 2017.

One reason these gaps exist is underinvestment in career and technical education. Of the more than $139 billion in annual federal student aid spending for higher education, just $19 billion goes to career and tech ed. Students generally can’t use federal Pell Grants to fund short-term, non-college-credit training programs, such as for welding certifications and commercial drivers’ licenses. Federal dollars under programs such as the Workforce Innovation and Opportunity Act are typically limited to the lowest-income workers.

Read Anne Kim’s full opinion piece in Governing by clicking here.

Is there room for a presidential candidate who stresses innovation and growth? Voters quite naturally want to see benefits from technology before they enthusiastically embrace more. As we have written in earlier reports, there are signs that digitization is starting to create new businesses and jobs in physical industries like manufacturing.

Another political argument for innovation and growth: The tech/telecom/ecommerce sector is still expanding at a rapid rate, benefiting both consumers and workers.

The tech/telecom/ecommerce sector grew by 7.3% in 2018, triple the 2.4% growth of the rest of the private sector. These figures–calculated by PPI based on the BEA’s newly-related 2018 industry GDP data— update our previous research that showed the tech/telecom/ecommerce sector far outperforming the rest of the private sector between 2007 and 2017.

Prices in the tech/telecom/ecommerce sector fell by 0.8% in 2018, compared to a 3% price increase in the rest of the private sector. That’s good news for consumers.

Perhaps more important is what we see on the labor side. Job growth in the tech/telecom/ecommerce sector exceeded job growth in the rest of the private sector, propelled by ecommerce fulfillment and delivery jobs, which added 178,000 FTE positions in 2018. If these new jobs are all assigned to the ecommerce sector, then tech/telecom/ecommerce FTE employment grew by 4% in 2018, compared to 2.1% growth in the rest of the private sector.

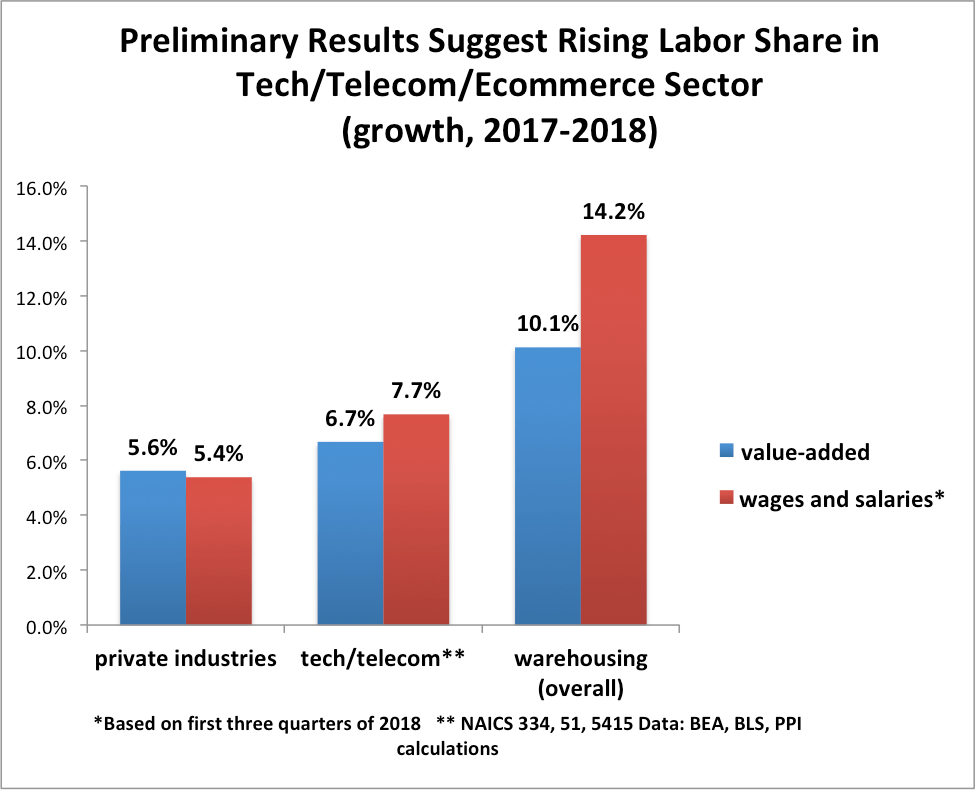

Finally, our preliminary calculations suggest that labor share rose in the tech/telecom/ecommerce sector in 2018, while falling in the broader private sector. We compared the percentage change in value-added with the percentage change in wages and salaries in the first three quarters of 2018, as reported by the BLS QCEW data. We found that value-added rose by 5.6% in the broader private sector, compared with a 5.4% increase in wages and salaries. To the extent that these trends continue in the fourth quarter and are reflected in compensation, labor share fell slight in the broader private sector.

By contrast, the available data points in favor of a rising labor share in the tech/telecom/ecommerce sector. For the purposes of this calculation we separated out tech/telecom from ecommerce, since the eventual ecommerce results will be greatly driven by the fourth quarter. For tech/telecom–computer and electronics manufacturing, software, telecom, communications, and Internet–value-added rose by 6.7% in 2018, compared to a 7.7% rise in wages and salaries. To the extent that these trends continue in the fourth quarter and are reflected in compensation, labor share rose in the tech/telecom sector in 2018.

We could not do a full analysis of labor share in ecommerce without the fourth quarter QCEW data, which is not available until June. However, we can look at warehousing, which is where ecommerce fulfillment centers are generally classified. We find that value-added in warehousing overall rose by 10.1% in 2018, while wages and salaries rose by 14.2% through the first three quarters. Assuming that these trends continue, there was a significant rise in labor share in the warehousing industry in 2018.

To emphasize: These are preliminary results, which may be revised substantially as new data comes in.

Political implications: In 2018, both consumers and workers were benefiting from the tech/telecom/ecommerce sector. Consumers were getting falling prices, and workers were getting faster job growth and a bigger share of the economic pie.

As digitization spread to other sectors, consumers and workers in those sectors will start sharing the fruits of faster growth. We suffer from too little innovation, not too much.

The U.S. economy is chugging toward a new record for longest expansion, and middle-class families, finally, are seeing decent wage gains. Yet our political leaders, as if stuck in a time warp, keep peddling a bleak narrative of economic victimhood and defeatism. 2020 is Democrats’ chance to channel and implement radically pragmatic, empowering, and innovative economic ideas.

On the other side, the Demsocs want Democrats to reject free enterprise in favor of a left-wing version of Trump’s splenetic and divisive populism. Instead, Democrats should channel the spirit of FDR and present voters with a hope-inspiring plan for how a reinvigorated private sector and government can work together to restore shared prosperity.

The global App Economy started in 2007, when Apple introduced the first iPhone. Apple’s opening of the App Store in 2008 – followed by Android Market (later renamed Google Play), Blackberry App World (later renamed Blackberry World) and other app stores – created a way for developers to write mobile applications (“apps”) that could run on smartphones anywhere. These apps became an essential part of daily life for most people – and an indispensable tool for business.

The rise of the App Economy has unleashed an abundance of “app developers.” These workers create, maintain, and support an ever-expanding range of apps. Mobile games are the most visible part of the App Economy, but certainly not the only component of it. Mobile apps include such key uses as shopping applications, home banking programs, smart automobile interfaces, healthcare apps for monitoring patients, and sophisticated apps for running manufacturing plants.

The extent of the App Economy workforce in a country reflects how quickly that country is embracing the next stage of the Information Revolution, which depends on mobile technology to digitize physical industries such as manufacturing and healthcare.

However, official economics statistics do not provide an easy way to measure the size of the App Economy. In response, PPI developed a methodology based on a systematic analysis of online job postings. In particular, we look for job postings that call for app-related skills such as knowledge of the iOS, Android, or Blackberry operating systems (though support for the Blackberry operating system is currently scheduled to cease at the end of 2019).

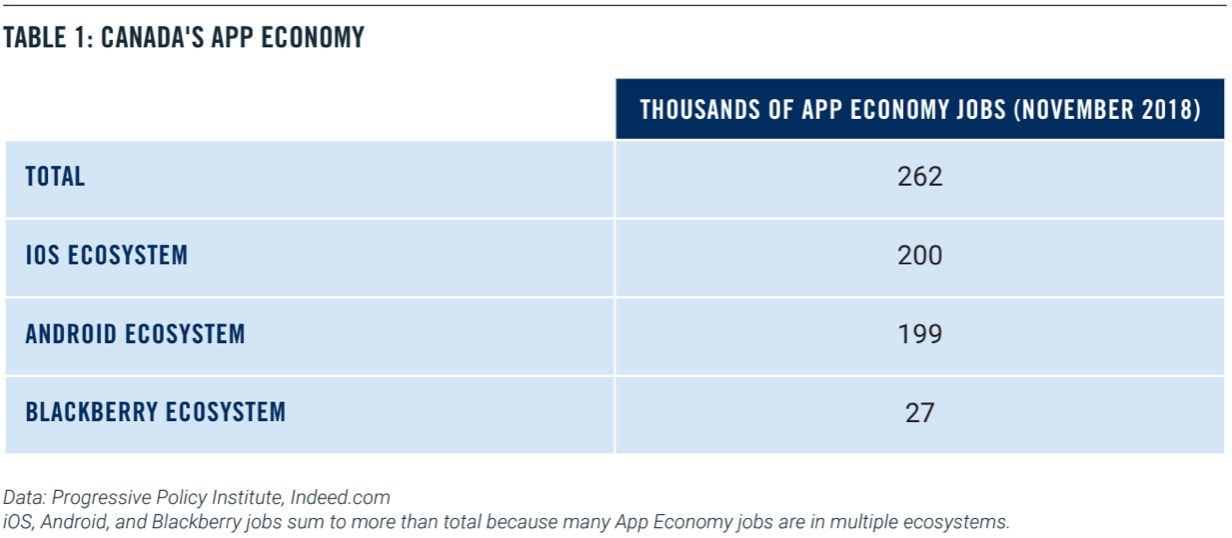

Based on this methodology, in this paper we provide an employment analysis of Canada’s App Economy. We provide an estimate of the total number of App Economy jobs; a breakdown of the jobs among iOS, Android, and Blackberry ecosystems; and an estimate of App Economy jobs by province. In particular, we estimate that Canada has 262,000 App Economy workers as of November 2018.

THE DEFINITION OF AN APP ECONOMY JOB

For this study, a worker is in the App Economy if he or she is in:

An IT-related job that uses App Economy skills – the ability to develop, maintain, or support mobile applications. We will call this a “core” App Economy job. Core App Economy jobs include app developers; software engineers whose work requires knowledge of mobile applications; security engineers who help keep mobile apps safe from being hacked; and help desk workers who support use of mobile apps.

A non-IT job (such as human resources, marketing, or sales) that supports core App Economy jobs in the same enterprise. We will call this an “indirect” App Economy job.

A job in the local economy that is supported by the income flowing to core and indirect App Economy workers. These “spillover” jobs include local retail and restaurant jobs, construction jobs, and all the other necessary services.

To estimate the number of core App Economy jobs, we use a multi-step procedure based on data from the universe of online job postings. Then the number of indirect and spillover jobs is estimated using a conservative job multiplier. The methodology is described in detail in previous research (2).

CANADA’S APP ECONOMY

Table 1 presents two pieces of information. First, we estimate Canada has 262,000 App Economy jobs as of November 2018. We also break down the total by ecosystem, finding the iOS ecosystem includes 200,000 jobs, the Android ecosystem includes 199,000 jobs, and the Blackberry ecosystem includes 27,000 jobs. The three sum to more than the total because many App Economy jobs belong to multiple ecosystems.

Using a different methodology, the Information and Communications Technology Council (ICTC) estimated total App Economy and related employment in Canada at 51,700 in its 2012 report, “Employment, Investment, and Revenue in the Canadian App Economy” (3). We infer from this that Canadian App Economy jobs roughly quintupled from 2012 to today. That’s consistent with what we have seen for the United States over the same time period.

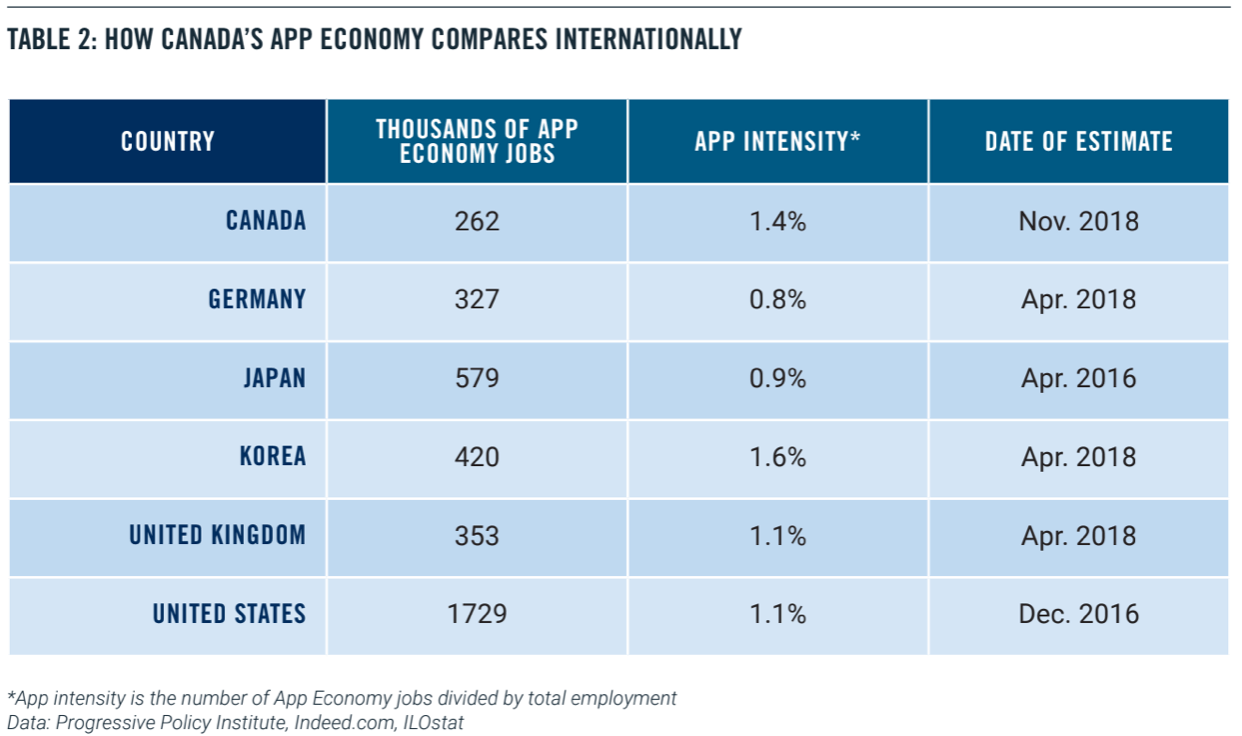

Now we compare Canada to some of its industrialized peers. In absolute numbers, Canada’s App Economy is relatively small. But, when we adjust for country size, Canada is doing very well. App intensity represents the number of App Economy jobs divided by total employment, where the latter figure is drawn from the International Labor Organization for standardization.

Canada’s app intensity of 1.4 percent ranks ahead of the United States, the United Kingdom, Germany, and Japan – and only slightly behind Korea.

Canada’s relative success can be attributed in part to its prioritization of digital connectivity and skills. Digital Canada 150 aimed to create jobs and economic growth by, among other things, connecting rural areas to high-speed Internet and investing in Canadian businesses and consumers through technology integration and skills development (4). Accomplishments include extending high-speed Internet to an additional 356,000 households, completing multiple spectrum auctions to improve wireless service, investing an additional $200 million to help entrepreneurs learn about IT technologies, and supporting up to 3,000 internships in high-demand fields. These types of policies help increase access to and employment in the App Economy.

GEOGRAPHIC DISTRIBUTION

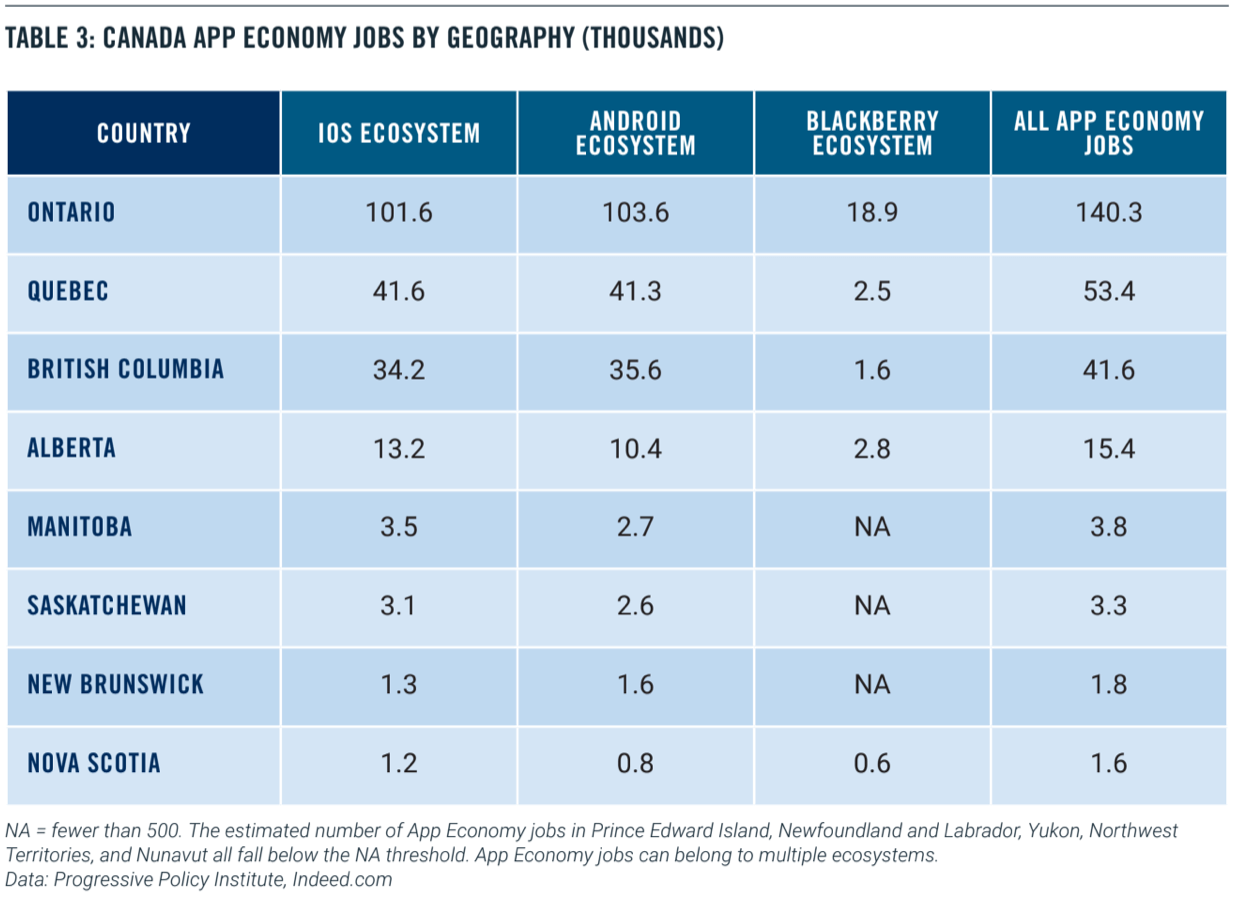

Our methodology also allows us to look at the geographic distribution of App Economy jobs by province – breaking out the different ecosystems. If we estimate fewer than 500 jobs in a region, we don’t report the number. Not surprisingly, Ontario leads in App Economy jobs, followed by Quebec and British Columbia. Also not surprisingly, the Blackberry ecosystem jobs are concentrated in the company’s home province of Ontario.

EXAMPLES OF APP ECONOMY JOBS

The Canadian App Economy is vibrant across a wide range of industries and geographies. As of October 2018, digital studio Adfab was searching for a front-end developer in Montréal with App Economy skills. Mobile device solutions firm Asset Science was seeking a mobile application developer with iOS and Android experience. Mango Software Inc. was looking for an Android developer in Montréal. IT firm CORE Resources was hiring a senior software engineer with Android experience in Mississauga.

Looking at Ontario in particular, as of October 2018, mapping software company Avenza Systems Inc. was searching for a full stack developer with experience in iOS and Android app development in Toronto. Life insurance company Manulife was seeking a senior Android developer in Kitchener. Digital billing company Sensibill was looking for a software developer with Android and iOS experience in Toronto. Household labor marketplace AskforTask was hiring a senior Android developer in Toronto.

As of October 2018, commercial contractor Flynn Group of Companies was hiring a mobile iOS developer in Mississauga, Ontario. Airline software firm NAVBLUE was seeking a software developer in Waterloo, Ontario. Fintech company Borrowell was looking for a React Native developer with experience building iOS and Android apps in Toronto. Consulting firm Neel-Tech Inc. was searching for an iOS developer in Mississauga.

In Quebec, as of October 2018, drone company Microdrones was hiring a senior Android developer in Vaudreuil-Dorion. Event app company Greencopper was seeking a mobile developer with iOS and Android experience in Montréal. Mobile payment company Mobeewave was searching for a mobile Android developer in Montréal. IT firm SolidByte was looking for a programmer with knowledge of iOS and Android programming in Montréal.

British Columbia has plenty of App Economy activity as well. As of October 2018, payment technology firm Alpha Pay was looking for an iOS or Android mobile developer in Richmond, British Columbia. Financial cloud company Global Relay was hiring a senior Android developer in Vancouver. Shopping app company StylePixi was seeking an iOS developer in Vancouver. Digital development firm Atimi was searching for a senior native mobile developer with iOS experience in Vancouver.

Considering Alberta, as of October 2018, GPS company Trimble Inc. was hiring a software engineer with iOS and Android experience in Calgary. Digital production firm Division [1] Media Corp was looking for a mobile app developer in Edmonton. The University of Alberta was searching for a lead software engineer with experience in Android and iOS in Edmonton. Aviation company Air Trail was seeking an intermediate iOS developer in Edmonton.

And the App Economy has spread even further. In Winnipeg, Manitoba, Pollard Banknote Limited – a leading supplier of instant lottery tickets – was hiring a senior applications developer with experience in mobile app development. In Saskatoon, Saskatchewan, Affinity Credit Union was searching for an iOS developer. In Fredericton, New Brunswick, Welltrack – a company that provides a suite of interactive self-help tools – was looking for a mobile developer. And in Bedford, Nova Scotia, IBM’s Client Innovation Centre was hiring a mobile application developer for iOS and Android.

Canadians are developing apps for the rest of the world, not only Canada. One well-known Canadian app that has spread globally is the messaging mobile app Kik, which was created in 2009 by University of Waterloo students and has 300 million users today around the world. Another example: Public transit app Transit was developed in Montréal in 2012. Today, Transit provides real-time crowdsourced data to users in 175 cities across the United States, Canada, and Europe. And well-regarded password manager 1Password, which was developed by Toronto-based AgileBits, has a global user base.

POLICY DEVELOPMENTS

As shown in this report, the Canadian App Economy has fared better in terms of scale than some of its industrial peers. Its growth since the introduction of the iPhone over a decade ago (and app intensity today) demonstrate the country is embracing the digital age and is well positioned to be a global leader. A few reforms could catalyze the next round of growth.

Unlike in the United States, where a patchwork of laws govern privacy, one law applies at the federal level in Canada – the Personal Information Protection and Electronic Documents Act (PIPEDA). But, while PIPEDA covers all health data, personal information, and employee information in one comprehensive structure, if a province has passed legislation deemed “substantially similar,” the province’s law prevails. For example, Alberta, British Columbia, and Quebec have laws in place that have been deemed substantially similar, thus serving as the prevailing law. But, as PPI has previously recognized, cross-border data flows means multiple regulatory regimes can be burdensome, unclear, and even contradictory for app developers – slowing the digitization of physical industries and economic growth.

The Canadian government began a review of its Broadcasting and Telecommunications Acts in 2018, with the intent of modernizing its legislative framework after the invention of new technology – particularly streaming services otherwise known as “over-the-top” (OTT) providers (5). OTT providers are those companies delivering video streaming, voice calls, or messaging via the Internet, without requiring users to subscribe to a traditional cable, satellite, or phone service. Policymakers should be cautious of taking a heavy-handed regulatory approach that would slow growth and, instead, should opt for a balanced approach that both promotes competition without jeopardizing the cost savings this technology has afforded consumers.

Lastly, according to the Information and Communications Technology Council’s latest ICT Labor Outlook, Canada will need an additional 216,000 ICT professionals by 2021 (6). Programs designed to incorporate and lower the cost of ICT skills development could help close this shortage. To that end, in their recent report on innovation and competitiveness, Canada’s Economic Strategy Tables recommend expanding on existing work-integrated learning opportunities, adopting portable competency-based credentials, and consolidating and streamlining skills and talent programming (7).

CONCLUSION

Canada has a vibrant App Economy that spans the iOS, Android, and Blackberry ecosystems. Compared to most of its industrialized peers, Canada’s app intensity is high, and represents a wide diversity of locations and jobs. Policy reforms such as streamlining privacy laws, taking a balanced regulatory approach when it comes to OTT providers, and closing the skills gap could help catalyze future growth.

1) PPI has issued App Economy reports on the United States, Japan, Vietnam, Indonesia, Korea, Thailand, Mexico, Brazil, Colombia, Argentina, Chile, and most of the countries of the European Union, including the United Kingdom, Germany, and France. Most notably, we have not yet issued reports on China and India.

2) A description of the methodology can be found in the appendix to Michael Mandel and Elliott Long, “The App Economy in Europe: Leading Countries and Cities, 2017,” Progressive Policy Institute, October 2017. https://www.progressivepolicy.org/wp-content/uploads/2017/10/PPI_EuropeAppEconomy_17.pdf

3) “Employment, Investment, and Revenue in the Canadian App Economy,” October 2012, Information and Communications Technology Council. https://www.ictc-ctic.ca/wp-content/uploads/2012/10/ICTC_AppsEconomy_Oct_2012.pdf

4) “Digital Canada 150,” Industry Canada. https://www.ic.gc.ca/eic/site/028.nsf/eng/home#item5

5) Canadian Heritage, “Government of Canada launches review of Telecommunications and Broadcasting Acts,” June 5, 2018. https://www.newswire.ca/news-releases/government-of-canada-launches-review-of-telecommunications-and-broadcasting-acts-684595661.html

6) “The Next Talent Wave: Navigating the Digital Shift – Outlook 2021,” Information and Communications Technology Council. https://www.ictc-ctic.ca/wp-content/uploads/2017/07/ICTC_Outlook-2021-ENG-Final.pdf

7) “The Innovation and Competitiveness Imperative Seizing Opportunities for Growth,” Canada’s Economic Strategy Tables. https://www.ic.gc.ca/eic/site/098.nsf/vwapj/ISEDC_SeizingOpportunites.pdf/$file/ISEDC_SeizingOpportunites.pdf

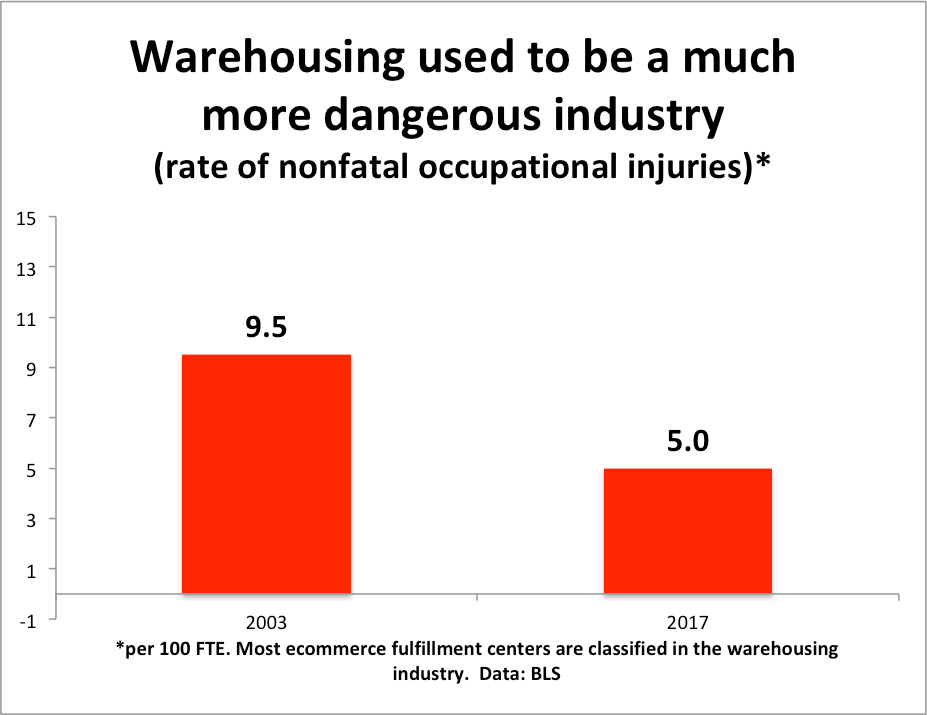

Worker safety is absolutely crucial. Driving down both nonfatal occupational injuries and workplace fatalities is one of the most important goals of government regulation. Since 2003 the rate of nonfatal occupational injuries and illnesses has dropped from 5.0 to 2.8 (per 100 FTE), according to a BLS survey.*

Despite this decline, jobs in physical industries are still more dangerous than office jobs. I say this as someone who respects the extra strain and danger faced by people who work in factories or hospitals, driving trucks or working on construction sites, or any other risky occupation.

From that perspective, I want to assess the current level of occupational injuries and fatalities in the warehousing industry. Driven by the rise of ecommerce fulfillment centers–which are mainly classified by the government as warehouses–this industry shown tremendous growth in recent years, creating jobs for hundreds of thousands of workers without a college degree. These are “mixed cognitive-physical” jobs: They require both physical labor, and also the ability to work with technologically sophisticated equipment.

One criticism of ecommerce fulfillment centers is that they are dangerous for workers. For example, we have all heard the story of how some workers in an Amazon fulfillment center in New Jersey were sent to the hospital after a can of bear mace fell off a shelf and discharged when a robot drive unit moved against it. Not a pretty picture!

But our question here: How does the safety record of the warehousing industry–including ecommerce fulfillment centers–stack up overall?

The first thing to note is that the rate of nonfatal occupational injuries in warehousing has fallen almost in half since 2003, going from 9.5 in 2003 to 5.0 in 2017 (per 100 FTE) (see chart below). The rate of nonfatal occupational injuries with lost days–a measure of the severity of the injury–has declined as well, going from 3.0 in 2003 to 1.8 in 2017 (once again, per 100 FTE) (not shown in chart).

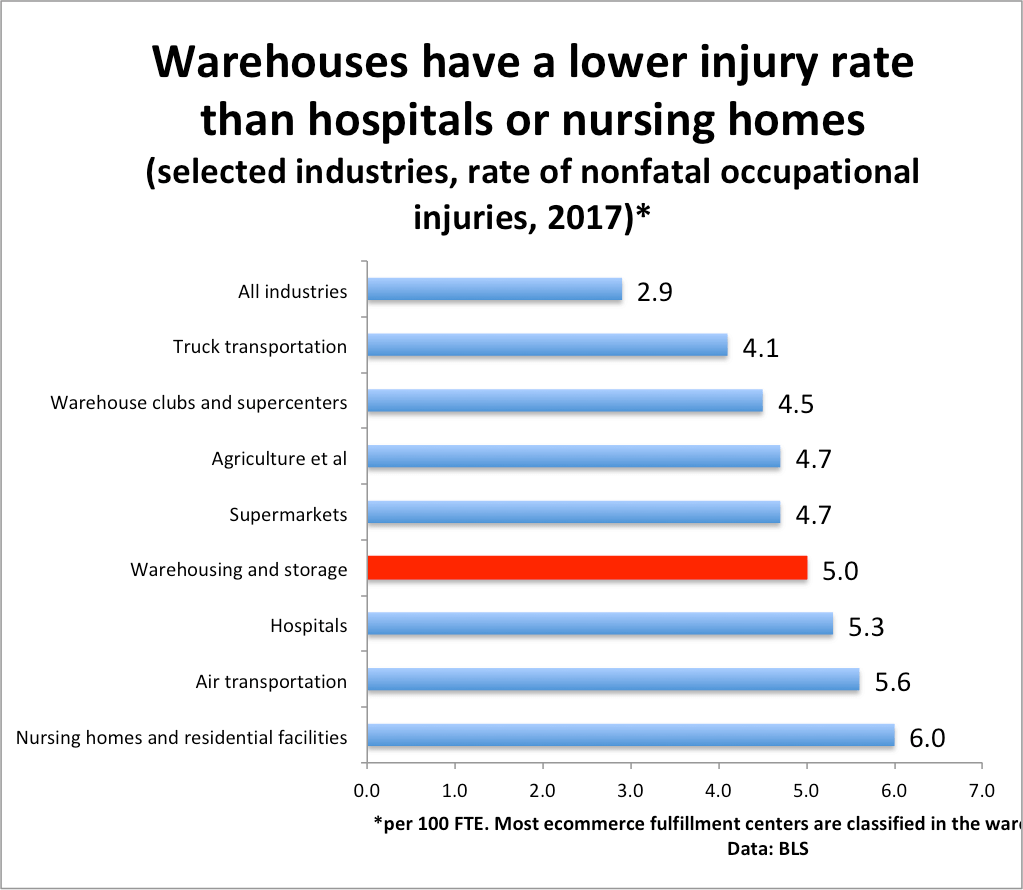

How does warehousing compare to other industries, in terms of safety? Warehousing has a somewhat higher injury rate than warehouse clubs, supermarkets, or agriculture, and somewhat lower than hospitals, nursing homes, and air transportation.

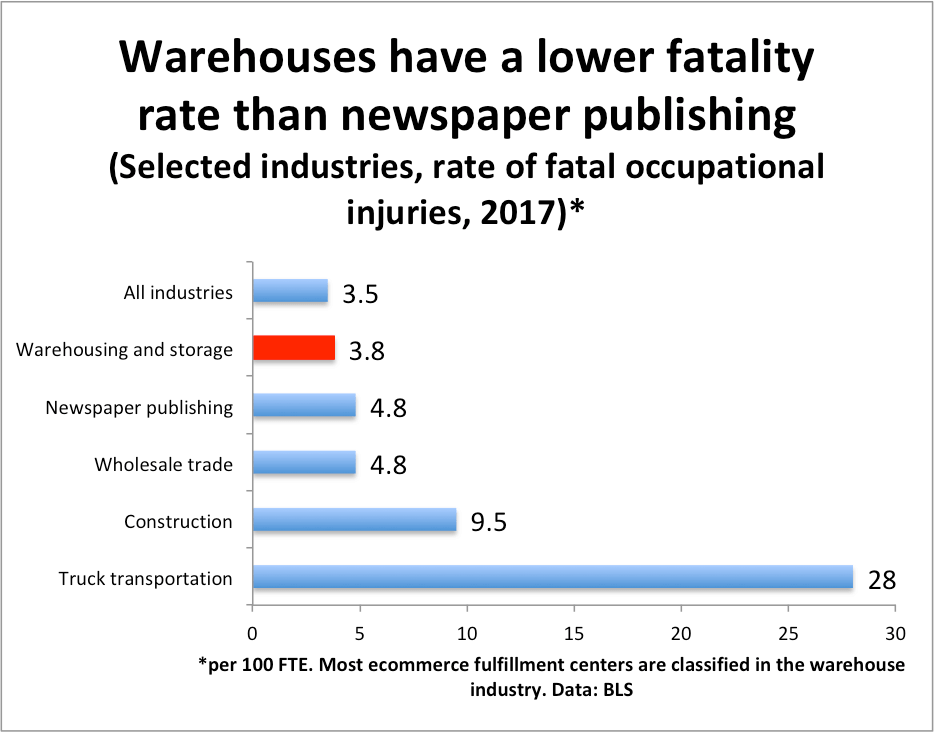

Finally, we come to fatal occupational injuries. This is a small but obviously important category. All told in 2017 there were 22 fatal occupational injuries in warehousing, out of 5147 total occupational fatal injuries across the economy (construction, by comparison, had 971 fatalities). In 2006, warehousing had 17 fatal occupational injuries.

The increase in fatalities, though, is purely reflective of the enormous growth of the industry. The fatality rate in warehousing fell from 4.9 in 2006 to 3.8 in 2017 (per 100,000 FTE). How does that compare to other industries? The chart below reports on occupational fatality rates for selected industries. We see that warehousing is slightly above average (the private sector had a fatality rate of 3.7). Interestingly, the fatality rate in warehousing is lower than newspaper publishing (4.8). Truck transportation had a stunning-high fatality rate of 28 (per 100,000 FTE).

How we interpret the data: Like the economy overall, the safety record of the warehousing industry has gotten better, even as ecommerce fulfillment centers have become an increasingly large share of employment. And as we think about how to further improve the occupational safety performance of ecommerce fulfillment centers, they should be judged against other physical industries such as healthcare and trucking, rather than against office environments.

*These statistics come from a BLS survey of employers. It’s clear that the survey undercounts injuries and illnesses, but the undercounts mostly seem to be concentrated among the smaller establishments. Research suggests that larger establishments (over 1000 workers) tended to be much less prone to undercounts. Moreover, the transportation/warehousing/utilities sector seems to have a relatively good track record for reporting occupational injuries and illnesses.

For many, becoming a small business owner has always been a part of the American Dream and for entrepreneurs launching a successful startup today is, in many ways, the 21st-century version of this ambition. But even if the business gets off the ground, it is becoming more and more challenging for company owners to scale up.

To put it in perspective, “young” businesses — 6 to 10 years — were half as likely to employ 1,000 workers or more in 2014 compared to 20 years ago. That’s based on an analysis of Census Bureau data in research released this month from the Progressive Policy Institute and Allied for Startups.

Large companies have been blamed for acquiring small companies before they can grow. However, there’s another explanation for the scaling-up trap that deserves more attention: the unintentional tax and regulatory cliff created by decades of policies favoring small businesses.

In the United States, small businesses are often exempt from obligations to provide certain employee benefits and comply with certain regulatory rules if the company is small enough. While these “carve-outs” are beneficial for companies who stay below the relevant thresholds, the threat of losing these exemptions can make entrepreneurs think twice before expanding. In fact, sometimes, selling small businesses to larger rivals is more lucrative for owners than scaling their own businesses.

Despite the low unemployment rate, productivity growth is still stuck in slow gear. Non-farm business output per hour increased by 1.3 percent from the third quarter of 2017 to the third quarter of 2018 – well below the post- war average of 2.2 percent.1 Other countries around the world are also grappling with this slowdown in productivity growth.2 Productivity growth is the primary factor in boosting wages and living standards.

The continued lack of productivity growth arises from several causes. One important issue is a growth shortfall in the amount of capital relative to the amount of labor, where capital represents investment in equipment, structures, software, and other intellectual property.

The Bureau of Labor Statistics (BLS) calculates a measure it calls “capital intensity,” which measures the services produced by capital assets relative to the number of labor hours worked in the non-farm business sector. As shown in Figure 1, capital intensity has grown much more slowly over the past 10 years than in previous 10-year periods.

There has been much debate over the reasons for this shortfall. Some have suggested that corporate managers and stock market investors have become myopic and too focused on short-run returns. Others blame excessive regulation.

But, no matter the reason for the investment shortfall, we think it’s important to identify those companies that are bucking the trend. Starting with our 2012 “Investment Heroes” report, and continuing through this report, we have focused on identifying those companies making the largest capital investments in the United States. By expanding the capital stock, these companies are helping boost productivity and wages, and creating new jobs.

The Progressive Policy Institute’s (PPI) Investment Heroes report provides an exclusive estimate of domestic capital spending for major U.S. companies. Currently, accounting rules do not require companies to report their U.S. capital spending separately. To fill this gap in the data, we created a methodology using publicly-available financial statements from non-financial Fortune 150 companies to identify the top companies that were investing in the United States. That methodology, with small modifications, has been used in each year’s report since the first in 2012.

As many as 4.4 million U.S. jobs are going unfilled due to shortages of workers with the right skills. Many of these opportunities are in so-called “middle-skill” occupations, such as IT or advanced manufacturing, where workers need some sort of post-secondary credential but not a four-year degree.

Expanding access to high-quality career education and training is one way to help close this “skills gap.” Under current law, however, many students pursuing short-term career programs are ineligible for federal financial aid that could help them afford their education. Pell grants, for instance, are geared primarily toward traditional college, which means older and displaced workers – for whom college is neither practicable nor desirable – lose out. Broadening the scope of the Pell grant program to shorter-term, high-quality career education would help more Americans afford the chance to upgrade their skills and grow the number of highly trained workers U.S. businesses need.

THE CHALLENGE: THE AMERICAN ECONOMY DESPERATELY NEEDS MORE SKILLED TALENT.

For years, U.S. businesses have complained of a “skills gap” – the inability to find the right talent for the positions they are seeking to fill. Though some have questioned the existence of these shortages, new research finds that, while some lower-skilled sectors have a surfeit of workers, other industries do indeed face a real – and dire – need for skilled employees.

Healthcare, finance, and information technology are among the fields with the greatest shortages of skilled workers.

A study by the U.S. Chamber of Commerce Foundation and Burning Glass Technologies finds that as many as 4.4 million American jobs are going vacant because companies can’t find the right employees. More than 1.1 million of these openings are in healthcare, followed by business and financial operations, office and administrative support, sales, and computers and math.

Many openings are in so-called “middle-skilled” jobs that require specialized training or education but not a four-year degree.

The vast majority of in-demand positions require some sort of post-secondary education beyond high school. In fact, the economy is shedding low-skill jobs even as demand for higher-skill occupations is rising. The Georgetown Center on Education and the Workforce, for instance, estimates that as many as 6.3 million jobs for workers without a high school diploma have permanently disappeared since the recession (2).

While some of the fastest-growing occupations require advanced schooling and extensive training – such as occupational therapy, physician’s assistant, and nurse practitioner – many well-paying jobs don’t require a four-year degree (3). These so-called “middle-skill” jobs currently account for more than half of all U.S. jobs (4) and include such fields as cybersecurity, welding and machining, truck driving, and home health (5). These jobs might demand an associates’ degree, but, in many cases, instead require a certificate, certification, license, or other industry-recognized credential attainable without attending a traditional college.

Federal financial aid for higher education is largely unavailable for career education and training.

Despite the need for middle-skill workers, current federal policy is tilted heavily in favor of traditional college over career and occupational education. In 2016, for instance, the federal government spent more than $139 billion on post-secondary education, including loans, grants and other financial aid for students. Yet, of this amount, just $19 billion went toward career education and training (6).

THE GOAL: EXPAND AFFORDABLE ACCESS TO HIGH-QUALITY CAREER EDUCATION – ESPECIALLY FOR OLDER AND NONTRADITIONAL STUDENTS

Restrictions in federal financial aid programs – that shut out many career-focused programs – are a major source of the disparity in federal support for traditional college versus career education and training. Federal Pell grants for low-income students, for example, can be used only for credit-bearing programs offered by accredited schools that last over 600 clock hours and run at least 15 weeks (7). Many high-quality coding “boot camps,” for instance, often don’t meet this standard; nor do many other occupational courses, such as programs aimed at helping students earn a welding certification or a commercial drivers’ license.

For example, Delaware’s Zip Code Wilmington, a non-profit coding school, offers an intensive computer skills program that has helped students’ salaries jump from an average of $30,173 to $63,071. Yet, because Zip Code Wilmington is not a college or university and the coursework is only 12 weeks long, the $3,000 course is ineligible for Pell funding – which could it make it unaffordable for many students (8).

THE PLAN: BROADEN THE AVAILABILITY OF PELL GRANTS TO INCLUDE HIGH-QUALITY SHORTER-TERM CAREER EDUCATION

Congress should expand the federal Pell grant program to include high-quality career education and training programs in fields with demonstrated demand for workers. Making career education more affordable through so-called “workforce Pell” would increase the pipeline for skilled talent, thereby diminishing the “skills gap” among U.S. companies. It would also open new opportunities for older and displaced workers for whom going to college or returning to school is neither practicable nor desirable. And, given the growing recognition that higher education is a lifelong endeavor (rather than one limited to the young adult years), this shift would help modernize federal higher education policy to better suit the needs of students, workers and businesses.

One promising approach is the Jumpstart Our Businesses by Supporting Students (JOBS) Act, proposed in the 115th Congress by Senators Rob Portman (R-OH) and Tim Kaine (D-VA), which would shorten the number of course hours required for Pell eligibility to 150 clock hours over eight weeks but also require that programs lead to an industry-recognized credential and meet other requirements for quality (9). Quality safeguards would help ensure that fly-by-night credential providers cannot exploit students – helping steer students toward top-flight programs.

Growing the Pell grant program need not come at the expense of higher education funding more broadly; potential sources for funding a Pell expansion include earmarking revenues from the excise tax on large university endowments (included in the 2017 tax bill), or limiting tax-preferred 529 college savings accounts, whose benefits overwhelmingly accrue to the upper middle class (10).

Although expanding Pell grants to more career education could ultimately make the program more costly, occupational credentials are typically much cheaper to acquire than college degrees, and the ultimate return – more workers in better jobs with better wages – makes the investment worthwhile.

1) Restuccia, Dan, Bledi Taska, and Scott Bittle, Different Skills, Different Gaps, Burning Glass Technologies, 2018, available at https://www.burning-glass.com/wp-content/uploads/Skills_Gap_Different_Skills_Different_Gaps_FINAL.pdf.

2) Anthony P. Carnevale, Tamara Jayasundera and Artem Gulish, Six Million Missing Jobs: The Lingering Pain of the Great Recession, Georgetown Center on Education and the Workforce, December 2015, https://1gyhoq479ufd3yna29x7ubjn-wpengine.netdna-ssl.com/wp-content/uploads/Six-Million-Missing-Jobs.pdf.

3) Chamber of Commerce Foundation and Burning Glass Technologies.

4) National Skills Coalition, United States’ Forgotten Middle, available at https://www.nationalskillscoalition.org/resources/publications/2017-middle-skills-fact-sheets/file/United-States-MiddleSkills.pdf.

5) Burning Glass Technologies, “Which Middle Skill Jobs Will Last a Lifetime?” June 20, 2018, available at https://www.burning-glass.com/blog/which-middle-skill-jobs-will-last-lifetime/. See also Anthony P. Carnevale, Jeff Strohl, Neil Ridley, and Artem Gulish, Three

Educational Pathways to Good Jobs: High School, Middle Skills and Bachelor’s Degree, Georgetown Center on Education and the Workforce, 2018, available at https://1gyhoq479ufd3yna29x7ubjn-wpengine.netdna-ssl.com/wp-content/uploads/3ways-FR.pdf.

6) Opportunity America/AEI/Brookings Working Class Study Group, Work, Skills, Community: Restoring Opportunity for the Working Class, Opportunity America, 2018, available at https://1gyhoq479ufd3yna29x7ubjn-wpengine.netdna-ssl.com/wp-content/uploads/3ways-FR.pdf.

7) 20 U.S. Code § 1088, accessed at https://www.law.cornell.edu/uscode/text/20/1088.

8) Anne Kim, Forget free college. How about free credentials? Progressive Policy Institute, October 2017, https://www.progressivepolicy.org/wp-content/uploads/2017/10/PPI_FreeCredentials_2017.pdf.

9) Office of Sen. Tim Kaine, “Kaine, Portman Introduce Bipartisan JOBS Act to Help Workers Access Training for In-Demand Career Fields,” Jan. 25, 2017, https://www.kaine.senate.gov/press-releases/kaine-portman-introduce-bipartisan-jobs-act-to-help-workers-access-training-for-in-demand-career-fields.

A D.C. housing development serves as a refuge for grandparents raising young children. Is it a model for the rest of the country?

It’s a few days after Christmas, and Akirah Carter is sitting in her living room, still wearing her Santa-and-reindeer-patterned pajamas and pointed elf slippers as she tinkers with her gifts: a PlayStation 4, a magic set, Harry Potter books. On the kitchen counter sits a plate of snickerdoodles the 10-year-old baked with her grandmother. She spent Christmas Eve at her great-uncle’s house in Bowie, Md., playing games with her family and singing “Santa Claus Is Coming to Town” on a karaoke machine. That night, after returning home, she left out a few cookies and a glass of milk for Santa.

“She knows there’s no Santa,” says Akirah’s grandmother Tonya Carter, 58. “But she still puts out cookies for me.”

For the past eight years, Carter has served as Akirah’s Santa. Akirah can’t remember a Christmas with her parents. Her mother has drifted in and out of homeless shelters and is now in South Carolina, and her father — who sees her every other weekend — lives miles away and can’t care for her on his own. So Akirah lives full time with her grandmother in Plaza West, a brand-new apartment building in Washington’s Mount Vernon Triangle neighborhood built especially with families like hers in mind.

Plaza West reserved 50 of its 223 units for “grandfamilies”: families made up of grandparents raising their grandchildren full time. It’s one of a handful of buildings across the country created for low-income grandfamilies to live in affordable apartments with neighbors in similar circumstances.

Grandparents taking in their grandchildren isn’t a new phenomenon, but their numbers have been growing in recent years. As of 2017, 2.8 million young people — about 4 percent of American children — were being raised by 2.6 million grandparents (including 7,250 kids in Washington, D.C.), according to the U.S. Census Bureau. Nationally, the number of children raised by their grandparents increased by nearly 15 percent between 2007 and 2017.