The results of the 2021 American Community Survey (ACS) were recently released, providing important information about the causes of the digital divide and how to fix it. The ACS asks a variety of internet-related questions `including whether the household subscribes to fixed broadband such as fiber, cable, or DSL. According to the ACS, 75% of households, and 82% of individuals have fixed broadband subscriptions. To put it another way, 25% of households and 18% of individuals do not have access to the internet through fixed broadband. This is an unacceptably high number.

On the other hand, the FCC’s broadband deployment data shows that as of June 2021, fixed wired broadband of at least 25/3 (25 Mbps download and 3 Mbps upload) is available to 94.3% of the American population. Or to put it the other way, only 5.7% of the American population does not have fixed wired internet of at least 25/3 bandwidth available. If we add in fixed wireless, the “unavailability” percentage goes down to 2.4%. (We are using ‘access’ to mean actually signed up for broadband services, and ‘available’ to mean that fixed broadband subscriptions are locally available for purchase).

This difference—between 25% of households and 18% of individuals without fixed wired internet access, and the 5.7% of the population without fixed wired internet availability—can be called the adoption gap. ‘Adoption’ refers to the willingness, or lack of willingness, of households and individuals to sign up for broadband when it is available.

It used to be more appropriate to call it the affordability/adoption gap, but for several reasons price has become a much less important issue. For one the Affordable Connectivity Program (ACP)—a permanent program that replaces the temporary Emergency Broadband Benefit program–provides a $30/month subsidy for eligible low-income families and individuals, which includes anyone who in a household earning less than 200% of the federal poverty guidelines, or participating in any of a number of assistance programs such as SNAP or Medicaid. And since many providers now offer $30/month basic internet plans, the cost of getting online has effectively fallen to zero for many low-income households as long as the ACP funding holds out.

In addition, government data shows a substantial decline in the price of internet access in recent years, even without subsidies. For example, the BLS reports that the producer price of residential internet access has fallen by almost 10% over the past five years. This decline in broadband prices has continued even through the inflationary surge of the past year. As the result of all of these factors, the latest NTIA Internet Use Survey (collected November 2021, before the ACP became active) showed that only 18% of households without internet access at home cited cost as a reason for being offline. Indeed, in the NTIA survey, 58% of the offline households “express no interest or need to be online.”

The exact size of the adoption gap is subject to dispute, as in most things telecom. But it’s clear that most states have a substantial number of people who have the opportunity and means to subscribe to fixed broadband, and choose not to. Some of them may be quite happy using their smart phone and a cellular data plan as their main access route. But for many other people, lack of digital literacy or a lack of credit cards or bank accounts may be important issues keeping them from making use of online government services or private sector transportation, shopping, entertainment, work or education opportunities.

How can the adoption gap be closed? First, we know what won’t work: Building expensive new networks in areas that already have high-speed broadband. If low-income households already can get “zero-cost” high-speed internet if they want, but choose not to, then laying costly fiber in their neighborhood won’t make a difference to their adoption.

Instead, that money should be funneled into programs to improve digital literacy and show, step-by-step, how to get online and utilize government and private resources. But by themselves, such programs are not enough, since adoption is driven by financial inclusion as well. In a data-driven economy, access to the internet becomes less valuable to someone without a credit card or a bank account, since it’s much harder to use online services such as ecommerce and ride-sharing. Indeed, it’s possible that the people who express no interest in being online are actually responding to these other obstacles.

In many ways, we’ve done the straightforward part of closing the digital divide: A massive investment in physical capital, funded mainly by the private sector, combined with the latest healthy dollop of public money to fill the gaps. Now it’s time to focus on building out the rest of the social and financial online infrastructure, to include everyone. Investment in human and social capital is as important as investment in physical capital.

A quick response after reading last Wednesday’s lengthy, startling, and troubling letter from Sen. Elizabeth Warren and Rep. Pramila Jayapal to Commerce Secretary Gina Raimondo: Don’t charge people with bad faith unless you have evidence of it. Progressives can do better.

By way of introduction, the two Members’ letter continues a correspondence begun in July whose point of departure is a disagreement on digital trade policy matters such as cross-border data flows, divergences in national privacy regulation, and data localization. Sen. Warren and Rep. Jayapal object along left-populist lines to potential Biden administration negotiating positions on some of these topics in trade venues such as the Indo-Pacific Economic Framework and U.S.-EU Trade and Technology Council.

Were these disagreements the core of their letters, this would be the standard stuff of Congressional correspondence and advocacy. Digital trade issues are intellectually and technically complex. Conclusions about the best way to define U.S. interests on them can vary in good faith. And while Sen. Warren and Rep. Jayapal may be mistaken, dissent is perfectly legitimate and their rights to their opinions are obvious.

But the core of their letter is not the substance of policy but an insinuation – unsupported by evidence – that the Commerce Department is forming its positions in an improper or even a corrupt way and is likely pursuing specifically tech-industry goals rather than acting on good-faith Biden administration judgments about American interests. The letter uses two quite troubling lines of argument to back this up:

(1) Charges without evidence: For the Commerce Department as a whole, the letter notes that “several former employees” of tech firms work at the Department, and uses this bare fact to claim that “Big Tech” has an “untoward influence” on trade negotiations and may be “exploiting the revolving door with the Department” to set policy from outside. Apart from noting that several Department officials once held tech-sector jobs, the letter provides no evidence that the Commerce Department has taken any decision on any grounds other than its best assessment of U.S. interests and policy goals.

(2) Guilt by association: For individual officials, the letter cites past tech sector employment as evidence of “Big Tech’s current influence within the Department”, and a likelihood that “the Department’s revolving door with Big Tech firms will provide those companies the avenue they need to push their proposals across the finish line.” That is to say, some Department officials are pushing for goals they know are not in the general interest. Again, the letter does not cite any specific case in which any individual might have acted in bad faith, or provided advice that he or she did not sincerely view as good policy

The October letter, as did the July letter, then concludes by asking for lengthy lists of names – all Commerce appointees and civil servants who have previously held tech-sector jobs; all who left the Department after President Biden’s inauguration for tech-industry work – and accompanying lists of all tech-industry meetings these officials attended, or for which they helped in preparation and follow-up work. Again, no such list would provide any evidence of bad faith or improper policymaking.

Two thoughts on this:

First, as a practical matter, the letters’ premise leads to an absurd conclusion about policymaking and government personnel. To wit, U.S. government agencies should never employ people from sectors in which they have any oversight or policy responsibility, because such a person will inevitably put the interest of former employers above the national interest and his or her sworn duties. Applied to the Department of Agriculture, for example, such a standard would bar hiring farmers or people who might want to work in production agriculture later on. At the Centers for Disease Control, the presumption would be against hiring doctors and public health professionals. The Labor Department would likewise be well advised to avoid union members, and the Transportation Department should steer clear of airplane pilots and bridge architects, and even the Justice might need to stay away from anyone with a law firm background.

Second and more fundamentally, this premise – past employment with tech firms should entail presumption of bad-faith policymaking, and the Department and the individual officers need to disprove it – is wrong and unfair. Accusations of bad faith policymaking should require evidence of wrongdoing. American government officials, whether civil servant or political, qualify for their jobs based on three things: (1) they take an oath of office; (2) they pass an FBI security clearance investigation at the appropriate clearance level; and (3) they understand and respect national ethics laws and administration policy, for example by recusing themselves in cases these laws and policies define as posing a conflict of interest. If there is evidence that any official has fallen short on these responsibilities, provide it. If not, keep your argument to the merits. But neither letter provides any evidence that any Administration official has fallen short on any of these responsibilities.

The digital trade agenda as such is important in immediate economic terms, and more basically as a question of future world Internet policy. Obviously it has lots of implications for growth, for science, and for individuals. There’s no reason to shy away from spirited debate over it. But there’s also no reason at all to substitute attacks on character and integrity for this sort of debate. Progressives really need to do better.

Online platforms face an increasingly complex regulatory environment in the European Union. Altering their business models to comply with EU regulation while simultaneously experiencing intense scrutiny from competition authorities, American tech companies are being pushed to evaluate their profitability in Europe. Yet, proposals circulating within the EU are seeking to capitalize on this profitability by taxing these same companies to subsidize broadband infrastructure expansion.

While the sector is currently engaging in high levels of investment and enjoying consistent revenue growth, the notion that any industry can withstand significant taxation on top of mounting regulatory compliance costs threatens both the jobs created by the sector and the promise of future investment. These are circumstances that the European telecommunications industry knows well. With amassed regulation corresponding to relatively weak revenue growth over time, EU telcos have struggled to invest in the development of new high speed network technology such as 5G at the same rate as their counterparts in the United States and China. As high-capacity networks become the norm for consumers who rely on data-heavy services like streaming high-quality video and video conferencing tools, Europe risks being left behind in the next era of technological innovation. Though plagued with its own set of problems such as the ongoing debate over net neutrality, the U.S. telecommunications industry has managed to sustain a high level of investment, resulting in widespread 5G infrastructure and connectivity. Concurrently, European telcos have faced weak revenue growth and difficulty translating the demand for online services into a demand for new subscriptions.

Despite the apparent lag, the European Union’s “Plan for the Digital Decade” has set the goals that by 2030 every home in Europe will have Gigabit connectivity and every populated area of Europe will have access to 5G service. While this sounds like a great leap forward in digital expansion, the reality is that each of these goals presents a massive capital investment challenge to European telecommunications companies. Aware of this funding gap, the governments of France, Italy, and Spain released a joint paper in August 2022 calling on the European Commission to craft legislation requiring large online platforms pay a “fair share” of network infrastructure in Europe. EU regulators and industry groups such as the European Telecommunications Network Operators’ Association have echoed this proposal, with the idea being that the growth of these online platforms is dependent on the quality of network infrastructure. They make the claim that “over-the-top” (OTT) companies such as Google and Netflix need improved networks because of the data-intensive nature of their content and should thus contribute to the cost.

But there are regulatory factors preventing European telecommunications companies from accruing the revenue needed for significant network infrastructure investment which additional regulation will not solve. A recent letter signed by 13 European telecom CEOs points out the harm that EU price regulation causes to the competitive market for telecom services, 4 and major operators such as Vodafone have been vocal in their calls for market consolidation to support the scale needed for companies to invest in network expansion. In light of this, those calling for similar action against the tech sector should evaluate whether an additional tax in the face of strict competition guidelines and increasing regulatory hurdles will result in more network investment in the long run, or similarly impair the ability of the tech sector to contribute. This report offers a comparative analysis of the performance of the U.S. and European telecommunications industries, focusing specifically on their ability to achieve widespread high-speed network connectivity to examine the relationship between capacity for investment and heavy regulation. It finds that U.S. companies generally have had greater success in terms of connectivity and services speeds while Europe’s emphasis on low consumer prices may have resulted in underinvestment in its telecommunications sector. It recommends that for Europe to realize its full potential in terms of future technological innovation, the EU must adjust its regulatory policies to acknowledge the trade-off between low prices and investment, avoiding overregulation of high investment industries and supporting a sustainable digital transition for EU’s telecommunications industry.

COMPARING TELECOMMUNICATIONS MARKETS IN THE UNITED STATES AND EUROPEAN UNION

Over the last decade there has been a global shift in consumer preferences from a reliance on voice-enabled communication to more data-driven internet services such as online messaging and video-calling. The consequence has been a shift in profitability from telecommunications operators to companies which operate internet platforms.

This trend is evident when looking at the percentage of profit held by telecom companies and internet platforms over time. Combining the telecom and internet sector, the global industry had a cumulative profit of $251 billion in 2014. Of this, 74% was profit by telecom companies, leaving the remaining 26% as the profit made my internet platforms. Just five years later, the cumulative profit remained similar at $260 billion, but internet companies now accounted for 60% of the profit.

However, when looking at the telecom industry with a more regional lens, this loss in revenue may not be equally distributed across all telecommunications markets. Though they face similar challenges, there’s a difference in capital investment and subsequent levels of connectivity when comparing the United States and Europe.

Capital Investment by Telecom Operators

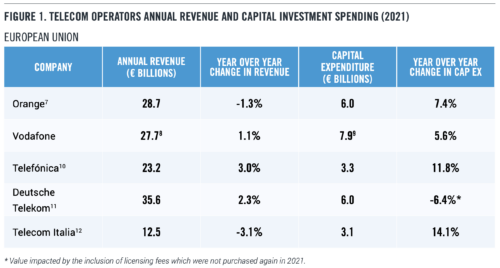

Telecommunications is a capital-intensive industry which requires continuous investment to maintain and develop efficient networks able to meet the challenges of rapidly evolving technology. With the struggle to reach new consumers looming over these companies, revenue growth is slow across the industry. However, while a handful of top European telcos experienced negative revenue growth in 2021, top American telecom operators grew a minimum of 4% — with T-Mobile’s U.S. division experiencing growth of almost three times that.

Figure 1 displays five of the top telecom operators by annual revenue in the European Union and United States, as well as their 2021 capital expenditure. Displayed are only the revenue and expenditures of these companies as they relate to telecommunications — excluding other lines of business. This data is reflective only of the company’s activity within the United States and EU member states and thus does not encompass global operations. Discrepancies such as the inclusion of spectrum licensing fees and inclusion of small amounts of overseas data may be present based on a company’s methods of reporting.

Despite the wavering profitability of the telecom business model globally, American companies are experiencing higher rates of revenue growth and therefore have the wherewithal to boost their capital spending on broadband. Many companies’ annual reports note that a significant amount of this expenditure is being directed to the expansion of 5G networks in the U.S., increasing American capacity for data intensive services. European consumers are not benefitting from the same level of investment in high-capacity networks, and European telecom operators are not experiencing the revenue growth required to catch up.

Service Speeds and Connectivity

The heightened need for investment in network infrastructure comes as global online traffic increased roughly 60% in 202018— tasking the telecom industry with ensuring not only widespread connectivity but that their networks have the bandwidth for high levels of consumer use. European networks were not prepared for the surge in online activity, making bandwidth comparatively scarce. As a result, in 2020 the EU called on streaming platforms to lower the quality of their video streaming services to reduce the bandwidth needed to bring video to consumers. In response, platforms such as Netflix and YouTube lowered the quality of video offered to consumers in certain European countries, lightening bandwidth needed to use their services to free capacity for other users.

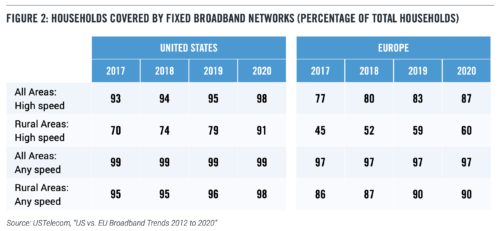

But bandwidth has not been the only challenge. The EU also trails behind the United States when it comes to levels of coverage. Though by 2020 Europe had begun to match the U.S. on the percentage of households covered by broadband networks, there are still disparities in levels of rural and high-speed coverage. The following figure considers connection to be “high speed” if it allows download speeds above 30 Mbps. In the U.S. in 2020, 98% of all households were covered by high-speed broadband, while in Europe only 87% percent of households had access to the same speeds. This is largely driven by the lack of high-speed connection in rural areas of Europe.

When it comes to internet connection speeds, America holds a substantial lead. Median download speeds in the United States more than quadrupled in the period between 2017 and 2020, when download speed grew by 157.7% year over year. Europe’s median speed also increased with a year over year growth rate of 76.2%, but this still left them lagging substantially behind. In 2021, the U.S. median of 83 Mbps was more than double the EU’s median of 38 Mbps. Only four European cities (Copenhagen, Stockholm, Bern, and Budapest) had reported median download speeds faster than the nationwide median reported stateside in 2021.

The United States has also pushed deployment of advanced networks, including fiber optics, at a higher rate than in Europe (see Figure 2). In general, American consumers are more likely to opt into internet subscriptions with higher service speeds. A study by USTelecom found that in 2020, 55% of connected U.S. households had subscriptions with speeds reaching at least 100 Mbps, while only 34% of connected European households had subscriptions capable the same speeds. Whatever the reasons for this wide performance gap, it’s clear that the United States proved better able to support surging demand for online services and commerce during the pandemic.

Differences in the Price of Service to Consumers

One metric by which the European telecom industry has the upper hand is prices paid by consumers for internet services. A study by New America’s Open Technology Institute found that in 2020, the average monthly cost of internet service in Europe was $44.71, compared to $68.38 in the United States.

During a period of global inflation there is considerable value in the EU’s prioritization of maintaining low costs to consumers who are juggling rising prices across other sectors. In the context of analysis of the sustainability of the telecommunications industry, however, is important to take account of the trade-offs associated with low prices. European telcos exhibit lower revenue growth, lower levels of capital investment and lower rates of high-speed connectivity than their U.S. counterparts. As Figure 2 shows, the United States also has a significantly higher proportion of rural households with access to high-speed broadband. Rural broadband comes at a high cost to the network operator. As companies expand coverage into less dense areas, the average cost per potential customer rises. Sparsely populated areas don’t provide companies with the return on investment through user fees needed to cover the cost of that network expansion. This generates pressures for both government subsidies and price hikes. Rural regions often also present geographic challenges, both in terms of remote locations and rough terrain for laying cables, further raising the cost to companies.

Prices in the European Union are also lower because of more aggressive regulatory intervention. Europe has maintained a stricter approach to competition policy in the telecommunications industry, contributing to the lower prices when compared to the more consolidated American sector. Additionally, regulations like the EU’s “roam like at home” policy, which requires telcos based in one country to provide service across borders within the European Union at no additional charge, also keep prices down — protecting consumers from predatory behavior by companies overcharging for roaming fees but at the expense of the profits firms need to make robust investments in high-speed networks.

Adoption of 5G Service

With the newfound prominence of data services, the telecommunications industry has largely looked to rising demand for 5G to fill the hole in revenue created by consumer preferences shifting away from traditional telephone lines and voice traffic. 5G technology is integral to business innovations such as driverless cars, virtual reality-based platforms like the Metaverse, the development of more integrated smart cities, and other Internet of Things applications. But many of these products are in their infancy, meaning that for consumers who would be accessing 5G networks from smartphones, which operate just as effectively on lower capacity networks, the benefits of 5G are relatively intangible. Without consumer need for these networks, the incentive for companies to invest the capital required for widespread deployment is low.

Still, European companies have joined their international counterparts in deploying 5G technology in preparation for that next wave of consumer tech products. The industry association GSMA estimated that as of May 2022, 34 out of 50 European countries had some level of 5G deployment and 92 of 173 operators in the region launched 5G networks. However, even though there are networks available in most countries, only 2.5% of all online connections in Europe were 5G connections in 2021. When compared to other leading economies such as the United States, where 5G accounted for 14.2% of connections, and China, where 5G accounted for 28%, this demonstrates a significant lag in deployment and consumer adoption. This is a trend which is also reflected in the types of hardware being purchased by consumers. The majority of smartphones purchased in Europe are 5G enabled, but 5G smartphones accounting for 60% of smartphone sales in Europe adoption still falls behind the 73% of smartphone sales in North America.

Advocates for 5G expansion tout its potential to support much higher speeds, superior network reliability, and negligible latency. But consumer tech products like smartphones aren’t going to operate much differently between 4G and 5G networks — leaving the appeal of 5G dependent on the promise of future technology. Telecom companies have invested in these networks nonetheless but, without an influx of products on the market which rely on it, the demand is unlikely to translate into the revenue needed for more network expansion. When you add the premium price operators would have to charge to improve their networks, consumers may not consider it a good deal. This is why analysts expect business adoption to be the main driver of 5G demand, though the lag in consumer adoption compared to the United States and China is concerning for the immediate financial state of the European telecom industry.

CONTRIBUTIONS OF OVER-THE-TOP COMPANIES TO NETWORK INVESTMENT

A 2022 report by MTN Consulting found that investment by global telecom operators as a proportion of their total revenues peaked at 17.3% in 2021, driven by 5G network deployments. However, because of the low return on 5G investment, this proportion is expected to decline in coming years. In any case, telecom investment alone doesn’t give us a full picture of the size and extent of broadband infrastructure in Europe or the United States. Six American companies — Meta, Google, Apple, Amazon, Microsoft, and Netflix — currently account for 56% of all global data traffic between both fixed and mobile networks.

They are considered “over-the-top” or OTT platforms because they are companies reliant on the internet to deliver their products to consumers, in contrast to content mediums such as cable and broadcast. Each of these companies offers highly data-intensive products such as streaming, putting significant strain on areas where the coverage does not offer sufficient bandwidth to run these services.

This is the rationale for the notion that over-the-top platforms are free riders on the telecom investments that allow them to reach their users. However, contrary to over-the-top moniker, these platforms have also made significant global investments in the underlying infrastructure required to support their services. The aforementioned six American companies invested a cumulative $137.3 billion globally in 2021, including $58.2 billion from Amazon 31, 24.6 billion from Google, and $24.2 billion from Microsoft. Included in these figures are investments into the construction of data centers, subsea cables, and network edge locations — all which store and transmit the data traffic that European networks are currently struggling to support.

These investments have been largely focused on supporting the creation and expansion of a cohesive global internet. For example, a partnership between Microsoft, Facebook, and Telxius, a Spanish telecom infrastructure company, finished construction of a transatlantic cable in 2017 connecting the U.S. to Spain with the capability to transmitting up to 160 terabits of data per second. Additionally, Google has least 15 subsea cable projects underway around the world, totaling over 10,000 miles of submarine cable. Outside of the EU and U.S., the company has announced $1 billion in investment to support network expansion in Africa in 2021.

Each of these cables can cost several hundred million dollars apiece, signaling that capital investment by these companies is both large and growing as more of these types of projects are announced. Combined, it is estimated that the subsea cable projects by American OTT platforms contributed to an increase in global data transmission capacity by 41% in 2020.

As they seek to extend the efficiency and accessibility of their products to new customer bases, OTT platforms are expected to increase their capital expenditure from an average of 26.4% of their revenues over the past five years to more than 37% over the next half-decade. That means OTTs likely will be the main driver behind global network infrastructure investment moving forward.

Another overlooked aspect of network infrastructure is the construction of global data centers and network edge locations. Data centers are facilities crucial to storing, processing, and disseminating data and applications over the internet or through the cloud, and network edge locations are facilities geographically distributed to efficiently deliver content to nearby end-users. These are vital investments for over-the-top platforms which, while relying on telecom networks to reach users, need physical locations to support global data transmission.

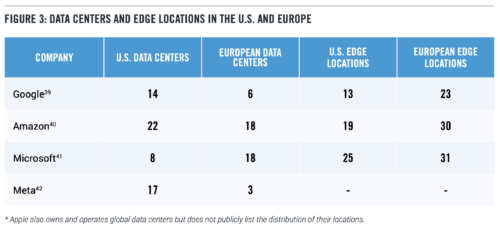

Five of the six big U.S. tech platforms (Netflix is the exception) the EU identifies as bandwidth hogs own and operate their own data centers and edge locations with both U.S. and European presence, as shown in Figure 3, highlighting the investment made to the larger network. Without construction of their own centers, companies outsource to third party content delivery networks to store and transmit data over the cloud. Netflix, for example, largely relies on Amazon’s AWS network for data storage and computing.

WHAT REGULATORY DIFFERENCES ARE HOLDING EUROPEAN COMPANIES BACK?

Although wireless prices have largely been flat in both European and American markets, U.S. telcos have been able to invest more in 5G and other high-speed network expansion. While some of this investment gap may be explained by lower prices and varying consumer interest in paying for high-capacity networks, the difference in regulatory strategies also is likely at play.

The EU has prioritized the lowest possible price to consumers through rigorous enforcement of competition law to discourage consolidation as well as caps on the prices paid for certain services. In contrast, U.S. policymakers have emphasized investment in high-capacity networks and rural broadband. Though favorable to consumers, it is difficult to see how the EU can sustain its strategy of price-focused regulation and still meet its aggressive connectivity targets for the next decade.

Enforcement of Competition Law Telecommunications networks present a unique challenge when it comes to competition law. Barriers to entry for new telecom operators are high given the capital needed to compete with established networks.

Because the cost of entry is so high, large companies utilize economies of scale to expand and maintain massive networks.

The United States and Europe tackle this challenge in different ways. The U.S. telecommunications market tend to be dominated by a few massive players. European countries aim at forming more localized markets with multiple providers, with regulations that ensure high levels of cooperation between companies to maintain a single coherent network.

High levels of competition help to keep consumer prices low. But as the U.S. case shows, a more consolidated market may allow for the economies of scale required to invest in areas where the return on investment is very low — allowing for higher quality service to rural communities.

This is not to say that the American model is ideal. Too many areas of the United States are served by only one provider, leaving consumers without the ability to shop for prices or consumer-friendly contracts. But for there to be substantial competition in more remote areas of the country, there either needs to be an influx of small telecom operators building rural networks — unlikely given the extremely low return on investment of expanding networks into sparsely populated places — or more large companies which can serve remote areas. This is the logic behind a federal judge’s approval of the merger between T-Mobile and Sprint in 2020. The judge reasoned that the combined company would be better equipped to compete with established industry giants Verizon and AT&T. Thus, despite the market becoming more consolidated, the merger would bring a new player to the top of the market putting pressure on incumbent companies in terms of service quality and price.

In contrast, the EU has been far stricter about the size of telecommunications companies, preventing consolidation and instead encouraging network sharing between operators. As a result, the European telecom market is highly fragmented with most countries hosting as many as four mobile operators, many of which are wary of making significant investment in 5G without clear signals that they will see a profitable return. This has prompted companies such as Vodafone and Orange to call for consolidation, claiming that overcrowding in European markets is making it difficult to invest and that network providers do not currently have the financial capacity to pay for the infrastructure needed to develop 5G technology

Europe’s fragmented broadband market necessitates a complex array of network sharing agreements between operators to ensure that their services work throughout the country. EU regulators have been clear in the goal that European consumers should have seamless access to data and voice services when traveling within the EU, requiring companies to negotiate with one another to ensure that their customers will have service in areas of the continent not covered by their own networks. In order for these agreements to be acceptable under EU antitrust law, they must ensure that they’re not reducing incentives for competition in deployment of infrastructure, putting an additional burden on companies which are struggling to achieve the scale needed to expand. It is for these reasons that CEOs of European companies such as Telefonica, Vodafone, and Norway’s Telenor have said that consolidation is necessary because current price wars and low margins are limiting funds available for 5G deployment. Critics of the movement for consolidation cite the likelihood that it will result in higher prices.

Government Funding for Network Expansion and Accessibility

In the U.S., the government spends billions annually to expand access to affordable internet service. Its efforts are mainly directed at subsidizing private companies to offer discount prices to low-income households. The pandemic-induced transition to online school and work in 2020 provided fresh impetus for these programs. In 2021, the Bipartisan Infrastructure Law allocated $65 billion broadband infrastructure deployment and affordability programs, including $401 million to provide access to high-speed internet for 31,000 rural residents and businesses in 11 states. Other programs such as the Affordable Connectivity Program are targeted specifically at long-term affordability for low-income households with a discount of $30 per month for internet service plans.

European funding for such projects differs on a country-by-country basis, but there are also initiatives being spearheaded at the EU level. The EU’s targets for the “Digital Decade” detail a series of initiatives for member states between 2021 and 2030. In addition to the ambitious connectivity targets, Brussels envisions a broader digital transformation in which at least of 80% of the population have digital skills and 75% of EU companies utilize the Cloud or other data services. As previously mentioned, under this plan the EU hopes to have Gigabit connectivity for everyone in Europe and 5G connectivity in all populated locations. To finance these goals, the EU suggests that member states allocate 20% of their funding from the Recovery and Resilience Facility — an EU program meant to finance reform and recovery post-pandemic — to the digital transition.

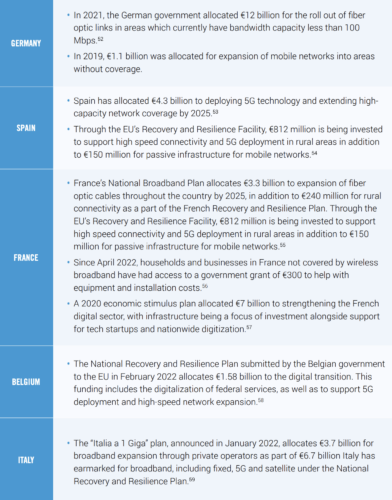

In addition to funding from the EU, member countries have put varying levels of public investment into expansion of fixed and mobile networks. While not a comprehensive list, the table below provides examples of the funding initiatives taken on by a handful of European countries since 2021.

European Price Caps on Telecom Services

While the U.S. government has negotiated with private network providers to lower prices of internet service for low-income Americans and implemented programs to give benefits for these households to front the costs, capping the prices that telecom operators can charge for given services without subsidy is a policy that is uniquely European.

Potentially the most consequential example of this is the EU’s “roam-like-at-home” policy, which allows customers with EU service plans to travel within the EU without additional charges for data roaming. In addition to requiring no charge to the consumer for crossing national borders, companies are required to ensure that data usage is available abroad at the same capacity and speed as the consumer would be paying domestically, with any additional surcharges for surpassing that data usage at €2 per GB of data. It would be infeasible for companies to have network infrastructure everywhere in the EU to meet the requirements of this policy, so it is made possible through network sharing. European telecom operators must enter agreements with other companies so that their customers can access other networks. This can be a costly process for telecom companies so, in the interest of supporting the sustainability of this policy for the telecom operators, wholesale caps are in place to provide a maximum amount that a visited operator may charge for the use of its network in order to provide roaming services.

The problems associated with this policy from a business standpoint are intuitive. By capping roaming fees, the EU limits telecom profits. On top of that lid on profits, companies are not allowed to charge one another more than the wholesale cap. If a company’s costs are at or above the cap, it loses money whenever its customers travel within the EU.

In addition to caps on roaming charges, in 2019 the European Parliament approved a rule to control the prices of intra-EU communication, capping cross-border phone charges at 19 cents per minute for calls and 6 cents per text message. Its purpose is to lower costs to consumers and bolster competitiveness for EU businesses, which will pay less for telecom services. However, for EU telecom operators forced to offer services with a lower profit margin, the net result is less global competitiveness.

There is no question that this is a beneficial policy for consumers in the short term, but the long-term impact is that such policies will disincentivize investment into Europe, ultimately hurting the individual who is having to consume other products at a lower quality than others around the world because of a lack of bandwidth and might not have access to future data-heavy services without network updates. Disincentivizing investment in Europe also pushes European telecom providers to bring their capital investment elsewhere. Vodafone has been in the Indian market since 2007 and continues to invest heavily in expansion in the region, working on bringing 5G to India. Similarly, as shown in Section I, T-Mobile in the United States is now much larger in terms of both revenue and capital investment than their parent company and European line of business, Deutsche Telekom.

CONCLUSION

The United States and the European Union have vastly different telecommunications sectors in terms of market structure, regulation, and operating capacity. Though these differing approaches have worked in the past, the recent influx in demand for bandwidth has exposed cracks in the European system which differ from those in the United States.

As Europe’s example shows, heavily regulated industries tend to invest less. In deciding how to move forward with goals for connectivity and digitalization, the trade-off between low prices to consumers must be weighed with the telecom operator’s propensity to invest such that the industry is not crippled by inability to achieve sufficient scale for network expansion.

This trade-off must also be weighed in the case imposing a fee on internet platforms. While over-the-top internet platforms are currently experiencing high growth, the mentality that they are therefore too big to fail and can withstand heavy regulation and taxation is an oversimplification of the market. This is a heightened risk given the other regulatory activities affecting the tech industry in Europe such as the Digital Markets Act passed in July 2022, which identifies many of these same companies as “gatekeepers” for purposes of competition law, further regulating their ability to profit in European markets. When an entity is taxed, it will also invest less. To add responsibility for network expansion to a growing list of recent EU regulations on leading American online platforms puts strain on an industry which currently engages in enormous capital expenditure, altering the incentive for them to continue to operate and invest within the EU.

With China and the United States leading the way for 5G and high-capacity networks, now is the time for Europe to strengthen its own networks to compete in the next era of technological innovation. As we move toward products that require higher data traffic there is a demonstrated need for updates to global network infrastructure. This will require global cooperation and investment, both from the telecom sector and the OTT platforms which are investing in ways to connect the international internet ecosystem in ways which are not necessarily covered by telecommunications companies. For a successful push toward global digitization, governments must recognize and support this private investment such that European innovation isn’t left behind.

Europe has ambitious targets for telco connectivity – and very real investment needs. But what’s the best way to attract the capital Europe so clearly requires? Some say the best idea is a tax or fee leveraged on so-called “content and application providers” to create a unique, two-sided market – generating new revenue streams for telcos but adding additional costs to consumers and content producers alike. Others see an opportunity for the European Commission to build on its landmark approach to modern telecommunications: creating framework conditions that attract investment, open markets to new entrants and drive forward a vibrant European data economy in a triple win for citizens, businesses and government alike.

At this high-level roundtable, co-convened by two leading transatlantic think tanks – The Lisbon Council in Brussels and Progressive Policy Institute (PPI) in Washington DC – leading telecommunications-sector experts will present new evidence and incisive analysis intended to form a backdrop to ongoing debate on Europe’s telco financing needs. Michael Mandel, vice-president and chief economist of PPI, and Malena Dailey, technology policy analyst, will present Funding the Next Generation of European Broadband Networks, a new policy brief comparing telco investment strategies between the U.S. and Europe and asking a crucial question: who got it right?

A High-Level Panel of leading telco experts will chime in with additional contributions on the outlook ahead.

Panelists:

Malena Dailey, technology policy analyst, PPI; co-author, Funding the Next Generation of European Broadband Networks

Michael Mandel, vice-president and chief economist, PPI; co-author, Funding the Next Generation of European Broadband Networks

Konstantinos Masselos, president, Hellenic Telecommunications and Post Commission, Greece; professor, department of informatics and telecommunications, University of Peloponnese; vice-chair (incoming), Body of European Regulators for Electronic Communications (BEREC)

Rita Wezenbeek, director, connectivity, directorate-general for communications networks, content and technology, European Commission TBC

Paul Hofheinz, president and co-founder, the Lisbon Council (Moderator)

Friedrich Nietzsche’s famous quote that “what doesn’t kill you only makes you stronger” is only true, at least in politics, if you learn from your mistakes. And last year was a teachable moment for Democrats.

Democratic leaders missed huge opportunities on election reform (including the all-important Electoral Count Act), climate change, police reform, the right kind of immigration reform and much else, all because their eyes were too big, packages were too ambitious and most of all because they refused to say “no” to the extremist purity tests of the party’s hard left. Build Back Better was sacrificed on that altar.

Success requires tapering untested grandiosities and selling commonsense ideas to the 70% or so of the public that reject the extremes of the hard right and the hard left.

Today, the Progressive Policy Institute(PPI) released its annual Investment Heroes report, which shows companies with high and sustained capital investment in the United States have helped hold down price increases in the digital sector throughout the past year of otherwise record inflation. The report, titled “Investment Heroes: Fighting Inflation with Capital Investment”is authored by Dr. Michael Mandel, Vice President and Chief Economist at PPI, and Jordan Shapiro, Data and Economic Analyst at PPI.

Nine of the 11 companies topping this year’s Investment Heroes list are in tech, broadband, or e-commerce. Amazon invested an amazing $46.7 billion in the U.S. in 2021, according to PPI estimates. AT&T and Verizon tied for second place at $20.3 billion, and Alphabet invested $18.7 billion in the U.S. in 2021.

PPI has created a unique methodology using publicly available financial statements from non-financial Fortune 200 companies to independently identify the top companies that were investing in the United States. These companies — our “Investment Heroes” — have helped to create good jobs, boost capacity, and reduce inflation as we recover from the aftershocks of the COVID-19 pandemic.

“Policymakers should praise and encourage those companies who invest in the United States, keep prices low, and reduce vulnerability against future shocks. That’s a clearcut win for consumers, workers, and the American economy,” write report authors Dr. Michael Mandel and Jordan Shapiro.

“Conversely, government leaders can’t pursue policies that reduce or discourage domestic capital investment and then complain when we don’t have enough capacity to meet our changing needs at an affordable price, whether it’s energy or semiconductor chips or anything else. In particular, it’s perplexing that Congress is putting so much energy into tech antitrust, when the sector has been a low-inflation, high-investment star performer,” the authors conclude.

See the full list of PPI’s 2022 Investment Heroes:

Read and download the full report here:

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

In 2019, the House Judiciary Committee initiated an investigation into the state of competition in digital markets, looking particularly at the dominance of America’s biggest online platforms. Three years later, a slew of bills have been introduced at both federal and state level intended to curb the power of “Big Tech.” The driving force behind many of these efforts is the claim that companies like Google, Amazon, Facebook (Meta), and Apple are simply too big, with their size posing a competitive threat to smaller tech companies. A handful of these bills are being introduced with the purpose of updating America’s antitrust laws to meet the challenge of today’s supposed tech monopolies.

The American Innovation and Choice Online Act (S. 2992) sponsored by Senators Amy Klobuchar, D-Minn., and Chuck Grassley, R-Iowa, for example, is being sold to Congress and the American public as being comprehensive antitrust legislation to rein in the power of “Big Tech.” Whatever its merits, however, the bill isn’t really based in antitrust law and policy. Rather, it’s an ad hoc set of new rules which replace the current standards for antitrust enforcement based on market power and consumer welfare with a more generalized approach which targets just one industry — online platforms. The Senate bill looks at platforms with a large number of users and assumes excessive market power as a result of size, forgoing the need for economic analysis required to prove illegal monopoly power. The bill then imposes additional competitive requirements onto this predetermined set of companies.

A genuine antitrust analysis would examine not just firm size, but the conditions of the market in which a company operates, the presence of direct competitors, and its potential for consumer harm. Instead, the Senate bill takes a cookie cutter approach to antitrust enforcement: An online platform that hosts third party business users with over 50 million U.S. monthly active users (or 100,000 business users) and a market capitalization or net annual sales over $550 billion should be subject to different rules regarding competition. Essentially, a company-specific carveout without precedent in antitrust law.

There is a demonstrated need for changes in how antitrust law is enforced in order to encompass the business models of today’s digital platforms and e-commerce sites. However, the Senate bill fails to offer a rigorous economic analysis of digital markets, fundamentally changing enforcement methods in ways unacknowledged by the bill’s supporters.

This report explores three ways in which the Senate bill falls short:

• For the past 40 years, U.S. antitrust enforcement has been based on the assessment of quantifiable harm resulting from a firm’s market power, which most often takes the form of price effects. Supporters of the Senate bill, however, make no such assessment.

• In addition to being incompatible with current antitrust law and practice, the American Innovation and Choice Online Act’s size-based model would put American companies at a competitive disadvantage against other big competitors in global markets.

• Businesses such as internet platforms with low costs and significant network effects require a more sophisticated approach to examining consumer harm which accounts for damage to consumers other than rising prices. This might include adverse changes to company policies or reduction in accessibility of a service and may, in the end, warrant additional regulation. The current proposed legislation does not make such a case.

Today’s dominant technology companies may warrant scrutiny under antitrust law, but to investigate the merits of this claim it is critical that assessment of an illegal monopoly is based on market power rather than size. By considering metrics of consumer harm beyond price effects, it is possible to evaluate harmful market power in a way that considers the nature of these growing industries without discounting the additional value to the consumer presented by companies with large network effects.

“The American Innovation and Choice Online Act is not based on sophisticated economic analysis of how digital markets work. The size-based, company-specific approach fails to account for the reality of the global market for online platforms, and is a departure from the precedent of assessing market power prior to imposing rules associated with competition,” writes Malena Daileyin the report.

The report dives deep into the history of U.S. competition policy, and outlines the shift in theories surrounding antitrust enforcement since the 1970s. The ways in which the Klobuchar-Grassley-led S. 2992 — the American Innovation and Choice Online Act — misaligns with current antitrust enforcement could have unintended consequences if enacted, such as limiting U.S. technology leadership, overregulating a fluctuating global market, and unfairly singling out four of America’s most successful companies.

“There is a demonstrated need for changes in how antitrust law is enforced in order to encompass the impact of digital platforms and e-commerce. However, the Senate bill fails to offer a rigorous economic analysis of digital markets, fundamentally changing enforcement methods in ways unacknowledged by the bill’s supporters,” Ms. Dailey argues about S. 2992.

The report explores three ways in which S. 2992 falls short in responding to concerns regarding competition, arguing that this bill fails to assess “Big Tech’s” market power and alleged quantifiable harm to consumers, puts American companies at a competitive disadvantage against other big competitors in global markets — notably, giving China the upper hand in technology leadership — and establishes overly broad, potentially damaging standards.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Today, the Progressive Policy Institute released a new report on the challenges United States policymakers and regulators face in establishing oversight for the rapidly growing — and increasingly volatile — cryptocurrency and digital asset market.

Cryptocurrency has faced fitful bursts of growth and decline since its inception in 2008, with a dramatic recent crash from $3 trillion in November 2021 to $1.3 trillion in mid-May 2022. According to the report author, on any given day, more than $90 billion in digital assets change hands.

The report is titled “The Cryptocurrency Conundrum: The uncertain road toward a coherent oversight structure,” and is authored by Rob Garver.

“The crypto ecosystem’s explosive growth might continue, bringing more and more people into the universe of digital assets, with real-world effects on the financial security of individuals and families,” writes Rob Garver in the report. “Should some of the more promising use cases of blockchain technology prove viable, the crypto ecosystem has the potential to significantly transform areas as diverse as cross-border payments, management of public assistance programs, and online commerce.”

As policymakers look to regulate and provide oversight to this market, they must weigh the benefits and costs of who regulates the market and how heavy of a hand is used in regulation. Garver’s report asks if the unique nature of cryptocurrency requires a new, regulating body, or if Senators Gillibrand and Lummis’ recently introduced legislation proposing regulation through the Commodity Futures Trading Commission (CFTC) is the path forward. Garver also explores security and consumer protection issues faced by the industry, and explores the tax treatment experienced by investors.

Rob Garver is a freelance writer based in Alexandria, Virginia. He has covered banking and financial services policy for more than 20 years, and currently edits the BankThink section for American Banker.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Lindsay Mark Lewis, Executive Director of the Progressive Policy Institute, released the following statement in response to mounting Democratic criticism of the Klobuchar-Grassley bill’s content moderation provisions.

“Democratic Senators are rightly raising red flags about S. 2992, especially content moderation provisions inserted in the bill in a bid to gain Republican co-sponsors. While bipartisanship is often a virtue, it shouldn’t be purchased at the price of making huge concessions to pro-Trump Republicans like Sens. Ted Cruz and Josh Hawley. Rather than asking Senators to vote for a poorly drafted bill, these and other glaring defects should be fixed.

“As reported today, Senators Schatz, Wyden, Baldwin and Lujan are standing up to protect Americans from online falsehoods, conspiracy theories and hate speech from right-wing extremists. Sen. Schatz’s amendment affirming tech companies’ responsibility and ability to moderate online content should be the starting point for a new and better competition bill.

“S. 2992 is supposedly intended to update U.S. antitrust laws, but as PPI has pointed out repeatedly, it offers little convincing evidence that competition is lacking in America’s dynamic tech and ecommerce sector. To make matters worse, the bill also caves to right-wing demands to flood the internet with Trump-style lies and disinformation.

“This alone is reason enough for Senate leaders to send the bill back to the drawing board.”

President Biden’s policies have helped to subdue the COVID pandemic and put people back to work. But he’s getting little credit because Americans are transfixed by soaring prices for fuel, food and other necessities.

Inflation hovers like an alien spaceship over the Democrats’ midterm election prospects. U.S. voters say they trust Republicans over Democrats to handle it, by a whopping 19 points. They also give Republicans a 14-point lead on managing the economy.

To make matters worse, some congressional Democrats are pressing for a vote this summer on ill-conceived “antitrust” legislation aimed at dismantling America’s most innovative and competitive tech companies.

With inflation eating away at working families’ purchasing power, it’s hard to imagine a more effective way for Democrats to show they are out of touch with voters’ everyday economic struggles.

Yet again, party leaders again are letting the progressive left’s ideological zeal dictate their economic agenda. That’s triggered private grumbling by some Senate Democrats facing competitive re-election campaigns this fall. California Democrats who represent lots of tech workers understandably are balking, too. In general, however, the party’s pragmatic, pro-growth wing, which should be a forceful champion for U.S. high-tech innovation, has yet to find its voice.

Sens. Amy Klobuchar and Chuck Grassley, architects of the Senate anti-tech bill, insist that it’s a popular and bipartisan measure. But there’s no discernible public groundswell for breaking up or drastically regulating big tech companies. In fact, market concentration and antitrust don’t even register when voters are asked to name their top concerns.

Instead, the anti-tech crusade springs from the fevered brow of the nation’s political class. It’s propelled mainly by left-leaning academics, activists and journalists, business-bashing liberals like Sen. Elizabeth Warren, and a smattering of Trumpist Republicans like Sens. Ted Cruz and Josh Hawley. The left claims that “Big Tech” uses its market power to quash competitors, while the right whines about social media platforms censoring Donald Trump and other veracity-challenged conservatives.

Americans do have some qualms about big tech companies, even if they aren’t top of mind. In opinion research PPI has commissioned, battleground voters were most worried about their privacy and data security. They are less concerned about market power, and in fact are more inclined to see the size of U.S. tech companies as an advantage for our workers and economy.

Although presented as an update of U.S. antitrust laws, the Senate bill does not tackle market concentration across the U.S. economy. Instead, it draws a bead on a handful of big tech companies: Alphabet (formerly Google), Apple, Amazon, Meta (formerly Facebook) and perhaps Microsoft.

The anti-tech coalition evidently sees big as synonymous with bad. Amazon, they say, takes advantage of network effects to drive consumers to its online marketplace and provide popular products and services that brick-and-mortar stores can’t match. The big platforms also are accused of preferencing their own products and services in searches, even though the same could be said about the shelf placements in your friendly neighborhood grocery stores. Apple and Android control the sale of apps for their smartphones not to assure quality and data security, but to rake off lucrative fees. All the companies are accused of gobbling up potential competitors.

Big, powerful companies always merit close scrutiny. But tech’s foes haven’t made a convincing case that they harm U.S. consumers, throttle competition or stifle innovation in the vibrant tech-ecommerce ecosystem.

Consumers won’t be happy if Congress forces tech platforms to cut back or spin off integrated services they’ve come to rely on, such as Google Maps and Amazon Prime’s free next-day shipping. Google’s instant search results would be subject to endless second-guessing by regulators and rivals. People might lose access to Amazon Prime as well as the “Fulfillment by Amazon” services offered to hundreds of thousands of small businesses that sell on the behemoth’s platform. Smartphone users could be vulnerable to malware installed on side-loading apps not vetted by device manufacturers.

U.S. workers wouldn’t be any better off either. According to calculations by PPI economist Michael Mandel, the tech-ecommerce sector has replaced the health-care industry as the economy’s biggest job creator, over the past five years accounting for 40% of all job growth in the U.S. economy.

These jobs also pay well. Average tech-ecommerce pay is higher than average manufacturing pay in almost every state, says Mandel. Production and nonsupervisory workers in the warehousing industry, which includes most fulfillment centers, have seen their hourly pay jump by 15% over the past year.

While all sectors have been hit by rising prices, inflation has been notably restrained in the digital sector — the opposite of what you’d expect if it were truly dominated by tech monopolists busy snuffing out competition. Online prices increased by only 2.9% in April compared to a year earlier, according to the Adobe Digital Price Index.

Finally, unraveling the nation’s most dynamic tech companies would undermine U.S. innovation and global competitiveness. Biden says America is locked in a race with China for tech mastery; gutting tech companies would be akin to shooting ourselves in the foot.

So Democrats have a choice to make. Will they join left- and right-wing populists in taking a sledgehammer to America’s most successful companies? Or will they look to correct abuses in a smart way that doesn’t hamstring innovative companies that are investing at home, creating good jobs, keeping prices low, and helping America outcompete China?

Marshall is the president and founder of the Progressive Policy Institute.

A new report from the Progressive Policy Institute (PPI)’s Innovation Frontier Project finds inflation in the digital sector is still low, despite rapid price increases in much of the rest of the economy. Moreover, the deflationary influence of the digital economy has not been fully captured in official measures of inflation

The report is authored by world-renowned economist Marshall Reinsdorf, and is titled “Is Inflation Still Low in the Digital Economy?”. Prior to opening his own independent research consultancy, Mr. Reinsdorf was senior economist at the International Monetary Fund and president of the International Association for Research in Income and Wealth. Prior to joining the IMF, he was chief of the National Accounts Research Group at the U.S. Bureau of Economic Analysis.

“Given the value of technology in moderating inflation, policymakers should seek opportunities to promote uses of digital technology to enhance growth and promote price stability,” writes report author Marshall Reinsdorf.

“Four decades of relatively low inflation have made the current inflation figures particularly troubling. Over this same time, advances in the digital economy have greatly increased the speed of communication and access to information, saving Americans substantial amounts of time and money. Given these continuous improvements, recent inflation figures may be overstated. More accurate price reporting would help economic policymakers and consumers take action to counteract inflation’s effects on government and household budgets,” Mr. Reinsdorf concludes.

Reinsdorf also lays out why the frequent introductions of new models and new products and rapid growth of e-commerce make inflation in the digital economy challenging to measure. Correcting these blindspots would give economists and policymakers a better picture of the role of the digital economy in easing inflation.

Read the report and expanded policy recommendations here:

Based in Washington, D.C., and housed in the Progressive Policy Institute, the Innovation Frontier Project explores the role of public policy in science, technology and innovation. The project is managed by Jack Karsten. Learn more by visiting innovationfrontier.org.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

A new report from the Progressive Policy Institute (PPI)’s Innovation Frontier Project warns that the proposed antitrust legislation would have far-reaching negative effects on competitiveness and technology leadership.

“The U.S. technology sector is facing barriers to its ability to advance its position in an increasingly competitive world. The package of antitrust legislation introduced in Congress may adversely affect the tech sector by limiting the ability of platforms to design new products, integrate existing ones and operate in downstream segments,” write report authors Ashish Arora and Sharon Belenzon. “In this report we highlight the potential impact of these limitations on American science and technology leadership. We examine the role that big firms play in advancing U.S. technology, the foreign competition they increasingly face, and the fragile nature of the U.S. innovation ecosystem.”

According to the report, the package of antitrust legislation moving through Congress would limit tech companies’ ability to integrate new products, promote new features, and compete in new market segments. Antitrust regulations that reduce the size and limit the scope of tech firms weaken their incentives to make the large-scale, long-run investments in science and technology vital for national security and economic prosperity.

Additionally, at a time when the United States critically depends on a handful of firms to pursue large scale research projects, such proposals would play into the hands of foreign rivals. U.S. leadership in four of the five emerging technologies identified by the Biden Administration as a national priority would be adversely impacted by proposals to restrict digital platforms.

Read the report and expanded policy recommendations here:

This report was authored by Ashish Arora and Sharon Belenzon of Duke University. Mr. Arora is the Rex D. Adams Professor of Business Administration at the Duke Fuqua School of Business. He received his PhD in Economics from Stanford University in 1992, and was on the faculty at the Heinz School, Carnegie Mellon University, where he held the H. John Heinz Professorship, until 2009. Mr. Belenzon is a professor in the Strategy area at the Fuqua School of Business of Duke University and a Research Associate at the National Bureau of Economic Research (NBER). His research investigates the role of business in advancing science and has been featured in top academic journals, such as Management Science, Strategic Management Journal and American Economic Review. Mr. Belenzon received his PhD from the London School of Economics and Political Science and completed post-doctorate work at the University of Oxford, Nuffield College.

Based in Washington, D.C., and housed in the Progressive Policy Institute, the Innovation Frontier Project explores the role of public policy in science, technology and innovation. The project is managed by Jack Karsten. Learn more by visiting innovationfrontier.org.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

A new paper from the Progressive Policy Institute (PPI) digs into the radical transformation of both the social and security considerations of digital privacy on a global scale, weighing the three pillars of the issue: the legal rights of the consumer, data security, and innovation.The report is titled “Why Digital Privacy Is So Complicated” and is authored by PPI’s Economic and Data Policy Analyst, Jordan Shapiro.

The paperlays out the privacy models of the United States, Europe, and China, and also examines the models adopted in the United Kingdom, Canada, and India. Report author Jordan Shapiro examines each country’s current social and legal structure, the technical design of security and transparency, and the economic implications of privacy and innovation.

“Ultimately, a holistic approach to digital privacy is what’s missing in the global efforts to strengthen data privacy,” said report author Jordan Shapiro. “Here in the U.S., we have an opportunity to replicate what’s working – and avoid what isn’t – from our international partners’ approaches to digital privacy. To protect consumers, we need to refocus our efforts around privacy to include comprehensive technical security requirements and measures to better protect the individual consumer. At the same time, we need to strengthen privacy rules that support innovation.”

Read and download the full report:

Jordan Shapiro is an Economic and Data Policy Analyst at PPI. Prior to joining PPI, she worked as a data and innovation research consultant supporting businesses and non-profits to understand the interplay between technology and public systems.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visitingprogressivepolicy.org.

The exact definition of digital privacy is complex, imperfectly aligned with typical understandings of privacy in an analog context. Historically, the vast majority of human actions and interactions existed beyond the scope of surveillance. Today, it’s nearly impossible to go about our daily lives without digital tools that facilitate modern life, but also collect data about individuals. When this growing flood of data is linked to an individual it is called “personal identifying information” (PII), the centerpiece of the debate over digital privacy.

The discussion of digital privacy is complicated precisely because it operates on three distinct but interrelated levels. First, privacy’s social and legal dimensions depend on whether individuals, corporations, or governments are assumed to hold primary rights to personal data collected about those individuals. In Europe, for example, the individual holds primary rights over their data, while in China, the state takes precedence.

The second level of the privacy discussion addresses data use and the technical protection and security of personal information to safeguard it from unwanted intrusion or theft while allowing individuals transparent access to their data. These complicated technical issues arise no matter privacy’s social and legal structure.

The third level of the privacy debate deals with the economics of PII. How does the chosen privacy model interact with innovation and growth? And how can it be assured that individuals get the appropriate benefits from their data?

This paper will lay out the privacy models of the United States, Europe, and China, with smaller sections on the United Kingdom, Canada, and India. For each area, we will discuss the social and legal structure, the technical design of security and transparency, and the economic implications of privacy and innovation. This paper sets out a framework for PPI’s ongoing privacy work. It lays the groundwork for future discussions of privacy legislation in the United States.

President Joe Biden rightfully focused the economic portion of his State of the Union address on jobs, inflation, and the need to boost investment at home. He rightfully claimed credit for more than 6 million jobs generated on his watch, and the steps his Administration is taking to cut costs for Americans.

But inexplicably, Biden did not cite some real economic success stories. On the job front, the most consistent job creator since the pandemic started has been the digital sector, with employment in the tech, broadband and ecommerce industries up by 1 million jobs since January 2020.

And even as prices for traditional goods like energy and autos have skyrocketed, digital economy inflation has remained almost non-existent. Two examples: the price of internet access services fell 1.3% in the year ending January 2022, according to the latest producer price report from the Bureau of Labor Statistics, released February 15. And the price of data processing fell by 0.3% over the same stretch.

Meanwhile the overall consumer price index rose by 7.5% over the same stretch. The producer price index for final demand rose by 9.7%.

This lack of inflation in the tech, broadband and ecommerce worlds is a stunning phenomenon that deserves a lot more attention from the White House, which is debating internally whether to blame rising prices on corporate greed. Why are these digital companies holding the line on inflation — at least so far — when old-line industries are bingeing on double-digit price increases? After all, consumers can spend their dollars on digital goods and services just as easily as traditional goods, especially during the era of Covid-19.