The Mosaic Economic Project application process is now open for the March 2022 Women Changing Policy workshop, scheduled for February 28 to March 2, 2022.

“The Women Changing Policy workshop is an opportunity to connect with and learn alongside other diverse experts in fields where women are traditionally underrepresented” said Jasmine Stoughton, Project Lead. “Through our interactive workshop, participants hone the skills necessary to engage with lawmakers and the media.”

This is the fourth Women Changing Policy workshop. Previous workshops have included candid conversations with seasoned media professionals, policy leaders, and representatives from the United States Congress.

Applicants should be well established in their careers and eager to grow their profile in the policy arena. This workshop will be held in person in Washington, D.C., and the deadline to apply is February 11, 2022.

The Mosaic Economic Projectis a network of diverse women with expertise in the fields of economics and technology. Their programming aims to bring new voices to the policy arena by connecting cohort members with opportunities to engage with top industry leaders, lawmakers, and the media.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

In 2020, for the first time, the federal government financed the majority of health care spending in the United States. Though the use of health care services declined during the first year of the pandemic as the country shut down and people avoided unnecessary interactions with doctors and hospitals, health care spending still grew by 9.7% in 2020 over 2019, reaching $4.1 trillion — a record high. That’s because the federal government spent record high amounts on public health, provider relief funds, and a larger social safety net, propping up the health care industry as a whole.

The government stepped in to support the health care industry to help meet the demands of an unprecedented pandemic. Through Operation Warp Speed, bolstering the strategic stockpiles of drugs, funding clinical trials and guarantee purchase orders for vaccines, supporting health facility preparedness, and increased enrollment in public health programs, public health spending increased over two fold from the year prior. Excluding federal public health activity and programs, health care spending only increased 1.9% over 2019.

The federal government provided financial relief to health care providers, which propped up the sector even while people used less care overall. Hospital and doctor spending largely remained constant in 2020 thanks to federal assistance to health care providers through the Provider Relief Fund ($122 billion) and the Paycheck Protection Program ($53 billion). Even while health care utilization was down, hospital expenditures increased 6.4% in 2020, similar to the 6.3% growth rate in 2019. Physician and clinical service expenditures increased 5.4%, more than a percentage point higher than the 4.2% growth in 2019.

Medicaid and the Affordable Care Act (ACA) served as a safety net as many people lost jobs. Though the pandemic led to huge economic and employment downturns, the number of uninsured people declined by 0.6 million, or 1.9%. This was in stark contrast to the great recession when 9.3 million people lost their health insurance tied to employment. This time, safety net programs like Medicaid and subsidies available through the ACA kept people from losing health care coverage during a public health emergency. Medicaid and CHIP enrollment increased to 83.2 million, up nearly 18% since February of 2020. Because many people didn’t use services or lost their private sector coverage, spending on health care by private businesses declined 3.1% in 2020 compared to a 3.8% increase in 2019.

The pandemic’s impact on the overall economy and the health care sector was unprecedented. The GDP contracted by 2.2% (the largest drop since 1938), but because of efforts to support the health care sector, the health spending share of GDP was 19.7%, a two-percentage point increase from 2019 (17.6%).

While there were many failures throughout the pandemic, the government stepped in and mitigated a lot of the damage that could have happened to the health care sector. It supported hospitals as COVID cases surged and demand for other types of health care services waned, it protected people from losing health care coverage, and it partnered with private industry to develop and distribute vaccines at an unprecedented speed. Democrats shouldn’t forget to highlight the successes of these programs as they seek to run on their records in 2022.

On a new episode of Radically Pragmatic, PPI’s Mosaic Economic Project examines the findings of the 2021 Greater New Orleans Startup Report. The episode explores topics such as the growth, resiliency, and economic sustainability of New Orleans – including the effects of increased remote work options – and dives into solutions to bridge gaps in race and gender equity in critical areas from entrepreneurship to COVID relief.

Hosts Jasmine Stoughton and Crystal Swann were joined by Emily Egan, Director of Strategic Initiatives at the Albert Lepage Center for Entrepreneurship and Innovation at Tulane University, and Ann Marshall Tilton, Community Engagement Manager at the Albert Lepage Center.

Read the 2021 Great New Orleans Startup Report here.

Learn more about the Mosaic Economic Project here.

Learn more about the Progressive Policy Institute here.

On a new episode of the Radically Pragmatic podcast, PPI’s Mosaic Economic Project examines the findings of the 2021 Greater New Orleans Startup Report. The episode explores topics such as the growth, resiliency, and economic sustainability of New Orleans – including the effects of increased remote work options – and dives into solutions to bridge gaps in race and gender equity in critical areas from entrepreneurship to COVID relief.

Hosts Jasmine Stoughton and Crystal Swann were joined by Emily Egan, Director of Strategic Initiatives at the Albert Lepage Center for Entrepreneurship and Innovation at Tulane University, and Ann Marshall Tilton, Community Engagement Manager at the Albert Lepage Center.

Listen to the podcast here:

The Mosaic Economic Project is a network of diverse women with expertise in the fields of economics and technology. Mosaic programming aims to bring new voices to the policy arena by connecting cohort members with opportunities to engage with top industry leaders, lawmakers, and the media.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Will Marshall, President of the Progressive Policy Institute, released the following statement on the one-year anniversary of the January 6th insurrection at the United States Capitol:

“One year ago today, a lame duck president incited a mob of followers to storm the Capitol to overturn the 2020 election results. Dozens of police officers were injured in the ensuing violence, which eventually claimed five lives.

“For orchestrating this seditious and deadly attack on our elected representatives, Donald Trump was rightly impeached for a second time. But Congressional Republicans, in violation of their oath to defend the Constitution, failed again to hold Trump accountable for his lawless conduct.

“Their cowardly dereliction of duty opened the door to Trump’s despicable campaign over the past year to undermine public faith in the integrity of U.S. elections and launch what amounts to a coup attempt against our legitimately elected president, Joe Biden. It will fail, but not before eroding confidence at home and abroad in America’s commitment to democracy.

“From Trump, we can expect nothing but self-aggrandizing lies. Looking ahead, the deeper danger comes from the legions of Trump voters who seem willing to swallow his preposterous claims, and the elected Republican ‘leaders’ who lack the courage to stand up to his treacherous fabrications.

“That’s why Americans must never forget what happened on January 6th. The bipartisan House Select Committee’s investigation into the actions of the president and others who organized the insurrection must continue despite Republican stonewalling and disingenuous cries to ‘move on.’

“And what of the 147 Republican lawmakers who voted only moments after the outrage in the Capitol to support Trump’s bogus claims of a stolen election? Let’s make sure U.S. voters won’t forget their names when they go to the polls in this year’s midterm elections.”

###

Media Contact for PPI: Aaron White – awhite@ppionline.org

49 of the world’s 100 tallest buildings have opened in the last five years.

THE NUMBERS:

World’s tallest buildings*, 2600 BCE to present

YEARBUILDING HEIGHT 2010 2,716 feet (Burj Khalifa, UAE)

2004 1,666 feet (Taipei 101, Taipei) 1998 1,482 feet (Petronas Towers, Kuala Lumpur) 1974 1,450 feet (Sears Tower, Chicago) 1972 1,368 feet (World Trade Center, New York) 1931 1,250 feet (Empire State Building, New York) 1930 1,046 feet (Chrysler Building, New York) 1913 792 feet (Woolworth Building, New York) 1908 612 feet (Singer Building, New York) 1901 548 feet (City Hall, Philadelphia) 1311 525 feet? (Lincoln Cathedral, UK) ~2550 BCE 481 feet (Great Pyramid, Egypt)

WHAT THEY MEAN:

Stone buildings can’t get much above 500 feet, since the weight of the upper tiers will crack and break the load-bearing pillars and walls beneath. This is why the 481-foot Great Pyramid outside Cairo held the world’s-tallest-building title for 3,800 years, until topped by a few slightly higher Gothic cathedrals in the 13th century. The cathedrals in turn held their lead until the early 20th century — unless you count free-standing towers like the 555-foot Washington Monument (1884) or 986-foot Eiffel Tower (1889) — when Chicago engineers devised the steel-skeleton frame, using curtain walls held in place by steel girders to add another 750 feet of space, metal, and glass.

Computer-aided design and new alloys — for example, twisting facades to minimize wind torque, and lightweight cladding to resist heat — enabled another jump during the 1990s. The results accelerated in the last decade with a bloom, or rash, of ultra-high skyscrapers at 1500 feet and above, mostly in Asia and the Arabian Peninsula. As 2022 begins, 49 of the world’s 100 tallest buildings, and four of the top ten, have opened since 2017. Only 13 20th century buildings remain among the top 100, and only four opened before 1990. Eleven-year-old Burj Khalifa in Dubai remains largest of all, more than a half-mile tall at 2,717 feet or 828 meters. By location, the top 100-list maintained by the New York-based Council on Tall Buildings and Urban Habitat breaks down as follows:

China: 45 of the top 100 and five of the top 10, including second-place Shanghai Tower (2015) at 2,073 feet and fourth-place Ping An Tower in Shenzhen (2017). Hong Kong adds five more.

United Arab Emirates: 17, with Burj Khalifa’s 2,716 feet basically one old skyscraper’s height above the Shanghai Tower. Saudi Arabia’s competing “Kingdom Tower,” aiming for more than 1,000 meters (3,281 feet), stalled out at 1000 feet in 2018 after a contract dispute.

United States: 15, including 7 in New York — One World Trade Center, at 1,776 feet, is the world’s sixth-highest — along with 5 in Chicago, and one each in Philadelphia and Los Angeles.

The rest: 18, including five in Russia, four in Malaysia, four in Korea, two in Taiwan, and one each in Vietnam, Kuwait, and Saudi Arabia.

Once unrivalled in the count of very high buildings, the U.S. now ranks third. The American intellectual role in skyscraper design and construction, though, remains central. Specialized U.S. architecture firms in Chicago, New York, New England, and California remain at the core of worldwide tall building design, having designed seven of the current top ten and 24 of the 49 most recent entries to the list.

Burj Khalifa in the UAE stands at 2,716 feet.

FURTHER READING

New York’s Council on Tall Building and Urban Habitat lists the world’s 100 tallest buildings.

Burj Khalifa features 160 floors, a spiral shape to minimize wind torque on the upper levels, specialized glass and heat-resistant glazed aluminum/stainless steel cladding on the outer walls.

San Francisco-based Gensler designed the 2,073-foot Shanghai Tower, with “sky gardens” on the 37th of its 127 floors. BEA unromantically considers this an export of “architectural services”; in this sense, U.S. exports average about $900 million per year, against $135 million in imports. Read more from Gensler on the Shanghai Tower.

Is China slowing down? Central government puts a cap on ultra-tall, weird, or “xenocentric” buildings.

A brief survey of three earlier tall-building eras:

1. Pyramids & Ziggurats, Middle East, 2600 BCE to 2000 BCE: Pyramid-building began with Djoser’s 203-foot Step Pyramid around 2650 BCE and peaked a century later with Khufu’s 481-foot Great Pyramid. Just outside modern Cairo, this building held the world’s-tallest-building title for 3,800 years, even if nobody was around to measure and compare. Not just a lame pile of rocks, the G.P. is a “smart pyramid” with a complex interior design of chambers, tunnels, and ventilation shafts meant for practical, religious, and perhaps astronomical purposes, all pointing to sophisticated architectural drafting and engineering as well as lots of donkeys and human labor. The slightly younger ziggurats in neighboring Sumer and Akkad were made of brick. The squishier material means they couldn’t be as tall, and topped out at about 170 feet, with small temples on top.

The Ziggurat of Ur is solid brick all the way through, with a (long-vanished) moon goddess temple on top, built around 2100 BCE per order of Sumerian King Ur-Nammu. Read more from Iraq Heritage.

Book recommendation: The Babylon ziggurat “Etemanki” supposedly had “hanging gardens”, like the Shanghai Tower but open-air. Herodotus describes the ziggurat — eight tiers also with a temple on top — but doesn’t mention any gardens. British Assyriologist Stephanie Dalley investigates, and concludes that they probably existed but were somewhere else.

2. Gothic Cathedrals, Europe, 1200 to 1400: “It was as though the world had shaken herself and cast off her old age, and clothed herself everywhere in a white garment of churches…” Large buildings with enormous glass windows, hundred-foot stone pillars, and flying buttresses to relieve stress on load-bearing walls. Designed without printing presses, standardized weights and measures, or mathematics beyond flat-plane geometry, cathedrals overtook pyramids in the 14th century and with the exception of Philadelphia’s 548-foot City Hall (1901) remain the world’s tallest stone-on-stone buildings. Lincoln Cathedral, completed in 1311, is said to been the highest Gothic cathedral, with a central spire rising to 525 feet. But the spire fell down in 1549 so we can’t be sure. The largest one still standing is Germany’s 512-foot Ulm Cathedral.

Read about Abbot Sugar and the 12th-century Gothic boom.

3. Skyscrapers, United States, 1908 to 1974: Steel-skeleton buildings surpassed cathedrals with the completion of the Singer Building (referring to the sewing machine company, not the arts) in New York City in 1908. The Otis hydraulic elevator system made sure people could get to the top floors, and architects devoted occasional floors to water tanks and pumps so penthouse suites and executive offices could get toilets that flush and faucets that spout water rather than sucking air. Woolworth quickly overtopped Singer, Chrysler hit 1,000 feet in 1930, then the Empire State Building in 1931.

Chicago’s William LeBaron Jenney, a Union army engineering corps vet, and Paris-trained architect, designed the first girders-and-curtain wall “skyscraper” — the 180-foot Home Insurance Building on South LaSalle, demolished to make way for the Field Building in 1931.

ABOUT ED

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank ProgressiveEconomy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

Republicans hoping to capitalize on high inflation have proposed a surprising solution: ending COVID-19 restrictions. But surrendering to COVID is the wrong cure for inflation. It would endanger public health without addressing the supply-chain snarls that are pushing prices higher. Ending pandemic inflation requires making the global economy a safe place to spend, work and live by continuing the fight against the virus.

The United States is enjoying an exceptionally strong economic recovery thanks in part to the bold stimulus actions lawmakers took last March. But businesses are raising prices, some because they and their competitors are bidding up the cost of workers and materials, and others simply because strong demand means that they can. Consumer prices were 6.8 percent higher in November than they were a year before, and almost half of households say inflation is hurting their finances.

Summary: Because of their mixed urban/rural nature, swing states are a magnet for digital “tech-ecommerce” jobs. Democrats should consider building their 2022 political narrative around support for the digital economy, which brings strong job growth, higher wages, and lower inflation to swing states.

1. This piece is primarily economic, not political. But to focus our analysis, we start with a list of eight potential 2022 Senate swing states: Arizona, Florida, Georgia, Nevada, New Hampshire, North Carolina, Pennsylvania, and Wisconsin. Adding or subtracting a state from this list doesn’t change the analysis appreciably.

2. For the most part, swing state employment is still below pre-pandemic levels, creating a handicap for the party in power. For example, Wisconsin had 260,000 fewer private sector jobs in November 2021 than in November 2019. The only swing state above pre-pandemic employment levels is Arizona.

3. Average hourly wage growth has significantly lagged national inflation in most swing states, That means real wages are falling on average in the swing states, an obstacle to making a positive economic argument. Once again, there is one exception, North Carolina.

4. However, voters in most swing states are benefiting from exceptionally dynamic job creation in the digital “tech-ecommerce” sector. The reason is not hard to understand. Swing states, by their nature, tend to have a mixed urban/rural character. Not surprisingly, ecommerce fulfillment centers are often sited in areas that are within easy driving distance of large populations but where land is relatively cheap, making them a good match for swing states. Similarly, software and internet operations looking to broaden out from the Bay Area and Boston will pick cheaper locations near to good urban amenities.

5. Digital employers gravitated to swing states during the Biden Administration. From the second quarter of 2020 to the second quarter of 2021, the most recent data available, swing states showed a 14% gain in tech-ecommerce jobs By comparison, the rest of the country only showed an 8% gain in tech-ecommerce jobs over the same period.

6. We’ve bolded the key numbers in the table below, which lays out the job gains by digital industry. Ecommerce fulfillment and warehousing jobs registered a 22% gain in the swing states, almost double the 12% gain in the rest of the country. The same thing held true for the electronic shopping industry (which mainly consists of those establishments that are in the technology end of electronic shopping but don’t do fulfillment). Also showing strong swing state growth was internet publishing, which also includes search and other “internet-type” companies.

By contrast, job growth in manufacturing and healthcare was weaker in the swing states than the rest of the country. These states see their future in tech and ecommerce.

Table 1. Swing States Lead In Digital Growth

Employment change, 20Q2-21Q2

Swing states

Other states

Computer and electronic manufacturing

-1.6%

-0.4%

Electronic shopping

18.5%

11.8%

Local delivery

12.4%

13.9%

Ecommerce fulfillment and warehousing

22.1%

12.3%

Software publishing

11.8%

8.7%

Data hosting

12.6%

6.1%

Internet publishing and other information services

14.6%

6.1%

Computer software systems

7.1%

3.5%

Tech-ecommerce (total)

14.0%

8.1%

Private

11.2%

10.6%

Manufacturing

5.0%

6.1%

Healthcare and social assistance

5.6%

6.4%

7. What are the positive economic stories in individual swing states? Digital employers in Arizona, Florida, Nevada, North Carolina, and Wisconsin are adding digital jobs at a faster rate than private sector jobs. Voters in North Carolina, for example, have benefited from 20% growth in tech-ecommerce jobs, almost double private sector job growth.

Table 2. Digital Jobs Drive Swing State Growth

Employment change, 20Q2-21Q2

Tech-ecommerce

Private sector

Arizona

16.7%

8.6%

Florida

18.2%

10.8%

Georgia

8.6%

10.4%

Nevada

24.6%

21.4%

New Hampshire

8.4%

13.4%

North Carolina

20.3%

11.5%

Pennsylvania

7.8%

12.4%

Wisconsin

10.2%

9.1%

Swing states

14.0%

11.2%

All other states

8.1%

10.6%

8. A strong economic narrative around digital growth in the swing states depends on wages as well. On average, tech-ecommerce jobs pay significantly more than the average for the private sector in every swing state. For example, in the second quarter of 2021, tech-ecommerce workers in swing states got paid at an average annual rate of $81,000, 39% more than the private sector average of $58,000. This includes the full range of tech-ecommerce jobs, from software developers to fulfillment center workers.

Table 3. Workers in Digital Jobs Are Paid More on Average

Annual pay, thousands of dollars, based on 21Q2

Tech-ecommerce

Private sector

Arizona

76

59

Florida

81

57

Georgia

83

60

Nevada

65

57

New Hampshire

111

71

North Carolina

86

57

Pennsylvania

81

62

Wisconsin

77

53

Swing states

81

58

All other states

123

66

All other states except California and Washington

96

62

9. The core of the tech-ecommerce job boom in the swing states is the expansion of ecommerce jobs. These jobs pay well for high-school educated workers. Amazon pays its starting distribution workers an average of $18 per hour. That’s roughly comparable to starting manufacturing wages in many parts of the country. Overall, ecommerce industries pay about 30% more than brick-and-mortar retail in swing states, on average. This is at the heart of a powerful political narrative of growth that creates better jobs.

Table 4. Ecommerce Industries Pay More than Brick-and-Mortar Retail

21Q2 pay in thousands at annual rates

Ecommerce industries

Brick-and-mortar retail

Arizona

48

41

Florida

49

39

Georgia

45

36

Nevada

46

39

New Hampshire

57

38

North Carolina

40

35

Pennsylvania

51

34

Wisconsin

45

31

Swing states

47

37

Other states

62

38

Other states ex California and Washington

51

37

10. Democrats have a chance to build a powerful economic narrative around strong digital growth in swing states. They should embrace this opportunity.

Ben Ritz is Director of the Center for Funding America’s Future at the Progressive Policy Institute, Jason Fichtner is Vice President and Chief Economist at the Bipartisan Policy Center, and Charles Blahous is the J. Fish and Lillian F. Smith Chair and Senior Research Strategist at the Mercatus Center.

Despite repeated warnings from Social Security’s trustees that the program is facing a growing financial shortfall, lawmakers seem to have reached a bipartisan consensus to kick the can down the road. If they continue procrastinating until Social Security’s trust funds near depletion in the 2030s, it will be impossible to save the program without abruptly cutting benefits for retirees or significantly reducing the lifetime incomes of young workers. Americans who rely on Social Security cannot afford to wait much longer for lawmakers to enact corrections.

Unfortunately, a new proposal that was the subject of a congressional hearing earlier this month, Social Security 2100: A Sacred Trust, moves in the wrong direction. It would worsen intergenerational inequities by providing substantial benefit increases for those becoming benefit-eligible in 2022-2026, while passing the costs to everyone else, especially young workers already getting the short end of the stick under current law. There is no justification for such discriminatory treatment. In fact, those who would receive the proposed windfall already benefit from superior treatment under current Social Security law, relative to those who would pay for it.

Mr. Ritz is the director of the Progressive Policy Institute’s Center for Funding America’s Future, which released a framework for paring down the Build Back Better plan in October.

Senator Joe Manchin of West Virginia seemingly dealt a terrible setback to President Biden’s agenda on Sunday, when he told Bret Baier of Fox News that he could not support the version of the Build Back Better Act passed by the House last month. Although Democrats were rightfully frustrated by the way in which Mr. Manchin expressed his concerns, he was raising a valid critique: This bill was deeply flawed, and the “compromises” his colleagues made did nothing to address the concerns he has been consistently raising since this summer.

Other Democrats may not realize it, but Mr. Manchin may well have given them a gift. They should’ve gone back to the drawing board months ago, when it first became clear that their budgetary gimmickry was turning the bill into a confusing mess. Now, they will have to — and if they revise the bill to cut the number of programs they propose while making the ones they do propose permanent and easier for Americans to navigate, it could deliver Democrats both lasting policy change and the political victory they so desperately need.

Remittances from overseas workers to poor and middle-income countries are double the size of all foreign aid programs.

THE NUMBERS:

Central American GDP and international income, 2020

$200 billion GDP $45.6 billion Exports $25.3 billion* Remittances from migrants $1.6 billion Foreign aid $3.4 billion Foreign Direct Investment

* Assuming about 95% of remittances to Central America came from the U.S. in 2020, as the World Bank has estimated for 2017 (most recent year available).

WHAT THEY MEAN:

Who changes the world? Governments, intellectuals, scientists, entrepreneurs, NGOs, and charities? Doubtless they do their part. But do not discount the power and generosity of humbler, less celebrated people. An example:

Small banks and wire services in Central American neighborhoods around the U.S. are busy this week, as Christmas money flows south from places like Maryland’s Wheaton or LA’s Pico Union to Chalatenango, Intipuca, and La Union. World Bank research suggests that these “remittance” flows to the five Central American republics totaled $25 billion in 2021, with about 95% of this total coming from the United States. About $55 million will likewise move from the homes of security guards and drivers in New Zealand to small Pacific island towns in Tonga and Samoa; $11.6 billion will arrive from the Gulf states to places like Medan and Dhaka, sent by Indonesian and Bangladeshi maids, clerks, nurses, and construction workers.

How significant is this? Three ways to answer the question:

(1) In the economic lives of recipient countries, sometimes very large. Central America joins the Pacific Islands, Central Asia, and the Caribbean among the world’s most remittance-reliant regions, and so provides an illustrative (if somewhat extreme) example. The $25 billion in remittance flows at the north end of the wire make up about 12.5% of a $200 billion regional ‘GDP’ (combining Guatemala, El Salvador, Honduras, Nicaragua, and Costa Rica) with peaks of 24% of GDP for El Salvador and Honduras. Meanwhile, in 2020 the five countries together (a) earned $45 billion from exports; (b) received about $1.6 billion in much-debated but relatively modest flows of foreign aid, and (c) received $3.4 billion in foreign direct investment from international businesses. Thus at the macro end, remittances from migrant workers and their families rank below (but not far below) trade as a source of income, and are five times the combined value of aid and FDI.

Moving the lens back, the picture shifts but does not fundamentally change. Twelve countries rely on remittances for more than 20% of GDP, with Tonga at 35% and then Somalia, Lebanon, South Sudan, Kyrgyzstan, Tajikistan, El Salvador, Honduras, Nepal, Haiti, Jamaica, and Lesotho. If we combine all low- and middle-income countries (using the World Bank definition but excluding China, Russia, and EU members Bulgaria and Romania), trade is easily the largest earner, with remittances a fairly distant second and about equal to FDI and foreign aid combined:

$14,210 billion GDP

$3,850 billion Exports

$462 billion Remittances

$267 billion Foreign Direct Investment

$175-$250 billion* Foreign Aid

* The aid total depends upon how one estimates Chinese aid programs. The OECD reports $175 billion from OECD members, plus Saudi Arabia, the UAE, Taiwan, and several other non-OECD donors. The scale of Chinese aid programs is uncertain, but probably large, with private-sector estimates going up to a maximum of ~$80 billion depending on one’s definition of Belt and Road Initiative loans.

(2) From the donor perspective, quite a lot. A Honduran-American population of about 1 million, for example, likely sent $5 billion in remittances this year. The median income for adult workers, by a Pew Research estimate, is around $25,000, which suggests that workers spent as much as a fifth of their earnings on remittances.

(3) From the recipient perspective, often of great value: Remittances seem most valuable to the poor and lower-middle class. Central America again provides some interesting examples. About 20% of families in El Salvador families receive remittances. A 2016 report for the Inter-American Development Bank reported that 70% of these recipients are women; that 47% live in rural provinces; that 70% have primary education or less, and that 79% are poor or “vulnerable”.

In this holiday season, one need not doubt the potential of thoughtful governments, energetic intellectuals and scientists, or entrepreneurs, NGOs and charities to change the world for the better. But the populist force of quite humble communities of migrant workers — tens of millions of Salvadoran waitresses and construction workers, Filipina nurses, Indonesian maids, Haitian cooks and security guards, Nigerian taxi drivers and Jordanian accountants — looks to be at least their match.

Closing note: PPI’s Trade Fact service will be closed next week and return in the New Year. We wish friends and readers a happy and peaceful holiday, grateful for our good fortune and mindful of those who have less.

FURTHER READING

Overview

The World Bank’s remittances page has figures by region and country for 2020; $701 billion in remittance flows, or about 1% of the world’s $75 trillion GDP. Bank experts trace $471 billion back to the source, with $70 billion of this coming from the United States; by comparison, USAID reports $51 billion in official U.S. foreign aid.

The Kingdom of Tonga (population 105,000, an hour’s flight southeast of Fiji when service is available) is the country most reliant on remittances, accounting for 48% of GDP, with money coming principally from New Zealand, the U.S., and Australia.

Miami-based Haitian Times on a COVID-era lifeline for Haiti.

Aid: The OECD’s Development Assistance Council page details $175 billion from OECD members and other sources (though not China) in 2020 aid by recipient.

Aid: The U.S. Agency for International Development’s data dashboard has U.S. foreign assistance figures by country, project, and topic.

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank ProgressiveEconomy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

Brexit is done and U.S. voters have fired Donald Trump, but the neo-nationalist uprising that gave rise to both continues to shake up transatlantic politics. No country has seen its traditional political order more thoroughly fractured than France.

President Emmanuel Macron, who is running for reelection next spring, leads a centrist party he created in a tour de force of political improvisation after leaving the Socialist Party shortly before his 2017 election. Long France’s leading party of the left, the Socialists have been decimated. Their presidential candidate, Paris Mayor Anne Hidalgo, barely registers in the polls with about 4 percent support.

The wild card in the race is Eric Zemmour, a political neophyte many observers are calling the French Trump. He is a writer and television pundit whose best-selling book, “Le Suicide Francais,” contends that immigration, globalization and a fast-growing Muslim minority represent fundamental threats to French values and culture.

As the U.S. Senate postpones its vote on the Build Back Better Act (BBBA) into next year, it’s becoming increasingly clear that lawmakers’ attempt to enact almost every major program proposed by President Biden on a temporary basis — rather than prioritize a few key programs or find enough revenue to sustainably finance all of his proposed programs permanently — threatens both the bill’s prospects for passage and the success of its core initiatives should the bill become law. Democrats must rethink and revise this approach to address the most urgent national needs and secure a successful legacy for President Joe Biden.

The problem became clear last week in part thanks to a new estimate from the nonpartisan Congressional Budget Office, which suggested that the policies in the House-passed version of the BBBA would cost over $4.7 trillion between now and 2031 if none of them are allowed to expire before then. CBO’s analysis has given pause to Sen. Joe Manchin (D-W.Va.), who has consistently said he would only commit to supporting a bill that increases federal spending by no more than $1.5 trillion over the next decade and fully covers offsets the additional cost. Manchin holds the crucial 50th vote needed to pass any bill through the Senate without Republican support, so the bill cannot move forward until his concerns are addressed.

This month’s glamor rocket, rising next Wednesday from the Arianespace launch site in French Guiana, is an “Ariane 5”: a 170-foot tower weighing 780 tons and carrying 180 tons of liquid hydrogen/liquid oxygen fuel. Operated by the European Space Agency, its task is to lift the 44-foot, 7-ton, $9.7 billion James Webb Space Telescope off the Earth (pictured below), and direct it to “Lagrange 2,” a stable orbital a million miles from the Earth and well beyond the Moon. Successor to the Hubble, the Webb carries a 360-kilo, 21-foot-in-diameter mirror faced with ultra-polished beryllium, along with a set of four detection instruments designed at NASA’s Goddard Space Center in Maryland. For the next decade, these will analyze infrared radiation in hopes of understanding exoplanet atmospheres, observing star and galaxy formation, investigating “dark matter,” and examine the very early universe.

The Webb is very much in the Gemini, Apollo, Skylab, Voyager, and Mars Rover tradition: a government-led, big-science. international (NASA: the Webb is an “international collaboration among NASA, the European Space Agency (ESA), and the Canadian Space Agency (CSA) abstract-knowledge-and-benefit-of-humanity project. Around this newest example of a familiar tradition, however, are hundreds of illustrations of a quite different and much newer space concept — about 1,400 more satellite launches, the large majority by private-sector rocket companies carrying small satellites meant for very prosaic commercial use rather than scientific exploration or public policy. Examples from this month’s launch schedule include:

> RocketLab Electron, from Mahia in New Zealand, carrying two communications satellites for BlackSky’s earth observation satellite network. This provides imaging services via a network of two dozen small satellites — about 135 pounds, smaller than the 184-pound Sputnik satellite of 1957 — orbiting about 270 miles above the Earth.

> Virgin LauncherOne, launched not from a pad on the ground but from a converted Boeing 747 flown from California, carrying two “nano-satellites” weighing about 5 pounds for Polish firm SatRevolution (along with eight for the U.S military). SatRevolution eventually hopes for a network of 1,024 low-orbit nanosats providing imaging to agricultural, business, and government clients.

> Space Falcon 9 from Cape Canaveral, with 51 small satellites for SpaceX’s “Starlink” system, meant as part of a future network of 42,000 small satellites at 350 miles providing “video calls, online gaming, streaming, and other high data rate activities” to areas the global fiber-optic cable system that carries most Internet traffic does not reach, at a projected cost of $10 billion or so — that is, about the same as the Webb.

Wednesday’s launch, then, underlines the continuing strength and romantic appeal of the 65-year-old tradition of government-led, science-first space exploration. This year’s parallel launches of its hundreds of small private-sector cousins suggest that, for the first time, civilian commercial space industry now operates on the same scale.

* Official counts of satellites are surprisingly inconsistent. The UN’s count reports 8,089 man-made objects in orbit at the moment; the Union of Concerned Scientists says “more than 4,550.” Either way, adding 1,400 more in a single year is a lot.

As the Webb heads for its million-mile orbit and commercial satellite networks multiply, a burning question: Which generation-old sci-fi show saw the future best? Two nominees:

“Boldly go”: Deep space exploration, international cooperation, frontiers of knowledge, and the common good

“20 Minutes into the Future”: Ubiquitous disposable low-orbit satellites, ruthless media competition, vast streams of addictive low-quality information, and social fracture

ABOUT ED

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank ProgressiveEconomy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

Clearly Americans are concerned about inflation. Prices for most food and energy products are soaring, which hits them right in the wallet. The Biden Administration finds itself on the political defensive, as prices increases are outstripping wage increases for most workers.

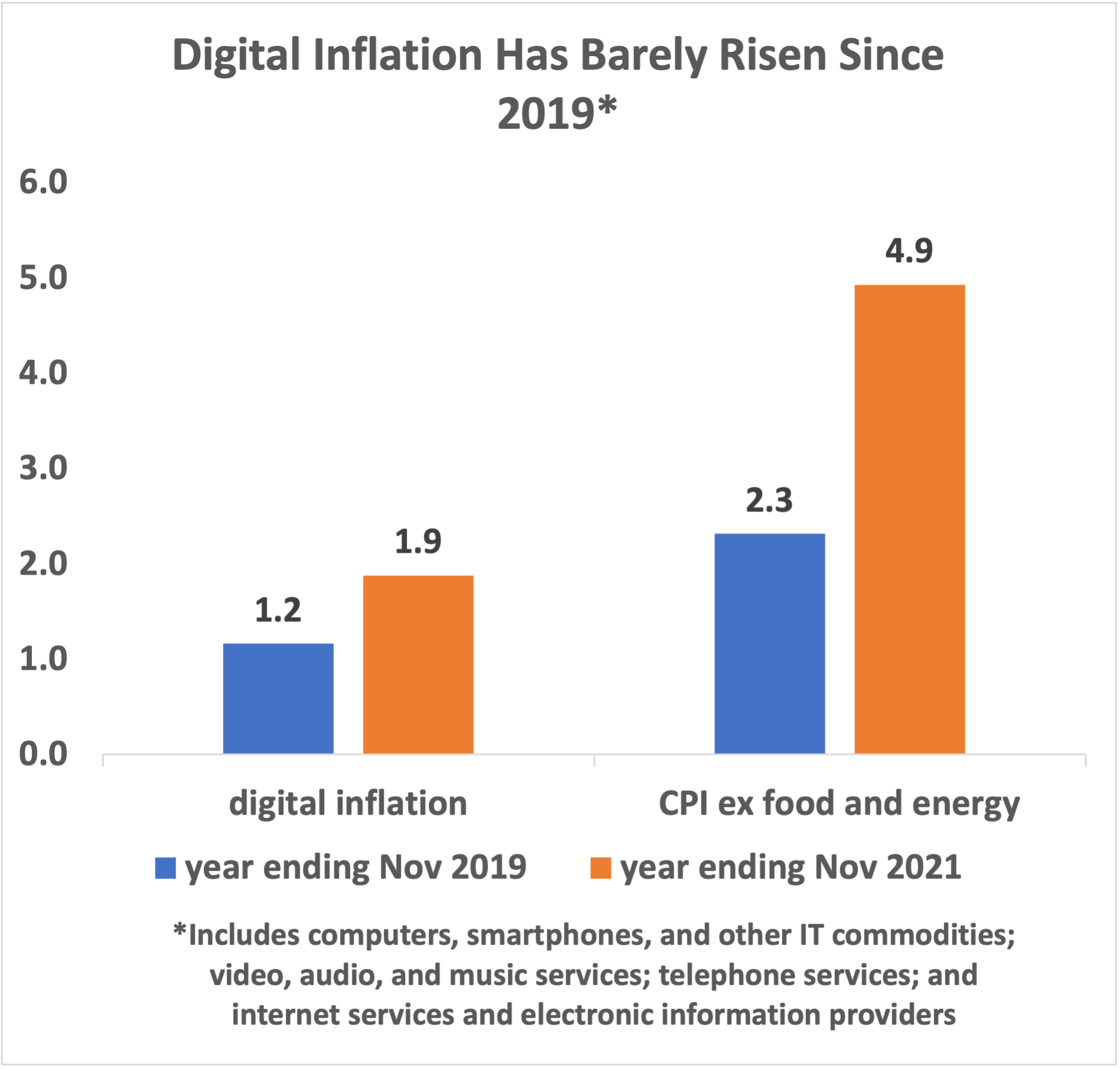

But here’s an important piece of good news that is not getting enough attention. Inflation remains low in the digital sector, even as it accelerates across much of the economy. Start with consumer inflation (as measured by the CPI). Over the past year, prices for digital consumer goods and services tracked by BLS (see graphic) have risen by only 1.9% overall, compared to 4.9% for CPI ex food/energy and 6.8% for total CPI.

Digital consumer goods and services include computers, smartphones and other IT commodities; video, audio, and music services; wired and wireless phone services; and internet services and electronic information providers.

The chart shows that digital consumer inflation has risen only 0.7 percentage points (PP) compared to November 2019, while consumer inflation ex food/energy has risen 2.6 PP. For example, the inflation rate for “internet services and electronic information providers” has only risen by 0.7 PP (from 1.5% to 2.3%).

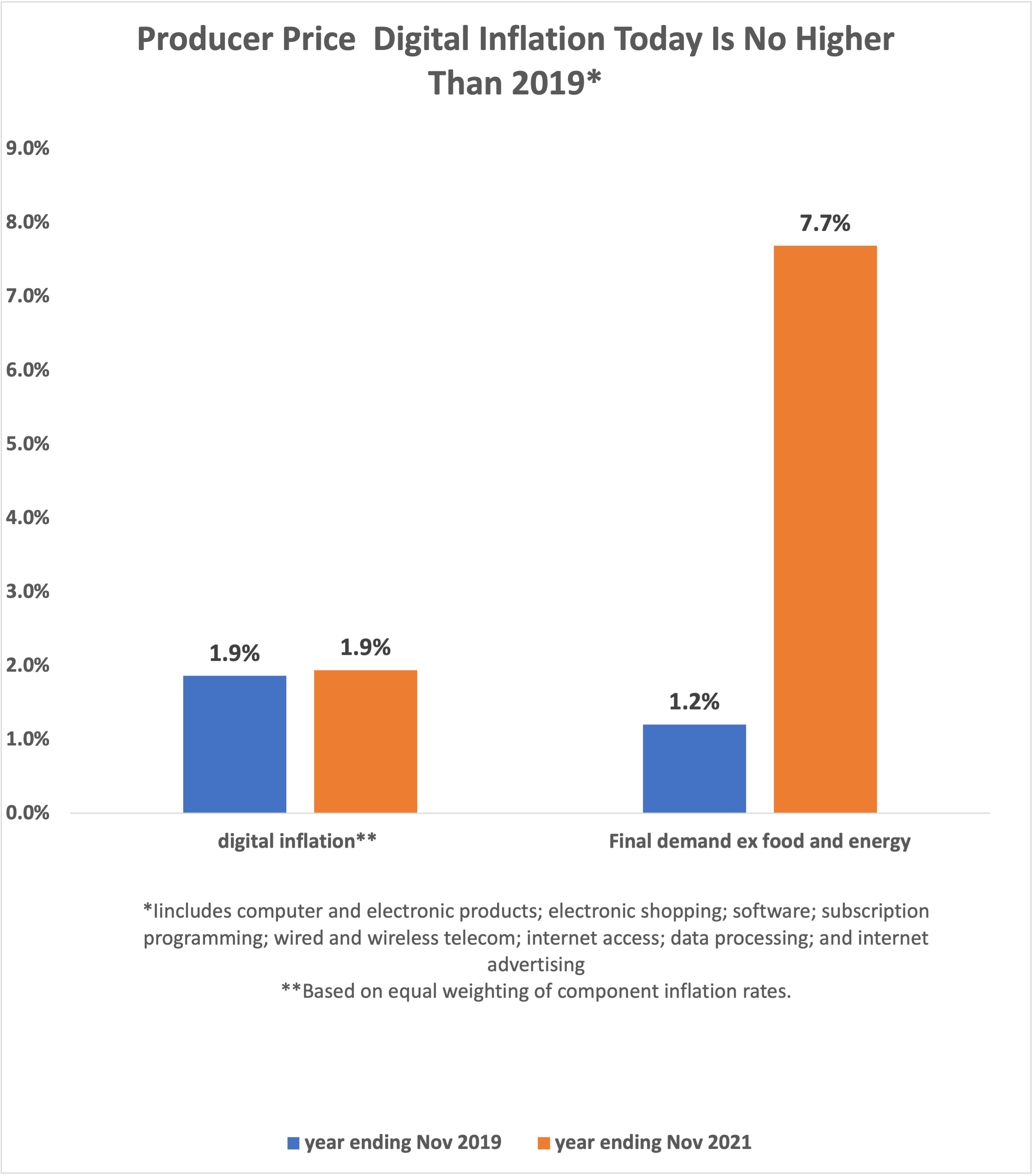

When we look at producer prices, we see a very similar phenomenon:Producer price inflation in the digital sector is no higher today than it was before the pandemic. Over the past year, producer prices for digital goods and services tracked by BLS (see graphic) have risen by only 1.9%, compared to 7.7% for final demand ex food and energy.

Final demand inflation (ex food and energy) accelerated from 1.2% in the year ending Nov 2019 to 7.7% in the year ending Nov 2021. But digital producer price inflation was roughly constant at 1.9% in both periods (this calculation was done giving equal weights to each component).

Digital producer prices include computer and electronic manufacturing; electronic and mail order shopping services; software publishers; cable and other subscription programming; wired and wireless telecom; internet access; data processing; and internet publishing and web search advertising.

Some examples: The producer price of internet access services rose by only 0.3% over the past year, up only slightly from the -0.3% rate in November 2019. The producer price charged by software publishers fell by 0.3%, a slightly bigger decline compared to two years ago. The producer price index for telecommunications, both business and residential, is running at a 1.1% rate, slightly down from the 1.2% rate in November 2019.

The digital sector is exerting a dampening effect on both consumer and producer price inflation, reflecting large productivity-enhancing capital investments by digital companies. Meanwhile productivity has lagged in sectors such as food processing, where prices are skyrocketing.

However, the digital sector is not getting enough “credit” in the overall numbers for holding down inflation. For example, there’s no doubt that the digital sector is much more important to Americans today than it was in pre-pandemic 2019. Yet the digital sector gets a smaller weight in the CPI today than it did in 2019, because spending on digital goods and services is a smaller share of the consumer basket. That’s good news, but it has a perverse effect on the calculation of the overall inflation rate.

We may have to move towards a time-weighted versus expenditure-weighted CPI. Certain tasks, like dealing with the DMV or health insurers, are more “costly” in time than money. Conversely, digital services save you time that doesn’t show up in the official stats.

Time-weighted CPI would take into account that digitizing tasks, including shopping, generally reduces time spent by consumers, while adding more regulations generally increases time spent.

A time-weighted approach to CPI would likely show higher inflation for rural and poorer Americans. It would allow us to think about how cutting government bureaucracy and saving the time of Americans actually reduces inflation.

From the political perspective, the Biden Administration can make a strong case that the digital goods and services that are so important to Americans these days are barely rising in price. And America’s digital leadership will continue to hold down price increases once the temporary supply chain issues abate.

With Russian troops massing on Ukraine’s border, and President Biden urging Russia’s Vladimir Putin not to invade, the geopolitics of Russian natural gas are growing increasingly intolerable. European gas imports are a mainstay of cash for Putin’s regime, with over one-third of Kremlin funding coming directly from oil and gas revenue, even as Russia increases repression at home, attempts to undermine democratic elections abroad and continues to use its gas as a geopolitical weapon against Europe.

If that weren’t enough, Russia is the world’s largest emitter of methane, a super climate pollutant whose mitigation is now crucial to global climate change efforts. The EU gets more than 25 percent of its total gas and half its gas imports from Russia’s leaky, antiquated gas production system with emissions of methane eight times higher than EU domestic gas. With methane leaks of at least 5 to 7 percent, the EU is addicted to Russian gas that increases warming twice as much as the coal it’s meant to replace.