A new report from the nonpartisan Congressional Budget Office shows that the amount of money spent by the federal government each year to service our national debt is on track to reach unprecedented highs within the next 10 years. These findings should give Congressional Democrats renewed urgency to pass a reconciliation bill that reduces federal budget deficits before the political window for action closes later this summer.

The good news is that the 2022 edition of the CBO’s annual Budget and Economic Outlook, published Wednesday, showed this year’s federal budget deficit falling dramatically from its $3.1 trillion peak in 2020. The decline was due almost entirely to the expiration of stimulus programs created to shepherd the economy through the COVID pandemic, and the rapid economic growth those programs helped facilitate. But these stimulus measures also came at a cost: They both increased our national debt and contributed to higher rates of inflation, which the Federal Reserve is now rapidly raising interest rates to combat.

Governed well, technological innovation can be a powerful force for good – connecting the world and providing tools to help address humanitarian, environmental, and health challenges while powering economic growth and recovery. But there is a growing international consensus for the need to adapt regulatory practices to realize the opportunities and mitigate the risks from innovation.

Enter “agile governance.”

Agile governance seeks to use dynamic, flexible, and iterative regulatory principles and techniques to achieve a more effective balance, one which helps us address societal challenges while also seizing the full promise of innovation. To support high-impact dialogue on these important topics Agile Governance for Our Future will feature leaders from government, business, academia, and civil society discussing their experiences with agile governance and offering new perspectives on how we can rethink regulation so that it is fit for purpose, now and into the future.

The program will include a keynote by Cass Sunstein (Harvard Law School), a fireside chat with Kent Walker (President of Global Affairs, Google), a panel of senior policymakers from the US, Europe, and Asia (invitations pending), and to bring a civil society perspective, remarks from Michael Mandel (Progressive Policy Institute).

President Joe Biden’s State of the Union address last week highlighted two of the greatest foreign and domestic challenges facing the United States. Russia’s invasion of Ukraine has undermined decades of peace in Europe, causing a humanitarian and geopolitical crisis while sending energy prices soaring. At home, inflation is rising at the fastest pace in 40 years and outstripping wage gains for many workers.

A new proposal offered by Sen. Joe Manchin (D-W. Va.) shortly after Biden’s address gives Democrats a strong approach for tackling both of these challenges — one that even has support from many progressives in the House with whom Manchin has often clashed. Manchin suggests Democrats pursue changes to the tax code and prescription drug pricing that would raise revenue without hurting our international competitiveness. He also recommends that this revenue be split evenly between deficit reduction and funding investments to expand domestic clean energy production, so America is less vulnerable to swings in energy costs.

A new report from the Progressive Policy Institute (PPI)’s Innovation Frontier Project, calls for United States policymakers to revamp our manufacturing sector to ensure the U.S. remains a leader in the global economy.

The report, authored by Keith Belton titled “Building a Stronger (More Complex) U.S. Manufacturing Sector,” provides policy recommendations, compares complexity in exports across several countries, and dives deep into theories behind manufacturing complexity, trade and competition.

“American manufacturing is on the decline, but we have a unique opportunity to kick this vital sector into high gear by making it more complex and diverse. We can strengthen it now with pragmatic legislation and look to our international competitors for a blueprint. With Keith Belton’s smart roadmap, our next generation of manufacturers could be working in a more secure, advanced and competitive manufacturing sector,” said Jack Karsten, Managing Director of the Innovation Frontier Project at PPI.

Belton argues that there are three public policy areas in which we can leverage complexity theory, including revising the national strategic plan for manufacturing at the White House Office of Science and Technology Policy, reviewing domestic supply chains, and establishing new statutory programs to strengthen the defense industrial base.

He also points to the need for the government to drive private sector investment in more complex manufacturing, which is being considered by Congressional leadership as the House and Senate reconcile the House-passed COMPETES Act with the Senate-passed United States Innovation and Competition Act (USICA). Global examples may be a launching point for the government as we look to replicate manufacturing competitiveness expansion in the next decade.

Read the report and expanded policy recommendations here:

Based in Washington, D.C., and housed in the Progressive Policy Institute, the Innovation Frontier Project explores the role of public policy in science, technology and innovation. The project is managed by Jack Karsten. Learn more by visiting innovationfrontier.org.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

When we look back on this period, a big inflation story will be the dog that didn’t bark. While prices for traditional goods like energy, food, and autos have skyrocketed, digital economy inflation has remained almost non-existent.

This relative lack of inflation in the tech, broadband and ecommerce worlds — including ecommerce margins — is a stunning phenomenon that deserves a lot more attention than it is getting. Why are these companies holding the line on inflation when old-line industries are bingeing on double-digit price increases?

One real possibility is that innovation and investment in the digital sector may have a dampening effect on inflation. Basic economics tells us that when tech and telecom companies spend tens of billions of dollars to create new capacity and deploy new technology, it’s going to be hard for anyone to raise prices, including themselves. PPI’s Investment Heroes report from last year showed that eight out of the top 10 companies in terms of domestic capital spending — Amazon, Verizon, AT&T, Alphabet, Intel, Facebook, Microsoft and Comcast — were in the tech, ecommerce, and broadband sectors. PPI has not yet done the most recent Investment Heroes report, but it’s clear that massive spending on information technology, 5G networks, and ecommerce fulfillment centers is holding down digital prices.

Let’s take a look at the data from the January 2022 Producer Price report, released February 15. Overall, this report show relatively high inflation, with final demand prices up 9.7% over the past year, and the prices of final demand less food and energy up 8.3% (the last line of the table below).

But in the middle of this price surge, tech and telecom prices showed relative small increases or even decreases. The table below compares pre-pandemic inflation (January 2019 to January 2020) with the most recent year (January 2021 to January 2022).

We see that in the latest year, the producer price of cable and other subscription programming, internet access services, and data processing and related services are all falling. The producer price of wireless communications is basically flat (we note that the consumer price of wireless is down by -0.5% over the past year, consistent with the picture painted by the producer price data).

Margins for electronic and mail order shopping services are rising at only a 1.1% rate (we’ll discuss these further below). Prices for advertising sales by internet publishers and web search portals are rising at a 3.5% pace, only slightly faster than the pre-pandemic inflation rate of 3.4%. Relative to January 2015, prices for advertising sales by internet publishers and web search portals are down by 16.9%.*

The one major exception to the low inflation story is the producer price of computer and electronic product manufacturing, which did take a substantial jump, probably in part because of supply chain disruptions.

Tech and Telecom Producer Prices Show Very Little Inflation

(change in producer prices)

Jan19-Jan20

Jan21-Jan22

Cable and other subscription programming

2.8%

-1.8%

Internet access services

0.5%

-1.3%

Data processing and related services

3.0%

-0.3%

Wireless telecommunications carriers

0.2%

0.1%

Information technology (IT) technical support and consulting services (partial)

1.4%

0.9%

Electronic and mail-order shopping services

1.4%

1.1%

Software publishers

-0.9%

1.1%

Wired telecommunications carriers

2.4%

2.6%

Internet publishing and web search portals – advertising sales

3.4%

3.5%

Computer & electronic product mfg

1.3%

4.1%

Comparison: Final demand for goods and services less foods and energy

1.6%

8.3%

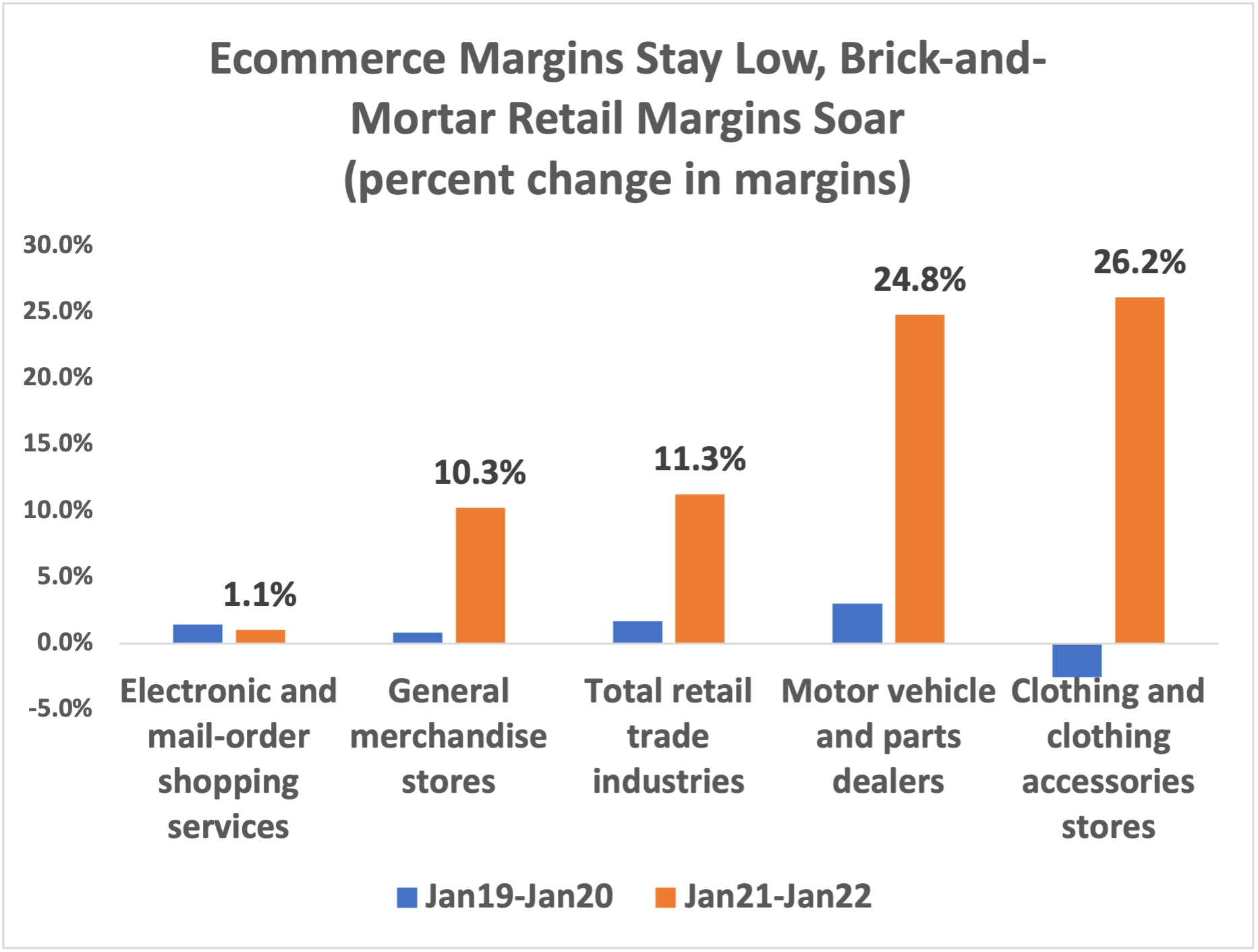

For retail industries, the BLS collects “margin” prices, which is the selling price of a good minus the acquisition price of the good. A bigger margin indicates that the retailer is either getting a higher profit, or having to cover increased costs for labor, energy, and other inputs.

The chart below shows that in the year ending January 2022, overall retail margins rose by 11.3%, a big jump over their pre-pandemic rate of 1.7%. General merchandise store margins rose by 10.3%, while the margins of motor vehicle and parts dealers rose by almost 25%.

Note that this increases could reflect the higher cost of running brick-and-mortar establishments during a pandemic, or they could reflect higher profits. But what is clear is that ecommerce margins have barely rose in the year ending January 2022.

*I looked at long-term trends in internet and print advertising prices in a 2019 paper, “The Declining Cost of Advertising: Policy Implications.”

In recent years, politicians on the far left have leaned on Modern Monetary Theory (MMT) to justify offering increasingly exorbitant spending proposals without plans to pay for them. Then roughly $6 trillion in deficit-financed stimulus approved by Congress in 2020 and 2021 provided policymakers a natural experiment to evaluate the claims proponents of MMT made. The results exposed the critical flaws in their approach, and rather than being able to take a victory lap, MMT is now on its last legs.

The idea that government should use deficit spending to support an economy in crisis is not unique to MMT – economists across the political spectrum supported an aggressive fiscal response in 2020. The core tenet of MMT is that a monetarily sovereign nation, like the United States, can always simply print however much currency it needs to buy whatever goods and services programs require. This is the lens through which proponents of MMT have argued that the only constraint on deficit spending should be inflation that materializes when the economy is utilizing all available resources.

The Surface Transportation Board (STB) has resurrected a 2016 regulation on “reciprocal switching” that would require railroads to “unbundle” their transportation services and provide competitors with access to their infrastructure, at regulator-determined prices and service requirements. There are plenty of problems with this proposed regulation, including discouraging private sector investment and increasing operational problems. In this note, however, we will focus on the broader question of why forced unbundling of railroad transportation services is precisely the wrong regulatory strategy for today’s “Supply Chain Economy,” leading to the potential worsening of supply chain disruptions and an increase in inflation.

To understand why a 2016-vintage regulatory approach is totally wrong for the 2022 economy, we must first consider the underlying economics of supply chains. A supply chain consists of a flow of goods, of course, from producers to buyers and consumers, via transportation links such as railroads, container ships, airlines and truckers, and intermediaries such as importers and wholesalers. But equally important is the flow of data which allows all of this production and movement to be coordinated.

As I note in a forthcoming article in the Winter 2022 issue of The International Economy, it is better to think of a supply chain as a “supply-and-data chain.” In that spirit, supply-chain management has been defined by the Association of Supply Chain Management as the “design, planning, execution, control, and monitoring of supply-chain activities with the objective of creating net value, building a competitive infrastructure, leveraging worldwide logistics, synchronizing supply with demand and measuring performance globally.”

Today’s domestic and global economies are built around these “supply-and-data chains.” A retailer like Walmart uses its knowledge of expected U.S. consumer demand to place orders with factories around the world months ahead of when the goods are needed, and then coordinates the movements of these goods to its far-flung stores. At every point along the way, the goal is to use data to reduce costs and ensure a smooth flow of goods.

This “Supply Chain Economy” is very different than the classic picture of an economy consisting of a series of unbundled arms-length transactions. In an economy with forced unbundling, factories would have to commit themselves to production runs without knowing if the demand existed, and without knowing if the transportation capacity was available.

In a supply chain economy, companies compete on the basis of who can best use data to organize production and logistics across the global economy, lowering costs and increasing reliability. The key is to take a big picture view across a wide range of markets, rather than focusing on competition in individual markets.

From this perspective, forced “reciprocal switching” would divert resources away from the optimization of supply chains. Railroads would have to give a high priority to moving goods in a way that met the reciprocal switching requirements, rather than lowering costs and speeding goods to their ultimate customers. The result would be more supply chain disruptions, and higher inflation. That’s not an outcome that anyone wants right now.

“Dynamic democracies should periodically reconsider existing policy norms to evaluate if they continue to serve policy goals well. If MMT seeks to change long-standing policy norms, the onus is on its advocates to persuade us that old norms do not serve us well and to communicate precisely what new norms will prevail and how they will affect the economy’s performance,” writes Eric Leeper in the report. “Until MMTers are ready to take these steps, their ideas must remain in the realm of guess and conjecture. In the meantime, we should apply to economic policy the basic principle we apply to health policy: follow the science. Economic science, such as it is, provides no support for MMT’s central claims.”

“For years, advocates of MMT have argued that policymakers should only care about budget deficits when the economy is facing inflation,” said Ben Ritz, Director of PPI’s Center for Funding America’s Future. “Now that inflation has finally materialized, they’ve moved the goalposts and left policymakers seeking answers about what to do in response. Dr. Leeper’s thorough deconstruction of MMT makes clear that they have none to offer. Democrats should reject this ‘supply-side economics’ of the left that is nothing more than a recipe for economic misery.”

For several years, politicians and leaders on the Far Left argued that a monetarily sovereign nation, like the United States, can simply print more currency needed to purchase goods and services for its constituents. As more exorbitant expensive spending programs were introduced and pitched to the American public, politicians often leaned on MMT to ensure voters that the economy could remain strong, even with deficit-financed spending. The only constraint on deficit spending, these advocates argued, was inflation.

This report breaks down several flaws in the economic thought behind MMT, including the constraints that ultimately finite resources place on governments, the inability of MMT to explain the relationship between inflation and demand when an economy is operating below its resource constraint, how it would overcome the structural and political challenges that prevent elected lawmakers from responsively managing inflation, and the indiscriminate approach it takes to the impact of different tax and spending policies, among others.

Mr. Leeper calls for the advocates of MMT to persuade the economic community that the standing norms of economic theory no longer serve us well, and to thoroughly evaluate the effects of the new economic theory with an eye on the practical and political implications of the proposal. He calls for the economic community, economic journalists, and policymakers to pause on active or passive exaltation of MMT until this evaluation is made, and continue to follow the science on economic theory and history – which unwaveringly points away from MMT’s fiscal financing plans.

Eric Leeper a contributing scholar for the Progressive Policy Institute. He is also the Paul Goodloe McIntire Professor in Economics at the University of Virginia, a research associate at the National Bureau of Economic Research, director of the Virginia Center for Economic Policy at the University of Virginia, and a visiting scholar and member of the Advisory Council of the Center for Quantitative Economic Research at the Federal Reserve Bank of Atlanta.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Launched in 2018, PPI’s Center for Funding America’s Future works to promote a fiscally responsible public investment agenda that fosters robust and inclusive economic growth. We tackle issues of public finance in the United States and offer innovative proposals to strengthen public investments in the foundation of our economy, modernize health and retirement programs to reflect an aging society, and transform our tax code to reward work over wealth.

By Eric Leeper

Contributing Author for the Progressive Policy Institute

EXECUTIVE SUMMARY

Modern Monetary Theory (MMT) gained popularity at a time when U.S. inflation was benign, income and wealth inequality was on the rise, and progressive politicians saw a political opportunity to pass big-ticket spending programs. To the nagging perennial question, “How do we pay for it?,” MMT serves up a tasty answer. You don’t need to raise taxes or reduce other spending. You don’t need to secure low-cost borrowing. A monetarily sovereign nation, like the United States, can create more currency to buy the goods and services that the programs require.

Large new spending programs often invoke in U.S. voters fears of persistent budget deficits and rising inflation. MMT delivers the reassuring message that those fears are grounded in defunct “orthodox” economic reasoning that limits the federal government’s capabilities: we have nothing to lose but our outmoded fiscal bromides and much to gain by replacing historic policy norms with fresh ideas. MMT explicitly ties itself to populist policies, self-labeling their plans “the birth of the people’s economy” [subtitle of Kelton (2021)]. Any sensible elected leader, whose vision is not impaired by conventional economic thought, would happily gobble up such a fiscal banquet.

MMT is the progressive counterpoint to supply-side economics. It supplants the claim that tax cuts pay for themselves with the claim that “…[federal] spending is self-financing” [Kelton (2021, p. 87), emphasis in original]. Both claims contain a germ of economic substance. Both claims are carefully crafted to provide elected officials seemingly plausible economic grounds to support their preferred fiscal policies (though at opposite ends of the political spectrum). Both offer policy makers an ideology freed of trade offs.

Because economic policy is too important to be reduced to catchy phrases and clever marketing, this essay analyzes MMT economics dispassionately. It does not assess the worthiness of MMT’s goals. Instead, it asks if MMT can achieve its goals without doing grave damage to America’s fiscal standing and, quite possibly, its economy. The answer: probably not.

MMT suffers from several flaws:

1. It denies a fundamental concept in economics: in a society with finite resources but unlimited wants, market prices adjust to induce individuals and policy makers to make trade offs that ultimately align supply and demand. Economics quantifies the costs and benefits of those trade offs to inform policy makers.

2. That denial leads MMT to see no need to offer a comprehensive theory of inflation. It maintains that inflation gets triggered when economy-wide demand for resources exceeds the economy’s resource limit, but has little to say about inflation and its determinants when, as it usually does, the economy operates below that limit.

3. MMT’s solution to inflation from high resource utilization is to raise “taxes,” without specifying which taxes. Governments have many tax instruments at their disposal—labor, sales, capital, wealth, and inflation—and each tax affects individuals and the macro economy differently. Generic advice to control inflation with higher taxes is vacuous until MMTers provide far more detail.

4. MMT does not acknowledge that even well-intentioned policy makers face incentives to use inflation to achieve employment or fiscal financing goals. Because those incentives to inflate are especially powerful for elected officials, many countries, including the United States, have adopted the norms of (i) independent central banks tasked with inflation control and macroeconomic stabilization and (ii) fiscal policies that largely pay for government spending with current and future taxes. Those policy norms have improved inflation performance and social welfare. MMT overthrows those norms to move inflation control and countercyclical policies from the Federal Reserve to Congress, to finance federal spending by creating new currency, and to subjugate monetary policy to fiscal needs.

5. It does not appreciate the central role that safe and liquid U.S. Treasurys perform in the global financial system. Neither does it apprehend the extent to which its policy proposals may destabilize financial markets and undermine the special status of Treasurys and the dollar in the world economy, a status that strengthens the U.S. economy.

The problems begin with the basic assumptions that underpin MMT. Its advocates attribute all unemployment to insufficient demand for workers and believe unemployment should be alleviated through a federal guaranteed jobs program. Weak demand frequently underlies unemployment, particularly during economic downturns. But workers themselves have a say in their employment status. During the COVID-19 pandemic, a broad cross section of workers left the labor market and voluntarily have not re-entered. From March 2020 to October 2021, labor force participation rates were depressed relative to the previous year: 2.5% for men, 2.6% for women, and 3.8% for workers 55 and older. Employers across the country have positions that remain unfilled. COVID is surely an unusual situation, but it serves to illustrate that employment outcomes are not always driven by insufficient demand.

MMT is at its weakest when addressing inflation, how it gets determined and how policies can control it. Its most common argument reduces to: inflation control is not a problem until it is. Problems arise when resource utilization reaches some limit, at which point higher taxes can keep inflation in check. But resource utilization is not the only factor that affects inflation. In late 2021, consumer price inflation hit a 40-year high of over 6%, yet compared to their pre-COVID levels, employment, capacity utilization, and industrial production are lower, while the unemployment rate is higher. Inflation is not rising because the overall economy has hit its resource limit. To be sure, supply-chain issues have driven up some prices relative to others, but these issues are not what anyone means by economy-wide resource limits. MMT’s weak theory of inflation is stunning because the potential of the MMT agenda to trigger inflation is the most frequently voiced criticism of the theory [Summers (2019), Cochrane (2020), Hartley (2020), Mankiw (2020)].

The guaranteed jobs program points to a more general theme of MMT: the federal government can solve big problems once policy makers grasp the key tenets of MMT. Kelton (2021) identifies seven “deficits,” defined in terms of both quantity and quality, that MMT can help to close: good jobs, saving, health care, education, infrastructure, climate, and democracy. MMT promises to address each of these deficiencies by first altering policy makers’ understandings of fiscal financing matters.

MMT abandons two long-standing policy norms. The first came from Alexander Hamilton in 1790 and can be summarized as “federal budget deficits beget budget surpluses,” meaning that debt-financed spending is backed by future taxes. This norm has contributed to less costly financing and bestowed on U.S. treasurys status as the world’s go-to safe and liquid assets, enabling their critical role in global financial markets. The second norm evolved from the 1951 Treasury-Fed Accord to make monetary policy operationally independent. Legislation houses countercyclical policy primarily in the Federal Reserve with the mandate that the Fed achieve price stability, maximum sustainable employment, and low long-term interest rates, and facilitate financial stability.

MMT instead posits that a dollar of new government debt need not carry any assurance of tax backing. It regards treasury securities solely as a means for the central bank to achieve its interest rate target. MMT shifts responsibility for achieving full employment and controlling inflation from monetary policy to fiscal policy. The central bank’s primary tasks are to serve as the Treasury’s bank and to maintain zero interest rates. Despite MMT claims to the contrary, monetary policy is completely subservient to fiscal policy, tossing aside Federal Reserve independence and the social benefits that accrue from it.

Full embrace of MMT’s policy proposals and new norms—whatever they may be—carries significant risks. Those risks include higher and more volatile inflation and interest rates and financial market instability, which would disrupt and depress real economic activity and harm most the people MMT aims to benefit.

Eric Leeper is a contributing scholar for the Progressive Policy Institute. He is also the Paul Goodloe McIntire Professor in Economics at the University of Virginia, a research associate at the National Bureau of Economic Research, director of the Virginia Center for Economic Policy at the University of Virginia, and a visiting scholar and member of the Advisory Council of the Center for Quantitative Economic Research at the Federal Reserve Bank of Atlanta.*

* The author thanks Joe Anderson for many helpful discussions and insights and Campbell Leith, Jim Nason, and PPI staff for detailed comments.

Today, the House of Representatives passed the America COMPETES Act, which will help ease supply chain tension, invest in American innovation, and strengthen our standing in the race to technological leadership.

Aaron White, Director of Communications for the Progressive Policy Institute (PPI) released the following statement:

“The Progressive Policy Institute is encouraged to see the House passage of the America COMPETES Act, a companion bill to the Senate’s bipartisan United States Innovation and Competition Act, which will invest in American innovation, ease the tensions on U.S. and global supply chains, and strengthen America’s standing in our race with China for technological leadership.

“This bill has the potential to spur long-term growth through significant investment in scientific innovation and new-age manufacturing and logistics advancements. The American technology sector has long been a leading global innovator; by investing in emerging technologies, research and development, the future workforce and the U.S. high-tech productive base, America can once again lead the world with a robust 21st century economy and expand opportunity for generations to come.

“Notably, it is unfortunate that House Republicans refused to vote for legislation that mirrored bipartisan bills and committee provisions, particularly given the Senate was willing to compromise and pass their companion bill on a bipartisan vote months ago. Important issues like supporting American innovation, technological leadership, and strengthening our economy should transcend partisanship, especially as we recover from the pandemic.

“We must acknowledge that there is still room for improvement. As the Senate and House begin the conference process for the United States Innovation and Competition Act and the America COMPETES Act, PPI encourages conference committee members to more closely examine the trade provisions within the final bill, and take the time needed — through hearings, public comments or other means — to consider the wide ranging implications for U.S. exporters and importers of several of the bill’s trade provisions.

“We also encourage the conference committee to consider reverse the Trump and GOP-era tax increase on scientific research that took effect this year. If left in place, this tax change threatens to undo much of the good that this legislation would do for American innovation. Finally, we hope lawmakers will wait for an official score from the Congressional Budget Office before voting on passage of the bill in its final form. Even if some public investments generate high enough returns to justify borrowing to pay for them, as PPI believes may be the case for some provisions in this bill, it is essential that our leaders have the necessary information to consider all the costs and tradeoffs.

“We thank Speaker Pelosi and Majority Leader Schumer for their continued work in advancing this legislative package, and congratulate President Biden for spearheading this historic advancement in American economic leadership. The finished product will be a major win for American workers, consumers, and manufacturers alike.”

U.S. Technological Innovation Needs Government Procurement to Succeed

Ongoing geopolitical pressures, primarily the modern rise of China, have brought American technological superiority back to the fore as a central political objective. By revitalizing corporate science and economic innovation through government procurement, policymakers can promote U.S. scientific leadership while protecting our national security, argues a new report from the Progressive Policy Institute (PPI)’s Innovation Frontier Project.

The report, authored by Sharon Belenzon and Larisa C. Cioaca of Duke University’s Fuqua School of Business, is titled “Government Procurement: A Policy Lever to Revitalize Corporate Scientific Research.”It details the history of government procurement from the 1957 Sputnik shock to the rise of China, along with evidence that an increase in procurement contracts leads firms to invest more in upstream R&D, especially when private market incentives are weaker.

“There’s no reason that America can’t lead the world again in science and technology. And as the authors of this report argue, the rise of China represents not only a threat, but an opportunity,” said Jack Karsten, Managing Director of the Innovation Frontier Project at PPI. “By bolstering corporate scientific research with the right targeted reforms to the procurement process, the U.S. government can constructively address the national security challenges it faces while reinvigorating domestic innovation.”

Belenzon and Cioaca call for the government to incentivize the participation of the private sector in procurement, while still responsibly and efficiently managing taxpayer dollars. They recommend that policymakers consider returning to the practice of rewarding firms that demonstrate technological superiority, encouraging domestic innovation while keeping us competitive abroad.

PPI releases this report as the U.S. House of Representatives considers the America COMPETES Act, a package meant to address supply chain issues, increase domestic production, and invest in American scientific and technological leadership. The legislation would appropriate $45 billion to prevent supply chain shortages and disruptions and $52 billion for semiconductor production in America, along with a collection of bipartisan science, research and technology bills.

Based in Washington, D.C., and housed in the Progressive Policy Institute, the Innovation Frontier Project explores the role of public policy in science, technology and innovation. The project is managed by Jack Karsten. Learn more by visiting innovationfrontier.org.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Jasmine Stoughton, Program Lead for the Mosaic Economic Project at the Progressive Policy Institute (PPI), released the following response in reaction to Biden’s Federal Reserve Nominations:

“President Biden’s nomination of the Hon. Sarah Bloom Raskin, Dr. Lisa Cook, and Dr. Philip Jefferson to the Board of Governors of the Federal Reserve System is a key step toward ensuring stable economic growth that will be felt by every American, and it is a demonstration of Biden’s commitment to uplift leaders that reflect the diversity of our country.

“Raskin, Cook, and Jefferson are well-respected and highly qualified to serve on the Board. Combined, they have decades of experience in academia and government and have each shown extraordinary judgement and skill throughout their careers.

“Diversity in leadership is among the most important elements of successful governance. If the Senate confirms Biden’s nominations, the complete Board will be majority women for the first time in its 108-year history. Incredibly, Cook will be the first Black woman to serve on the Board, and Jefferson will be the fifth Black governor — representation that is long overdue.”

TheMosaic Economic Projectis a network of diverse women with expertise in the fields of economics and technology. Mosaic programming aims to bring new voices to the policy arena by connecting cohort members with opportunities to engage with top industry leaders, lawmakers, and the media.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

The Progressive Policy Institute (PPI) released the following statements ahead of the Senate Banking Committee’s hearing on the nominations of the Hon. Sarah Bloom Raskin, Dr. Lisa Cook, and Dr. Philip Jefferson for the Board of Governors of the Federal Reserve System:

“President Biden has overseen a year of remarkable achievement in restoring economic growth, with steady job creation and strong evidence of wage increases. With the economy stabilized after the COVID-19 pandemic experience but concerns about inflation rising, the country needs both professional management and imaginative policy in the coming years,” said Ed Gresser, Vice President and Director of Trade and Global Markets for PPI.

“President Biden’s excellent nominations for the Federal Reserve Board of Governors demonstrate his awareness of this challenge. The current chair and nominee for vice chair, Jerome Powell and Lael Brainard, are exceptional public servants who have helped to steer the Fed through the turbulence of the Trump years and the COVID crisis, and fully merit confirmation. New nominees Lisa Cook, Sarah Bloom Raskin, and Phillip Jefferson are outstanding economists who will bring a diversity of strengths and experience to the Fed, with its dual mandate of price stability and full employment, and will help ensure that the Board of Governors takes its next steps with consideration for both macroeconomic consequences and impacts on Americans at all income levels and in all walks of life. This is a very strong group of nominees which will serve the country well during a very complex time, and deserves support,” concluded Gresser.

“The Progressive Policy Institute applauds President Biden and the Biden-Harris administration for this historic, diverse, and highly qualified slate of nominees to the Board of Governors of the Federal Reserve. At a time when our nation faces several economic challenges — caused primarily by the COVID-19 pandemic and evolving variants — this group will bring steady, competent leadership. America is getting back on track after an unimaginable health and economic crisis, and President Biden is proving his commitment to Build Back Better by prioritizing strong leadership in every facet of the federal government,” said Sarah Paden, Vice President and National Political Director.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

While the system of credit scoring used by Fannie Mae and Freddie Mac (the Enterprises) has been in effect for some time, Congress recently asked them — along with the Federal Housing Finance Agency (FHFA) — to review their credit scoring model to determine if additional models could be used to increase competition. But as Fontenot explains, the incorporation of a flawed new model could have unforeseen impacts and potentially drive up borrower costs.

The report concludes that the Enterprises have used a current credit scoring model that has produced necessary liquidity in the market in both good and difficult times — and that as the FHFA oversees the next phase of testing alternative credit score models, it should ensure that the models are subjected to scrutiny concerning the cost and market affects any change would have.

Read the full paper, expanded conclusion, and questions for consideration here.

Brodi Fontenot is President of Fontenot Strategic Consulting LLC. Mr. Fontenot was previously appointed by President Obama to be the Department of the Treasury’s Assistant Secretary for Management and was nominated to serve as Treasury’s Chief Financial Officer. Fontenot also served in a variety of senior roles at the Department of Transportation, including Assistant Secretary for Administration, Chief Human Capital Officer (CHCO), and Senior Sustainability Officer (SSO).

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

The Federal Reserve made clear in its December 2021 meeting that it intends to raise interest rates in 2022. Interest rate changes flow through the economy and affect the rates borrowers pay on all types of loans. In particular, the increases in interest rates may place greater pressure on home mortgage rates and the credit scores that are used by financial institutions to determine who qualifies for loans.

In the area of housing finance, how credit scores are used by key market players has received attention for some time. The better the credit score, the more likely a borrower will qualify for a mortgage at the best possible rate, saving the borrower money over the life of the loan. There has been debate, however, over the models used to create those scores — should there be more competition and, more important, can new models lower costs for home buyers and ensure equity of access to loans.

Two of the most important entities in housing finance are the nation’s housing government sponsored enterprises — Fannie Mae and Freddie Mac (Enterprises) — which are now under government conservatorship overseen by Federal Housing Finance Agency (FHFA). As a result, many policymakers and elected officials have encouraged the FHFA to take steps to promote more competition in the credit scoring models used by the Enterprises to help lower costs to consumers and give greater access to credit for previously underserved individuals.

These are important goals and should be pursued. However, some reforms presented would have had a less than optimal effect — decreasing competition and potentially driving up mortgage costs rather than lowering them. The Enterprises have used a valid credit score model for over 20 years. Introducing competitive reforms has merit, but it must be done in a way that does not create unfair advantages. FHFA has a clear mandate to keep the Enterprises solvent and help homeowners, as witnessed by their recent COVID assistance. But FHFA must ensure that any reforms maintain competition and keep prices low for consumers.

This paper reviews how credit scores are presently used by the Enterprises and discusses some of the issues that can be addressed to keep competition in the credit score market. This paper also discusses some of the pitfalls associated with some proposed reforms to credit score markets.

ENTERPRISES HAVE USED PROVEN CREDIT SCORE MODELS FOR OVER TWO DECADES

Fannie Mae and Freddie Mac (Enterprises) are commonly known as housing government sponsored enterprises. Somewhat unique in their structure, they were originally chartered by Congress, but owned by shareholders, to provide liquidity in the mortgage market and promote homeownership.[1] The Enterprises maintained this unique ownership structure until their financial condition worsened during the financial crisis of 2008, when they were placed in government conservatorship under the leadership of the Federal Housing Finance Agency (FHFA).

The Enterprises do not create loans. They purchase loans made by others (such as banks), and then package those loans into securities which are then sold on the secondary market to investors. The loans purchased by the Enterprises can only be of a certain size and home borrowers must have a minimum credit score to qualify. The Enterprises use these and other criteria to minimize the risk that the loans they purchase will not be paid back (default) — an important step because it is this step of buying loans from banks and other lenders, thereby providing them with replenished funding that allows further home lending.

The loans purchased by the Enterprises then are packaged into securities that have specific characteristics which are told to investors — including the credit scores on the loans in the security. According to FHFA, the Enterprises use credit scores to help predict a potential borrowers likeliness to repay and has been using a score developed from a model, FICO Classic,[2] for over 20 years.[3] In discussing FICO Classic, FHFA points out that it “and the Enterprises believe that this score remains a reasonable predictor of default risk.”[4]

While the current system has been in effect for some time, Congress recently asked FHFA and the Enterprises to review their credit scoring model to determine if additional credit scoring models could be used by the Enterprises to increase competition. Specifically, FHFA was to “establish standards and criteria for the validation and approval of third-party credit score models used by Fannie Mae and Freddie Mac.”[5] Advocates of using alternatives to FICO Classic said, at the time, that using other validated credit scoring models would lead to more access.[6] While a worthy goal, incorporating a flawed new model, could have impacts and potentially drive-up costs.

CONFLICT OF INTEREST COULD LEAD TO DECREASED COMPETITION

Beginning in 2017, FHFA proposed a rule which would set the stage for reviewing the Enterprises’ credit score models. The rule FHFA finalized in 2019 directed the Enterprises to review and validate alternative credit models in the coming years.

Section 310 of the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 (Pub. L. 115–174, section 310) amended the Fannie Mae and Freddie Mac charter acts and the Federal Housing Enterprises Financial Safety and Soundness Act of 1992 (Safety and Soundness Act) to establish requirements for the validation and approval of third-party credit score models by Fannie Mae and Freddie Mac.[7]

At the time of the proposed rule, some thought that alternative credit scores could open access to a larger group of homeowners.[8][9] While an admirable goal, and in keeping with FHFA’s mission for the Enterprises even now, a major issue was left unresolved. The proposed rule “would have required credit score model developers to demonstrate, upon applying for consideration, that there was no common ownership with a consumer data provider that has control over the data used to construct and test the credit score model.”[10]

The proposed rule would have created a separation between those who create and control the data, from those in charge of the model creating the scores — an important goal. Not surprisingly, the proposed rule received significant comments. Sadly, the final rule did not adopt this important provision which required those submitting models to not have a conflict of interest or “common ownership with a consumer data provider that has control over the data used to construct and test the credit score model.”[11] This lack of clear independence could set the stage for a lack of competition in the future.

While the rule was being proposed, former FHFA director Mel Watt in 2017 said, “how would we ensure that competing credit scores lead to improvements in accuracy and not to a race to the bottom with competitors competing for more and more customers? Also, could the organizational and ownership structure of companies in the credit score market impact competition? We also realized that much more work needed to be done on the cost and operational impacts to the industry. Given the multiple issues we have had to consider, this has certainly been among the most difficult evaluations undertaken during my tenure as Director of FHFA.”[12]

Several at the time of the proposed rule pointed out that having one dominant player possibly replaced by another, would not further competition but could further consolidate it. One commentator stated, “to push for alternative scoring models may simply trade one dominant player (FICO) for another (Vantage),”[13] in referring to legislation which would ultimately be incorporated into the bill where the proposed rule was developed. The Progressive Policy Institute (PPI) held an expert panel discussion at the time which also discussed the problems with adopting VantageScore due to conflict of interest.[14] “The reason? Because the owners of Vantage control the supply of information currently used by FICO to make its determination. And given the history of monopolies, it would not be surprising to see Equifax, Experian, and TransUnion use that leverage to the advantage of Vantage, and eventually force FICO out of business.”[15]

The proposed rule points out that “VantageScore Solutions, LLC is jointly owned by the three nationwide CRAs. The CRAs also own, price, and distribute consumer credit data and credit score. This type of common ownership could in theory negatively impact competition in the marketplace.”[16] Another writer at the time, also acknowledged the potential conflict of interest provision of the proposed rule.[17] While these issues were not resolved in the final rule, they still matter and can affect not only competition but also costs in the residential mortgage marketplace.

Competition is key to innovation and inclusiveness is important to further homeownership. Using alterative data, rent payments, utility payments, bank balances, all could potentially be used help complete the credit picture and increase access to credit.[18] Other research organizations have acknowledged that FICO has improved models and incorporated alternative sources of data that are available,[19] which would not have the conflict of interest that VantageScore would have. FHFA must ensure that competition is maintained, without creating unfair advantages.

LACK OF REAL COMPETITION COULD INCREASE COSTS

Before any changes can happen, however, FHFA must articulate all costs to consumers, lenders, the Enterprises, and investors of any change. COVID-19 proved a real-world laboratory for the Enterprises under stress. FHFA’s recent Performance Report lays out the series of actions the Enterprises took to help borrowers affected by COVID-19, including payment deferrals, forbearance, and evictions suspensions.[20] These actions likely kept many homeowners in their homes during a difficult period, and kept the Enterprises functioning. The relief provided was important and was balanced against the risk to the Enterprises — but it did come at a cost.

FHFA made their first announcement on COVID assistance to homeowners in March 2020.[21] A few months later in August 2020, FHFA announced that the Enterprises would charge a fee of 50-baisis points per refinancing to help make up for any potential losses the Enterprises might experience.[22] An initial estimate put the projected losses at $6 billion. Thankfully the Enterprises saw declining rates of loans in forbearance and the fee was ultimately ended in July 2021.[23]

Changes at the Enterprises have affects across the industry. Just as the potential increases in interest rates by the Federal Reserve this year could raise interest costs to home buyers, at time of the proposed rule, former FHFA Director Watt knew that changes to the credit scoring model could raise costs and even stated “much more work needed to be done on the cost and operational impacts to the industry,”[24] before changes were made. Clearly, the FHFA realizes that any changes to its credit scoring models will also likely have increased costs to the housing finance sector. As an aside, the related issue of changes to issues such as mortgage servicing have led to increased costs in the home purchase ecosystem.[25]

Changes to the credit scoring models could also affect prices in the secondary market for mortgage-backed securities (MBS) and credit risk transfers (CRT). As the FHFA pointed out, investors “in Enterprise MBS and participants in Enterprise CRT transactions would need to evaluate the default and prepayment risks of each of the multiple credit score options.”[26] While the FHFA in the final rule did not address the costs of these evaluations, incorporating multiple credit score options could raise the cost investors demand and ultimately increase the costs to home buyers via the fees the Enterprises would need to pass on.

Others have pointed out that changes to credit scoring models could have cost impacts for banks, investors, pension funds, and others.[27] These issues of cost and operational impacts need to be given serious consideration, because as the recent Enterprise actions related to COVID-19 made clear — they matter. The lending industry was upset when the Enterprises raised a temporary fee to help ensure Enterprises’ soundness through the difficult period.[28] What would the costs be with a wholesale change to the credit score model system? And who would ultimately pay those costs? These are questions the FHFA must address as they review any changes to the credit scoring model.

One of the FHFA’s current core goals is to “Promote Equitable Access to Housing.”[29] To ensure that the Enterprises can undertake their important role in addressing long standing issues of equity, they need to be in the best place possible financially to do that. A question that FHFA needs to address as they review credit scoring models is, would using a model with a conflict of interest hurt their goal of equity? Would changes raise prices or worse, limit access for those FHFA is looking to provide access into the market?

CONCLUSION AND QUESTIONS FOR CONSIDERATION

The crisis of COVID-19 and its effects on the housing market were serious, but thankfully not detrimental due to prudent planning and oversight of the Enterprises and FHFA. The Enterprises have used a current credit scoring model that has produced necessary liquidity in the market in both good and difficult times. As FHFA oversees the next phase of testing alternative credit score models, it should ensure that the models are subjected to the criteria laid out in their final rule — with emphasis placed on the cost and market affects any change would have. The Enterprises were called upon to help homeowners during the recent crisis and could do so with minimal disruption to the consumers and housing finance stakeholders. The Enterprises and FHFA should take seriously how any further changes would impact competition, soundness of the Enterprises, and how those changes could increase the costs for everyone in housing finance.

REFERENCES

[1]“Fannie Mae and Freddie Mac in Conservatorship: Frequently Asked Questions,” Congressional Research Service, July 22, 2020, https://crsreports.congress.gov/product/pdf/R/R44525.

[2] “Selling Guide: B3-5.1-01, General Requirements for Credit Scores,” Fannie Mae, September 2021, https://selling-guide.fanniemae.com/Selling-Guide/Origination-thru-Closing/Subpart-B3-Underwriting-Borrowers/Chapter-B3-5-Credit-Assessment/Section-B3-5-1-Credit-Scores/1032996841/B3-5-1-01-General-Requirements-for-Credit-Scores-08-05-2020.htm.

[3] “There’s More to Mortgages than Credit Scores,” Fannie Mae, February 2020, https://singlefamily.fanniemae.com/media/8511/display.

[4] “Credit Score Request for Input,” FHFA Division of Housing Mission and Goals, December 20, 2017, https://www.fhfa.gov/Media/PublicAffairs/PublicAffairsDocuments/CreditScore_RFI-2017.pdf.

[5] “FHFA Issues Proposed Rule on Validation and Approval of Credit Score Models,” Federal Housing Finance Agency, December 13, 2018, https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Issues-Proposed-Rule-on-Validation-and-Approval-of-Credit-Score-Models.aspx.

[6] “Validation and Approval of Credit Score Models,” Federal Housing Finance Agency, August 13, 2019, https://www.fhfa.gov/SupervisionRegulation/Rules/RuleDocuments/8-7-19%20Validation%20Approval%20Credit%20Score%20Models%20Final%20Rule_to%20Fed%20Reg%20for%20Web.pdf.

[8] Karan Kaul, “Six Things That Might Surprise You About Alternative Credit Scores,” Urban Institute, April 13, 2015, https://www.urban.org/.

[9] Michael A. Turner et al., “Give Credit Where Credit Is Due,” Brookings Institution, June 2016, https://www.brookings.edu/wp-content/uploads/2016/06/20061218_givecredit.pdf.

[12] Melvin L. Watt, “Prepared Remarks of Melvin L. Watt, Director of FHFA at the National Association of Real Estate Brokers’ 70th Annual Convention,” Federal Housing Finance Agency, August 1, 2017, https://www.fhfa.gov/Media/PublicAffairs/Pages/Prepared-Remarks-of-Melvin-L-Watt-Director-of-FHFA-at-the-NAREB-70th-Annual-Convention.aspx.

[13] Paul Weinstein Jr., “No Company Should Have a Monopoly on Credit Scoring,” The Hill, December 7, 2017, https://thehill.com/opinion/finance/363755-no-company-should-have-a-monopoly-on-credit-scoring.

[14] “Updated Credit Scoring and the Mortgage Market,” Progressive Policy Institute, December 4, 2017, https://www.progressivepolicy.org/event/updated-credit-scoring-mortgage-market/.

[16] “Validation and Approval of Credit Score Models: Final Rule,” Federal Register, August 16, 2019, https://www.federalregister.gov/documents/2019/08/16/2019-17633/validation-and-approval-of-credit-score-models.

[17] Karan Kaul and Laurie Goodman, “The FHFA’s Evaluation of Credit Scores Misses the Mark,” Urban Institute, March 2018, https://www.urban.org/sites/default/files/publication/97086/the_fhfas_evaluation_of_credit_scores_misses_the_mark.pdf.

[18] Kelly Thompson Cochran, Michael Stegman, and Colin Foos, “Utility, Telecommunications, and Rental Data in Underwriting Credit,” Urban Institute, December 2021, https://www.urban.org/research/publication/utility-telecommunications-and-rental-data-underwriting-credit/view/full_report.

[19] Laurie Goodman, “In Need of an Update: Credit Scoring in the Mortgage Market,” Urban Institute, July 2017, https://www.urban.org/sites/default/files/publication/92301/in-need-of-an-update-credit-scoring-in-the-mortgage-market_2.pdf.

[21] “Statement from FHFA Director Mark Calabria on Coronavirus,” Federal Housing Finance Agency, March 10, 2020, https://www.fhfa.gov/Media/PublicAffairs/Pages/Statement-from-FHFA-Director-Mark-Calabria-on-Coronavirus.aspx.

[22] “Adverse Market Refinance Fee Implementation Now December 1,” Federal Housing Finance Agency, August 25, 2020, https://www.fhfa.gov/Media/PublicAffairs/Pages/Adverse-Market-Refinance-Fee-Implementation-Now-December-1.aspx.

[23] “FHFA Eliminates Adverse Market Refinance Fee,” Federal Housing Finance Agency, July 16, 2021, https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Eliminates-Adverse-Market-Refinance-Fee.aspx.

[25] Laurie Goodman et al., “The Mortgage Servicing Collaborative,” Urban Institute, January 2018, https://www.urban.org/sites/default/files/publication/95666/the-mortgage-servicing-collaborative_1.pdf.

[27] Pete Sepp and Thomas Aiello, “Risky Road: Assessing the Costs of Alternative Credit Scoring,” National Taxpayers Union, March 22, 2019, https://www.ntu.org/publications/detail/risky-road-assessing-the-costs-of-alternative-credit-scoring.

Aaron White, Director of Communication for the Progressive Policy Institute (PPI), released the following response in reaction to the Senate Judiciary Committee’s advancement of the American Innovation and Choice Online Act:

“For those of us that believe in good governance and the importance of legislative deliberation and debate, today’s markup of the American Innovation and Choice Online Act was embarrassing for the Senate.

“The Judiciary Committee’s markup made it crystal clear that there are still significant, unresolved concerns on both sides of the aisle. As written, the bill sparks major national security and privacy risks, includes overly broad and burdensome language, and will harm American consumers, workers, and the digital economy.

“Senator after Senator raised concerns that this was a rushed legislative process, and this bill is not ready for primetime, yet Senator Klobuchar chose to force this vote. The Senate should do its job and return to the legislative process that all Senators can be proud of. This bill should not see the Senate floor until the legitimate concerns of Senators are addressed.

“The digital economy is a hallmark American achievement that has created millions of middle-class jobs. Scrutiny is important and healthy; but the Senate must address their concerns in a deliberative fashion — not in a haphazard, potentially reckless manner.”