Today, the Progressive Policy Institute (PPI) released a new research deck on how Senators Amy Klobuchar and Chuck Grassley’s anti-tech antitrust bill, the American Innovation and Choice Online Act, could do irreparable harm to the services and products millions of Americans rely on every day.

“The bill is notable for combining very broad language, very heavy penalties, and very narrow grounds for affirmative defense,” said Dr. Michael Mandel, Vice President and Chief Economist for the Progressive Policy Institute. “The problem is that this three-way combination goes far beyond imposing normal compliance costs and regulatory burdens, creating huge financial and business risks for even ordinary business decisions.”

Well-liked services such as Google Search, Fulfillment by Amazon, and the Apple App Store, could have to be substantially reconfigured and/or limited, according to the deck’s authors, Mandel, John Scalf of NERA Economic Consulting and D. Daniel Sokol of University of Southern California Gould School of Law. Popular smartphone features and user reviews on online marketplaces could be affected as well. These proposed standards would not only undermine the tech companies that would be subjected to the legislation, but inevitably harm its users.

Consumers could also suffer from reduced innovation, as the targeted companies would have to obtain regulatory pre-approval with every new product or meet the unspecified criteria in the bill.

A mark-up of the bill is scheduled for Thursday of this week in the Judiciary Committee. Read PPI’s statement on the markup and the bill here.

This deck was authored by Michael Mandel of the Progressive Policy Institute, John Scalf of NERA Economic Consulting, and D. Daniel Sokol of the University of Southern California Gould School of Law.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

The American Innovation and Choice Online Act Would Likely Harm Consumers

SUMMARY:

Recently, Senator Klobuchar introduced the American Innovation and Choice Online Act (“AICOA”) proposing sweeping regulations for a handful of tech companies that operate digital services used by both businesses and consumers.

While the Bill is ostensibly intended to prevent self-promotion and discriminating against competitors, it would end up sweeping up a broad range of ordinary business operations that provide huge benefits to consumers.

The Bill is notable for its combination of very broad and vague language for defining illegal activity; very heavy penalties for companies and corporate officers; and very narrow language for affirmative defense.

Moreover, the Bill makes no mention of consumer benefits as an affirmative defense and hence advances the interests of certain businesses over the interests of consumers and small businesses that use such services.

The problem is that this three-way combination goes far beyond imposing normal compliance costs or regulatory burdens, by creating huge financial and business risks for even ordinary business decisions.

In response, well-liked services such as Google Search, Fulfillment by Amazon, and the Apple App Store, will have to be substantially reconfigured and/or limited. These proposed standards would not only undermine the tech companies that would be subjected to the legislation, but inevitably harm its users as well.

In fact, because the Bill fails to distinguish between markets that are competitive and markets that suffer from market power, it would inevitably harm competition in digital markets as well. The Bill would essentially make it less likely that either firms subjected to the regulations or ones arbitrarily protected from them would invest in new, innovative consumer products.

Consumers could lose out on a range of products and services offered by the targeted companies that would be swept up by the Bill. Just a few of the products and services that could hampered by the Bill include:

Search engines that concentrate on delivering the most relevant results to consumers from Google

Online shopping with massive product catalogs and two-day shipping from Amazon

Smartphones and a vast library of third-party apps that have revolutionized everyday life from Apple

Consumers would also suffer from reduced innovation, as the targeted companies would have to obtain regulatory pre-approval with every new product to meet the unspecified criteria in §2(a) and (b) of the Bill.

Far beyond its stated goals, the Bill could end up harming consumers by breaking the products and services that they have come to greatly value and depend on.

View the full research deck by Dr. Michael Mandel of the Progressive Policy Institute, Dr. John Scalf of NERA Economic Consulting, and Professor D. Daniel Sokol of the University of Southern California Gould School of Law.

In a statement released after the latest consumer price report, President Biden remarked on the “meaningful reduction in headline inflation” but indicated that there was still “more work to do, with price increases still too high and squeezing family budgets.”

In particular, the Biden Administration wants to protect consumers by identifying markets where sellers are taking advantage of the pandemic and supply chain snarls to raise prices. That’s a great plan.

At the same time, it’s also important to recognize and acknowledge those industries where price increases have been moderate and restrained.

In that spirit, we examine the inflation performance of the digital sector of the economy, encompassing tech, ecommerce, broadband, and related industries. These companies have come under fire for a variety of different reasons, some deserved, some not.

In this blog item we will show, based mainly on government data, that digital companies are helping hold down inflation at a time when prices are soaring in many other parts of the economy. For the Democrats and the Biden Administration, this is a success story they can build on.

The Historical Perspective

We’re used to computers getting cheaper over time, as they become more powerful and versatile. The Internet opened up entirely new dimensions of free websites, with everything from recipes to news to maps and directions. Long distance phone calls have effectively become free. Broadband networks, both wired and wireless, have become faster, connecting almost every part of the country. Content has become more varied and cheaper, at the same time.

There is no doubt that technology has been a profoundly disinflationary force historically. But what about today? The GDP inflation rate was 4.6% in the year ending with the third quarter of 2021. That’s a big jump from the 1.7% GDP inflation rate in the third quarter of 2019, before the inflation. How much of that acceleration is coming from the tech sector?

The answer is, precisely none. As part of its calculation of GDP, the Bureau of Economic Analysis (BEA) calculates price changes by industry. It turns out that inflation rates in four key digital industries are not only negative but falling (Table 1). For example, the inflation rate in the “data processing, internet publishing, and other information services” industry fell from +0.5% in 2019 to -1.1% today.

The same is true for the other three key digital industries. Digital is still following the historical trends of being disinflationary.

Table 1. Digital is Still Disinflationary

(change in value-added prices)

year ending

2019Q3

2021Q3

Computer and electronic product manufacturing

-0.1%

-1.8%

Broadcasting and telecommunications

-0.9%

-2.6%

Data processing, internet publishing, and other information services

0.5%

-1.1%

Computer systems design and related services

-0.2%

-2.8%

Gross domestic product

1.7%

4.6%

Data: BEA, based on Table TVA104-Q

Ecommerce and inflation

Let’s now consider ecommerce prices in particular. As of the third quarter of 2021, ecommerce accounted for 13% of retail sales according to the Census Bureau. That’s back on the long-term trend line after a temporary pandemic-induced jump.

But still, there’s an important question: Why isn’t ecommerce a bigger share of retail sales, given how much we are all shopping online? One reason might be that online prices tend to rise at a slower rate than brick-and-mortar prices, according to the available evidence. Indeed, government data shows that the long-term trend of ecommerce has been and continues to be disinflationary.

Consider this: The BLS measures changes in gross margins in all major retail industries, where the margin is defined as the selling price of a good minus the acquisition price for the retailer. Margins include all costs, such as labor, capital, and energy, plus profits, taking into account gains in productivity. A slower rise in margins translates directly into less inflation for consumers, all other things being equal.

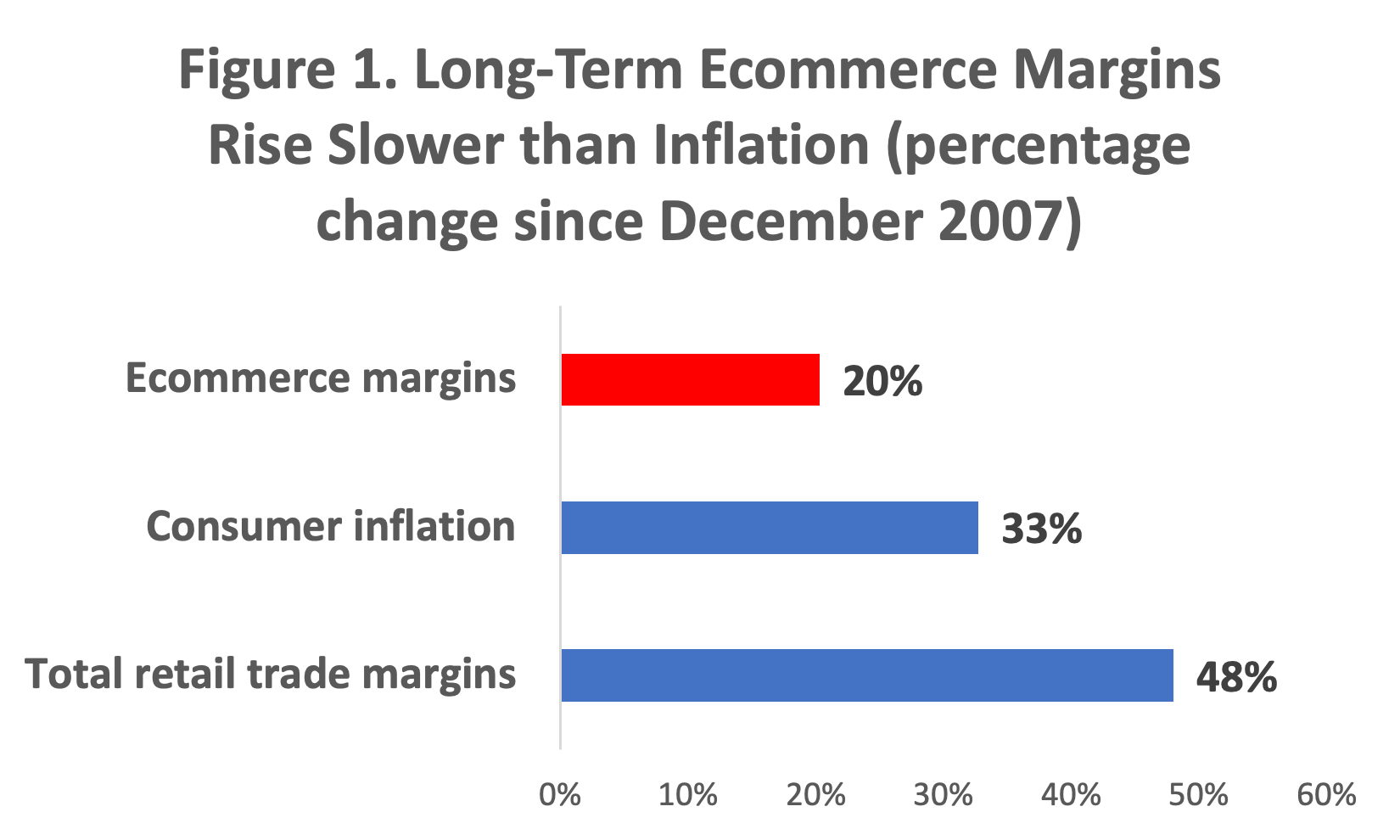

Between December 2007 and December 2021—a 14-year stretch that included the financial crisis, the long boom, and the pandemic—margins in the electronic shopping industry rose by 20%, according to BLS data (Figure 1). Over the same stretch, consumer prices rose by 33%. The implication: Ecommerce companies were accepting thinner margins in real terms, and passing those benefits onto consumers.

By comparison, the data for the overall retail industry has shown a much worse inflation performance, measured by margins. Margins for the total retail industry rose by 48% since December 2007, much faster than consumer inflation. As a result, real margins for the retail industry as a whole have risen, putting upward pressure on consumer prices.

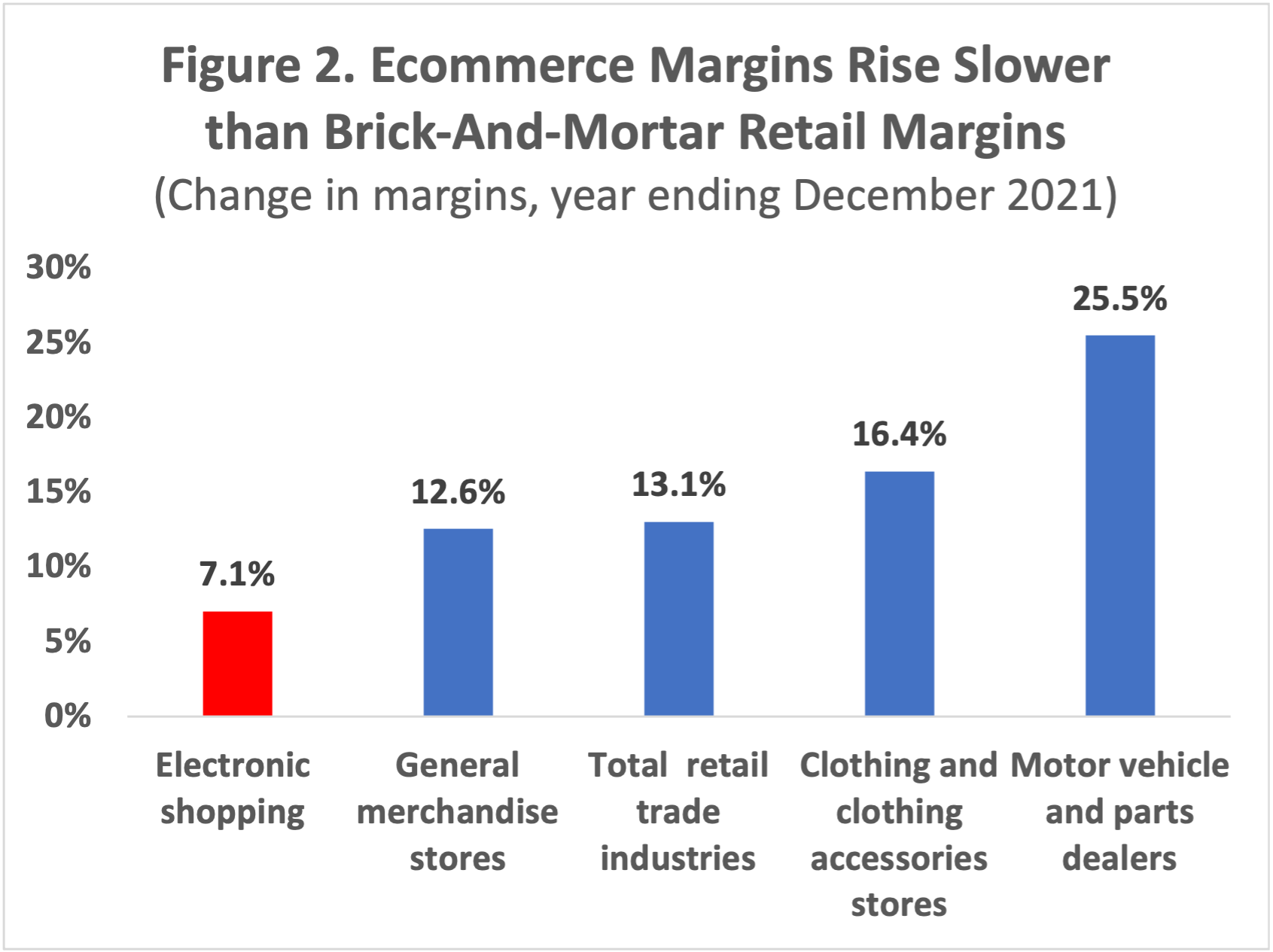

Now let’s look at the current situation. Even in today’s inflationary burst, ecommerce stands out as a force holding down margin increases compared to the rest of retail. In the year ending December 2021, overall retail margins rose by 13.1%. Meanwhile margins at general merchandise stores like warehouse outlets rose by 12.6%. Margins at auto dealers and other auto-related retailers rose by a stunning 26%, far outpacing inflation

By comparison, over the past year, ecommerce margins only rose by 7.1%, about the rate of inflation (Figure 2). These results are completely consistent with the economic literature, which mostly concludes that prices for online goods rise slower than the prices for comparable goods sold offline. A 2018 paper co-authored by Austan Goolsbee (CEA head under President Obama) found that online inflation was more than a full percentage point lower than the corresponding official consumer price index. Sometimes the difference can be much greater. The latest “Digital Price Index” report issued by Adobe shows that the price of furniture and bedding sold online rose by 3% in the year ending November 2021. Meanwhile the official CPI for furniture and bedding, including all brick-and-mortar stores, rose by 12%,

Moreover, the slow growth of ecommerce margins came at the same time that ecommerce fulfillment centers were dramatically boosting employment and pay. Over the last year, the average hourly earnings for production and nonsupervisory workers in the warehousing industry rose by 19.4%. That covers the great majority of ecommerce fulfillment centers.

The ability to simultaneously hold down prices for consumers, reduce shopping time for households, and boost pay for workers, represents a rare win-win proposition. What could be better?

Smartphones, Telecom, and the Digital Economy

During the pandemic, the daily life of Americans has been supported by wired broadband and wireless networks, by content delivered to the home and to wireless devices such as smartphones. This Digital Economy has been essential for work, school, and social contacts in the midst of these bizarre years.

But equally important, the Digital Economy is also a low-inflation economy. While the price of old economy products like cars, clothing, and gasoline has been soaring, the inflation rate of digital goods and services like smartphones, video and audio services, wireless, and internet access has remained low.

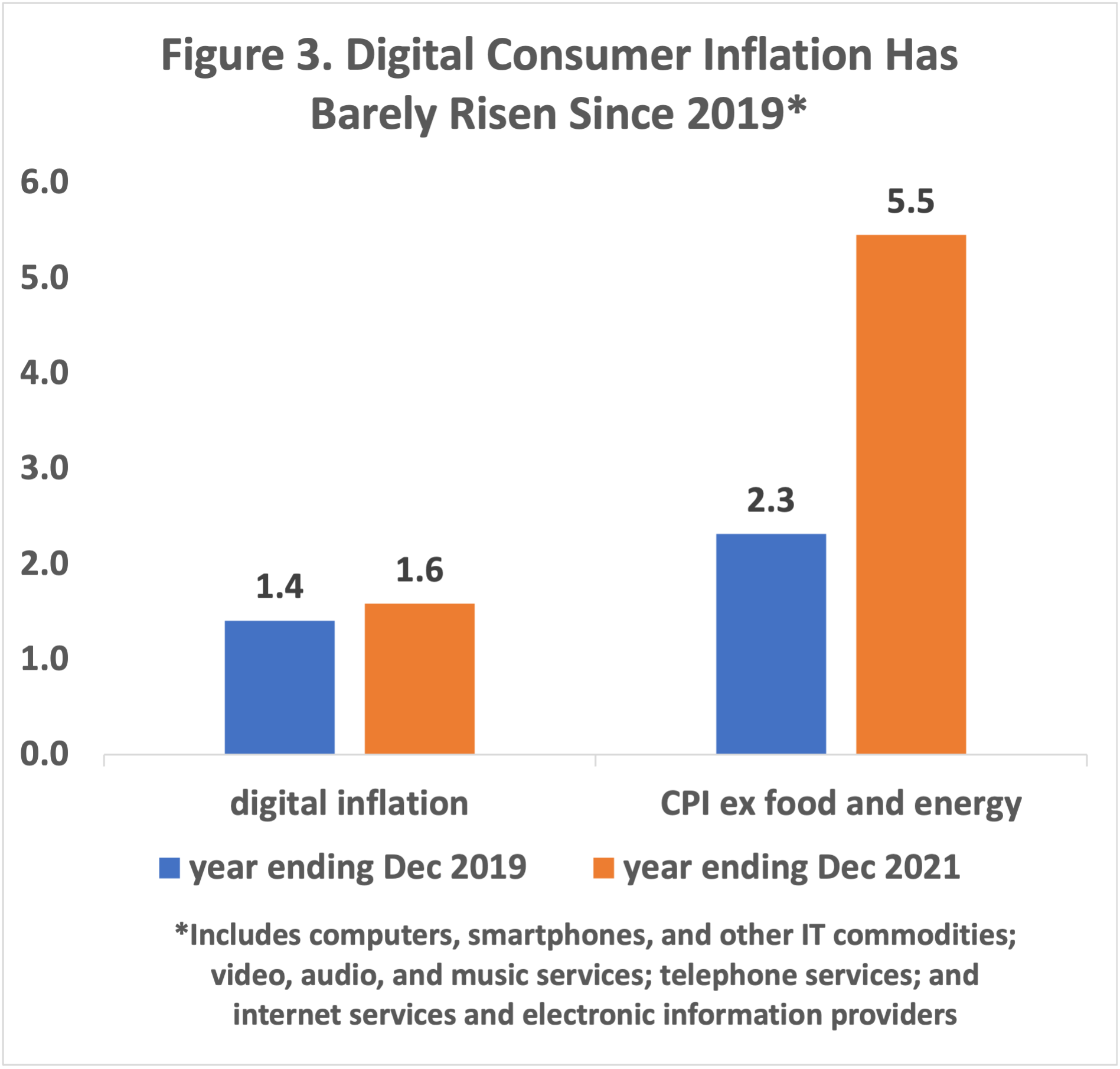

According to our analysis of BLS data, the digital consumer inflation rate was only 1.6% in the year ending December 2021, barely above the 1.4% rate in the year ending December 2019, before the pandemic started (Figure 3). This figure includes computers, smartphones, and other IT commodities; video, audio, and music services; telephone services; and internet services and electronic information providers. We use BLS spending shares to weight the components of the digital inflation rate.

Looking at individual items, the inflation rate for video and audio services, including cable and satellite television service, fell from a 3.1% rate in 2019 to a 2.6% rate in 2021. The inflation rate for telephone services, including wireless, went from 1.6% in 2019 to 0.7% in 2021. Perhaps most striking, the price of smartphones continued their relentless plunge in 2021, dropping in price by 14% after adjusting for quality.

By contrast, there was a huge jump in core consumer inflation, which went from 2.3% in 2019 to 5.5% in 2021. Note that even if some of the components of digital inflation are mismeasured, as some have argued, looking at the change over time should be more accurate if the size of the mismeasurement stays the same.

Tech Inflation

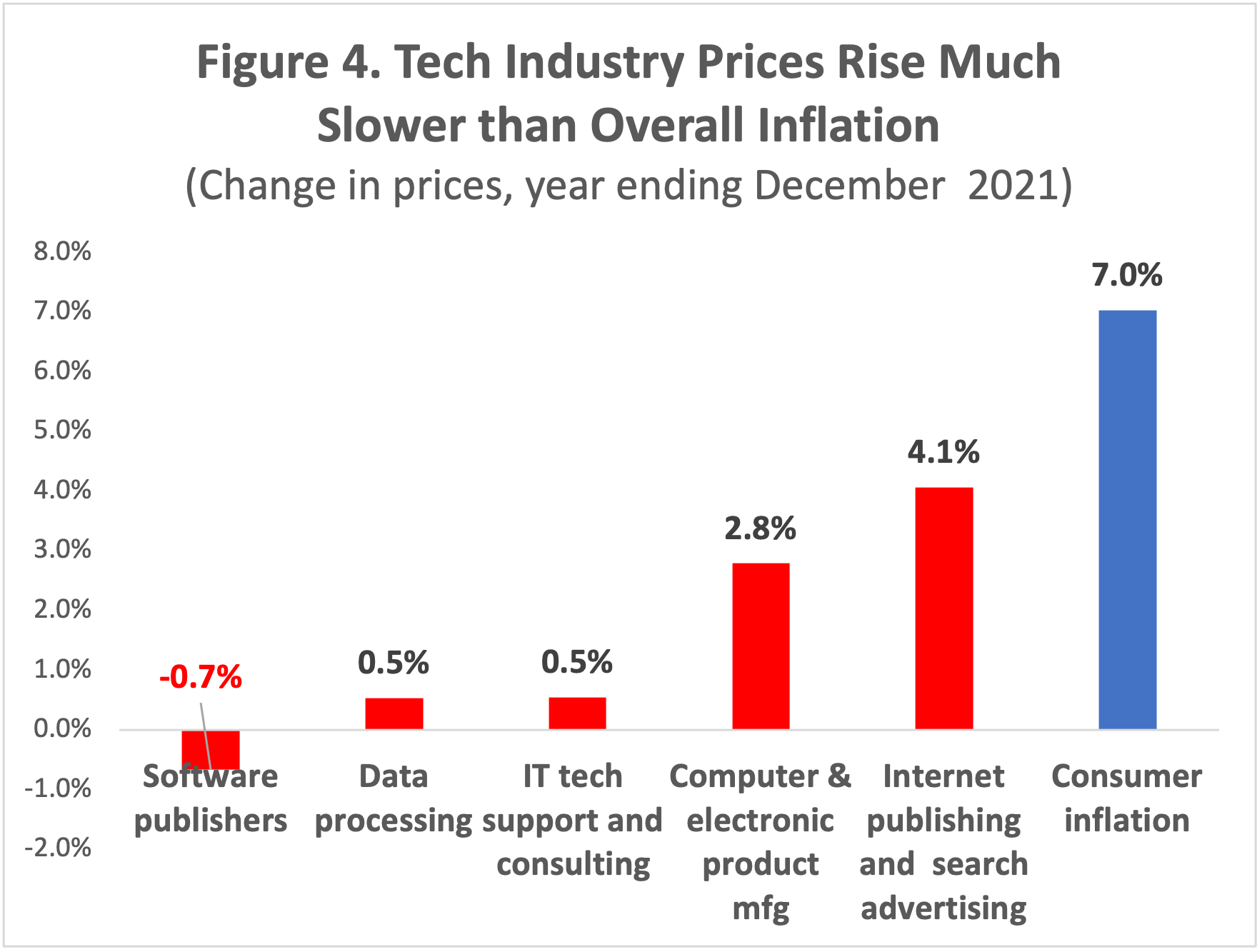

Here we drill down into inflation performance into various components of the tech sector, using data from the BLS Producer Price program. Figure 4 compares inflation in several tech-related industries with consumer inflation.

According to the BLS, prices for the software publishing industry fell by 0.7% in the year ending December 2021. Prices for data processing and IT support and consulting rose by a measly 0.5%. Computer and electronic product manufacturing prices rose by 2.8%. And the price of internet publishing and search advertising rose 4.1%, considerably slower than the overall consumer inflation rate. That means in real terms the price of internet publishing and search advertising has been getting relatively cheaper.

The App Economy

Finally, we come to the App Economy and the app stores. Arguably one of the great technological shifts of all time, the introduction of the Apple iPhone in 2007 and then the Apple App Store in 2008 created an entirely new model for delivering services to consumers conveniently and at a low price. It is clear that the App Economy is a profoundly disinflationary force.

The current price statistics do not break out app-relevant price measures, like the price of app downloads or in-app purchases, either from the consumer or app developer perspective. Nevertheless, a careful look at the structure of the pricing structure of the app stores suggests they are contributing to low inflation today.

App store pricing comes in two parts. First, both the Apple App Store and Google Play charge a nominal fee for registering for a developer account. Google Play charges $25 to register, an amount that hasn’t changed in years. Similarly, the Apple App Store charges an annual fee $99 for a basic developer membership, an amount that also hasn’t changed in the U.S. for years (there are a variety of exemptions). As a result, the inflation-adjusted fee has fallen substantially over time.

Most app developers pay no more than this initial fee, or the somewhat higher fee for enterprise developers. As Judge Yvonne Gonzalez Rogers wrote in her September 2021 decision in the court case involving Apple and game developer Epic: “over 80% of all consumer accounts [in the Apple App store] generate virtually no revenue as 80% of all apps on the App Store are free.” These are apps which are free to download, and have no in-app purchases or subscriptions. Many of them, like banking or airline apps, may be quite frequently downloaded and used. This huge swath of the app stores is disinflationary, with a price that is fixed in dollars over time.

Then there are the small percentage of apps which collect significant consumer revenues on the app stores. Most of these are gaming apps. For the purposes of assessing their impact on inflation, there are two important factors. One factor is whether the price of the subscription or in-app purchase is rising. The other factor is whether the percentage fee charged by Apple and Google for use of their platform is rising or falling.

We have little visibility into the price evolution of subscription costs and IAP prices. One survey from Sensor Tower suggest that the median price of subscriptions for non-game apps did not change from 2017 to 2020, while the median price of in-app purchases for non-game apps rose by 50%. However, even in the latter case, we have no way of knowing whether consumers are buying the same digital goods or shifting to higher value purchases, which matters for inflation.

We have much better information on the effect on inflation of the fees charged by Apple and Google. The statistical literature makes it clear that if the fee percentages stay the same, they has a neutral impact on inflation. If the fee percentages rise, that is inflationary. If fee percentages fall, that is disinflationary.

In the past year or so, both Google and Apple have voluntarily cut fees for a significant portion of their developer base. Apple, for example, cut the App Store fee from 30% to 15% for all developers who earned less than $1,000,000 in 2019. By one estimate, that covered 98% of apps with revenue in 2019. Google reduced its fee on subscriptions to 15% (previously it had charged 30% for the first year). These are substantial changes.

With the app store registration or membership fee being held constant in money terms, and revenue-based fee percentages falling, it’s clear that the app stores are contributing to disinflationary pressures.

Conclusion

Both historically and currently, the broad swath of tech, telecom, and ecommerce companies appear to be leaders in the fight against inflation. Data from the government and elsewhere shows no evidence of accelerating price increases in this sector.

Today, the Senate Judiciary Committee announced a markup of an antitrust bill aimed at a handful of America’s most successful technology companies, led by Senator Amy Klobuchar (D-MN). The bill will harm American consumers and American middle-class jobs from coast to coast.

Dr. Michael Mandel, Vice President and Chief Economist of the Progressive Policy Institute, released the following statement:

“The digital economy should be a source of pride for Democrats. Digital inflation is low, wage growth in the tech-ecommerce sector is extremely rapid, and digital job creation is strong – especially in pivotal swing states.

“Instead, if this bill is passed, it will undercut the tech and ecommerce industries – which are vital to our 21st century economy – and give China the edge in leadership and the digital economy. The Senate and House bills are unpopular with voters in the battleground congressional districts, and will likely stunt job growth in these pivotal swing states ahead of the 2022 election.

“Senate Democrats should rethink their push to cater toward the extremes of the party and instead focus on pragmatic, pro-growth legislation that makes the digital economy stronger.”

The Mosaic Economic Project application process is now open for the March 2022 Women Changing Policy workshop, scheduled for February 28 to March 2, 2022.

“The Women Changing Policy workshop is an opportunity to connect with and learn alongside other diverse experts in fields where women are traditionally underrepresented” said Jasmine Stoughton, Project Lead. “Through our interactive workshop, participants hone the skills necessary to engage with lawmakers and the media.”

This is the fourth Women Changing Policy workshop. Previous workshops have included candid conversations with seasoned media professionals, policy leaders, and representatives from the United States Congress.

Applicants should be well established in their careers and eager to grow their profile in the policy arena. This workshop will be held in person in Washington, D.C., and the deadline to apply is February 11, 2022.

The Mosaic Economic Projectis a network of diverse women with expertise in the fields of economics and technology. Their programming aims to bring new voices to the policy arena by connecting cohort members with opportunities to engage with top industry leaders, lawmakers, and the media.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

On a new episode of the Radically Pragmatic podcast, PPI’s Mosaic Economic Project examines the findings of the 2021 Greater New Orleans Startup Report. The episode explores topics such as the growth, resiliency, and economic sustainability of New Orleans – including the effects of increased remote work options – and dives into solutions to bridge gaps in race and gender equity in critical areas from entrepreneurship to COVID relief.

Hosts Jasmine Stoughton and Crystal Swann were joined by Emily Egan, Director of Strategic Initiatives at the Albert Lepage Center for Entrepreneurship and Innovation at Tulane University, and Ann Marshall Tilton, Community Engagement Manager at the Albert Lepage Center.

Listen to the podcast here:

The Mosaic Economic Project is a network of diverse women with expertise in the fields of economics and technology. Mosaic programming aims to bring new voices to the policy arena by connecting cohort members with opportunities to engage with top industry leaders, lawmakers, and the media.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Republicans hoping to capitalize on high inflation have proposed a surprising solution: ending COVID-19 restrictions. But surrendering to COVID is the wrong cure for inflation. It would endanger public health without addressing the supply-chain snarls that are pushing prices higher. Ending pandemic inflation requires making the global economy a safe place to spend, work and live by continuing the fight against the virus.

The United States is enjoying an exceptionally strong economic recovery thanks in part to the bold stimulus actions lawmakers took last March. But businesses are raising prices, some because they and their competitors are bidding up the cost of workers and materials, and others simply because strong demand means that they can. Consumer prices were 6.8 percent higher in November than they were a year before, and almost half of households say inflation is hurting their finances.

Summary: Because of their mixed urban/rural nature, swing states are a magnet for digital “tech-ecommerce” jobs. Democrats should consider building their 2022 political narrative around support for the digital economy, which brings strong job growth, higher wages, and lower inflation to swing states.

1. This piece is primarily economic, not political. But to focus our analysis, we start with a list of eight potential 2022 Senate swing states: Arizona, Florida, Georgia, Nevada, New Hampshire, North Carolina, Pennsylvania, and Wisconsin. Adding or subtracting a state from this list doesn’t change the analysis appreciably.

2. For the most part, swing state employment is still below pre-pandemic levels, creating a handicap for the party in power. For example, Wisconsin had 260,000 fewer private sector jobs in November 2021 than in November 2019. The only swing state above pre-pandemic employment levels is Arizona.

3. Average hourly wage growth has significantly lagged national inflation in most swing states, That means real wages are falling on average in the swing states, an obstacle to making a positive economic argument. Once again, there is one exception, North Carolina.

4. However, voters in most swing states are benefiting from exceptionally dynamic job creation in the digital “tech-ecommerce” sector. The reason is not hard to understand. Swing states, by their nature, tend to have a mixed urban/rural character. Not surprisingly, ecommerce fulfillment centers are often sited in areas that are within easy driving distance of large populations but where land is relatively cheap, making them a good match for swing states. Similarly, software and internet operations looking to broaden out from the Bay Area and Boston will pick cheaper locations near to good urban amenities.

5. Digital employers gravitated to swing states during the Biden Administration. From the second quarter of 2020 to the second quarter of 2021, the most recent data available, swing states showed a 14% gain in tech-ecommerce jobs By comparison, the rest of the country only showed an 8% gain in tech-ecommerce jobs over the same period.

6. We’ve bolded the key numbers in the table below, which lays out the job gains by digital industry. Ecommerce fulfillment and warehousing jobs registered a 22% gain in the swing states, almost double the 12% gain in the rest of the country. The same thing held true for the electronic shopping industry (which mainly consists of those establishments that are in the technology end of electronic shopping but don’t do fulfillment). Also showing strong swing state growth was internet publishing, which also includes search and other “internet-type” companies.

By contrast, job growth in manufacturing and healthcare was weaker in the swing states than the rest of the country. These states see their future in tech and ecommerce.

Table 1. Swing States Lead In Digital Growth

Employment change, 20Q2-21Q2

Swing states

Other states

Computer and electronic manufacturing

-1.6%

-0.4%

Electronic shopping

18.5%

11.8%

Local delivery

12.4%

13.9%

Ecommerce fulfillment and warehousing

22.1%

12.3%

Software publishing

11.8%

8.7%

Data hosting

12.6%

6.1%

Internet publishing and other information services

14.6%

6.1%

Computer software systems

7.1%

3.5%

Tech-ecommerce (total)

14.0%

8.1%

Private

11.2%

10.6%

Manufacturing

5.0%

6.1%

Healthcare and social assistance

5.6%

6.4%

7. What are the positive economic stories in individual swing states? Digital employers in Arizona, Florida, Nevada, North Carolina, and Wisconsin are adding digital jobs at a faster rate than private sector jobs. Voters in North Carolina, for example, have benefited from 20% growth in tech-ecommerce jobs, almost double private sector job growth.

Table 2. Digital Jobs Drive Swing State Growth

Employment change, 20Q2-21Q2

Tech-ecommerce

Private sector

Arizona

16.7%

8.6%

Florida

18.2%

10.8%

Georgia

8.6%

10.4%

Nevada

24.6%

21.4%

New Hampshire

8.4%

13.4%

North Carolina

20.3%

11.5%

Pennsylvania

7.8%

12.4%

Wisconsin

10.2%

9.1%

Swing states

14.0%

11.2%

All other states

8.1%

10.6%

8. A strong economic narrative around digital growth in the swing states depends on wages as well. On average, tech-ecommerce jobs pay significantly more than the average for the private sector in every swing state. For example, in the second quarter of 2021, tech-ecommerce workers in swing states got paid at an average annual rate of $81,000, 39% more than the private sector average of $58,000. This includes the full range of tech-ecommerce jobs, from software developers to fulfillment center workers.

Table 3. Workers in Digital Jobs Are Paid More on Average

Annual pay, thousands of dollars, based on 21Q2

Tech-ecommerce

Private sector

Arizona

76

59

Florida

81

57

Georgia

83

60

Nevada

65

57

New Hampshire

111

71

North Carolina

86

57

Pennsylvania

81

62

Wisconsin

77

53

Swing states

81

58

All other states

123

66

All other states except California and Washington

96

62

9. The core of the tech-ecommerce job boom in the swing states is the expansion of ecommerce jobs. These jobs pay well for high-school educated workers. Amazon pays its starting distribution workers an average of $18 per hour. That’s roughly comparable to starting manufacturing wages in many parts of the country. Overall, ecommerce industries pay about 30% more than brick-and-mortar retail in swing states, on average. This is at the heart of a powerful political narrative of growth that creates better jobs.

Table 4. Ecommerce Industries Pay More than Brick-and-Mortar Retail

21Q2 pay in thousands at annual rates

Ecommerce industries

Brick-and-mortar retail

Arizona

48

41

Florida

49

39

Georgia

45

36

Nevada

46

39

New Hampshire

57

38

North Carolina

40

35

Pennsylvania

51

34

Wisconsin

45

31

Swing states

47

37

Other states

62

38

Other states ex California and Washington

51

37

10. Democrats have a chance to build a powerful economic narrative around strong digital growth in swing states. They should embrace this opportunity.

Ben Ritz is Director of the Center for Funding America’s Future at the Progressive Policy Institute, Jason Fichtner is Vice President and Chief Economist at the Bipartisan Policy Center, and Charles Blahous is the J. Fish and Lillian F. Smith Chair and Senior Research Strategist at the Mercatus Center.

Despite repeated warnings from Social Security’s trustees that the program is facing a growing financial shortfall, lawmakers seem to have reached a bipartisan consensus to kick the can down the road. If they continue procrastinating until Social Security’s trust funds near depletion in the 2030s, it will be impossible to save the program without abruptly cutting benefits for retirees or significantly reducing the lifetime incomes of young workers. Americans who rely on Social Security cannot afford to wait much longer for lawmakers to enact corrections.

Unfortunately, a new proposal that was the subject of a congressional hearing earlier this month, Social Security 2100: A Sacred Trust, moves in the wrong direction. It would worsen intergenerational inequities by providing substantial benefit increases for those becoming benefit-eligible in 2022-2026, while passing the costs to everyone else, especially young workers already getting the short end of the stick under current law. There is no justification for such discriminatory treatment. In fact, those who would receive the proposed windfall already benefit from superior treatment under current Social Security law, relative to those who would pay for it.

As the U.S. Senate postpones its vote on the Build Back Better Act (BBBA) into next year, it’s becoming increasingly clear that lawmakers’ attempt to enact almost every major program proposed by President Biden on a temporary basis — rather than prioritize a few key programs or find enough revenue to sustainably finance all of his proposed programs permanently — threatens both the bill’s prospects for passage and the success of its core initiatives should the bill become law. Democrats must rethink and revise this approach to address the most urgent national needs and secure a successful legacy for President Joe Biden.

The problem became clear last week in part thanks to a new estimate from the nonpartisan Congressional Budget Office, which suggested that the policies in the House-passed version of the BBBA would cost over $4.7 trillion between now and 2031 if none of them are allowed to expire before then. CBO’s analysis has given pause to Sen. Joe Manchin (D-W.Va.), who has consistently said he would only commit to supporting a bill that increases federal spending by no more than $1.5 trillion over the next decade and fully covers offsets the additional cost. Manchin holds the crucial 50th vote needed to pass any bill through the Senate without Republican support, so the bill cannot move forward until his concerns are addressed.

Clearly Americans are concerned about inflation. Prices for most food and energy products are soaring, which hits them right in the wallet. The Biden Administration finds itself on the political defensive, as prices increases are outstripping wage increases for most workers.

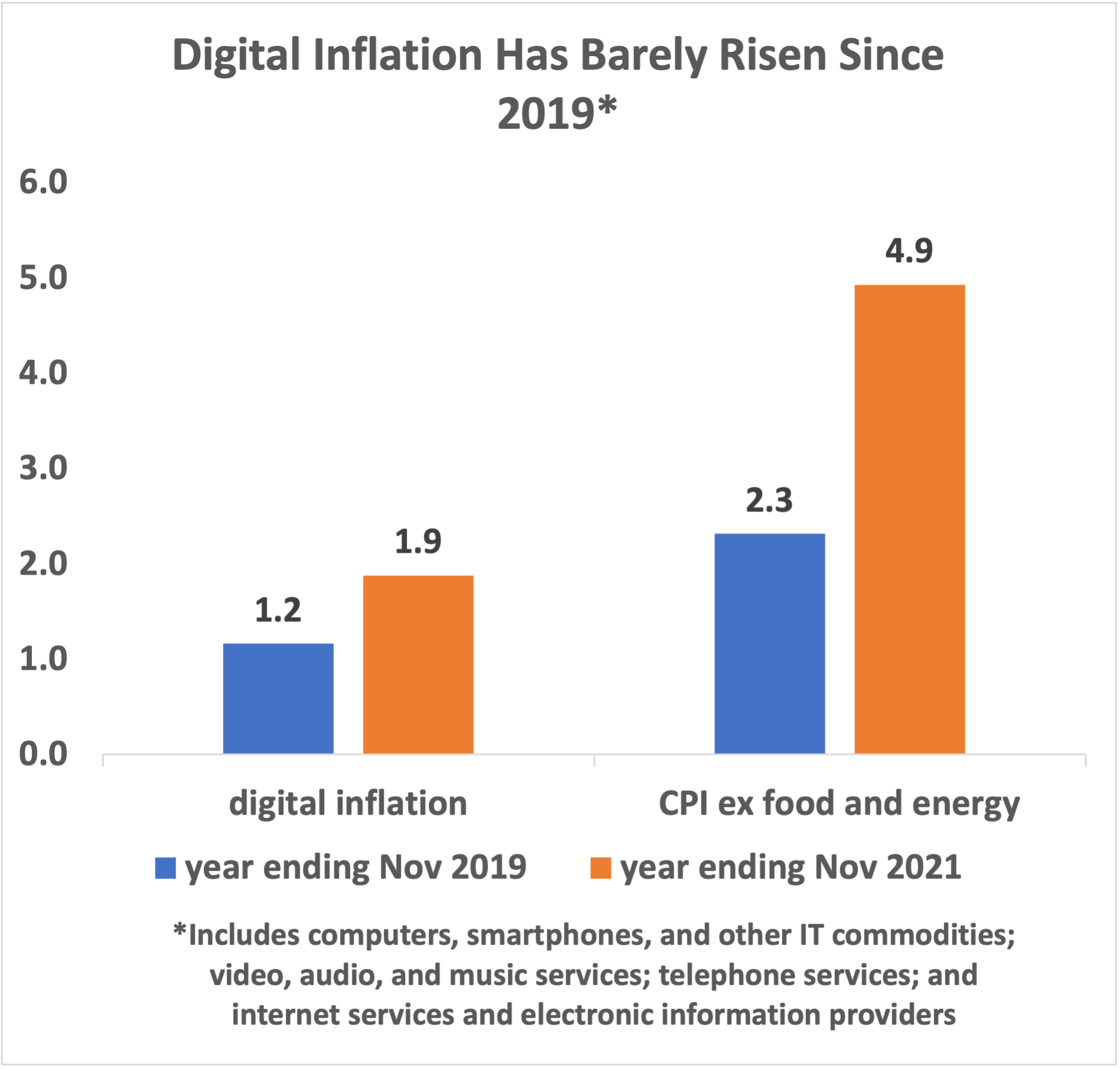

But here’s an important piece of good news that is not getting enough attention. Inflation remains low in the digital sector, even as it accelerates across much of the economy. Start with consumer inflation (as measured by the CPI). Over the past year, prices for digital consumer goods and services tracked by BLS (see graphic) have risen by only 1.9% overall, compared to 4.9% for CPI ex food/energy and 6.8% for total CPI.

Digital consumer goods and services include computers, smartphones and other IT commodities; video, audio, and music services; wired and wireless phone services; and internet services and electronic information providers.

The chart shows that digital consumer inflation has risen only 0.7 percentage points (PP) compared to November 2019, while consumer inflation ex food/energy has risen 2.6 PP. For example, the inflation rate for “internet services and electronic information providers” has only risen by 0.7 PP (from 1.5% to 2.3%).

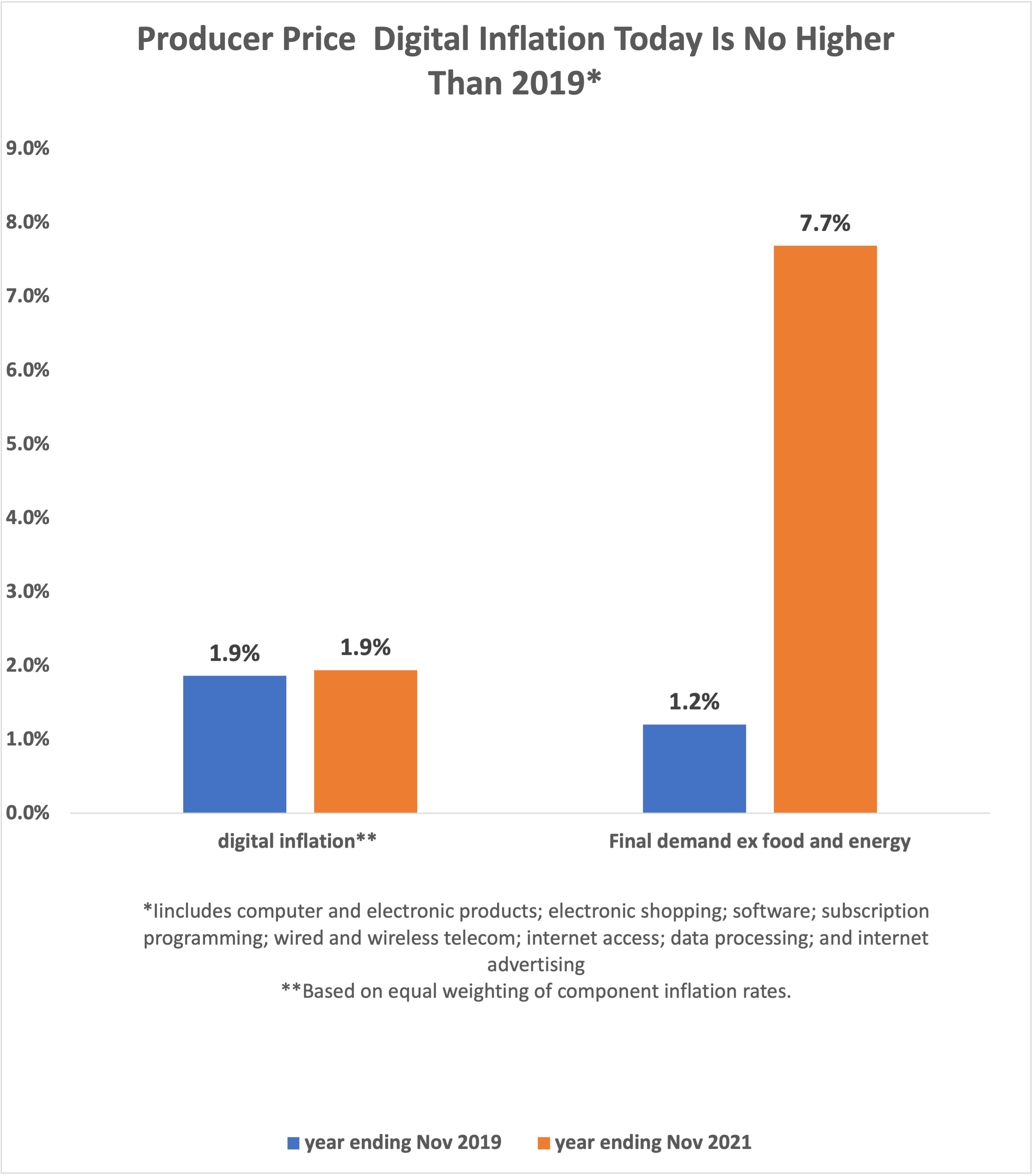

When we look at producer prices, we see a very similar phenomenon:Producer price inflation in the digital sector is no higher today than it was before the pandemic. Over the past year, producer prices for digital goods and services tracked by BLS (see graphic) have risen by only 1.9%, compared to 7.7% for final demand ex food and energy.

Final demand inflation (ex food and energy) accelerated from 1.2% in the year ending Nov 2019 to 7.7% in the year ending Nov 2021. But digital producer price inflation was roughly constant at 1.9% in both periods (this calculation was done giving equal weights to each component).

Digital producer prices include computer and electronic manufacturing; electronic and mail order shopping services; software publishers; cable and other subscription programming; wired and wireless telecom; internet access; data processing; and internet publishing and web search advertising.

Some examples: The producer price of internet access services rose by only 0.3% over the past year, up only slightly from the -0.3% rate in November 2019. The producer price charged by software publishers fell by 0.3%, a slightly bigger decline compared to two years ago. The producer price index for telecommunications, both business and residential, is running at a 1.1% rate, slightly down from the 1.2% rate in November 2019.

The digital sector is exerting a dampening effect on both consumer and producer price inflation, reflecting large productivity-enhancing capital investments by digital companies. Meanwhile productivity has lagged in sectors such as food processing, where prices are skyrocketing.

However, the digital sector is not getting enough “credit” in the overall numbers for holding down inflation. For example, there’s no doubt that the digital sector is much more important to Americans today than it was in pre-pandemic 2019. Yet the digital sector gets a smaller weight in the CPI today than it did in 2019, because spending on digital goods and services is a smaller share of the consumer basket. That’s good news, but it has a perverse effect on the calculation of the overall inflation rate.

We may have to move towards a time-weighted versus expenditure-weighted CPI. Certain tasks, like dealing with the DMV or health insurers, are more “costly” in time than money. Conversely, digital services save you time that doesn’t show up in the official stats.

Time-weighted CPI would take into account that digitizing tasks, including shopping, generally reduces time spent by consumers, while adding more regulations generally increases time spent.

A time-weighted approach to CPI would likely show higher inflation for rural and poorer Americans. It would allow us to think about how cutting government bureaucracy and saving the time of Americans actually reduces inflation.

From the political perspective, the Biden Administration can make a strong case that the digital goods and services that are so important to Americans these days are barely rising in price. And America’s digital leadership will continue to hold down price increases once the temporary supply chain issues abate.

Looking out at the Pacific this year, worried farmers see giant cargo ships turning around empty, leaving their wine, butter and almond cargoes on the docks and at least $1.5 billion in exports lost. Meanwhile, 80-ship pileups off the coast of Southern California mean weeks or even months of delays unloading industrial inputs and consumer goods; and with truckers and warehouse workers quitting their jobs at record rates, full containers are piling up in fields and parking lots.

The port problems are complicated and serious enough to worry even President Biden, who has given speeches and put out policies to head off complaints about everything from empty shelves during Christmas shopping weeks to lost farm exports and inflationary bottlenecks.

But they’re also the sort of problems administrations are happy to have. This is because they’re evidence of confident consumers, workers finding new opportunities, and a successful effort, at least so far, by the Biden administration’s work to create a strong economy that grows from the middle out.

Today, the Innovation Frontier Project (IFP), a project of the Progressive Policy Institute, hosted a virtual conference for policymakers, staffers and journalists titled “How Better Statistics Lead to Better Policy in a Changing World.” The Innovation Frontier Project assembled a panel of leading experts who addressed the need for new statistics in the key areas of the digital economy; healthcare; and supply chains. They showed how a relatively small investment in improving our data can avoid huge policy mistakes.

The Progressive Policy Institute’s Innovation Frontier Project hosted a virtual conference for policymakers, staffers and journalists titled “How Better Statistics Lead to Better Policy in a Changing World”.

Our economy is becoming increasingly global and digital, but economic statistics are slow to adapt to this new reality. In many ways policymakers are flying blind: Why don’t we have the data we need on the digital economy, the price and value of cutting-edge medical treatments, and global supply chains and inflation? Innovation is everywhere except in the economic statistics.

The Innovation Frontier Project assembled a panel of leading experts who addressed the need for new statistics in the key areas of the digital economy; healthcare; and supply chains. They showed how a relatively small investment in improving our data can avoid huge policy mistakes.

Watch the event here.

WHAT: Virtual conference for policymakers, staffers, and journalists

WHEN: Friday, December 3; 11:00am-2:00pm ET; Zoom

PURPOSE: This conference brings together leading experts to show how our economic statistics need to be improved to avoid policy mistakes in the digital and global economy.

MODERATORS:

Michael Mandel, Vice President and Chief Economist, PPI Arielle Kane, Director of Health Policy, PPI

A package of antitrust legislation recently introduced in Congress aims to improve competition in the U.S. technology sector. The proposed provisions in these bills would limit digital platforms’ ability to integrate product features, promote new products, or even compete in new market segments.

We conclude that such restrictions will harm U.S. scientific and technological leadership, hurting U.S. competitiveness and living standards.

Antitrust regulations that reduces commercial scale and product scope weaken incentives for corporate research and undermine the ability to innovate.

We highlight how these limitations may affect American scientific and technological leadership in the world. We also consider the role of information technology firms in advancing U.S. technology, the foreign competition they face, and the fragile nature of the U.S. innovation ecosystem.

Today, the Innovation Frontier Project (IFP), a project of the Progressive Policy Institute, released a comprehensive research deck on the threats facing American innovation. The authors of the deck, innovation experts Ashish Arora and Sharon Belenzon of Duke University, found the United States has lost a substantial amount of corporate research since the 1980s, with only a handful of present-day U.S.-based companies investing in research at a meaningful level.

This deck also lays out clear political implications for lawmakers. The Biden Administration’s top strategic economic priorities are based on a foundation of strong U.S. competitiveness and innovation, yet Congress’s percolating anti-tech antitrust legislation would undermine these priorities by impairing the ability of America’s few leading R&D performers to develop new products and enter new markets. The restrictions on these companies will reduce our national investment in R&D and hurt American economic prosperity and national security.

“America’s technological leadership is being challenged, and if we undermine our business research leaders we risk losing this fight with China. The Biden Administration has identified key priorities in emerging technologies, but Congress’s anti-tech antitrust legislation would hurt these priorities. Our policymakers need to get smart about the steps needed to regain our footing as a technological leader,” said Dr.Michael Mandel, Chief Economist for the Progressive Policy Institute.

The deck findings issue a stark warning:

America’s technological leadership is under challenge.

The United States has lost a substantial amount of corporate research since the 1980s.

Corporate research is the source of many breakthrough innovations.

American leadership in emerging technologies depends on corporate research and only a few companies continue to invest in research at a meaningful level.

The antitrust proposals will impair the ability of these few leading R&D performers to develop new products and enter new markets.

The loss of tech companies with scale and scope would reduce U.S. investments in R&D and hurt American economic prosperity and security.

This deck was authored by Ashish Arora and Sharon Belenzon of Duke University. Mr. Arora is the Rex D. Adams Professor of Business Administration at the Duke Fuqua School of Business. He received his PhD in Economics from Stanford University in 1992, and was on the faculty at the Heinz School, Carnegie Mellon University, where he held the H. John Heinz Professorship, until 2009. Mr. Belenzon is a professor in the Strategy area at the Fuqua School of Business of Duke University and a Research Associate at the National Bureau of Economic Research (NBER). His research investigates the role of business in advancing science and has been featured in top academic journals, such as Management Science, Strategic Management Journal and American Economic Review. Mr. Belenzon received his PhD from the London School of Economics and Political Science and completed post-doctorate work at the University of Oxford, Nuffield College.

Based in Washington, D.C., and housed in the Progressive Policy Institute, the Innovation Frontier Project explores the role of public policy in science, technology and innovation. The project is managed by Jack Karsten. Learn more about IFP by visiting innovationfrontier.org.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

By comparison, the data for the overall retail industry has shown a much worse inflation performance, measured by margins. Margins for the total retail industry rose by 48% since December 2007, much faster than consumer inflation. As a result, real margins for the retail industry as a whole have risen, putting upward pressure on consumer prices.

By comparison, the data for the overall retail industry has shown a much worse inflation performance, measured by margins. Margins for the total retail industry rose by 48% since December 2007, much faster than consumer inflation. As a result, real margins for the retail industry as a whole have risen, putting upward pressure on consumer prices.