The U.S. economy recently marked 10 years of economic expansion – its longest in history – but there’s an important exception: new business creation. In recent decades, the American entrepreneurial engine has decelerated. Regulatory reform could help revive American entrepreneurship, reducing the burden on new businesses and realizing gains in economic growth. That doesn’t necessarily mean deregulation, but rather streamlining and updating old or obsolete rules to provide entrepreneurs with flexibility in today’s fast-changing world.

New and young businesses are the foundation of the United States’ economy, creating jobs and spreading wealth across our society. “Together, startups and high-growth firms (which are disproportionately young) account for about 70 percent of firm-level gross job creation in a typical year,” write entrepreneurship researchers Decker et al. Many of these young companies go on to become the next generation of small businesses, which employ 48 percent of private sector employees.

Unfortunately, the rate at which new businesses are being created has fallen off in the wake of the Great Recession. While firm deaths have returned to their pre-recession levels, firm births are down 22 percent compared to 2006 levels. And, for the first time since the Census Bureau began collecting data, firm deaths exceeded firm births from 2009 to 2011.

Smart policy can help increase the number of new businesses that are created and the number that scale up, though. Regulation is one area where policy can be made more efficient. A 2017 National Small Business Association survey estimated that the average small business owner spends at least $12,000 every year on compliance, with nearly one in three spending more than 80 hours every year dealing with federal regulation.

We know from research by Victor Bennett and Ronnie Chatterji that many people have entrepreneurial aspirations, but fail at many steps along their path to move to actual business formation. While many fail at early stages, such as basic market research, others undoubtedly run up against these mountainous regulatory costs and say, “not worth it.”

One way to reduce these costs is to focus on the steady buildup of regulation, or regulatory accumulation. The Code of Federal Regulations, where rules promulgated by the federal government are published annually, swelled by 17 percent from 2008 to 2018 alone. While Washington has dozens of agencies that issue new rules, not one institution is dedicated to streamlining the accumulated body of regulations. That’s why PPI proposed the Regulatory Improvement Commission (RIC). The RIC would fill an institutional vacuum in regulation policy by creating a mechanism for the periodic clearing out of obsolete rules.

Modeled on the Base Realignment and Closure Commission (BRAC) and comprised of a bipartisan group of highly qualified stakeholder appointees, the RIC would be an independent commission of eight members, appointed by the President and Congress, with regulatory expertise across industry and government. It would meet as authorized by Congress to review and, following a public comment period of 60 days, draw up a list of 15 to 20 rules for elimination or modification. The package would be sent to Congress for an up-or-down vote, and the RIC would be disbanded. If the proposed changes pass Congress, they would go to the president’s desk for signature or veto.

In 2015, bipartisan groups of lawmakers introduced bills in the House and Senate to establish the RIC based on the BRAC model. House cosponsors included Mick Mulvaney (R-SC), now acting White House Chief of Staff, and Kyrsten Sinema (D-AZ), now a Democratic Senator from Arizona.

Startup-friendly policies such as the RIC can help reduce compliance and opportunity costs, catalyzing a rebound in America’s startup rate and spurring economic growth. Streamlining regulation would help inventors and entrepreneurs spend less time and resources on regulatory compliance and focus instead on delivering goods and services and scaling their enterprises.

Research assistance was provided by Roman Darker, economics intern at the Progressive PolicyInstitute.

How much do the Apple App Store and Google Play, the two major mobile application stores, charge? The short and obvious answer is that Apple and Google levy a fee of 30% of the revenue from downloading paid apps; 30% of revenue from in-app purchases of digital goods and services; and a lower charge of 15% for renewed subscriptions.

But this answer is at best incomplete, and perhaps wrong. The two major app stores also provide a distribution and download service for millions of “free” apps—including testing them for malware—while charging only a minimal fixed fee to each developer. These free apps can potentially generate a big benefit for consumers and a large return for their owners.

To put it more precisely, the app stores provide a distribution, search and validation service to all app developers and app owners for nearly nothing. This service is the equivalent of a major retailer like Walmart providing free shelf space to millions of different goods owned and sold by other companies.

The average price charged by Apple and Google is therefore much less than the face value of 30%, if we take into account the large number of free apps. Our preliminary scenario analysis suggests that the revenues collected by the app stores could be in the range of 4-7% of the value generated by all apps in the app stores, including both free and paid.

For many Americans, one traffic ticket could be all it takes to derail their financial security — and perhaps even their livelihood.

Loathe to raise taxes, many states and cities are increasingly relying on fines and fees — whether for traffic offenses, court costs or misdemeanors such as littering — to fill their coffers. The amounts demanded are often exorbitant, and fall disproportionately on low-and moderate-income Americans who can least afford to pay. In California, for instance, the Lawyers’ Committee for Civil Rights found that a $100 traffic ticket can ultimately cost a motorist as much as $815 after various surcharges, “administrative” fees and late penalties are factored in — a cripplingly large figure even for someone who is relatively wealthy.

Unlike such polarizing issues as health care, immigration and climate change, repairing and updating our economic infrastructure is something both parties say they are for. Yet somehow our political leaders can’t get the job done.

President Trump often complains about the shabby state of America’s airports, highways and railways. “The only one to fix the infrastructure of our country is me — roads, airports, bridges,” he tweeted just before launching his 2016 presidential bid. “I know how to build, pols only know how to talk!”

Yet Trump’s lack of focus and discipline, along with his clownish political antics, keep sabotaging bipartisan progress on infrastructure. In a meeting with House Speaker Nancy Pelosi and Senate Democratic leader Chuck Schumer in April, Trump proposed to spend $2 trillion on infrastructure. But the deal quickly unraveled as Republican Senators made clear they wouldn’t support gas or other tax increases to pay for it.

As Congress begins to turn toward tax policies to help clean energy manufacturing, electric vehicle tax credits aimed directly at more affordable vehicles are gaining speed, just as a previous Forbes column and a Progressive Policy Institute (PPI) white paper urged several months ago.

The question now is will EV advocates in Congress, the U.S. auto industry and labor unions get the message and reform tax incentives to benefit middle-income Americans. Such revised tax credits focused on more affordable EVs will increase the chances new incentives become law, and will better allow the U.S. to reap the remarkable economic, health, manufacturing and environmental benefits of EVs. Yet as of now, new EV tax credits have been left entirely out of a so-called “tax extenders” outline circulating among House Ways and Means Committee members.

But a series of new developments are demonstrating that tax credits focused on affordable vehicles are gaining momentum.

President Donald Trump staked his successful claim to the U.S. presidency with his appeal to the discontents of blue-collar America — i.e., non-college-educated Americans who have perhaps been the hardest hit by globalization and technological change.

The same voters are the target of some of Trump’s Democratic 2020 challengers, most notably former Vice President Joe Biden. Biden, for instance, launched his campaign in a Pennsylvania union hall, declaring himself to be “a union man, period.”

Both Biden and Trump are right to focus their attentions on this group of Americans, whose fortunes have not risen with the overall economy but stagnated or even fallen. Without the benefit of higher education, working class Americans have been unable to compete for jobs demanding specialized technical skills, while the places they live have been hollowed out by shifts in global supply chains and the death of low-skilled manufacturing. So long as these workers feel left out of the economic mainstream, they will remain a potent political force, including in the upcoming 2020 election.

President Trump is apparently a trade alchemist. He’s taken the core of NAFTA (the “worst trade deal ever”), liberally sprinkled in modern rules from the Trans Pacific Partnership (a “potential disaster”), and created a “brand new” trade deal — the US-Mexico-Canada Agreement (USMCA).

Trump’s hyperbole aside, the USMCA, while not perfect, would do a creditable job of preserving the essential rules of the road for North America’s highly integrated, $22 trillion economy. It would also update the decades-old NAFTA by, among other things, adding enforceable labor and environmental rules, promoting digital commerce, and cutting red tape for small business. Given Trump’s years of railing against NAFTA and repeated threats to terminate the Agreement, this is a positive development.

For the USMCA to enter into force, it must be approved by Congress, including the Democratic-controlled House. In recent weeks, Trump hasn’t been helping this process. Insulting and trying to bulldoze House Democratic leaders and threatening damaging new tariffs on Mexico are hardly constructive strategies.

Progressives say that they want Corporate America to think long-term rather than short-term: To invest in research and development, to spend more on domestic plant and equipment, and to hire more workers with decent pay and decent benefits. In fact, we’ve designed the tax system specifically to give companies incentives to do that.

That’s why Joe Biden should be applauding Amazon rather than criticizing it. In a tweet on Thursday, Biden wrote: “I have nothing against Amazon, but no company pulling in billions of dollars of profits should pay a lower tax rate than firefighters and teachers. We need to reward work, not just wealth.”

But if there’s any company that’s about investing in America and American workers, it’s Amazon. Amazon was #3 in our 2017 list of the top companies ranked by U.S. capital spending, putting $12 billion into the U.S. economy that year alone. Because of the productivity gains from these investments, the company was able to institute a $15 minimum wage for all full-time, part-time and temporary workers, covering even low-wage states like Tennessee, where the hourly median wage for all workers is less than $17. The productivity gains have also sent the stock price soaring, putting billions of taxable dollars into the hands of Amazon employees in the form of restricted stock units. And Amazon funnels back billions of dollars each year in long-run R&D spending.

The federal tax system is intentionally designed to reward this type of corporate behavior and strong performance. For example, the 2017 changes to the tax code allow a company like Amazon to deduct much of its capital spending from its taxable income right away, lowering its tax bill. R&D spending gets a sizable tax credit from the federal government as well. And the rules covering the exercise of stock grants, while lowering Amazon’s tax bill, could be generating a great deal of personal tax revenue for the government.

Here’s why: A stock grant—which were given to many Amazon employees, and not just the top ranking executives—is more valuable the higher the stock goes. When the employee is granted stock, it is generally taxed by the government as ordinary income. Meanwhile, part of that cash is deducted from the company’s income, just like any other worker pay, lowering the company’s taxable income. In other words, the more successful the company is, in terms of a rising stock price, the more money flows to employees. And the more money that flows to employees, the more taxes are paid by the employees as personal taxes rather than corporate taxes.

So it’s not surprising that a successful company like Amazon that is investing in America is going to have a lower tax rate than workers—the tax system is designed that way. Conversely, a company that is not investing in R&D or capital spending, and has a falling stock price, may be paying a bigger share of its income in taxes—but is it really benefiting Americans?

Progressives may not be satisfied with everything that Amazon is doing. But Biden and other Democrats shouldn’t blame Amazon for investing in America, and then following the rules of a tax system that is specifically designed to encourage corporate investment. It’s good for workers and consumers.

Trade war! In my previous column on China and digital manufacturing, I observed that the low price of Chinese imports has been artificially suppressing domestic investments in manufacturing automation. The process of digitization is expensive and risky, and rational investors and managers won’t spend money if they know they will be immediately undercut by Chinese competitors.

Now President Donald Trump has amped up a trade war with China. The new tariffs will hit consumers in their wallets, as even Trump economic advisor Larry Kudlow agrees. Moreover, the trade war runs the risk of boosting inflation, raising interest rates, and potentially tipping the economy into recession.

But for companies in the digital manufacturing space, there’s a silver lining to the dark cloud of the trade war. Suddenly the risk-benefit calculation of investment in digitization starts to look more attractive, purely as an economic proposition. For one, sourcing parts out of China is becoming riskier and potentially more expensive.

With perfect timing, Xometry, a Gaithersburg, Md-based manufacturing platform which calls itself “the largest on-demand manufacturing marketplace,” with more than 2500 U.S. manufacturing partners, just announced a $50 million equity funding round to further build out its capabilities. An article in the Wall Street Journal noted that Xometry’s business “can help blunt small companies’ exposure to price fluctuations and shortages as trade tensions and U.S. tariffs on steel and aluminum make prices more volatile.”

“We’ve definitely seen more requests for reshoring but I don’t think the tides have fully turned,” adds Dave Evans, CEO and co-founder at Fictiv, a high-profile San Francisco-based manufacturing platform. Rather, says Evans, companies are “tariff engineering” their product to reduce costs by making specific parts or assembling locally in the U.S.

For manufacturers of robotics and other industrial automation equipment, the trade war is a mixed bag. On the one hand, domestic companies are gearing up to invest more in robotics. On the other hand, China has been investing heavily in automation, and those markets may be in trouble as the trade war heats up.

For now, manufacturers are still hoping that the China-US trade war will turn out to be only a skirmish. But at some point, companies that have relied on China for their production will decide that the combination of trade tensions and new technology and new business models–what we have called the Internet of Goods–make it more profitable to produce in the domestic market for the domestic market. And that’s when the digital revolution in manufacturing will really take off.

If you think your credit report is accurate, there is a good chance you are wrong. According to the Federal Trade Commission (FTC), one in five Americans has a potentially material error in their credit file, and one of the biggest contributors is medical bills—with half of all medical bills containing an error.

In fact, mistakes on credit reports have become so pervasive that around a third of all complaints filed annually to the Consumer Financial Protection Bureau (CFPB) resulted from problems with consumer credit reports.

Credit report errors are a serious threat to the financial well-being of American families. As Senator Elizabeth Warren has noted, “credit reports regularly contain errors that can make it harder for families to access credit, find jobs, and get housing.” And as many consumers know all too well, it’s very difficult to get those errors corrected.” (1)

Under the Fair Credit Reporting Act, the company that furnished the information to the credit bureau must conduct an investigation to verify the information and correct a mistake, if they find one. Unfortunately, consumers who want to try to fix mistakes on their credit report face three daunting obstacles.

First, the system put into place by the credit reporting agencies heavily favors creditors and other data furnishers. Credit bureaus almost exclusively depend on lenders (such as banks, credit unions, credit card providers, and mortgage underwriters).

Consumers contacted the credit reporting agencies approximately eight million times in 2011 to initiate a credit dispute. But only a small fraction of those disputes was resolved internally by credit bureau staff. According to the CFPB, 85 percent of credit report disputes are passed on to data furnishers (the lenders) to investigate and resolve. (2) Unfortunately, in most cases the disputes are then shelved unless the consumer perseveres.

Second, the credit report agencies earn their profits by providing services such as credit checks to the very entities that provide the data used to create the credit reports – banks, mortgage lenders, credit card companies, retailers, and other businesses that provide credit. This creates a serious conflict of interest.

Third, despite several notable efforts to try to empower consumers, trying to correct errors on your credit report is still tedious, confusing, and time consuming.

CREDIT REPAIR ORGANIZATIONS AND COMPANIES

Because the system is rigged against them, many consumers turn to credit counseling agencies or credit repair companies. The dispute system designed to help consumers fix the problem favors the position of the debt collector over the consumer. Specifically, the credit bureau is only legally required to check with the creditor or debt collector and ask them whether they stand by their claim. As long as the creditor says you owe money, the dispute is resolved in their favor. As the National Consumer Law Center concludes: “Credit bureaus have little economic incentive to conduct proper disputes or improve their investigations.” (3)

Credit counseling agencies are typically a free resource from nonprofit financial education organizations that review your finances, debt and credit reports with the goal of teaching you to improve and manage your financial situation.

A credit repair company is a firm that offers to improve your credit in exchange for a fee. Unfortunately, the quality of these firms varies greatly. Some credit repair firms are highly reputable and follow best practices. Unfortunately, a significant cohort of credit repair firms are not good actors and, in some cases, have committed outright fraud. In 2016 the Consumer Financial Protection Bureau (CFPB) stated that “more than half of people who submitted complaints with the CFPB about credit repair chose the issue ‘fraud or scam’ to describe their complaints.”

There are some telltale signs for consumers trying to separate the bad actors from legitimate credit repair firms. Companies should be avoided that:

Demand an upfront payment.

Don’t provide a written agreement that includes cancellation rights for consumers.

Guarantee they’ll raise your credit score or fix an error.

Have multiple complaints against them with the Consumer Financial Protection Bureau or the attorney general’s office in the state where they operate.

Suggest they can remove legitimate negative information.

Offer to create a new credit profile based on a new employer identification number, rather than your Social Security number.

In contrast, responsible credit repair companies not only follow federal and state law but also:

Offer a free consultation

Have a track record and consistently solid reviews from past clients.

Have an attorney on staff.

Are licensed, bonded and insured.

WHAT NEEDS TO CHANGE?

To protect consumers, some policymakers have suggested new regulations to further police the credit repair industry. They note that credit repair firms don’t do anything someone with a bad credit report couldn’t do on their own. Anyone can dispute credit errors on their own behalf. But the Do-It-Yourself approach can be dauntingly complicated and time-consuming for harried families.

In essense, paying for credit repair assistance is really no different than paying an accountant or purchasing software to do your taxes – something 90 percent of Americans do according to the Internal Revenue Service.

It is important to note that there is already existing legislation to regulate the credit repair system. The Credit Repair Organizations Act (CROA) was signed into law in 1996 to protect consumers from the unscrupulous practices commonly used by several credit scammers.

Because of CROA, credit repair organizations are not permitted to misrepresent the services they provide, including guaranteeing the removal of negative credit listings. Credit repair organizations are also not permitted to attempt to create a “new” credit file or advise you to lie about your credit history. The Act also bars companies offering credit repair services from demanding advance payment, gives consumers certain contract cancellation rights as well as the right to sue a credit repair organization that violates CROA. (4)

CROA is a sensible law, and despite criticisms that it does not go far enough in regulating the credit repair industry, the law does provide consumers with protections against bad actors in the credit repair sector without eliminating legitimate credit repair firms. CROA needs strengthening, not in the form of new regulations but rather more effective enforcement.

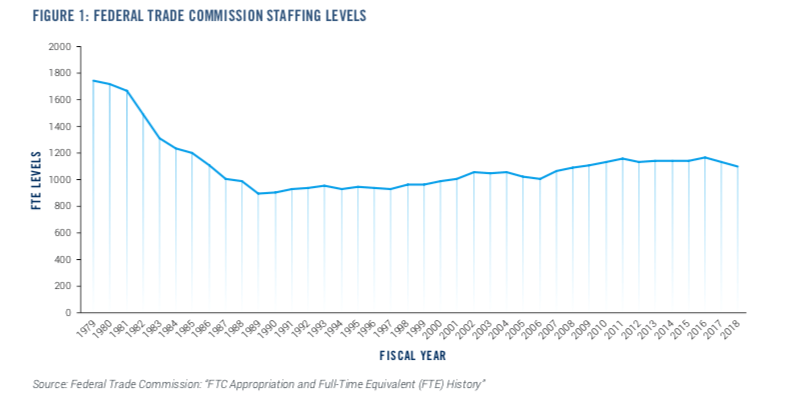

Under CROA, the Federal Trade Commission (FTC) is the primary enforcement body at the federal level. The problem is the FTC is severely underfunded and understaffed. In a Senate hearing last year Commissioner Rebecca Slaughter said the FTC’s staff level is 50 percent below its level at the beginning of the Reagan administration in 1981. Senators Jerry Moran (R-Kan.) and Catherine Cortez Masto (D-Nev.) agreed the FTC needs more resources and is “understaffed.” (5)

As Table 1 confirms, FTC staffing levels dropped dramatically during the 1980s and have never really recovered. Yet, over the same time, the responsibilities of the agency have dramatically changed and expanded. Today the FTC has to address some 2.7 million complaints a year in areas from debt collection, to identify theft, to imposter scams. (6)

Better enforcement of CROA would obviate the need to pile on new rules. Unfortunately, in fact, Congress has added to the FTC’s workload even as its workforce has shrunk. The simplest solution is to provide the FTC with additional resources dedicated to enforcing CROA and protecting consumers from those credit repair companies that have acted fraudulently or in bad faith.

To pay for this increase in supervisors, a small annual fee could be placed on the credit reporting agencies (Equifax, TransUnion, and Experian). To create an incentive for these agencies to be more responsive to consumer complaints about credit reporting agencies, the fee could be lowered or raised in synchronization with the number of consumer complaints about their credit reports.

OTHER REMEDIES

Another approach to fixing the current system is to go to the source of the problem, eliminating some of the causes for the extraordinary amount of errors made by the credit reporting industry. As Aaron Klein of the Brookings Institution has noted, there are three major reasons why credit scores are so inaccurate: “size, speed, and economic incentives of the system.”

One way to change the incentive structure would be to create some consequences for credit rating companies that frequently give lenders inaccurate data about borrowers. Lawmakers could consider legislation that would penalize credit reporting agency error rates above a certain level. Klein’s approach would use a random sample method (5 to 10 percent of complaints) to review credit rating firms’ performance. Another approach would be to grade the credit bureaus on their error and response rates.

CONCLUSION

While it is tempting to lump all credit repair firms into the same basket, many of these firms act in good faith and follow CROA to the letter of the law. Yet there is no doubt that a significant number of these companies are misleading consumers and sometimes acting fraudulently. If lawmakers really want to crack down on these bad actors, however, the first step should be strengthening enforcement of existing law.

Otherwise, spawning new laws and regulations would likely enmesh all credit repair firms in new layers of regulatory complexity and compliance burdens, making it even harder for consumers to detect and correct errors on their credit reports. In CROA we have the consumer protection law we need, now it’s time to focus on oversight and enforcement.

Many of the Democratic presidential candidates are vying to see who can be toughest on the tech sector. But here’s the paradox: New data shows that the tech boom is a major force driving down unemployment, lifting economic growth, and helping voters — precisely the people that the Democratic candidates are trying to reach.

The key here is that the economic data produced by the government is not typically presented in a form that easily shows the benefits of the tech boom. Software firms, for example, are spread across at least three different industries. Ecommerce — related activities are spread across at least two industries, electronic shopping and warehousing. And telecom includes at least two three industries, telecom services, communications equipment, and data processing and hosting.

Corporate profits are soaring. Yet Americans’ paychecks are inching upward by comparison. It’s no wonder many Americans feel anxious despite an economy that, by the numbers, is booming.

This disconnect between shareholders’ prosperity and workers’ precarity has led many on the progressive left to question the very future of capitalism. Some 2020 presidential candidates, such as Sens. Elizabeth Warren and Bernie Sanders, now routinely paint Big Business as the enemy of middle-class mobility and have called for drastic measures to rein in corporate power and mandate better behavior.

It might be too soon, however, to write off U.S. companies as a force for good.

Republicans despise federal micromanagement, but that hasn’t kept Rep. Don Young of Alaska from hopping aboard the Washington-Knows-Best Express. He recently introduced a bill mandating that freight trains have a minimum of two crew members on board trains at all times.

While Young justifies his bill on safety grounds, the bill also appears to reflect pressure from rail workers’ unions fearful that automation is putting their members out of jobs.

Here’s the backstory: Following the fatal 2008 Chatsworth train collision in Los Angeles, President Bush signed the Rail Safety Improvement Act into law. The law required freight railroads, by the end of 2020, to integrate Positive Train Control (PTC) — a nationwide system of technologies that constantly process thousands of data points to stop a train before human error-caused accidents occur. One of the benefits of PTC was that it was a win-win for consumers and the railroads, enhancing safety and allowing railroads to boost productivity by moving to one-person crews somewhere down the road.

Americans are fed up seeing corporate profits soaring even as their paychecks inch upward by comparison. Companies need stronger incentives to share their prosperity with workers – something the 2017 GOP tax package should have included.

Though President Donald Trump promised higher wages as one result of his corporate tax cuts, the biggest winners were executives and shareholders, not workers. Nevertheless, a growing number of firms are doing right by their workers, taking the high road as “triple-bottom line” concerns committed to worker welfare, environmental stewardship and responsible corporate governance. Many of these are so-called “benefit corporations,” legally chartered to pursue goals beyond maximizing profits and often “certified” as living up to their multiple missions. Congress should encourage more companies to follow this example. One way is to offer tax breaks only for high-road companies with a proven track record of good corporate citizenship, including better wages and benefits for their workers.

THE CHALLENGE: Good corporate citizenship is punished, not rewarded, in a market that puts profits first.

The pressure to return profits to shareholders – the tyranny of so-called “shareholder primacy” – is one reason companies have been disinvesting in their workers. As Brookings Institution scholars Bill Galston and Elaine Kamarck have noted, many companies are increasingly reverting to “short-termist” behavior to avoid missing the quarterly earnings targets promised to shareholders (1). For instance, one notable survey of more than 400 CFOs found that 80 percent would “decrease discretionary spending on R&D, advertising and maintenance … to meet an earnings target” and 55 percent would “delay starting a new project” even if it meant sacrificing long-term value (2).

Companies also don’t seem to be raising wages or investing in worker training. Even as many firms have been reporting some of their best profits in years during this recovery (3), companies are cutting back on benefits like health insurance and offering less on-the-job training than they once did. And despite their recent uptick, workers’ wages haven’t caught up to where they should be. According to a Brookings Institution analysis, real wages for the middle quintile of workers grew by just 3.41 percent between 1979 and 2016, and actually fell slightly for the bottom fifth.

Corporate short-termism is bad for workers, who don’t get the wages and training they deserve. It’s also bad for companies, which are shortchanging their long-term health to satisfy short-term shareholder demands. But as long as current corporate culture remains fixated on companies’ stock prices, firms will feel tremendous pressure to put short-term profits above all other priorities – and often at workers’ expense.

THE GOAL: ENCOURAGE MORE BUSINESS TO BE “TRIPLE-BOTTOM LINE” CONCERNS THAT PUT PEOPLE ON PAR WITH PROFITS

A small but growing number of firms have begun to reject the hold of “shareholder primacy” and have organized themselves as “triple-bottom line” companies committed equally to social and environmental good as well as profit. Among these is the growing number of “benefit corporations” specially organized under state law with the purpose of “creating general public benefit.” Since 2010, 34 states and the District of Columbia have passed legislation legally recognizing benefit corporations and protecting them from shareholder lawsuits for decisions that don’t maximize profits. Notably these states include Delaware, which is the leading “domicile” – or legal home – for most of America’s major companies. A significant number of benefit corporations have also won third-party certification from the nonprofit B Lab as “Certified B Corps” – essentially a Good Housekeeping seal of approval for benefit companies that have met strict standards for worker treatment, environmental stewardship and social responsibility. Among the many factors considered for certification are the share of workers who get formal training; rates of employee retention and internal promotion; the share of workers receiving tuition reimbursement or similar benefits for training and education; the extent to which “worker voice” plays a role in the company’s governance; pay equity; and company practices to reduce its environmental footprint.

According to the nonprofit B Lab, more than 2,500 businesses globally are certified B Corps. While the vast majority of these businesses are small, certified B Corps include such well-known U.S. and global brands as outdoor clothing maker Patagonia, Cabot Creamery, Ben and Jerry’s Ice Cream, and New Belgium Brewery, the makers of Fat Tire beer. A small but growing number of B Corps are now publicly traded, including cosmetics company Natura; Sundial Brands, a subsidiary of Unilever; and Silver Chef, a company that finances commercial kitchen equipment purchases for restaurateurs. These firms are proof that companies with an avowed social mission can in fact succeed in a cutthroat capital market. If more companies follow suit, the result could be a dramatic and beneficial shift away from the stranglehold of shareholder primacy and toward better corporate practices.

THE SOLUTION: OFFER TAX BREAKS TO “BENEFIT CORPORATIONS” AND HIGH-ROAD FIRMS THAT DEMONSTRATE SOCIAL RESPONSIBILITY

Many companies may feel they can’t “afford” to invest in their workers if it affects the bottom line for their shareholders. Targeted tax cuts to reward high road companies such as certified benefit corporations could, however, change the calculus for some companies and encourage them to change their behavior. These tax benefits could be structured in one of two ways:

Option One: Preferential tax rate.

As PPI has previously proposed, one option is to modify the new corporate tax rate to establish a preferential “public benefit corporation” rate for businesses that meet “high-road” requirements. Only the most deserving companies should qualify for the new 21 percent corporate tax rate; all others should pay a rate that is two to three percentage points higher.

To be entitled to these benefits, companies would meet one of two requirements: (1) that they be legally organized as “public benefit corporations” in their state and can provide good evidence of how they are fulfilling that mission; or (2) they must meet a minimum set of standards for worker treatment and investment, to be promulgated by a new standards-setting body authorized by Congress (effectively behaving like benefit corporations without the formality of legal status). To set the required standards, Congress could establish an inter-agency “workers’ council,” including representatives from labor and business, to establish guidelines for public benefit corporation rate eligibility (though enforcement would be left to the IRS). Companies would apply for a discounted tax rate in the same way that charities and nonprofits apply to the IRS for tax-exempt status, with the proviso that companies must also report annually on their performance, either in their public filings or in separate submissions to the IRS.

Option two: Benefit corporation tax credit.

A second option for structuring a high road company tax incentive is to create a tax credit for benefit corporations like the “sustainable business tax credit” offered by the city of Philadelphia. Under this benefit, first launched in 2012, Philadelphia businesses that are either certified B Corps or that can show they meet similar standards of social and environmental responsibility can qualify for a tax credit of up to $8,000 against their revenues. Up to 75 firms can apply for the credit on a first-come, first-served basis.

This structure might be especially beneficial for small and medium-sized benefit corporations structured as “pass-through” entities not subject to the corporate tax rate. As Jenn Nicholas, co-founder of the Philadelphia-based graphic design firm Pixel Parlor told Governing magazine, the credit has helped her afford higher wages and other benefits for her 10 workers. “It’s a challenge to be profitable and provide benefits to our employees,” Nicholas said. “Every tiny bit helps, and it feels like somebody is looking out for us when the general climate [for small businesses] is the opposite” (10).

While some policymakers have proposed requiring companies to treat their workers more fairly, tax incentives for high-road businesses are a better approach. Top-down mandates tend to invite resistance or evasion and will not succeed in changing the overall spirit of corporate culture in favor of shareholders over workers. Encouraging companies to reform themselves will ultimately prove the more enduring tactic. As more businesses see that they can indeed “do good and do well,” the grip of shareholder primacy will weaken, and workers will benefit.

Sources:

1) Galston, William A., and Elaine C. Kamarck. More builders and fewer traders: a growth strategy forthe American economy. Washington, DC: Brookings Institution, 2015.

2) Graham, John R., Campbell R. Harvey, and Shiva Rajgopa. The Economic Implications of Corporate Financial Reporting. N.p., 2005.

3) Bureau of Economic Analysis. “Gross Domestic Product, Third Quarter 2018 (Second Estimate); Corporate Profits, Third Quarter 2018 (Preliminary Estimate).” News release. November 28, 2018. Accessed March 28, 2019. https://www.bea.gov/news/2018/gross-domestic-product-third-quarter-2018-second-estimate-corporate-profits-third-quarter.

4) Kim, Anne. Tax Cuts for the Companies That Deserve It. Washington, DC: Progressive Policy Institute, 2018.

5) Shambaugh, Jay, Ryan Nunn, Patrick Liu, and Greg Nantz. Thirteen Facts About Wage Growith. Washington, DC: Brookings Institution, 2017.

6) B Lab. “State by State Status of Legislation.” benefitcorp.net. Accessed March 28, 2019. https://benefitcorp.net/policymakers/state-by-state-status.

7) Title 8: Corporations, Delaware Code §§ CHAPTER 1. GENERAL CORPORATION LAW; Subchapter XV. Public Benefit Corporations-361-386 (2017).

8) B Lab. “Certified B Corporation: About B Corps.” Benefitcorp.net. Accessed March 28, 2019. https://bcorporation.net/about-b-corps

9) Id.

10) Kim, Anne. “The Rise of Do-Gooder Corporations.” Governing, Jan 2019.

Is there room for a presidential candidate who stresses innovation and growth? Voters quite naturally want to see benefits from technology before they enthusiastically embrace more. As we have written in earlier reports, there are signs that digitization is starting to create new businesses and jobs in physical industries like manufacturing.

Another political argument for innovation and growth: The tech/telecom/ecommerce sector is still expanding at a rapid rate, benefiting both consumers and workers.

The tech/telecom/ecommerce sector grew by 7.3% in 2018, triple the 2.4% growth of the rest of the private sector. These figures–calculated by PPI based on the BEA’s newly-related 2018 industry GDP data— update our previous research that showed the tech/telecom/ecommerce sector far outperforming the rest of the private sector between 2007 and 2017.

Prices in the tech/telecom/ecommerce sector fell by 0.8% in 2018, compared to a 3% price increase in the rest of the private sector. That’s good news for consumers.

Perhaps more important is what we see on the labor side. Job growth in the tech/telecom/ecommerce sector exceeded job growth in the rest of the private sector, propelled by ecommerce fulfillment and delivery jobs, which added 178,000 FTE positions in 2018. If these new jobs are all assigned to the ecommerce sector, then tech/telecom/ecommerce FTE employment grew by 4% in 2018, compared to 2.1% growth in the rest of the private sector.

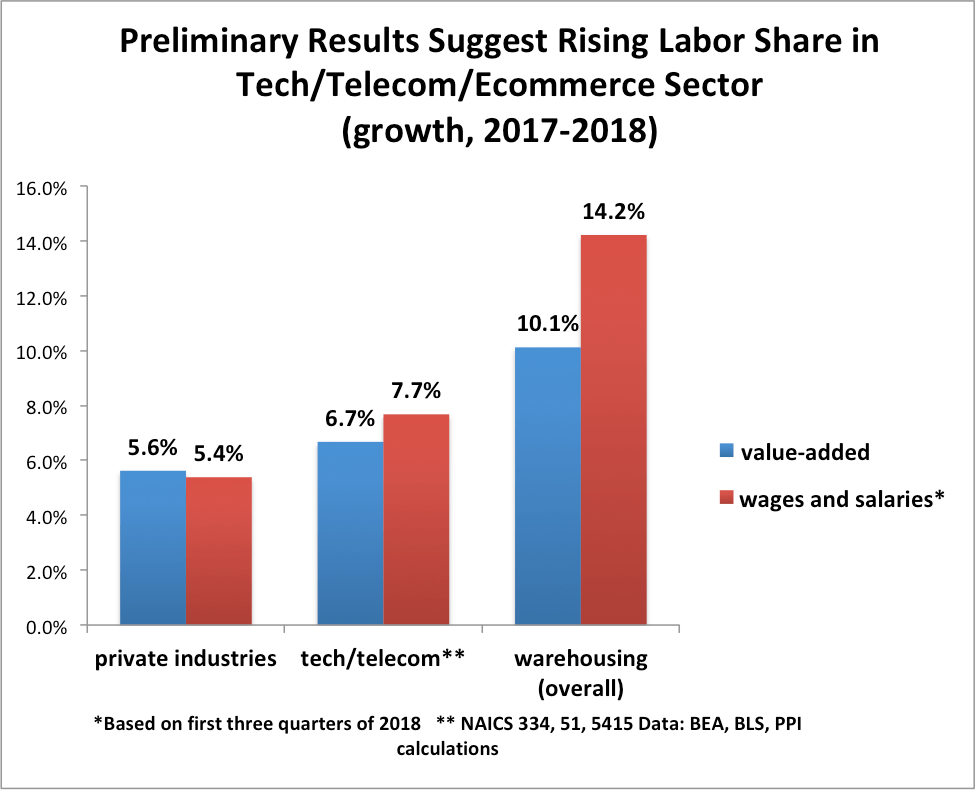

Finally, our preliminary calculations suggest that labor share rose in the tech/telecom/ecommerce sector in 2018, while falling in the broader private sector. We compared the percentage change in value-added with the percentage change in wages and salaries in the first three quarters of 2018, as reported by the BLS QCEW data. We found that value-added rose by 5.6% in the broader private sector, compared with a 5.4% increase in wages and salaries. To the extent that these trends continue in the fourth quarter and are reflected in compensation, labor share fell slight in the broader private sector.

By contrast, the available data points in favor of a rising labor share in the tech/telecom/ecommerce sector. For the purposes of this calculation we separated out tech/telecom from ecommerce, since the eventual ecommerce results will be greatly driven by the fourth quarter. For tech/telecom–computer and electronics manufacturing, software, telecom, communications, and Internet–value-added rose by 6.7% in 2018, compared to a 7.7% rise in wages and salaries. To the extent that these trends continue in the fourth quarter and are reflected in compensation, labor share rose in the tech/telecom sector in 2018.

We could not do a full analysis of labor share in ecommerce without the fourth quarter QCEW data, which is not available until June. However, we can look at warehousing, which is where ecommerce fulfillment centers are generally classified. We find that value-added in warehousing overall rose by 10.1% in 2018, while wages and salaries rose by 14.2% through the first three quarters. Assuming that these trends continue, there was a significant rise in labor share in the warehousing industry in 2018.

To emphasize: These are preliminary results, which may be revised substantially as new data comes in.

Political implications: In 2018, both consumers and workers were benefiting from the tech/telecom/ecommerce sector. Consumers were getting falling prices, and workers were getting faster job growth and a bigger share of the economic pie.

As digitization spread to other sectors, consumers and workers in those sectors will start sharing the fruits of faster growth. We suffer from too little innovation, not too much.

The global App Economy started in 2007, when Apple introduced the first iPhone. Apple’s opening of the App Store in 2008 – followed by Android Market (later renamed Google Play), Blackberry App World (later renamed Blackberry World) and other app stores – created a way for developers to write mobile applications (“apps”) that could run on smartphones anywhere. These apps became an essential part of daily life for most people – and an indispensable tool for business.

The rise of the App Economy has unleashed an abundance of “app developers.” These workers create, maintain, and support an ever-expanding range of apps. Mobile games are the most visible part of the App Economy, but certainly not the only component of it. Mobile apps include such key uses as shopping applications, home banking programs, smart automobile interfaces, healthcare apps for monitoring patients, and sophisticated apps for running manufacturing plants.

The extent of the App Economy workforce in a country reflects how quickly that country is embracing the next stage of the Information Revolution, which depends on mobile technology to digitize physical industries such as manufacturing and healthcare.

However, official economics statistics do not provide an easy way to measure the size of the App Economy. In response, PPI developed a methodology based on a systematic analysis of online job postings. In particular, we look for job postings that call for app-related skills such as knowledge of the iOS, Android, or Blackberry operating systems (though support for the Blackberry operating system is currently scheduled to cease at the end of 2019).

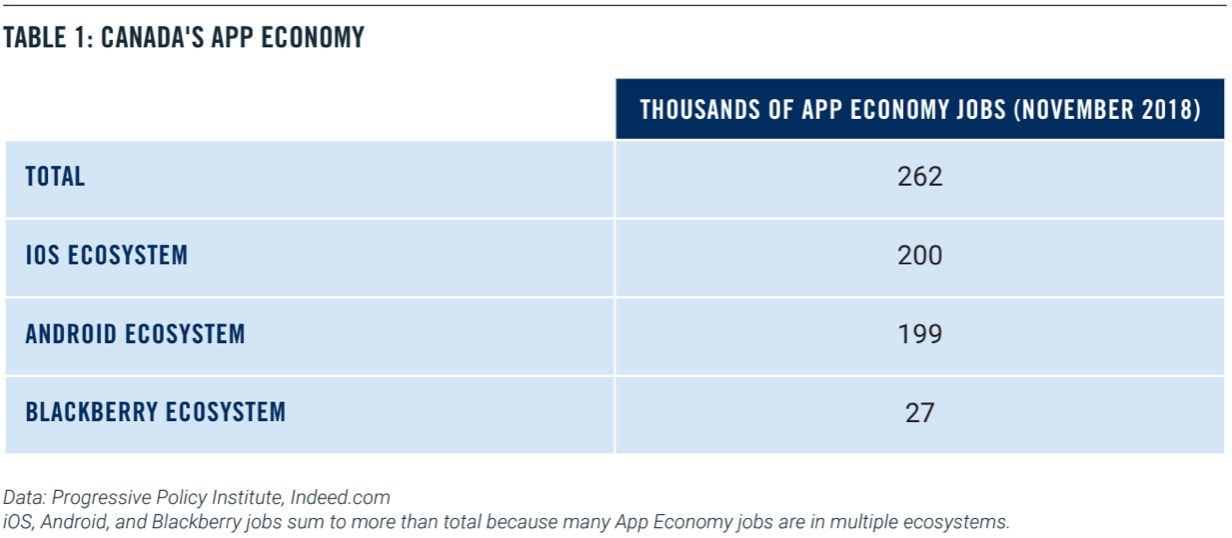

Based on this methodology, in this paper we provide an employment analysis of Canada’s App Economy. We provide an estimate of the total number of App Economy jobs; a breakdown of the jobs among iOS, Android, and Blackberry ecosystems; and an estimate of App Economy jobs by province. In particular, we estimate that Canada has 262,000 App Economy workers as of November 2018.

THE DEFINITION OF AN APP ECONOMY JOB

For this study, a worker is in the App Economy if he or she is in:

An IT-related job that uses App Economy skills – the ability to develop, maintain, or support mobile applications. We will call this a “core” App Economy job. Core App Economy jobs include app developers; software engineers whose work requires knowledge of mobile applications; security engineers who help keep mobile apps safe from being hacked; and help desk workers who support use of mobile apps.

A non-IT job (such as human resources, marketing, or sales) that supports core App Economy jobs in the same enterprise. We will call this an “indirect” App Economy job.

A job in the local economy that is supported by the income flowing to core and indirect App Economy workers. These “spillover” jobs include local retail and restaurant jobs, construction jobs, and all the other necessary services.

To estimate the number of core App Economy jobs, we use a multi-step procedure based on data from the universe of online job postings. Then the number of indirect and spillover jobs is estimated using a conservative job multiplier. The methodology is described in detail in previous research (2).

CANADA’S APP ECONOMY

Table 1 presents two pieces of information. First, we estimate Canada has 262,000 App Economy jobs as of November 2018. We also break down the total by ecosystem, finding the iOS ecosystem includes 200,000 jobs, the Android ecosystem includes 199,000 jobs, and the Blackberry ecosystem includes 27,000 jobs. The three sum to more than the total because many App Economy jobs belong to multiple ecosystems.

Using a different methodology, the Information and Communications Technology Council (ICTC) estimated total App Economy and related employment in Canada at 51,700 in its 2012 report, “Employment, Investment, and Revenue in the Canadian App Economy” (3). We infer from this that Canadian App Economy jobs roughly quintupled from 2012 to today. That’s consistent with what we have seen for the United States over the same time period.

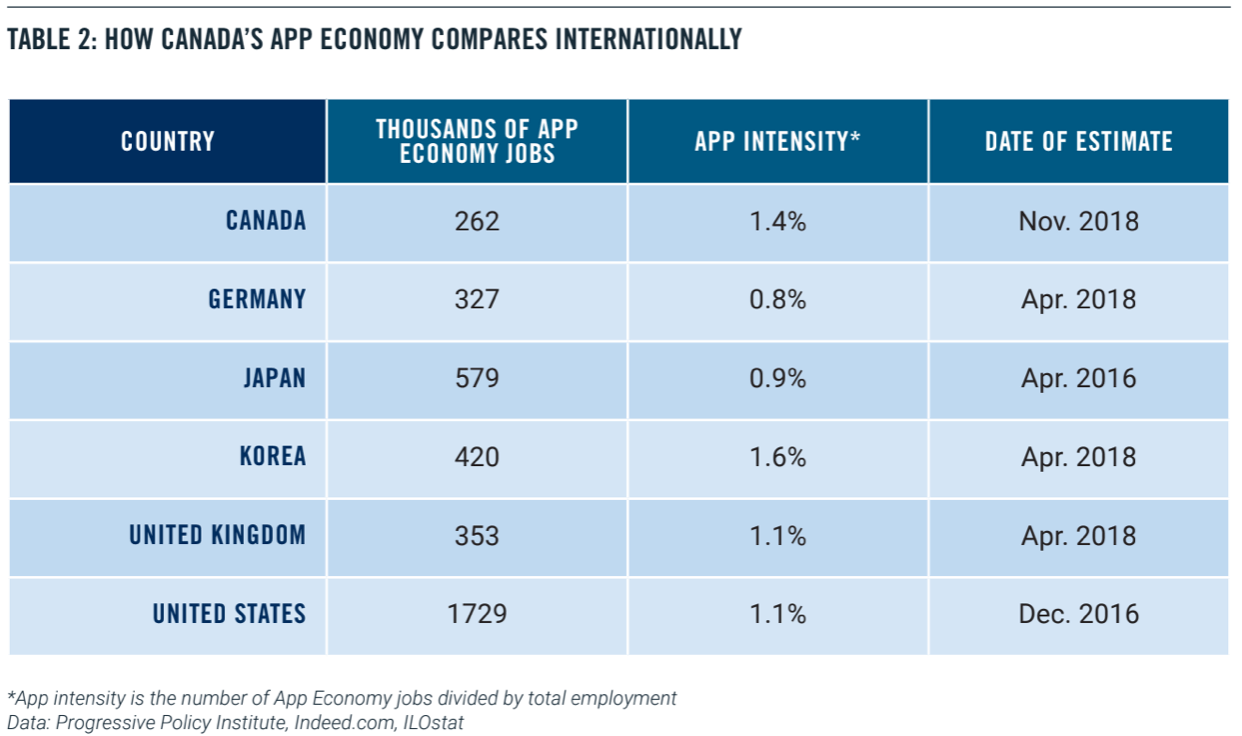

Now we compare Canada to some of its industrialized peers. In absolute numbers, Canada’s App Economy is relatively small. But, when we adjust for country size, Canada is doing very well. App intensity represents the number of App Economy jobs divided by total employment, where the latter figure is drawn from the International Labor Organization for standardization.

Canada’s app intensity of 1.4 percent ranks ahead of the United States, the United Kingdom, Germany, and Japan – and only slightly behind Korea.

Canada’s relative success can be attributed in part to its prioritization of digital connectivity and skills. Digital Canada 150 aimed to create jobs and economic growth by, among other things, connecting rural areas to high-speed Internet and investing in Canadian businesses and consumers through technology integration and skills development (4). Accomplishments include extending high-speed Internet to an additional 356,000 households, completing multiple spectrum auctions to improve wireless service, investing an additional $200 million to help entrepreneurs learn about IT technologies, and supporting up to 3,000 internships in high-demand fields. These types of policies help increase access to and employment in the App Economy.

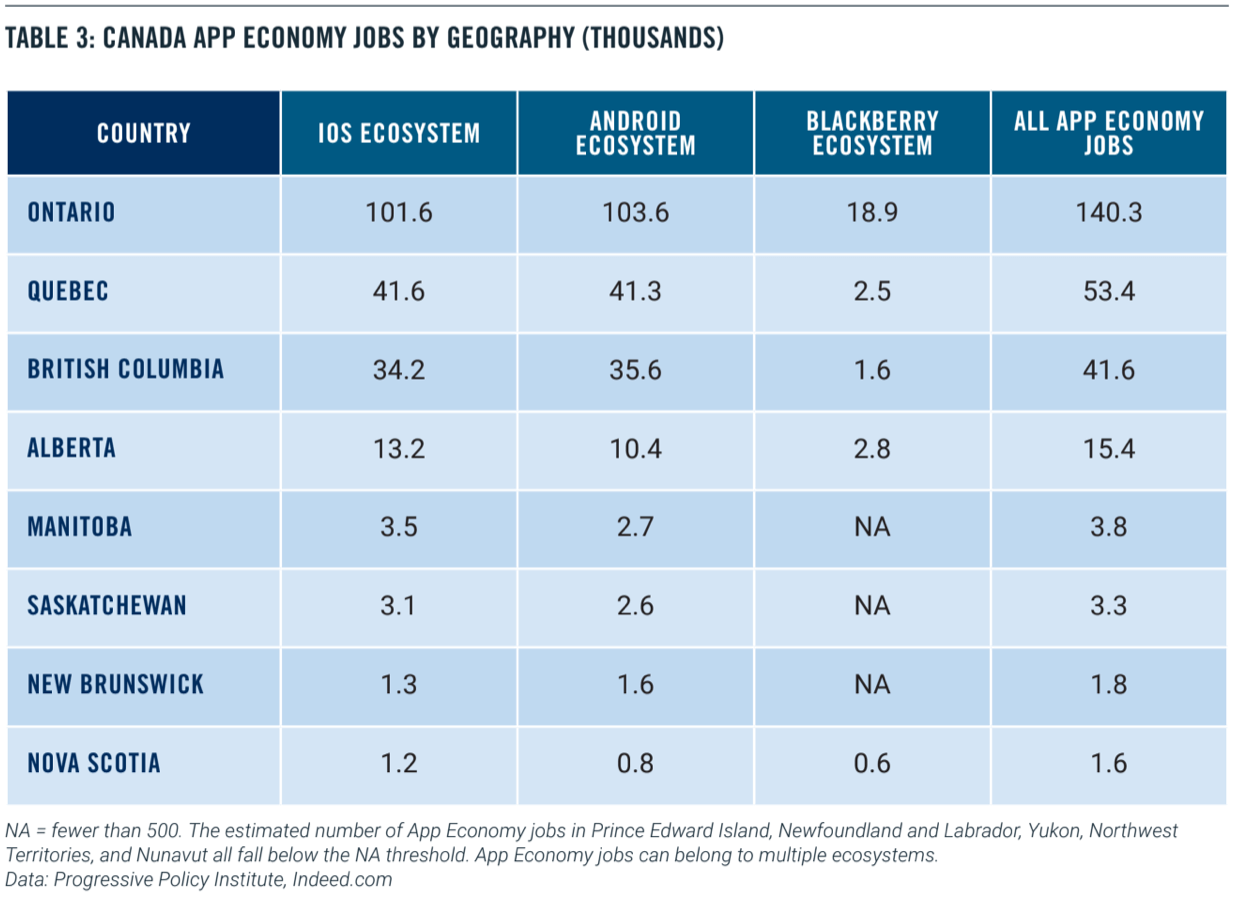

GEOGRAPHIC DISTRIBUTION

Our methodology also allows us to look at the geographic distribution of App Economy jobs by province – breaking out the different ecosystems. If we estimate fewer than 500 jobs in a region, we don’t report the number. Not surprisingly, Ontario leads in App Economy jobs, followed by Quebec and British Columbia. Also not surprisingly, the Blackberry ecosystem jobs are concentrated in the company’s home province of Ontario.

EXAMPLES OF APP ECONOMY JOBS

The Canadian App Economy is vibrant across a wide range of industries and geographies. As of October 2018, digital studio Adfab was searching for a front-end developer in Montréal with App Economy skills. Mobile device solutions firm Asset Science was seeking a mobile application developer with iOS and Android experience. Mango Software Inc. was looking for an Android developer in Montréal. IT firm CORE Resources was hiring a senior software engineer with Android experience in Mississauga.

Looking at Ontario in particular, as of October 2018, mapping software company Avenza Systems Inc. was searching for a full stack developer with experience in iOS and Android app development in Toronto. Life insurance company Manulife was seeking a senior Android developer in Kitchener. Digital billing company Sensibill was looking for a software developer with Android and iOS experience in Toronto. Household labor marketplace AskforTask was hiring a senior Android developer in Toronto.

As of October 2018, commercial contractor Flynn Group of Companies was hiring a mobile iOS developer in Mississauga, Ontario. Airline software firm NAVBLUE was seeking a software developer in Waterloo, Ontario. Fintech company Borrowell was looking for a React Native developer with experience building iOS and Android apps in Toronto. Consulting firm Neel-Tech Inc. was searching for an iOS developer in Mississauga.

In Quebec, as of October 2018, drone company Microdrones was hiring a senior Android developer in Vaudreuil-Dorion. Event app company Greencopper was seeking a mobile developer with iOS and Android experience in Montréal. Mobile payment company Mobeewave was searching for a mobile Android developer in Montréal. IT firm SolidByte was looking for a programmer with knowledge of iOS and Android programming in Montréal.

British Columbia has plenty of App Economy activity as well. As of October 2018, payment technology firm Alpha Pay was looking for an iOS or Android mobile developer in Richmond, British Columbia. Financial cloud company Global Relay was hiring a senior Android developer in Vancouver. Shopping app company StylePixi was seeking an iOS developer in Vancouver. Digital development firm Atimi was searching for a senior native mobile developer with iOS experience in Vancouver.

Considering Alberta, as of October 2018, GPS company Trimble Inc. was hiring a software engineer with iOS and Android experience in Calgary. Digital production firm Division [1] Media Corp was looking for a mobile app developer in Edmonton. The University of Alberta was searching for a lead software engineer with experience in Android and iOS in Edmonton. Aviation company Air Trail was seeking an intermediate iOS developer in Edmonton.

And the App Economy has spread even further. In Winnipeg, Manitoba, Pollard Banknote Limited – a leading supplier of instant lottery tickets – was hiring a senior applications developer with experience in mobile app development. In Saskatoon, Saskatchewan, Affinity Credit Union was searching for an iOS developer. In Fredericton, New Brunswick, Welltrack – a company that provides a suite of interactive self-help tools – was looking for a mobile developer. And in Bedford, Nova Scotia, IBM’s Client Innovation Centre was hiring a mobile application developer for iOS and Android.

Canadians are developing apps for the rest of the world, not only Canada. One well-known Canadian app that has spread globally is the messaging mobile app Kik, which was created in 2009 by University of Waterloo students and has 300 million users today around the world. Another example: Public transit app Transit was developed in Montréal in 2012. Today, Transit provides real-time crowdsourced data to users in 175 cities across the United States, Canada, and Europe. And well-regarded password manager 1Password, which was developed by Toronto-based AgileBits, has a global user base.

POLICY DEVELOPMENTS

As shown in this report, the Canadian App Economy has fared better in terms of scale than some of its industrial peers. Its growth since the introduction of the iPhone over a decade ago (and app intensity today) demonstrate the country is embracing the digital age and is well positioned to be a global leader. A few reforms could catalyze the next round of growth.

Unlike in the United States, where a patchwork of laws govern privacy, one law applies at the federal level in Canada – the Personal Information Protection and Electronic Documents Act (PIPEDA). But, while PIPEDA covers all health data, personal information, and employee information in one comprehensive structure, if a province has passed legislation deemed “substantially similar,” the province’s law prevails. For example, Alberta, British Columbia, and Quebec have laws in place that have been deemed substantially similar, thus serving as the prevailing law. But, as PPI has previously recognized, cross-border data flows means multiple regulatory regimes can be burdensome, unclear, and even contradictory for app developers – slowing the digitization of physical industries and economic growth.

The Canadian government began a review of its Broadcasting and Telecommunications Acts in 2018, with the intent of modernizing its legislative framework after the invention of new technology – particularly streaming services otherwise known as “over-the-top” (OTT) providers (5). OTT providers are those companies delivering video streaming, voice calls, or messaging via the Internet, without requiring users to subscribe to a traditional cable, satellite, or phone service. Policymakers should be cautious of taking a heavy-handed regulatory approach that would slow growth and, instead, should opt for a balanced approach that both promotes competition without jeopardizing the cost savings this technology has afforded consumers.

Lastly, according to the Information and Communications Technology Council’s latest ICT Labor Outlook, Canada will need an additional 216,000 ICT professionals by 2021 (6). Programs designed to incorporate and lower the cost of ICT skills development could help close this shortage. To that end, in their recent report on innovation and competitiveness, Canada’s Economic Strategy Tables recommend expanding on existing work-integrated learning opportunities, adopting portable competency-based credentials, and consolidating and streamlining skills and talent programming (7).

CONCLUSION

Canada has a vibrant App Economy that spans the iOS, Android, and Blackberry ecosystems. Compared to most of its industrialized peers, Canada’s app intensity is high, and represents a wide diversity of locations and jobs. Policy reforms such as streamlining privacy laws, taking a balanced regulatory approach when it comes to OTT providers, and closing the skills gap could help catalyze future growth.

1) PPI has issued App Economy reports on the United States, Japan, Vietnam, Indonesia, Korea, Thailand, Mexico, Brazil, Colombia, Argentina, Chile, and most of the countries of the European Union, including the United Kingdom, Germany, and France. Most notably, we have not yet issued reports on China and India.

2) A description of the methodology can be found in the appendix to Michael Mandel and Elliott Long, “The App Economy in Europe: Leading Countries and Cities, 2017,” Progressive Policy Institute, October 2017. https://www.progressivepolicy.org/wp-content/uploads/2017/10/PPI_EuropeAppEconomy_17.pdf

3) “Employment, Investment, and Revenue in the Canadian App Economy,” October 2012, Information and Communications Technology Council. https://www.ictc-ctic.ca/wp-content/uploads/2012/10/ICTC_AppsEconomy_Oct_2012.pdf

4) “Digital Canada 150,” Industry Canada. https://www.ic.gc.ca/eic/site/028.nsf/eng/home#item5

5) Canadian Heritage, “Government of Canada launches review of Telecommunications and Broadcasting Acts,” June 5, 2018. https://www.newswire.ca/news-releases/government-of-canada-launches-review-of-telecommunications-and-broadcasting-acts-684595661.html

6) “The Next Talent Wave: Navigating the Digital Shift – Outlook 2021,” Information and Communications Technology Council. https://www.ictc-ctic.ca/wp-content/uploads/2017/07/ICTC_Outlook-2021-ENG-Final.pdf

7) “The Innovation and Competitiveness Imperative Seizing Opportunities for Growth,” Canada’s Economic Strategy Tables. https://www.ic.gc.ca/eic/site/098.nsf/vwapj/ISEDC_SeizingOpportunites.pdf/$file/ISEDC_SeizingOpportunites.pdf