The $3.5 trillion budget blueprint unveiled earlier this week by Senate Democrats would fund many policies from President Joe Biden’s American Jobs and Families Plans not covered by the $579 billion Bipartisan Infrastructure Framework. But among many worthwhile public investments is a new proposal that should give lawmakers pause: a costly expansion of Medicare paid for entirely by young Americans. Although lawmakers should be open to thoughtful improvements to Medicare, any changes must be financed in a way that is fair to Americans of all ages.

There are two possible changes to Medicare that Sen. Bernie Sanders, I-Vt., the chairman of the Senate Budget Committee, wants to include in the next major spending bill. The first proposal is to offer vision, dental, and hearing services not currently covered by Medicare at no additional cost to beneficiaries. The second proposal is to give Americans ages 60-64 the option to enroll in Medicare with the same premiums and benefits currently available to those over age 65 (which are heavily subsidized by income and payroll taxes paid by younger workers).

The problem with these proposals is that Medicare is already struggling to pay for the current suite of benefits it offers. Medicare Part A, which offers hospital insurance that is supposed to be fully funded by payroll taxes, will face a 10% budget shortfall five years from now. The amount of general revenue needed to subsidize Medicare Parts B and D, which cover physician services and prescription drug benefits, is projected to nearly double as a percent of gross domestic product over the next 20 years. These costs will impose a significant burden on young Americans, either by crowding out investments in their future or requiring them to pay higher taxes than current retirees did when they were in the workforce.

Giving today’s seniors, who have collectively enjoyed greater gains in income and wealth than younger Americans, a suite of new benefits they didn’t finance over their working lives or in retirement would only compound the intergenerational inequity built into current policy. That’s especially true if the Senate blueprint foregoes some investments in clean energy or child welfare, such as a permanent expansion of the Child Tax Credit, to make room for this costly expansion of Medicare.

There are better alternatives. Americans ages 60-64 could be allowed to buy into Medicare at a premium that covers the full cost of their coverage rather than the heavily subsidized one currently paid by people aged 65 and over. This option would still be cheaper for most beneficiaries than private insurance because Medicare is able to negotiate lower prices for services than private insurers. Any new vision, dental, or hearing benefits should have a significant share of the cost covered by income-based premiums and co-pays, as is currently the case for Parts B and D. A broad-based consumption tax that is paid by all consumers regardless of age could also help finance benefits in a way that doesn’t place the burden on anyone generation. Lawmakers should also consider pairing or preceding any benefit expansion with measures to close the existing financial shortfall in Medicare, such as the bipartisan TRUST Act.

For too long, Washington has allowed the growth of retirement programs to crowd out critical public investments in infrastructure, education, and scientific research. The new budget agreement is a once-in-a-generation opportunity to right this intergenerational wrong. It would be shameful for lawmakers to choose affluent retirees over working families yet again. Any expansion of Medicare should require some contribution by those who would benefit, or it should be dropped from the budget agreement altogether.

As lawmakers return to Washington this week, one of their top priorities will be crafting legislation based on the bipartisan infrastructure framework agreed to by President Biden and Senate negotiators last month. Although that agreement set top-line numbers for broad categories of spending, the details for how the money would be spent still need to be fleshed out. Congress should maximize the impact of this transformative investment by including provisions to reduce construction costs and direct funds towards the most beneficial projects.

The costs of building infrastructure in the United States are significantly higher than they are in other countries. New York is home to some of the world’s most expensive mass transit projects, sometimes costing several billion dollars per mile, while costs in other American cities also dwarf those of comparable projects internationally. Roads are no better: A recent tunnel in Seattle cost more than three times as much as a similar project in Paris and seven times as much as one in Madrid. If policymakers can bring the cost of each project down closer to international norms, they can build more infrastructure with the same pool of funds.

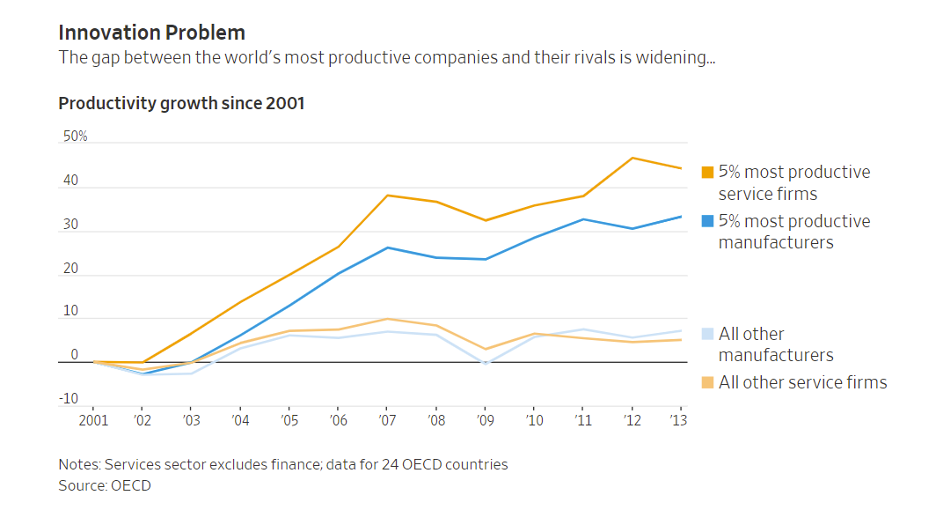

For the firms that adopt them, artificial intelligence (AI) systems can offer revolutionary new products, increase productivity, raise wages, and expand consumer convenience.[1] But there are open questions about how well the ecosystem of small and medium-sized enterprises (SMEs) across the United States is prepared to adopt these new technologies. While AI systems offer some hope of narrowing the recent productivity gap between small and large firms, that can only happen if the technologies actually diffuse throughout the economy.

While some large firms in the U.S. are on the cutting edge of global AI adoption, the challenge for policymakers now is to help these technologies diffuse across the rest of the economy. To realize the full productivity potential of the U.S., AI tools need to be available to 89% of U.S. firms that have fewer than 20 employees and the 98% that have fewer than 100.[2] An AI-enabled productivity boost would be particularly timely as SMEs are recovering from the effects of the ongoing COVID-19 crisis.

The report discusses the promise for AI systems to increase productivity among U.S. SMEs, the current barriers to AI uptake, and policy tools that may be useful in managing the risks of AI while maximizing the benefits. In short: there is a wide range of policy levers that the U.S. can use to proactively provide the underlying digital and data infrastructure that will make it easier for SMEs to take the leap in adopting AI tools. Much of this infrastructure operates as a type of public good that will likely be underprovided by the market without public support.

Benefits of AI adoption:

The central case for AI adoption is that human cognition is limited in a variety of ways, most notably in time and processing power. Software tools can improve decision-making by increasing the speed and consistency with which decisions can be made, while also allowing more decisions to be planned out ahead of time in the event of various contingencies. Under this broad framework, we can think about “AI” as being a broad suite of technologies that are designed to automate or augment aspects of human decision-making.

While many of AI’s most eye-catching use cases will likely remain the preserve of large platforms, the technology also holds tremendous promise for SMEs. The adoption of third-party AI systems will notably enable SMEs to streamline mundane (but often costly) tasks such as marketing, customer relationship management, pre- and post-sales discussions with consumers, and Search Engine Optimization (SEO). These systems can provide a lifeline for SMEs who are overwhelmed by the many challenges of running a business, and they can expand the number of businesses that are eligible for certain financial supports. For example, AI tools can be used to improve the accuracy of credit risk underwriting models and using alternative data sources and a streamlined process, they can make it easier for SMEs to take out loans they otherwise might not qualify for under traditional methods. Along similar lines, research shows that AI-driven robotics have (and will continue) to boost the productivity of SMEs in the manufacturing industry.

Importantly, this upcoming wave of AI technology can help SMEs catch up with larger, international firms because it can democratize the benefits of large information technology (IT) investments that superstar firms have been seeing over the last decade.

The economist James Bessen has argued that the top 5% of firms in many industries have been increasingly pulling away from the rest of the field because they’ve made large investments in proprietary IT systems. Their smaller rivals struggle to develop their own systems because they lack the necessary scale to hire a large stable of in-house technical talent. Amazon, for example, has a team of 10,000 employees working to improve their Alexa and Echo systems.

While AI tools can’t fully reverse this trend, they can help shrink the gap when embedded into Software as a Service (SaaS) platforms that smaller firms can make use of without the same level of investment. Essentially, through general-purpose AI tools, SMEs can have access to a host of productivity enhancements that these proprietary IT systems offer, but at a price point that is economical for SMEs. By shrinking this productivity gap, smaller firms can begin to compete in earnest while differentiating from large firms through improved customer service and greater product diversity. This will give a large leg up to SMEs who adopt these AI systems and help them better compete with large global incumbent firms.

Consider a firm like Keelvar Systems, which uses advanced sourcing automation to help businesses rapidly shift supply chains around the globe in the event of disruptions or delays. Essentially, it replaces or augments the work that a large supply chain and sourcing office would do within a firm. By using their service, or others like it, SMEs have the ability to benefit from similar levels of sophistication in their supply chain management without having employees spend hundreds of hours on tedious tasks or maintaining expensive proprietary IT systems.

There are firms like Legal Robot that have created a series of tools to help small businesses access legal services that would otherwise require a small army of in-house lawyers. With their service, SMEs can use smart contract templates based on their industry, receive instant contract analysis to make sure they are receiving fair terms and can automate certain aspects of compliance with laws like the GDPR.

Likewise, companies like Bold360 have helped SMEs improve their customer service experiences by offering a variety of AI-powered-chatbots and tools. Many basic customer concerns about products or delivery can be handled by these basic chatbots, freeing up human customer representatives to focus their time on the hard or advanced cases. Again, the pattern here is there is a service that large, multinational companies have been investing billions of dollars to create proprietary versions of, and now the customizability of AI is helping this service become more accessible to SMEs.

What are the barriers to AI adoption for SMEs in the U.S. and what can policymakers do to help create a welcoming environment?

Data investment as a public good

Depending on the context, data can often have the same traits as other public goods. First, it is non-rival—the marginal cost of producing a new copy of a piece of data is zero. Stated differently, multiple individuals can use the same dataset at almost no additional cost. The second important trait is that data is hard to exclude. Consider this report. Once it has been posted online, it is difficult to prevent people from accessing and sharing it as they see fit. This is one of the reasons why copyright infringement is so hard to stamp out.

Oversimplifying, these two features can lead to two opposite problems. On the one hand, economic agents might underinvest in public goods, absent government-created appropriability mechanisms (such as patent and copyright protection). Conversely, public goods tend to be underutilized (at least from a static point of view). Any price that enables economic agents to recoup their investments in a public good will be above the good’s “socially optimal” marginal cost of zero. Public good policies thus involve a tradeoff between incentives to create and incentives to disseminate. For example, patents give inventors the exclusive right to make, use and sell their invention; but inventors must disclose their inventions, and these fall into the public domain after twenty years.

What does this mean for data and artificial intelligence? If policymakers think that data is an essential input for cutting-edge AI, then they should question whether obstacles currently prevent firms from investing in data generation or disseminating their data.

While policies in this space involve significant tradeoffs, some offer much higher returns to social welfare. For instance, to the extent policymakers believe existing datasets are being underutilized, purchasing private entities’ data (through voluntary exchanges) and placing it in public data trusts would be a better policy than imposing data sharing obligations (which could undermine firms incentive to produce data in the first place). This is akin to the idea of government patent buyouts.

Of particular interest for policymakers, however, is the fact that some SMEs are sitting on top of data flows that are not being fully utilized because it is expensive to make data usable and these datasets may not be very valuable in isolation. As an example, industry-level manufacturing data might be quite valuable to all firms in a sector, but the dataflows from one SME are much less valuable. The U.S. could align incentives by providing investment funds to quantify various aspects of business flows and then submit them to public data trusts, which could be accessible for use by all firms in the industry. This would essentially be treating valuable dataflows as a type of public infrastructure that needs government investment to be fully realized.

This kind of public investment can happen not only through incentives for private firms but through the public sector as well. Governments at all levels (state, local, and national) have valuable dataflows regarding infrastructure development, the organization of public transportation, and general macro-level economic data that can be turned into open datasets for public and commercial use. Particularly on the national level, the U.S. should consider investment in IT infrastructure that can coordinate the submission of open datasets on the state and local level.

Indeed, if key scientific or commercial datasets do not yet exist, the public sector may be best positioned to create them in the first place as a type of digital infrastructure provision. One notable structure that may help in this regard is the idea of a Focused Research Organization, which would provide a team of researchers with an ambitious budget and a nimble organizational structure with the specific goal of creating new public datasets or toolkits over a set time period.

Provide regulatory certainty

For SMEs deciding whether to invest in adopting AI tools, regulatory and compliance costs can be a significant deterrent. Policymakers should recognize that regulation is often more burdensome for small firms that generally have less ability to shoulder compliance costs. Especially in industries with low marginal costs, such as the tech sector, larger firms can spread fixed compliance costs across more consumers, giving them a competitive edge over smaller rivals. Regulation can thus act as a powerful barrier to entry. For instance, a study found that the European experiment with GDPR led to a 17% increase in industry concentration among technology vendors that provide support services to websites.

This is not to say that additional regulation is, or is not, necessary in the first place. Indeed, there are a host of malicious or unintentional harms that can occur from improperly calibrated AI systems. Regulation can be a powerful tool to prevent these harms and, when well-balanced, can promote greater trust in the overall ecosystem. But potential regulation should follow sound policymaking principles that reduce the regulatory burden imposed on firms, notably by making regulation easy to understand, risk based, and low-cost to comply with.

In the U.S. there is to date no overriding national AI regulation. Instead, each sectoral regulator (i.e. Federal Aviation Administration, Security and Exchange Commission, Federal Trade Commission, etc.) has been steadily increasing their oversight over the use of algorithms and software in their specific area. This is likely an appropriate approach, as the kinds of risks and tradeoffs at play are going to be very different in healthcare or financial decision-making when compared to consumer applications. As this approach develops, it would be prudent to develop a risk-based framework that allows for more scrutiny of algorithmic decision-making in sensitive areas while giving SMEs confidence to invest in low-risk areas with the knowledge they will not later take on large compliance costs.

However, regulation over data protection has been far more segmented and piecemeal. And the state-by-state patchwork of rules that has developed can be a significant deterrent for SMEs when considering whether to invest in the use of certain AI tools. Policymakers should consider an overriding national privacy law that would be able to set standard rules of the road over the protection of data in all 50 states so that U.S. SMEs can invest with confidence.

Finally, U.S. policymakers should consider aggregating all this information through the creation of a dedicated AI regulatory website that provides a toolkit of resources for SMEs about the benefits of AI adoption for their business, the potential obligations and roadblocks that they need to be aware of, and best practices for cybersecurity hygiene and data sharing.

Expand the AI talent pool

A lack of skilled talent is one of the biggest barriers to AI adoption as the technical skills required to build or adapt AI models are in short supply. In the U.S., especially, smaller companies struggle to compete with the high salaries paid out by large tech firms for top-end machine learning engineers and data scientists.

In broad strokes, this skills shortage can be alleviated in two ways: through upskilling the domestic population and by improving immigration pathways for global talent.

To upskill the domestic population, one relatively simple lever would be to pay some portion of the costs of individuals and businesses who wish to upskill. In the U.S., a portion of a worker’s retraining costs may be written off as a business expense so long as the worker is having their productivity improved in a role they currently occupy. But this expense is not tax deductible if the proposed training would enable them to take on a new role or trade.

For example, if a small manufacturing firm has technically competent IT staff who wish to attend a specialized training course on using machine vision systems in a warehouse environment, this expense would not currently be deductible as it would enable them to take on a new role within the company. This inadvertently creates an incentive to spend more on capital productivity investments than labor productivity investments. Addressing this imbalance would incentivize more firms to invest in worker retraining and help speed the creation of an AI workforce in the U.S.

Secondly, the U.S. needs to urgently address the shortcomings in the U.S. immigration system which make it more difficult for startups to compete with large incumbents on the basis of talent. Approximately 79% of the graduate students in computer science (and related subfields) studying in the U.S. are international students, which means a large majority of potential AI workers U.S. firms may look to recruit must operate through the immigration system. The cost, complexity, and length of this process inevitably favors large, incumbent firms who can afford to navigate the regulatory maze of procuring an H-1B or related work visa.

A recent NBER paper showed in detail the myriad ways in which access to international talent is important for startup success. Utilizing the random nature of the H-1B lottery system, the paper compared startups that randomly received a higher percentage of their visa applications approved to those who did not. The random nature of the H-1B lottery makes an ideal policy experiment because it allows for a clean test in which other potentially confounding variables are controlled for. The study found that a one standard deviation increase in the likelihood of successfully sponsoring an H-1B visa correlated with a 10% increase in the likelihood of receiving external funding, a 20% increase in the likelihood of a successful exit, a 23% increase in successful Initial Public Offering, and a 4.8% increase in the number of patents filed by the startup.

Policymakers could begin to counter this effect by waiving immigration fees for firms of a certain size and by streamlining the application process.

Further, policymakers should look to create a statutory startup visa so that international entrepreneurs have a viable pathway into the U.S. to launch firms of their own. According to research by Michael Roacha and John Skrentny, international STEM PhD students are just as likely to report wanting to work for or launch their own firm as native-born students, but the difficulty of our immigration system pushes them towards working at large incumbent firms.

Using these two levers of upskilling and immigration reform, the U.S. should increase the supply of AI talent available to SMEs or to launch SMEs themselves and thereby spur the adoption of AI adoption.

Conclusion

Artificial intelligence systems hold great potential to streamline the costs of doing business in a modern economy, particularly for SMEs. The last 20 years of the information technology revolution have helped large, established firms reach the cutting edge of productivity while smaller firms have been left behind. But general-purpose AI tools now provide an opportunity for SMEs to take advantage of many of these IT advancements at a cost and a scale that is feasible for them. Policymakers should attempt to proactively build out the digital infrastructure that will make it easier for SMEs to take the leap in adapting AI tools.

Summary of policy recommendations:

Data investment as a public good:

Where appropriate, align incentives for the private sector to contribute industry-level SME data to public and private data trusts that could be used by everyone.

Invest in making more government datasets open to the public.

Fund Focused Research Organizations or similar groups with the explicit goal of creating new scientific and commercial public datasets.

Provide regulatory certainty:

Clarify existing regulations and the obligations that SMEs must meet when utilizing a new AI tool.

Encourage the development of a risk-based framework that allows for more stringent regulation of sensitive applications while giving certainty to SMEs on investment in low-risk applications.

Pass an overriding national privacy law so that SMEs aren’t deterred from investing by a patchwork of differing state-by-state laws.

Consider the creation of a new SME regulatory website that provides informational resources to SMEs about the benefits of AI adoption for their business and the potential roadblocks that they need to be aware of.

Expand the AI talent pool

Encourage upskilling of the U.S. population by making worker retraining deductible as a business expense.

Reevaluate U.S. immigration pathways to make them more attractive for international technical talent.

Streamline the immigration application process and waive fees for firms below a certain size to make it easier for SMEs to compete for technical talent.

[1] This report is an adaptation of an earlier paper coauthored with Dirk Auer titled “Encouraging AI Adoption in the EU”.

[2] Annual Survey of Entrepreneurs – Characteristics of Businesses: 2016 Tables, United States Census Bureau

It’s rare when a single acquisition can offer insight into two different important questions in innovation. But the proposed purchase of cancer-diagnostic developer Grail — a startup with tremendous potential — by gene-sequencing leader Illumina is just that pivotal. First, is it pro-innovation for European antitrust regulators to have the power to block a deal involving two American biotech companies that do no substantial business in Europe? We argue that such “regulatory imperialism” by the EU has the potential to slow down biotech innovation, especially given the region’s generally lagging performance in biotech (BioNTech notwithstanding).

Second, under what conditions is vertical integration a socially beneficial strategy for accelerating innovation? Successful innovation in the biosciences often combines risk-taking by small companies with the development and regulatory resources of larger companies. We conclude that excessive antitrust focus on blocking vertical integration in the biosciences could impede the development of important new products and treatments.

These issues go far beyond Illumina and Grail. But it’s helpful to have the facts about this particular case. Grail has spent the past five years developing a diagnostic capable of screening for 50 different cancers at once — a test set to launch this year — while Illumina makes the hardware that performs those tests. Illumina offered to buy Grail, with the idea of integrating Grail’s technology with its own, to simplify the process of using gene sequencing for clinical diagnostics on a massive scale. If successful, this would dramatically reduce the cost of performing cancer screenings.

The Federal Trade Commission (FTC) intervened to block the acquisition, worried that Illumina would block potential competitors of Grail from using its gene sequencers. Illumina promised to supply these competitors with gene sequencing equipment and supplies without price increases. The FTC, through a complicated series of maneuvers that are not relevant to this paper, temporarily pulled back from its intervention to allow the European Commission to take the first swing at blocking the acquisition. The EU antitrust regulators are planning to rule by July 27 on whether to clear the merger.

And here’s where we come to the first issue: Should the EU antitrust regulators be considering a biotech deal that by the ordinary rules would not come under their jurisdiction? As the Wall Street Journal notes, “Since the merger doesn’t qualify for antitrust review under the bylaws of the European Union or any member states, the Commission asked countries to invoke Article 22 of the EU’s Merger Regulations. This rarely used provision allows countries to refer transactions to the Commission when their governments lack jurisdiction.”

This fits the general EU strategy of “regulatory imperialism.” Rather than focusing on innovation, the EU has tried to position itself as the global leader in regulation in a variety of areas, from artificial intelligence to chemicals to GMOs to data privacy. The European approach to regulation has been framed by the precautionary principle, which puts less weight on the benefits of innovation and more on the potential harms.

That risk-avoiding approach is one important reason why Europe has consistently lagged in biotech. European biotech is not nonexistent — after all, Pfizer partnered with a German biotech firm, BioNTech, to develop a very successful COVID-19 vaccine. Nevertheless, data from the Organisation for Economic Co-operation and Development shows that business spending on biotech research and development (R&D) in the EU comes to roughly one-third that of the U.S.

Tacitly accepting European jurisdiction over American biotech deals has the potential to slow down commercialization of important technologies. According to the New York Times, Europe has been “a world leader in technology regulation, including privacy and antitrust.” In a recent speech, Emmanuel Macron said that during its turn at the helm of the EU presidency, France would “try to deliver a maximum of regulation and progress.” When the EU sets the global standard on regulation and companies choose to comply with it everywhere (even where standards are lower), that’s known as the “Brussels effect.”

First, on privacy, the General Data Protection Regulation (GDPR) has become a de facto floor on policy for many large multinational companies. The problem for companies — especially in biotech and software — is that there are very high fixed costs to product development (and low marginal costs for distribution), and reworking a product for a different regulatory environment is often more trouble than it’s worth. That leads to a race to the top (or bottom, depending on your perspective) in terms of regulation.

In its first few years in effect, GDPR’s flaws have become manifest and EU policymakers are starting to consider reforms to the law. According to a recent joint report from three academy networks, “GDPR rules have stalled or derailed at least 40 cancer studies funded by the US National Institutes of Health (NIH).” The authors go on to note that “5,000 international health projects were affected by GDPR requirements in 2019 alone.” This flawed model for privacy regulation has unfortunately been exported around the globe.

Second, mergers between globally competitive firms with a presence in multiple jurisdictions have to get clearance from multiple antitrust enforcement agencies. If a single agency in a large market objects to the merger, the deal might fall apart completely. For example, a merger between U.S.-based Honeywell and U.S.-based General Electric collapsed after the EU competition enforcement agency decided to block the deal out of concern it would create a monopoly in jet engines. Of course, the EU’s investigation of the Illumina-Grail merger takes that one step further, given the fact that Grail doesn’t conduct any business in the EU, and Illumina’s business there isn’t substantial, with revenues below the usual threshold for antitrust scrutiny for both the European Commission and individual countries.

The next important question raised by the Illumina-Grail purchase is the role of vertical integration. We start with the simple observation that innovating in complex systems is both risky and expensive. That’s true in frontier industries such as electric vehicles and e-commerce, and it’s especially true in the biosciences, with the high hurdle set by the need for safety and efficacy.

The cost to bring a drug to market is a huge barrier for startups to remain independent. A 2020 paper in JAMA examining 63 of the 355 new therapeutic drugs and biologic agents approved by the U.S. Food and Drug Administration between 2009 and 2018 found that the median capitalized research and development cost per medicine was $985 million. Other studies using private data have found even higher figures. A 2019 study published in the Journal of Health Economics estimated the average cost to reach approval at $2.6 billion (post-approval R&D costs nudge the total up to $2.9 billion).

Should these complex systems be built by one company, which is better able to integrate all the pieces of the puzzle? (Tesla comes to mind when we are discussing electric vehicles). Or is it better to distribute the risk over multiple companies? The biotech industry has mostly followed this second strategy. Risky R&D is done by small firms with financing by high-risk capital such as venture firms. Then the resulting product, if successfully passing clinical trials, is acquired by a larger firm for commercialization.

In some cases, both strategies are important. The initial stages of research and development of a new idea are farmed out to a smaller company and financed by risk capital. And then when it comes time to build the idea into a complex system, the actual integration is done by a larger company, which has an established distribution network and marketing resources for reaching patients in a targeted fashion. This can greatly accelerate the development process.

The question, then, is whether this integration would be easier within one company or at arms-length. Illumina has made an offer to buy Grail, which was originally spun off from Illumina in order to get funding from risk capital. The goal, obviously, is to accelerate the development of this game changing integration.

The FTC has objected to the acquisition, because the agency worries about Illumina prioritizing its internal customer over other potential cancer diagnostics systems. Certainly, it’s true that some vertical mergers are anti-competitive. “Killer acquisitions” are one type of merger in biotech that is anti-competitive in nature. A recent paper from Ederer, Cunningham and Ma found that between 5% and 7% of acquisitions in the pharmaceutical industry are killer acquisitions, meaning the incumbent firm purchased the startup with the intention of shutting down one or more of its products, because the legacy company offers a competing product that is more profitable.

There is increasing agreement among regulators on both sides of the Atlantic that acquisitions — especially in the pharmaceutical sector — need to be scrutinized more closely if products have the potential to be killed off post-acquisition. One heuristic a regulator might use is to look at how much overlap there is between the acquired product and the incumbent, especially in terms of benefits and use cases. If the incumbent’s product is still on patent, then there is a significant incentive to acquire a competitive product that might be disruptive to an acquirer’s portfolio and shut down the new product.

But there’s little evidence that most vertical acquisitions are anti-competitive. Vertical mergers — or the combination of two companies at different layers of the supply chain — are less likely than horizontal mergers — acquisition of a direct competitor — to be anticompetitive as both economic theory and empirical evidence show. Regarding the theory, firms are engaged in “make or buy” decisions all the time. If they choose to produce an input in-house instead of buying it from the market, then they have vertically integrated (either by developing the capacity on their own or by acquiring another firm with that capacity). Prohibiting firms from vertically integrating via acquisition would forgo some of the benefits of economies of scope and economies of scale. A literature review by Lafontaine and Slade showed that vertical mergers were procompetitive on average.

One of the most common reasons vertical mergers are less suspect than horizontal mergers has to do with “double marginalization.” If you assume two products are monopolies in their respective markets, then the producers of those products will each charge the monopoly price, which is higher than socially optimal. If the two products are complementary, then the companies can merge and create a positive sum scenario by lowering prices. Lower prices reduce deadweight loss, which is good for consumers, and lead to higher profits for the combined firm.

We note that if the FTC ruling stands, it will mean that developers of complex integrated systems will choose to keep their technologies in house rather than spinning them out and run the risk of having an acquisition blocked. And innovative development will be slowed rather than accelerated.

President Biden has proposed to finance his $4 trillion American Jobs and Families Plans by raising taxes exclusively on corporations and households that earn above $400,000 — the top 1.5 percent of taxpayers. Biden is right that the rich should pay more than they currently do given the staggering income inequality in America that’s been made worse by the COVID pandemic.

Almost 60 percent of Americans support funding Biden’s spending plans with his proposed tax increases — seven times the share that supports debt-financing them. But while taxing the rich is smart policy and politics, funding America’s future and realizing Biden’s policy vision will also require asking more taxpayers to contribute to the public good.

The Biden administration released its American Jobs Plan yesterday – a bold package with critical investments in infrastructure and America’s workers. Among its more ambitious aims is $100 billion set aside for workforce development. This includes a long overdue investment to diversify career pathways, through approaches such as apprenticeship programs, a focus on sector partnerships, and a new and robust program for dislocated workers. There is a lot to cheer for in the AJP—here are five ways it gets it right in pairing job creation with next-generation training programs.

Investing in Workforce Development and Worker Protection. For decades, the United States has lagged other high-income countries in workforce development. The AJP calls for a $48 billion investment in workforce development and worker protection, which includes funding for registered apprenticeships and pre-apprenticeship programs. In total, this would create one to two million new registered apprenticeships. PPI has long-called for the U.S. to increase apprenticeships 10-fold and provide workers with career pathways that do not require a four-year degree. We’ve also advocated for two specific ways to modernize apprenticeships: Congress should formalize and incentivize intermediaries (public or private) by subsidizing them to create “outsourced” apprenticeships, and government at all levels should create public service apprenticeship opportunities and programs, including in industries such as information technology, accounting, and health care.

Expanding Career and Technical Education. The plan recognizes the need for investments to expand career and technical education (CTE) and workforce-readiness programs for middle- and high-school students. The 10 million jobs lost by Americans at the pandemic’s onset disproportionally impacted young adults between the ages of 16 and 24, and some estimate that as many as 25 percent of our youth will neither be in school nor working when the pandemic ends. According to the U.S. Department of Education, high school students enrolled in programs with a CTE concentration are more likely to both graduate and earn higher median annual salaries than those who did not participate. These investments will set up students to be better prepared to enter the labor force upon graduation and gain their economic footing as they transition to adulthood.

Addressing Inequities. Women and minorities have been disproportionately impacted by job losses during the pandemic and have historically been excluded from infrastructure jobs. Acknowledging these inequities, the plan calls for “strengthening the pipeline for more women and people of color to access apprenticeship opportunities,” such as through the Women in Apprenticeships in Non-Traditional Occupations program. Another option would be to increase training programs and increase apprenticeship slots in industries dominated by women that face worker shortages, such as early childhood education and care, and pair these jobs with competitive wages.

Supporting Job Training with Smart, Evidence-Based Policies. The AJP acknowledges that we need forward-looking, evidence-based approaches to train the next generation of American workers and help those who might need to reskill or upskill, including laid off workers during the pandemic. The White House calls for a “a $40 billion investment in a new Dislocated Workers Program and sector-based training.” These funds would be allocated to help train workers get trained with skills in high-demand industries, such as clean energy, manufacturing, and caregiving. To ensure the success of such programs, the White House draws on evidence that completion rates are highest when workers are provided with wrap-around services, income supports, counseling, and case management to overcome the barriers to finishing their training.

Empowering Workers and Unions. Lastly, the AJP emphasizes the important role of union jobs as the backbone of the American middle class. The proposed legislation includes important provisions for strengthening the rights of workers to organize and for making sure that employers who benefit from the plan adhere to appropriate labor standards and do not interfere with workers’ exercise of their rights. Enhancing the power of workers in our economy is critical to supporting good jobs and a strong middle class.

The Covid recession has left over 10 million Americans out of a job and millions of workers might not have a job to return to when the pandemic is over. For them, the AJP would create a diverse set of pathways to connect them with quality jobs offering livable wages. We hope that when Congress takes up this package in the coming months, they will pursue equity not just for underrepresented groups in workforce development, but also for those who lack a college degree yet make up a majority of the labor market. For them, access to pathways that do not require a four-year degree will be critical to help them regain their economic footing. Overall, the AJP meets the moment to address historic job losses and infrastructure in need of significant public investment.

Washington, D.C. – Today, Congress passed the Biden Administration’s American Rescue Plan Act, a $1.9 trillion emergency pandemic relief package that will help ramp up COVID-19 vaccine production and distribution, support small businesses and workers, and provide the necessary resources to safely reopen schools and communities.

Will Marshall, President of the Progressive Policy Institute (PPI), released the following statement:

“Passage of the American Rescue Plan is a landmark achievement for President Biden and the new Democratic Congress – one that gives us reason to hope our government may not be broken after all.

It’s not a perfect bill, but after a long, grinding year of sickness, economic privation and social isolation, this isn’t the time to make the perfect the enemy of the good. Policy disagreements aside, President Biden has rightly gauged the magnitude of the nation’s health and economic emergency and responded resolutely. His decision to “go big” was right, as was his desire to avoid vilifying his political opponents and deepening the nation’s paralyzing cultural rifts.

That’s the way our democracy is supposed to work.

By clearing his first big hurdle, President Biden has dealt himself a strong political hand for the next one: Winning passage of his coming “Build Back Better” plan for building a more just, clean and resilient U.S. economy.”

The Progressive Policy Institute is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

This week’s episode is a joint episode of the Neoliberal Podcast and the PPI Podcast, featuring guest host Colin Mortimer of PPI’s Center for New Liberalism. Colin sits down with Oregon State Treasurer Tobias Read to talk about the ways Oregon is optimizing its treasury to support and empower Oregonians. Colin and Treasurer Read discuss the day-to-day role of a State Treasurer, and how his team uses the state’s investment power to help citizens, as well as how behavioral ‘nudge’ programs can increase retirement savings.

On Monday, congressional Democrats unveiled a proposal to dramatically expand the Child Tax Credit (CTC), one of the bigger policies in President Biden’s $1.9 trillion American Rescue Plan. On the same day, Sen. Mitt Romney (R-Utah) gave the concept bipartisan backing by offering a Republican proposal for turning the CTC into an expanded child allowance. Both proposals would raise the current benefit from $2,000 per child to $3,000, provide additional credit for children under age six, make the full value of the benefit available for low-income families, deliver the payments in a monthly installment instead of a lump sum at the end of the year and dramatically reduce child poverty in America.

It’s no surprise that policymakers in both parties are prioritizing child poverty. As many as one in seven children, or close to 11 million, are poor. The United States consistently has among the highest levels of child poverty among the world’s wealthiest countries, many of which offer so-called “child allowances” to support low-income parents. The Democratic proposal would not just help these kids in the short term by lifting an estimated five million children out of poverty. It would also have long-run benefits for social mobility and support Black and Hispanic families the most. This Democratic proposal is estimated to cut child poverty nearly in half while the Romney proposal would reduce it by one-third.

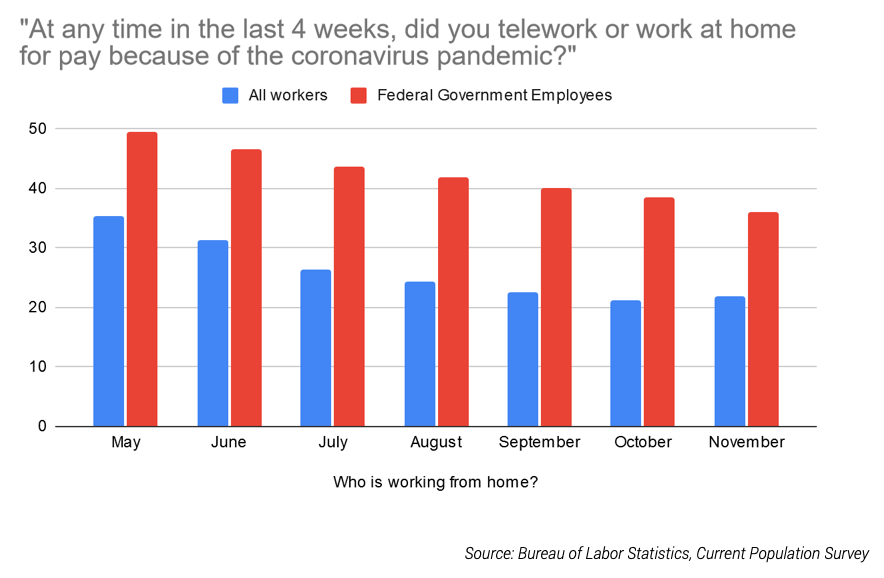

Covid-19 has taught employers the surprising lesson that for many more positions than expected, remote work is preferred by workers and seems to have little negative impact on workplace productivity. Within the federal government, a September poll showed that 53 percent of remote federal employees agreed they could perform their duties with minimal or no disruption and a November survey of managers at the Department of Transportation found 55 percent of units were more productive during the pandemic than before.

A more distributed federal government would likely raise real worker wages, improve recruiting, and lower the government’s overall operating costs. But the federal government has several additional reasons to prefer a more distributed workforce.

By allowing jobs to be performed by people who do not live in DC, a more distributed workforce can combat the trend of ever widening geographic inequality. Compared to policies like the relocation of federal agencies, it is more incremental, less political, spreads jobs to more areas, and will likely result in far less employee attrition.

Remote work brings the federal government closer to the governed, advancing the goal of recruiting a workforce drawn from all segments of society.

Property prices in DC have increasingly pulled away from national levels, but the federal presence in DC is large enough that a more distributed workforce could lead to meaningful downward pressure on residential and office rental prices in the city, benefiting residential and business renters who do not relocate.

“The Biden Administration has a unique opportunity to help distribute the federal bureaucracy across the U.S. and thereby empower workers, improve hiring, and promote regional economic development. This natural experiment over the past year has shown that for more workers than previously anticipated, working remotely can be just as effective and has unexpected benefits. Moving to a model where even 20% of the federal workforce is distributed would be a significant change. The U.S. government has aspired to achieve a workforce from all segments of society and by embracing remote work, where appropriate, we can bring that closer to reality.”

The Biden administration has a unique and largely undiscussed opportunity. Prior to Covid-19, 5 percent of the U.S. workforce primarily worked from home. During the pandemic, this share rose as high as 50 percent; as of November, 36 percent of federal workers were still working remotely. With vaccines already beginning to roll out, this temporary arrangement is likely to end during the Biden administration. The government will face a choice between making what has been a temporary experiment permanent or returning to the status quo ante and bringing everyone back to the office. We believe the latter would be a mistake.

Covid-19 has taught employers the surprising lesson that for many more positions than expected, remote work is preferred by workers and seems to have little negative impact on workplace productivity. Within the federal government, a September poll showed that 53 percent of remote federal employees agreed they could perform their duties with minimal or no disruption and a November survey of managers at the Department of Transportation found 55 percent of units were more productive during the pandemic than before. Full-time remote work also decouples where workers live and work, allowing firms to employ workers from anywhere. Hiring from outside of expensive urban centers tends to lower costs and expands the pool of applicants from which an organization can hire. For these reasons, surveys indicate private companies anticipate a dramatic expansion of permanent remote work relative to before Covid-19.

The federal government should follow suit and give current workers the choice to continue to work remotely full-time if they were able to function well during the crisis. Going forward, the government should start with the assumption that new positions will offer workers the same choice, opening up federal positions to people living anywhere in the country. While not every position can be performed remotely, a large fraction of the 36 percent currently being done remotely can.

A more distributed federal government would likely raise real worker wages, improve recruiting, and lower the government’s overall operating costs. But the federal government has several additional reasons to prefer a more distributed workforce.

By allowing jobs to be performed by people who do not live in DC, a more distributed workforce can combat the trend of ever widening geographic inequality. Compared to policies like the relocation of federal agencies, it is more incremental, less political, spreads jobs to more areas, and will likely result in far less employee attrition.

Remote work brings the federal government closer to the governed, advancing the goal of recruiting a workforce drawn from all segments of society.

Property prices in DC have increasingly pulled away from national levels, but the federal presence in DC is large enough that a more distributed workforce could lead to meaningful downward pressure on residential and office rental prices in the city, benefiting residential and business renters who do not relocate.

With the end of the pandemic finally in sight, now is the time to move to a more distributed workforce. It will never be easier than it is now to reorganize the federal bureaucracy into a more decentralized model. Managed well, all these goals can be advanced without sacrificing the quality of federal government service.

A Historic Opportunity

This is a unique opportunity to reorganize the large federal bureaucracy. Moving from a co-located to a distributed labor force presents significant challenges for any organization: new technology must be acquired and allocated, processes rethought and rewritten, and employees trained to use new technology and follow new procedures. Even then, there will be uncertainty: what problems are unforeseen and will need to be solved? Will they be solvable? And looming above it all is a bias towards the status quo (don’t fix what isn’t broken). For all these reasons, firms have historically been hesitant to pivot to remote work, even when it was technically feasible.

But due to the Covid-19 global pandemic, many of these sources of friction have been overcome. Organizations that can operate remotely are likely to have more than a year’s experience doing so by the time they can safely bring workers back into the office. Technology has been acquired and allocated, processes have been changed, and workers have learned to use their new tools and procedures. Uncertainty is resolving and with practice organizations are getting better — not worse — at working remotely. Perhaps most importantly, remote work is now the status quo for much of the federal government.

Reinforcing this rationale is the unusually large employee turnover that is expected to occur during the Biden administration due to the retirement of the baby boomers. In 2018, just 14 percent of federal employees were eligible to retire, but this number is expected to rise to 30 percent by 2023. NASA, HUD, the Treasury, and the EPA are all forecast to have more than 40 percent of employees eligible for retirement by 2023.

This presents an unusual opportunity to reorient the federal workforce towards workers who prefer remote work. One potential challenge to a more distributed federal workforce is that federal workers may believe career advancement is more difficult for remote workers if senior managers have a preference for co-location. Indeed, in pre-Covid surveys, older workers do tend to be less interested in remote work than young ones. When this is the case, remote work may become unattractive to the most ambitious (young) workers, which can undermine the successful transition of an organization to remote work. Fortunately, the retirement wave presents an opportunity to give the federal government a large infusion of workers who are comfortable with managing and working remotely, which should help mitigate these concerns.

The Benefits of Decentralization

Allowing more remote and distributed federal work has several advantages.

Morale and Real Wages

Workers like remote work. As described in detail in another report, remote work is valued by workers for a variety of reasons. The freedom to work from anywhere allows workers to move to be closer to friends and family or to where they can live in their preferred lifestyle. Remote work also eliminates commuting time, tends to reduce meetings and distractions, and frequently increases schedule flexibility. In a pre-Covid study workers were willing to accept wages that were 8 percent lower in exchange for the opportunity to work remotely; another showed that remote work significantly reduced employee turnover.

In the era of Covid-19, greater experience with remote work has done little to dampen enthusiasm for it. Overall, 76.1 percent of workers who can work from home say they want to do so at least a day a week when the pandemic is over, and 27.3 percent want to be fully remote. Among tech workers, the desire to be remote is even higher: a November survey found that 95 percent with the option to work remotely permanently would choose to work remotely on a permanent basis, and that 6 in 10 would take a pay cut to work remotely. Giving federal workers the option to work fully remotely is a cost-effective way to raise employee morale.

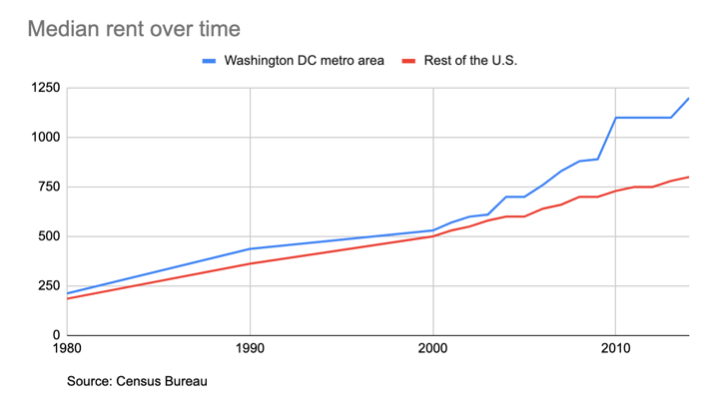

Remote work’s most salient benefit for federal workers may be its potential impact on the real wage of federal workers (i.e., the wage relative to their cost of living). A plurality of federal workers live in and around Washington, D.C., where the cost of living has diverged from the national average at an increasing rate. BEA data shows the overall cost of living in the DC metro area was 17.4 percent higher than the average for the U.S. in 2019. This difference is largely driven by significantly higher housing costs, which Census data show has increasingly pulled ahead of the rest of the country over the last two decades.

By allowing federal workers to relocate from the Washington metro region to areas with a lower cost of living, federal workers in Washington, D.C. can benefit from an increase in their real wage (that is, their wage relative to cost of living). Given the BEA’s estimate, D.C.-based federal employees can enjoy the equivalent of a 17.4 percent reduction in living expenses by moving to a region with a nationally representative cost of living.

This benefit, of course, depends on how much pay is adjusted for remote workers. In principle, the federal government could allow workers to retain their original pay, regardless of their location, or it can adjust pay to reflect local cost of living (as is current federal policy for full-time telework). The maximum benefit to federal workers would allow workers to retain their original salary, while the maximum savings to government would adjust pay to reflect cost of living.

It is important to note that D.C.-based federal workers could very well see their real wages rise if they relocate, even under the current system of locality-based pay. Federal workers are typically paid according to the general schedule, which includes locality pay adjustments based on the prevailing local wages for non-federal employees. For the year 2021, the location pay adjustment for the Washington, D.C. metro area was 30.5 percent, as compared to the lowest locality adjustment of 16.0 percent for “rest of the United States.” Thus, in general, a worker relocating to a place with nationally representative prices would see their cost of living decline by 17.4 percent according to BEA data, but would see their wages reduced at most by 14.5 percent.

This understates the potential gains from relocation, since the places with the lowest locality pay have lower than average costs of living. To take one example, the location pay adjustment for Des Moines, Iowa (where one of the authors of this report resides) is also 16.0 percent. A federal worker relocating from Washington, D.C. to Des Moines would see their salary reduced by 14.5 percent, but would see their cost of living fall by nearly twice as much (27.2 percent).

An alternative approach would be to default to the current system of locality wages in the new location while retaining the option for agencies to hire using the D.C adjusted pay scale on a case-by-case basis. Doing so would essentially allow agencies a 17.4 percent average increase in the real wage they could afford to pay under the General Schedule pay scale. This would enable the federal government to attract more qualified candidates than would ordinarily be the case.

Not everyone prefers remote work, but there is no reason the federal government cannot provide office space in D.C. for workers who prefer it. One of the main advantages of remote work is greater choice and autonomy for workers, including the choice to work in a traditional office environment. Others will prefer a hybrid arrangement, enjoying a less frequent commute into the office (as was already the norm for much of the federal workforce prior to Covid-19). Moreover, even federal workers who do not work remotely will likely benefit from a more remote friendly policy. In San Francisco, an exodus of tech workers due to the option to work remotely led to a 27 percent drop in real rental prices over the year. Downward pressure on rental prices in the D.C. area would also serve to raise the real wages of federal employees who are unable to relocate to areas with a cheaper cost of living. It could also reduce congestion and commuting times for D.C. residents. This is important since, as we discuss later, the majority of federal positions will probably remain co-located for the foreseeable future.

Lower Costs

Whether the government ultimately chooses to adjust pay based on locality, remote work will allow the work of the federal bureaucracy to be done at lower cost. Renting office space in Washington, DC is expensive. According to Moody’s Analytics, office space is 41.6 percent above average for the U.S., making the D.C. metro area the 7th most expensive in the country. The US Patent and Trademark Office, which already has a work-from-anywhere program for patent examiners, estimated remote work saved it $52.1mn on reduced office space requirements in 2019 alone. And just as workers unable to relocate from D.C. may benefit from lower property prices if a significant portion of D.C. workers relocate, D.C. based agencies may benefit from lower prices for office space due to reduced local demand.

Office space isn’t the only source of savings. Increased worker morale due to remote work has been found to reduce employee turnover in some settings. The USPTO estimated that increased retention accounted for $23mn in savings over 2019.

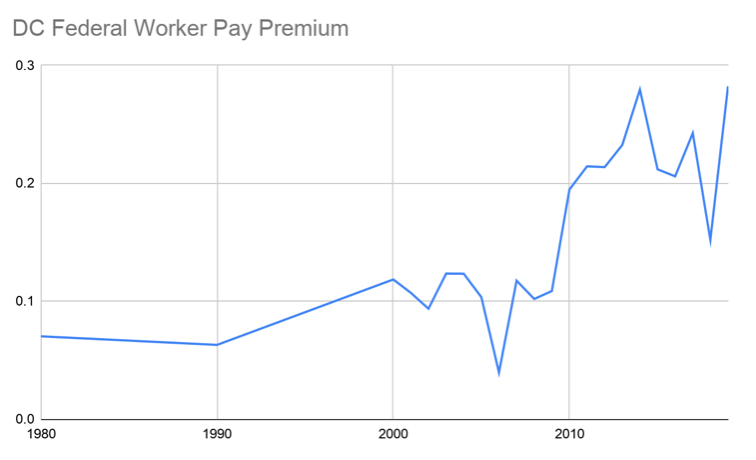

As noted above, a more distributed federal government could also choose to save money by adjusting pay by locality. To estimate the potential savings if some portion of D.C.-based federal workers relocated, we use data on 1.5 million federal government employees from U.S. Census data from 1980 through 2019 to estimate the DC pay premium with regression analysis. The results show that (conditional on age and time varying education premiums) the relative cost of employing workers in DC has gone from around 6 – 7 percent in the 1980s and 1990s, to 10 percent in the early 2000s, to around 22 percent in the most recent years, relative to federal workers in the rest of the country.

A Larger Labor Market

Remote capabilities can also improve government quality by facilitating access to the best job candidates in the nation, rather than the best in the local job market. Thus, even if a given worker is slightly less productive when working remotely than in an office (and they probably are not, as discussed later), this disadvantage can be more than outweighed by the benefits of access to a larger labor market. As an illustration, suppose it’s a bit harder to do some job remotely; any particular worker is 5 percent less productive performing their job remotely than they would be in an office. Since the remote job is open to anyone in the country, if that lets the government hire a worker who is 6 percent more productive than could be had locally, this will more than offset the decreased productivity of doing the job remotely.

These issues are particularly salient to the federal government.

First, relative to the nation as a whole, the federal government is unusually suited to remote work. As indicated in the figure below, the share of federal workers who are working remotely has persistently been 15 percentage points higher than the national average of all workers.

Importantly, the estimates above are likely to be conservatively low, since BLS estimates only refer to working remotely due to the pandemic and exclude those who were already remote. In addition, otherestimates find significantly higher rates of overall remote working than the BLS, suggesting it is on the conservative end of the spectrum.

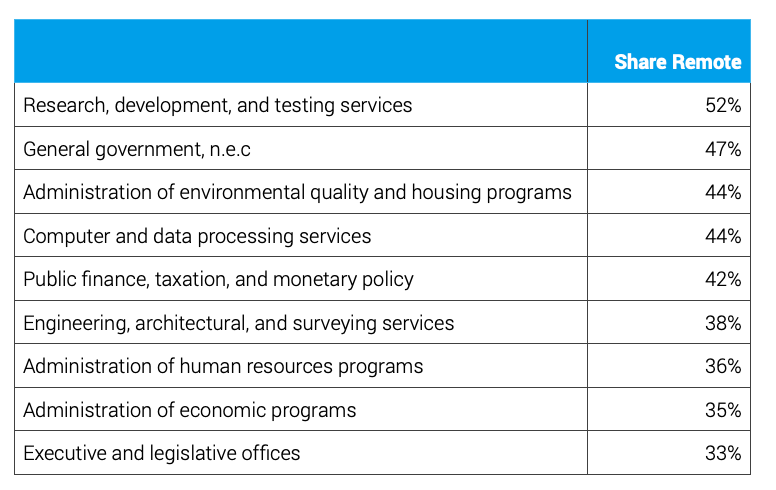

To get a better sense of the kinds of federal positions that can be done remotely, we can turn to the current population survey, which has asked employees if they are working remotely due to the pandemic since May. Over September, October, and November 2020, federal government position types with more than 30 percent remote workers are displayed below.

Note: From 2020 CPS, limited to cells with a sample size of 100 responses or more.

Note that many of these position types require high levels of skills, education, or experience, which can make hiring challenging. This is important given the anticipated spike in retirement eligibility during the Biden administration as the baby boomers retire. Making the federal bureaucracy remote will facilitate filling these vacancies quickly with the best candidates in the country. Moreover, given the move to remote work by much of the private sector (one survey found 22 percent of US workdays will be remote even after the pandemic subsides), the US government will be at a significant hiring disadvantage if it insists workers relocate to accept positions and other organizations do not.

Finally, it’s worth considering new types of talent that wouldn’t previously have considered working for the federal government that would be open to public service under a permanent remote work arrangement. In particular, the federal government has struggled to increase its technical capacity with many workers earning higher salaries at firms like Google, Facebook, and Microsoft than are possible working under the General Schedule pay scale. To combat this, the federal government has attempted to increase the frequency of technical “tours of duty” that tech workers can undertake. However, take-up has remained low, with one reason being the difficulty of relocating to D.C. for a temporary fellowship. But if these workers could work remotely, opportunities within federal agencies will become more attractive.

Geographically Dispersed Workforce

A geographically dispersed workforce has several other advantages for the federal government. The first principal of the US Merit System is (emphasis added):

Recruitment should be from qualified individuals from appropriate sources in an endeavor to achieve a work force from all segments of society, and selection and advancement should be determined solely on the basis of relative ability, knowledge and skills, after fair and open competition which assures that all receive equal opportunity.

By removing relocation barriers to employment, more opportunities to work from anywhere would contribute to a more geographically representative workforce. These barriers can be significant, even when the monetary cost of relocation to D.C. is covered by the employers. A 2020 study found the typical U.S. adult would need to be paid an additional $24,000 (43 percent of the typical salary) to relocate to a job that took them away from friends and family.

Otherstudies have highlighted the importance of informal ties and social networks for finding jobs. Clustering federal jobs in a small number of locations means the social networks of government workers are geographically constrained, contributing to an information gap about job openings, the desirability of different positions, the kinds of experiences that would be valued, and so on, outside major federal clusters. Over time, a dispersed workforce would help erode these information gaps.

More speculatively, a geographically dispersed workforce could help rebuild trust in government, which has been nearing historic lows. Working from home during the Covid-19 pandemic has been associated with a 31 percent increase in white collar crime tips to the Securities and Exchange Commission, which may have been caused by a more arms-length and professional relationship between coworkers. A dispersed workforce may also be harder to improperly influence for similar reasons (it is harder to convince someone to bend the rules over email than dinner and drinks). Lastly, it is worth noting that historically, Americans have trusted their local government more than their state government, and their state government more than the federal government. No doubt this is partially due to the social and physical distance between the local, state and federal governments and the governed.

Economic Development

Finally, remote work could be a new tool for economic development in regions that are being increasingly left behind by the rising importance of agglomeration effects. The increased importance of agglomeration effects over the last several decades have led to economic prosperity for cities and economic decline in rural areas. This is one of the root causes of the serious political and social challenges we face today. A variety of policies have been suggested to revitalize or at least slow the decline of lagging US regions, including proposalstorelocateseveral federal agencies outside of Washington, D.C. The purpose of relocation is to move jobs to regions with shrinking economies (and tax bases). These are not just the jobs of the workers in federal agencies, but also workers in related fields who work with the agencies (lawyers, lobbyists, etc.), and workers who provide services to high-paid government workers (barbers, restaurant workers, IT personnel, etc.).

Dispersing the federal bureaucracy is a much easier way to gain the benefits of economic development that is relocation’s goal.

It would distribute the gains of relocation more widely, including to rural areas, rather than concentrating them in a handful of expensive, urban cities.

It would allow more jobs to be moved out of Washington. Agencies that do not need to be physically present in Washington could go remote. But, even more workers from agencies that cannot relocate could also go remote, as long as their specific position does not require physical proximity.

It would be far less politically contentious than deciding centrally where to relocate entire agencies. Instead, workers would have the choice on if and where to relocate.

It would avoid the attrition and disruption that typically accompanies relocation. For example, the relocation of the USDA Economic Research Service to Kansas City led to the loss of at least half the staff (and up to 93 percent) as workers declined to move.

Moves could be implemented incrementally, one open position at a time.

It would be cheaper and logistically easier than organizing a move. The costs and logistics are borne by staff, not the Agency.

Embracing remote work at the federal level will help entrench remote work as a new mode of organizing business in general. As more firms adopt a remote-first orientation, geographic inequality will be further reduced.

Data from the BLS suggests approximately 40 percent of federal workers were working at home in September, and a survey of remote workers from the same month found that slightly over half agreed that they could perform their work remotely with minimal or no disruption. Taking these estimates seriously suggests 20 percent of federal jobs can already be performed remotely. Given that the federal government has consistently had more remote workers than the national average, this estimate is likely conservative: a survey from Upwork of 1,000 hiring managers found they were planning an average of 22.9 percent workers fully remote in the long-run.

Looking only at the 400,000 federal workers based in D.C., Maryland, and Virginia, 20 percent equals 80,000 workers. For comparison, a 2019 Brookings report about the potential economic development benefits of relocating federal agencies listed 19 greater D.C.-based agencies and sub-agencies as potentially able to be relocated. They collectively employ a similar number in the same three states: 89,000 workers. But remote work would also be available to the federal government’s other 1.4mn US-based federal workers, many of whom are also based in expensive urban centers.

Addressing Some Potential Fears of Remote and Distributed Work

Like any policy change, dispersing the federal workforce may entail some costs as well as benefits. In this section, we address two major concerns and conclude they are not significant enough to outweigh the benefits discussed above.

Does Remote Work Really Work?

A primary reason that remote work was not more widespread prior to Covid-19 was a perception that it was not as productive as a traditional office. Even if this was true, it would not necessarily mean remote work is undesirable, since any disadvantages associated with productivity might be more than offset by cost savings and access to a larger labor market. Fortunately, for a wide variety of job types, no such trade-off is necessary: for many positions, remote work appears to be just as productive as traditional office-based work.

A review of the economic literature about the efficacy of remote work prior to Covid-19 found little evidence that it results in any reduction in worker productivity for a wide variety of positions. Indeed, plenty of evidence —including a particularly relevant study from the US Patent and Trademark Office’s work-from-anywhere program —found remote workers were more productive than those in a traditional office environment. The fact that modern remote work is productive is the likely explanation for the steady rise of full-time working from home before Covid-19 from under 3 percent to 5 percent over 1980 to 2018 (with a marked acceleration after 2010). Even 5 percent understates the true extent of remote work prior to Covid-19, since it excludes work away from both the home and the office, such as in coworking spaces. Including these raises the share of full-time remote workers prior to Covid-19 to 10 percent. Even without Covid-19, businesses were (slowly) learning that remote work worked.

Extensive experience with remote work during Covid-19 has accelerated that process. It is now clear that in a wide variety of contexts, there really is no question that remote work can be at least as productive as traditional work. A number of high-profile companies have made the switch to permanent remote work after several months of experience with it (e.g., Microsoft, Facebook, Twitter). This is not limited to a few anecdotes either; in a survey of 1,000 hiring managers by Upwork, 60 percent planned to increase their use of remote work in the future, as a result of their experience with Covid-19.

Within the federal government, experience has also been broadly positive as workers gained experience. Whereas an April poll of federal workers working remotely found just 15 percent reporting minimal or no disruption due to the shift to remote work, a follow-up poll in September saw this number rise to 53 percent. A November survey of managers at the Department of Transportation found 55 percent of units were more productive during the pandemic than before.

Systematic evidence on the longer-term viability of remote work is unfortunately limited at the moment. While there are examples of organizations that have successfully organized in a distributed manner for many years (the USPTO has had a work-from-anywhere program since 2012, WordPress since 2005), any evidence about the long-term efficacy of remote work necessarily predates the recent transition to remote work due to Covid-19. It may be that longer term challenges to successful remote work will yet emerge. At the same time, it is likely that new organizational and technological solutions will emerge (indeed, the number of patent applications related to remote work technology has increased dramatically since February 2020), so that remote work is just as likely to function better in the long run than in the short run. The experience of remote work is also likely to improve once widespread vaccination allows children to return to full time childcare and social gatherings outside of work are viable.

Nonetheless, given long run uncertainty one possibility would be to implement a multi-year trial for remote work. To realize most of the benefits of remote work, such a trial needs to be sufficiently long, because if workers feel they will be required to return to a D.C. office in the near term, they will be unwilling to relocate. As an example, the U.S. Patent and Trademark Office’s work-from-anywhere program began as a five-year pilot program in 2017.

Benefits of Agglomeration

Another critique of remote work focuses not on the level of individual workers and businesses, but on the broader ecosystems in which they operate. Physically clustering a large number of workers in a particular industry has traditionally led to at least two major benefits: more efficient matching of workers to positions, and learning. One concern may be that these benefits will be lost if an organization goes remote, even though at the level of individual workers productivity is unaffected. Fortunately, the internet and cheaper travel has significantly eroded both of these advantages of physical proximity.

First, clustering workers together can make it easier to match the right worker with the right job. Physical proximity makes it easier to share information and form informal social networks (which can be just as important for helping people find jobs that are good fits). While these effects no doubt continue to exist, their relevance may be fading with the advent of online job markets, the use of algorithms for matching workers to jobs, and the growth of online social networks (which allow people to maintain geographically distributed networks of informal friends).

Second, economists frequently point to learning via “local knowledge spillovers” as another reason why organizations choose to cluster together. A variety of evidence shows innovative businesses learn from each other, borrowing and improving on the ideas and inventions of their neighbors. But here too, there is a lot of evidence that these effects are shrinking —possibly to the point of irrelevance in some sectors — as the internet and cheap travel makes it no longer necessary to physically reside near each other to learn from each other.

Moreover, it is unclear if these kinds of knowledge spillovers are relevant in the context of the federal government. Furthermore, while keeping the majority of federal employees clustered together in Washington, D.C. makes it easy for them to share knowledge with each other, it makes it harder to learn from the policies and processes of 50 state governments and thousands of local ones.

In sum, it is true that a more distributed federal workforce might find it benefits less from matching and learning than it would if it remained in D.C. But, at a minimum, the internet and cheaper travel have eroded the importance of these factors. And for learning, it may in fact be the case that a more distributed government would benefit more from learning than one clustered in DC. At any rate, the challenges associated with remote work are likely smaller than they have ever been, while the benefits remain as large as ever.

Conclusion

The Covid-19 pandemic has shown us that for many more positions than previously suspected, remote work has come of age. It is now possible for a significant share (perhaps 20 percent) of federal positions to be done effectively by a distributed workforce of full-time remote workers residing where they choose. Moving the federal workforce in this direction would have myriad advantages. It would make working for the federal government more attractive, both by giving workers the autonomy to work in the place and manner they prefer, and by potentially allowing for increased real wages for workers who choose to live in places with a lower cost of living. Combined with access to a larger national labor market, this would facilitate hiring and retaining quality employees. This is especially important given the expected retirement wave that will come in the years ahead. A more distributed federal workforce would also likely lead to lower costs for the government, in terms of office space and possibly wages. It may also benefit workers who continue to reside in Washington, D.C., through its beneficial impact on congestion and property prices. Lastly, a more distributed workforce would be a tool for economic development of lagging regions and allow the government to better achieve its goal of hiring a workforce that is representative of the population it governs.