The outbreak of COVID-19 (commonly known as coronavirus) has created a global market downturn and raised the prospect that the United States could enter its first recession since the 2008 financial crisis. Last night, President Donald Trump and U.S. House Speaker Nancy Pelosi offered two competing approaches for securing both the health and economic security of the American people. While the president’s proposals would arguably do more harm than good, Speaker Pelosi and House Democrats should be commended for swiftly developing a comprehensive and serious plan to effectively tackle the crisis.

During the last recession, Speaker Pelosi passed a stimulus bill that used a combination of deficit-financed tax cuts and government spending increases to boost the economy. With interest rates on government debt now below projected inflation, many are calling for her to now take similar action. The problem is that commerce is currently being constrained by proactive measures people are taking to limit the spread of a pandemic, not a lack of money in consumers’ pockets. Additionally, the coronavirus has disrupted global supply chains, which no amount of demand-side stimulus can alleviate in the short term. A unique economic problem requires a unique solution.

Some are concerned that subprime auto loans – which offer higher interest loans to riskier borrowers – pose a threat to the stability of the global economy in much the same way that the subprime mortgage market contributed to the Great Recession. Democratic presidential candidate Elizabeth Warren, in particular, has raised the warning flags as part of her campaign. But these worries are ill-founded and based on misleading data and faulty analogies.

In particular:

Auto loans account for a relatively small percentage of the increase in nonfinancial debt over the past five years;

Americans are spending less of their budgets on car purchases today, including finance charges, than they were before the recession;

Low-income households saw motor vehicle purchases and finance charges fall from 8.5 percent of household budgets in 2000 to 4.9 percent in 2018;

Over the past five years, the share of new auto loans going to low-credit borrowers has remained relatively constant. There are no signs that low-credit borrowers are either being frozen out of the market or becoming too large a share of loans;

Newly delinquent auto loans, as a percentage of current balances, have been falling over the past two years; and

Subprime auto loans differ significantly from subprime mortgages in key respects that make them less likely to pose a serious threat to financial stability

Risk-based pricing of auto loans appears to be working so far, keeping low-income borrowers in the market without driving up delinquencies or to low-income consumers, while not posing the same risk that the subprime mortgage market.

Introduction

To purchase a vehicle, Americans with low or non-existent credit scores often use auto loans with higher interest rates than loans to prime borrowers. Some market watchers have indicated concern about “subprime” auto-loan trends and the potential for a crisis similar to the subprime mortgage crisis that heralded the last recession.

The subprime mortgages and the related mortgage-backed bonds remain the classic case of a poorly executed financial innovation. The initial impetus behind the idea was a good one. Housing is a key element of middle-class wealth, so expanding the system of mortgage finance to help lower-income households buy homes seemed like a positive. However, the subprime mortgages and bonds were designed in such a way that they assumed rising housing prices. When housing prices started to fall, the subprime mortgage system collapsed and contributed to the financial crisis.

Will subprime auto loans create the same problems? In a recent essay, Democratic presidential candidate Senator Elizabeth Warren raised the warning flag:

Auto loan debt is the highest it has ever been since we started tracking it nearly 20 years ago, and a record 7 million Americans are behind on their auto loans — many of which have similar abusive characteristics as pre-crash subprime mortgages1 .

Warren is not alone in her worries. In late 2016, for example, the Office of the Comptroller of the Currency warned that auto-lending risk was increasing and that banks (and other investors in securitized assets) did not have sufficient risk-management policies in place. Fed Governor Lael Brainard pointed to subprime auto lending as an area of concern in a May 2017 speech, while analysts worried about “deep subprime” auto loans2. Some groups used the term “predatory” auto lending.3

But these concerns are misplaced. As we will show later in this paper, the statistic cited by Senator Warren does not reflect the current state of the auto loan market, as it includes old loans from much weaker economic times. Perhaps most fundamental to understanding the problem with drawing a parallel between the mortgage crisis and today is the fact that subprime mortgages and subprime auto loans are very different products.

Naturally, lower-income households with low credit scores or limited credit history may have fewer financial resources and be inherently riskier borrowers. Moreover, the fact that motor vehicles depreciate over time means that the collateral for the loan becomes less valuable.

Nevertheless, the ability to own a car and, therefore, access credit is crucial for this population. Risk-based pricing charges low- rated borrowers higher interest rates, but in return, offers them the opportunity to borrow money to buy a vehicle that might otherwise be financially inaccessible.

For many lower-income households, their vehicle is the single biggest asset they own.

While vehicles do not appreciate in value as homes do, vehicles are income-producing assets in the sense that they are often essential for commuting to work, especially in non-urban areas. As one report noted, “Owning a car is the price of admission to the economy and society in much of America.”4

In this paper, we analyze the auto loan market, paying particular attention to auto loans made to low-income Americans and to people with bad credit. We find that:

Auto loans account for a relatively small percentage of the increase in nonfinancial debt over the past five years;

Americans are spending less of their budgets on car purchases today, including finance charges, than they were before the recession;

Low-income households saw motor vehicle purchases and finance charges fall from 8.5 percent of household budgets in 2000 to 4.9 percent in 2018;

Over the past five years, the share of new auto loans going to low-credit borrowers has remained relatively constant. There are no signs that low-credit borrowers are either being frozen out of the market or becoming too large a share of loans;

Newly delinquent auto loans, as a percentage of current balances, have been falling over the past two years; and

Subprime auto loans differ significantly from subprime mortgages in key respects that make them less likely to pose a serious threat to financial stability.

Risk-based pricing of auto loans appears to be working so far, keeping low-income borrowers in the market without driving up delinquencies or threatening the financial system. We conclude that the subprime auto loan market is beneficial to low-income consumers, while not posing the same risk that the subprime mortgage market did before the financial crisis. While it will be instructive to observe subprime auto loan trends going forward, current trends do not indicate significant instability concerns in this market.

Recent Patterns in Debt Accumulation

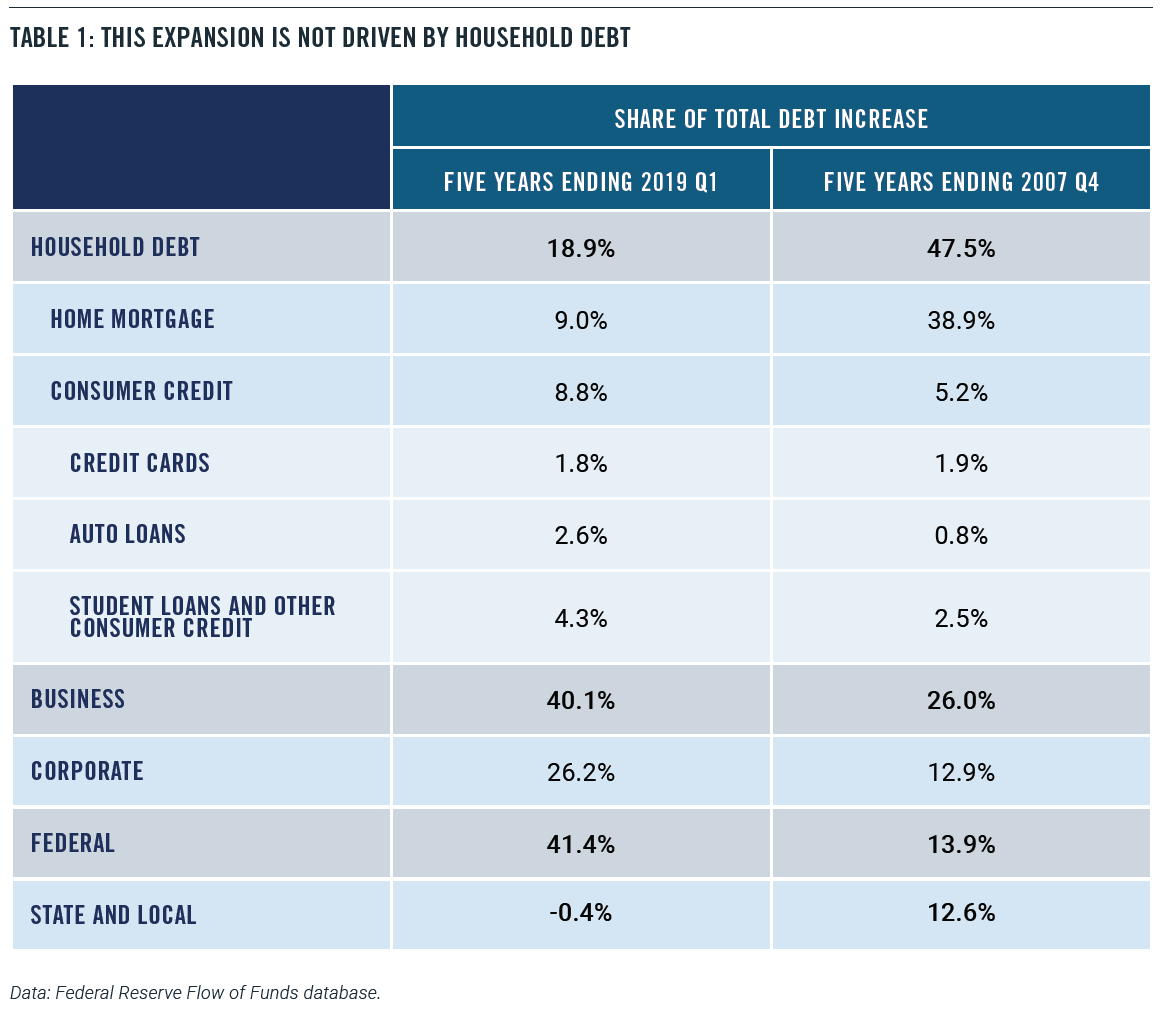

Recent patterns in debt accumulation are very different from those that preceded the financial crisis and Great Recession. Non-mortgage consumer credit – including auto loans, credit cards, and student debt – has risen by $900 billion over the past five years, according to Federal Reserve data. While that figure sounds substantial, that increase amounts to less than 9 percent of the total increase in domestic nonfinancial debt – that is, all debt except borrowing by financial institutions. The rise in consumer borrowing is dwarfed by the increase in business debt ($4.1 trillion) and federal debt ($4.2 trillion) over the same period. Those two categories together account for 82 percent of the increase in domestic nonfinancial debt (Table 1). The leading contributors to business debt growth are mortgages and corporate bonds.

Indeed, businesses have taken the greatest advantage of low-interest rates. Nonfinancial corporations have almost doubled their outstanding corporate bonds since the end of 2007 when the last recession started. Meanwhile, household debt has risen by only 10 percent.

Taking home mortgages into account, households have only accounted for 19 percent of the increase in domestic nonfinancial debt since 2014. By contrast, in the five years leading up to the Great Recession, households accounted for 48 percent of the debt increase. In other words, the financial boom in the pre-recession years was heavily driven by household borrowing, while households have only contributed a small portion to the current debt increase.

A skeptic could argue that, given derivatives and financial engineering, it’s possible for a relatively small portion of the debt market to drive an outsize increase in risk for the whole system. Indeed, that’s what happened ahead of the 2008 financial crisis. In May 2007, then-Chairman of the Federal Reserve Ben Bernanke famously said, “We believe the effect of the troubles in the subprime sector on the broader housing market will be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system.”5 At the time, the value of subprime mortgages was about $1.3 trillion, which was only 10 percent of the mortgage market and an even smaller share of total borrowing. Bernanke and other policymakers figured that the problems in subprime mortgages could be easily contained.

What Bernanke and others failed to reckon with, however, was how the subprime mortgages had been designed to make sense only in a rising real estate market. Subprime mortgages were constructed effectively to subsidize interest rates with the possibility of appreciation. These financial instruments would offer low upfront rates that enabled lower-income borrowers to qualify. When the teaser rates eventually reset to much higher levels, the assumption was that the borrower could refinance into a new mortgage.

Moreover, the subprime mortgages were then securitized and used to build complicated financial derivative products. And when the subprime mortgages failed because of declining home prices, so did the derivatives. In other words, problems in a relatively small financial sector could be amplified and have a much larger effect on the rest of the economy.

Despite this concern, there is evidence to suggest that subprime auto lending is not a substantial risk to the broader economy. Auto loans are only 7.4% of household debt, which is the 40-year historical average.6 Moreover, the auto asset-backed securities (ABS) market is likewise dwarfed by the mortgage-backed securities (MBS) market. As of the second quarter of 2019, there was a mere $264 billion in auto-related securities, which included only $55 billion in subprime auto securities. By comparison, the amount of outstanding mortgage-related securities came to almost $10 trillion.7

Further, subprime auto loans don’t work the same way that subprime mortgage loans did in the pre-crisis era. Cars and trucks depreciate steadily over time, so the value of the collateral diminishes. That means lenders can’t afford to offer teaser rates, or excessive levels of negative equity, to buyers with low credit scores. They must charge higher rates, properly pricing risk. As one article put it, “the very nature of a real estate loan is very different from an auto loan. Real estate is an investment that typically appreciates over time. During the bubble years, consumers and lenders falsely believed appreciation would bail them out from poor judgment. Vehicles, on the other hand, depreciate. There is no false hope of higher values in the future to bail out a borrower or a lender.”8

The Auto Market

Despite the relatively small role that consumer debt is playing in the current debt expansion, some people can’t shake the idea that Americans are over-spending and over-borrowing to maintain a particular lifestyle. Consider this quote from an April 2019 piece from Business Insider:

The fact that America’s top-selling vehicle — a Ford truck with a price starting at nearly $30,000 – and many like it cost nearly half the median household income hasn’t stopped people from buying them and hasn’t stopped lenders from facilitating loans.9

Over the past five years, the price of new motor vehicles has risen by only 1.1 percent, according to estimates by the Bureau of Economic Analysis (BEA).10 By contrast, the overall price level of consumer goods and services have risen by 6.7 percent over the same stretch.11 In other words, the relative price of new motor vehicles has fallen over this period.

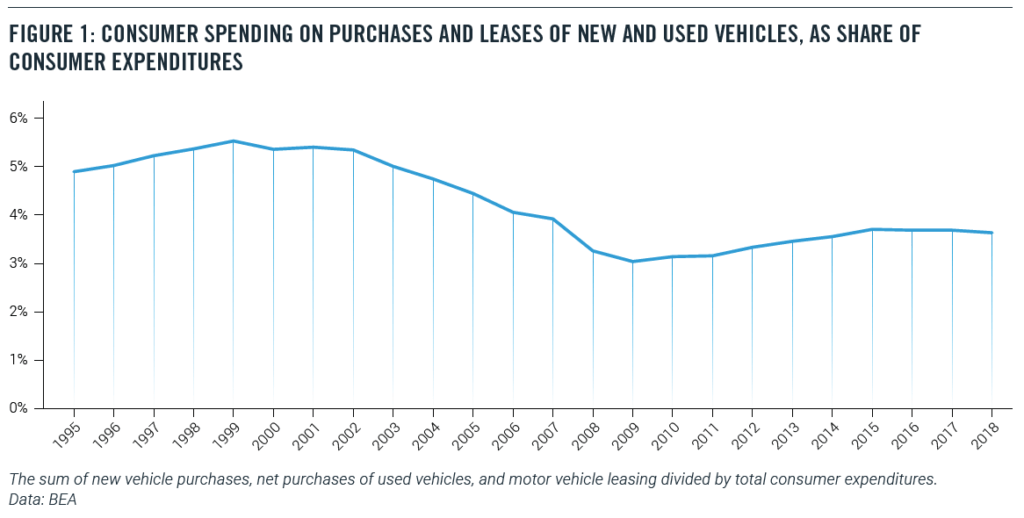

Not surprisingly, the share of consumer spending on new and used vehicles has fallen as well. In 2000, 5.4 percent of consumer spending went to purchases and leases of new and used vehicles. Today, that share is down to 3.6 percent (Figure 1).12

The BLS Consumer Expenditure Survey tells the same story. In 2000, motor vehicle purchases and finance charges amounted to 9.7 percent of household outlays. As of 2018, the last year for which full data is available, the share of vehicle purchases and finance charges fell to only 6.7 percent of household outlays.13 In part, this decline may represent a lengthening of the term of auto loans.14 (These figures would not be changed much by including automobile lease-related payments, which amount to about 10 percent of automobile purchase-related payments in 2018.)

The State of the Low-Income Auto Market

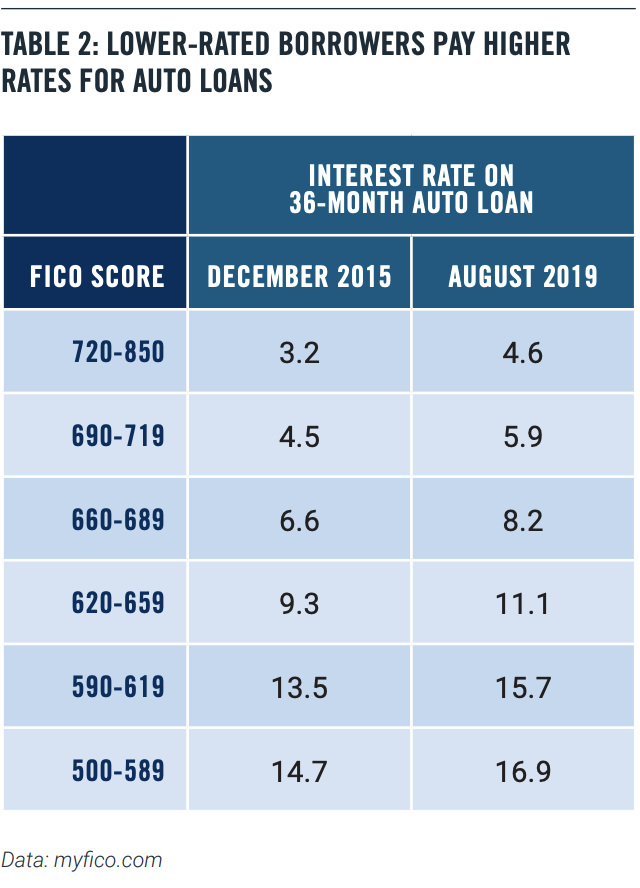

It’s not surprising that lower-rated borrowers pay more for their auto loans. Table 2 below shows interest rates for a 36-month new car loan at different credit rates for December 2015, which was close to the bottom of the credit cycle, and August 2019 (Table 2).

We can see that rates have risen for all credit-rating levels, but more so for the low-rated borrowers.

This risk-based pricing means that low-rated borrowers are not frozen out of the auto loan market. That’s good news, since, in many parts of the country, a car or truck is a necessity, even for low-income households. There is little or no public transit outside of densely populated urban areas, and ride-sharing services are not viable alternatives in many places. So, it is unsurprising that the share of low-income (the bottom quintile) households with a vehicle hold steady at 66 percent in both 2000 and 2018.

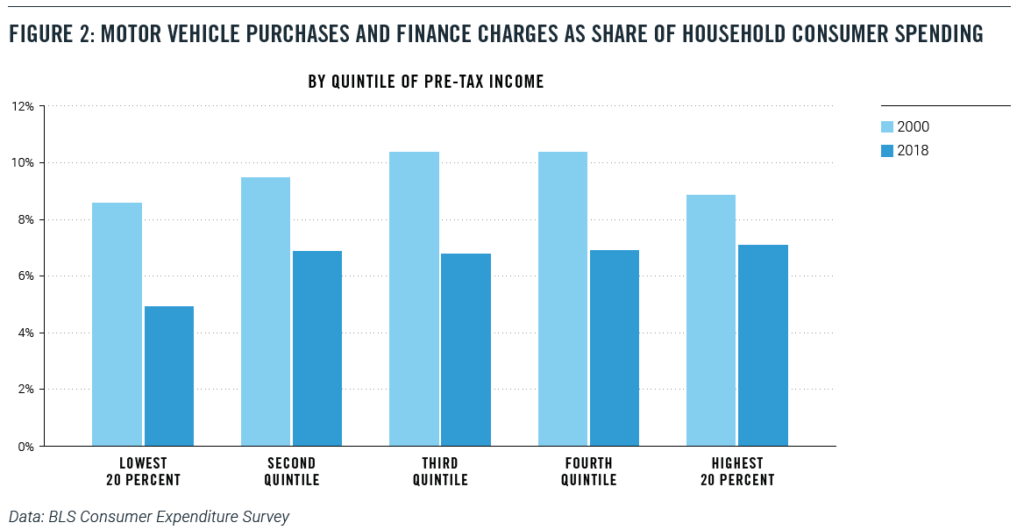

At the same time, low-income households saw motor-vehicle purchase and finance taking a smaller share of their budgets. In the bottom quintile of pre-tax income, motor vehicle purchases and finance charges fell from 8.5 percent of household budgets in 2000 to 4.9 percent in 2018 (Figure 2), a drop of almost four percentage points.15

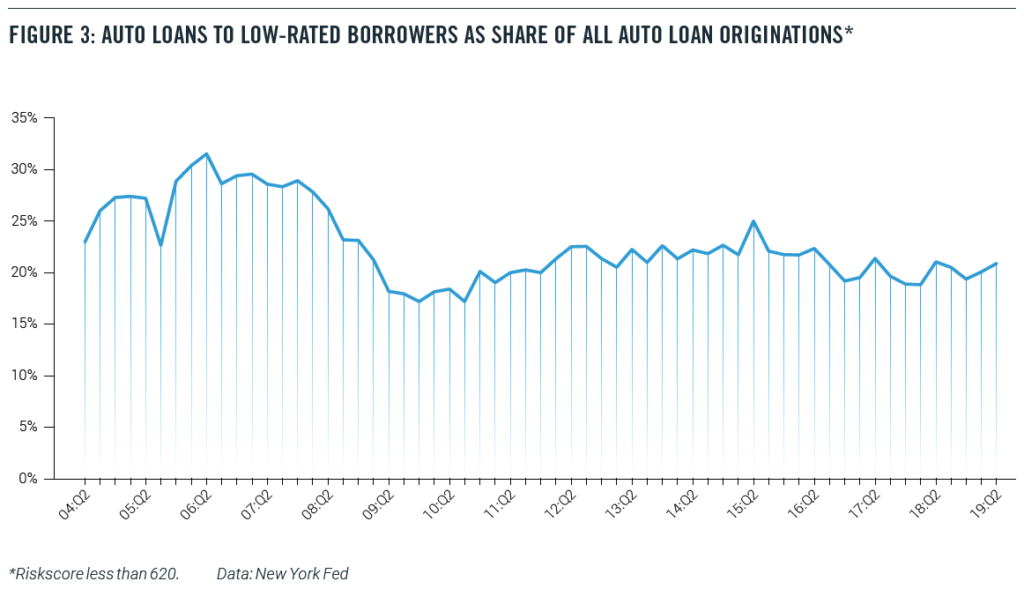

Similar data from the New York Fed’s Household Debt and Credit Report confirm that low-income households are not being uniquely stressed financially by automobile borrowing. Figure 3 shows the share of all auto loan originations that are going to low-rated borrowers (with a Riskscore of less than 620). Before the financial crisis, about 30 percent of new auto loans were going to low-rate borrowers, a startlingly high percentage. That share fell to 20 percent after the crisis and shows no signs of rising (Figure 3).16

The biggest piece of negative news has come from the New York Federal Reserve’s well-publicized finding in February 2019:

…(T)here were over 7 million Americans with auto loans that were 90 or more days delinquent at the end of 2018. That is more than a million more troubled borrowers than there had been at the end of 2010 when the overall delinquency rates were at their worst since auto loans are now more prevalent.18

This startling number, while impressive, simply doesn’t mean what it seems to suggest. This figure includes anyone who still has an old, bad auto loan on their credit record, even if the loan was made and written off years earlier.19 In fact, even after the lender writes off the loan, the loan servicer could continue to report the account to the credit bureaus.

The recent economic history of the United States helps to explain this figure. The number of nonfarm jobs did not return to pre-recession levels until 2014, while the employment-population ratio for Americans with a high school diploma but no college did not bottom out until 2015. As a result, today’s subprime borrowers are carrying around bad loans from the days when the labor market for less-educated workers was still struggling.

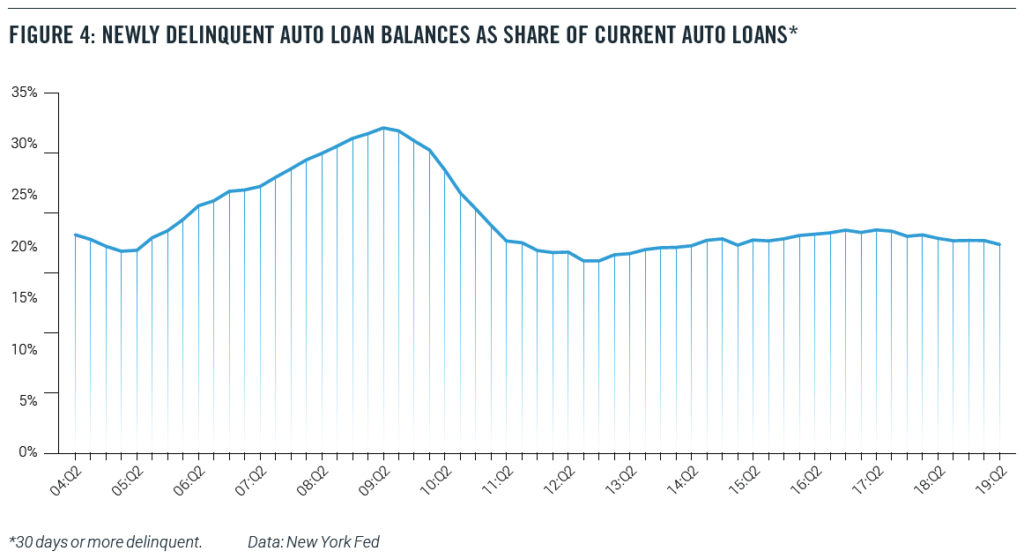

Indeed, in an August 2019 blog item, New York Fed economists recommend that anyone interested in the current performance of debt should look at the transition into delinquency- that is, a chart such as Figure 4.20 And by that measure, auto loans are doing far better than in the pre-recession years.

Conclusion

In the event of a recession or a significant economic slowdown, auto loan delinquencies will predictably rise. Subprime auto borrowers, who are more likely to have fewer resources, will be likely to fall behind in their payments when times turn bad.

Nevertheless, a careful look at the data does not suggest that either the origination of subprime auto loans or the exposure of the broader macroeconomy to the auto loan market is a cause for concern. In particular, the subprime auto-loan market looks nothing like the mortgage market before the Great Recession.

Newly delinquent auto loans, as a percentage of current balances, have been falling over the past two years, and the fact that a record number of Americans have a bad auto loan on their credit record is a testimony to economic history more than current loan practices and economic conditions, particularly given the rapid rise in total car sales during this period.

Indeed, risk-based pricing in the auto loan market appears to be supplying a steady flow of credit to low-rated borrowers without imposing excess stress on the financial system.

About the Authors

Michael Mandel is Chief Economic Strategist of the Progressive Policy Institute.

Douglas Holtz-Eakin is President of the American Action Forum.

Thomas Wade is Director of Financial Services Policy of the American Action Forum.

Projections published today by the non-partisan Congressional Budget Office confirm that the federal government is on course to spend $1 trillion more than it raises in revenue in Fiscal Year 2020. Trillion-dollar deficits continue as far as the eye can see, with CBO estimating a 10-year deficit of over $13 trillion.

Legislative changes since August have increased projected deficits by more than $500 billion, according to CBO. More than 90 percent of the increase comes from a package of irresponsible tax cuts added to a year-end spending agreement passed in December. But most of the change was offset by a decline in the projected interest rates and other technical changes, leaving 10-year deficit forecasts “only” $160 billion more than they were in August 2019.

What’s driving these deficits? Primarily the growth in federal health-care and retirement programs caused by our ageing population. Federal spending on Social Security, Medicare, and other health programs is projected to grow from 11 percent of gross domestic product today to 14 percent in 2030. All other non-interest spending, meanwhile, is projected to shrink as a percentage of GDP. Revenue won’t keep up with these costs, in large part because the Trump administration keeps charging tax cuts upon tax cuts to the national credit card. If anything, CBO’s projections are overly optimistic because the agency is required to assume most of these tax cuts expire in 2025 as they are scheduled to under current law.

Ben Ritz, the Director of PPI’s Center for Funding America’s Future, presented to students during two breakout sessions at the New England College Convention in Manchester, New Hampshire this week. The first session was a joint presentation about the national debt as an intergenerational issue with Bob Bixby from The Concord Coalition and Brian Riedl from the Manhattan Institute. The panelists spoke with local radio host Chase Hagaman about their presentation on his show, Facing the Future, which airs on New Hampshire’s WKXL station and can be found at the link below. Hagaman also moderated a second session in which Ben discussed with students the public investment proposals presented so far in the presidential campaign, how candidates would fund their agendas, and the impact these plans would have on young Americans.

Congress voted this week for a $1.9 trillion tax and spending deal, over a quarter of which was added to our $23 trillion national debt. Thanks to this and other fiscally irresponsible legislation signed into law by President Donald Trump, the federal government will run an annual budget deficit of over $1 trillion this year and every year that comes after it. Yet of over 500 questions asked throughout six presidential debates, not a single one has raised the issue.

The House of Representatives earlier this afternoon passed two bills to provide $1.4 trillion in funding for defense and non-defense spending programs that must be appropriated on an annual basis. As is often the case with must-pass legislation at the end of the year, these bills have become “Christmas trees” decorated with various policy riders and pet projects for members of both parties in Congress. What are the major provisions attached to this legislation that help add $500 billion to its price tag, and should they put Congress on the naughty or the nice list?

The Director of PPI’s Center for Funding America’s Future, Ben Ritz, joined personal-finance advisor Ric Edelman on his nationally syndicated radio show to discuss the challenges facing Social Security, their role in the 2020 election, and PPI’s proposal to strengthen the program for future generations. Listen to the interview below and read our full plan here.

A new report from the Congressional Budget Office projects federal budget deficits between 2019 and 2029 to be $872 billion higher than was projected just three months ago. As a result, Donald Trump will be forced to campaign for re-election next year with his government running a trillion-dollar deficit. Democrats should hold the “king of debt” accountable for his inability to manage the nation’s finances and present voters with a compelling alternative: a new progressivism that invests in our country without burying young Americans under a mountain of debt.

The increase in CBO’s deficit projections is largely due to the bipartisan budget deal signed into law this month and other spending policies enacted over the summer, which CBO says together will cost nearly $2 trillion – making them almost as expensive as the tax-cut bill enacted by Trump and the Republican-controlled Congress in 2017. Projected deficits also increased by almost $280 due to technical changes in CBO’s modeling. Partially offsetting these costs was a reduction in CBO’s forecast for interest rates, which brought projected deficits down by a whopping $1.4 trillion.

That a change of less than one percentage point in interest rates can cost nearly as much as the budget deal or the Trump tax cuts is a testament to the size of our national debt on which that interest is owed. The $16.5 trillion debt (which grows to almost $22.5 trillion if one includes intragovernmental debt such as that owed to the Social Security and Medicare Trust Funds) will only become worse moving forward as the government is projected to spend $1 trillion more than it raises in revenue every single year from 2020 onward if current laws remain unchanged.

The Canadian App Economy is strong both in terms of app exports and compared to its industrialized peers. The Canadian App Economy has 262,000 App Economy workers as of November 2018, according to a recently released report by the Progressive Policy Institute (PPI). App Economy workers are those that develop, maintain, or support mobile applications. What’s more, Canada is outperforming many of its industrialized peers.

During the most recent Facing the Future, Ben Ritz discussed PPI’s latest policy proposal, “A Progressive Budget for Equitable Growth.” The blueprint addresses a variety of issues, such as the national debt, taxes, health care, infrastructure, climate change, and more.

WASHINGTON—The Progressive Policy Institute and House Blue Dog Coalition will host a lunchtime discussion today at the Longworth House Office Building about what leaders in Congress can do to invest in equitable growth while reducing our national debt.

America suffers from a shortsighted fiscal policy that promotes consumption today instead of investing in tomorrow. The federal government now spends more to service our growing national debt than it does on public investments in education, infrastructure, and scientific research combined. Meanwhile, a perfect storm of fiscally irresponsible tax cuts and an unwillingness to tackle escalating health and retirement spending are feeding trillion-dollar deficits as far as the eye can see. This is not a fiscal policy for strengthening America’s future – it’s blueprint for American decline.

At the event, PPI will release a comprehensive budget plan with over 50 policy recommendations for the next administration to make room for public investments in education, and infrastructure, and scientific research; modernize federal health and retirement programs to reflect an aging society; and create a progressive, pro-growth tax code that raises the revenue necessary to pay the nation’s bills.

Lunch will be provided. This event is open to the press.

Who:

Rep Stephanie Murphy (D-FL), Co-Chair of the House Blue Dog Coalition

Rep. Ed Case (D-HI), Co-Chair of the Blue Dog Task Force on Fiscal Responsibility and Government Reform

Rep. Ben McAdams (D-UT), Co-Chair of the Blue Dog Task Force on Fiscal Responsibility and Government Reform

Ben Ritz, Director of PPI’s Center for Funding America’s Future

Marc Goldwein, Senior Vice President at the Committee for a Responsible Federal Budget

Emily Holubowich, Executive Director of the Coalition for Health Funding and Co-Founder of NDD United

Will Marshall, President of PPI, Moderator

When: Thursday, July 25, 2019

12:00 PM – 1:30 PM

Where: Longworth House Office Building, Room 1302

15 Independence Ave, SE

Washington, D.C. 20515

For press inquires, please contact Carter Christensen, media@ppionline.org or 202-525-3931.

The budget deal scheduled for a vote tomorrow gets two things right and nearly everything else wrong. The main thing it gets right is the need to unshackle domestic public investment that would be subject to an across-the-board cut known as “sequestration” in the absence of legislative action. It also suspends the federal debt limit for two years, which will allow the Treasury Department to continue paying the bills America has already incurred without risking the prospect of a catastrophic default on our debts. What it gets wrong is charging $320 billion in new spending to our national credit card, which will further grow those debts and so perpetuate Washington’s governing dysfunction.

“Health care and poverty are inseparable issues and no program to improve the nation’s health will be effective unless we understand the conditions of injustice which underlie disease. It is illusory to think that we can cure a sickly child and ignore his need for enough food to eat.” Robert Kennedy, 1968

Reframing the 2020 Health Care Debate by the Honorable John A Kitzhaber, M.D.

Last month’s Democratic debates demonstrate how central health care will be in the 2020 election. Indeed, health care, more than any other issue, propelled the Democrats to regain control of the House of Representatives in 2018. Whether the upcoming election leads to meaningful relief for the millions of families struggling under the escalating financial burden of medical care, however, depends largely on how the issue is framed and on the clarity with which we see our policy goal and the steps necessary to achieve it.

Today the vast majority of dollars in our health care system are spent on the after-the-fact treatment of acute and chronic medical conditions rather than on investments that could prevent these conditions in the first place.

If we could reduce our health care spending from the current 18 percent of the GDP to the 12 percent average of most other industrialized nations, it would free up well over a trillion dollars a year for the social investments that actually improve health (1).

What concerns voters most about health care and, by a wide margin, is the cost — but, and this is important — not the cost of the overall U.S. health care system, but the cost to them as individuals (2). Most voters believe, to some extent in the abstract, that everyone should have access to affordable health care, but they are far more concerned that they as individuals have access to affordable health care. This is understandable because, at the end of the day, health care is intensely personal.

And yet, it is fair to say that nobody wants to need medical care or to be a “patient.” When you are sick or injured it is important that you have timely access to care at a cost you can afford, but we also know that among the factors contributing most to lifetime health status, our medical system is a relatively minor contributor. Far more important are things like healthy pregnancies, affordable housing, nutrition, stable families, good jobs, safe communities and the other “social determinants of health” (3),(4).

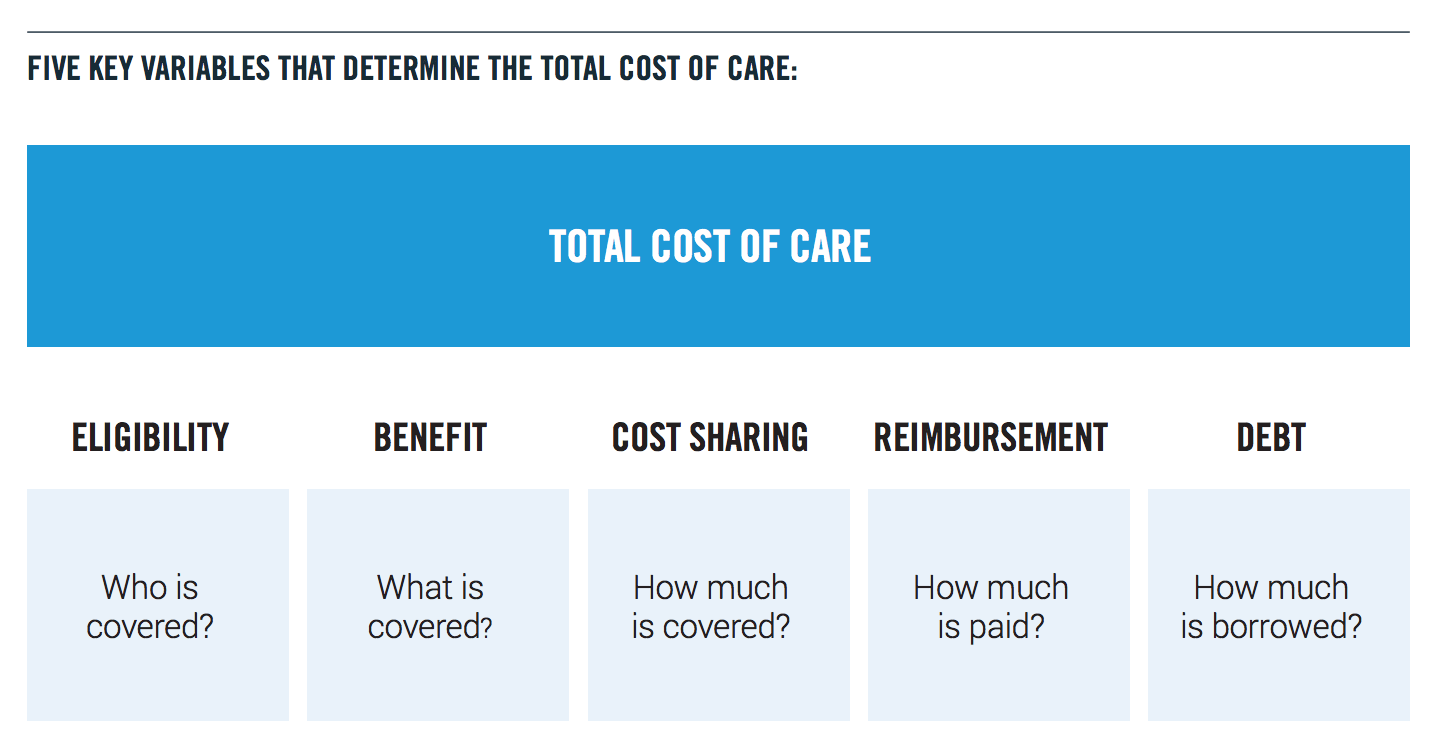

Therefore, our policy goal should be to improve the health of our people through a system that is financially stable, ensures that all Americans have timely access to effective, affordable, quality medical care; and also makes, strategic long-term investments in the social determinants of health. A system that can achieve this goal must include five core elements: 1. Universal coverage; 2. an affordable defined benefit; 3. a delivery system that assumes risk and accountability for quality and outcomes; 4. a global budget indexed to a sustainable rate of growth; and 5. savings reinvested upstream in the community to address the social determinants of health.

A system that incorporates these elements can take many forms, but without all five we cannot achieve our goal of improving health care in a financially sustainable way.

The most significant obstacle to achieving this goal is the total cost of care and the structure of the delivery system that is driving it. Health care is the only economic sector that produces goods and services none of its consumers can afford. Such a system only works because the care for individuals is heavily subsidized—increasingly with public resources—either directly through public insurance programs like Medicare and Medicaid; or indirectly through the tax exclusion for employer sponsored health insurance; and the public subsidies for those purchasing insurance through the Affordable Care Act (ACA) exchanges.

For decades, the national health care debate has been focused on these subsidies—on who pays them and how much they pay—rather than on why health care costs are so much in the first place. The political paralysis around this issue is due largely to the fact that neither Republicans nor Democrats assume any change in the health care delivery model: we either pay for it or we don’t, creating a false choice between cost and access. Republicans want to spend less on health care (e.g. “repeal and replace” the ACA) while Democrats want to spend more (e.g. Medicare for All). Neither approach directly addresses the total cost of care.

The burden of rising health care costs on individuals manifests itself in a variety of ways: rising insurance premiums and deductibles, short-term insurance policies that actually cover very little, the denial of coverage based on preexisting medical conditions, surprise billing, and the high cost of prescription drugs. It is not surprising, then, that most Democratic voters blame insurance companies and drug companies for the high cost of care. Generally, consumers do not blame health care providers, the delivery system itself, or the many new health care related startups and huge private equity firms that are making a profit off the $3.5 trillion health care budget (5).

And while Democrats are right to go after short-term junk health insurance policies, huge drug price increases, and surprise health care bills, these fixes only address shortcomings with health insurance rather than the total cost of medical care. The total cost of care is the primary driver of increases in insurance premiums as well as the increase in copayments and deductibles.

Since none of the current proposals address the systemic cost of care, they cannot prevent cost shifting onto individuals. All of these short-term fixes are worth making, but they are treating symptoms of the problem, not the problem itself.

The problem is illustrated by viewing our health care system through the lens of five questions or “variables”: 1. who is covered (eligibility); 2. what is covered (benefit); 3. how much is covered (cost-sharing—e.g. premiums, copayments, deductibles); 4. how much are we paying (reimbursement); and 5. how much is borrowed (debt financing).

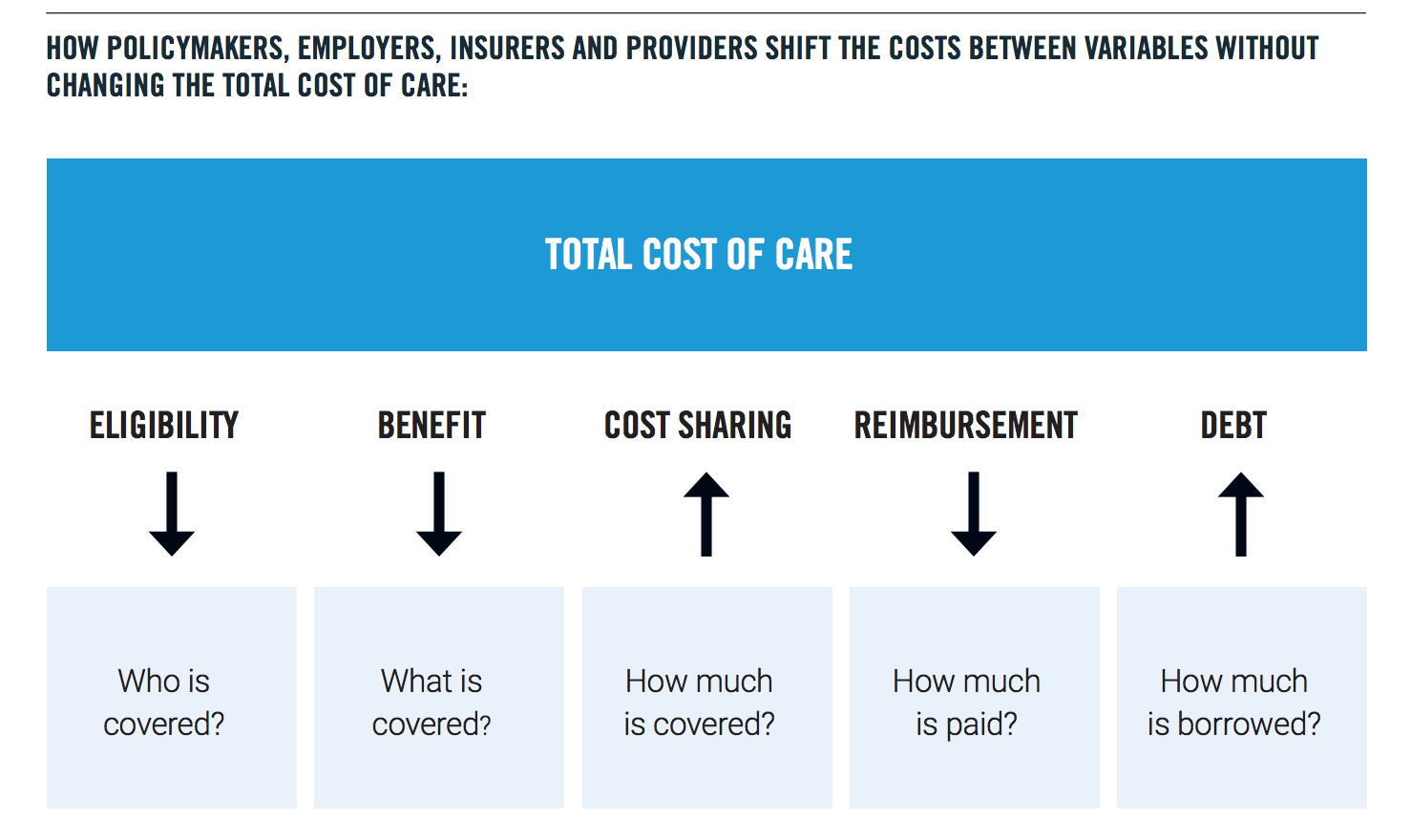

When the total cost of care exceeds the ability/ willingness of the major third-party payers (government and private sector employers) to pay for it, instead of seeking to reduce the cost of care, payers use one of five strategies to shift the cost to individuals who cannot afford it; or to future generations. These strategies include: reducing eligibility, reducing benefits and/or raising premiums, copayments and deductibles— all of which shift cost to individuals; reducing provider reimbursement which often results in efforts by providers to avoid caring for those who cannot pay; and pushing the cost of care into the national debt, shifting cost to future generations.

Cost shifting is the way we avoid directly confronting both the reality of fiscal limits and the fact that health care in the United States has simply become unaffordable for individuals, employers and the government. Cost shifting does not reduce the total cost of medical care. Furthermore, at 18 percent of our GDP, the cost of medical care, more than anything else, is undermining our ability to invest in children and families, housing, economic opportunity and the many other things that contribute to health. This is the primary reason why the U.S. has such embarrassingly poor population health statistics when compared to other industrialized nations that spend far less on medical care and far more on the social determinants (6).

The one indispensable step in moving toward a realistic and effective solution is to cap the total cost of care through a global budget indexed to a sustainable annual growth rate, while requiring providers to assume financial risk and accountability for quality and outcomes within that budget. Taking this step will fundamentally shift the debate from the subsidies to the delivery system. As long as we allow an ever-increasing share of our public resources to be spent paying whatever prices are demanded—whether for prescription drugs, hospital care or to grow profits of private equity funds—American families will continue to struggle under the burden of medical costs and this crisis will deepen.

Capping the total cost of care will allow us to expand coverage for a basic benefit package to all Americans (universal coverage); and to begin to invest upstream in the social determinants of health. The only way to expand access and to make room in the federal budget for serious investment in the social determinants of health is to reduce the total cost of care.

We already have two very successful examples of how global budgets work to bring down the total cost of care: Oregon’s Coordinated Care Organizations, which manage the state’s Medicaid program, and Medicare Advantage, that today serves more than 20 million seniors. Under these care models, providers receive a fixed amount of money for a defined population, without sacrificing quality (7). If the global budget is exceeded in any given year, the providers are at financial risk for the difference. In short, these care models begin to change the system incentives from rewarding sickness to rewarding wellness.

Extending these models more broadly across the U.S. health care system will reduce the total cost of care and free up resources to invest in the social determinants of health. It’s not necessary at this point in the 2020 election cycle to be prescriptive about how providers, insurers and other stakeholders in the current system will operate under a global budget cap indexed to a sustainable growth rate, but setting a target effective date for such a cap would fundamentally change the nature and the focus of the health care debate from where we want to go to how we are going to get there.

That is exactly what President John F. Kennedy did in 1962, when he challenged the nation to put a man on the moon. He did not give us a roadmap, he gave us a destination and, in so doing, unleashed American ingenuity and technological innovation to serve a common cause. Fifty years ago, this month, we achieved that goal. We succeeded in going to the moon because we were clear on our destination and because we imagined it; because the story preceded the accomplishment.

Surely, we can imagine linking the total cost of medical care to a sustainable growth rate within the next few years, then work backwards to create a health system that meets the objectives of both Democrats and Republicans: expanding coverage and improving health and quality; while reducing the rate of medical inflation through fiscal discipline and responsibility.

That’s the challenge. It’s not a challenge of technology—it is a challenge of political will and human compassion. And it’s not nearly as difficult as going to the moon.

Stuart M. Butler, Dayna Bowen Matthew, and Marcela Cabello, “Re-balancing Medical and Social Spending to Promote Health: Increasing State Flexibility to Improve Health Through Housing,” February 2017. https://www.brookings.edu/blog/usc-brookings-schaeffer-on-health-policy/2017/02/15/re-balancing-medical-and-social-spending-to-promote-health-increasing-state-flexibility-to-improve-health-through-housing/

Ashley Kirzinger, Cailey Muñana, Bryan Wu, and Mollyann Brodie, “Data Note: Americans’ Challenges with Health Care Costs,” The Henry J Kaiser Family Foundation, June 11, 2019, https://www.kff.org/health-costs/issue-brief/data-note-americans-challenges-health-care-costs/

Len M. Nichols and Lauren A. Taylor, “Social Determinants as Public Goods: A New Approach to Financing Key Investments in Health Communities,” Health Affaits, August 2018,https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2018.0039

Ara Ohanian, “The ROI of Addressing Social Determinants of Health,” American Journal of Managed Care, January 11, 2018, https://www.ajmc.com/contributor/ara-ohanian/2018/01/the-roi-of-addressing-social-determinants-of-health

Rabah Kamal and Cynthia Cox, “Total health expenditures have increased substantially over the past several decades,” Peterson-Kaiser Health System Tracker, December 10, 2018, https://www.healthsystemtracker.org/chart-collection/u-s-spending-healthcare-changedtime/#item-total-health-expenditures-have-increased-substantially-over-the-past-several-decades_2017

Carlyn M. Hood, Keith P. Gennuso, Geoffrey R. Swain, Bridget B. Catlin, “County Health Rankings: Relationships Between Determinant Factors and Health Outcomes,” American Journal of Preventive Medicine, 2015. https://www.countyhealthrankings.org/sites/default/files/Hood_AmJPrevMed_2015.pdf

The Institute of Medicine defines quality as “the degree to which health care services for individuals and populations increase the likelihood of desired health outcomes and are consistent with current professional knowledge.”

The U.S. economy recently marked 10 years of economic expansion – its longest in history – but there’s an important exception: new business creation. In recent decades, the American entrepreneurial engine has decelerated. Regulatory reform could help revive American entrepreneurship, reducing the burden on new businesses and realizing gains in economic growth. That doesn’t necessarily mean deregulation, but rather streamlining and updating old or obsolete rules to provide entrepreneurs with flexibility in today’s fast-changing world.

New and young businesses are the foundation of the United States’ economy, creating jobs and spreading wealth across our society. “Together, startups and high-growth firms (which are disproportionately young) account for about 70 percent of firm-level gross job creation in a typical year,” write entrepreneurship researchers Decker et al. Many of these young companies go on to become the next generation of small businesses, which employ 48 percent of private sector employees.

Unfortunately, the rate at which new businesses are being created has fallen off in the wake of the Great Recession. While firm deaths have returned to their pre-recession levels, firm births are down 22 percent compared to 2006 levels. And, for the first time since the Census Bureau began collecting data, firm deaths exceeded firm births from 2009 to 2011.

Smart policy can help increase the number of new businesses that are created and the number that scale up, though. Regulation is one area where policy can be made more efficient. A 2017 National Small Business Association survey estimated that the average small business owner spends at least $12,000 every year on compliance, with nearly one in three spending more than 80 hours every year dealing with federal regulation.

We know from research by Victor Bennett and Ronnie Chatterji that many people have entrepreneurial aspirations, but fail at many steps along their path to move to actual business formation. While many fail at early stages, such as basic market research, others undoubtedly run up against these mountainous regulatory costs and say, “not worth it.”

One way to reduce these costs is to focus on the steady buildup of regulation, or regulatory accumulation. The Code of Federal Regulations, where rules promulgated by the federal government are published annually, swelled by 17 percent from 2008 to 2018 alone. While Washington has dozens of agencies that issue new rules, not one institution is dedicated to streamlining the accumulated body of regulations. That’s why PPI proposed the Regulatory Improvement Commission (RIC). The RIC would fill an institutional vacuum in regulation policy by creating a mechanism for the periodic clearing out of obsolete rules.

Modeled on the Base Realignment and Closure Commission (BRAC) and comprised of a bipartisan group of highly qualified stakeholder appointees, the RIC would be an independent commission of eight members, appointed by the President and Congress, with regulatory expertise across industry and government. It would meet as authorized by Congress to review and, following a public comment period of 60 days, draw up a list of 15 to 20 rules for elimination or modification. The package would be sent to Congress for an up-or-down vote, and the RIC would be disbanded. If the proposed changes pass Congress, they would go to the president’s desk for signature or veto.

In 2015, bipartisan groups of lawmakers introduced bills in the House and Senate to establish the RIC based on the BRAC model. House cosponsors included Mick Mulvaney (R-SC), now acting White House Chief of Staff, and Kyrsten Sinema (D-AZ), now a Democratic Senator from Arizona.

Startup-friendly policies such as the RIC can help reduce compliance and opportunity costs, catalyzing a rebound in America’s startup rate and spurring economic growth. Streamlining regulation would help inventors and entrepreneurs spend less time and resources on regulatory compliance and focus instead on delivering goods and services and scaling their enterprises.

Research assistance was provided by Roman Darker, economics intern at the Progressive PolicyInstitute.

If you think your credit report is accurate, there is a good chance you are wrong. According to the Federal Trade Commission (FTC), one in five Americans has a potentially material error in their credit file, and one of the biggest contributors is medical bills—with half of all medical bills containing an error.

In fact, mistakes on credit reports have become so pervasive that around a third of all complaints filed annually to the Consumer Financial Protection Bureau (CFPB) resulted from problems with consumer credit reports.

Credit report errors are a serious threat to the financial well-being of American families. As Senator Elizabeth Warren has noted, “credit reports regularly contain errors that can make it harder for families to access credit, find jobs, and get housing.” And as many consumers know all too well, it’s very difficult to get those errors corrected.” (1)

Under the Fair Credit Reporting Act, the company that furnished the information to the credit bureau must conduct an investigation to verify the information and correct a mistake, if they find one. Unfortunately, consumers who want to try to fix mistakes on their credit report face three daunting obstacles.

First, the system put into place by the credit reporting agencies heavily favors creditors and other data furnishers. Credit bureaus almost exclusively depend on lenders (such as banks, credit unions, credit card providers, and mortgage underwriters).

Consumers contacted the credit reporting agencies approximately eight million times in 2011 to initiate a credit dispute. But only a small fraction of those disputes was resolved internally by credit bureau staff. According to the CFPB, 85 percent of credit report disputes are passed on to data furnishers (the lenders) to investigate and resolve. (2) Unfortunately, in most cases the disputes are then shelved unless the consumer perseveres.

Second, the credit report agencies earn their profits by providing services such as credit checks to the very entities that provide the data used to create the credit reports – banks, mortgage lenders, credit card companies, retailers, and other businesses that provide credit. This creates a serious conflict of interest.

Third, despite several notable efforts to try to empower consumers, trying to correct errors on your credit report is still tedious, confusing, and time consuming.

CREDIT REPAIR ORGANIZATIONS AND COMPANIES

Because the system is rigged against them, many consumers turn to credit counseling agencies or credit repair companies. The dispute system designed to help consumers fix the problem favors the position of the debt collector over the consumer. Specifically, the credit bureau is only legally required to check with the creditor or debt collector and ask them whether they stand by their claim. As long as the creditor says you owe money, the dispute is resolved in their favor. As the National Consumer Law Center concludes: “Credit bureaus have little economic incentive to conduct proper disputes or improve their investigations.” (3)

Credit counseling agencies are typically a free resource from nonprofit financial education organizations that review your finances, debt and credit reports with the goal of teaching you to improve and manage your financial situation.

A credit repair company is a firm that offers to improve your credit in exchange for a fee. Unfortunately, the quality of these firms varies greatly. Some credit repair firms are highly reputable and follow best practices. Unfortunately, a significant cohort of credit repair firms are not good actors and, in some cases, have committed outright fraud. In 2016 the Consumer Financial Protection Bureau (CFPB) stated that “more than half of people who submitted complaints with the CFPB about credit repair chose the issue ‘fraud or scam’ to describe their complaints.”

There are some telltale signs for consumers trying to separate the bad actors from legitimate credit repair firms. Companies should be avoided that:

Demand an upfront payment.

Don’t provide a written agreement that includes cancellation rights for consumers.

Guarantee they’ll raise your credit score or fix an error.

Have multiple complaints against them with the Consumer Financial Protection Bureau or the attorney general’s office in the state where they operate.

Suggest they can remove legitimate negative information.

Offer to create a new credit profile based on a new employer identification number, rather than your Social Security number.

In contrast, responsible credit repair companies not only follow federal and state law but also:

Offer a free consultation

Have a track record and consistently solid reviews from past clients.

Have an attorney on staff.

Are licensed, bonded and insured.

WHAT NEEDS TO CHANGE?

To protect consumers, some policymakers have suggested new regulations to further police the credit repair industry. They note that credit repair firms don’t do anything someone with a bad credit report couldn’t do on their own. Anyone can dispute credit errors on their own behalf. But the Do-It-Yourself approach can be dauntingly complicated and time-consuming for harried families.

In essense, paying for credit repair assistance is really no different than paying an accountant or purchasing software to do your taxes – something 90 percent of Americans do according to the Internal Revenue Service.

It is important to note that there is already existing legislation to regulate the credit repair system. The Credit Repair Organizations Act (CROA) was signed into law in 1996 to protect consumers from the unscrupulous practices commonly used by several credit scammers.

Because of CROA, credit repair organizations are not permitted to misrepresent the services they provide, including guaranteeing the removal of negative credit listings. Credit repair organizations are also not permitted to attempt to create a “new” credit file or advise you to lie about your credit history. The Act also bars companies offering credit repair services from demanding advance payment, gives consumers certain contract cancellation rights as well as the right to sue a credit repair organization that violates CROA. (4)

CROA is a sensible law, and despite criticisms that it does not go far enough in regulating the credit repair industry, the law does provide consumers with protections against bad actors in the credit repair sector without eliminating legitimate credit repair firms. CROA needs strengthening, not in the form of new regulations but rather more effective enforcement.

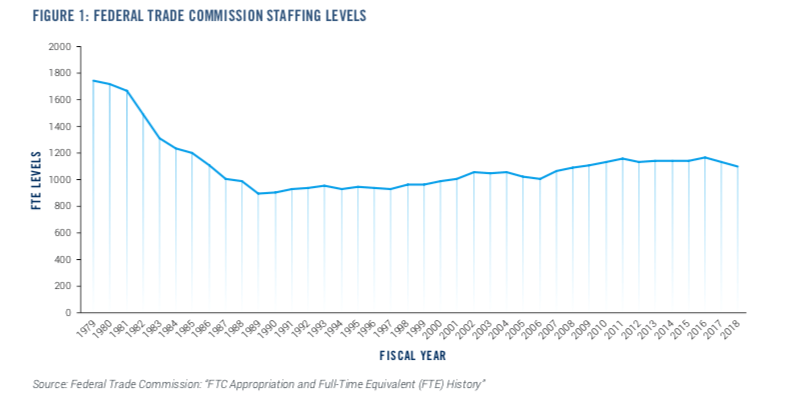

Under CROA, the Federal Trade Commission (FTC) is the primary enforcement body at the federal level. The problem is the FTC is severely underfunded and understaffed. In a Senate hearing last year Commissioner Rebecca Slaughter said the FTC’s staff level is 50 percent below its level at the beginning of the Reagan administration in 1981. Senators Jerry Moran (R-Kan.) and Catherine Cortez Masto (D-Nev.) agreed the FTC needs more resources and is “understaffed.” (5)

As Table 1 confirms, FTC staffing levels dropped dramatically during the 1980s and have never really recovered. Yet, over the same time, the responsibilities of the agency have dramatically changed and expanded. Today the FTC has to address some 2.7 million complaints a year in areas from debt collection, to identify theft, to imposter scams. (6)

Better enforcement of CROA would obviate the need to pile on new rules. Unfortunately, in fact, Congress has added to the FTC’s workload even as its workforce has shrunk. The simplest solution is to provide the FTC with additional resources dedicated to enforcing CROA and protecting consumers from those credit repair companies that have acted fraudulently or in bad faith.

To pay for this increase in supervisors, a small annual fee could be placed on the credit reporting agencies (Equifax, TransUnion, and Experian). To create an incentive for these agencies to be more responsive to consumer complaints about credit reporting agencies, the fee could be lowered or raised in synchronization with the number of consumer complaints about their credit reports.

OTHER REMEDIES

Another approach to fixing the current system is to go to the source of the problem, eliminating some of the causes for the extraordinary amount of errors made by the credit reporting industry. As Aaron Klein of the Brookings Institution has noted, there are three major reasons why credit scores are so inaccurate: “size, speed, and economic incentives of the system.”

One way to change the incentive structure would be to create some consequences for credit rating companies that frequently give lenders inaccurate data about borrowers. Lawmakers could consider legislation that would penalize credit reporting agency error rates above a certain level. Klein’s approach would use a random sample method (5 to 10 percent of complaints) to review credit rating firms’ performance. Another approach would be to grade the credit bureaus on their error and response rates.

CONCLUSION

While it is tempting to lump all credit repair firms into the same basket, many of these firms act in good faith and follow CROA to the letter of the law. Yet there is no doubt that a significant number of these companies are misleading consumers and sometimes acting fraudulently. If lawmakers really want to crack down on these bad actors, however, the first step should be strengthening enforcement of existing law.

Otherwise, spawning new laws and regulations would likely enmesh all credit repair firms in new layers of regulatory complexity and compliance burdens, making it even harder for consumers to detect and correct errors on their credit reports. In CROA we have the consumer protection law we need, now it’s time to focus on oversight and enforcement.

Many of the Democratic presidential candidates are vying to see who can be toughest on the tech sector. But here’s the paradox: New data shows that the tech boom is a major force driving down unemployment, lifting economic growth, and helping voters — precisely the people that the Democratic candidates are trying to reach.

The key here is that the economic data produced by the government is not typically presented in a form that easily shows the benefits of the tech boom. Software firms, for example, are spread across at least three different industries. Ecommerce — related activities are spread across at least two industries, electronic shopping and warehousing. And telecom includes at least two three industries, telecom services, communications equipment, and data processing and hosting.