The coronavirus pandemic has opened some gaping holes in our nation’s social safety net, especially where hunger and malnutrition are concerned. Millions of low-income workers have lost their jobs (and will soon lose expanded unemployment benefits if Congress fails to extend them) and millions of children in low-income families have lost access to school meals because the K-12 system has shutdown. These twin blows have triggered a dramatic rise in hunger and food insecurity in America.

Even before the pandemic hit, an estimated 37 million people, including 11 million children, reported experiencing food insecurity or hunger. Unless Covid-19 is contained, that estimate could reach 54 million by the end of 2020.

America’s most vulnerable populations – poor families with children, Black Americans, Hispanics and those living in rural areas and the South – are disproportionately affected by food insecurity and hunger. Their school-aged children also are more likely to rely on free and reduced-price school meals to meet their nutritional needs.

In March, Congress passed the Families First Coronavirus Response Act, which provided emergency food assistance and authorized the U.S. Department of Agriculture and the states to adapt the Supplemental Nutrition Assistance Program (SNAP, formerly food stamps) to meet the needs of the hungry during the crisis. According to a Center on Budget Policy Priorities report, almost all states have taken advantage of the flexibility the Act provides to maintain SNAP benefits to households with children missing school meals.

Before Covid-19, the national school lunch program on average served nearly 29 million students, and the school breakfast program served nearly 15 million students. When the schools closed in March, many school districts scrambled to keep feeding their students, by establishing “Grab and Go” sites for picking up meals, or establishing daily meal delivery routes using buses to deliver food rather than transport students.

Despite these improvisations, however, most school aged children apparently are not receiving as much food as they did before their schools closed. For example, a survey of school nutritional professionals found that 80 percent of school districts reported serving fewer meals since school closures. Of those districts, 59 percent have seen the number of meals served drop by 50% or more.

In response to the K-12 shutdown, the Families First Act created the Pandemic Electronic Benefit Transfer program that provides food to families that have lost access to free and reduced-priced meals. This one-time meal replacement benefit is added to an existing electronic benefits transfer card for families already receiving SNAP. Families with school-age children that don’t receive SNAP can also get a card.

SNAP historically has proven to be one of the nation’s most effective programs for providing low-income households with food during economic downturns. That makes it a powerful counter-cyclical policy tool. Research shows each $1 of SNAP benefits generates between $1.50 and $1.80 in total economic activity. Yet when Congress in April passed its next pandemic relief measure, the CARES Act, it increased more operational funding for SNAP operations but failed to increase SNAP direct benefits.

There are compelling moral and economic reasons why U.S. lawmakers should make offering more food aid a top priority as Covid-19 infections climb in most of the states, slowing economic recovery and causing more workers to file for unemployment. In the first place, hungry and malnourished people are more vulnerable to disease. There’s also a strong possibility that many K-12 students will not be able to go back to school in September, despite President Trump’s ill-considered calls for a general reopening. Additionally, by supporting food consumption by low-income families, more aid stimulates demand and keeps our stricken economy afloat.

To meet the immediate crisis, PPI endorses anti-hunger provisions of the HEROES Act that House Democrats passed in May, but is now blocked by Republican Senate Majority Leader Mitch McConnell. These include:

• Increasing the SNAP maximum benefit by 15 percent through September 30, 2021, which translates into an additional $25 per person each month;

• Raising the minimum monthly benefit from$16 to $30;

• Adding $3 billion for child nutrition programs; and,

• Extending the Pandemic Electronic Benefits program through the fall of next year.

MODERNIZING THE SAFETY NET

This is also the right time to look beyond the current crisis and ask how our country can build a more resilient system of social supports that can better protect our most vulnerable citizens against future pandemics and other emergencies.

“While it’s true that government safety net programs help tens of millions of Americans avoid starvation, homelessness, and other outcomes even more dreadful than everyday poverty, it is also true that, even in ‘normal times,’ government aid for non-wealthy people is generally a major hassle to obtain and to keep,” notes Joel Berg, CEO of Hunger Free America.

“Put yourself in the places of aid applicants for a moment,” Berg added. “You will need to go to one government office or web portal to apply for SNAP, a different government office to apply for housing assistance or UI, a separate WIC clinic to obtain WIC benefits, and a variety of other government offices to apply for other types of help—sometimes traveling long distances by public transportation or on foot to get there—and then once you’ve walked through the door, you are often forced to wait for hours at each office to be served. These administrative burdens fall the greatest on the least wealthy Americans.”

A survey of low-income households by Hunger Free America found that 42 percent said it was “time-consuming and/or difficult to apply” for Unemployment Insurance, and nearly a quarter said the same about applying for SNAP. In addition, “40 percent of respondents said they had problems reaching government offices while applying for SNAP, with 36 percent stating that they never received a call back after leaving

a message.”

To reduce the high “opportunity costs” of being poor in America, the federal and state governments should adopt modern digital technologies that help low-income families apply once for public benefits without having to run a bureaucratic gauntlet of siloed programs for nutrition, housing, unemployment, job training, mental health services, and more. Specifically, as Berg proposed in a 2016 report for PPI, governments at all levels should cooperate to create online accounts from which families can apply remotely for all the benefits they qualify for, and into which they can deposit their public assistance.

This proposal is the centerpiece of a new bill introduced by U.S. Reps. Joe Morelle (D-NY) and Jim McGovern (D-Mass) and Senator Kirsten Gillibrand (D-NY). The Health, Opportunity, and Personal Empowerment (HOPE Act) would fund state and local pilot projects setting up online HOPE accounts to make it easier for low-income people to apply for multiple benefits programs with their computer or mobile phone. In addition to saving them time, money and aggravation, HOPE accounts enable people to manage their benefits – effectively becoming their own “case manager” – and easing their dependence on often inefficient and unresponsive social welfare bureaucracies.

In keeping with former Vice President Joe Biden’s “Build back better” theme, expanding food aid now to stem a surge in hunger, while deploying digital technology to give low-income Americans more control over their economic security, can help us weave a stronger and more resilient social safety net, rather than simply plugging holes in the old one.

The federal government is on track to run a record-shattering $4 trillion budget deficit in 2020, in large part due to its aggressive fiscal response to the pandemic-induced recession. Some on the right have raised alarm about this borrowing, despite their support for budget-busting tax cut and border-control policies over the last three years. The hypocritical chorus will likely only grow louder if Democrat Joe Biden is elected president in November.

But temporary deficits are an invaluable tool for mitigating the damage caused by economic downturns, as government spending replaces a drop in demand from the private sector. The long-term fiscal costs of failing to support an economy with a double-digit unemployment rate would far exceed those of even the most overzealous stimulus measures. Necessary fiscal support should therefore continue as long as the economy remains hobbled by the coronavirus, no matter the cost.

However, Washington also faces structural deficits that will persist long after the pandemic has been contained. Thanks to the Trump administration’s reckless borrowing binge at a time when the unemployment rate was below 5 percent, the federal government was already projected to spend over $1 trillion more than it raised in revenue even before the pandemic hit. This structural deficit will only grow worse in the coming years because our nation’s aging population is causing federal spending on health-care and retirement programs to grow significantly faster than the revenues needed to finance them. The Trump administration did not create these problems, but it did make them significantly worse with its pre-pandemic fiscal policy and its disastrous handling of the public health crisis.

In the two years following the 2008 financial crisis, the national debt grew from less than 40 percent of gross domestic product to more than 60 percent of GDP. In 2020 alone, the debt will likely surpass the all-time high it reached following the end of World War 2 (106 percent of GDP). The rising cost of servicing this growing debt threatens to crowd out critical public investments that lay the foundation for long-term growth after the recession ends.

The federal government spent more money servicing the national debt last year than it spent on critical public investments in education, infrastructure, and scientific research combined. Although interest rates are low now, they eventually will rise as the economy recovers. Allowing interest payments on our debt to further crowd out these investments – which have already fallen by nearly 40 percent in real terms since the 1980s – would have disastrous consequences, including lower incomes, fewer high-quality jobs, and reduced economic mobility.

It is therefore essential to pay down the debt during expansions to create fiscal space for the necessary surge in short-term borrowing during recessions. Unfortunately, Washington has often waited too long to enact sufficient stimulus in response to recessions, and then failed to summon the will to narrow the structural gap between taxes and spending when the economy rebounds.

To make our economy more resilient against downturns, PPI proposes the federal government adopt a “fiscal switch” that automatically balances out the business cycle by increasing spending during recessions and recouping the cost during subsequent periods of economic growth. This switch would trigger based on economic variables such as the unemployment rate and operate through three mechanisms: a rebalanced relationship between federal and state governments, a more dynamic and progressive tax code, and phased-in reforms to mandatory spending programs driving our structural deficits. Implementing these automatic mechanisms, as recommended here and in PPI’s Emergency Economics report earlier this year, takes politics out of these decisions and ensures stimulus or deficit reduction will be implemented as warranted by economic conditions.

The first step is to better leverage the federal government’s unique borrowing capacity, which is unavailable to the vast majority of state and local governments required by law to balance their budget each year. Many government programs, including Medicaid, infrastructure, and education spending, are partnerships in which the federal government provides matching grants for state and local spending.

Some of these partnerships could be improved by allowing matching rates to adjust up or down automatically based on a state’s unemployment rate. This would prevent state and local governments from having to cut essential services during a downturn while asking them to shoulder a greater share of program costs when their budgets are healthy.

Other programs that currently function as a federal-state partnership but whose costs fluctuate significantly with the business cycle would benefit from becoming more nationalized. For example, when Congress tried to ensure that unemployment insurance replaced a minimum percentage of lost wages for everyone who was laid off in the early days of the coronavirus recession, lawmakers found they were unable to do so because of outdated operational infrastructure in a messy patchwork of 50 different state programs. As a result, policymakers were forced to settle for a controversial across-the-board benefit increase of $600 per week that gave some laid-off workers even more income from unemployment benefits than they lost in missed wages, while failing to make others whole. Even worse, Congressional squabbling over how long to maintain this benefit increase allowed them to lapse temporarily in the midst of an economic crisis.

Moving the operations of unemployment insurance and similarly-situated safety-net programs off state balance sheets and onto the federal government’s, in addition to automatically making benefits more generous during downturns and phasing them out in recoveries, would leverage Washington’s fiscal firepower in recessions when it’s needed most.

The second step is to make the income tax code more progressive, which serves as a strong automatic fiscal stabilizer by boosting average tax rates when incomes rise in expansions and lowering them when incomes fall in recessions. This objective could be accomplished by closing tax preferences for the wealthy, such as lower tax rates on inherited income and income from capital gains, while expanding the Earned Income Tax Credit and other pro-worker tax incentives. PPI also favors replacing the antiquated payroll tax with a dynamic value-added tax – which has a rate that automatically falls during recessions and rises during expansions – to encourage hiring and consumption when the economy needs it most and reclaim substantial revenues during economic expansions.

Finally, lawmakers must take additional measures to rein in the drivers of underlying structural deficits automatically when the fiscal switch calls for a pivot away from stimulus. Social Security and Medicare – the two largest programs in the federal budget – both face the prospect of becoming insolvent within the next decade, potentially leading to sudden and across-the-board benefit cuts for millions of seniors if lawmakers take no action to close the growing gap between dedicated revenue and scheduled benefits. Significant deficit reduction that takes effect in the middle of a recession could be catastrophic, but lawmakers should put in place a process now to develop and phase in a balanced package of revenue increases and benefit changes as the economy recovers. PPI’s Progressive Budget for Equitable Growth offers policymakers a model for how they can modernize these programs to strengthen work incentives, retirement security and financial sustainability in a way that is fair to both younger workers and older beneficiaries.

The right fiscal policy in a recession is not the right fiscal policy for an expansion, and vice versa. Washington politicians are often too slow or ideologically beholden to react sufficiently swiftly to changing economic circumstances. Taking these steps and creating a two-sided fiscal switch will give our government the tools it needs to manage the economy through both the ups and the downs of the business cycle.

Millions of America’s smallest businesses have been severely affected by the COVID-19 crisis. They’ve seen revenue evaporate and have been forced to lay off millions of workers. Over two million small businesses had simply disappeared by June 2020. The U.S. economy now finds itself in a deep hole, with millions of small businesses gone for good—and a dried-up pipeline of new business creation.

By the end of June, the American economy also was without tens of thousands of new “employer” businesses (those with employees) that normally would have been started. The pandemic and economic crisis have wreaked havoc on existing small businesses and the new start-ups that the economy depends on for job creation and innovation.

Meanwhile, the Trump administration’s implementation of the Paycheck Protection Program (PPP), authorized by Congress to provide billions in loan guarantees through the Small Business Administration (SBA), has been flawed. The Treasury department has provided insufficient, and constantly changing, guidance to lenders and businesses. The SBA’s own Inspector General found that the administration did not adhere to Congressional intent in deploying PPP funds.

Even before COVID-19, the Trump administration had proven itself incapable of inspiring entrepreneurial confidence. Business formation had trended steadily downward over the previous two years. According to a PPI analysis of Census Bureau data earlier this year, new business applications fell steadily from the middle of 2018, after rising more or less interrupted since 2012. Business applications that have a “high propensity” of turning into employer businesses had also fallen since the middle of 2018.

The picture gets worse the deeper you dig. The pandemic recession has disproportionately affected female, Black, and Latinx business owners. By April, the number of female-owned businesses had fallen by 25 percent (compared to 20 percent for male-owned businesses). The number of Black- and Latinx-owned businesses had shrunk by, respectively, 41 and 32 percent (compared to 17 percent for white-owned businesses).

These are astonishingly high losses and they come on top of a small business landscape already tilted against minorities and women. According to Census data, going into the crisis, Blacks owned just two percent of employer businesses in this country, despite comprising 13 percent of the population. Latinos and Latinas, making up 18 percent of the population, owned six percent of businesses. Male-owned businesses were larger and with higher revenues than female-owned businesses.

What’s needed now is a major national push to reinvigorate business creation and address underlying demographic disparities in business ownership. For women and minorities, when it comes to entrepreneurship, returning to the pre-crisis status quo is simply not an option. It shouldn’t be an option for the country, either. Greater business creation and ownership among women, Blacks, Latinx, and others will accelerate recovery and strengthen resilience.

Over the last 40 years, new businesses have, on average, created about six jobs per year, per company. If one million new Black and Latinx businesses opened (replacing the ones that have closed permanently) and were joined by half a million additional new businesses, we could see about nine million new jobs created. Not all these companies would survive—in the “normal” course of economic activity—but a significant subset of them would not only survive but also thrive. Young companies that survive and grow drive the lion’s share of net new job creation each year.

Public policy should seek to help stimulate new business creation and support the survival and growth of young businesses. The focus of this effort should be on women- and minority-owned businesses. Vice-President Joe Biden has proposed renewing the State Small Business Credit Initiative (SSBCI), an Obama-era program, to focus on these businesses. Evaluations of the SSBCI found positive effects in terms of investment and job creation, but a much larger effort is likely needed. The federal government has many tools at its disposal to be leveraged in support of new business formation and to aid specific types of entrepreneurs.

PPI believes the federal government should launch a National Start-Up Initiative that aims to spur creation of at least two million new businesses as our country recovers from the pandemic recession. It would include the following key actions:

Create a startup visa for founders of new companies. These would include foreign students graduating from a U.S. university, those transitioning out of Optional Practical Training, or any H1B visa-holder after three years. The foreign-born start companies at disproportionately high rates; encouraging them to do so would give a significant boost to overall business creation. This could be accompanied by incentives for business creation in specific geographic areas or neighborhoods.

Leverage federal research funding to reform technology commercialization processes at universities. America’s research universities are the best in the world at knowledge creation, yet their ability to turn knowledge into innovation and new companies has been declining. Many promising entrepreneurial ventures get stuck in bureaucratic processes. The federal government, which provides billions of dollars to support university research, should create new incentives for those institutions that devise more effective commercialization practices and generate new businesses for their communities.

Create a new “Start-Up Tax Credit” to encourage new businesses to grow into large businesses. Modeled on the Earned Income Tax Credit, the Startup Credit is designed to help these businesses avoid the scale-up trap unintentionally posed by tax breaks and regulatory exemptions for new enterprises. For example, businesses with fewer than 50 employees are exempt from the employer shared responsibility payment of the Affordable Care Act and providing unpaid leave. While these “carveouts” certainly help small businesses get off the ground, they impose an implicit tax when those companies grow past a certain threshold. The Startup Tax Credit would mitigate that tax.

As proposed by PPI economist Elliott Long, the Startup Tax Credit would be tied to the number of employees and payroll at a small business. Firms that have been operating for fewer than five years would be eligible for a credit equal to half the employer-side payroll tax they pay on their first 100 employees, up to a maximum credit of $1,200 per employee in 2020 (indexed to inflation). The proportion of payroll taxes offset by the credit and the maximum credit per employee would then gradually phase down as businesses grow until phasing out entirely once the business reaches 500 employees. PPI estimates this proposal would cost roughly $150 billion over 10 years.

PPI has also supported the New Business Preservation Act, introduced by Sen. Amy Klobuchar (D-MN). This would allocate $2 billion in federal funding to match private investments in areas of the country bereft of startup equity investments.

These steps would help seed the ground for new business creation, just as our country needs to create millions of them to provide jobs to U.S. workers whose previous jobs vanished in the pandemic shutdown. They would also create conditions that would make America’s entrepreneurial culture more vibrant and resilient against future public emergencies of all kinds.

As Covid-19 wreaks havoc in Southern and Sunbelt states, America’s battered economy faces a new round of shutdowns, bankruptcies and layoffs. Yet one sector seems strangely buoyant – the financial markets. From its all-time high in mid-February, the S&P 500 plummeted 34%, only to recoup all its losses by mid-June.

What explains Wall Street’s remarkable resilience while Main Street endures a punishing pandemic recession?

Although the three economic relief packages Congress has passed since the crises began no doubt have played a supportive role, the answer mainly lies in bold intervention by the Federal Reserve. The Fed played a similar role in staving off a financial collapse following the 2007-08 housing crisis. With a robust toolkit at its disposal, from slashing interest rates, purchasing securities, lending money directly and backstopping unstable markets, the Fed allayed investor fears about the impact of the Covid-19 lockdown on corporate profits and debts.

While Fed action to keep capital markets afloat is essential to prevent a wider economic implosion, it does have the unfortunate consequence of aggravating economic inequality. Only about 55% of Americans own stocks, and the top 1% percent own 50% of all equities. Pushing up stock prices, in other words, helps the rich get richer.

The progressive response to this distributional dilemma is not to let financial markets crash, but to democratize capital ownership in America.

U.S. policymakers therefore should emerge from the Covid-19 crisis resolved to tackle a growing “wealth gap” that is largely defined by race and ethnicity. According to the Urban Institute, the median wealth of white families in 1963 was $45,000 higher than the median wealth of nonwhite families. By 2016, the median wealth of white families had climbed to $171,000, or $132,600 more than the median wealth of black families ($17,400) and of Hispanic families ($21,000).

The strategy for narrowing the nation’s wealth gap has three key parts: Reduce racial and ethnic wage disparities, expand home ownership, and create new opportunities for Americans now locked out of capital markets to build financial assets that allow them to take advantage of the power of compound interest.

Focusing here on the third element, PPI endorses a radically pragmatic idea for democratizing capital ownership: Create lifetime savings accounts for all newborns, tied to voluntary national service. Here’s how these new “America Serves” investment accounts would work:

At birth, the federal government would stake every U.S. child to a $5,000 investment account similar to a government Thrift Savings Plan or a 401k. The money would be invested in a market index or target date fund to ensure the high average returns of investing in equities rather than low-return T-bills. With one stroke, this action would put America on the road toward universal capital ownership.

Families could also contribute post-tax earnings to their children’s accounts. No one could touch the funds in the account until the children turned 18. An “asset waiver” would also protect the account, preventing the income from being counted toward means testing for financial aid, food stamps, Supplemental Security Income (SSI), Social Security Disability Insurance (SSDI) or Medicaid.

Upon turning 18, account owners would face a choice. If they agree to perform a year of national service before they turn 25, they would be deemed 100% vested and could tap their funds after serving for specified purposes at tax advantaged rates. These include: post-secondary tuition, down payment on a first home, or starting a business.

Our goal is to start by engaging one million young adults in qualified domestic and international service programs (including active military), out of the roughly four million who turn 18 every year. Those who choose not to serve would be entitled to only the returns (and principal) on half the original stake — $2,500. The other half of their accounts would revert back to the taxpayers via the U.S. Treasury.

Although the governments’ upfront investment is considerable, over the long-term costs of America Serves accounts will likely decline. We estimate that the first 10 years would cost $230 billion, and a 25-year timeline sees total outlays of just under $700 billion.

It’s even possible that after 25 years, the program could become self-financed, depending on how many people choose to serve. Our projections are based on the assumption that one in four newborns will receive the full government contribution via service.

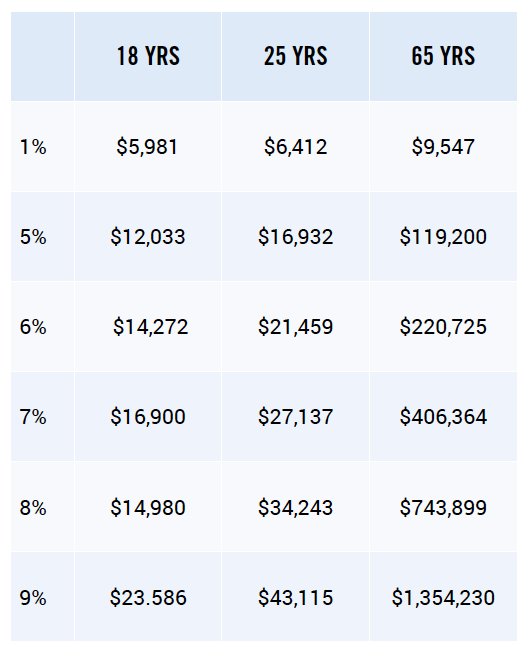

We use a historic average return rate on the S&P 500 of 8% for our assumptions. That means the $5,000 initial taxpayer contribution invested in the market grows to $34,250 after 25 years (See tables below). Assuming that one in four account holders choose to serve, the rest will be required to return to the U.S. Treasury half their savings – $17,125 (half the original government contribution plus market earnings.) That would be enough to stake three newborns with $5,000 contributions.

By creating a strong incentive to serve, this proposal – in the spirit of the World War II G.I. Bill — would link the opportunity to start building significant financial assets to civic responsibility. It would help to scale up voluntary national service and make it a more potent tool for public problem solving. Volunteers, for example, could assist in contact tracing during future pandemics, provide services to the swelling population of older Americans, help tutor low-income children, clean up public spaces, and much more.

A large national service program would also help our divided society bridge its class, racial and cultural divisions by bringing together youths from all backgrounds to engage in a common civic enterprise.

The organizing framework already exists: AmeriCorps and Peace Corps and other volunteer programs that operate under the aegis of the Corporation for National and Community Service (CNCS). The 75,000 yearly volunteers in these civilian service programs are in addition to the approximately 180,000 Americans who join the active duty military each year, and who would also qualify for full “America Serves” investment accounts.

The idea of expanding national service already enjoys bipartisan support in Congress. Senators Chris Coons, (D-DE), Roger Wicker (R-MS) and Cincy Hyde Smith (R-MS) recently introduced the CORPS ACT, which would increase from 75,000 to 150,000 in year 1, and up to 300,000 in years 2 and 3, the number of civilian national service slots.

“As we work to recover from the dual challenge of a public health crisis and an economic crisis, national service presents a unique opportunity for Americans to be part of our response and recovery while earning a stipend and education award and gaining marketable skills,”

Sen. Coons has said. “Expanding these programs to all Americans who wish to serve should be a key part of our recovery effort.” Another sponsor of the bill, Sen. Tammy Duckworth (D-IL), a Purple Heart military veteran gravely wounded in action, notes that “Just as picking up a rifle to defend our country is ‘American Service,’ so is helping out a food pantry for those at risk of hunger, assisting students with remote education and helping patients make critical health care decisions.”

WHY INVEST FUNDS IN THE MARKET?

Simply put, stock markets have been the most reliable generator of long-term wealth accumulation in history, and financial capital grows traditionally faster than wages. There have also been a series of innovations that have helped underpin the ability to efficiently and safely invest for the long term.

These include Index based, passive investing in target date ETF’s (Exchange Traded Funds), which essentially invest in a diverse basket of stocks or other assets such as commodities or bonds, and manages risk according to a future “target date” – usually when someone plans to retire. This passive investment approach diversifies the risk of any single stock plunging in value, and uses the ETF structure with minimal fees as opposed to active management models that assess much higher fees. Small investors get access to higher returns with less risk and keep more of their money as it grows.

To illustrate how “America Serves” investment accounts could grow, consider these projections of possible returns over 18, 25, and 65 years from an initial $5,000 contribution:

Let’s look at the standard market benchmark of the S&P 500, which since adopting 500 stocks to the index in 1957 has produced an annual return of 8% (through 2018). Yet, since stocks and bonds fall as well as rise in value, it is worth looking at the largest “drawdown” (market pullback) since that time. According to S&P Dow Jones Indices:

“the most significant market downturn occurred in the early 1970s, coinciding with the U.S. economy reeling from double-digit inflation courtesy of a quadrupling in oil prices. During this period, the S&P 500 declined by 45% over a 21-month period and took three and a half years to return to its previous local peak.”

This means that should the market be down in any given year, history shows us the largest pullback only took about 5 years to regain all its lost value. What that means is that by ensuring that every American has an opportunity to build a significant financial asset, this proposal would enhance their economic security and resilience in economic downturns from whatever sources.

CONCLUSION

The pandemic has thrown a harsh light on America’s economic and racial inequities. The government’s otherwise commendable efforts to keep the comatose U.S. economy from flatlining have had the unintended effect of making these disparities worse. By giving every newborn child a capital stake in America’s future, we will put our economy on a higher growth trajectory while also making it fairer. And by linking the accounts to service, we will create a powerful new incentive for young Americans to give back to their communities and their country.

(Note: The author would like to thank Alan Khazei, a longtime PPI friend and co-founder of Boston’s City Year voluntary service program, who with the late Harris Wofford and other leading national service advocates originally envisioned the link between “service bonds” and service.)

PPI President Will Marshall and Ben Ritz from the Center for Funding America’s Future are joined by Congresswoman Sharice Davis (KS-3) and Congressman Scott Peters (CA-52) for a conversation on the fiscal health of the United States, priorities for the upcoming stimulus bill, the election, and their perspective on how America’s economy can return with a resilient recovery.

Conservatives call the House Democrats’ Health and Economic Recovery Omnibus Emergency Solutions (HEROES) Act a “gigantic political scam.” Senate Republicans say HEROES, passed by the House on May 15th, is “dead on arrival when it reconvenes. As they negotiate with Democrats, Republicans should think carefully about certain student loan relief provisions in the bill.

Even in good times, a substantial portion of 45 million Americans’ paychecks go to student loan payments rather than to goods and services that keep our economy churning. There’s little doubt that this debt contributes to suppressed consumer consumption, which stifles economic growth. In this bad time, Americans collectively owe $1.6 trillion in student debt. This debt burden is now dramatically heavier with the economic shutdown and coming diminished post-pandemic employment opportunities.

Some say no additional student loan relief is needed because the Coronavirus Aid, Relief and Economic Security (CARES) Act that Congress passed in March temporarily suspended student loan payments. That would be a decent argument if CARES applied to everyone, but it doesn’t.

The U.S. House of Representatives is moving ahead with plans to vote today on the Health and Economic Recovery Omnibus Emergency Solutions (HEROES) Act: the fifth – and potentially final – a piece of major legislation addressing the coronavirus pandemic and its economic effects. The 1800-page bill is estimated to cost roughly $3 trillion and contains a mix of both good policies and bad but is perhaps most notable for what it leaves out: automatic stabilizers.

The biggest flaw with previous relief bills was that aid was limited by the availability of funds appropriated by Congress or arbitrary calendar dates it chose instead of being based on the real needs of our economy. As a result, measures like the Paycheck Protection Program (PPP) were exhausted within three weeks and many eligible businesses couldn’t get needed financial relief until Congress took additional action. The best way to prevent this problem in the future is by adopting “automatic stabilizers” — policies that cause spending to rise or taxes to fall automatically as predetermined economic or public-health benchmarks are met. For example, a proposal by Congressman Don Beyer and Senators Jack Reed and Michael Bennet would change the expansion of unemployment benefits included in the CARES Act to gradually phase out as the economy recovers instead of expiring arbitrarily on July 31st. The centrist New Democrat Coalition has also been vocal in calling on leadership to adopt automatic stabilizers in future relief bills.

Unfortunately, the HEROES Act doesn’t include any new automatic stabilizers – reportedly because House Speaker Nancy Pelosi is concerned about the bill’s $3 trillion price tag. On the one hand, Speaker Pelosi is right to be concerned about wasting taxpayer money on unnecessary expenses given our nation’s serious long-term fiscal challenges. But the unfortunate reality is that supporting our economy during the worst public health crisis of our lifetimes is a large and necessary expense. It is no less fiscally responsible to pass one $3 trillion bill than three $1 trillion bills if the money is efficiently targeted to support our economy throughout this pandemic. Moreover, there are a number of costly provisions included in the HEROES Act that are a poor trade-off for sacrificing automatic stabilizers.

The outbreak of COVID-19 (commonly known as coronavirus) has created a global market downturn and raised the prospect that the United States could enter its first recession since the 2008 financial crisis. Last night, President Donald Trump and U.S. House Speaker Nancy Pelosi offered two competing approaches for securing both the health and economic security of the American people. While the president’s proposals would arguably do more harm than good, Speaker Pelosi and House Democrats should be commended for swiftly developing a comprehensive and serious plan to effectively tackle the crisis.

During the last recession, Speaker Pelosi passed a stimulus bill that used a combination of deficit-financed tax cuts and government spending increases to boost the economy. With interest rates on government debt now below projected inflation, many are calling for her to now take similar action. The problem is that commerce is currently being constrained by proactive measures people are taking to limit the spread of a pandemic, not a lack of money in consumers’ pockets. Additionally, the coronavirus has disrupted global supply chains, which no amount of demand-side stimulus can alleviate in the short term. A unique economic problem requires a unique solution.

Some are concerned that subprime auto loans – which offer higher interest loans to riskier borrowers – pose a threat to the stability of the global economy in much the same way that the subprime mortgage market contributed to the Great Recession. Democratic presidential candidate Elizabeth Warren, in particular, has raised the warning flags as part of her campaign. But these worries are ill-founded and based on misleading data and faulty analogies.

In particular:

Auto loans account for a relatively small percentage of the increase in nonfinancial debt over the past five years;

Americans are spending less of their budgets on car purchases today, including finance charges, than they were before the recession;

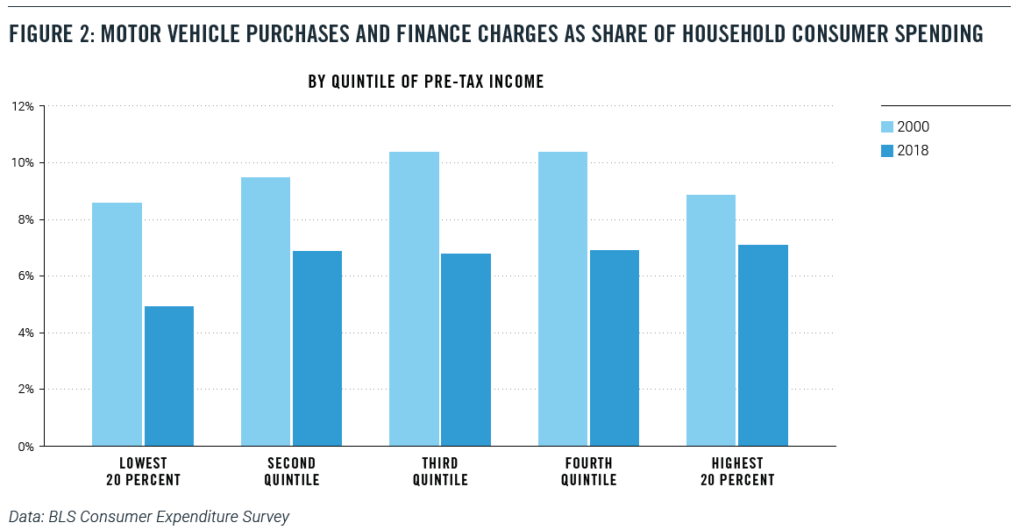

Low-income households saw motor vehicle purchases and finance charges fall from 8.5 percent of household budgets in 2000 to 4.9 percent in 2018;

Over the past five years, the share of new auto loans going to low-credit borrowers has remained relatively constant. There are no signs that low-credit borrowers are either being frozen out of the market or becoming too large a share of loans;

Newly delinquent auto loans, as a percentage of current balances, have been falling over the past two years; and

Subprime auto loans differ significantly from subprime mortgages in key respects that make them less likely to pose a serious threat to financial stability

Risk-based pricing of auto loans appears to be working so far, keeping low-income borrowers in the market without driving up delinquencies or to low-income consumers, while not posing the same risk that the subprime mortgage market.

Introduction

To purchase a vehicle, Americans with low or non-existent credit scores often use auto loans with higher interest rates than loans to prime borrowers. Some market watchers have indicated concern about “subprime” auto-loan trends and the potential for a crisis similar to the subprime mortgage crisis that heralded the last recession.

The subprime mortgages and the related mortgage-backed bonds remain the classic case of a poorly executed financial innovation. The initial impetus behind the idea was a good one. Housing is a key element of middle-class wealth, so expanding the system of mortgage finance to help lower-income households buy homes seemed like a positive. However, the subprime mortgages and bonds were designed in such a way that they assumed rising housing prices. When housing prices started to fall, the subprime mortgage system collapsed and contributed to the financial crisis.

Will subprime auto loans create the same problems? In a recent essay, Democratic presidential candidate Senator Elizabeth Warren raised the warning flag:

Auto loan debt is the highest it has ever been since we started tracking it nearly 20 years ago, and a record 7 million Americans are behind on their auto loans — many of which have similar abusive characteristics as pre-crash subprime mortgages1 .

Warren is not alone in her worries. In late 2016, for example, the Office of the Comptroller of the Currency warned that auto-lending risk was increasing and that banks (and other investors in securitized assets) did not have sufficient risk-management policies in place. Fed Governor Lael Brainard pointed to subprime auto lending as an area of concern in a May 2017 speech, while analysts worried about “deep subprime” auto loans2. Some groups used the term “predatory” auto lending.3

But these concerns are misplaced. As we will show later in this paper, the statistic cited by Senator Warren does not reflect the current state of the auto loan market, as it includes old loans from much weaker economic times. Perhaps most fundamental to understanding the problem with drawing a parallel between the mortgage crisis and today is the fact that subprime mortgages and subprime auto loans are very different products.

Naturally, lower-income households with low credit scores or limited credit history may have fewer financial resources and be inherently riskier borrowers. Moreover, the fact that motor vehicles depreciate over time means that the collateral for the loan becomes less valuable.

Nevertheless, the ability to own a car and, therefore, access credit is crucial for this population. Risk-based pricing charges low- rated borrowers higher interest rates, but in return, offers them the opportunity to borrow money to buy a vehicle that might otherwise be financially inaccessible.

For many lower-income households, their vehicle is the single biggest asset they own.

While vehicles do not appreciate in value as homes do, vehicles are income-producing assets in the sense that they are often essential for commuting to work, especially in non-urban areas. As one report noted, “Owning a car is the price of admission to the economy and society in much of America.”4

In this paper, we analyze the auto loan market, paying particular attention to auto loans made to low-income Americans and to people with bad credit. We find that:

Auto loans account for a relatively small percentage of the increase in nonfinancial debt over the past five years;

Americans are spending less of their budgets on car purchases today, including finance charges, than they were before the recession;

Low-income households saw motor vehicle purchases and finance charges fall from 8.5 percent of household budgets in 2000 to 4.9 percent in 2018;

Over the past five years, the share of new auto loans going to low-credit borrowers has remained relatively constant. There are no signs that low-credit borrowers are either being frozen out of the market or becoming too large a share of loans;

Newly delinquent auto loans, as a percentage of current balances, have been falling over the past two years; and

Subprime auto loans differ significantly from subprime mortgages in key respects that make them less likely to pose a serious threat to financial stability.

Risk-based pricing of auto loans appears to be working so far, keeping low-income borrowers in the market without driving up delinquencies or threatening the financial system. We conclude that the subprime auto loan market is beneficial to low-income consumers, while not posing the same risk that the subprime mortgage market did before the financial crisis. While it will be instructive to observe subprime auto loan trends going forward, current trends do not indicate significant instability concerns in this market.

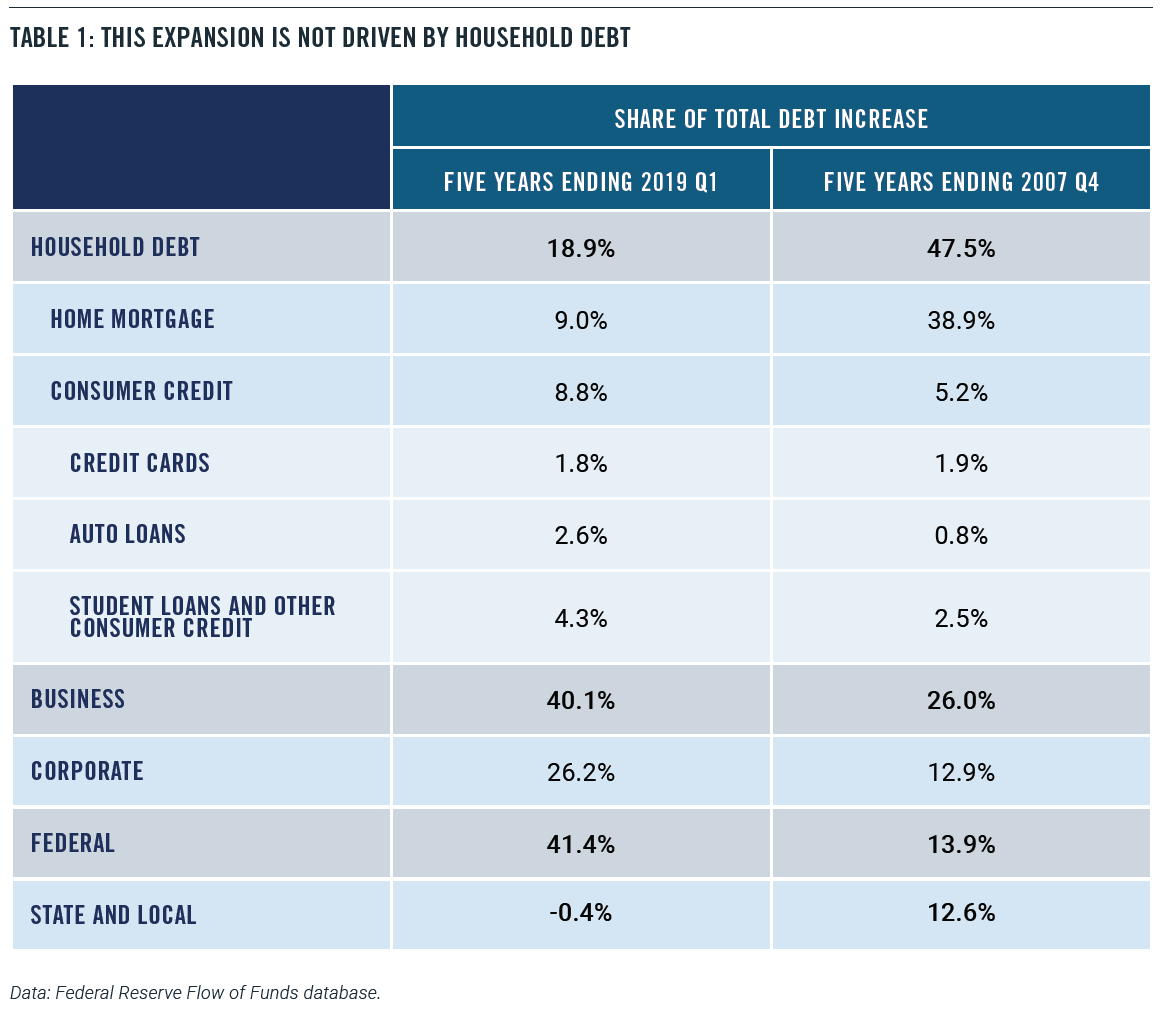

Recent Patterns in Debt Accumulation

Recent patterns in debt accumulation are very different from those that preceded the financial crisis and Great Recession. Non-mortgage consumer credit – including auto loans, credit cards, and student debt – has risen by $900 billion over the past five years, according to Federal Reserve data. While that figure sounds substantial, that increase amounts to less than 9 percent of the total increase in domestic nonfinancial debt – that is, all debt except borrowing by financial institutions. The rise in consumer borrowing is dwarfed by the increase in business debt ($4.1 trillion) and federal debt ($4.2 trillion) over the same period. Those two categories together account for 82 percent of the increase in domestic nonfinancial debt (Table 1). The leading contributors to business debt growth are mortgages and corporate bonds.

Indeed, businesses have taken the greatest advantage of low-interest rates. Nonfinancial corporations have almost doubled their outstanding corporate bonds since the end of 2007 when the last recession started. Meanwhile, household debt has risen by only 10 percent.

Taking home mortgages into account, households have only accounted for 19 percent of the increase in domestic nonfinancial debt since 2014. By contrast, in the five years leading up to the Great Recession, households accounted for 48 percent of the debt increase. In other words, the financial boom in the pre-recession years was heavily driven by household borrowing, while households have only contributed a small portion to the current debt increase.

A skeptic could argue that, given derivatives and financial engineering, it’s possible for a relatively small portion of the debt market to drive an outsize increase in risk for the whole system. Indeed, that’s what happened ahead of the 2008 financial crisis. In May 2007, then-Chairman of the Federal Reserve Ben Bernanke famously said, “We believe the effect of the troubles in the subprime sector on the broader housing market will be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system.”5 At the time, the value of subprime mortgages was about $1.3 trillion, which was only 10 percent of the mortgage market and an even smaller share of total borrowing. Bernanke and other policymakers figured that the problems in subprime mortgages could be easily contained.

What Bernanke and others failed to reckon with, however, was how the subprime mortgages had been designed to make sense only in a rising real estate market. Subprime mortgages were constructed effectively to subsidize interest rates with the possibility of appreciation. These financial instruments would offer low upfront rates that enabled lower-income borrowers to qualify. When the teaser rates eventually reset to much higher levels, the assumption was that the borrower could refinance into a new mortgage.

Moreover, the subprime mortgages were then securitized and used to build complicated financial derivative products. And when the subprime mortgages failed because of declining home prices, so did the derivatives. In other words, problems in a relatively small financial sector could be amplified and have a much larger effect on the rest of the economy.

Despite this concern, there is evidence to suggest that subprime auto lending is not a substantial risk to the broader economy. Auto loans are only 7.4% of household debt, which is the 40-year historical average.6 Moreover, the auto asset-backed securities (ABS) market is likewise dwarfed by the mortgage-backed securities (MBS) market. As of the second quarter of 2019, there was a mere $264 billion in auto-related securities, which included only $55 billion in subprime auto securities. By comparison, the amount of outstanding mortgage-related securities came to almost $10 trillion.7

Further, subprime auto loans don’t work the same way that subprime mortgage loans did in the pre-crisis era. Cars and trucks depreciate steadily over time, so the value of the collateral diminishes. That means lenders can’t afford to offer teaser rates, or excessive levels of negative equity, to buyers with low credit scores. They must charge higher rates, properly pricing risk. As one article put it, “the very nature of a real estate loan is very different from an auto loan. Real estate is an investment that typically appreciates over time. During the bubble years, consumers and lenders falsely believed appreciation would bail them out from poor judgment. Vehicles, on the other hand, depreciate. There is no false hope of higher values in the future to bail out a borrower or a lender.”8

The Auto Market

Despite the relatively small role that consumer debt is playing in the current debt expansion, some people can’t shake the idea that Americans are over-spending and over-borrowing to maintain a particular lifestyle. Consider this quote from an April 2019 piece from Business Insider:

The fact that America’s top-selling vehicle — a Ford truck with a price starting at nearly $30,000 – and many like it cost nearly half the median household income hasn’t stopped people from buying them and hasn’t stopped lenders from facilitating loans.9

Over the past five years, the price of new motor vehicles has risen by only 1.1 percent, according to estimates by the Bureau of Economic Analysis (BEA).10 By contrast, the overall price level of consumer goods and services have risen by 6.7 percent over the same stretch.11 In other words, the relative price of new motor vehicles has fallen over this period.

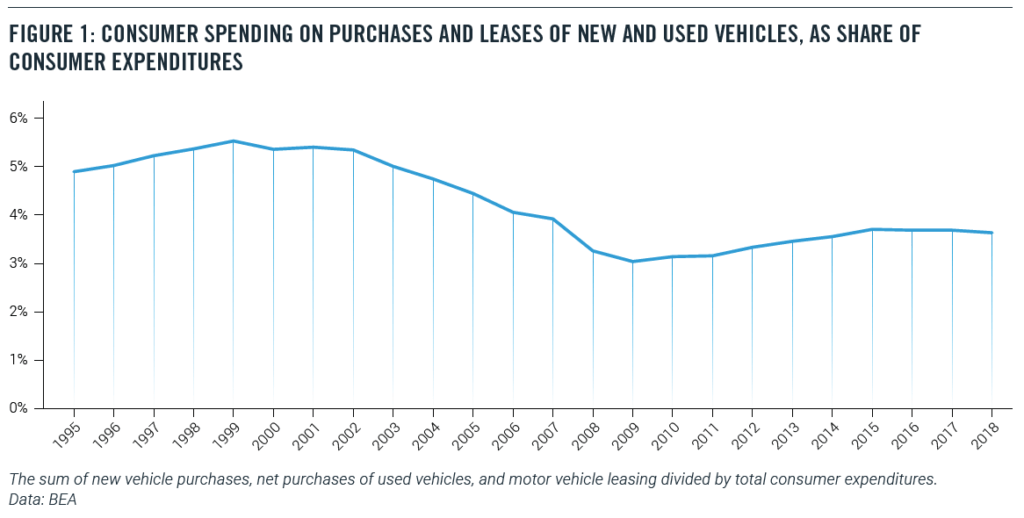

Not surprisingly, the share of consumer spending on new and used vehicles has fallen as well. In 2000, 5.4 percent of consumer spending went to purchases and leases of new and used vehicles. Today, that share is down to 3.6 percent (Figure 1).12

The BLS Consumer Expenditure Survey tells the same story. In 2000, motor vehicle purchases and finance charges amounted to 9.7 percent of household outlays. As of 2018, the last year for which full data is available, the share of vehicle purchases and finance charges fell to only 6.7 percent of household outlays.13 In part, this decline may represent a lengthening of the term of auto loans.14 (These figures would not be changed much by including automobile lease-related payments, which amount to about 10 percent of automobile purchase-related payments in 2018.)

The State of the Low-Income Auto Market

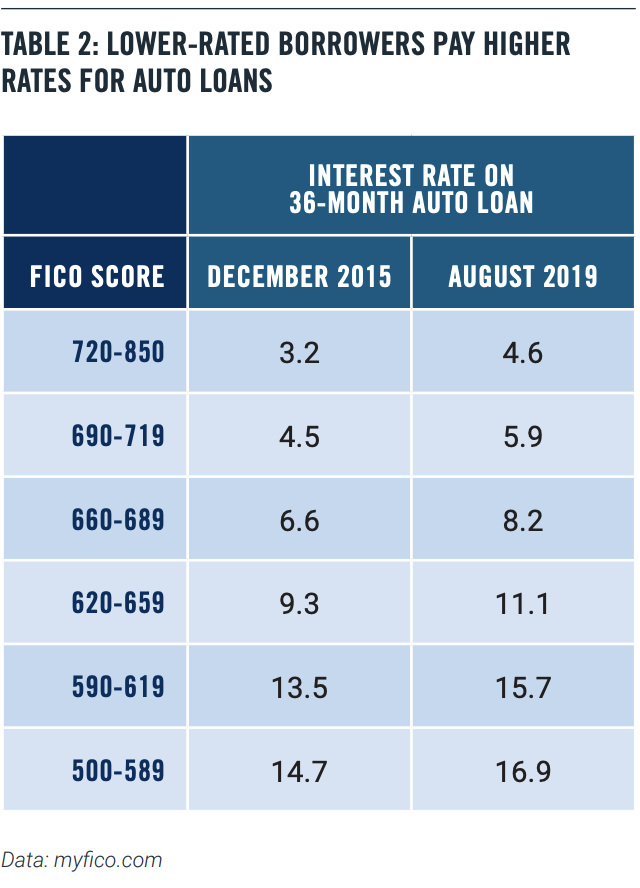

It’s not surprising that lower-rated borrowers pay more for their auto loans. Table 2 below shows interest rates for a 36-month new car loan at different credit rates for December 2015, which was close to the bottom of the credit cycle, and August 2019 (Table 2).

We can see that rates have risen for all credit-rating levels, but more so for the low-rated borrowers.

This risk-based pricing means that low-rated borrowers are not frozen out of the auto loan market. That’s good news, since, in many parts of the country, a car or truck is a necessity, even for low-income households. There is little or no public transit outside of densely populated urban areas, and ride-sharing services are not viable alternatives in many places. So, it is unsurprising that the share of low-income (the bottom quintile) households with a vehicle hold steady at 66 percent in both 2000 and 2018.

At the same time, low-income households saw motor-vehicle purchase and finance taking a smaller share of their budgets. In the bottom quintile of pre-tax income, motor vehicle purchases and finance charges fell from 8.5 percent of household budgets in 2000 to 4.9 percent in 2018 (Figure 2), a drop of almost four percentage points.15

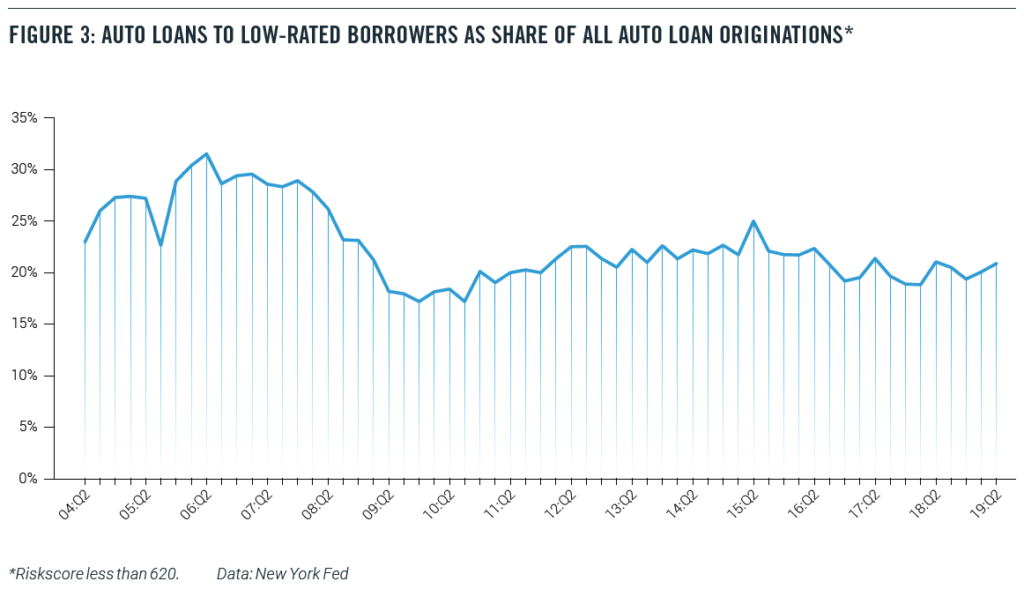

Similar data from the New York Fed’s Household Debt and Credit Report confirm that low-income households are not being uniquely stressed financially by automobile borrowing. Figure 3 shows the share of all auto loan originations that are going to low-rated borrowers (with a Riskscore of less than 620). Before the financial crisis, about 30 percent of new auto loans were going to low-rate borrowers, a startlingly high percentage. That share fell to 20 percent after the crisis and shows no signs of rising (Figure 3).16

The biggest piece of negative news has come from the New York Federal Reserve’s well-publicized finding in February 2019:

…(T)here were over 7 million Americans with auto loans that were 90 or more days delinquent at the end of 2018. That is more than a million more troubled borrowers than there had been at the end of 2010 when the overall delinquency rates were at their worst since auto loans are now more prevalent.18

This startling number, while impressive, simply doesn’t mean what it seems to suggest. This figure includes anyone who still has an old, bad auto loan on their credit record, even if the loan was made and written off years earlier.19 In fact, even after the lender writes off the loan, the loan servicer could continue to report the account to the credit bureaus.

The recent economic history of the United States helps to explain this figure. The number of nonfarm jobs did not return to pre-recession levels until 2014, while the employment-population ratio for Americans with a high school diploma but no college did not bottom out until 2015. As a result, today’s subprime borrowers are carrying around bad loans from the days when the labor market for less-educated workers was still struggling.

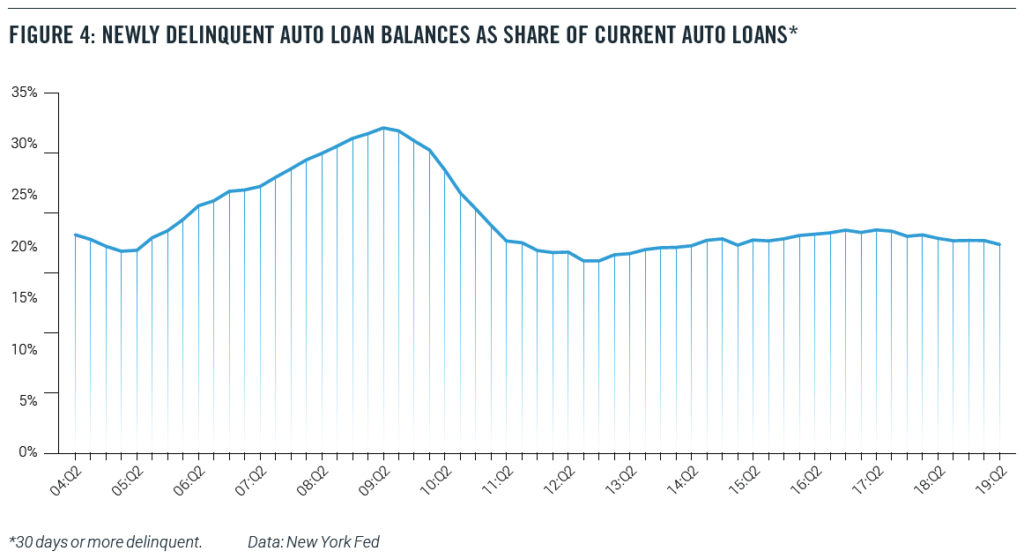

Indeed, in an August 2019 blog item, New York Fed economists recommend that anyone interested in the current performance of debt should look at the transition into delinquency- that is, a chart such as Figure 4.20 And by that measure, auto loans are doing far better than in the pre-recession years.

Conclusion

In the event of a recession or a significant economic slowdown, auto loan delinquencies will predictably rise. Subprime auto borrowers, who are more likely to have fewer resources, will be likely to fall behind in their payments when times turn bad.

Nevertheless, a careful look at the data does not suggest that either the origination of subprime auto loans or the exposure of the broader macroeconomy to the auto loan market is a cause for concern. In particular, the subprime auto-loan market looks nothing like the mortgage market before the Great Recession.

Newly delinquent auto loans, as a percentage of current balances, have been falling over the past two years, and the fact that a record number of Americans have a bad auto loan on their credit record is a testimony to economic history more than current loan practices and economic conditions, particularly given the rapid rise in total car sales during this period.

Indeed, risk-based pricing in the auto loan market appears to be supplying a steady flow of credit to low-rated borrowers without imposing excess stress on the financial system.

About the Authors

Michael Mandel is Chief Economic Strategist of the Progressive Policy Institute.

Douglas Holtz-Eakin is President of the American Action Forum.

Thomas Wade is Director of Financial Services Policy of the American Action Forum.

Projections published today by the non-partisan Congressional Budget Office confirm that the federal government is on course to spend $1 trillion more than it raises in revenue in Fiscal Year 2020. Trillion-dollar deficits continue as far as the eye can see, with CBO estimating a 10-year deficit of over $13 trillion.

Legislative changes since August have increased projected deficits by more than $500 billion, according to CBO. More than 90 percent of the increase comes from a package of irresponsible tax cuts added to a year-end spending agreement passed in December. But most of the change was offset by a decline in the projected interest rates and other technical changes, leaving 10-year deficit forecasts “only” $160 billion more than they were in August 2019.

What’s driving these deficits? Primarily the growth in federal health-care and retirement programs caused by our ageing population. Federal spending on Social Security, Medicare, and other health programs is projected to grow from 11 percent of gross domestic product today to 14 percent in 2030. All other non-interest spending, meanwhile, is projected to shrink as a percentage of GDP. Revenue won’t keep up with these costs, in large part because the Trump administration keeps charging tax cuts upon tax cuts to the national credit card. If anything, CBO’s projections are overly optimistic because the agency is required to assume most of these tax cuts expire in 2025 as they are scheduled to under current law.

Ben Ritz, the Director of PPI’s Center for Funding America’s Future, presented to students during two breakout sessions at the New England College Convention in Manchester, New Hampshire this week. The first session was a joint presentation about the national debt as an intergenerational issue with Bob Bixby from The Concord Coalition and Brian Riedl from the Manhattan Institute. The panelists spoke with local radio host Chase Hagaman about their presentation on his show, Facing the Future, which airs on New Hampshire’s WKXL station and can be found at the link below. Hagaman also moderated a second session in which Ben discussed with students the public investment proposals presented so far in the presidential campaign, how candidates would fund their agendas, and the impact these plans would have on young Americans.

Congress voted this week for a $1.9 trillion tax and spending deal, over a quarter of which was added to our $23 trillion national debt. Thanks to this and other fiscally irresponsible legislation signed into law by President Donald Trump, the federal government will run an annual budget deficit of over $1 trillion this year and every year that comes after it. Yet of over 500 questions asked throughout six presidential debates, not a single one has raised the issue.

The House of Representatives earlier this afternoon passed two bills to provide $1.4 trillion in funding for defense and non-defense spending programs that must be appropriated on an annual basis. As is often the case with must-pass legislation at the end of the year, these bills have become “Christmas trees” decorated with various policy riders and pet projects for members of both parties in Congress. What are the major provisions attached to this legislation that help add $500 billion to its price tag, and should they put Congress on the naughty or the nice list?

The Director of PPI’s Center for Funding America’s Future, Ben Ritz, joined personal-finance advisor Ric Edelman on his nationally syndicated radio show to discuss the challenges facing Social Security, their role in the 2020 election, and PPI’s proposal to strengthen the program for future generations. Listen to the interview below and read our full plan here.

A new report from the Congressional Budget Office projects federal budget deficits between 2019 and 2029 to be $872 billion higher than was projected just three months ago. As a result, Donald Trump will be forced to campaign for re-election next year with his government running a trillion-dollar deficit. Democrats should hold the “king of debt” accountable for his inability to manage the nation’s finances and present voters with a compelling alternative: a new progressivism that invests in our country without burying young Americans under a mountain of debt.

The increase in CBO’s deficit projections is largely due to the bipartisan budget deal signed into law this month and other spending policies enacted over the summer, which CBO says together will cost nearly $2 trillion – making them almost as expensive as the tax-cut bill enacted by Trump and the Republican-controlled Congress in 2017. Projected deficits also increased by almost $280 due to technical changes in CBO’s modeling. Partially offsetting these costs was a reduction in CBO’s forecast for interest rates, which brought projected deficits down by a whopping $1.4 trillion.

That a change of less than one percentage point in interest rates can cost nearly as much as the budget deal or the Trump tax cuts is a testament to the size of our national debt on which that interest is owed. The $16.5 trillion debt (which grows to almost $22.5 trillion if one includes intragovernmental debt such as that owed to the Social Security and Medicare Trust Funds) will only become worse moving forward as the government is projected to spend $1 trillion more than it raises in revenue every single year from 2020 onward if current laws remain unchanged.

The Canadian App Economy is strong both in terms of app exports and compared to its industrialized peers. The Canadian App Economy has 262,000 App Economy workers as of November 2018, according to a recently released report by the Progressive Policy Institute (PPI). App Economy workers are those that develop, maintain, or support mobile applications. What’s more, Canada is outperforming many of its industrialized peers.