During the most recent Facing the Future, Ben Ritz discussed PPI’s latest policy proposal, “A Progressive Budget for Equitable Growth.” The blueprint addresses a variety of issues, such as the national debt, taxes, health care, infrastructure, climate change, and more.

issue: Fiscal Policies

Media Advisory: Building a #BetterBudget, A Forum on Investing in America’s Future and Tackling Our National Debt

WASHINGTON—The Progressive Policy Institute and House Blue Dog Coalition will host a lunchtime discussion today at the Longworth House Office Building about what leaders in Congress can do to invest in equitable growth while reducing our national debt.

America suffers from a shortsighted fiscal policy that promotes consumption today instead of investing in tomorrow. The federal government now spends more to service our growing national debt than it does on public investments in education, infrastructure, and scientific research combined. Meanwhile, a perfect storm of fiscally irresponsible tax cuts and an unwillingness to tackle escalating health and retirement spending are feeding trillion-dollar deficits as far as the eye can see. This is not a fiscal policy for strengthening America’s future – it’s blueprint for American decline.

At the event, PPI will release a comprehensive budget plan with over 50 policy recommendations for the next administration to make room for public investments in education, and infrastructure, and scientific research; modernize federal health and retirement programs to reflect an aging society; and create a progressive, pro-growth tax code that raises the revenue necessary to pay the nation’s bills.

Lunch will be provided. This event is open to the press.

Who:

- Rep Stephanie Murphy (D-FL), Co-Chair of the House Blue Dog Coalition

- Rep. Ed Case (D-HI), Co-Chair of the Blue Dog Task Force on Fiscal Responsibility and Government Reform

- Rep. Ben McAdams (D-UT), Co-Chair of the Blue Dog Task Force on Fiscal Responsibility and Government Reform

- Ben Ritz, Director of PPI’s Center for Funding America’s Future

- Marc Goldwein, Senior Vice President at the Committee for a Responsible Federal Budget

- Emily Holubowich, Executive Director of the Coalition for Health Funding and Co-Founder of NDD United

- Will Marshall, President of PPI, Moderator

When: Thursday, July 25, 2019

12:00 PM – 1:30 PM

Where: Longworth House Office Building, Room 1302

15 Independence Ave, SE

Washington, D.C. 20515

For press inquires, please contact Carter Christensen, media@ppionline.org or 202-525-3931.

Ritz for Medium: “Budget Deal Perpetuates Broken Status Quo”

The budget deal scheduled for a vote tomorrow gets two things right and nearly everything else wrong. The main thing it gets right is the need to unshackle domestic public investment that would be subject to an across-the-board cut known as “sequestration” in the absence of legislative action. It also suspends the federal debt limit for two years, which will allow the Treasury Department to continue paying the bills America has already incurred without risking the prospect of a catastrophic default on our debts. What it gets wrong is charging $320 billion in new spending to our national credit card, which will further grow those debts and so perpetuate Washington’s governing dysfunction.

Read the full piece on Medium by clicking here.

Reframing the 2020 Health Care Debate

“Health care and poverty are inseparable issues and no program to improve the nation’s health will be effective unless we understand the conditions of injustice which underlie disease. It is illusory to think that we can cure a sickly child and ignore his need for enough food to eat.” Robert Kennedy, 1968

Reframing the 2020 Health Care Debate by the Honorable John A Kitzhaber, M.D.

Last month’s Democratic debates demonstrate how central health care will be in the 2020 election. Indeed, health care, more than any other issue, propelled the Democrats to regain control of the House of Representatives in 2018. Whether the upcoming election leads to meaningful relief for the millions of families struggling under the escalating financial burden of medical care, however, depends largely on how the issue is framed and on the clarity with which we see our policy goal and the steps necessary to achieve it.

Today the vast majority of dollars in our health care system are spent on the after-the-fact treatment of acute and chronic medical conditions rather than on investments that could prevent these conditions in the first place.

If we could reduce our health care spending from the current 18 percent of the GDP to the 12 percent average of most other industrialized nations, it would free up well over a trillion dollars a year for the social investments that actually improve health (1).

What concerns voters most about health care and, by a wide margin, is the cost — but, and this is important — not the cost of the overall U.S. health care system, but the cost to them as individuals (2). Most voters believe, to some extent in the abstract, that everyone should have access to affordable health care, but they are far more concerned that they as individuals have access to affordable health care. This is understandable because, at the end of the day, health care is intensely personal.

And yet, it is fair to say that nobody wants to need medical care or to be a “patient.” When you are sick or injured it is important that you have timely access to care at a cost you can afford, but we also know that among the factors contributing most to lifetime health status, our medical system is a relatively minor contributor. Far more important are things like healthy pregnancies, affordable housing, nutrition, stable families, good jobs, safe communities and the other “social determinants of health” (3),(4).

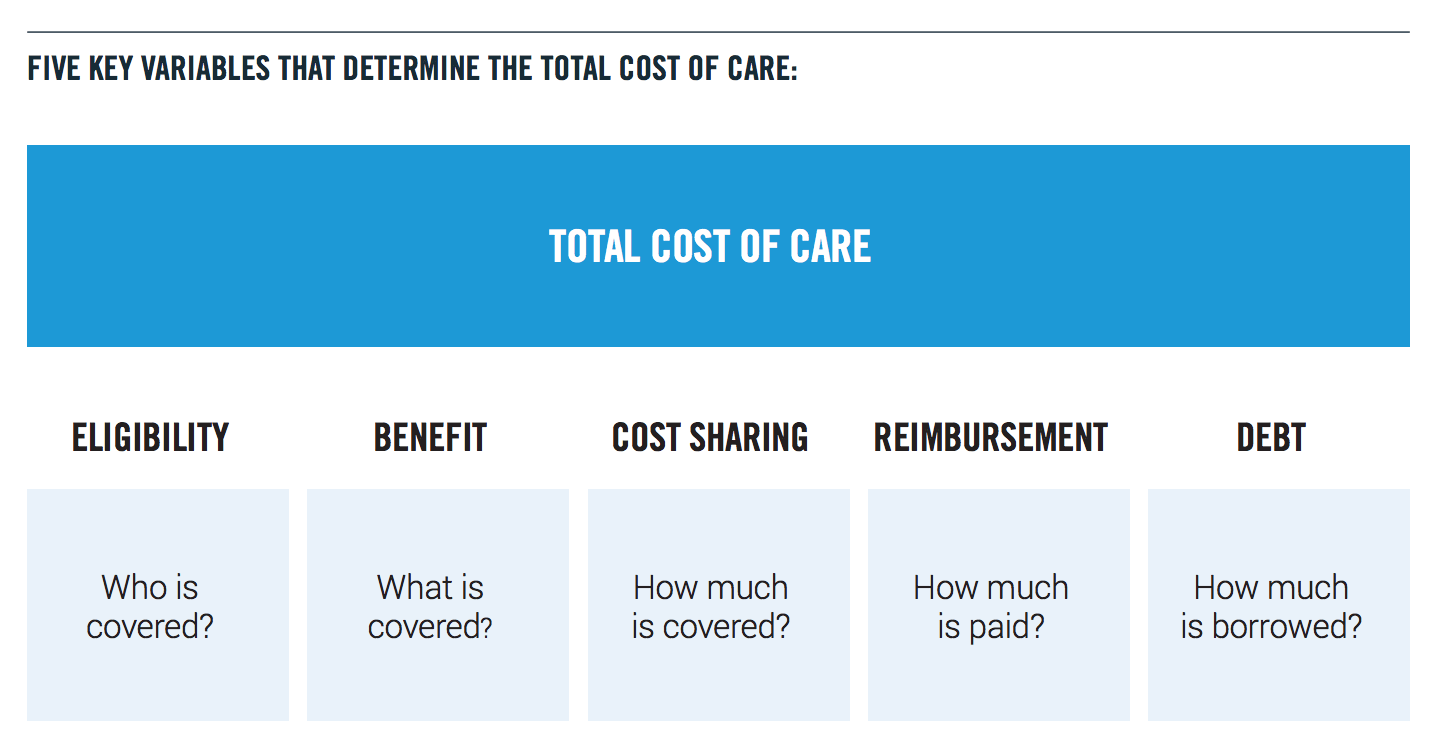

Therefore, our policy goal should be to improve the health of our people through a system that is financially stable, ensures that all Americans have timely access to effective, affordable, quality medical care; and also makes, strategic long-term investments in the social determinants of health. A system that can achieve this goal must include five core elements: 1. Universal coverage; 2. an affordable defined benefit; 3. a delivery system that assumes risk and accountability for quality and outcomes; 4. a global budget indexed to a sustainable rate of growth; and 5. savings reinvested upstream in the community to address the social determinants of health.

A system that incorporates these elements can take many forms, but without all five we cannot achieve our goal of improving health care in a financially sustainable way.

The most significant obstacle to achieving this goal is the total cost of care and the structure of the delivery system that is driving it. Health care is the only economic sector that produces goods and services none of its consumers can afford. Such a system only works because the care for individuals is heavily subsidized—increasingly with public resources—either directly through public insurance programs like Medicare and Medicaid; or indirectly through the tax exclusion for employer sponsored health insurance; and the public subsidies for those purchasing insurance through the Affordable Care Act (ACA) exchanges.

For decades, the national health care debate has been focused on these subsidies—on who pays them and how much they pay—rather than on why health care costs are so much in the first place. The political paralysis around this issue is due largely to the fact that neither Republicans nor Democrats assume any change in the health care delivery model: we either pay for it or we don’t, creating a false choice between cost and access. Republicans want to spend less on health care (e.g. “repeal and replace” the ACA) while Democrats want to spend more (e.g. Medicare for All). Neither approach directly addresses the total cost of care.

The burden of rising health care costs on individuals manifests itself in a variety of ways: rising insurance premiums and deductibles, short-term insurance policies that actually cover very little, the denial of coverage based on preexisting medical conditions, surprise billing, and the high cost of prescription drugs. It is not surprising, then, that most Democratic voters blame insurance companies and drug companies for the high cost of care. Generally, consumers do not blame health care providers, the delivery system itself, or the many new health care related startups and huge private equity firms that are making a profit off the $3.5 trillion health care budget (5).

And while Democrats are right to go after short-term junk health insurance policies, huge drug price increases, and surprise health care bills, these fixes only address shortcomings with health insurance rather than the total cost of medical care. The total cost of care is the primary driver of increases in insurance premiums as well as the increase in copayments and deductibles.

Since none of the current proposals address the systemic cost of care, they cannot prevent cost shifting onto individuals. All of these short-term fixes are worth making, but they are treating symptoms of the problem, not the problem itself.

The problem is illustrated by viewing our health care system through the lens of five questions or “variables”: 1. who is covered (eligibility); 2. what is covered (benefit); 3. how much is covered (cost-sharing—e.g. premiums, copayments, deductibles); 4. how much are we paying (reimbursement); and 5. how much is borrowed (debt financing).

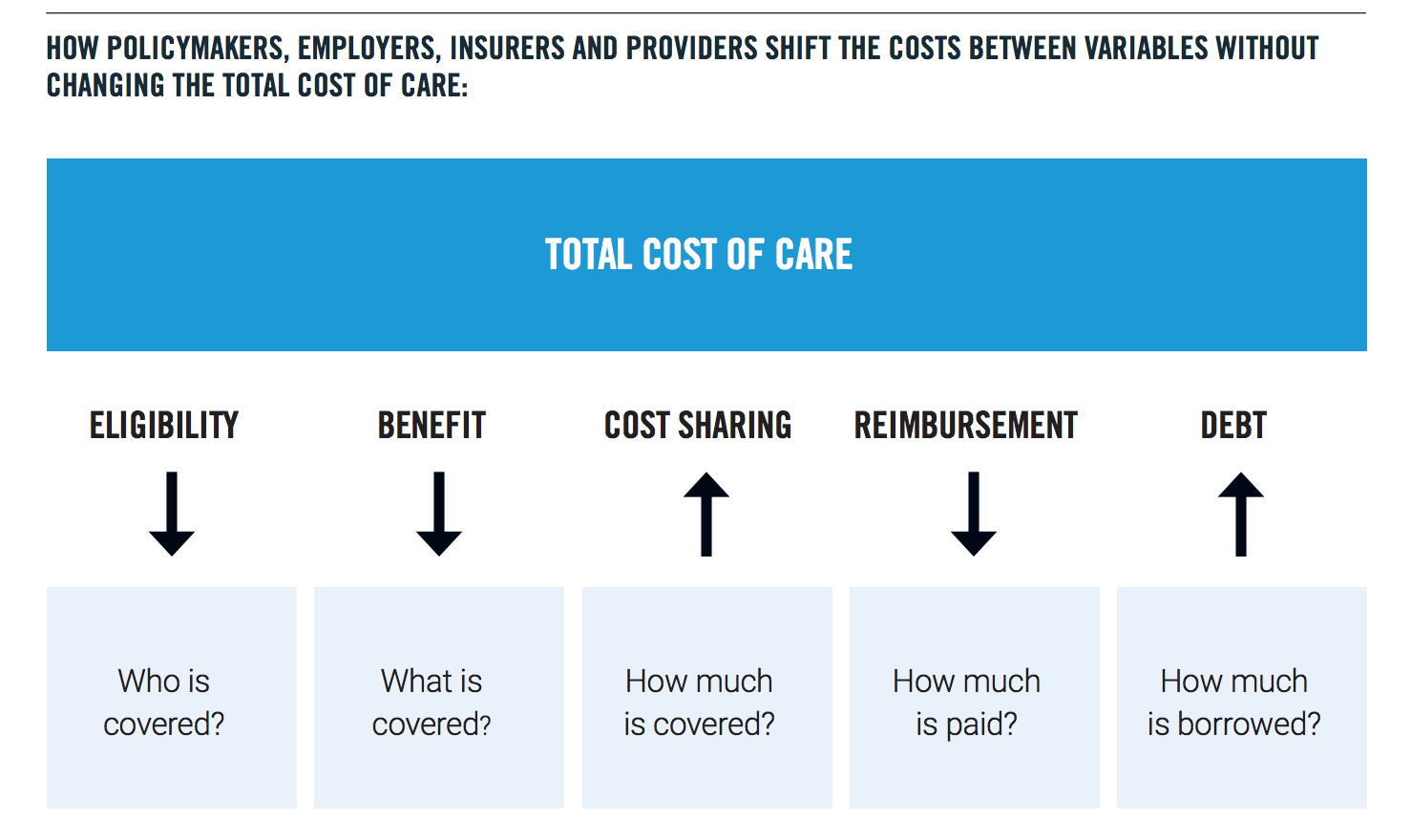

When the total cost of care exceeds the ability/ willingness of the major third-party payers (government and private sector employers) to pay for it, instead of seeking to reduce the cost of care, payers use one of five strategies to shift the cost to individuals who cannot afford it; or to future generations. These strategies include: reducing eligibility, reducing benefits and/or raising premiums, copayments and deductibles— all of which shift cost to individuals; reducing provider reimbursement which often results in efforts by providers to avoid caring for those who cannot pay; and pushing the cost of care into the national debt, shifting cost to future generations.

Cost shifting is the way we avoid directly confronting both the reality of fiscal limits and the fact that health care in the United States has simply become unaffordable for individuals, employers and the government. Cost shifting does not reduce the total cost of medical care. Furthermore, at 18 percent of our GDP, the cost of medical care, more than anything else, is undermining our ability to invest in children and families, housing, economic opportunity and the many other things that contribute to health. This is the primary reason why the U.S. has such embarrassingly poor population health statistics when compared to other industrialized nations that spend far less on medical care and far more on the social determinants (6).

The one indispensable step in moving toward a realistic and effective solution is to cap the total cost of care through a global budget indexed to a sustainable annual growth rate, while requiring providers to assume financial risk and accountability for quality and outcomes within that budget. Taking this step will fundamentally shift the debate from the subsidies to the delivery system. As long as we allow an ever-increasing share of our public resources to be spent paying whatever prices are demanded—whether for prescription drugs, hospital care or to grow profits of private equity funds—American families will continue to struggle under the burden of medical costs and this crisis will deepen.

Capping the total cost of care will allow us to expand coverage for a basic benefit package to all Americans (universal coverage); and to begin to invest upstream in the social determinants of health. The only way to expand access and to make room in the federal budget for serious investment in the social determinants of health is to reduce the total cost of care.

We already have two very successful examples of how global budgets work to bring down the total cost of care: Oregon’s Coordinated Care Organizations, which manage the state’s Medicaid program, and Medicare Advantage, that today serves more than 20 million seniors. Under these care models, providers receive a fixed amount of money for a defined population, without sacrificing quality (7). If the global budget is exceeded in any given year, the providers are at financial risk for the difference. In short, these care models begin to change the system incentives from rewarding sickness to rewarding wellness.

Extending these models more broadly across the U.S. health care system will reduce the total cost of care and free up resources to invest in the social determinants of health. It’s not necessary at this point in the 2020 election cycle to be prescriptive about how providers, insurers and other stakeholders in the current system will operate under a global budget cap indexed to a sustainable growth rate, but setting a target effective date for such a cap would fundamentally change the nature and the focus of the health care debate from where we want to go to how we are going to get there.

That is exactly what President John F. Kennedy did in 1962, when he challenged the nation to put a man on the moon. He did not give us a roadmap, he gave us a destination and, in so doing, unleashed American ingenuity and technological innovation to serve a common cause. Fifty years ago, this month, we achieved that goal. We succeeded in going to the moon because we were clear on our destination and because we imagined it; because the story preceded the accomplishment.

Surely, we can imagine linking the total cost of medical care to a sustainable growth rate within the next few years, then work backwards to create a health system that meets the objectives of both Democrats and Republicans: expanding coverage and improving health and quality; while reducing the rate of medical inflation through fiscal discipline and responsibility.

That’s the challenge. It’s not a challenge of technology—it is a challenge of political will and human compassion. And it’s not nearly as difficult as going to the moon.

[gview file=”https://www.progressivepolicy.org/wp-content/uploads/2019/07/GK_AK_HealthcareFinal.pdf”]

ENDNOTES

- Stuart M. Butler, Dayna Bowen Matthew, and Marcela Cabello, “Re-balancing Medical and Social Spending to Promote Health: Increasing State Flexibility to Improve Health Through Housing,” February 2017. https://www.brookings.edu/blog/usc-brookings-schaeffer-on-health-policy/2017/02/15/re-balancing-medical-and-social-spending-to-promote-health-increasing-state-flexibility-to-improve-health-through-housing/

- Ashley Kirzinger, Cailey Muñana, Bryan Wu, and Mollyann Brodie, “Data Note: Americans’ Challenges with Health Care Costs,” The Henry J Kaiser Family Foundation, June 11, 2019, https://www.kff.org/health-costs/issue-brief/data-note-americans-challenges-health-care-costs/

- Len M. Nichols and Lauren A. Taylor, “Social Determinants as Public Goods: A New Approach to Financing Key Investments in Health Communities,” Health Affaits, August 2018,https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2018.0039

- Ara Ohanian, “The ROI of Addressing Social Determinants of Health,” American Journal of Managed Care, January 11, 2018, https://www.ajmc.com/contributor/ara-ohanian/2018/01/the-roi-of-addressing-social-determinants-of-health

- Rabah Kamal and Cynthia Cox, “Total health expenditures have increased substantially over the past several decades,” Peterson-Kaiser Health System Tracker, December 10, 2018, https://www.healthsystemtracker.org/chart-collection/u-s-spending-healthcare-changedtime/#item-total-health-expenditures-have-increased-substantially-over-the-past-several-decades_2017

- Carlyn M. Hood, Keith P. Gennuso, Geoffrey R. Swain, Bridget B. Catlin, “County Health Rankings: Relationships Between Determinant Factors and Health Outcomes,” American Journal of Preventive Medicine, 2015. https://www.countyhealthrankings.org/sites/default/files/Hood_AmJPrevMed_2015.pdf

- The Institute of Medicine defines quality as “the degree to which health care services for individuals and populations increase the likelihood of desired health outcomes and are consistent with current professional knowledge.”

Regulatory Reform Could Revitalize Sluggish Business Creation

The U.S. economy recently marked 10 years of economic expansion – its longest in history – but there’s an important exception: new business creation. In recent decades, the American entrepreneurial engine has decelerated. Regulatory reform could help revive American entrepreneurship, reducing the burden on new businesses and realizing gains in economic growth. That doesn’t necessarily mean deregulation, but rather streamlining and updating old or obsolete rules to provide entrepreneurs with flexibility in today’s fast-changing world.

New and young businesses are the foundation of the United States’ economy, creating jobs and spreading wealth across our society. “Together, startups and high-growth firms (which are disproportionately young) account for about 70 percent of firm-level gross job creation in a typical year,” write entrepreneurship researchers Decker et al. Many of these young companies go on to become the next generation of small businesses, which employ 48 percent of private sector employees.

Unfortunately, the rate at which new businesses are being created has fallen off in the wake of the Great Recession. While firm deaths have returned to their pre-recession levels, firm births are down 22 percent compared to 2006 levels. And, for the first time since the Census Bureau began collecting data, firm deaths exceeded firm births from 2009 to 2011.

Smart policy can help increase the number of new businesses that are created and the number that scale up, though. Regulation is one area where policy can be made more efficient. A 2017 National Small Business Association survey estimated that the average small business owner spends at least $12,000 every year on compliance, with nearly one in three spending more than 80 hours every year dealing with federal regulation.

We know from research by Victor Bennett and Ronnie Chatterji that many people have entrepreneurial aspirations, but fail at many steps along their path to move to actual business formation. While many fail at early stages, such as basic market research, others undoubtedly run up against these mountainous regulatory costs and say, “not worth it.”

One way to reduce these costs is to focus on the steady buildup of regulation, or regulatory accumulation. The Code of Federal Regulations, where rules promulgated by the federal government are published annually, swelled by 17 percent from 2008 to 2018 alone. While Washington has dozens of agencies that issue new rules, not one institution is dedicated to streamlining the accumulated body of regulations. That’s why PPI proposed the Regulatory Improvement Commission (RIC). The RIC would fill an institutional vacuum in regulation policy by creating a mechanism for the periodic clearing out of obsolete rules.

Modeled on the Base Realignment and Closure Commission (BRAC) and comprised of a bipartisan group of highly qualified stakeholder appointees, the RIC would be an independent commission of eight members, appointed by the President and Congress, with regulatory expertise across industry and government. It would meet as authorized by Congress to review and, following a public comment period of 60 days, draw up a list of 15 to 20 rules for elimination or modification. The package would be sent to Congress for an up-or-down vote, and the RIC would be disbanded. If the proposed changes pass Congress, they would go to the president’s desk for signature or veto.

In 2015, bipartisan groups of lawmakers introduced bills in the House and Senate to establish the RIC based on the BRAC model. House cosponsors included Mick Mulvaney (R-SC), now acting White House Chief of Staff, and Kyrsten Sinema (D-AZ), now a Democratic Senator from Arizona.

Startup-friendly policies such as the RIC can help reduce compliance and opportunity costs, catalyzing a rebound in America’s startup rate and spurring economic growth. Streamlining regulation would help inventors and entrepreneurs spend less time and resources on regulatory compliance and focus instead on delivering goods and services and scaling their enterprises.

Research assistance was provided by Roman Darker, economics intern at the Progressive Policy Institute.

Repairing Credit: The Right Way to Fix a Broken System

If you think your credit report is accurate, there is a good chance you are wrong. According to the Federal Trade Commission (FTC), one in five Americans has a potentially material error in their credit file, and one of the biggest contributors is medical bills—with half of all medical bills containing an error.

In fact, mistakes on credit reports have become so pervasive that around a third of all complaints filed annually to the Consumer Financial Protection Bureau (CFPB) resulted from problems with consumer credit reports.

Credit report errors are a serious threat to the financial well-being of American families. As Senator Elizabeth Warren has noted, “credit reports regularly contain errors that can make it harder for families to access credit, find jobs, and get housing.” And as many consumers know all too well, it’s very difficult to get those errors corrected.” (1)

Under the Fair Credit Reporting Act, the company that furnished the information to the credit bureau must conduct an investigation to verify the information and correct a mistake, if they find one. Unfortunately, consumers who want to try to fix mistakes on their credit report face three daunting obstacles.

First, the system put into place by the credit reporting agencies heavily favors creditors and other data furnishers. Credit bureaus almost exclusively depend on lenders (such as banks, credit unions, credit card providers, and mortgage underwriters).

Consumers contacted the credit reporting agencies approximately eight million times in 2011 to initiate a credit dispute. But only a small fraction of those disputes was resolved internally by credit bureau staff. According to the CFPB, 85 percent of credit report disputes are passed on to data furnishers (the lenders) to investigate and resolve. (2) Unfortunately, in most cases the disputes are then shelved unless the consumer perseveres.

Second, the credit report agencies earn their profits by providing services such as credit checks to the very entities that provide the data used to create the credit reports – banks, mortgage lenders, credit card companies, retailers, and other businesses that provide credit. This creates a serious conflict of interest.

Third, despite several notable efforts to try to empower consumers, trying to correct errors on your credit report is still tedious, confusing, and time consuming.

CREDIT REPAIR ORGANIZATIONS AND COMPANIES

Because the system is rigged against them, many consumers turn to credit counseling agencies or credit repair companies. The dispute system designed to help consumers fix the problem favors the position of the debt collector over the consumer. Specifically, the credit bureau is only legally required to check with the creditor or debt collector and ask them whether they stand by their claim. As long as the creditor says you owe money, the dispute is resolved in their favor. As the National Consumer Law Center concludes: “Credit bureaus have little economic incentive to conduct proper disputes or improve their investigations.” (3)

Credit counseling agencies are typically a free resource from nonprofit financial education organizations that review your finances, debt and credit reports with the goal of teaching you to improve and manage your financial situation.

A credit repair company is a firm that offers to improve your credit in exchange for a fee. Unfortunately, the quality of these firms varies greatly. Some credit repair firms are highly reputable and follow best practices. Unfortunately, a significant cohort of credit repair firms are not good actors and, in some cases, have committed outright fraud. In 2016 the Consumer Financial Protection Bureau (CFPB) stated that “more than half of people who submitted complaints with the CFPB about credit repair chose the issue ‘fraud or scam’ to describe their complaints.”

There are some telltale signs for consumers trying to separate the bad actors from legitimate credit repair firms. Companies should be avoided that:

- Demand an upfront payment.

- Don’t provide a written agreement that includes cancellation rights for consumers.

- Guarantee they’ll raise your credit score or fix an error.

- Have multiple complaints against them with the Consumer Financial Protection Bureau or the attorney general’s office in the state where they operate.

- Suggest they can remove legitimate negative information.

- Offer to create a new credit profile based on a new employer identification number, rather than your Social Security number.

In contrast, responsible credit repair companies not only follow federal and state law but also:

- Offer a free consultation

- Have a track record and consistently solid reviews from past clients.

- Have an attorney on staff.

- Are licensed, bonded and insured.

WHAT NEEDS TO CHANGE?

To protect consumers, some policymakers have suggested new regulations to further police the credit repair industry. They note that credit repair firms don’t do anything someone with a bad credit report couldn’t do on their own. Anyone can dispute credit errors on their own behalf. But the Do-It-Yourself approach can be dauntingly complicated and time-consuming for harried families.

In essense, paying for credit repair assistance is really no different than paying an accountant or purchasing software to do your taxes – something 90 percent of Americans do according to the Internal Revenue Service.

It is important to note that there is already existing legislation to regulate the credit repair system. The Credit Repair Organizations Act (CROA) was signed into law in 1996 to protect consumers from the unscrupulous practices commonly used by several credit scammers.

Because of CROA, credit repair organizations are not permitted to misrepresent the services they provide, including guaranteeing the removal of negative credit listings. Credit repair organizations are also not permitted to attempt to create a “new” credit file or advise you to lie about your credit history. The Act also bars companies offering credit repair services from demanding advance payment, gives consumers certain contract cancellation rights as well as the right to sue a credit repair organization that violates CROA. (4)

CROA is a sensible law, and despite criticisms that it does not go far enough in regulating the credit repair industry, the law does provide consumers with protections against bad actors in the credit repair sector without eliminating legitimate credit repair firms. CROA needs strengthening, not in the form of new regulations but rather more effective enforcement.

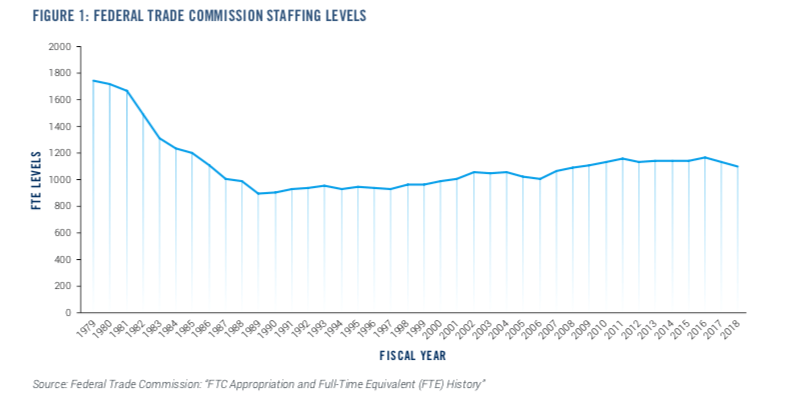

Under CROA, the Federal Trade Commission (FTC) is the primary enforcement body at the federal level. The problem is the FTC is severely underfunded and understaffed. In a Senate hearing last year Commissioner Rebecca Slaughter said the FTC’s staff level is 50 percent below its level at the beginning of the Reagan administration in 1981. Senators Jerry Moran (R-Kan.) and Catherine Cortez Masto (D-Nev.) agreed the FTC needs more resources and is “understaffed.” (5)

As Table 1 confirms, FTC staffing levels dropped dramatically during the 1980s and have never really recovered. Yet, over the same time, the responsibilities of the agency have dramatically changed and expanded. Today the FTC has to address some 2.7 million complaints a year in areas from debt collection, to identify theft, to imposter scams. (6)

Better enforcement of CROA would obviate the need to pile on new rules. Unfortunately, in fact, Congress has added to the FTC’s workload even as its workforce has shrunk. The simplest solution is to provide the FTC with additional resources dedicated to enforcing CROA and protecting consumers from those credit repair companies that have acted fraudulently or in bad faith.

To pay for this increase in supervisors, a small annual fee could be placed on the credit reporting agencies (Equifax, TransUnion, and Experian). To create an incentive for these agencies to be more responsive to consumer complaints about credit reporting agencies, the fee could be lowered or raised in synchronization with the number of consumer complaints about their credit reports.

OTHER REMEDIES

Another approach to fixing the current system is to go to the source of the problem, eliminating some of the causes for the extraordinary amount of errors made by the credit reporting industry. As Aaron Klein of the Brookings Institution has noted, there are three major reasons why credit scores are so inaccurate: “size, speed, and economic incentives of the system.”

One way to change the incentive structure would be to create some consequences for credit rating companies that frequently give lenders inaccurate data about borrowers. Lawmakers could consider legislation that would penalize credit reporting agency error rates above a certain level. Klein’s approach would use a random sample method (5 to 10 percent of complaints) to review credit rating firms’ performance. Another approach would be to grade the credit bureaus on their error and response rates.

CONCLUSION

While it is tempting to lump all credit repair firms into the same basket, many of these firms act in good faith and follow CROA to the letter of the law. Yet there is no doubt that a significant number of these companies are misleading consumers and sometimes acting fraudulently. If lawmakers really want to crack down on these bad actors, however, the first step should be strengthening enforcement of existing law.

Otherwise, spawning new laws and regulations would likely enmesh all credit repair firms in new layers of regulatory complexity and compliance burdens, making it even harder for consumers to detect and correct errors on their credit reports. In CROA we have the consumer protection law we need, now it’s time to focus on oversight and enforcement.

[gview file=”https://www.progressivepolicy.org/wp-content/uploads/2019/05/CreditFinal.pdf”]

(1) Brian Schatz Press Release: “Following Equifax Breach, Schatz, Warren, McCaskill, Colleagues Reintroduce Legislation to Help Consumers Catch And Correct Credit Report Errors,” September 11, 2017

(2) Kelly Dilworth, “Consumer watchdog report details credit bureaus’ work,” Creditcard.com, December 13, 2013

(3) Aaron Klein, “The Real Problem with Credit Reports is the Astounding Number of Errors,” Brookings Institution, September 28, 2017

(4) 15 USC Chapter 41, Subchapter II-A: Credit Repair Organizations

(5) Kate Patrick, “FTC Asks for More Control Over Big Tech, Privacy Issues,” Insidesources.com, November 30, 2018

(6) Federal Trade Commission, “FTC Releases Annual Summary of Complaints Reported by Consumers,” March 1, 2018

(7) Aaron Klein, “The Real Problem with Credit Reports is the Astounding Number of Errors,” Brookings Institution, September 28, 2017

(8) Ibid

Mandel for Medium: “Tech/Telecom/Ecommerce sector grew by 7.3% in 2018, Political Implications”

Many of the Democratic presidential candidates are vying to see who can be toughest on the tech sector. But here’s the paradox: New data shows that the tech boom is a major force driving down unemployment, lifting economic growth, and helping voters — precisely the people that the Democratic candidates are trying to reach.

The key here is that the economic data produced by the government is not typically presented in a form that easily shows the benefits of the tech boom. Software firms, for example, are spread across at least three different industries. Ecommerce — related activities are spread across at least two industries, electronic shopping and warehousing. And telecom includes at least two three industries, telecom services, communications equipment, and data processing and hosting.

Read the full piece on Medium by clicking here.

Ritz for Forbes, “Keep the White Walkers Out of Our Tax Code”

Millions of Americans watched the 70th episode of HBO’s Game of Thrones last Sunday to see who would win the ultimate battle between the people of Westeros and the undead army of the White Walkers. But there is another undead threat here in America that has gotten far less attention, one that marches not on our lands and castles, but on our tax code: they’re called “tax extenders.”

What exactly are tax extenders, you may be wondering, and how are they at all similar to the mythical antagonists from Westeros? Tax extenders were a package of “temporary” provisions that that gave preferential tax treatment to particular industries or activities. For nearly 30 years, Congress voted to extend the life of these provisions – which primarily benefited niche special interest groups – for just one or two years at a time. The main purpose of this ritual was to hide the true long-term costs of these special-interest handouts from the American people.

Ritz for Forbes, “Donald Trump’s Budget For A Declining America”

After the president’s budget was released on Monday, House Budget Committee Chairman John Yarmuth (D-KY) called it “A Budget for a Declining America.” Unfortunately, that might be an understatement.

The Trump administration’s Fiscal Year 2020 budget proposal is a compilation of the worst ideas to come out of the Republican Party over the last decade. It would dismantle public investments that lay the foundation for economic growth, resulting in less innovation. It would shred the social safety net, resulting in more poverty. It would rip away access to affordable health care, resulting in more disease. It would cut taxes for the rich, resulting in more income inequality. It would bloat the defense budget, resulting in more wasteful spending. And all this would add up to a higher national debt than the policies in President Obama’s final budget proposal.

The most harmful aspect of Trump’s fiscal blueprint is its scheme for gutting investments in public goods that are core responsibilities of government. The administration proposes to reduce the share of gross domestic product devoted to non-defense (domestic) discretionary spending – the category of the budget that is annually appropriated by Congress and includes most federal spending on infrastructure, education, and scientific research – by more than half over the next decade. The result is deep cuts to all three of these important investments that provide the foundation for long-term economic growth.

Investment Heroes 2018: Encouraging and Diffusing Innovation Throughout the Economy

Despite the low unemployment rate, productivity growth is still stuck in slow gear. Non-farm business output per hour increased by 1.3 percent from the third quarter of 2017 to the third quarter of 2018 – well below the post- war average of 2.2 percent.1 Other countries around the world are also grappling with this slowdown in productivity growth.2 Productivity growth is the primary factor in boosting wages and living standards.

The continued lack of productivity growth arises from several causes. One important issue is a growth shortfall in the amount of capital relative to the amount of labor, where capital represents investment in equipment, structures, software, and other intellectual property.

The Bureau of Labor Statistics (BLS) calculates a measure it calls “capital intensity,” which measures the services produced by capital assets relative to the number of labor hours worked in the non-farm business sector. As shown in Figure 1, capital intensity has grown much more slowly over the past 10 years than in previous 10-year periods.

There has been much debate over the reasons for this shortfall. Some have suggested that corporate managers and stock market investors have become myopic and too focused on short-run returns. Others blame excessive regulation.

But, no matter the reason for the investment shortfall, we think it’s important to identify those companies that are bucking the trend. Starting with our 2012 “Investment Heroes” report, and continuing through this report, we have focused on identifying those companies making the largest capital investments in the United States. By expanding the capital stock, these companies are helping boost productivity and wages, and creating new jobs.

The Progressive Policy Institute’s (PPI) Investment Heroes report provides an exclusive estimate of domestic capital spending for major U.S. companies. Currently, accounting rules do not require companies to report their U.S. capital spending separately. To fill this gap in the data, we created a methodology using publicly-available financial statements from non-financial Fortune 150 companies to identify the top companies that were investing in the United States. That methodology, with small modifications, has been used in each year’s report since the first in 2012.

Kim for Governing, “The Rise of Do-Gooder Corporations”

Doing good pays dividends for both corporations and governments. Just ask Philadelphia.

Azavea is a 65-person software development company based in Philadelphia. Its business is helping governments and nonprofits use geospatial data to achieve various public goals, such as improving traffic flow or reducing pollution. Many would call Azavea a dream employer. It shares its profits with its workers, buys locally, pays generously for training and allows employees to spend 10 percent of their time on personal projects. “We’re very much a people-first, employees-first company,” says CEO Robert Cheetham.

A growing number of firms are, like Azavea, on the leading edge of corporate reforms to make American businesses better stewards of the environment and worker well-being. They are so-called benefit corporations, whose charter explicitly allows them to pursue purposes other than sheer profit. Many are also certified, meaning they’ve met strict standards set by the nonprofit B Lab. More than 2,600 certified “B Corps” operate globally, according to the group, including such well-known brands as ice cream maker Ben and Jerry’s, women’s clothier Eileen Fisher and crowdfunding platform Kickstarter.

Now, an increasing number of governments are facilitating the growth of benefit companies. At least 34 states and the District of Columbia have passed laws — most of them within the past six years — that allow companies to organize as legally recognized benefit corporations. Legal status confers a potentially significant advantage for a company: protection from shareholder liability if executives fail to maximize profit in pursuit of other goals.

A Strong First Year for PPI’s Center for Funding America’s Future

As the Progressive Policy Institute’s Center for Funding America’s Future wraps up its first year, we want to thank everyone who followed and supported our work. Below you’ll find a compilation of our contributions to the public discourse in 2018.

Through op-eds, blog posts, media interviews, research reports, engagement with elected officials, and public forums organized in key battleground states, the Center drew much-needed attention to America’s interconnected problems of deteriorating public investment and soaring federal budget deficits. We fought back against Republican efforts to make these problems worse and challenged Democrats to counter them by offering a new progressivism that invests in our country without leaving the bill for future generations.

We concluded the year with a public forum in Iowa to kick off the 2020 presidential debate over fiscal issues in the nation’s first caucus state – and this is only the beginning. Now that we’ve made the case for a fiscally responsible public investment agenda that fosters robust and inclusive economic growth, we’re ready to offer concrete proposals for making it a reality.

In 2019, PPI will publish a series of specific policy recommendations to renew public investments in the foundation of our economy, modernize federal health and retirement programs to reflect an aging society, and enact pro-growth tax reform that raises the revenue necessary to support both of these critical government functions. We’re excited for the year ahead and hope you’ll continue to follow our work in 2019 and beyond.

Read Our Major Reports

Ending America’s Public Investment Drought

Ben Ritz and Brendan McDermott (12/19)

Defunding America’s Future: The Squeeze on Public Investment in the United States

Ben Ritz (10/15)

Watch Our Public Forums

Ending America’s Public Investment Drought – Des Moines, IA (12/19)

Former U.S. Secretary of Agriculture and Iowa Governor Tom Vilsack

Former Iowa Lieutenant Governor Patty Judge

Iowa Rep. Chris Hall, Ranking Member on the House Appropriations Committee

Ben Ritz, Director of PPI’s Center for Funding America’s Future

Moderated by PPI President Will Marshall

Defunding America’s Future – Philadelphia, PA (11/19)

U.S. Rep. Madeline Dean (D-PA)

Dr. Robert Inman, Professor of Finance at the Wharton School

Ben Ritz, Director of PPI’s Center for Funding America’s Future

Moderated by David Thornburgh, CEO of Committee of Seventy

Check Out Our Op-Eds and Media Coverage

DC Think Tank Urging Iowans to Ask Presidential Candidates About Infrastructure

O. Kay Henderson, Radio Iowa (12/22)

A Fitting End for Disgraceful House Republicans

Ben Ritz, Forbes (12/22)

Social Security, Public Projects and Rural America with Tom Vilsack (Radio)

Michael Libbie, Insight on the Business Hour on News/Talk 1540 KXEL (12/20)

American Children are Getting a Raw Deal Under GOP Leadership

Brodi Fontenot, The Hill (12/20)

Top Democrats Host Policy Roundtable (TV)

ABC 5, Des Moines (12/19)

Trump Once Again Shows Contempt for Young Americans

Ben Ritz, Forbes (12/6)

Welcome to Post-Thrift America

Andrew Yarrow, RealClearPolicy (12/04)

Victorious Democrats Should Thank Young Voters by Funding America’s Future

Ben Ritz, Forbes (11/8)

Reality Check 10.17.18 (Radio)

Charles Ellison, WURD Radio Philadelphia (10/17)

Defend or Defund Our Future? (Radio)

Chase Hagaman, Facing the Future on NH News Radio WKXL (10/16)

Time to Get DC’s Finances Under Control

Paul Weinstein, RealClearPolicy (10/17)

The Deficit Is Heading to $1 Trillion. How Worried Should We Be?

Michael Rainey, The Fiscal Times (9/24)

Democrats Must Bridge the Generational Divide to Prevent Climate and Budget Crises

Paul Bledsoe and Ben Ritz, The Hill (7/18)

How Trump and Republicans are Damning Social Security and Medicare

Ben Ritz, NY Daily News (6/14)

Making Social Security’s Retirement Age Work for Workers

Andy Rotherham, The Hill (6/8)

Medicare is Running Out of Money. Democrats Want to Expand It

W. James Antle III, Washington Examiner (6/7)

The Deficit Debate

David Leonhardt, The New York Times (4/20)

The Parallel Universe of Trump’s Budget, Explained

Sam Petulla and Gregory Krieg, CNN (2/13)

Welcome to a New Era of Federal Spending

Sam Petulla, CNN (2/10)

12 of the Most Important Things in Congress’s Massive Spending Deal

Heather Long and Jeff Stein, The Washington Post (2/8)

Find More Analysis on the PPI Blog

Republicans Double Down on Deepening Deficits (9/13)

CBO Report Shows That We Really Can’t Afford All These Tax Cuts (8/9)

New Projections Make Clear We Can’t Afford the Trump Agenda (6/27)

Before Expanding Medicare, We Have to Pay for Current Beneficiaries (6/7)

Trustees Reports Highlight Challenges Facing Medicare and Social Security (6/6)

CBO Analysis Exposes Trump’s Faulty Fiscal Policy (5/30)

Are Democrats Really the Party of Fiscal Responsibility? Part 2 (4/19)

A Tax Day Review of Trump’s “Tax Cuts” (4/17)

Are Democrats Really the Party of Fiscal Responsibility? Yes, But… (4/16)

PPI Analysis of CBO’s 2018 Budget and Economic Outlook (4/10)

House GOP’s Balanced Budget Amendment is a Sham (4/10)

Even After Budget Deal, Discretionary Spending Remains Low (3/14)

New Analysis Highlights Dire Fiscal Situation (3/5)

Six Charts That Reveal the Absurdity of the Trump Budget (2/14)

See Our Press Releases

PPI Kicks Off 2020 Economic Debate with Iowa Fiscal Forum (12/19)

New Report: Washington is Crippling America’s Economic Future (10/15)

New CBO Report Highlights the Cost of Trump’s First Year (4/9)

Statement on the Passing of Peter G. Peterson (3/20)

Ritz for Forbes, “A Fitting End For Disgraceful House Republicans”

This year concludes the same way it began: with a partial shutdown of the federal government. There is no doubt that President Donald Trump is primarily responsible for this shutdown – less than two weeks ago, during a nationally televised meeting in the Oval Office, he explicitly said so himself.

“If we don’t get what we want,” said Trump, “I will shut down the government. And I’ll tell you what, I am proud to shut down the government for border security, [Sen. Chuck Schumer]… I will take the mantle. I will be the one to shut it down. I’m not going to blame you for it … I will take the mantle of shutting down.”

Not a whole lot of wiggle room there: this is clearly a Trump Shutdown. But the president was bolstered by support from his allies in the House Republican Conference and their retiring leader, House Speaker Paul Ryan. While the Senate did its job and unanimously passed a continuing resolution that would have kept the government open and prevented the shutdown, Ryan refused to allow a vote on similar legislation, allowing the electorally-disgraced House Republican majority to create one last pointless budget crisis on its way out the door.

Fontenot for The Hill, “American children are getting a raw deal under GOP leadership”

American children born today are getting a raw deal. As they come of age to drive or vote, they will be saddled with unimaginable levels of public debt because of the decisions their political leaders are making today.

I know this because the official keepers of the budget accounts for Congress — the Congressional Budget Office (CBO) — told us in vivid detail that public debts will swell, and a recent study shows this debt will overwhelm and constrain the future generations’ ability to make investment decisions available to current decision-makers and respond to unforeseen crises.

Recent policy choices unfortunately have constrained the ability of future generations to deal with unanticipated problems in their era. Reversing this problem will be difficult, but, as history has shown, it will come from a return to Democratic vision and leadership.

Mandel for NJ Spotlight, “It Would Be A Mistake to Make Brick-and-Mortar Retailers in NJ Accept Cash”

It would be better to go cashless, while creating new low-cost banking options for poor residents

Is cash a bane or a boon?

The underlying trends are clear. Across the country, from high-end salad chain Sweetgreen to the new Amazon Go stores, more and more retailers are going cashless as technology improves. For a company like Amazon, doing without cash means speeding or eliminating the checkout process, including getting rid of long lines at peak times. For small retailers, the advantages are fewer losses from cash theft and much simplified operations, especially in high-crime areas.

In response, New Jersey is considering new legislation that would require all brick-and-mortar stores to accept cash. Similar bills have been introduced in Chicago, Washington, D.C. and Philadelphia. Supporters say that such legislation is important to protect poor Americans who don’t have access to credit cards or bank accounts.

This move to lock in the status quo is a mistake. The shift to cashless stores is a positive for poor Americans and small retailers, if combined with a concerted effort to bring low-cost banking to poor Americans. Moreover, regulations requiring cash are likely to reduce the competitiveness of brick-and-mortar stores against e-commerce.

Yarrow for RealClearPolicy, “Welcome to Post-Thrift America”

How did we arrive at a new normal of indifference to living on borrowed money? Federal budget deficits are poised to eclipse $1 trillion in 2020 and may never fall below that level again. There was hardly a word about this once-hot issue among Democrats or Republicans running in the midterm elections. Similar problems of matching spending with revenues exist at the state level, where unfunded pension liabilities grow while taxes are cut.

At the individual household level, following an uptick in savings after the Great Recession, most Americans can’t or don’t care about saving or balancing spending and income. About 80 percent of the population carries debt, totaling about $13 trillion, and one in five households have zero or negative assets.

The transition to this new normal has been as much a cultural story as a political or economic one. Whether one speaks of “thrift,” “living within one’s means,” or “pay as you go,” these were long the dominant values and standard practices of both governments and families. Throughout U.S. history, Americans and their government generally spent no more than their income or revenues and, ideally, would save some money. Of course, there were exceptions — such as wars and emergencies, and for individuals, poverty and other hardships — that necessitated borrowing. Economically, saving and investment were underpinnings of successful capitalism, and, morally, profligacy was a sin. Those who spent extravagantly were shady characters, while responsible budgeting was a sign of moral rectitude.