PPI’s Ben Ritz, Director of the Center for Funding America’s Future, released the following statement about the omnibus spending package:

Once again, Congress has waited until the last minute to carry out its most basic responsibility: funding the federal government’s normal operations. Thanks to a combination of brinkmanship and procrastination by leaders on both sides of the aisle, lawmakers will soon be forced to choose between voting for roughly $1.7 trillion of spending with little time to review legislative text or shutting down the government. This is no way to run a country.

The omnibus appropriations bill increases federal discretionary spending next year at a rate faster than overall economic growth. Boosting fiscal stimulus is exactly what lawmakers should not be doing with inflation still running at over 7%. Instead, Congress should be pursuing a fiscal policy that supports the Federal Reserve’s efforts to rein in rising prices.

It’s disappointing that, despite the increase in overall spending levels, it appears appropriators have failed to fund federal R&D efforts at the targets authorized by the CHIPS and Science Act passed earlier this year. The omission of much-needed permitting reforms also will reduce the efficacy of infrastructure investments Congress passed earlier this session. Together, these decisions represent a setback for the restoration of bold public investment that this Congress had been on track to accomplish.

But the package could have been worse. With the exception of some retirement provisions that are offset by gimmicks, the omnibus is mostly free of deficit-financed tax cuts that usually ride on end-of-the-year packages such as this. Although it would have been best for negotiators to agree on a fiscally responsible compromise to restore the pre-2022 tax treatment of R&D expenses and some expansion of the Child Tax Credit, their decision to omit these policies rather than to further fuel inflation by borrowing to pay for them was the right one.

It’s also good news that the omnibus will strengthen democracy at home and abroad through improvements to the Electoral Count Act and additional military assistance to help the Ukrainian people stand up to Russia’s brutal war of conquest.

Perhaps the next Congress could notch another win for democracy by following a rational and transparent budget process next time around. That shouldn’t be too much to ask of America’s elected representatives.

New initiative will push investments for 21st century job training and upward mobility

Today, the Progressive Policy Institute (PPI)announced the launch of the New Skills for a New Economy Project, which seeks to promote bold and pragmatic workforce development policies that level the playing field for degree and non-degree workers and ensure greater upward mobility for all working Americans. The project will be led by Taylor Maag, Director of Workforce Development Policy at PPI.

“The New Skills for a New Economy Project comes at a critical time for workers in America – we face unprecedented workforce challenges and more and more working Americans, especially those without degrees, are feeling left behind. This project will develop innovative policy solutions to address these challenges and ensure workers excel in today and tomorrow’s economy.” said Taylor Maag, Director of Workforce Development Policy at PPI.

The New Skills for a New Economy Project will help shape policy discussions at the federal and state levels around investments in a robust workforce development system that is fully-funded, modern, industry-responsive, and equips current and future workers with the skills they need to get ahead. The project will promote policy solutions that address the current challenges facing workers’ success and help the U.S. remain competitive by lifting up new ideas and best practices happening across the country.

Learn more about the project by visiting the project’s website, and read more about the project’s goals here.

Taylor Maag is the Director of Workforce Development Policy at PPI. Prior to joining PPI, Taylor worked at Jobs for the Future (JFF) where she assisted in the development and implementation of JFF’s federal and state policy agenda, focusing on workforce reform and innovation, access and affordability in postsecondary education and federal poverty alleviation policy. Additionally, Taylor led JFF’s congressional and workforce-related practitioner networks to ensure federal policymakers were staying connected with leaders implementing innovative and successful strategies on the ground.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Today, the Progressive Policy Institute’s Innovation Frontier Project released a new report exploring the critical role contract workers play in this post-pandemic workforce, and the policies that will help provide support to this important workforce. The report is titled “Supporting Contractors’ Career Development in the Future of Work,” and is authored by Dr. Liz Wilke, Principal Economist at Gusto and cohort member of PPI’s Mosaic Project.

“Supporting contractors to continually invest in their skills, confidently and expertly manage their professional affairs, and ensure that they benefit from basic workplace protections available to employees can support this important segment of the workforce, ensure their long-term success, and enhance the benefits they bring to American businesses,” writes report author Liz Wilke.

Reliance on contract workers is expected to increase as 90% of companies expect to use them more in the future. The report looks at the rise of contract and gig workers in recent years and identifies some of the resources needed to sustain America’s growing workforce.

In addition to releasing the paper, Dr. Wilke and the Director of PPI’s Mosaic Project, Jasmine Stoughton, sat down to examine Dr. Wilke’s findings in a new “Mosaic Moment” podcast, a series on PPI’s Radically Pragmatic podcast. They discussed gaps in the social safety net for both contractors and employees, the complexities of filing taxes as an independent worker, and how upskilling and career training could be the key to navigating our modern economy.

Liz Wilke, PhD, is a Principal Economist at Gusto, researching the state of work and business in the modern economy. She is a veteran of both the technology and government sectors, where she directed research programs and public spending that supports dynamic, resilient companies and workers across the globe. Liz currently lives in Washington, D.C.

Based in Washington, D.C., and housed in the Progressive Policy Institute, the Innovation Frontier Project explores the role of public policy in science, technology and innovation. The project is managed by Jordan Shapiro. Learn more by visiting innovationfrontier.org.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

PPI’s Center for Funding America’s Future today called on Congressional Leaders to prioritize the fight against inflation above all else as both Chambers race to complete the legislative priorities of the 117th Congress.

In their memo to leadership, Ben Ritz and Nick Buffie argue that Congress should not cut taxes or increase spending over the next year or in future years without concurrently offsetting the costs over the same time period. Doing so would double down on a borrowing binge that has worsened inflation and raised costs for hardworking Americans.

PPI’s Center for Funding America’s Future’s outlines key priorities for lawmakers to address in a fiscally responsible way that supports our economy and helps the Federal Reserve bring down inflation:

Providing adequate appropriations for normal government operations and new public investments

Supporting the fight for democracy in Ukraine

Restoring some expansion of the child tax credit

Restoring immediate expensing for R&D investments

Improving retirement security without costly budget gimmicks, and

Passing energy permitting reform to boost energy supply and combat climate change

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Platform work offers more flexibility and better earning opportunities for millions of working Americans providing unpaid care

Today, the Progressive Policy Institute (PPI) released a new report showing that on the average day, 36% of working-age Americans provide unpaid care for children, parents and other loved ones. This unpaid labor is worth $980 billion per year, according to this new report, titled “Platform Work and the Care Economy” and authored by PPI Vice President and Chief Economist Dr. Michael Mandel.

The report examines how the stress of this immense burden can be eased by the availability of flexible platform work, including companies such as Lyft, Uber, Doordash, and Instacart.

“Platform work provides an alternative that offers better scheduling and earning opportunities for unpaid caregivers,” writes Dr. Michael Mandel in the report. “Rather than requiring a choice between full-time work and no paid work at all, there is a flexible alternative.”

The report also explores the possibility that platform work may help narrow the longstanding gender gap in unpaid caregiving.

Dr. Michael Mandel is Vice President and Chief Economist at the Progressive Policy Institute in Washington DC and senior fellow at the Mack Institute for Innovation Management at the Wharton School (UPenn). He was chief economist at BusinessWeek prior to its purchase by Bloomberg.With experience spanning policy, academics, and business, Dr. Mandel has helped lead the public conversation about the economic and business impact of technology for the past two decades. His work has been featured by the Wall Street Journal, New York Times, Washington Post, Boston Globe, and Financial Times, among others.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Welcome to the Care Economy, a term that is being used much more frequently these days. America’s aging population means that many workers are spending more hours than ever taking care of older parents. At the same time, the time burden of raising children has not diminished. That means roughly 36% of the working-age population is engaged in providing unpaid care on any given day, according to the annual American Time Use Survey from the Bureau of Labor Statistics (ATUS).

Overall, if Americans were paid $15 per hour for their unpaid caregiving labor, then the total value of the time spent on unpaid care would be $980 billion per year.

The nature of work in America, though, means that unpaid care is more stressful than it needs to be. In an ideal world, many people with caregiving responsibilities would search out part-time positions that fit their specific situations. But conventional part-time employment tends to offer much lower hourly pay than comparable full-time positions and, it turns out, much less flexibility. Therefore, caregivers are forced to either (1) accept low paying and inflexible parttime jobs; (2) take conventional full-time jobs, with all the stress of combining work and unpaid care responsibilities; or (3) drop out of the paid workforce completely. Notably, this difficult decision — and the burden of unpaid care in general — falls mainly on women. We estimate that the size of the caregiving gender gap can be valued at $325 billion per year.

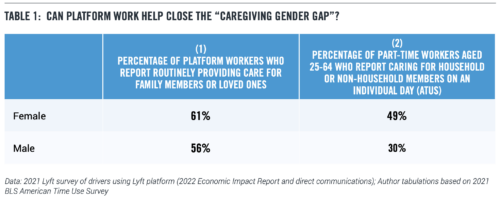

This “caregiving gender gap” is especially large for part-time job holders. Among working-age women who hold part-time employment, 49% have unpaid care responsibilities on the average day, compared to 30% of men with part-time employment, based on our tabulations of the 2021 ATUS (Column (2), Table 1).

Further, these averages do not convey the unpredictable nature of the caregiving role. It’s one thing for a single working mother to arrange her schedule to be home by six o’clock to make dinner and assist with homework. It’s quite something else when a child suddenly falls ill and needs to be kept home from school for a day or a week. Eldercare is even more unpredictable. Medical crises can happen suddenly, as when an aging parent falls, breaks their hip, and can no longer stay in the house where they have lived for 50 years. The nature of aging is that unpaid care responsibilities cannot be postponed or scheduled in advance.

Government policies can certainly help ameliorate the burden of unpaid care. For example, the Family and Medical Leave Act of 1993 (FMLA) requires covered employers to provide unpaid leave for certain medical and family obligations. Currently, 11 states, including California, have put in place paid family and medical leave policies. In his April 2021 American Families Plan, President Biden proposed subsidizing high-quality child care for low-income and middle-income households, and “creating a national comprehensive paid family and medical leave program that will bring America in line with competitor nations that offer paid leave programs.” Some of these programs were incorporated into earlier versions of the Build Back Better legislation, but not the version that eventually passed Congress as the Inflation Reduction Act of 2022.

Even if this legislation had passed in its entirety, the structure of most full-time and part-time jobs is not supportive of unpaid caregiving responsibilities. First, most employers run lean operations without excess labor to rely on in times of emergency. The number of open positions hit record levels in the first half of 2022, according to the Bureau of Labor Statistics, driven by short-staffing in industries such as retail, health care, and transportation. Under these conditions, employers struggle when their employees can’t show up on short notice because of the need to suddenly take an aging parent to the doctor.

Second, government-mandated paid leave plans, like the one proposed by President Biden or currently in effect in states like California, typically offer only partial reimbursement of a participant’s usual pay. The workers who take time off to fulfill caregiving duties additionally have to worry about making up the lost income after the immediate crisis is over. Even the most flexible and supportive employers may be incapable of rearranging work schedules to provide more hours for someone returning from leave.

THIS PAPER: A FOCUS ON PLATFORM WORK

In this paper we demonstrate how platform work, such as work facilitated by companies such as Lyft, Uber, DoorDash, and Instacart can improve earnings opportunities for many Americans in the Care Economy. We first estimate the number of paid employees in the Care Economy, then compare it to unpaid job equivalents. All told, there are roughly 4.5 million full-time equivalent (FTE) workers engaged in eldercare. The child care services industry employs roughly about 700,000 (FTE) workers, up 10% since 2007.

These are substantial numbers, but fall far short of the actual time devoted to caregiving. Second, we use the ATUS to estimate the number of hours of unpaid caregiving, and translate those hours into full-time equivalent (FTE) jobs. We find that unpaid caregiving is equal to more than 30 million FTE jobs. By comparison, the health care and social assistance sector includes 17 million FTE paid jobs.

Third, we analyze how the unpredictability of caregiving is more conducive to platform work than to traditional part-time employment. In particular, we show two key advantages that platform work has over conventional part-time work: “downward flexibility” and “upward flexibility.” We define downward flexibility as the ability of the worker to choose to reduce hours on short notice to deal with unpredictable caregiving issues. We define upward flexibility as the ability of workers to increase hours after a caregiving crisis is over to meet existing financial goals and commitments.

Downward flexibility is often cited as an advantage of platform work for unpaid caregivers. They can fully customize their working hours, choosing to be home when children are home from school. They can adjust when, or even if, they work, to match unforeseen short-term changes in care arrangements, such as school being closed for a day. And they can step away from their work for extended periods to deal with major health crises, such as an elderly parent who is injured.

Upward flexibility usually receives less attention, but it is a key characteristic of platform work that differentiates it from an employer-employee relationship. In general, most jobs are timecapped, in the sense that the worker needs special permission from their immediate supervisor or higher-ups in order to work more hours. Someone who misses out on income when they take time off to care for their aging parent has no guarantee of getting enough hours to meet existing financial goals and commitments, especially if the company is operating under a tight budget.

Upward flexibility provides a way of addressing unexpected caregiving responsibilities while still continuing to pay for essentials, such as housing and food, meeting debt obligations, and/or saving for the future. Upward flexibility is especially important for low-income households that otherwise may struggle to stay afloat and take care of their children and parents at the same time.

Downward and upward flexibility makes it easier for both men and women to combine platform work with caregiving. A 2021 survey of drivers on one platform suggests that the percent of male drivers who report routinely providing care for family members or loved ones (56%) is quite high, and very near the percent of female drivers who are caregivers (61%), as shown in Table 1 (Column (1)). Indeed, the “caregiving gender gap” between men and women who choose platform work is much smaller than that gap for part-time workers in the general population.

Platform work could lead to a smaller caregiving gender gap because men who are unpaid caregivers, whether for children or adults, are more likely to seek out the flexibility offered by platform work. Alternatively, men who participate in platform work for other reasons can find it easier to take on unpaid care responsibilities, especially since they have the flexibility to earn more and still fulfill financial commitments and goals, including meeting debt obligations and saving for the future. Overall, this suggests that platform work can help narrow the caregiving gender gap.

THE GROWTH OF THE CARE ECONOMY

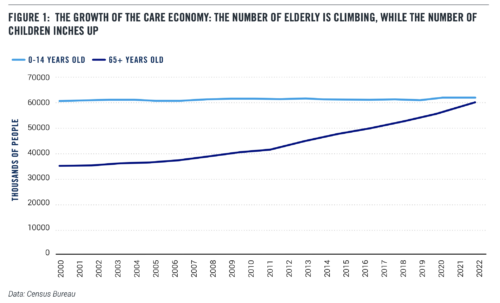

The Care Economy is becoming more economically meaningful in the United States, as the total number of people who need some form of care continues to grow. At the younger end of the age spectrum, the number of children under the age of 15 is up slightly in the 15 years since 2007. At the older end of the age spectrum, the number of Americans who are 65 and over has risen almost 60% since 2007 (Figure 1).

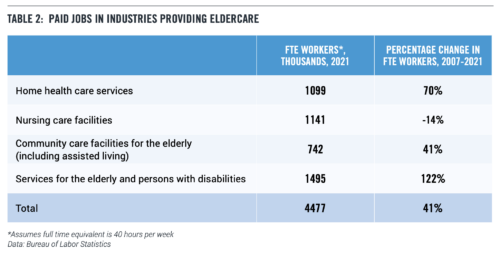

Over the same period, the amount of paid Care Economy work has continued to rise, especially work serving the needs of the elderly. Paid FTE employment in eldercare-related industries such as home health care providers and nursing facilities has risen by 41% since 2007 (Table 2). In particular, FTE employment at home health care agencies is up 70%. By comparison, the amount of overall FTE private sector employment rose only 8% since 2007. All told, there are roughly 4.5 million full-time equivalent workers engaged in eldercare.

The child care services industry employs roughly 700,000 FTE workers, up 10% since 2007. If we include all the informal arrangements with people who are paid to monitor and care for kids in their homes, then the total number goes up to roughly 1.5 million, based on a 2019 report from the CED. And to the degree that elementary and middle schools play a “caretaking” role, some portion of the roughly 6 million public school instructors and staff should be booked against the Care Economy as well.

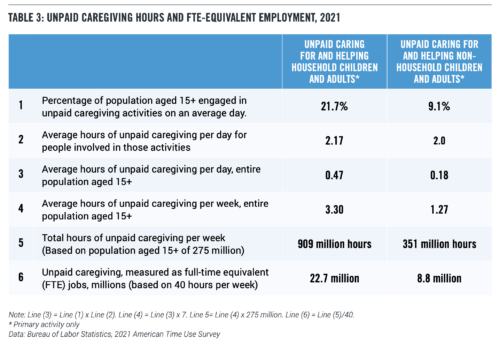

So far, we have been considering paid caregiving. However, we can estimate the number of unpaid caring hours, based on the annual American Time Use Survey from the Bureau of Labor Statistics (BLS). The BLS collects data on daily activities from a rolling sample of about 9,000 adult Americans over the course of a year. Broad categories of time use include personal care, working, household activities such as food preparation and cleanup, purchasing goods and services, and leisure and sports (including watching television).

The categories of time use that we focus on are “caring for and helping household children and adults” and “caring for and helping nonhousehold children and adults.” (These two categories also include travel time). Table 3 lays out some of the basic facts from the 2021 ATUS about the number of hours devoted to unpaid caregiving as a primary activity. Line (1) gives the average percentage of the population aged 15+ engaged in unpaid caring or helping children and adults inside or outside the household. The table shows that 21.7% of the population cares for household members on an average day, and 9.1% of the population cares for non-household members on an average day.20 Line (2) gives average hours of unpaid caregiving per day for people involved in those activities. We multiply line (1) by line (2) to get line (3), the average hours of unpaid caregiving per day for the entire population, and then multiply line (3) by 7 to calculate the average hours of unpaid caregiving per week (line (4)).

We multiply line (4) by 275 million, the number of people 15 and over, to derive the total number of hours devoted to unpaid caregiving (line (5)). Finally, we calculate full-time equivalent employment by dividing by 40 hours per week (line (6)).

In total, we find that unpaid caregiving hours are equivalent to more than 30 million FTE jobs. That far exceeds the current amount of paid employment in the health care and social assistance sector, which is 17 million paid FTE jobs.

To put it another way, if people were paid $15 per hour for their unpaid caregiving labor, then the total economic impact of the unpaid care sector work would be $980 billion per year.

THE UNPREDICTABILITY OF THE CARE ECONOMY

The problem, of course, is that much of the unpaid caregiving is supplied by individuals who already have other responsibilities, including paid work. And it is often difficult to integrate since unpaid Care Economy tasks are often unpredictable. Caring for children, as any parent knows, involves frequent unanticipated crises of uncertain duration. Children may suddenly get sick, especially during the age of COVID, and can’t go to school or child care, leaving parents with no choice but to stay home or ask for help from friends or relatives.

The literature and anecdotes suggest that unpredictability is an even more important characteristic of unpaid eldercare. The elderly are likely to suddenly suffer from major illnesses or injuries, such as a stroke, that require a large amount of support. And their ability to take care of daily tasks, like getting themselves to the doctor, may deteriorate at unpredictable rates.

Unpredictability is an important reason why studies and reports consistently show a constant friction between work schedules and unpaid care needs. As one analysis notes:

“Particularly when care demands increase, the unpredictability and the duration of the caregiver experience is accompanied by increased stress, distraction and anxiety over lost productivity.”

The stress can be seen in an employee survey done for a 2019 report on “The Caring Company” from the “Project on Managing the Future of Work” at the Harvard Business School. The survey revealed that “32% of all employees had voluntarily left a job during their career due to caregiving responsibilities.”

What drove these voluntary departures? According to the report:

A closer look at the 32% of employees who admitted to leaving a job due to caregiving showed that this is a multigenerational issue. Care obligations can arise at one or more stages of a worker’s career. Employees cited taking care of a newborn or adopted child (57%), caring for a sick child (49%), or simply managing a child’s daily needs (43%) as the top three reasons for leaving. However, the obligation to provide care for other adults also featured prominently. A third of employees who left a position (32%) cited taking care of an elder with daily living needs as the reason. Almost 25% did so to care for an ill or disabled spouse, partner, or extended family member.

One academic paper identifies a clear difference between child care and eldercare:

While childcare has a fairly predictable pattern with children becoming less dependent on parents as they get older, eldercare is unpredictable, varies in duration, and tends to increase in amount and intensity over time as the care recipient ages.

The burden of the unpredictability of unpaid care mostly falls on women, because they disproportionately provide most of the unpaid care. That’s the “caregiving gender gap,” and no matter what set of numbers you look at, the caregiving gender gap is wide. Going back to Table 1, 49% of women aged 25-64 who work part-time report caring for household or nonhousehold members, compared to 30% of men aged 25-64 who work part-time. That’s based on the 2021 ATUS.

Here’s another illustration of the caregiving gender gap. Table 3 calculates that there are 909 million hours per week in unpaid care for household members, and 351 million hours per week in unpaid care for non-household members, for a total of 1.260 billion hours per week in unpaid care.

Out of those more than one billion hours of unpaid care per week in the United States, roughly 66%, or 840 million hours, come from women, and roughly 34%, or 420 million hours come from men. That’s a difference of 420 million hours per week. Valuing time at $15 per hour — which clearly is a floor — the size of the caregiving gender gap can be quantified as $325 billion per year (420 million hours per week x $15 per hour x 52 weeks).

CONVENTIONAL PART-TIME JOBS, FLEXIBILITY, AND WAGES

It’s important to stress that working a conventional part-time job — say, in the retail sector —typically does not solve the unpaid care issue. Research shows that conventional part-time employment is less flexible and lower-paid than full-time employment. For example, a February 2022 report from the Bureau of Labor Statistics used newly collected data to ask the question: “Does part-time work offer flexibility to employed mothers?” The authors’ answer was no.

…mothers working part-time are employed in jobs that lack many of the attributes that would characterize these jobs as flexible. Mothers in part-time jobs were less likely to have paid leave, work-at-home access, and advanced schedule notice. Although part-time jobs require fewer work hours, these shorter work hours may come at a cost of reduced flexibility, pay, and availability of family-friendly benefits.

For example, the report noted that mothers who worked part-time were less likely to have access to paid leave. Only 29.3% of mothers who were part-time workers had access to paid leave, compared to 76.0% of mothers who worked full-time.

Moreover, the report showed that employed mothers have less control over their work schedule in part-time jobs. According to the data, 22% of mothers in part-time jobs had less than a week’s notice of their work schedule, compared to 10% percent of their full-time counterparts. Similarly, only 50% of employed mothers in part-time jobs had at least 4 weeks advance notice of their schedule, compared to 71% for full-time employed mothers.

Other studies show similar results. “Among 30,000 employees at 120 of the largest retail and food-service firms in the United States… we find that a third of workers are involuntarily working part-time: They usually work fewer than 35 hours and would like to be scheduled for more hours at their job.”

Then there’s the question of pay. BLS data shows that part-time jobs pay considerably less than full-time jobs. Across the private sector, as of June 2022, average hourly wages and salaries for part-time workers came in at only $16.60 per hour, 47% below average full-time wages and salaries. Part-time work is also paid much less within the same occupational category. For example, within service occupations, part-time workers are paid wages and salaries of $13.16 per hour on average, 26% than full-time workers. Within sales and related occupations, part-time workers are paid $13.98 per hour on average, a full 55% less than full-time workers.

Obviously, part of that gap is because part-time workers have different demographic and education characteristics than full-time workers. But even taking those differences into account, the wage penalty for part-time work is still huge. According to a 2020 study, part-time workers “are paid 29.3% less in wages per hour than workers with similar demographic characteristics and education levels who work full-time. Even after controls for industry and occupation are added, part-time workers are paid 19.8% less than their full-time counterparts. … By gender, the adjusted wage penalty is 15.9% for women and 25.8% for men, suggesting that men pay a noticeably higher price for working part time.”

Moreover, “within all occupational groups, mothers earned less per hour when they worked part-time rather than full-time.” Most strikingly, “women working part-time in service occupations and sales and office occupations earned 75% of the earnings of their full-time counterparts, or 25 cents on the dollar less per hour.”

CHARACTERISTICS OF PLATFORM WORK FOR THE CARE ECONOMY

So far, we have established that unpaid care work is pervasive across the economy. Moreover, the high time demands and unpredictability of unpaid care suggests that caregivers would prefer work that leaves them enough time to provide care; is flexible enough to adapt to care crises; and does not require them to absorb a lower hourly wage for the “privilege” of working part-time.

Yet it is clear that conventional part-time work is profoundly biased against precisely the caregiving groups that would want to take advantage of it. With part-time work having lower hourly pay and potentially less flexibility, many people with care responsibilities opt for full-time jobs, or not working at all.

Table 4 shows the distribution of unpaid caregiving hours across full-time and part-time employees, and people who don’t have paid work, broken down by gender. We see that less than 14% of unpaid caregiving hours come from part-time employees. That low figure shows how problematic conventional part-time work is for people doing unpaid caregiving.

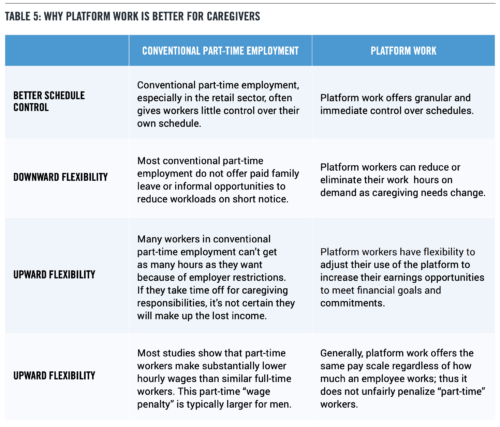

By comparison, platform-based work is better suited to people with unpaid care responsibilities. Table 5 lays out the reasons why. These include better schedule control, downward flexibility in work hours, upward flexibility in work hours, and earnings consistency. Let’s discuss each of these in turn.

Better control over schedules: As documented in the previous section, conventional part-time employment, especially in the retail sector, often gives workers little control over their own schedule. By contrast, platform economy work offers workers granular and immediate control over their own schedule. Given the unpredictability of caregiving responsibilities, that control is a huge advantage.

Downward flexibility is the ability of the worker to choose to reduce hours on short notice to deal with unpredictable caregiving issues. That is a major advantage of platform work for unpaid caregivers. They can choose totally customized working hours, such as being home when children are home from school. They can adjust their working schedules to match unforeseen shortterm changes in care arrangements, such as school being closed for a day. And they can step away from their work for extended periods to deal with major health crises that require focusing on caregiving responsibilities.

Upward flexibility can be defined as the ability of platform workers to adjust their use of the platform to increase their earnings opportunities to meet financial goals and commitments. That includes paying for essentials such as food and housing; paying for extras such as gifts and vacations; paying off debt; and saving for retirement or home purchase.

Upward flexibility is a key characteristic of platform work that differentiates it from an employer-employee relationship. In general, most conventional jobs are time-capped, in the sense that the worker needs special permission from their immediate supervisor or higher-ups in order to work more hours. Someone who needs to take off two weeks to care for their aging parent has no guarantee of getting enough hours to make up for the lost income, especially if the company is operating under a tight budget.

Upward flexibility provides a way of reconciling unexpected caregiving responsibilities while still meeting the family’s financial goals and commitments. Upward flexibility is especially important for low-income households that otherwise may struggle to stay afloat and take care of their children and parents at the same time.

Earnings consistency: Conventional part-time work usually incurs a wage penalty; most studies show that part-time workers make substantially lower hourly wages than similar full-time workers. This part-time “wage penalty” is typically larger for men. By contrast, platform work generally offers the same pay scale no matter how much time a worker puts in. To the extent that there are small wrinkles in the pay structure, such as incentives for driving during high-demand periods, they are mostly available to all drivers. Thus, platform work does not unfairly penalize workers for the “privilege” of working part-time.

IMPLICATIONS

The stresses of unpaid caregiving responsibilities are not well-suited to conventional part-time employment, forcing people to either work full-time or withdraw completely from the workforce. The choice is especially tough for people working in retail, service, or production occupations, which have less flexibility even than full-time jobs. And because women typically do two-thirds of the unpaid caregiving, the lack of a good flexible alternative falls even more heavily on them.

Platform work provides an alternative that offers better scheduling and earnings opportunities for unpaid caregivers. Rather than requiring a choice between full-time work and no paid work at all, there is a flexible alternative.

In addition, platform work may help spread the burden of caregiving. Consider the caregiving gender gap. As shown in Table 1, 49% of women aged 25-64 who work part-time are unpaid caregivers for household or non-household members. That’s according to the 2021 American Time Use Survey. But only 30% of men aged 25-64 who work part-time are caregivers. That’s a huge gap. By contrast, a 2021 survey of drivers on one platform shows that 56% of male drivers report that they “routinely provide care for family members or other loved ones” almost identical to the 61% of female drivers who report being caregivers. While these numbers are not directly comparable to the figures produced by the ATUS, the much smaller gender gap for the platform survey suggests that platform work makes it easier for men to combine part-time work with caregiving.

This reduced caregiving gender cap could be because men who have unpaid caregiving responsibilities, whether for children or adults, are more likely to seek out flexible platform work. Alternatively, men who are already doing platform work find it easier to take on unpaid caregiving without changing their overall goals and commitments, since they can add on more hours of work as needed to make up for the time spent on caregiving. Either way, platform work is associated with a more even distribution of caregiving responsibilities across genders.

As America ages, navigating the stress of the Care Economy in a fair way is going to become increasingly important. Platform work has an important role to play.

Over the last several weeks, there has been increased focus and attention on the competition and antitrust debate in Washington. There has been a debate about the connection between these policies and efforts to address historically high inflation. With real consequential decisions looming for consumers, it’s perplexing why the administration chooses to focus on industries that provide consumers with more choices of quality products at competitive prices, such as the beer industry.

Yet, the Biden administration has voiced its concern. In a February report, the U.S. Treasury claims that the beer industry is facing increasing consolidation, lessening consumer choice, and ultimately asks that regulators evaluate whether mergers in the beer industry are providing fewer options for American customers.

The future of Social Security and Medicare has unexpectedly become a central point of contention in the final week before the 2022 midterm elections. As the two biggest non-emergency spending programs in the federal budget and the foundation of retirement security for nearly all American workers, it makes perfect sense to have a conversation about Social Security and Medicare during election season – particularly since both programs face serious financial challenges as our population ages. Unfortunately, the debate currently playing out on the campaign trail is devoid of the serious substance voters deserve, and it’s abundantly clear that neither party has a good plan to secure these programs for current and future beneficiaries.

Sen. Rick Scott (R-Fla.), who leads the GOP’s Senate campaign arm, kicked off the discourse when he released a proposal that would allow all federal programs – including Social Security and Medicare – to expire if not reauthorized every five years. Sen. Ron Johnson (R-Wis.), a far-right senator who is up for re-election next week, then suggested requiring the programs be reauthorized annually. Such a radical change that would enable these essential programs to suddenly vanish every few years would be catastrophic for American workers, who must plan their retirements around them years or even decades in advance.

The Progressive Policy Institute (PPI) recently commissioned a national survey by IMPACT Research of midterm voters’ attitudes on competition issues across a variety of industries. The survey found that a large bipartisan majority of voters are not focused on competition issues and do not want Congress or the federal government to take new regulatory action within the beer industry, as outlined in the Treasury Department’s February 2022 report. The polling finds that inflation is top of mind for likely 2022 voters and they generally don’t blame companies for high prices across industries.

“This data shows that overwhelmingly, voters want Congress and the Biden Administration to focus on inflation and the rising cost of living — and not on imposing unnecessary regulations on successful U.S. companies and a thriving industry. Americans have more choices for beer and more opportunities to buy from different brewers than ever before, with over 9,000 in the U.S. alone,” said Lindsay Mark Lewis, Executive Director at PPI. “This isn’t the time or place for the White House to raise prices on working families.”

Inflation continues to be the top priority of voters ahead of the 2022 midterm elections, while increasing competition between big companies ranks last. According to IMPACT Research’s findings, voters have concerns that new rules or regulations would raise the price of beer. PPI found in September 2021 that beer actually had a low rate of inflation compared to the overall price levels for personal consumption expenditures.

The memo on this exclusive polling can be found here.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C., with offices in Brussels and Berlin. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Europe has ambitious targets for telco connectivity – and very real investment needs. But what’s the best way to attract the capital Europe so clearly requires? Some say the best idea is a tax or fee leveraged on so-called “content and application providers” to create a unique, two-sided market – generating new revenue streams for telcos but adding additional costs to consumers and content producers alike. Others see an opportunity for the European Commission to build on its landmark approach to modern telecommunications: creating framework conditions that attract investment, open markets to new entrants and drive forward a vibrant European data economy in a triple win for citizens, businesses and government alike.

At this high-level roundtable, co-convened by two leading transatlantic think tanks – The Lisbon Council in Brussels and Progressive Policy Institute (PPI) in Washington DC – leading telecommunications-sector experts will present new evidence and incisive analysis intended to form a backdrop to ongoing debate on Europe’s telco financing needs. Michael Mandel, vice-president and chief economist of PPI, and Malena Dailey, technology policy analyst, will present Funding the Next Generation of European Broadband Networks, a new policy brief comparing telco investment strategies between the U.S. and Europe and asking a crucial question: who got it right?

A High-Level Panel of leading telco experts will chime in with additional contributions on the outlook ahead.

Panelists:

Malena Dailey, technology policy analyst, PPI; co-author, Funding the Next Generation of European Broadband Networks

Michael Mandel, vice-president and chief economist, PPI; co-author, Funding the Next Generation of European Broadband Networks

Konstantinos Masselos, president, Hellenic Telecommunications and Post Commission, Greece; professor, department of informatics and telecommunications, University of Peloponnese; vice-chair (incoming), Body of European Regulators for Electronic Communications (BEREC)

Rita Wezenbeek, director, connectivity, directorate-general for communications networks, content and technology, European Commission TBC

Paul Hofheinz, president and co-founder, the Lisbon Council (Moderator)

Superbugs: The Coming Global Crisis to our Public and Economic Health

Wednesday, September 21, 2022

2:00 p.m. — 3:00 p.m.

Zoom Webinar

About this event

Join public health experts and economists for a conversation on the coming global crisis: antimicrobial germs, or ‘superbugs’.

The Progressive Policy Institute (PPI) recently published a new report, titled “The World Needs Better Incentives to Combat Superbugs” which called for swift action on this growing crisis. As outlined in their new report, antimicrobial resistant germs are killing tens of thousands of Americans annually, and the problem is only getting worse in the post-COVID age.

Hear from leading experts about the health and economic costs of the crisis, and the policy actions needed now.

Panelists: Amanda Jezek, Senior Vice President for Public Policy and Government Relations at the Infectious Diseases Society of America (IDSA) Dr. Robert Popovian, PPI Senior Fellow for Health Policy (Moderator) Dr. Michael Mandel, PPI’s Chief Economist

The Progressive Policy Institute (PPI) released a new report today calling for action from U.S. policymakers on the global “superbug” crisis. Antimicrobial resistant germs are killing tens of thousands of Americans annually, and the problem is only getting worse in the post-COVID age. The paper is titled, “The World Needs Better Incentives to Combat Superbugs”and is co-authored by Arielle Kane, Director of Health Care at the Progressive Policy Institute and Dr. Michael Mandel, Vice President and Chief Economist at the Progressive Policy Institute.

“Without changing how we use and develop new antimicrobials, millions more people will die, and health advances will be lost,” the co-authors write in the report.

Ms. Kane and Dr. Mandel outline a troubling public health trend that has far-reaching implications – including global economic stressors. The report authors note that roughly 35,000 Americans are killed annually by germs resistant to antimicrobials, or medicines like antibiotics and antifungals that are used to treat infections. These infections are on the rise, and without policy intervention, could kill 12 million people annually worldwide by 2050.

This crisis extends beyond a public health crisis – it is also putting the global economy at risk. According to a World Bank study, these infections could also reduce global GDP by 2%-3.5% by 2050.

The authors call for three methods in combating superbugs and the continuation of this trend, including curtailing the overuse of antimicrobials in medicine, limiting the use of antimicrobials on animals and agriculture; and new incentives to invest in the development of new antimicrobials.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Ben Ritz, Director of the Center for Funding America’s Future project at the Progressive Policy Institute (PPI), released the following statement regarding President Biden’s executive order to cancel up to $20,000 of student debt for most borrowers:

“We are disappointed that the Biden administration has caved in to left-wing demands to pursue mass debt cancellation through executive action. This decision will cost taxpayers much more money than the Inflation Reduction Act will save for the foreseeable future and undermine the administration’s claim that it is doing everything it can to bring rising prices under control.

“Whether it’s through inflation today, or higher taxes and spending cuts tomorrow, workers who don’t reap the benefits of a college education will bear the costs of canceling debt for those who do. Policymakers should instead be focusing on finding ways to control the underlying problem of skyrocketing tuition and provide stronger post-secondary pathways to good jobs that are more affordable and flexible than a traditional four-year degree.

“Attempting to grant mass debt cancellation by executive order also risks setting a dangerous precedent that would allow future presidents to unilaterally spend over a trillion dollars of taxpayers’ money without explicit approval from their representatives in the House and Senate. Congress and the courts must set clear guardrails to prevent future presidents from abusing their discretion and usurping the power of the purse.”

Listen to Ben’s recent TV and radio interviews on student debt cancellation.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Next week, President Biden’s executive order imposing a freeze on student loan repayments and interest accrual is set to expire. It’s almost guaranteed that the president will extend the freeze for a fifth time because no effort has been made to notify borrowers that payments are resuming, and to do so now would be providing too little time to prepare.

But in addition to extending the current freeze, Biden is under tremendous pressure from a years-long campaign by leftwing activists to cancel at least $10,000 of debt per borrower under a certain income threshold. This is a regressive and fiscally irresponsible demand likely to further estrange Democrats from working-class voters. Here are six reasons why he should develop a plan to resume payments in a timely manner that doesn’t include mass debt cancelation by executive order.

The American Rescue Plan Act (ARP) passed in March 2021 provided $525 billion in COVID-19 relief to states and local governments, including $350 billion in Fiscal Recovery Funds (FRF) to prevent budget constraints from forcing public services cuts as they did after the 2008 recession. However, many states have ended up with budget surpluses as the economic situation has improved and are now debating the best uses for extra revenue, with some deciding to finance inflationary policies such as tax cuts and stimulus checks. States that are not doing so already should shift their uses of FRF to long-term investment and COVID-19 relief, which will not worsen inflation or create budgetary burdens in future years.

When the ARP was passed, states were given flexibility with funding use, but there were a few federal strings attached. These included prohibitions on making tax cuts above a certain size, funding public employee pensions, and paying off existing debts. However, many states have fought against the prohibition on tax cuts, with attorneys general in 21 states attempting to overturn it. State officials claim that tax cuts will provide consumers with additional resources to compensate for rising prices, but these tax cuts will only worsen inflation rates as people effectively bid up prices. No doubt tax cuts are popular, but states shouldn’t be using federal relief dollars to pump up demand, thereby contributing to a worsening inflationary cycle.

Tax cuts will also damage the states’ long-term fiscal health. After the 2008 recession, states faced funding shortfalls that resulted in public service cuts. This is precisely what the federal government sought to avoid with the ARP. State tax cuts will undermine this goal because some states have constitutional obstacles to raising taxes, like referenda or supermajority requirements, that make it harder politically to reverse tax cuts than to enact them. As a result, states are increasingly likely to face revenue shortfalls once ARP funding is exhausted.

Although Republican-controlled states are leading the tax-cutting craze, other states are pursuing inflationary policies as well. For example, California Governor Gavin Newsom (D) has proposed giving Californians $400 for every car owned by the household to defray sky-high gas prices. By insulating people from gas price spikes, this proposal would boost demand, putting upward pressure on prices just as they are beginning to fall back to earth. This proposal also comes with a high opportunity cost. As PPI’s Ben Ritz wrote recently for Forbes, the cost of this new fuel subsidy could pay for COVID-19 tests, vaccines, and treatments for the entire nation.

Meanwhile, the Republican-controlled government in Georgia approved stimulus checks of up to $500 for constituents, and Florida Governor Ron DeSantis (R) has supported a planned gas tax suspension in October, which would cost $200 million. Lawmakers on both sides of the aisle need to focus on their states’ fiscal well-being and keeping prices down instead of throwing federal dollars at their constituents.

The best way for states to help get inflation under control would be to pump the brakes on all un-offset spending for the foreseeable future. But since the federal government is requiring them to spend down their FRF within the next two years, and no governor is likely to leave that money on the table, states should focus on the most effective uses of funds which will improve long-term economic outcomes.

For example, states should start by fully funding public services if they are still experiencing revenue losses resulting from the pandemic. But because the ARP gave states far more money than they needed to fill budget shortfalls, relief funds will mostly need to be spent on new purposes. States should prioritize continuing the fight against COVID-19 infections, particularly as the highly contagious BA-5 variant spreads. More tests, treatments, and vaccines are needed, along with investments in medical facilities and equipment such as ventilators and PPE.

States could also use FRF for mental health and violence prevention programs. As of March 2022, the pandemic had caused a 25% increase in the prevalence of anxiety and depression as people faced fear, isolation, and grief. Increases in violence have also been observed, particularly in domestic violence against women who were isolated with their abusers, and in gun violence as structural inequities fueling gun violence worsened. Along with measures to fight COVID-19 infections, mental health and violence prevention programs can improve and even save lives, making them a worthwhile use of funding.

Another good use of FRF would be responding to pandemic-induced economic losses. Low-income households bore the brunt of COVID-19 deaths and job losses. They face the largest barriers to recovery and ought to be the focus of relief efforts. Investment in education is sorely needed to deal with steep learning losses for kids as well as many parents’ long absences from labor markets. Temporary expansions of tutoring and job apprenticeship programs can be scaled back more easily than tax cuts can be repealed.

Finally, states should use spare ARP funds to make one-time investments in infrastructure that will support economic growth for years to come. For example, business and school closings during the pandemic drove home the need for greater access to broadband. While the Infrastructure Investment and Jobs Act (IIJA) is providing funding for many new projects, ARP funding gives states the flexibility to meet the immediate needs of their communities without having to apply for specific grants. Investing in infrastructure, especially with one-time investments which will not create burdens in future years, will benefit citizens without harming states’ fiscal health or worsening inflation.

States should focus on projects that will not burden their budgets once FRF runs out and which will help citizens still battling the effects of the pandemic. Making investments in future economic growth and public service delivery, while continuing to fight COVID-19 infections, is a wiser course for states than burning through a one-time federal windfall.

Ben Ritz, Director of the Center for Funding America’s Future at the Progressive Policy Institute (PPI) released the following statement:

“The Progressive Policy Institute applauds Senate Democrats for passing the Inflation Reduction Act of 2022. This historic bill will help combat the climate crisis and promote American energy security with the largest investment in clean energy ever. The health care provisions will reduce costs for millions of families. New resources to help the IRS crack down on tax cheats will reverse the defunding of our tax police and ensure all Americans pay their fair share. And the bill would not only cover the cost of these policies, it would also reduce deficits by more than a quarter trillion dollars over the coming decade, which will help bring inflation under control.

“As is the case for most bills, the Inflation Reduction Act is not perfect. Its deficit reduction depends on a flawed plan to outsource tax policy to the Financial Accounting Standards Board, a private organization that solely exists to serve the information needs of investors rather than determine an economically efficient tax base. Other, better revenue-raisers were dropped, leaving the bill’s modest savings unable to offset the deficit increases created by legislation Congress passed just last month. And we’re sorry that many other progressive priorities we advocated for throughout the reconciliation process, such as closing the Medicaid coverage gap, could not be included.

“But the final bill is still far better than the mishmash of half-baked social programs and irresponsible budget gimmicks that many on the left were pushing earlier in the reconciliation process. PPI is proud of the role our Reconciling with Reality framework and analysis of various proposals played in shaping this historic legislation. We thank Senator Manchin, Leader Schumer, Speaker Pelosi, President Biden, and all the other lawmakers whose leadership contributed to this great outcome.

“The Inflation Reduction Act, together with the Bipartisan Infrastructure Law and the CHIPS and Science Act, represents the largest increase in public investment since the Johnson administration – it is a historic accomplishment for Democratic leaders in Washington. Now we urge them to finish the job by passing the permitting reform legislation they’ve promised to cut red tape, maximize taxpayers’ bang for their buck, and get these critical investments built in a timely manner. We also hope that additional legislation and executive orders they pursue later this year will build upon rather than squander the Inflation Reduction Act’s hard-earned deficit reduction.”

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.