The Progressive Policy Institute (PPI) released the following statement on the Inflation Reduction Act of 2022:

“PPI applauds Senator Joe Manchin and Majority Leader Chuck Schumer for returning to the negotiating table and agreeing on a historic reconciliation bill that would invest in clean energy, lower the cost of health care, and modestly reduce federal budget deficits. This bill advances precisely the kind of pro-growth, innovative climate policy that PPI has been calling for throughout the process and that America needs. It will not only spur new investments, create jobs, reduce emissions, and critically lower the cost of living for millions of Americans, but also strengthen our country’s economic future for generations to come.

“This deal is a major step forward for Congressional Democrats and the American people, and while it does not include as many legislative priorities as the original framework, PPI is encouraged to see a few well-funded programs that will result in transformational change rather than a broad progressive wish list. We are also encouraged that the deal includes a plan for taking up additional legislation to reform federal permitting processes later this year, which has long been a PPI priority.

“This package isn’t perfect. It doesn’t close the Medicaid coverage gap, or permanently fix the ACA subsidy cliff. More deficit reduction would have strengthened the legislation’s inflation-fighting potential. But the perfect cannot be the enemy of the good, especially when Democrats have an ideologically diverse caucus with no votes to spare in the Senate. Democrats should take the win now and continue to work on making further progress in these areas next Congress.

“Together with the CHIPS and Science Act and the bipartisan infrastructure law, the Inflation Reduction Act of 2022 will cement President Biden’s legacy of the largest increase in domestic public investment in modern history. Democrats in both chambers should act quickly and decisively to advance these bills and secure a stronger future for all Americans.”

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

The passage of the Infrastructure Investment and Jobs Act (IIJA) in November marked the first large investment in American infrastructure in decades. The $1.2 trillion law includes over $550 billion in sorely needed new spending for areas including broadband, transportation, and sustainability. The Biden administration has prioritized quick implementation, but tools for accountability and efficiency have been lacking. To prevent misuse or wasting of funds, more centralized sources of information about current projects should be available to public entities, private sector investors, and citizens. Actions to increase accountability and efficiency will improve public confidence in the administration and ensure funds are being used for their intended purposes.

So far, around $110 billion in funding has been released and over 4,000 infrastructure projects are underway. Two recent projects include the Airport Terminal Program, which just announced $1 billion for improving terminals in 85 airports nationwide, and the Internet for All initiative, which provides funding for broadband infrastructure. The rapid action taken to implement the IIJA reflects the White House’s awareness of the law’s transformative potential. Mitch Landrieu, White House Senior Advisor and Infrastructure Implementation Coordinator, told CBS, “If we can … learn how to do big things again, which we are confident that we can do, it’s gonna be a wonderful thing to see.”

The Biden administration has demonstrated a desire to improve accountability and efficiency after the rapid dispersal of COVID-19 relief funds resulted in waste and fraud. The Office of Management and Budget (OMB) issued a guidance memorandum to executive branch agencies directing them to work closely with Inspectors General and OMB during IIJA implementation. This collaboration should result in the evaluation of risks in implementation plans to reduce the potential for costly disruptions. In May, the White House released a Permitting Action Plan outlining the administration’s strategy for making sure environmental reviews and permitting processes are effective, efficient, and transparent, illustrating the administration’s determination to accelerate permitting processes to avoid expensive delays.

The White House has also created a Permitting Dashboard to allow the public to keep track of approved projects, adding another level of accountability. Additionally, in May, the administration released the Bipartisan Infrastructure Law Technical Assistance Guide to help communities and entities across the country access and employ infrastructure funding. These actions are good first steps for promoting transparency and efficiency because they show the American people what actions have been taken and provide resources to streamline implementation.

But there is still room for improvement. A main goal of the administration should be to centralize information about how IIJA funding is being spent and what funding opportunities are currently available. This interactive map released by the White House for the six-month anniversary of the law’s passage is useful for cursory examinations of funding outlays, but only provides information about total funding for each state and the percentage of funding spent on each of three main categories: Transportation; Climate, Energy, & Environment; and Other.

This map could be a powerful tool if it contained details about specific programs to assure the public that their taxpayer dollars are being spent wisely. Public accountability is essential and could keep state and local governments on track. For instance, one announced program is the Carbon Reduction Program (CRP), which provides states with funding for projects designed to reduce carbon dioxide emissions from on-road sources. However, this program allows states to transfer up to 50% of CRP funds to another state apportionment from the Department of Transportation, meaning outcomes from the CRP could vary greatly depending on state priorities. Transparency about each state’s use of CRP funding could ensure governments are held accountable for using this money as it was intended.

The Biden administration should also take steps to centralize information about available funding so eligible entities do not miss opportunities. With programs spanning multiple executive branch departments, it is difficult to track every program being announced. One tool, the Grants.gov database, is not operating as efficiently as it could be. When “Infrastructure Investment and Jobs Act” is selected in this database, few funding opportunities come up even though there are many more IIJA-funded projects elsewhere in the database. The federal government is therefore running the risk of communities missing out on much needed funding by categorizing projects incorrectly.

While technical assistance is being made available as stated in the White House guide, it is also important that outreach to stakeholders is increased. For instance, individuals and households often qualify for internet service discounts through the Affordable Connectivity Program (ACP) because they are eligible for SNAP, Medicaid, WIC, Pell Grants, or another assistance program, but there does not appear to have been any ACP information distributed through these programs to participants. Private sector inclusion in project planning and management also needs to be enhanced so the most efficient technologies and construction methods are utilized. Helping communities leverage private sector investment can ensure that even projects that are not part of competitive funding programs meet high standards for future performance.

The IIJA represents a meaningful investment in America’s future, but to reach its full potential, the federal government needs to consolidate information about its implementation. This will allow all stakeholders, from individuals to states, to hold the government and other entities accountable and access opportunities to better their communities.

Ben Ritz, Director of the Center for Funding America’s Future project at the Progressive Policy Institute (PPI) released the following statement:

“Earlier this week, PPI encouraged Congressional Democrats to give high priority to passing the U.S. Innovation and Competition Act (USICA) and a reconciliation bill that includes significant deficit reduction and clean energy provisions. Unfortunately, media accounts suggest that both initiatives are shrinking.

“We shared Sen. Manchin’s concerns about the original reconciliation bill’s overreaching and likely impact on inflation. But walking away from a bill with roughly half a trillion dollars of deficit reduction and significant investments in increasing energy supply would squander the best chance Congress has to help the Federal Reserve rein in rising prices. We hope he and Sen. Schumer will not give up on negotiating a compromise on these components of a reconciliation bill.

“Pro-growth Democrats who want to see the United States outcompete China also should be concerned about reports of a plan to vote next week on a bill that only includes funding for semiconductor subsidies. Losing government R&D funds and other key provisions in the U.S. Innovation and Competition Act (USICA) would be an enormous setback for America’s innovation and scientific prowess.

“We understand that Senate Minority Leader Mitch McConnell’s blindly partisan decision to withhold Republican support from a conferenced innovation bill complicates its path to passage. But retreating to a CHIPS-only approach would unnecessarily doom many higher priority pro-innovation policies. Instead, we urge Speaker Pelosi to put the full Senate-passed USICA on the floor for a vote in the House to circumvent McConnell’s obstructionism.

“Democrats must not snatch defeat from the jaws of victory.”

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Today, the Progressive Policy Institute(PPI) released its annual Investment Heroes report, which shows companies with high and sustained capital investment in the United States have helped hold down price increases in the digital sector throughout the past year of otherwise record inflation. The report, titled “Investment Heroes: Fighting Inflation with Capital Investment”is authored by Dr. Michael Mandel, Vice President and Chief Economist at PPI, and Jordan Shapiro, Data and Economic Analyst at PPI.

Nine of the 11 companies topping this year’s Investment Heroes list are in tech, broadband, or e-commerce. Amazon invested an amazing $46.7 billion in the U.S. in 2021, according to PPI estimates. AT&T and Verizon tied for second place at $20.3 billion, and Alphabet invested $18.7 billion in the U.S. in 2021.

PPI has created a unique methodology using publicly available financial statements from non-financial Fortune 200 companies to independently identify the top companies that were investing in the United States. These companies — our “Investment Heroes” — have helped to create good jobs, boost capacity, and reduce inflation as we recover from the aftershocks of the COVID-19 pandemic.

“Policymakers should praise and encourage those companies who invest in the United States, keep prices low, and reduce vulnerability against future shocks. That’s a clearcut win for consumers, workers, and the American economy,” write report authors Dr. Michael Mandel and Jordan Shapiro.

“Conversely, government leaders can’t pursue policies that reduce or discourage domestic capital investment and then complain when we don’t have enough capacity to meet our changing needs at an affordable price, whether it’s energy or semiconductor chips or anything else. In particular, it’s perplexing that Congress is putting so much energy into tech antitrust, when the sector has been a low-inflation, high-investment star performer,” the authors conclude.

See the full list of PPI’s 2022 Investment Heroes:

Read and download the full report here:

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

The theme of this year’s Investment Heroes report is the powerful link between high investment and low inflation. Every year, the Progressive Policy Institute (PPI) analyzes the financial reports of large U.S. companies and ranks them by their capital investment in the United States. Nine of the top 11 companies on this year’s Investment Heroes list are in tech, broadband, or e-commerce industries. Amazon is at the top of the list, investing $46.7 billion in the United States in 2021 according to estimates by PPI. Tied for second are AT&T and Verizon, followed by Alphabet, Meta Platforms, Microsoft, Intel, Walmart, Comcast, Duke Energy, and Apple.

But here’s an important point for policymakers: As shown in a recent PPI paper, inflation in these digital industries has been extraordinarily low.1 High and sustained investment in new equipment and technology has created enough capacity to hold down most price increases in the digital sector, even as inflation has soared in other parts of the economy. For example, the price of wireless services at the consumer level was down by 0.7% in the year ending May 2022. In the year ending May 2022, the price of online advertising by internet publishing and web search portals only rose 0.6%.2

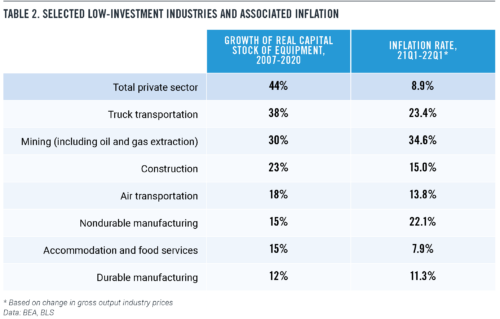

Policymakers should note that the link between investment and inflation works in the other direction as well: Low-investment industries are typically supply-constrained and more likely to boost prices when hit by an unexpected shock. Indeed, low-investment industries — including most of manufacturing, construction, trucking, air transportation, accommodations and food service, and mining — have all shown moderate to high inflation rates. And it’s generally agreed that domestic capital investment in the semiconductor industry has lagged, one of the few sectors of the digital economy contributing to inflation.3

For better or for worse, the case of the oil and natural gas industry illustrates the ways that low investment can lead to higher inflation.

Domestic investment in oil and gas drilling and exploration peaked in 2014 and collapsed by nearly two-thirds by 2016, according to data from the Bureau of Economic Analysis (BEA), as oil and gas companies faced a combination of low prices, pressures to use less fossil fuels for environmental reasons, and problems of pipeline and refinery capacity. And even though several energy production companies are still on our Investment Heroes list, their domestic capital outlays have continued to fall in the face of clear signals discouraging investment in fossil fuels. Exxon Mobil, in particular, decreased its U.S. capital spending by 43% from $11.2 billion in 2020 to $6.4 billion in 2021. This left the U.S. vulnerable to rising oil and gas demand and the unexpected shock of Russia’s invasion of Ukraine.

The key word here is “vulnerable.” No one is denying that free trade and globalization helped hold down prices for years. But when globalization is accompanied by a lack of domestic investment, the result is an inevitable increase in vulnerability and a loss of resilience. American workers become more vulnerable to foreign competition and downward pressure on real wages; American consumers become more vulnerable to domestic and international shocks and higher inflation; the country as a whole becomes more vulnerable from a national security perspective.

The policy and political implications are clear: Policymakers should praise and encourage those companies who invest in the United States, keep prices low, and reduce vulnerability against future shocks. That’s a clearcut win for consumers, workers, and the American economy. In some cases, like the semiconductor industry, it may be appropriate to use government funds to support domestic investment.

Conversely, government leaders can’t pursue policies that reduce or discourage domestic capital investment and then complain when we don’t have enough capacity to meet our changing needs at an affordable price, whether it’s energy or semiconductor chips or anything else. In particular, it is perplexing that Congress is putting so much energy into tech antitrust, when the sector has been a low-inflation, high-investment star performer. We would be better off as a country if other industries followed the tech/ecommerce/broadband lead and invested in America.

THE LINK BETWEEN INVESTMENT AND INFLATION

Over the past four years, Amazon, the top company on our list this year, has invested more than $115 billion in the United States, according to PPI estimates. This level of capital spending has powered unprecedented job creation, as Amazon operates e-commerce fulfillment centers across the country, and now employs more than 1.1 million workers in the United States.4

But perhaps equally important to U.S. consumers, Amazon’s investments in new logistics capacity have also helped keep down inflation, despite pandemic-related shocks. According to the Bureau of Labor Statistics (BLS), margins in “electronic and mail-order shopping” have shrunk by 6.4% in the year ending May 2022, compared to a 9.3% increase in margins for retail overall.5 Narrower margins for e-commerce means lower prices for consumers who shop online.

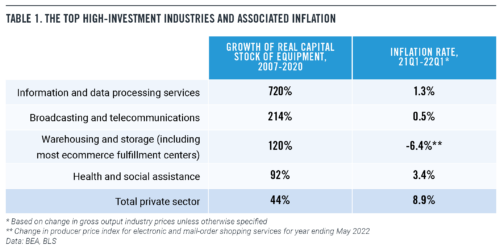

Indeed, tech, broadband, and ecommerce have all shown extraordinarily high long-term growth in their stock of productive capital (Table 1). For example, from 2007 to 2020, the stock of productive equipment in the information and data processing services rose by 720%, compared to a 44% increase for the private sector as a whole. The second biggest percentage gain was in the telecommunications and broadcasting industry, and the third biggest percentage gain was in the warehousing industry, which reflects the growth of e-commerce fulfillment centers.

At the same time, the tech, broadband and e-commerce industries have shown extraordinarily low rates of price increases during this inflationary surge. In addition to the shrinking margins in e-commerce already mentioned, the price of broadband access is down by 0.2% at the producer price level in the year ending May 2022. Overall, prices in the telecommunications and broadcasting industry have only risen by 0.5% in the year ending the first quarter of 2022, according to the BEA, despite everyone’s increased need for broadband and wireless connections. Prices in the information and data processing industry, which includes most internet companies, are up by only 1.3% in the year ending with the first quarter of 2022.

On the other hand, low-investment industries are more likely to be prone to inflation. Consider the paper and wood product industries. Since the pandemic began, Americans have been bedeviled by a series of seemingly inexplicable shortages of paper products, running from the great toilet paper gap of early 2020, to more recent shortages of disposable coffee cups6 and tampons.7 The shortages become less surprising when you realize that paper product companies have reduced their domestic manufacturing capacity by 17% since the beginning of the financial crisis in 2007. Capacity in the domestic wood product manufacturing industry is down 23% over the same period.8

Moreover, anyone who studied the economics of supply and demand in college won’t be surprised that prices rose in the paper and wood industries as paper mills closed and capacity shrank. Producer prices in the paper industry have soared by 16% over the past year. And since the pandemic began, producer prices in the wood industry are up a startling 67%.

And the disinvestment continues. Consider paper-making giant Georgia-Pacific, part of privately-owned Koch Industries. In March 2022, GP executives announced that they were shutting down a paper mill in Green Bay, Wisconsin, that had been making tissues and toilet paper since 1901.9 This followed a string of other paper mills and related manufacturing facilities that Georgia-Pacific’s managers had closed in recent years, including GP’s January 2021 announcement that it was shutting a Dixie Cup factory in Easton, Pennsylvania.10 GP has announced specific investments, but the private company is not required to release its overall capital investment figures publicly.

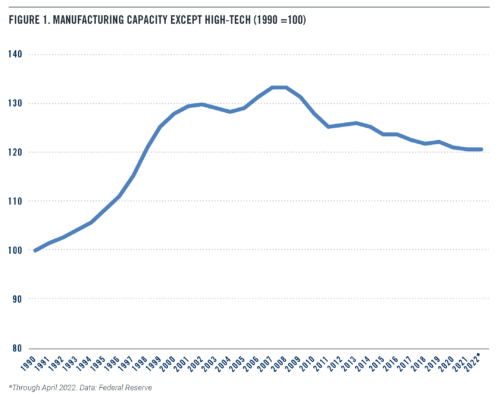

Overall, domestic manufacturing capacity, outside of high-tech, peaked in 2007, and since then has fallen by almost 10% (Figure 1). Over the same period, consumer purchases of goods, outside of high-tech, are up about 45%. With this growing mismatch between supply and demand, the U.S. has become ever more vulnerable to shocks in the global trading system.

Similarly, domestic iron and steel product capacity peaked in 2009, and since then has fallen by 25%, including a continued decline during the pandemic. Not surprisingly, the domestic price of steel has skyrocketed, because there is much less domestic capacity that can be brought online when needed.

When we look outside of manufacturing, we see the same pattern: For example, the stock of equipment such as airplanes owned by the air transportation industry rose by only 18% from 2007 to 2020, far slower than the 44% gain for the private sector as a whole.11 Not surprisingly, producer prices charged by the airline industry, including passengers and freight, jumped by 27% in the year ending May 2022 to their highest levels ever.

THE BIG PICTURE

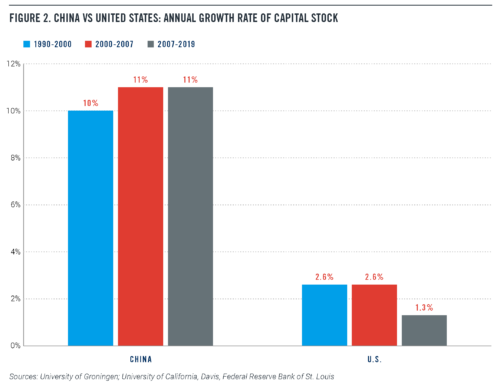

The United States entered the pandemic struggling with a capital investment drought that had lasted more than a decade. During the financial crisis of 2008-2009, domestic nonresidential investment in structures and equipment plunged as a share of gross domestic product, and never really recovered. As a result, the rate of U.S. capital stock growth fell in half, going from an average annual rate of 2.6% from 1990 to 2007, to only 1.3% from 2007 to 2019.

Meanwhile the capital stock in China has been growing at an 11% annual rate. As long as global supply chains worked well, the U.S. domestic investment shortfall didn’t matter too much to consumers (though it did matter to U.S. workers whose productivity and real wages weren’t rising). Inflation was low, held down by a flood of cheap goods coming out of China, the rest of East Asia and Europe.

However, this capital investment drought set up the conditions under which the United States has become more vulnerable to inflation, just like a dried-out forest is ready to burst into flames from an errant spark or lightning strike. Any kind of a shock — like the pandemic, supply chain disruptions, armed conflicts — can translate into price increases.

But some companies have been fighting the prevailing trend of capital spending weakness. Since 2012, PPI has provided unique estimates of domestic capital spending for individual major U.S. companies. Currently, accounting rules do not require companies to report their U.S. capital spending separately. To fill this gap in the data, we created a methodology using publicly available financial statements from non-financial Fortune 200 companies to identify the top companies that were investing in the United States.

We call these companies “Investment Heroes” because their capital spending is helping to create good jobs, boost capacity, and reduce inflation across the country. In 2021, the 25 companies on our list invested $260 billion in the U.S. This year’s list includes 10 tech, broadband, and e-commerce companies; seven energy production and distribution companies; two transportation companies; three automotive companies; two retail companies; and one health care company (Table 3). Later in this paper, we discuss the methodology that we use to estimate these figures.

Let’s look at each company on the list individually:

1. Amazon’s 2021 estimated U.S. capital spending was $46.7 billion, a 38% increase compared to its already impressive 2020 total. Principally, its increase in spending was directed toward augmenting the capacity of its fulfillment centers and growing its cloud services.

2. (tie) AT&T was tied for second with Verizon, spending an estimated $20.3 billion in the U.S. in 2021, up from $17.8 billion in 2020 (adjusted for the change in methodology described below). Its U.S. investment focused on expanding its network capacity.

2. (tie) Verizon Communications, tied for second with AT&T, increased its domestic capital expenditures to $20.3 billion in 2021, up from $18.2 billion in 2020 (adjusted for the change in methodology described below). The company continued to invest in adding capacity and density to its 4G network while building out its 5G network.

4. We estimate that Alphabet invested $18.8 billion dollars on U.S. capital expenditures in 2021. The company directed its investments toward technical infrastructure including servers, network equipment, and data center construction as well as office facilities and building improvements.

5. Meta Platforms came in fifth this year with an estimated $15.6 billion in U.S. capital spending. The social media company continues to invest in data center capacity, servers, network infrastructure, and office facilities. In 2021, the company increased metaverse-related investments.

6. Sixth is Microsoft with an estimated $13.1 billion in domestic capital spending based on its July 2021 10-K, the most recent available. The software company continues to invest in new facilities, data centers, computer systems for research and development, and its cloud offerings.

7. Intel slightly increased its domestic capital expenditure in 2021 to $12.9 billion, up from our estimate of $12.5 billion in 2020. Intel started work on two new fabs in Arizona, and announced investments in Ohio and New Mexico.

8. Walmart spent a reported $10.6 billion on U.S. capital expenditures in its fiscal year ending January 31, 2022, up sharply from $7.8 billion the previous fiscal year. Its investments were principally directed toward supply chain and customer service improvements. In addition, the company invested in online grocery services and selected Spartanburg County, South Carolina, as the location for its new hightech grocery distribution center.12

9. We estimate in 2021 that Comcast invested $10.1 billion in the U.S. Increases in capital spending were directed toward scalable infrastructure and line extensions.

10. Duke Energy invested $9.7 billion, slightly less than its 2020 figure. The decrease in spending was due to lower investment in the commercial renewables segment.

11. Apple is eleventh on this year’s list, investing an estimated $8.1 billion, a 37% increase in domestic capital spending from the previous year. Our estimates are based on Apple’s October 2021 10-K, which is the most recent annual report. The company began plans for a North Carolina campus with 3,000 employees.13

12. Exelon spent $8.0 billion on capital investments in 2021, a slight decrease from 2020.

13. PG&E invested $7.7 billion in 2021, about even with 2020 levels. In 2021, the company announced the beginning of a decade of spending to bury its powerlines as a wildfire prevention strategy.23

14. Fourteenth on the list is Charter Communications with domestic capital expenditures of $7.6 billion, a slight increase from the 2020 figure of $7.4 billion. The increase is due to payments for scalable infrastructure and network upgrades.

15. Exxon Mobil decreased its U.S. capital spending by 43% from $11.2 billion in 2020 to $6.4 billion in 2021. The company decreased its upstream, downstream, and chemical spending. In 2022, the company announced plans for a carbon capture and storage project in Baytown, Texas.

16. Dominion Energy invested $6.1 billion on U.S. capital expenditures, a slight decrease from $6.3 billion in 2020. Dominion is involved in the construction of an American-built wind turbine installation vessel.

17. Chevron’s reported U.S. capital expenditure in 2021 was $5.8 billion, a slight decrease from $6.1 billion in 2020.

18. General Motors invested $4.9 billion dollars in the U.S. in 2021 according to our estimates, a 28% increase from 2020. The company has announced large investments in electric vehicles and battery plants.

19. FedEx’s domestic capital expenditures in 2021 were estimated at $4.5 billion, a very small decrease from our 2020 estimate, based on its July 2021 10-K. The company’s capital spending was directed toward package handling and sorting as well as to aircraft and vehicle spending in their transportation segment.

20. The twentieth company on the list this year is Ford Motor with an estimated $4.3 billion in U.S. capital spending in 2021. The company announced new factories in Kentucky and Tennessee to support electric vehicle production.15

21. ConocoPhillips increased its U.S. capital spending by 41% in 2021 to $4.2 billion. Development activities included investment in the Permian, Eagle Ford, and Bakken regions.

22. Tesla is No. 22 with a big increase in estimated domestic capital spending to $4.1 billion. The increase is due to the construction of a Gigafactory in Texas and expansion of a factory in Fremont, California.

23. HCA Healthcare directed $3.6 billion to capital investments in 2021, an increase from 2020. HCA announced plans to build 3 new hospitals in Florida and 5 in Texas.

24. Target invested $3.5 billion in the United States this year, up 34%.The additional spending was targeted at store remodels, store reopening, and supply chain initiatives. In 2021, the company remodeled 145 stores around the country and expanded digital fulfillment capabilities.

25. The twenty-fifth company to make the list is Delta Airlines with an estimated $3.2 billion in U.S. capital expenditures in 2021. The airline’s capital spending was primarily related to aircraft and airport improvements, in mid-2021, it announced adding 30 new Airbus A321neo models to its fleet.16

METHODOLOGY

Our U.S. Investment Heroes ranking for 2022 follows the same methodology as our most recent report in 2021, with a few small tweaks. We started with the top 200 companies of the 2021 Fortune 500 list as our universe of companies, expanded from the previous 150 companies. We removed all financial companies and all insurance companies except health insurance companies. We also omitted the financing operations of non-finance companies when possible.

Except as noted, we use the global capital expenditure reported on the most recent 10-K through April 2022 as the starting point for the analysis. In this report, we refer to all estimates as “2021,” even if the fiscal year ended in 2022. Capital expenditures generally cover plant, equipment, and capitalized software costs. For energy production companies, capital expenditures can include exploration as well.

For wireless companies, we did not include their often sizable spending on purchases of wireless spectrum as part of capital expenditures, since that category is not counted as investment spending by the economists at the Bureau of Economic Analysis. Companies purchasing spectrum in 2021 notably includes Verizon (which paid $45.5 billion for the licenses it won in a February 2021 spectrum auction) and AT&T (which paid $22.9 billion for spectrum won at the same auction).

The companies in these rankings are all based in the United States. Non-U.S.-based companies were not included in this list because of data comparability issues, although there are many non-U.S. companies that invest in America. Notably, T-Mobile US, with more than $12 billion in purchases of property and equipment in 2021, would have made the Investment Heroes list if it was not owned by Deutsche Telekom.

For transportation companies, our report estimates the booked location of spending on capital expenditures for the company’s most recent fiscal year, rather than how much of those acquired assets are actually being used within the U.S.

Most multinational companies do not provide a breakdown of capital expenditures by country in their financial reports. However, PPI has developed a methodology for estimating U.S. capital expenditures based on the information provided in the companies’ annual 10-K statements and other financial documents. After developing our internal estimate, we contact the investor relations offices of the companies on our top 25 list to ask them to point us to any additional public information that might be relevant. Notwithstanding these queries, we acknowledge that the figures in this report are estimates based on limited information.

Our estimation procedure goes as follows:

If a company has no foreign operations, we allocated all capital spending to the United States.

If a company reported U.S. capital spending separately, we used that figure.

If a company did not report U.S. capital spending separately, but did report changes in global and U.S. long-lived assets or plant and equipment, we used that information plus depreciation to estimate domestic capital spending. As appropriate, we adjust for large acquisitions. That was not necessary this year.

If a company has small foreign operations that were not reported separately, or if the company’s net capital stock is falling, we allocated capital spending proportionally to domestic versus foreign assets, revenues, or employees.

Some adjustments of note:

For Amazon, the methodological issue was their extensive use of finance leases. We chose to specify global capital expenditures as purchases of property and equipment (net of proceeds from sales and incentives) plus principal repayments of finance leases. We then used reported changes in U.S. and non-U.S. property and equipment, net, and operating leases to allocate global capital expenditures, taking into account depreciation and removing the effect of operating leases.

Similarly, as part of our process for estimating domestic capital spending for Microsoft, Meta Platforms, UPS, and Kroger, we included principal repayments on finance leases reported on the company’s 10K, or amortization of finance leases based on 10K data, as part of capital spending.

In previous years for Verizon, we made a small adjustment for foreign operations, even though non-U.S. assets or revenues are not broken out in the company’s 10K. This year we made the judgment call to stop making that adjustment, which had the effect of somewhat increasing Verizon’s estimated domestic capital spending.

AT&T reported vendor-financed purchases of equipment separately from capital expenditures. We made the decision this year to add them back in. We allocated capital spending domestically in proportion to the U.S. share of net property, plant, and equipment.

In the case of Comcast, we allocated all of its cable operations and corporate capital expenditures, including cash paid for intangible assets such as capitalized software, to the U.S. NBC Universal’s capital expenditures was allocated to the U.S. in proportion to our estimate of the US share of NBC Universal’s revenues.

For consistency, we omitted capital spending by the finance arm of companies such as General Motors and Ford, which reflects the financing of leased equipment rather than actual direct investment.We then used our estimates to construct two lists, the main list (Table 3) and an additional list (Table 4) which omits non-energy companies. The second list is relevant because capital spending by energy exploration and extraction companies tend to fluctuate sharply with the price of energy.

5. Based on Producer Price Index data released by the Bureau of Labor Statistics on Jun 14, 2022.

6. Mike Pomranz, “Starbucks Is Struggling to Keep Stores Stocked with Coffee Cups,” Food & Wine, February 10, 2022, https://www. foodandwine.com/news/disposable-paper-cup-shortage-starbucks.

7. Taylor Telford, “Yes, There’s a Tampon Shortage. Here’s Why,” The Washington Post, June 13, 2022, https://www.washingtonpost.com/ business/2022/06/13/tampon-shortage-product-shortages-inflation-supply-chain/

10. “GP to Expand Dixie Capacity in Lexington, Ky.; Will Close Operations in Easton, Pa., End of 2021,” Georgia-Pacific News, https://news. gp.com/2021/01/gp-to-expand-dixie-capacity-in-lexington-ky-will-close-operations-in-easton-pa-end-of-2021

11. A sizable number of planes are owned by leasing companies. But even taking those into account, the capital stock of aircraft only rose by 26% over this period, well below the average for the private sector as a whole.

12. “Walmart Selects Spartanburg County for New, High-Tech Grocery Distribution Center,” South Carolina Office of the Governor Henry McMaster, October 19, 2021, https://governor.sc.gov/news/2021-10/walmart-selects-spartanburg-county-new-high-tech-grocerydistribution-center.

13. Stephen Nellis, “Apple to Establish North Carolina Campus, Increase U.S. Spending Targets,” Reuters, April 26, 2021, https://www. reuters.com/technology/apple-establish-north-carolina-campus-increase-us-spending-targets-2021-04-26/.

14. Bryan Pietsch, “After a Slew of Disastrous Wildfires, PG&E Will Bury 10,000 Miles of California Power Lines,” The Washington Post, July 22, 2021, https://www.washingtonpost.com/nation/2021/07/22/pge-power-lines-california-wildfires/.

15. Phoebe Wall Howard, “Ford to Build New Plants in Tennessee, Kentucky in $11 Billion Investment in Electric Vehicles,” Detroit Free Press, September 28, 2021, https://www.freep.com/story/money/cars/2021/09/28/ford-motor-company-electric-vehicle-plants-batterieskentucky-tennessee/5896095001/.

16. Woodrow Bellamy, “Delta Air Lines Expands Fleet with New Airbus A321neo Order,” Aviation Today, August 24, 2021, https://www. aviationtoday.com/2021/08/24/delta-air-lines-expands-fleet-new-airbus-a321neo-order/

In a high-inflation environment, railroads are one of the few positive notes. Adjusting for the rising price of inputs like energy, so-called “value-added” prices of rail services are down by 2.6% over the last year. Meanwhile, value-added prices for air freight and passenger services are up by 20.5%, and value-added prices for trucking services are up by 33.4%, also adjusting for the price of inputs such as energy.

That’s why the current bargaining impasse in the railroad industry is distressing. The national railroads and rail labor unions are in a 30-day “cooling off period” that ends July 18. To avoid a strike or a lock-out, President Biden is likely to appoint a Presidential Emergency Board (PEB) to make settlement recommendations before a final cooling off period ends in mid-September.

While not directly part of the national negotiations, an important backdrop that the Tier 1 rail carriers have invested more than $11 billion in installing Positive Train Control (PTC), a system that makes rail movements much safer. The carriers propose to use this new technology to operate more efficiently by redeploying many conductors out of trains to ground-based positions. The rail unions are resisting this change at the individual carrier level, while demanding higher wages at the national level.

To work their way through the complicated puzzle of technology, wages, and productivity, President Biden needs to appoint PEB members who understand the railroad industry, and who are experienced arbitrators. That is the best route towards achieving a fair outcome that doesn’t disrupt the economy and further fuel inflation.

Progressive Policy Institute President Will Marshall and Center for Funding America’s Future Director Ben Ritz today urged Congressional Democrats to focus on four top legislative priorities ahead of the looming August recess break.

In a memo to Democrats, Marshall and Ritz argue Congress should seize the opportunity to:

Protect our democracy with Electoral Count Act reform;

Tackle inflation, energy, and health care costs through reconciliation;

Help America outcompete China by passing the bipartisan U.S. Innovation and Competition Act (USICA); and

Fill all 77 judicial vacancies

With control of both the House and Senate up for grabs in the fall, this could be the last chance to pass these crucial reforms before the usual midterm losses put MAGA extremists in a position to block any national progress for the remainder of President Biden’s first term,” Will Marshall and Ben Ritz write. “By taking action before the August recess on these four urgent priorities, Congressional Democrats could compile an impressive record of progressive reform and governing competence to run on in November.

Read the memo below:

MEMORANDUM

TO: Congressional Democrats

FROM: Will Marshall and Ben Ritz, PPI

RE: Four Legislative Priorities Before the August Recess

Under Democratic leadership, the 117th Congress has produced major wins for the American people. Nearly 70% of Americans are “fully vaccinated” against COVID and 80% have had at least one dose. The United States is enjoying its strongest job recovery ever and wages are rising. The bipartisan infrastructure law increased domestic infrastructure spending by $550 billion, the largest investment in America’s productive capacity in a generation. Congress approved President Biden’s request for military aid to help Ukraine defend itself against Russian aggression. The U.S. Senate confirmed Ketanji Brown Jackson as the first Black woman on the Supreme Court. And a determined Congress just passed the bipartisan Safer Communities Act — the first national gun safety bill in over 30 years.

Before they leave for August recess, Congressional Democrats should seize the opportunity to build on this solid record of accomplishment by acting to safeguard our democracy, ease inflationary pressure, expand America’s high-tech lead, create new jobs in clean energy, and lower health care premiums. With control of both the House and Senate up for grabs in the fall, this could be the last chance to pass these crucial reforms before the usual midterm losses put MAGA extremists in a position to block any national progress for the remainder of President Biden’s first term.

Therefore, we urge Congressional Democrats to focus on these four vitally important priorities over the next month:

PROTECT DEMOCRACY WITH ELECTORAL COUNT ACT REFORM

The top priority should be to reinforce the guardrails around America’s Constitutional democracy. Although his violent Jan. 6 coup attempt failed, ex-president Donald Trump continues to undermine the integrity of U.S. elections. In a blatant bid to rig future elections in advance, he’s backing MAGA election deniers running for Congress as well as governor and secretary of state in the key battleground states he lost in 2020. Congress must update the Electoral Count Act to make it impossible for defeated presidents and their accomplices to overrule American voters and steal a national election.

TACKLE INFLATION, ENERGY, AND HEALTH CARE COSTS THROUGH RECONCILIATION

Americans across the political spectrum agree that inflation is the greatest economic challenge we face today. The new, more focused reconciliation bill Democratic leaders are crafting with Sen. Joe Manchin could help reduce the cost of living while also salvaging some key elements of last year’s overreaching Build Back Better blueprint. It would cut budget deficits by roughly $500 billion, making it easier for the Federal Reserve to rein in rising prices without triggering a recession.

The new reconciliation bill also should include an ambitious set of consumer and business tax incentives for dozens of clean energy technologies, based on a $325 billion, 10-year package of clean energy tax incentive bill approved by the Senate Finance Committee last year, a version of which has already passed the House. These measures would stimulate hundreds of billions of dollars in private sector clean technology investment throughout the economy while creating millions of new jobs. They are also very popular with voters.

Congress made health insurance more affordable for over 13 million Americans this year when it increased the subsidies for plans purchased through the Affordable Care Act exchanges as part of the American Rescue Plan. But the increase was temporary, and if lawmakers let it expire, premiums will increase 53% on average. To make matters worse for Democrats, rate increase notices will be sent out in October, even if they don’t go into effect until January. It is unlikely that the full increase can be made permanent because of its high costs, but Democrats can blunt the pain and permanently fix the ACA “subsidy cliff” that existed before this year for less than $150 billion over 10 years as part of a sustainably financed reconciliation bill.

It’s essential that Democratic leaders and Sen. Manchin get to “yes” on a radically pragmatic reconciliation bill that unites their ideologically diverse party and delivers a major win for President Biden’s domestic agenda. They should resist pressure from the progressive left to enact other gimmicky giveaways that would squander these savings and undermine the bill’s inflation-fighting potential.

HELP AMERICA OUTCOMPETE CHINA BY PASSING THE BIPARTISAN INNOVATION BILL

Lawmakers have yet to finish conferencing the U.S. Innovation and Competition Act (USICA) passed last year by the Senate with the House-passed America COMPETES Act. This bipartisan innovation bill would make an historic investment in semiconductor manufacturing capacity, research and development, STEM workforce development, and supply chain resilience. By passing it, Congress would signal its determination to keep America ahead of China in the race for scientific and technological leadership.

USICA also presents an opportunity for Congress to set up a more robust and equitable system of career pathways for non-college workers. The COMPETES Act, for example, would expand apprenticeship opportunities to reach historically underserved populations, including youth and people re-entering their community after incarceration. It would also promote apprenticeships in non-traditional industries, creating nearly one million additional opportunities in new and emerging fields over the next five years.

But the House version of the bill unfortunately was larded with extraneous trade provisions that are unrelated to the bill’s core emphasis on boosting U.S. innovation and competitiveness. These should be set aside and argued out in some other legislative context. Meanwhile, Senate Minority Leader Mitch McConnell has vowed to pull his party’s support from the conference as long as Democrats continue work on passing a budget reconciliation bill. Although there are elements of the Senate bill that could be improved in a conference committee, the best way to circumvent McConnell’s blatant obstructionism may be for House Democrats to simply vote to send the Senate-passed USICA to President Biden’s desk, negating the need for further negotiations.

FILL COURT VACANCIES FASTER

The Supreme Court’s recent flurry of deeply polarizing decisions underscores the perils of allowing Republicans to pack federal courts with far-right ideologues. Although President Biden has nominated and confirmed more temperate federal judges at a record pace, it hasn’t been fast enough to keep up the rate of judicial retirements. To fill all 77 vacancies, he and Senate leaders must pick up the pace.

By taking action before the August recess on these four urgent priorities, Congressional Democrats could compile an impressive record of progressive reform and governing competence to put before the voters in November.

Will Marshall is the President and Founder of the Progressive Policy Institute.

Ben Ritz is the Director of PPI’s Center for Funding America’s Future.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

TO: Congressional Democrats

FROM: Will Marshall and Ben Ritz, PPI

RE: Four Legislative Priorities Before the August Recess

Under Democratic leadership, the 117th Congress has produced major wins for the American people. Nearly 70% of Americans are “fully vaccinated” against COVID and 80% have had at least one dose. The United States is enjoying its strongest job recovery ever and wages are rising. The bipartisan infrastructure law increased domestic infrastructure spending by $550 billion, the largest investment in America’s productive capacity in a generation. Congress approved President Biden’s request for military aid to help Ukraine defend itself against Russian aggression. The U.S. Senate confirmed Ketanji Brown Jackson as the first Black woman on the Supreme Court. And a determined Congress just passed the bipartisan Safer Communities Act — the first national gun safety bill in over 30 years.

Before they leave for August recess, Congressional Democrats should seize the opportunity to build on this solid record of accomplishment by acting to safeguard our democracy, ease inflationary pressure, expand America’s high-tech lead, create new jobs in clean energy, and lower health care premiums. With control of both the House and Senate up for grabs in the fall, this could be the last chance to pass these crucial reforms before the usual midterm losses put MAGA extremists in a position to block any national progress for the remainder of President Biden’s first term.

Therefore, we urge Congressional Democrats to focus on these four vitally important priorities over the next month:

PROTECT DEMOCRACY WITH ELECTORAL COUNT ACT REFORM

The top priority should be to reinforce the guardrails around America’s Constitutional democracy. Although his violent Jan. 6 coup attempt failed, ex-president Donald Trump continues to undermine the integrity of U.S. elections. In a blatant bid to rig future elections in advance, he’s backing MAGA election deniers running for Congress as well as governor and secretary of state in the key battleground states he lost in 2020. Congress must update the Electoral Count Act to make it impossible for defeated presidents and their accomplices to overrule American voters and steal a national election.

TACKLE INFLATION, ENERGY, AND HEALTH CARE COSTS THROUGH RECONCILIATION

Americans across the political spectrum agree that inflation is the greatest economic challenge we face today. The new, more focused reconciliation bill Democratic leaders are crafting with Sen. Joe Manchin could help reduce the cost of living while also salvaging some key elements of last year’s overreaching Build Back Better blueprint. It would cut budget deficits by roughly $500 billion, making it easier for the Federal Reserve to rein in rising prices without triggering a recession.

The new reconciliation bill also should include an ambitious set of consumer and business tax incentives for dozens of clean energy technologies, based on a $325 billion, 10-year package of clean energy tax incentive bill approved by the Senate Finance Committee last year, a version of which has already passed the House. These measures would stimulate hundreds of billions of dollars in private sector clean technology investment throughout the economy while creating millions of new jobs. They are also very popular with voters.

Congress made health insurance more affordable for over 13 million Americans this year when it increased the subsidies for plans purchased through the Affordable Care Act exchanges as part of the American Rescue Plan. But the increase was temporary, and if lawmakers let it expire, premiums will increase 53% on average. To make matters worse for Democrats, rate increase notices will be sent out in October, even if they don’t go into effect until January. It is unlikely that the full increase can be made permanent because of its high costs, but Democrats can blunt the pain and permanently fix the ACA “subsidy cliff” that existed before this year for less than $150 billion over 10 years as part of a sustainably financed reconciliation bill.

It’s essential that Democratic leaders and Sen. Manchin get to “yes” on a radically pragmatic reconciliation bill that unites their ideologically diverse party and delivers a major win for President Biden’s domestic agenda. They should resist pressure from the progressive left to enact other gimmicky giveaways that would squander these savings and undermine the bill’s inflation-fighting potential.

HELP AMERICA OUTCOMPETE CHINA BY PASSING THE BIPARTISAN INNOVATION BILL

Lawmakers have yet to finish conferencing the U.S. Innovation and Competition Act (USICA) passed last year by the Senate with the House-passed America COMPETES Act. This bipartisan innovation bill would make an historic investment in semiconductor manufacturing capacity, research and development, STEM workforce development, and supply chain resilience. By passing it, Congress would signal its determination to keep America ahead of China in the race for scientific and technological leadership.

USICA also presents an opportunity for Congress to set up a more robust and equitable system of career pathways for non-college workers. The COMPETES Act, for example, would expand apprenticeship opportunities to reach historically underserved populations, including youth and people re-entering their community after incarceration. It would also promote apprenticeships in non-traditional industries, creating nearly one million additional opportunities in new and emerging fields over the next five years.

But the House version of the bill unfortunately was larded with extraneous trade provisions that are unrelated to the bill’s core emphasis on boosting U.S. innovation and competitiveness. These should be set aside and argued out in some other legislative context. Meanwhile, Senate Minority Leader Mitch McConnell has vowed to pull his party’s support from the conference as long as Democrats continue work on passing a budget reconciliation bill. Although there are elements of the Senate bill that could be improved in a conference committee, the best way to circumvent McConnell’s blatant obstructionism may be for House Democrats to simply vote to send the Senate-passed USICA to President Biden’s desk, negating the need for further negotiations.

FILL COURT VACANCIES FASTER

The Supreme Court’s recent flurry of deeply polarizing decisions underscores the perils of allowing Republicans to pack federal courts with far-right ideologues. Although President Biden has nominated and confirmed more temperate federal judges at a record pace, it hasn’t been fast enough to keep up the rate of judicial retirements. To fill all 77 vacancies, he and Senate leaders must pick up the pace.

By taking action before the August recess on these four urgent priorities, Congressional Democrats could compile an impressive record of progressive reform and governing competence to put before the voters in November.

Will Marshall is the President and Founder of the Progressive Policy Institute.

Ben Ritz is the Director of PPI’s Center for Funding America’s Future.

The chapters on trade included in the Senate and House COMPETES Act/USICA raise some good ideas, but also some very questionable ones. A good principle here is: “simpler is better.” If the good can be salvaged, fair enough. But overall, the trade chapters’ contentious elements are not important enough to justify slowing the CHIPS Act, support for R&D and STEM workforce development, supply chain resilience, and the bill’s other major benefits.

On the positive side, the Senate’s renewal of an “exclusion” program for the Trump administration’s China tariffs is appropriate, helping to ease the burden these tariffs place on U.S. manufacturers and farmers. Likewise, it’s good that Congress is committed to renew the Generalized System of Preferences, though as PPI noted before, both the Senate and House bills overreach in adding many new eligibility criteria; these should be pared back to a more focused list and balanced with additional benefits as Reps. Stephanie Murphy and Jackie Walorski have proposed. Other ideas are best dropped.

For example, giving businesses wider openings to file trade lawsuits of the type that have recently derailed U.S. investment in solar energy, and banning families from getting “de minimis” tariff waivers for packages originating in China, are questionable on the merits, and also likely to put some additional upward pressure on prices when we need to do the opposite. They should be dropped in the interest of speeding the conclusion of the larger bill.

More fundamentally, the bills’ trade chapters seem to be missing the forest for the trees, or even the shrubs. Is it, for example, acceptable that the Biden administration is not seeking market access for American exporters, or more generally, designing a program ambitious enough to match China’s RCEP and Belt and Road (in its European, Asian, and Latin American trade “initiatives”?).

With the “301” tariffs having failed to change the direction of the U.S.-China relationship, is there a justification for continuing to ask American businesses and families to keep paying them? Did Congress surrender its rights by allowing presidents to personally impose tariffs through the “Section 301” and “Section 232” laws, and if so, should they be changed? And, as the administration investigates the effects of trade and trade policy on America’s low-income workers and communities, is there a role for pro-poor reform of the U.S.’ own trade regime?

These are the trade policy questions we hope Congress will begin asking, once it completes its competitiveness bill work.

The Bureau of Labor Statistics has just released detailed state and local job numbers for 2021, which allows us to calculate tech-ecommerce job growth by state. We analyzed the five-year period from 2016 to 2021.

Nationally, the tech-ecommerce sector, as defined by PPI, generated 2.045 million jobs from 2016 to 2021. That’s compared to private sector job growth of 2.188 million over the same period. Nationally, tech-ecommerce accounted for 93% of private sector job growth from 2016 to 2021.

For this blog item, we focus on the 12 states in the Census Midwest region: Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota, and Wisconsin. Overall, these states showed a gain of 26.6% for tech-ecommerce jobs from 2016 to 2021 (see table at the end of the item).

Ohio is the big Midwestern winner for tech-ecommerce jobs, with a 39.1% gain from 2016 to 2021, which translates into a mammoth employment increase of 73.2 thousand. Workers in Ohio’s tech-ecommerce sector were paid $69,000 on average in 2021, slightly higher than the average pay of $67,000 received by Ohio manufacturing workers (these figures include all workers in the sector, both managerial and production).

Among Midwest states, Kansas had the second highest growth rate for tech-ecommerce workers, with Illinois showing the second highest absolute gain of 59.5 thousand (both following Ohio). Workers in the tech-ecommerce sector in Illinois received an average of $95,000 in 2021, compared to average manufacturing pay of $79,000 in the state.

The biggest tech-ecommerce laggard in the Midwest is, surprisingly, Minnesota. Minnesota has a history as a mainframe computer manufacturing leader, but it has not been able to convert that legacy to tech-ecommerce jobs. From 2016 to 2021, the number of tech-ecommerce jobs in Minnesota rose by 8.4%, the second slowest in the country (after Vermont). The number of “tech industry” jobs (software publishing, data processing, internet publishing and other information services, and computer systems design) only rose by 4.4% in Minnesota, compared to a 25% gain nationally, and a 14% gain for all Midwest states overall.

In an April 2021 report, the Minnesota Chamber Foundation acknowledged the state’s weakness in tech.

…sluggish growth in Minnesota’s high-tech industries and tech occupations has been a source of underperformance in the state’s economy for almost a decade, and forecast data projects an underwhelming future if Minnesota does not change.

The chapter on Minnesota’s tech sector drives home the point:

…Our relative under-performance in some fast-growing high-tech subsectors, such a software publishing and data hosting/processing, also explains why Minnesota has lagged faster growing states in GDP and employment growth in the last decade. Our comparative lack of high-flying tech successes this decade may also act as a reputational drag on growth, as fast-growing companies and startups have tended to cluster in tech growth clusters, such as Silicon Valley, Seattle, Austin, or Boulder.

Finally, it is perhaps ironic that Minnesota, a state which has barely participated in the tech boom, is home to Senator Amy Klobuchar, the main sponsor of legislation designed to hobble the large tech companies that have created so many jobs nationally and in other Midwest states. Perhaps if Minnesota catches up and embraces investment from technology leaders, she would better understand the damage her poorly designed legislation would have.

Tech-Ecommerce Jobs in the Midwest: Leaders and Laggards

Change in tech-ecommerce jobs, 2016-2021

percent

thousands

Ohio

39.1%

73.2

Kansas

36.9%

17.0

Missouri

32.0%

30.8

Indiana

31.4%

34.9

South Dakota

28.6%

2.1

Michigan

28.0%

33.5

Illinois

26.6%

59.5

Wisconsin

18.6%

19.7

Iowa

18.2%

8.8

Nebraska

16.0%

5.4

North Dakota

10.3%

0.9

Minnesota

8.4%

10.5

Midwest

26.6%

296.4

Data: BLS, PPI. Based on NAICS 334, 4541,492, 493, 5112, 518, 519, 5415

Congress has the opportunity to increase chip manufacturing in the United States through the United States Innovation and Competition Act from the Senate, or the America Creating Opportunities for Manufacturing, Pre-Eminence in Technology and Economic Strength (COMPETES) Act from the House. Unfortunately, a stalemate over semi-unrelated trade provisions in the bill are preventing its passage, delaying $52 billion in funding provisioned to increase production in the United States. Continued stalemate is bad news for the future of the American economy.

Computer chips, or semiconductors, live in almost every electronic device we use on a daily basis. They’re needed for cars, cellphones, medical equipment, and national security. The growing thirst for chips came to a head in 2021 and 2022, when a national shortage drove up the prices of cars and other essential electronics.

The United States is the main designer of semiconductor chips with almost 50% of global sales, according to the Department of Commerce. But designing the chip is not the same as actually building it. Despite the dominance of U.S. design, only one U.S.-owned semiconductor foundry, or factory, exists in the United States, run by Infineon in Minnesota. Surprisingly, the U.S. lost its once supreme position in semiconductors by not investing in semiconductor “fabs,” leading it to only produce 11% of global semiconductors in 2019. Instead, Taiwan is the global leader in semiconductor manufacturing with two of the largest semiconductor foundries in the world, UMC and TSMC.

Moreover, the U.S. has fallen behind in two distinct ways. U.S. companies have fallen behind in the cutting-edge technologies that are used to make the “advanced” chips that power smartphones and game consoles. TSMC and Samsung are the only general-use chip manufacturers that can produce the most advanced chips.

Meanwhile, the U.S. has also not invested in the facilities that make the “mainstream” chips that power, among other systems, speedometers or car brakes. Chips for cars, while easier to manufacture, are cheaper and have a lower profit compared to smartphone and computer chips, which are the state-of-the-art versions that drive innovation in computing capabilities.

Chipmaking requires a lot of investment, resources, and research and development to keep up with the needs of computing. The global chip shortage demonstrated the challenges for digital societies in keeping up with demand; the European Union passed The European Chips Act in February 2022 in response to the shortage.

Congressional leaders have been negotiating to discuss differences in the Senate and House bills, which are extensive. Provisions around issues, such as the denial of “de minimis” tariff waivers on small packages from China, eased filing of anti-dumping lawsuits such as those recently targeting solar panel imports, digital trade negotiating goals, energy and research, space, green energy, and more are the subjects of disagreement. In contrast, only one major provision separates the two chambers on chips: PAYGO, with the House in support and the Senate against the budget provision.

In light of the importance of chips for everyday life and for future innovations, resolving the single disagreement over chips is both more pragmatic and necessary to increase American competitiveness and security in this sector.

Today, the Progressive Policy Institute released a new report on the challenges United States policymakers and regulators face in establishing oversight for the rapidly growing — and increasingly volatile — cryptocurrency and digital asset market.

Cryptocurrency has faced fitful bursts of growth and decline since its inception in 2008, with a dramatic recent crash from $3 trillion in November 2021 to $1.3 trillion in mid-May 2022. According to the report author, on any given day, more than $90 billion in digital assets change hands.

The report is titled “The Cryptocurrency Conundrum: The uncertain road toward a coherent oversight structure,” and is authored by Rob Garver.

“The crypto ecosystem’s explosive growth might continue, bringing more and more people into the universe of digital assets, with real-world effects on the financial security of individuals and families,” writes Rob Garver in the report. “Should some of the more promising use cases of blockchain technology prove viable, the crypto ecosystem has the potential to significantly transform areas as diverse as cross-border payments, management of public assistance programs, and online commerce.”

As policymakers look to regulate and provide oversight to this market, they must weigh the benefits and costs of who regulates the market and how heavy of a hand is used in regulation. Garver’s report asks if the unique nature of cryptocurrency requires a new, regulating body, or if Senators Gillibrand and Lummis’ recently introduced legislation proposing regulation through the Commodity Futures Trading Commission (CFTC) is the path forward. Garver also explores security and consumer protection issues faced by the industry, and explores the tax treatment experienced by investors.

Rob Garver is a freelance writer based in Alexandria, Virginia. He has covered banking and financial services policy for more than 20 years, and currently edits the BankThink section for American Banker.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

The extraordinary growth of the market for cryptocurrencies and other digital assets is one of the most remarkable stories of the past decade. In the United States, an estimated 40 million people have bought and sold digital assets, suggesting that what was once a niche interest is finding its way into the financial mainstream.

In the years after the pseudonymous Satoshi Nakamoto introduced the world to Bitcoin in a 2008 white paper,1 the use of digital assets grew steadily, reaching a market capitalization of about $14 billion in 2016. Since then, however, the total value of cryptocurrencies and crypto tokens in circulation has skyrocketed, rising to nearly $3 trillion in November 2021, before crashing down to $1.3 trillion in mid-May 2022. On any given day, more than $90 billion in digital assets change hands.

This spring’s crypto market collapse is just the latest reminder for investors that crypto assets come with extra risk and volatility, especially in times of economic and political uncertainty. It has also led for calls to establish rules to protect investors and ensure the proper functioning of the markets.

The potential benefits of widespread adoption of cryptocurrencies are many. The ability to make transactions without the assistance of an intermediary, like a bank, could create opportunities for individuals who do not have easy access to traditional financial services. The ability to transfer value quickly and securely across borders could make international trade much more efficient and remittances cheaper and faster. The use of “programmable” money could make complex business arrangements, like revenue sharing, execute in real time with perfect transparency.

However, growing public interest in a new and volatile marketplace is a prospect that has regulators in the U.S. deeply concerned. Fraud in the unregulated crypto marketplace is a significant problem, raising questions about the need for investor protections. Because it is possible to transact in digital assets without the use of an intermediary, like a regulated financial institution, and because those transactions can be made anonymously, such activity has been linked to billions of dollars’ worth of illegal activity.

The growing market for stablecoins, tokens with their value pegged to other assets, often a fiat currency, have raised questions about the possibility of systemically destabilizing runs on stablecoin issuers.

As more Americans become interested in investing and transacting in digital assets, there are real questions about whether and how they ought to be handled by existing financial institutions. Should banks be allowed to hold cryptocurrencies on their balance sheets? If so, how would they value the often-volatile assets?

Digital assets also raise important and complicated questions about tax policy. Current U.S. policy holds that every time a token changes hands, it reflects a taxable event, in which the person transferring the token incurs a capital gain or loss, and the person receiving it establishes the basis against which their eventual capital gain or loss will be measured.

The Biden administration, in March 2022, issued a sweeping executive order acknowledging the need for the federal government to adopt a coherent set of policies related to digital assets.7 While the announcement was welcomed by many in the crypto world,8 the executive order was light on specifics, effectively pointing out that the federal government has an enormous amount of work ahead of it as it tries to understand and oversee the market for digital assets.

The object of this paper is to identify some of the most significant areas in which regulators and/or the crypto community believe a policy response is required and the work currently being done to address those issues.

This week, Congressman Scott Peters (CA-52) sat down with the Progressive Policy Institute’s (PPI) Director of the Center for Funding America’s Future Ben Ritz and Policy Director for PPI’s Center for New Liberalism Jeremiah Johnson for a Twitter Spaces livestream to discuss the new Inflation Action Plan released by the New Democrat Coalition. During the event, Governor Jared Polis (D-CO) joined the conversation to applaud Congressman Peters and PPI for their work on the blueprint.

“Clearly people are struggling with inflation. It’s something that every elected is hearing about, and we know about… We’re New Dems, we actually want to take these challenges on and do something about it so I decided to help constitute an inflation working group. We first brought in some people to hear about what was causing this problem … you know, we’re not going to solve this problem tomorrow, but we got a lot of ideas about what to do to go forward and make some progress,” said Rep. Peters.

“I think part of the part of the challenge has been that because we didn’t take those suggestions [from the New Democrat Coalition during the drafting of the American Rescue Plan], and some of the policies we put in place weren’t quite calibrated to the moment, which helped contribute to the situation we’re in now. And so I think that it’s a lesson that we should have listened to the New Dems in the past when we could, but it’s not too late to take their recommendations now to get the problem under control and put us in a better place for the future.” said PPI’s Ben Ritz.

“I just really appreciate both PPI’s efforts and Congressman Scott Peters’ efforts on this and the New Dems as well, which I used to be a Vice Chair of when I was in Congress,” said Governor Polis.

With inflation continuing to rise at a historically rapid pace, the New Democrat Coalition released a 24-page action plan to tackle inflation and address supply chain issues that would provide much-needed relief for Americans. The plan would strengthen global supply chains and increase price competition by reducing tariffs and other barriers to trade, while also helping expand domestic supply by cutting onerous regulations that increase costs and making critical investments in scientific research and clean energy. In addition, the blueprint urges Congress to pass a reconciliation bill that reduces future budget deficits and presents ideas to make fiscal policy more responsive to macroeconomic needs.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

###

Media Contact: Tommy Kaelin; tkaelin@ppionline.org

Democrats have been struggling to respond to the highest inflation America has seen in 40 years. Many on the left are pushing a bogus “greedflation” narrative that blames rising prices on corporations’ desire to maximize profits, as if that were some new phenomenon. Others have proposed to compensate consumers for higher prices with cash handouts that will likely only make the problem worse. And Republicans, who sharply criticize Democrats’ approach to inflation, have offered no constructive ideas of their own for tackling the problem. Thankfully, the moderate New Democrat Coalition (NDC) came forward today with a pragmatic 24-page Action Plan to Fight Inflation — and it’s the best inflation-fighting blueprint to come out of Congress yet.

Fighting inflation requires an understanding of what drives the problem. First, supply chain disruptions caused by the COVID pandemic reduced the availability of goods and services. Then demand for those goods and services, bolstered by excessive government stimulus, reached unprecedented levels as the world began returning to normal. The result: too many dollars chasing too few goods and services, thus driving up prices. The problem was only made worse when Russia’s unjustifiable invasion of Ukraine cut off food and fuel exports.

Energy and food inflation concerns loom large for voters heading into the second half of 2022 and the midterm elections. Meanwhile the odds of recession are rising and expected growth is falling, according to economic forecasters surveyed by the National Association of Business Economists.

With these bread-and-butter issues on the table, is this the right time for Senate Democrats to spend time debating and voting on Senator Amy Klobuchar’s tech antitrust bill? Voters are not going to feel inflation relief from the bill. Remember that the tech sector is not the source of surging inflation, no matter how you look at it. For example, e-commerce, like every other industry, has been affected by rising fuel prices and supply chain disruptions. But BLS data shows that ecommerce margins — the difference between the acquisition price of goods and the sale prices — narrowed by 3% over the past year, benefitting consumers. By comparison, margins for the entire retail sector widened by 12%, giving an extra jolt to inflation.

And Senate Democrats won’t be able to point to the tech antitrust bill as a source of new jobs in case of a recession. Indeed, the timing is precisely wrong. The big tech companies showed their willingness to keep investing and hiring during 2020 and 2021, helping keep the U.S. economy afloat. Moreover, real wages are rising in the tech/ecommerce sector. That job and investment performance is unlikely to be repeated even if the Klobuchar legislation works exactly as proponents expect, since the bill is intended to restrain growth by the big tech companies and smaller rivals are not going to expand during a recession.

Whether or not you think that tech antitrust is a good idea in theory, this is the wrong time.