I found myself reacting to the Libor scandal more strongly than a lot of the earlier revelations of financial institutions misdeeds. First, the banks were just blatant out-and-out lying about a simple number.

Second, their lying led to a distortion of a crucial piece of publicly available data–the Libor rate. In a market economy, intentional misrepresentation of a market price is not a victimless crime –in fact, the victims are everyone who relied on that price to make decisions. That includes regulators who presumably watched Libor as one of their guides to the amount of stress in the global banking system. Here’s a chart of Libor across the key period (downloaded fromhttps://www.fedprimerate.com ).

Would Libor have shown more signs of stress sooner if it wasn’t being manipulated in 2007 and 2008? And would banks, regulators, and investors reacted sooner? We’ll never know.

But this confirms what I’ve written in the past–the financial crisis was in part a data crisis, where all sorts of numbers were sending misleading signals. In particular, the strength of the financial position of the banks was overstated.

The question is whether the Libor scandal is a vestige of the past, or a sign of future troubles to come. My sense is that we’ll see a lot more opportunities for manipulation of private data to send misleading public signals. Forget about financial markets for the moment. I’m thinking now about the way that websites continually try to game Google’s search algorithms in order to get a higher ranking. Hotels and restaurants have a big incentive to try and manipulate their reviews on consumer sites such as Yelp. App developers have an incentive to game their reviews on the Apple and Google app stores.

Will the bad information drive out the good? Or can we build information aggregation mechanisms that are more difficult to manipulate?

President Obama has proposed a National Infrastructure Bank, a simple declarative sentence that left most listeners wondering what he meant. The confusion arises partly because the administration did not follow up the president’s remarks with a specific proposal, but also because the operations of such a bank have never been fully fleshed out. Felix Rohatyn and I have elsewhere laid out the broad outline of how such a bank would function,1 and that description serves as a good starting point for our expectations regarding the president’s proposal and what Bank-type proposals generally ought to do.

As many writers have noted, American infrastructure is depreciating rapidly – we are likely well below the replacement rate of investment in roads, mass transit, airports, ports, rail, and water assets. The logical implication is that we need to invest more. But more investment in and of itself will not move us towards having the right mix of infrastructure assets in place.

The current mix results from one of two selection processes. The first is devolution to the states (for example the cost-sharing grants delivered by the Highway Trust Fund), and the second is selection by Federal agencies (e.g., the Corps of Engineers). At worst, these processes lead to politically motivated outcomes, either because state governments favor some projects for wholly non-economic reasons, or because the Congress can muscle the selection process from the federal agencies. The most recent transportation authorization bill, passed in 2005, made the word “earmark” famous by incorporating a stunning $24 billion of them – the price of having a law passed. Insofar as we have given the task of project selection to the political process, it would be surprising if this kind of event didn’t happen, not that it sometimes does.

Politicized project selection is one of several problems associated with the current process. But it is one of the reasons why a National Infrastructure Bank is so important and so urgently needed: not just because a bank might be able to lever federal dollars, but because it can use the existing dollars more wisely and obtain a higher public return.

What follows, then, is a description of the role a National Infrastructure Bank could play, taken from the perspective of the specific problems in the current process it might solve. This perspective also allows us to evaluate the administration’s proposal.

In a nutshell, Rohatyn and I propose that we collapse all of the federal “modal” transportation programs into the Bank. Any entity – whether state, local, or federal – would have standing to come to the Bank with a proposal requiring federal assistance. The Bank would be able to negotiate the level and form of such assistance based on the particulars of each project proposal. It could offer cash participation or loan guarantees, underwriting or credit subsidies, or financing for a subordinated fund to assure creditors. Any project requiring federal resources above some dollar threshold (on a credit scoring basis) would have to be approved by the Bank. Additionally, we imagine that some part of the funding for existing modal programs would be converted into block grants sent directly to the states and large cities to be spent on projects too small for the Bank’s oversight. Such grants could also be used for those programs desired by the states that do not pass muster on terms proposed by the Bank.

This is more a vision of infrastructure policy than a blueprint for the immediate future. Admittedly, it will take years and a meticulous reorganization to produce this configuration. But the best way to measure our progress in infrastructure policy (and the merits of the administration’s proposal) is not to see how quickly we adopt the Bank’s specific features, but to see how the Bank addresses the underlying infrastructure policy flaws it is designed to fix.

In a classic example of a “slippery slope,” Congress once again is looking for easy pickings by increasing guarantee fees (g-fees) that Fannie Mae and Freddie Mac charge lenders to guarantee their mortgage lending. Last December, Congress raised the GSE’s g-fee by 10 basis points for 10 years. The goal was to raise almost $36 billion to pay for the extension of the payroll tax cut. Although this was supposed to be a one-time revenue plug, some lawmakers called for extending the new fees (at a slightly decreased rate) for an eleventh year to pay for restoration and clean up of the Gulf coast.

We understand it’s difficult for Congress to find “pay fors” for important initiatives at a time when Republicans have dug in their heels against tax increases for any purpose, even debt reduction. But treating g-fees as a piggy bank is ill-advised. Here’s why: Raising g-fees will compound the weakness of an already anemic lending environment, discourage home refinancing and lower housing demand.

This week in housing was an especially busy one; PPI looks at just a few highlights with Case-Shiller numbers, a new government pilot program on housing and a huge announcement from Bank of America. Let’s get to it.

1. S&P Case-Shiller, the leading Index of national housing values, came out on Monday. The December data continued to highlight what is clearly the biggest drag on a recovery that is trying to find its footing, declining home values. Case Shiller’s latest numbers showed the composite of the three indices (national, 10 cities, and 20 cities) was down 3.8 percent for the fourth quarter of 2011 and were the lowest numbers for the popular Index since the crisis began in 2006.

In related “Index” news, PPI released the first edition of the “PPI Battleground Home Values Index” last week. The Index looks at home values since the 2008 election in 16 battleground states.

Two years after the meltdown in the nation’s housing market, housing re- mains weak. Home prices fell to a new low in the first quarter of this year— confirming a feared “double-dip” in the market. Prices are now down nearly 33 percent from their high five years ago.

With housing and its related industries—construction, home retail, etc.— constituting almost 19 percent of the nation’s economy over the last 40 years,2 restoring the housing market will be essential to a sustained eco- nomic recovery. And key to this will be ensuring a robust market for first- time home sales.

Yet, even with home prices as low as they currently are, many potential homebuyers may face more—not fewer—obstacles in their path to home- ownership. In the aftermath of the crisis, credit is tighter, as are down pay- ment requirements. At the same time, the stresses of the economy have meant that potential homebuyers are in worse shape financially than they once were.

The creation of a new, tax-preferred mechanism for down payment sav- ings—a “HomeK”—could help first-time homebuyers navigate these new hurdles while also promoting more savings. And if structured as a carve-out from existing retirement planning mechanisms, not as a new type of ac- count, the HomeK would have the added benefit of promoting retirement savings and will not contribute to further tax code complexity.

Whether U.S. Presidents succeed or fail often depends on a big factor beyond their control: the timing of the business cycle. Lucky Presidents – Ronald Reagan, George W. Bush – experienced downturns early in their first term, leaving plenty of time for an economic rebound to lift them to reelection.

Barack Obama, who took office months after the Great Recession started, must be cursing his luck. Just at the point when investment and jobs normally would be coming back, the U.S. economy has taken a sickening swoon.

Last month’s feeble job numbers – just 54,000 jobs created, far short of the 300,000 or more needed each month to return unemployment to pre-crisis levels – reinforced the public’s growing economic gloom. They also suggested that the administration has erred in viewing the economy’s problems as cyclical.

If that were true, the White House strategy of waiting for the economy to heal itself might make sense. But if America faces structural impediments to growth, we can’t just wait for the economy to revert to normal.

Since the Great Recession officially ended in the fall of 2009, the economy has grown just 2.8 percent per year, well below the average 4.6 percent growth that follows typical recessions, economist Lawrence Lindsey said. And instead of declining steadily, unemployment is rising again.

From GOP presidential aspirant Jon Huntsman to liberal columnist Paul Krugman, commentators across the spectrum are rightly talking about a “lost decade” of economic growth. According to the Wall Street Journal’s Gerald Seib, America has endured 11 straight years of lackluster growth since 2000, the last year in which economic growth exceeded four percent.

The job picture is even worse. As this useful chart shows, the U.S. economy created 23 million jobs on Clinton’s watch and 16 million on Reagan’s. Bush’s job-creation record is a paltry 3 million. And we can’t just blame the Great Recession. Even before it hit in December 2007, the rate of job growth lagged well behind the record of the previous decades.

No doubt about it: the aughts under Bush were a lost economic decade. While no president can be blamed for cyclical downturns, it is fair to say that Bush’s economic policies did little to address the structural roots of slower economic and job growth. On the contrary, his purblind economic policy mix – coupling a spending binge with deep tax cuts – helped dig America into a deep fiscal hole.

Nonetheless, the lingering economic malaise has cast a shadow over Obama’s reelection prospects and boosted Mitt Romney’s political stock – the two are now running neck-in-neck in the polls. The 2012 election will largely be a contest over which party has the most credible plan for reviving U.S. economic dynamism.

The Republicans have a simple fiscal theory that leads to an equally simple solution. They see the size and cost of government as the chief obstacle to growth. Cut public spending, and the economy will sit up on its haunches again and roar.

Many liberals, including Krugman, seem stuck in the Keynesian paradigm, arguing that the problem is inadequate demand, which means government needs to spend more until the economy recovers its “animal spirits.”

Obama is smart enough to reject a witless choice between less or more government. He has, however, yet to develop a plausible plan for restructuring the U.S. economy to unleash economic innovation, capture its benefits in good jobs that stay in America, and boost our ability to win in world markets.

Above all, Obama needs to spell out big, concrete initiatives that can inspire public confidence that his administration has properly diagnosed the economy’s structural ills and prescribed realistic remedies.

PPI has developed bold proposals that meet this standard: An independent National Infrastructure Bank, to unlock hundreds of billions of private investment in state-of-the-art transport, energy and water systems; pro-growth tax reform that closes inefficient tax expenditures and reduces the corporate tax rate; and a base-closing style commission charged with periodically pruning regulations that impede economic innovation and business start-ups, the engine of most new American job creation.

America can’t afford another lost economic decade – and neither can progressives. This is an FDR moment for Obama – a time for “bold, persistent experimentation” to get America’s economy moving again.

Amid the high drama of fiscal brinkmanship in Washington, it’s easy to forget that reducing budget deficits isn’t the biggest economic challenge we face. Even more important is kick-starting the great American job machine and reversing our country’s slide in global competition.

Critical to both goals is shoring up the decaying physical foundations of national prosperity. Without world-class infrastructure, the United States won’t be able to attract private investment, sustain rapid technological innovation and productivity growth, or keep good jobs from going overseas.

According to a new Gallup poll, general economic concerns (35 percent) and unemployment (22 percent) top voters list of worries, with federal deficits and debt a distant third at 12 percent. Fiscal restraint is important, but it must be balanced against the larger imperatives of jobs and global competition. Among other things, this means leaving room for public investment to replenish the nation’s stock of physical capital.

America can’t build a more dynamic and globally competitive economy on the legacy infrastructure of the 20th Century. Thanks to their parents’ far-sighted public investments, baby boomers grew up in a country that set the world standard for modern infrastructure. But after a generation of underinvestment, compounded by politicized spending decisions, we now face a massive infrastructure deficit that exerts a severe drag on U.S. productivity.

Meanwhile, China and other fast-rising countries are building gleaming new airports and bullet trains. To keep from falling farther behind, the United States needs to make large-scale capital investments in repairing decrepit roads and bridges; upgrading air and sea ports; building “intelligent” transportation systems and smart energy grids; modernizing the air traffic control system; speeding up our pokey rail networks; and leading the world in deploying ultra-fast broadband.

But with the government strapped for cash, it’s reasonable to ask where the money to rebuild America will come from. The answer is that we need to look more to the private sector. U.S. companies are sitting on $2 trillion in idle cash, and pension funds, overseas investors and sovereign wealth funds also are looking for places to invest. Although the federal government will have to put up seed capital, its main role should be to leverage private investment in state-of-the-art infrastructure.

That’s why America needs a National Infrastructure Bank. As proposed by the bipartisan trio of Senators John Kerry, Kay Bailey Hutchison and Mark Warner, the bank would use a modest, one-time appropriation of $10 billion to leverage enormous investments — $640 billion over 10 years — for projects with the greatest potential to put Americans to work and enhance U.S. competitiveness.

President Obama has repeatedly endorsed a national infrastructure bank and proposed the idea again in the budget he sent to Congress in February. But the Senate bill (and a separate House proposal championed by Rep. Rosa DeLauro) have decided advantages over President Obama’s proposal. The president’s approach starts with a smart idea to create programs that work more with the private sector to find financing solutions. But unlike the Kerry proposal, it does not focus enough on the most powerful tools for leveraging private investment: loan programs that include a reasonable cap on the federal share of project costs. Obama’s bank would also be housed within the Department of Transportation, whereas the Kerry bill would make the bank an independent, quasi-public entity. That’s an important difference, because to attract hard-headed capitalists who expect a real economic return on their investments, the government’s financing facility must be genuinely free of political interference.

An independent infrastructure bank would select projects based on their ability to generate real economic returns rather than their influential political patrons. As a self-sustaining entity that would not rely on future appropriations from Congress, the bank would not be subject to the pork barreling and earmarking that distorts federal and state infrastructure spending, especially on transportation.

It’s time to get serious about our dilemma: the U.S. economy is creating too few jobs to bring down unemployment to pre-recession levels. For that, we’d need nearly 12 million new jobs, or about 100,000 more on average than the 200,000 the economy is creating each month. Big capital projects would immediately create those jobs where they are most desperately needed–in the hard-hit construction industry, which is still struggling with a 20 percent unemployment rate.

In the short run, a big national push to build modern infrastructure could create high-skill jobs that can’t be exported. In the long run, it will ensure America’s return to being an engine of production, not just a global center for consumption. That’s why, as Congress struggles to contain federal deficits and debt, it needs to make room for a National Infrastructure Bank to rebuild America.

It’s crazy, I know, but imagine that U.S. political leaders after the midterm election called a truce in the partisan tong wars to work out a compromise solution to the nation’s fiscal dilemmas. The result would probably look a lot like a new fiscal reform blueprint drawn up by two canny policy veterans, Bill Galston and Maya MacGuineas.

In The Future Is Now: A Balanced Plan to Stabilize Public Debt and Promote Economic Growth, Galston and MacGuineas map a radically centrist course to fiscal discipline that demands equal sacrifice from the left and the right, and that doesn’t impede economic recovery. Here’s hoping that President Obama’s deficit commission, which is groping for a politically feasible formula for fiscal restraint, will give this plan a close look.

Reducing America’s swollen deficits and debts is fast becoming an urgent national priority. Since President Obama took office, we’ve added three trillion dollars to the public debt, largely thanks to emergency spending to rescue the banking system and goose a faltering economy. But it’s the zooming growth of health care and retirement spending that really threatens to drown the federal government in debt. For decades, we’ve ignored warnings about the growing funding gaps in Medicare, Medicaid, and Social Security, but with the first wave of baby boomers now reaching retirement age, the future really is now.

We’ve dug ourselves more than a hole – it’s a canyon. So any talk now about balancing the federal budget is pure fantasy. The best we can hope for is to arrest the runaway growth of public debt and bring it back down to a sustainable level.

The administration’s forecasts show public debt, 40 percent of GDP two years ago, rising to more than 100 percent in 2012. The Galston-MacGuineas plan would bring that down to 60 percent of economic output by the end of this decade. It also would slash annual budget deficits from a projected five-to-six percent to around one percent, ensuring that our debts don’t grow faster than the economy.

Inevitably, the plan envisions a 50-50 split between spending reductions and tax hikes. It’s hard to image any other way forward considering liberal resistance to spending cuts, especially for the big entitlements that are driving our long-term debt problem, and the conservative allergy to tax increases of any kind. The hacking and lifting, however, would be phased in gradually to give the economy room to breathe and recover.

More specifically, the plan would:

Make sizeable cuts in defense spending, and impose a war surtax should our current conflicts extend beyond mid-decade.

Freeze discretionary spending for three years, such that increases in spending in one area would have to be made up by cuts elsewhere.

Modernize Social Security by indexing the retirement age to longevity, and trimming benefits for affluent retirees in the future. It would also raise the minimum benefit, strengthening the program’s anti-poverty effect, cut the payroll tax and add a new, mandatory savings account.

Supplement the cost-containment features of President Obama’s comprehensive health plan, by raising Medicare premiums, reducing subsidies and adding tort reform.

Prune tax expenditures (which cost more than one trillion dollars a year) by 10 percent and limit their future growth. The proceeds would go to lower tax rates and deficit reduction.

Enact a carbon tax, both to “buy down” the payroll tax and cut deficits.

Many of these proposals, of course, are deemed politically radioactive now, even if they are familiar fixtures on the wish lists of serious fiscal hawks. So why should we expect a package stuffed with political non-starters to advance?

Because the habit of evading even modestly tough choices has allowed the debt problem to reach such ginormous proportions that it can’t be solved in any other way, say Galston and MacGuineas. And if it isn’t solved, it will slow down U.S. economic growth, transfer our wealth to overseas creditors, and limit the federal budget’s fiscal capacity to respond to future emergencies.

The big question is: what impact will the midterm election have on the politics of fiscal evasion? Republicans say cutting taxes is the way to shrink government, but showed little stomach for cutting spending when they were in office. Result: huge public debts. Some Democrats believe deficits should be closed mostly by tax hikes, but aren’t really willing to propose them. Result: huge public debts.

As the Galston-MacGuineas plan shows, solving our fiscal problems doesn’t have to be a political zero sum game. The question is whether our political leaders can rediscover the lost arts of compromise and risk-sharing to advance vital national goals.

The GSE conference at Treasury today included plenty of big names and good thoughts about the lingering question of how to restructure Fannie and Freddie before releasing them back into the wild. But one thing missing from the agenda was a sense of urgency. The conference wasn’t intended to move GSEs up on the agenda right now; it was simply a bit of theater to defuse the issue for a few more months, giving the Administration more time to kick some hard choices down the road.

Everyone knows we still need to do something about Fannie and Freddie. The problem for Geithner is that everyone keeps talking about it. The editorial chatter about GSEs is gaining momentum (after all, there’s only so much Steven Slater coverage even August can handle). The New York Times ran two op-eds last weekend (good and not-so-good), former Treasury Secretary Paulson weighed in on the Post’s opinion page, and think-tank proposals are popping up all over, especially from folks like Don Marron who want to shrink or privatize the role of Fannie and Freddie in lending markets.

So Secretary Geithner did what any good politician would do. He co-opted the debate to keep it from growing beyond his control. By inviting differing voices to vent their opinions in front of the cameras, Geithner got to look like he was on top of the situation and neutralize the situation for now with a concluding pleasantry that “it’s safe to say there’s no clear consensus yet on how best to design a new system.” Thanks for that, Tim. I guess we shouldn’t hold our breaths for “consensus” anytime soon, huh?

With elections weeks away and the crippled housing market still relying on the dual crutches of Fannie and Freddie to move forward at all, it’s no surprise the Administration and Congress are not falling over themselves to begin the fight for a specific reform plan. Geithner has said the Administration plans to release and administration proposal in January (well after the elections), and the tone of today’s conference was consistent with that schedule. For anyone who bothered to tune in today (and managed to stay awake), the message from the Administration was this: we know it’s important, and we’ll get around to it eventually . . . maybe once we get back from that Gulf-coast beach trip the President wants us all to take.

The economic news out of Washington this week has an eerie ring of déjà vu: Congress just passed an emergency spending bill, the Fed is buying debt securities to keep the economy from sliding toward collapse, and the Administration announced it is committing billions of dollars to mortgage relief for homeowners facing foreclosure. To be sure, none of these actions has the scale or urgency of the initial responses to the financial crisis, but they are perfect examples of the policy philosophy that has dominated both economic policy since the crisis: a focus on playing defense, rather than offense.

What we saw this week were Congress, the Administration, and the Federal Reserve continuing their roles as the three little Dutch boys of the American economy, sticking fingers in the dyke to save the country from disaster. The rhetoric of stimulus is oversold and misplaced: Washington’s fiscal and monetary policies have essentially all been economic tourniquets that are better characterized as containment measures than stimulus. The Fed is shifting into quantitative easing, but only as much as necessary to fight off deflation. Congress is sending aid to the states, but only enough to keep them from having to lay off teachers. Treasury and HUD are providing assistance to the housing market, but only enough to keep people from being kicked out of their houses.

Over and over since the crisis, policy makers in both parties have remained optimistic that the U.S. economy was inherently dynamic and resilient enough that we could rely on growth to materialize from somewhere, as long as we put a solid floor underneath to contain the damage and prevent more negative shocks to the economy. Given the huge amounts being spent and our country’s history from past recessions, this was not an unreasonable approach at the time, especially for those with any concern for fiscal responsibility.

So far, the containment strategy has proved extremely successful in keeping us from sinking into a full-blown depression. However, at this point, we still have farther to go on the path to a sustainable recovery than most economists and politicians had hoped. This morning we got the new jobless numbers, and they aren’t good. Wall Street was hoping for better news, and the markets’ negative reaction only compounds the growing anxiety (even allowing for the low volume in August, when stocks historically are more vulnerable to bad news). The extended string of bad economic news, coupled with a lack of credible cheerleading from Washington, is creating a palpable crisis of confidence in our economy and our leadership.

While the Fed is signaling between the lines that it may be prepared for stronger action, Congress and the President seem to be headed in the other direction. Campaign politics have lawmakers talking more about contractionary fiscal discipline than taking any new actions to boost the economy. Even in the debate about extending the Bush tax cuts, the options being considered do not include anything stimulative compared to the status quo. Congress has painted itself into a corner by waiting until taxes are automatically set to go up if it fails to act, and now it will likely be forced to extend most or all of them simply to avoid a contractionary fiscal outcome. Again, playing economic defense.

It’s time we think seriously about shifting gears and talking about reasonable stimulus again, instead of waiting for the next hole to plug. As Will Marshall has argued here, keeping public spending and debt under control is critically important, and Democrats need to talk openly about how we prepare for the day of reckoning when the spending claw-backs kick in, since Republicans have lost all credibility on fiscal discipline. However, growth is still the most urgent concern; the signals from bond-market vigilantes are telling us that, as Stan Collander argues well today.

There is a still a place in the debate for looking into additional stimulus, both on the tax side and with additional cost-effective spending. For example, public investment in infrastructure can be used to leverage private capital off the sidelines as well by making the private sector an active partner in stimulus efforts. Instead of continuing to put fingers in the dyke, we need to be more proactive in finding the companies in the private sector who want to rebuild the dyke, and put people and money to work again.

The Federal Reserve’s outlook on the economic recovery continues to get gloomier. In its statement released following the FOMC meeting today, the Federal Reserve acknowledged that “the pace of recovery in output and employment has slowed in recent months,” and “economic recovery is likely to be more modest in the near term than had been anticipated.” Not good news, especially when interest rates are already about as low as they can go. With today’s announcement that it is committed to keeping rates at rock-bottom levels ”for an extended period” going forward, the Fed also signaled that it is ready to go beyond rate setting to strengthen the economy.

After keeping the federal funds at historic lows for so long, with only disappointment to show for it, the Fed has decided that it’s no longer enough to lead the U.S. economy to water and wait for it to drink. So as part of its announcement today, the Fed signaled that it will once more resort to quantitative easing to pump money directly into the economy. Because there are risks to this strategy (see Krugman), the Fed couched this move in modest terms, explaining that it will be buying long-term Treasury notes to “keep constant” the level of assets on its balance sheet, which currently includes a large portfolio of mortgage securities it purchased to stabilize markets during the financial crisis.

The Fed will simply be rolling over its portfolio into Treasuries as the mortgage securities retire, which is actually not putting new money into the economy, as much as it is preventing the money supply from shrinking if the Fed’s portfolio were allowed to get smaller. But there are signals here for those who have been anticipating a new push for quantitative easing from the Fed.

The First Signal: The Fed is clearly ready to buy market securities to inject money into the economy as needed. This baby step toward quantitative easing is likely a preview of more dramatic asset purchases if the Fed sees real evidence of deflation or a double-dip recession. Be prepared for more.

The Second Signal: The Fed is not necessarily interested in using mortgage securities as an asset vehicle for expanding the money supply. Doing so would keep mortgage rates low, which would help prop up an ailing housing market. But mortgage rates are already the lowest on record, and that hasn’t helped sales much, so the Fed doesn’t need to waste time trying to lead another horse to water in housing markets.

The overall signal from today’s FOMC statement is not good news for the economy. The Fed is becoming less optimistic and less certain about the future. Bernanke and company are apparently convinced that stronger actions may still be needed for sustained stimulus. The fact that they are coming around to that view may do some good for restoring confidence in Fed policy. And the Fed needs all the help it can get these days, because it’s running out of useful monetary tools to boost the economy.

Hopefully the signals from today’s statement will be heard in Congress, where lawmakers still have a lot of steps they can take before the end of the year to bring better stimulus and more confidence to the economy.

The International Monetary Fund recently scolded the U.S. government for running large budget deficits. Leaving aside the absurdity of cutting deficits when unemployment is still extremely high, it’s clear that at some point – as joblessness declines toward 5 percent – deficit reduction will need to begin in earnest. But the real question is how to do that. There’s a risk that the Washington economic class – grounded as they are in 20th century neo-classical economics — will fail to balance the twin imperatives of fiscal discipline and public investment.

Indeed the common refrain that has become the new “group think” in DC is that “everything should be on the table” when it comes to addressing the debt. For example, the Bipartisan Policy Center’s Debt Reduction Task Force says, “everything should be on the table.” Even President Obama, who has at least rhetorically talked about the need for increases in public investment and fought to include public investment in the stimulus, now says that everything should be on the table. Other groups echo this intellectually easy, but intellectually simplistic, position. Pete Peterson’s Concord Coalition likewise calls for “applying budget discipline to all parts of the budget.” The New America Foundation’s Committee for a Responsible Budget supports a budget freeze on all discretionary spending. For these budget hawks, subsidies to farmers to produce crops that aren’t needed fall in the same category as funding for the National Science Foundation to advance science and technology critical to our nation’s future: they both cost money and both should be cut.

The Government’s Role

But there are some things that governments do – on the tax and spending sides – which drive productivity, spur innovation, improve health, clean up the environment and create other benefits that most certainly should not be on the table. The National Commission on Surface Transportation Financing (which I had the honor of chairing) recently highlighted a federal highway and transit funding gap of nearly $400 billion over the next five years. Increased federal support for highways and transit would lead to significantly greater societal benefits (reduced traffic congestion, higher productivity) than the costs in revenues. Yet some groups wave the budget red flag to oppose expanded infrastructure investment, even if increased user fees, such as the gas tax, pay it for. As ITIF has demonstrated, increasing the Research and Experimentation Tax Credit from 14 to 20 percent would return $9 billion more to the Treasury than it would cost. And as ITIF and the Breakthrough Institute have shown, solving climate change requires significant increases in federal support for clean energy innovation, but the benefits (saving the planet) are massive.

What’s behind this widespread unwillingness to prioritize investment? Budget hawks fear that sparing one item from the chopping block will only validate the demands of interest groups to exempt their pet programs. In addition, many adhere to a neo-classical economics perspective, which holds that government plays a negligible role in economic growth and should be neutral with regard to private sector activity. In the purest form of this thinking, everything is on the table, because nothing is more important than anything else. To paraphrase Michael Boskin, a neo-classical Bush I economist, a dollar of public investment on computer chips has the same societal value as a dollar spent on potato chips. But government should be anything but neutral. Science and infrastructure funding is more valuable than farm subsidies. Government support for research in computer chips is more valuable than support for potato chips.

For liberals, reducing spending on entitlements will not only harm working Americans, but will also reduce economic growth, since Keynesian doctrine holds that growth comes from increasing aggregate demand – meaning pump more money into the economy, period.

In contrast, an innovation economics approach to the budget distinguishes between spending on consumption and spending on investment. For innovation economics advocates, all spending (either on the tax or expenditure side) should be on the table, and all investment (on the tax and expenditure side) should be off the table.

Tax, Cut and Invest

The last time Washington paid attention to deficits was in the first Clinton term. At that time PPI Vice President Rob Shapiro wrote a series of reports with the title, “Cut and Invest.” The notion was that we should cut unnecessary spending and use a significant share of the savings to invest in the nation’s future, including education, infrastructure and research. That was the right message then and it is the right message now. Although today, such a report might be best titled, “Tax, Cut and Invest.” To solve the budget deficit in a way that enables the significant increases needed in investment, we need to raise some taxes, cut some spending and increase some investment.

The general outline should look like this: On the tax side, we should let the Bush tax cuts on the wealthy expire, including: dividend taxes, estate taxes (above a certain modest size) and top marginal rates. We should increase the gas tax by at least 15 cents a gallon (and index it to inflation) and at the same time institute a carbon tax. We should consider a border-adjustable business activity tax. We should eliminate the home mortgage interest deduction. (Home ownership has many societal benefits, but as we see from other nations without these large tax incentives, nations can get high levels of home ownership without wasteful subsidies.)

On the spending side, we need to deal with entitlements, including: progressive indexing of Social Security benefits and increasing the retirement age, continued health care reform — particularly focused on driving innovation to cut costs and cutting entitlements to farmers — farm subsidies. This should be a gradual process to spread the pain over time.

And most importantly, we should significantly expand investments. We need to expand investments in education and training, science and research, technology (including, but not limited to clean energy) and physical infrastructure. In order to ensure that companies in the U.S. are globally competitive and create jobs here at home, we need to expand corporate tax expenditures. For example, create a new corporate competitiveness tax credit that would include a much more generous credit for research and development, and a credit for business investments in workforce training and new capital equipment, especially software. Making these investments will cost money in the short run. But they will also generate returns to the economy and the government in the long term. In economic downturns, successful corporations don’t cut key investments because they know that these investments are vital to gaining market share and competitive advantage in the moderate term. Governments should think the same way.

So let’s stop talking about putting everything on the table and instead recognize that not only do investments need to be off the table, they need to get more from what’s on the table.

Rob Atkinson is president and founder of ITIF, a Washington-based think tank providing cutting-edge thinking on technology and economic policy issues.

First the giant stimulus package, then the ambitious revamping of America’s health care delivery system. Now Congress, under the patient prodding of President Obama, is lurching toward passage of another stupendously complex bill, this time centered on financial regulatory reform. Whether you like them or not, you have to admit that big things are getting done in Washington on Obama’s watch.

If Congress passes the Dodd-Frank bill, it will be another major notch in the belt of a president who could use a political victory about now. But what’s a non-master of the universe like me to make of this 2,000-page behemoth?

It may do considerable good, but we ought to be clear about one thing: It won’t prevent the next financial crisis. As long as there are fortunes to be made in financial markets, there will be excessive risk-taking and speculation, new bubbles and panics, and powerful incentives for chicanery and fraud. No regulatory scheme can fully protect the public against ingenious new forms of human greed and folly.

That, however, is not an argument for doing nothing. The government had to react to Wall Street’s near meltdown in the winter of 2008-2009. Its interventions, beginning under President Bush and continuing into Obama’s administration, doubtless averted a full-bore financial collapse. But they also triggered a fierce and abiding public backlash against bailouts.

The Dodd-Frank bill doesn’t get everything right, but on balance it’s a reasonable response to the crisis. It imposes new disciplines on bank behavior, increases transparency for complex financial transactions and institutions, and offers consumers new protections against the clever breed of predators who have degrees from elite universities and sport $3,000 suits.

Some liberals are chagrined that the bill doesn’t break up the big banks. Conservatives echo the Wall Street Journal’s charges that the bill is a regulatory nightmare that will make it more expensive for banks to supply capital to businesses. It’s tempting to say that Sen. Chris Dodd (D-CT) and Rep. Frank (D-MA) must therefore have found some kind of centrist sweet spot, but there is something to the left-right critiques.

Most important, for example, the bill doesn’t slay the “too-big-to-fail” dragon. It leaves financial power more concentrated than ever in the hands of five mega-banks: Goldman Sachs, J.P. Morgan, Citigroup, Morgan Stanley and Bank of America. True, Dodd-Frank does impose the “Volcker Rule,” forbidding banks covered by federal deposit insurance from making bets (called “proprietary trading”) with their own money. It increases capital reserve requirements to keep banks from taking excessive risks. It also sets up a council of financial guardians to anticipate systemic risks, and gives federal authorities power to seize and oversee the “orderly liquidation” of financial firms whose collapse could bring other institutions down as well.

But it’s hard to avoid the impression that the big banks will henceforth operate with a tacit government guarantee against systemic failure. This not only intensifies moral hazard – making it hard for administration officials to claim the bill would bar bailouts in the future – it also risks creating a privileged class of quasi-public banking utilities that will be able to borrow money more cheaply. That will raise the bar for new entrants and dampen competition in the banking sector.

Elsewhere, the picture looks more positive. Dodd-Frank would move much of the trade in financial derivatives onto exchanges and clearinghouses, though banks could still trade in over-the-counter derivatives to hedge their own risks. This seems like a sensible compromise that brings derivatives trading out of the shadows while retaining the ability of firms to hedge against interest rate and currency risks. In another boost for transparency, the bill would require private equity firms and hedge funds to register with regulators.

Dodd-Frank also puts in place what Obama last week called “the strongest consumer financial protections in history.” It creates a new Consumer Financial Protection Bureau housed with the Fed to police mortgage lending, credit and debit cards and other consumer loans – though not by auto dealers, who somehow won an exemption from oversight. This agency presumably will prevent abuses like the “no doc” and “liar” loans that helped to trigger the subprime lending frenzy, which was the spark that started the financial crisis.

The bill doesn’t deal at all with Fannie Mae and Freddie Mac. This is a huge omission, considering that these giant mortgage finance firms still hold a pile of dubious assets and are essentially in federal receivership.

For all its imperfections, Dodd-Frank seeks to protect consumers without creating undue regulatory obstacles to innovation in the financial sector, which traditionally has been a source of comparative economic advantage for the U.S. Pragmatic progressives ought to support it, while retaining a sense of humility about the ability of new regulatory bodies to prevent future abuses.

How to tell a good climate bill from a bad one? This series will guide you through the main issues that are likely to arise in the coming weeks as the Senate takes on climate change. In previous posts, we looked at the crucial and the merely important issues that factor in the climate debate. In this post we highlight issues that matter for climate policy, but will not necessarily make or break it. (To read the other posts in the series, click here.)

So far, we’ve established the absolutely critical aspects needed to make credible climate policy and identified the important features that would make that policy effective. Now we will focus on issues that aren’t quite on the same level, negotiable elements that could still have a meaningful role in determining the long-term viability and effectiveness of a domestic emissions mitigation program. These issues — specifically, price controls and the international implications of U.S. legislation — could become a big part of the political discussion.

Category III Issues: Negotiable Elements of Climate Policy

#1: Price controls: offsets and collars

An uncontrollably rising carbon price is a nightmare scenario for regulated firms and consumers, so industry groups have made a priority of getting robust price controls into climate legislation. Price controls generally take three different forms: banking and borrowing, offsets and price collars. Because banking and borrowing has such a strong effect on the emissions reduction path, we included them in our last post. Here we’ll focus on the two other strong cost containment mechanisms.

a) Offsets

If you’ve been paying attention to the debate over the past two years, you’ve likely heard something about offsets. They are one of the most controversial aspects of climate legislation. Environmentalists are suspicious of them and industry can’t live without them.

What exactly are offsets? As we mentioned in a previous post, carbon is a stock pollutant, meaning that we only care about its total accumulation in the atmosphere. If you keep adding carbon to the system, but remove an equal amount at the same time, it is just as good as no longer adding carbon at all. This is the underlying principle of offsets — firms that pay to remove greenhouse gases from the atmosphere (or keep them from entering in the first place) can receive the same credit they would get if they reduced their own emissions.

For example, with offsets in a cap-and-trade system, a utility that needs to reduce its carbon emissions by 20 million tons need not do so only through emissions cuts from its operations. It could reduce its own emissions by 15 million tons, then receive offset credits through financing a reforestation project and an agricultural methane reduction project that combined would lead to emissions reductions of five million tons, allowing the company to meet its target.

Here is a quick list of different kinds of offsets that might count under climate legislation:

Forestry: Forests absorb CO2 through natural respiration processes and store it in plant tissue and soil. When deforestation occurs, that stored carbon is released into the atmosphere, contributing to emissions. Deforestation and forest degradation count for around 15 percent of global CO2 emissions. Projects that reforest — increasing carbon sequestration — or reduce deforestation and forest degradation are growing increasingly popular in voluntary carbon markets and may facilitate significant savings. Some models have speculated that international forest offsets can account for 25 percent of emissions mitigation by 2020.

Agriculture: The agricultural sector accounts for six percent of U.S. emissions, but agricultural emissions will probably not be covered by a carbon price due to the complexity of measuring emissions from agricultural practices and the power of the farm lobby in Washington. The important gases from agriculture are methane emissions from large-scale cattle operations and manure management, and nitrous oxide emissions from fertilizer applications and soil management. Offset projects that capture renegade methane emissions or reduce nitrous oxide releases through better soil management will likely be the most widespread offsets available from the agriculture sector.

Renewable energy/energy efficiency: Projects that supplant dirty energy sources with cleaner sources or improve efficiency in energy production or end-use can also be eligible for offset credit. For example, a firm looking for cheap reductions could finance the development of a renewable energy project and receive credit for the emissions reduced when the renewable energy displaces conventional dirty energy. Additionally, projects that increase the efficiency of energy usage in buildings or facilities can count as offsets. These projects are a major component of the Clean Development Mechanism (CDM), which was established by the Kyoto Protocol. Using the CDM, developed countries can sponsor projects in developing countries and receive emissions reduction credit.

Waste management: The decay of garbage in the nation’s thousands of landfills represents the second largest source of U.S. methane emissions behind cattle operations. Methane flaring, a process that captures and burns these emissions, converting methane into CO2, is considered an offset, as CO2 has a lower global warming potential than methane. Combusting methane for energy generation may also generate offset credits.

Fugitive mine emissions: As with landfills, capturing fugitive methane emissions from coal mines presents an opportunity for offsets and may also have benefits in terms of miner safety.

While all of these offsets options are currently available in voluntary offset markets and allowed by regional cap-and-trade schemes like RGGI, they may not all be eligible for credit under federal regulation. Waxman-Markey does not count renewable energy, energy efficiency, waste management and coal emissions as offsets. Cantwell-Collins does not allow offsets in its trading system, but it does permit such projects to be paid for from its Clean Energy Reinvestment Trust.

Many offsets will be cheaper than actual emissions reductions, making them an important means of price control. This is especially true for international forest offsets — the EPA analysis of Waxman-Markey contended that allowance prices would be 96 percent higher without them. That said, Greenpeace and other environmental groups have firmly planted their flag in the anti-offset camp, and there are a number of issues that would need some serious policy attention in order to make forest offsets credible in the U.S. market.

There are four major requirements to making offsets a robust tool. First, they must be additional — that is, projects should only be considered offsets if the specific practice would not have happened anyway. Second, offsets should have permanence — projects are only useful if they are not quickly undone (an offset for planting a tree is of little value if it is rapidly cut down). Third, offsets should be verifiable — there must be some way to confirm that projects are doing what they claim (for forests, this can be very difficult). Finally, offset programs should address leakage — they should not simply shift emission-generating activities somewhere else. These are all valid concerns, and all four will have to be addressed for offsets to be a credible part of climate policy.

Potential hang-ups for offsets will likely involve politicians’ hesitations to send large sums of money overseas, the reliability and veracity of offset credits, the number of offsets allowed for use by regulated firms and the type of offsets available from domestic sources. Despite the misgivings of some policymakers and commentators, offsets will figure prominently in domestic legislation. Waxman-Markey included two billion tons worth of offsets annually, a significant proportion of overall U.S. emissions, the same amount as in the Kerry-Boxer bill introduced in the Senate last fall. Instead of spending time and energy railing against them, policy discussions should instead focus on setting up institutions to fix the problems listed above.

b) Price collars

More than anything else, firms want some certainty when it comes to climate regulations. Planning capital investments over the long-term will be significantly affected by carbon prices, and the more predictable the changes over time, the better firms can plan ahead. Moreover, sudden system shocks in the form of extreme drops or increases in prices can be very expensive and detract from the efficacy of cap-and-trade markets.

To protect the system and reduce price uncertainty, policy-makers are looking to use a price collar in the allowance market. A price collar is a way to define a general price path by restricting how much the price can rise or fall. Price collars work by establishing a price floor — under which the allowance price can never drop — and a price ceiling — above which the price will not rise. It is a simple mechanism in concept, and can provide a lot of certainty for regulated parties and market participants. The price floor and ceiling should be spaced far enough apart to accommodate market dynamics and rise at some rate to match the general rise in allowance prices.

When allowance prices hit the floor, they simply remain at that price until trading forces the price to rise again. Things get more complicated when they hit the ceiling, however. There are two options to bring down the price, depending on if you employ a hard collar or a soft collar. A hard collar releases additional allowances into the system until the price drops, regardless of how many it takes to do so. By contrast, a soft collar uses a strategic reserve of set-aside allowances to reduce the price below the ceiling. The difference between the two is a matter of emissions certainty. A soft collar maintains the overall emissions cap by taking some out of the system at the beginning, much like a rainy day fund, whereas a hard collar just dumps allowances into the market until the price changes. Firms may favor a hard collar because it provides more price certainty, but people concerned about overall emissions will prefer a soft collar.

#2: International aspects

If and when Congress does pass climate legislation, its impact will reach far beyond our borders. The international implications of domestic climate policy are extensive, and while they do not play a huge role in the political discourse, they have sway over some notable policy choices.

a) International negotiations

The Conference of Parties (COP) 15 in Copenhagen in December 2009 was advertised as a chance for the U.S. to reclaim its place at the world leader and innovator on environmental issues. The U.S. was able to do that only partially, and that was due largely to the extraordinary personal diplomacy of President Obama. U.S. negotiators had little to work with, bringing with them no official legislation to show other nations while trying to broker a deal that could pass Senate muster. Without a signed bill, the 2010 COP in Cancun this coming November will probably turn out similarly; nations will bicker and haggle and eventually end up not making any kind of serious commitment sans U.S. leadership. The EU does not have the sway to move a global climate deal forward, while other major emitters like China and India don’t have the incentive to act.

That’s not to say international negotiations will not have some influence on the shape of U.S. legislation. At Copenhagen, the U.S. committed to provide $30 billion from 2010 to 2012 to developing countries for mitigation, adaptation, technology transfer and other assistance. Additionally, the conference agreed to establish an annual $100 billion fund — of which the U.S. is expected to give roughly $20 billion — for developing countries for the same uses. Some of this funding will likely be partitioned from current programs, but it will certainly not be enough. Revenues from carbon markets established by climate legislation — as well as allowance allocations — will likely provide the most reliable source of international funds. The tradeoff is that every dollar spent on helping other nations adjust to climate change is one that can’t be used domestically. Though it won’t dominate the debate over any climate bill, the use of carbon revenues for international financing could end up having a real impact.

b) Competitiveness and leakage

Certain industries with intrinsically large carbon footprints, such as cement, steel and paper pulp, are particularly sensitive to carbon prices. These industries are concerned that paying for their sizable emissions will reduce their overall output, leading to job cuts and smaller profit margins. Moreover, they worry that a U.S. carbon price will lead to a shift in production to other countries that do not have similar regulatory burdens. When firms leave for other countries that don’t have a climate policy, it could lead to higher overall global emissions, a phenomenon known as leakage.

There are a couple of solutions to these problems. First, to help protect industries at home, climate policy can include rebates to industries — either in the form of cash or extra tradeable allowances — based on their output to help them adjust to the new reality of a price on carbon. Second (and more controversial), the federal government can establish border adjustments, slapping taxes on imports competing with vulnerable domestic industries. Essentially tariffs, such levies would put goods from countries without a climate policy on the same level as those from the U.S. Border adjustments can make for tricky politics, though. When the Waxman-Markey bill passed the House in 2009, President Obama openly criticized the inclusion of such measures. When the debate picked up in the Senate, however, 10 Midwestern senators stated they would not back any climate legislation that did not support manufacturing interests with some kind of border provision. Even if some compromise allows border adjustment to find its way into climate legislation, there’s a chance it would not be allowed under WTO agreements.

The Bottom Line

Last post, we reviewed important aspects of climate policy. In this post, we surveyed two areas that have value in generating good policy, but are negotiable in terms of their importance:

Is there a price collar? Are offsets allowed?

What is the effect of the proposal on international climate issues? How will it affect negotiations and commitments? How does it attempt to protect trade-vulnerable industries?

In our next and final post, we will focus on the issues that make little contribution to good climate policy — or might even be counterproductive.

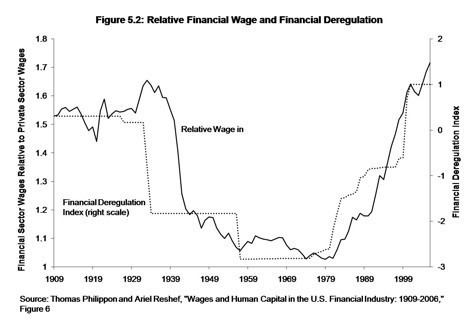

James Kwak, coauthor of the new financial crisis book 13 Bankers, recently sought to explain his thesis “in 4 pictures.” And impressive pictures they are. But I’ve been particularly struck by one of them — this chart, from a paper by economists Thomas Philippon and Ariell Reshef, showing the close correspondence between deregulation trends on the one hand and the ratio of financial sector wages to private sector wages on the other. My reaction to the chart was essentially, Huh. Those trend lines look like the basic income inequality trend line.

But to my knowledge, no one has really made this point since the chart has circulated widely. Certainly no one has tried to illustrate it.

Maybe people just lack my whiz-bang PowerPoint and Excel skills, or maybe I’ve actually had an Original Thought. But take a look at the chart I created, which overlays a trend line showing the share of income received by the top one percent (the black line) on top of the Philippon-Reshef chart. The trend line comes from the widely cited work of economists Thomas Piketty and Emmanuel Saez, who used IRS data to look at the incomes of the very rich:

I’ve argued before that I think the Piketty-Saez top-share trend line overstates the recent rise in income inequality, but I don’t see much reason to doubt the basic U-shape of the trend since the Great Depression. For all of the consensus around the basic inequality trend, there’s surprisingly little agreement or understanding as to why it looks the way it does (a major theme of Paul Krugman’s Conscience of a Liberal). Could it really be as simple as the extent of financial regulation? Every analyst bone in my body says this is too easy, but…but….

Of course, saying it’s all financial regulation trends isn’t necessarily inconsistent with Krugman-esque arguments that it’s all about changes in cultural acceptance of inequality. Maybe financial regulation flows from public attitudes about inequality.

As the Senate turns to financial reform this week, the big question is whether any Republicans will join in, or whether the party will stick to its new political doctrine of Maximum Feasible Obstruction.

This doctrine is predicated on the idea that Barack Obama, elected with nearly 53 percent of the vote, is a dangerous radical bent on extinguishing American liberties and importing Euro-style social democracy. It’s an idea so crazy on its face that many progressives are convinced that racism must lurk behind it.

Maybe, but some conservatives also convinced themselves that Bill Clinton maintained a secret airport in Arkansas to import narcotics from Central America. The right’s feral attacks on Clinton led a sympathetic Toni Morrison to dub him in a figurative sense “America’s first black president.”

Whether or not race is a factor, Republicans have evidently calculated that there is no political cost in withholding cooperation from Obama, at least on domestic issues. That may have been true of health care, which lost public support as the debate wore on. But fixing Wall Street is another matter.

The Pew Center for Research reported yesterday that Americans overwhelmingly favor (by 61-31) reform of financial rules, even as they evince growing skepticism of government activism. It’s pretty clear the public takes a “never again” stance toward bailing out Wall Street bankers, speculators and bonus babies.

That’s why Mitch McConnell, the GOP Senate leader, latched onto the theme that the bill crafted by Sen. Chris Dodd (D-CT) would actually make future bailouts more likely. President Obama blasted that “cynical and deceptive assertion” over the weekend, and McConnell yesterday seemed to back down.

Still, Democrats need Republican votes to bring a bill to the floor. The Washington Postreports this morning that Democrats are targeting Sens. Olympia Snowe and Susan Collins of Maine and Bob Corker of Tennessee. Bucking his party’s sullenly oppositionist temper, Corker has worked constructively with Sen. Mark Warner (D-VA) to offer sensible improvements to the Dodd bill.

That bill is snagged on GOP opposition to a new regulatory body, to be independent but lodged in the Federal Reserve, that would protect consumers of credit cards, mortgages and other loans from deceptive or predatory practices. Dodd has signaled a willingness to compromise on another controversial provision, an industry-financed $50 billion fund to liquidate bankrupt firms. And the New York Times reports today financial sector lobbyists have lavished contributions on members of the Agriculture Committee, which is grappling with a key provision to regulate derivatives.

During the health care debate, Republicans did not appear to be moved by the plight of Americans with no medical insurance. But financial reform involves something Republicans traditionally care deeply about – money. Where are the sobersided conservatives of yesteryear, who understood that the safety and soundness of our financial system is fundamental to America’s economic health? Striking the right balance between regulation and innovation, security and risk, is an urgent national priority that ought to engage responsible leaders in both parties.

If Republicans aren’t willing to set aside reflexive partisanship long enough to stand up for American capitalism, we really are in a world of political hurt.

In a classic example of a “slippery slope,” Congress once again is looking for easy pickings by increasing guarantee fees (g-fees) that Fannie Mae and Freddie Mac charge lenders to guarantee their mortgage lending. Last December, Congress raised the GSE’s g-fee by 10 basis points for 10 years. The goal was to raise almost $36 billion to pay for the extension of the payroll tax cut. Although this was supposed to be a one-time revenue plug, some lawmakers called for

In a classic example of a “slippery slope,” Congress once again is looking for easy pickings by increasing guarantee fees (g-fees) that Fannie Mae and Freddie Mac charge lenders to guarantee their mortgage lending. Last December, Congress raised the GSE’s g-fee by 10 basis points for 10 years. The goal was to raise almost $36 billion to pay for the extension of the payroll tax cut. Although this was supposed to be a one-time revenue plug, some lawmakers called for  This week in housing was an especially busy one; PPI looks at just a few highlights with Case-Shiller numbers, a new government pilot program on housing and a huge announcement from Bank of America. Let’s get to it.

This week in housing was an especially busy one; PPI looks at just a few highlights with Case-Shiller numbers, a new government pilot program on housing and a huge announcement from Bank of America. Let’s get to it.

Whether U.S. Presidents succeed or fail often depends on a big factor beyond their control: the timing of the business cycle. Lucky Presidents – Ronald Reagan, George W. Bush – experienced downturns early in their first term, leaving plenty of time for an economic rebound to lift them to reelection.

Whether U.S. Presidents succeed or fail often depends on a big factor beyond their control: the timing of the business cycle. Lucky Presidents – Ronald Reagan, George W. Bush – experienced downturns early in their first term, leaving plenty of time for an economic rebound to lift them to reelection.

The economic news out of Washington this week has an eerie ring of déjà vu: Congress just passed an emergency spending bill, the Fed is buying debt securities to keep the economy from sliding toward collapse, and the Administration announced it is committing billions of dollars to mortgage relief for homeowners facing foreclosure. To be sure, none of these actions has the scale or urgency of the initial responses to the financial crisis, but they are perfect examples of the policy philosophy that has dominated both economic policy since the crisis: a focus on playing defense, rather than offense.

The economic news out of Washington this week has an eerie ring of déjà vu: Congress just passed an emergency spending bill, the Fed is buying debt securities to keep the economy from sliding toward collapse, and the Administration announced it is committing billions of dollars to mortgage relief for homeowners facing foreclosure. To be sure, none of these actions has the scale or urgency of the initial responses to the financial crisis, but they are perfect examples of the policy philosophy that has dominated both economic policy since the crisis: a focus on playing defense, rather than offense. The Federal Reserve’s outlook on the economic recovery continues to get gloomier. In its

The Federal Reserve’s outlook on the economic recovery continues to get gloomier. In its  The International Monetary Fund recently scolded the U.S. government for running large budget deficits. Leaving aside the absurdity of cutting deficits when unemployment is still extremely high, it’s clear that at some point – as joblessness declines toward 5 percent – deficit reduction will need to begin in earnest. But the real question is how to do that. There’s a risk that the Washington economic class – grounded as they are in 20th century

The International Monetary Fund recently scolded the U.S. government for running large budget deficits. Leaving aside the absurdity of cutting deficits when unemployment is still extremely high, it’s clear that at some point – as joblessness declines toward 5 percent – deficit reduction will need to begin in earnest. But the real question is how to do that. There’s a risk that the Washington economic class – grounded as they are in 20th century  First the giant stimulus package, then the ambitious revamping of America’s health care delivery system. Now Congress, under the patient prodding of President Obama, is lurching toward passage of another stupendously complex bill, this time centered on financial regulatory reform. Whether you like them or not, you have to admit that big things are getting done in Washington on Obama’s watch.

First the giant stimulus package, then the ambitious revamping of America’s health care delivery system. Now Congress, under the patient prodding of President Obama, is lurching toward passage of another stupendously complex bill, this time centered on financial regulatory reform. Whether you like them or not, you have to admit that big things are getting done in Washington on Obama’s watch. So far, we’ve established the absolutely

So far, we’ve established the absolutely

As the Senate turns to financial reform this week, the big question is whether any Republicans will join in, or whether the party will stick to its new political doctrine of Maximum Feasible Obstruction.

As the Senate turns to financial reform this week, the big question is whether any Republicans will join in, or whether the party will stick to its new political doctrine of Maximum Feasible Obstruction.{kind=link}