Unfazed by President Trump’s non-stop belligerence in last Tuesday’s debate, Democratic presidential nominee Joe Biden embarked the next morning on a whistle stop tour of Ohio and Pennsylvania — two pivotal states Trump won in 2016 that now seem to be slipping from his grasp.

In addition to their huge importance as presidential battleground states, Pennsylvania and Ohio rank among the top five U.S. states in natural gas production. No wonder Trump keeps trying to convince voters there that the former vice president is a Green New Deal zealot eager to ban drilling for natural gas.

Only it’s not true, and it’s not working. According to a new ALG Research Poll commissioned by the Progressive Policy Institute (PPI), Biden is leading Trump in Pennsylvania (50-44) and Ohio (48-46). What’s more, Biden is running significantly ahead of Hillary Clinton’s 2016 performance in the “shale belt” — the gas-producing counties of Southeastern Ohio and Western Pennsylvania that Trump won handily last time.

Donald Trump is a serial vandalizer of America’s democratic ideals and institutions. Last night, his victim was the presidential debate.

Down in the polls and obviously frustrated by events he cannot control – especially the Covid-19 pandemic – Trump was like a disturbed child acting out in school to get attention. He simply could not control himself. He could not restrain himself even for the two minutes Joe Biden was allotted to answer questions.

Instead he interrupted constantly, talking over his opponent with a steady fusillade of taunts, insults and bald-faced lies. Biden correctly called him “unpresidential,” but that doesn’t begin to describe Trump’s sickening behavior last night. Bullying, malicious, ranting incoherently, he sabotaged every attempt at rational argument.

It will be interesting to see how Trump’s legion of apologists and lickspittles try to explain away his deranged performance in Cleveland. If here are any self-respecting conservatives and Republicans left who truly venerate America’s democratic traditions, they must be feeling very queasy this morning.

If Trump lacks the self-discipline to abide by the rules of presidential debates – rules his campaign officials agreed to – there’s no point in inflicting two more of them on the American people. Neither Biden nor the media has any obligation to collude in Trump’s attempts to turn presidential debates into a tawdry theater of demagoguery and abuse.

U.S. voters already know enough about Donald Trump and Joe Biden to make an informed choice in November. The vote can’t come soon enough.

Following last night’s debate, Joe Biden will campaign in Pennsylvania and Ohio, where a new poll released today by the Progressive Policy Institute (PPI) shows him leading President Trump. In addition to their huge importance as presidential battleground states, Pennsylvania and Ohio are energy powerhouses that rank among the top five U.S. states in natural gas production.

The poll, commissioned by PPI and conducted by ALG Research, finds Biden ahead by six points in Pennsylvania (50%-44%) and two points in Ohio (48%-46%), despite Trump’s attempts to brand Biden falsely as an opponent of “fracking” and natural gas. Biden also is running ahead of Hillary Clinton’s 2016 performance in the “shale belt” — the gas-producing counties of Southeastern Ohio and Western Pennsylvania.

“Unlike the ‘drill, baby drill’ right and the ‘keep it in the ground” left, voters in midwest states like Pennsylvania and Ohio show a deeply pragmatic streak on energy and climate issues,” said PPI President Will Marshall. “They are not climate deniers like Donald Trump, and they view natural gas as a bridge, not a barrier, to America’s clean energy transition.”

Key poll findings:

71% of Pennsylvania and Ohio voters — and 66% in gas-producing counties — say climate change is a “real and very serious problem.”

Voters oppose a ban on natural gas by an enormous margin — 53 points (74-21%).

Even among liberal leaning groups, there is little appetite for a ban: Democrats, young voters and advanced degree holders oppose a ban by 30, 29 and 55 points respectively.

Voters’ biggest worry about banning gas production is job loss, following by higher energy prices.

Voters do not want to use fossil fuels indefinitely, but they see natural gas as playing an important role in supporting U.S. renewable energy growth over the medium term.

Voters expect it will take a decade or more to end use of natural gas without disruptions to the economy, electric reliability, and energy bills.

Despite Biden’s lead in this poll, voters split over who they trust more on energy issues.

“Voters know where Trump stands on energy, but they aren’t as certain about Biden,” said Marshall. But when it’s described to them, 52% of voters say they support a Biden plan that does not ban fracking, continues to use natural gas and requires the United States to achieve zero carbon emissions by 2050.

Media contact: Carter Christensen, cchristensen@ppionline.org

Appendix B: State Breakdowns on Key Findings:

o Pennsylvania: Voters oppose a natural gas extraction ban by 72-23%.o Ohio: Voters oppose a natural gas extraction ban by 76-19%.

o Pennsylvania: Democrats oppose a ban on natural gas extraction by 59%-32%.o Ohio: Democrats oppose a fracking ban by 65-30%.

o Pennsylvania: The biggest worry associated with banning natural gas is job loss (40%), followed by increased energy prices (20%) and energy shortages (15%).

o Ohio: The biggest worry associated with banning natural gas is job loss (26%), followed by increased energy prices (18%) and energy shortages (15%).

o Pennsylvania: 57% of voters see natural gas as playing an important role in supporting U.S. renewable energy growth over the medium-term.

o Ohio: 53% of voters adhere to this view.

o Pennsylvania: 43% of voters say we should be using more natural gas; 34% say we should be using the same amount of natural gas versus; and, 18% say we should use less natural gas.

o Ohio: 41% of voters say we should be using more natural gas; 37% say we should be using the same amount of natural gas; and, 18% say we should use less natural gas.

Joe Biden’s job in tonight’s debate is actually very simple. It is to constantly remind viewers that Donald Trump isn’t what he claims to be, a radical outsider challenging a corrupt status quo. Trump is the swampy status quo in Washington. He’s an incumbent with a record to defend — and it’s indefensible.

As Bill Clinton likes to say, a presidential campaign is basically a job interview with the American people. Based solely on Trump’s job performance, voters should throw his own tagline back at him: “You’re fired.”

Trump excels at self-promotion, not producing actual results. The glimpse America has gotten at his tax records confirms that he is a clever tax evader (so far) and a lousy businessman. He loses more money than he makes and most of his branding ventures go belly up. Where are the Trump Steaks of yesterday?

But it doesn’t really matter, because Trump’s businesses are simply a means to an end: the glorification of Donald Trump. They provide a platform for Trump to impersonate a business tycoon. The fancy hotels and golf resorts, the now-bankrupt casinos and beauty pageants, the Playmates and private jets — it’s all for show.

Trump’s perverse genius lies in fabricating a loser’s idea of a winner. It’s no accident that his only recent money-maker was playing a capitalist buccaneer on TV.

Now the Trump Show has moved to Washington, where Trump is pretending to be president of the United States. Just as he lacks the patience and skill to effectively manage a business, he has zero interest in the details of governing. What’s his second-term agenda? The further feeding of Trump’s monstrous ego.

How do you debate a carnival barker who hogs the spotlight with a volcanic cascade of lies, abuse, bigotry and wild conspiracy theories? You don’t.

When future generations — or simply young people today — look back at the topics of recent U.S. presidential debates, they will be stunned that America’s political journalists ignored climate change, the issue that will overwhelm most others in coming years. In essence, debate moderators have pretended climate change doesn’t exist.

Not a single question on climate change was asked by any moderators in the three 2016 presidential debates, even though Donald Trump and Hillary Clinton had diametrically opposing views on climate science and policy. The same silence occurred in the previous round of debates in 2012, and also 2000, and 1996. And now climate change has been ruled out as a topic at the first 2020 Presidential debate this Tuesday in Cleveland.

The consequences on American policy of this willful climate silence during debates has been remarkably far-reaching, especially during Donald Trump’s presidency. The U.S. is the only country in the world to leave the Paris Climate Agreement, and Mr. Trump has ignored entreaties by other world leaders to use other means to make progress on the issue. Domestically, the Trump Administration has repealed or attempted to rollback every climate protection it can, especially limits on greenhouse gas emissions from most major sources, including power plants, cars, and oil and gas drilling.

At every turn, the Trump administration and Republicans in Congress have bungled the coronavirus pandemic and shortchanged our recovery. For the first month after most programs created by the CARES Act – the last major stimulus bill passed by Congress back in March – expired, the GOP wasted valuable time on half-measures that could not pass and executive orders that do not help. Washington Republicans have now completely abandoned work on further relief measures so they can focus on a partisan gambit to pack the Supreme Court with yet another right-wing justice before voters have a chance to make their voices heard in just five weeks.

It didn’t have to be this way. Back in May, House Democrats passed the $3 trillion HEROES Act that they intended to be a follow-up to the CARES Act. Although the bill had many flaws, it offered a starting point for negotiations. Their Republican counterparts in the Senate, on the other hand, spent two months doing literally nothing to advance any additional relief legislation. It was only a full month after the major provisions in the CARES Act had expired that the Republican-controlled Senate voted on a partisan $500 billion “skinny” stimulus bill, which then failed to pass the chamber. Negotiations have now stalled due to GOP’s insistence on penny-pinching for a critical stimulus bill that, it should be noted, would almost certainly be less expensive than the wasteful $2 trillion tax cut the party enacted at the height of our most recent economic expansion.

In an attempt to cover for his party’s fecklessness, President Trump issued a series of executive orders ostensibly designed to fill the needs for further relief unmet by Congress. But as is too often the case with Trump, these actions were almost entirely superficial – and in some cases, actively harmful to the people supposedly helped. Rather than playing these pointless partisan games, Republicans need to join Democrats at the negotiating table and deliver a real solution for the millions of Americans struggling to survive amidst a global pandemic and the worst economic crisis since the Great Depression.

Anyone at Risk of Contracting Coronavirus

The first priority for policymakers must be controlling the pandemic, as our economy cannot fully recover until people feel safe going in public to work or spend money. Adequate testing and tracing are essential to preventing the virus from spreading until a vaccine is found, but delays in test results have already undermined our COVID response. Democrats proposed $75 billion for coronavirus testing and contact tracing as part of their stimulus proposal in the HEROES Act, while Republicans proposed a much-smaller $25 billion investment, including just $16 billion of new funding not reallocated from CARES Act programs. But without a deal, neither side gets any investment – and the virus continues to spread through our communities.

People Who Have Lost Their Jobs

Up to 26 million Americans remain unemployed thanks to the pandemic. In normal times, unemployment benefits typically only cover 34-54 percent of lost wages for a limited period of time. These benefits, however, are woefully insufficient during a prolonged period when few job openings are available to be filled. The CARES Act sought to address this problem by increasing UI benefits by $600/week through the end of July and extending the maximum number of weeks someone could claim unemployment benefits until December.

Democrats proposed to continue the full $600/week until January (or tie the extension of benefits to real economic indicators), while Republicans wanted to replace it with a $300/week supplement through the election). There was a very reasonable middle-ground here, as both sides agreed that supplemental unemployment benefits should not be allowed to expire in their entirety – but because no agreement was reached, that is exactly what happened.

Trump claimed to resolve the problem with an executive order letting states use Federal Emergency Management Agency (FEMA) money to establish a supplement for unemployment insurance. But this approach was riddled with problems: it depended on state unemployment offices, which are already burdened with crushing caseloads and obsolete information technology, to set up new administrative structures, delaying the receipt of benefits. The new supplement was worth only half as much as the one authorized by the CARES Act, and was not made available to low-income workers who receive less than $100/week in normal unemployment benefits. Finally, the FEMA fund only had enough money to fund benefits for six weeks – and required drawing upon funds that will likely be needed to fight wildfires out west and repair damage from hurricanes in the south.

Landlords and Lenders

Failure to adequately support unemployed Americans will have cascading effects throughout the economy. Because the unemployed then cannot spend as much money as usual, the businesses that rely on their patronage also lose income, which hurts workers throughout the broader economy and deepens the recession. They are also more likely to fall behind on payments for rents, utilities, or mortgages. The CARES Act included a temporary moratorium on evictions, but now that it is expired, millions of American families are at risk of losing their homes by the end of the year. Democrats have proposed imposing an even broader moratorium than was included in the CARES Act. The Trump administration, meanwhile, ordered the Centers for Disease Control to enact a limited moratorium on evictions until the end of the year for low- and middle-class renters.

Although a moratorium may give at-risk renters some temporary relief, it fails to resolve the underlying issue: lost income. Trump’s moratorium simply delays the inevitable for any renter who is behind on rent and would otherwise face eviction. Meanwhile, smaller landlords will lose out on income they need to pay for mortgages and property taxes, which puts them at risk of default. Lenders may also face significant losses from landlords and homeowners unable to make their required payments. If Congress were to instead provide adequate income support for people who have lost their incomes in the pandemic, they would ensure people can afford to remain in their homes without creating these new burdens.

Small Businesses and Their Workers

The CARES Act included a Payroll Protection Program (PPP), which gave small- and medium sized-businesses money to retain their workforce. That funding dried up when the program ended on August 8th. Here, Congressional Republicans actually want to be more generous, proposing almost $360 billion in small business support, loans, and employee retention provisions, while Democrats proposed $290 billion. But without a deal, small businesses – many of which are operating in industries, such as dining and hospitality, that have been particularly hurt by the pandemic – have not gotten any more support.

The only support for small businesses in President Trump’s executive orders was a counterproductive payroll tax holiday. Neither party in Congress supported Trump’s previous proposals to temporarily cut the payroll tax, so instead he used his limited authority to defer collection of some payroll taxes until next year. But since workers will still owe that money in 2021, many employers are just withholding the tax anyway. Meanwhile, federal workers – including those in the military – who cannot opt out of deferral are being advised not to spend the money so they aren’t financially flattened by the massive tax bill for back taxes they will receive next year.

State and Local Governments

The coronavirus pandemic has blown a massive hole in the budgets of state and local governments: income and sales taxes are drying up while spending on safety-net programs, such unemployment insurance and Medicaid, have increased dramatically. Because most state and local governments are required to balance their budget, this fiscal squeeze will compel them to cut their budgets right when people and businesses need government support the most.

Although Congress included some aid for state and local governments as part of the CARES Act, it only allowed this money to be spent on new coronavirus-related expenses, not to replace lost revenues. Republicans have proposed to loosen rules on how states could spend this aid, but offered no additional funding. Democrats, meanwhile, included almost $1 trillion in new funding for state and local governments in the HEROES Act.

Many on the right have argued that providing further aid would be a “bailout” for the finances of poorly-managed states, but this criticism is at best deeply misguided. PPI projects that state and local governments will need at least $250 billion in additional support beyond what was already appropriated before the end of 2021 just absorb the pandemic’s financial impacts without making deep cuts to essential services – and this figure could be even higher if the economic impact of this unpredictable crisis is worse than current projections. Rather than argue over an arbitrary dollar amount, Congress can easily address the concerns of both Democrats and Republicans by designing programs that provide aid to state and local governments based on the real pandemic-induced shortfalls realized on their balance sheets.

Parents and Families

The pandemic has taken a particularly brutal toll on parents who are unable to send their children back to school this fall. It is difficult for workers to do their jobs, either remotely or in-person, when they are unable to access child care that they usually could depend on at this time of year. It also poses a special burden on students from low-income families who lack the internet access necessary to participate in online classes.

The good news here is that both parties have proposed about $100 billion in additional support for schools. But they disagree on what it should be used for: the Trump administration would use this money to pressure school districts across the country to return to in-person classes, the even though doing so would be unsafe without the proper public health safeguards in place. The Democrats’ proposal, on the other hand, would also enable schools to stand up high-quality remote learning to keep their students learning while school buildings remain closed.

Unfortunately, these nuances don’t even matter at the moment: because Congress failed to reach a broader agreement, schools have received no additional federal support. Even worse, the looming shortfalls facing state and local budgets are likely to result in deep cuts to education spending (as they did following the 2008 financial crisis), further jeopardizing the long-term opportunities for children and families.

Voters

State and local governments face an unprecedented challenge administering a national election in the midst of a pandemic, made even worse by foreign governments threatening to interfere again like they did in 2016. The HEROES Act included $3.6 billion to support election integrity and vote-by-mail operations to make sure every vote is counted, while the Senate bill included nothing. As we enter the final stretch of what is perhaps the most contentious presidential election in modern history against the backdrop of several overlapping national crises, the failure of federal policymakers to support election infrastructure jeopardizes the bedrock of our democracy.

Conclusion

Although neither party’s proposals have been perfect, only one is making any serious effort to find common ground and support our economy in a time of unprecedented crisis. While House Democrats prepare to vote this week on a new package of proposals that is more moderate than the HEROES Act they passed four months ago, President Trump and Senate Republicans are leaving millions of Americans in the lurch by prioritizing partisan court packing over any further fiscal relief. Democratic candidates for office and all stakeholders, from the worker who is at risk of losing her home along with her unemployment benefits to the parent who cannot save his small business and give his child a decent education at the same time, should pressure Republicans to return to the negotiating table and work in the public interest – or face severe consequences in November.

The Progressive Policy Institute hosted a conversation on how members of the Democratic Party can better protect recent gains made by Black and Brown students while advancing these gains after the 2020 Presidential Election. The conversation surrounded gains made by Black and Brown students, how these gains were made, and more importantly how Democrats can ensure the gains continue under the next Administration.

Speakers:

U.S. Senator Michael Bennet, (D) Colorado

David Osborne, Progressive Policy Institute

Honorable Antonio Villaraigosa, Former Mayor, City of Los Angeles

Keri Rodrigues, National Parents Union

Dr. Howard Fuller, Freedom Coalition for Charter Schools

Moderator: Curtis Valentine, Deputy Director of Reinventing America’s Schools Project.

The Covid-19 crisis has put a spotlight on how archaic government systems are failing to keep up with the times and handle an unexpected surge of applications for public assistance programs. Cybersecurity threats have demonstrated vulnerability in aging government IT systems. New missions and requirements for government technology capability have shown the limitations of 20th century technology systems and resources for addressing 21st century needs.

The scale of the problem is massive. According to our estimates, federal, state and local governments would have needed to spend an accumulated $316 billion more over the past 20 years to have kept up with the growth of software investment per worker in the private sector. This should be viewed as a lower bound on the shortfall in government IT investment, as this figure excludes hardware investments that also should have been made.

Washington needs to build incentives inside government for a technology culture of continuous improvement and innovation to keep up with external technology developments and changes. Absent such a major modernization strategy, government will become less and less functional in our everyday lives. We need a big push to modernize government, using new digital tools not only to deliver services more efficiently, but to reengineer public services to make them more citizen-friendly and empowering.

To meet public expectations for the kind of speed, versatility, accuracy and efficiency that Americans experience in the non-governmental aspects of modern daily life, we must once again reinvent government just as we did 25 years ago at the beginning of the internet age.

Congress has tried to provide critical relief to Americans during the Covid-19 pandemic — passing three phases of disaster relief totaling 13.6 percent of GDP — but the rollout of support has been marred by obsolete IT and bureaucratic culture.1 In June, the House Ways and Means Committee estimated between 30 to 35 million stimulus checks had yet to be issued.2

The initial rounds of the Paycheck Protection Program (PPP) also were plagued by institutional delays, internal IT system crashes and incomplete, inaccurate and lagging databases. An April 2020 survey by the National Federation of Independent Business found that 28 percent of small business owners were unsuccessful in submitting an application for funds.3 The Small Business Administration’s loan processing system, known as E-Tran, crashed twice in April, frustrating lenders and small business owners seeking relief.45

State governments have also stumbled. For example, unemployment offices have been stretched thin as roughly 58 million Americans have filed claims since March.6 In Washington State, only 41 percent of claims had been paid as of July 30.7 Florida’s unemployment website has crashed repeatedly, with phone calls to the office going unanswered8, and citizens complaining of lengthy delays. Frustrated workers in Oklahoma and Kentucky have camped out overnight in front of unemployment offices for answers.9

Government IT Woes Predate COVID

The COVID-19 crisis is just the latest example of a chronic issue plaguing government programs at the state and federal levels. Poor information technology infrastructure and practices, antiquated and siloed systems, and outdated databases, have led to three main issues: security vulnerabilities, poor user experience and lengthy delays for citizens interacting with their government.

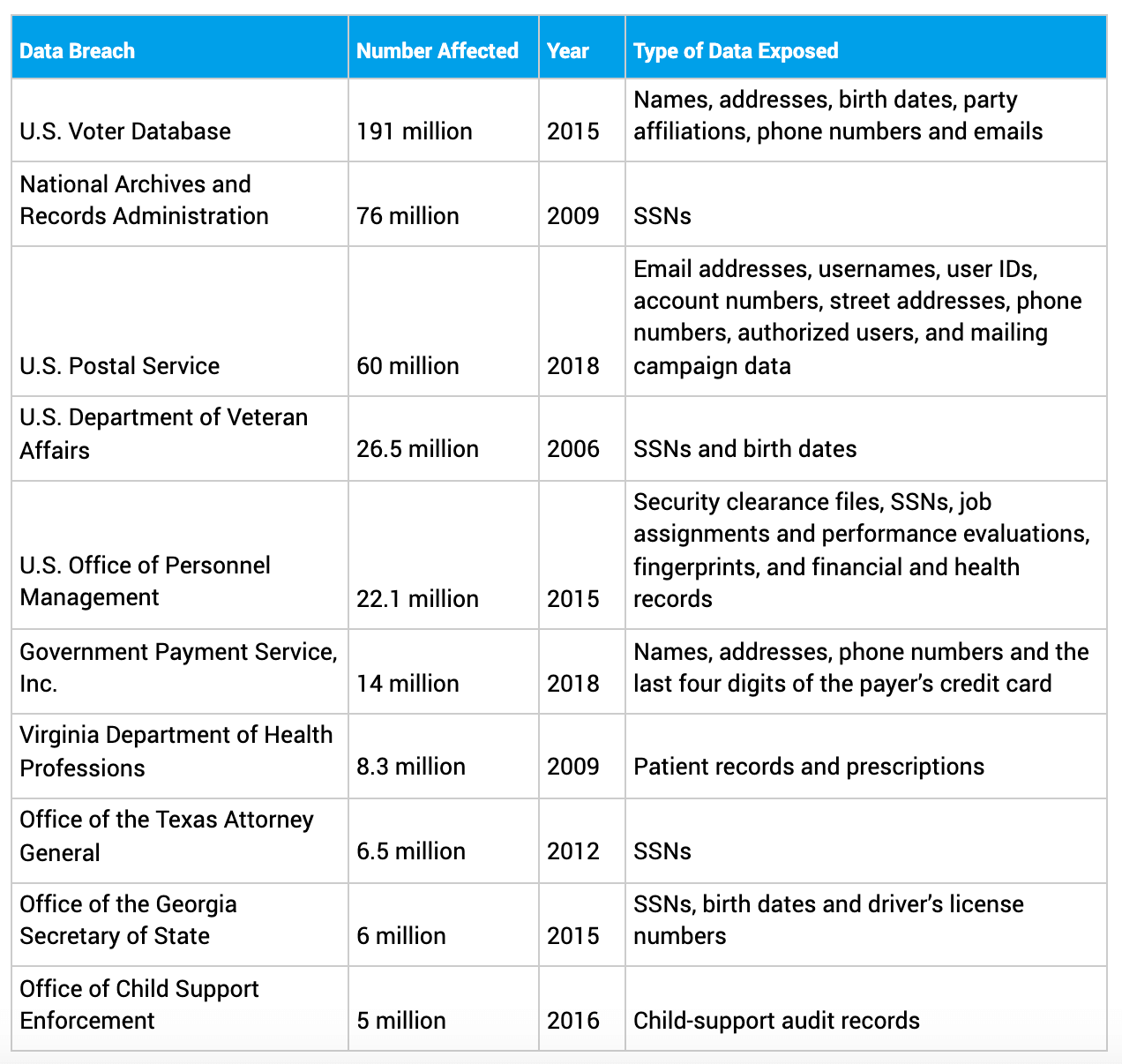

On the question of data security, perhaps the most infamous case is the data breach of the U.S. Office of Personnel and Management (OPM) in 2015 by hackers working for the Chinese military.10 The incident affected 22.1 million Americans and included data on security clearance files, Social Security numbers (SSNs), job assignments, performance evaluations, fingerprints, and financial and health records.

Most disturbingly, data missing from the OPM database could potentially be used by foreign spy services to uncover CIA operatives working under diplomatic cover, as Ellen Nakashima reported for TheWashington Post: “Names that appear on rosters of U.S. embassies but are missing from the OPM records might, through a process of elimination, reveal the identities of CIA operatives serving under diplomatic cover.”11

But while the OPM hack may have attracted the most attention in recent years, it wasn’t even the largest hack of U.S. government data in terms of the number of people affected. As shown in the table below, data breaches of the U.S. Voter Database, the National Archives and Records Administration (NARA), and the U.S. Postal Service (USPS) each affected more than 50 million Americans.

Table 1: Largest Government Data Breaches

Source: Government Accountability Office

15 In addition to data breaches, government databases are often inaccurate and out of date, leading to ineffective performance. For example, the IRS taxpayer database contains incomplete and aging data, which resulted in improper payments in PPP benefits to large numbers of dead taxpayers, returned payments that were misdirected, and even funds sent abroad to foreign citizens of other countries. 1213

Currently, the U.S. government spends the vast majority of its IT budget on maintaining and operating older legacy systems rather than upgrading and modernizing them. A 2019 Government Accountability Office report found that 80 percent of the $90 billion the federal government planned to spend on IT in 2019 would be used to operate and maintain existing systems.14 As shown in the table below, the report concludes that there are 10 legacy systems most in need of modernization, a few of which are more than 45 years old. One system at the Department of Education still runs on Common Business Oriented Language (COBOL), a programming language first introduced in 1959.

COBOL was originally designed for mainframe computers. While it has mostly died out in the private sector as businesses have transitioned from owning on-premise mainframe computers to renting cloud computing services from Amazon, Microsoft, or Google, COBOL has been in the news recently as government relief programs struggle to cope with surging demand.16

Government systems still rely on this outdated technology for essential services. At the state level, COBOL has been used to keep unemployment insurance programs running continuously for 40 years (34 state unemployment systems still depend on it today).1718 And during the current crisis, New Jersey’s governor put out a call for volunteers fluent in COBOL to help fix the state’s computer systems.19 Data from Indeed, a job listings search engine, showed a massive increase in search interest for “COBOL” in April.20 But there is a real risk these calls for help will go unanswered. COBOL is only the 43rd most popular programming language as of this year and the average age of a COBOL programmer is about 55-years-old.2122

Why haven’t millions of people received their economic impact payments from the IRS yet? COBOL seems to be the culprit there, too. Many Americans encountered error messages (“Payment Status Not Available”) when they tried to find out why they hadn’t received their stimulus check yet.23 The solution? Using only uppercase letters in the form (and if that didn’t solve the issue, people were advised to try abbreviating words like “Street” and “Avenue”).

But the problems are not just limited to outdated programming languages. The IRS has a profoundly outdated and inaccurate taxpayer database and its systems are unable to talk to each other. John Koskinen, the Commissioner of the IRS from 2013 to 2017, testified on multiple occasions in Congress, and made other public statements, about the dangerously outmoded condition of the agency’s IT infrastructure, even citing existing systems that date back to the Kennedy Administration.24

Other government processes are also antiquated. In New York, newly unemployed workers are required to fax in documentation.25 In some states, people can file for unemployment online, but only from a desktop or laptop computer.26 The state websites, it turns out, aren’t mobile-friendly — a significant barrier for the millions of people whose only internet access is via their smartphones.27 And some states, such as Illinois, even shut down their websites for multiple hours every day.28

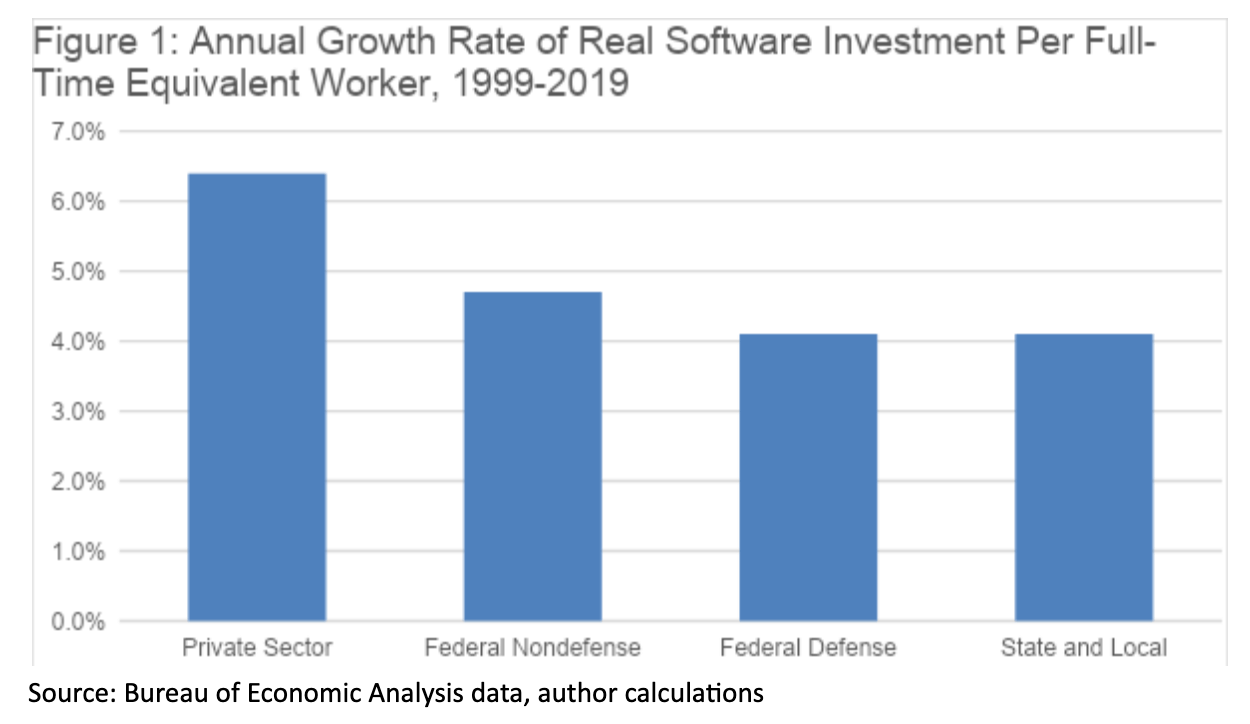

A Decades-Long Investment Shortfall

These problems with the government’s digital infrastructure didn’t arise overnight. Technical failures of this nature are the inevitable result of an accumulating investment deficit over recent decades. According to a Progressive Policy Institute analysis of Bureau of Economic Analysis data, federal and state government investment in software per worker significantly lags behind private sector investment.2930

As the pandemic recession grinds on, the federal and state governments must invest more in digitizing their operations if they are going to deliver aid faster and more accurately. U.S. officials should study the example of Estonia, which has digitized 99 percent of government services, including online voting, an e-residency platform that allows businesses across the European Union to establish and manage a business online, and a nationwide system of digitally-kept health records.31323334 Estonian officials estimate that digitizing these processes saves the country two percent of its Gross Domestic Product a year in salaries and expenses, roughly what it pays to meet its military obligations to NATO.35

The federal government has a Technology Modernization Fund, but it’s only been allocated $125 million since 2017 when it was created.3637 In its big relief bills (such as the Paycheck Protection Program and the CARES Act), Congress included funds for agencies to upgrade their technology systems. For example, the bills allocated nearly $3 billion to the Small Business Administration that could be used to upgrade and modernize its IT systems. But much of the money has gone to hire outside contractors rather than to acquire new technology. For instance, the Small Business Administration awarded RER Solutions $500 million for data analysis and loan recommendations as part of Covid-19 relief.38 Sufficient in-house technology systems would both limit the potential for breaches to occur and be a more prudent use of taxpayer money rather than continuously “renting” delivery systems.

For too long, the U.S. public sector has been a laggard in adopting the modern digital technologies that the rest of society have. That’s mainly been the result of underinvestment. To close this public-private technology gap, the federal and state governments need to invest more in software and systems improvements to ensure aid is rapidly delivered during the next crisis.

Government IT Needs Both Incremental Modernization and End-to-End Modernization

All of these issues might make it seem like the best approach is to tear everything out root-and-branch and start over. And while end-to-end modernization strategies might make sense in some cases, for the most essential government systems, an incremental strategy is actually best because it minimizes risks to essential services and limits downtime for users. As Alasdair Allan, a computer scientist at the Raspberry Pi Foundation, pointed out, legacy software systems have accumulated decades of solutions to corner cases and bug fixes. Starting from scratch would be a mistake:39

You should (almost) never rewrite from scratch, and (almost) never throw the legacy system away, it is your institutional knowledge. A legacy software system is years of undocumented corner cases, bug fixes, codified procedures, all wrapped inside software.

If you start from scratch you will miss things. There is no guarantee that you will end up in a better situation, just a different one. I have yet to speak to anyone that has been involved with a project to reimplement a large legacy code base from scratch that has anything good to say about the idea. Document, improve the build system, modernise the infrastructure around it. Write tests. But do not throw it away.

Modern programming languages can be used to deliver social services on modern devices (e.g., smartphones) while sitting on top of the existing mainframe servers. This approach would drastically improve the user experience while preserving the accumulated knowledge. But what might this look like in practice and where should the government start?

Start Small: Public-Private Partnerships and Pilot Projects

One area the federal government can look to improve incrementally in terms of delivery via information technology is anti-poverty programs. Low-income families spend inordinate amounts of time and energy running from one social service agency to the next to apply for public assistance. Now, with many offices shut down, social distancing, and intermittent mass transit, that job is harder than ever. The opportunity costs of simply applying for and receiving public support have risen dramatically. We need to use new digital tools to reduce those costs by empowering low income people to apply once online and receive benefits on an ongoing basis.

Over time, government IT systems have accrued a lot of technical debt — the cost of future work caused by choosing an easy, short-term fix.40 Solving these problems won’t be easy. But a step in the right direction would be passing the Health, Opportunity, and Personal Empowerment (HOPE) Act.41

As Joel Berg detailed in a white paper for PPI in 2016, the HOPE Act would jumpstart the modernization of social services with pilot projects and innovation contracts.42

“Currently, low-income families need to navigate a morass of bureaucracy to receive the benefits they need and deserve, including SNAP, WIC, and UI benefits. Filling out the requisite forms often requires waiting in long lines and traveling to far flung offices. For example, for residents of Panola, Alabama, the closest location to get a driver’s license is a 70-minute drive away.For more complicated processes, recipients often need to hire professionals to help them secure financial assistance from the government.

A 2016 PPI study found that low-income workers paid an average of about $400 each to national tax preparation storefront chains in low income neighborhoods.43 A better alternative would be to move all these services online and make them accessible from a single smartphone app.”

Nevertheless, the government — at both the federal and state and local levels — does not have a good track record of building large scale transactional systems. Moreover, poor customer experiences have too often resulted from government attempts to mimic the online transactional processes and consumer interfaces the public has come to expect from their daily experiences with private sector innovations. And as we’ve shown, the government has a big task ahead in fixing its current systems, in terms of financial resources, managerial resources, and tech talent resources.

However, the needs of the country also cannot wait for notoriously lengthy public procurement cycles to solve these problems. Just getting through the phases of systems design, specifications, and competitive procurement for major systems would take 5-10 years, while implementation of awarded contacts would take 5-10 years more, with high risk of obsolescence by the time of deployment. Successful government reinvention will therefore require reinvention of processes and strategies for service delivery in order to rapidly meet public expectations for performance. Innovative public-private partnerships, with appropriate public safeguards, should be a cornerstone methodology for government reinvention in the 21st century.

With all of that in mind, new online service delivery platforms could be provided via multi-sourced public-private partnerships – including those at no cost to either the public treasury or individual users — which would allow the government to harness the private sector’s technology capabilities and IT infrastructure, with a declared objective of creating an environment of continuous innovation and improvement. The government could then create supporting national public communications campaigns, down to the community level, to inform the public about the availability of these service platforms, so the working poor can know there is are free online, government-sponsored and regulated alternatives available to them.

According to Berg, the HOPE Act can help make this better alternative a reality:44

“Here’s how HOPE would work: The President and Congress would need to work together to enact a law that would authorize the federal Departments of Health and Human Services (HHS), Housing and Urban Development, (HUD), Treasury, and Agriculture (USDA) to work together – and to form public/private partnerships with banks, credit unions, and technology companies – to create HOPE accounts and action plans that combine improved technology, streamlined case management, and coordinated access to multiple federal, state, city, and nonprofit programs that already exist. States and localities would initially be asked to participate in pilot projects implementing the accounts and plans, and, if they work, would be required over time to implement them universally.”

The program would only cost $35 million in its initial stages and would go a long way to showing the potential benefits of bringing government tech into the 21st century. As Berg says, “In America, trying to get out of poverty can be a full-time job.”45 In normal times, this is a tragedy. In a pandemic, when tens of millions are at risk of becoming impoverished for the first time in their lives, this is a national emergency.

The HOPE Act can serve as the first step in a radically pragmatic approach to modernizing government IT. Senator Kirsten Gillibrand and Representative Joe Morelle have been leading the effort to include this bill in the Phase 4 relief package for the COVID crisis and low-income Americans need this change now more than ever.46

A big part of the problem is that government investment in software has not kept pace with the private sector. As Figure 1 shows, real private sector investment in software per full-time equivalent (FTE) worker increased at an annual growth rate of 6.4 percent over the last 20 years. Meanwhile real investment in software per FTE worker grew at a noticeably slower rate of 4.7 percent for federal nondefense, 4.1 percent for federal defense, and 4.1 percent for state and local governments.

If the federal nondefense sector had kept pace with the private sector, software investment in 2019 would be 38 percent, or $10.7 billion higher (Table 2). Software investment in the federal defense sector would be 55 percent higher, and state and local government software investment would be 54 percent higher.

Table 2: The 2019 Software Gap (billions)

Actual software investment

Necessary software investment*

Size of the gap

Federal Nondefense

28.3

39.0

38%

Federal Defense

12.6

19.5

55%

State and Local

20.1

31.0

54%

*assuming that real software investment per FTE had kept up with private sector

Data: BEA, PPI

But that’s not the worst of it. This gap has accumulated over time, as year after year the government has spent less than it should have. According to our estimates, the accumulated shortfall in government software investment since 1999 has totaled $316 billion. As Table 3 shows, federal nondefense, federal defense and state and local governments would have invested an additional $123.6 billion, $89.5 billion, and $102.5 billion, respectively, to match the private sector’s pace over the last 20 years. This should be viewed as a lower bound on the shortfall in government IT investment, as this figure excludes hardware investments that will also need to be made.

Table 3: Accumulated Shortfall in Software Investment, 1999-2019 (Billions)

Federal Nondefense

$123.6

Federal Defense

$89.5

State and Local

$102.5

Total

$315.6

Source: Bureau of Economic Analysis data, author calculations

*See Methodology Appendix

While the task of modernizing government technological capabilities may seem immense, it pales in comparison to the opportunity cost of not acting at all. A Technology CEO Council report highlighting opportunities for innovation in government use of technology estimated the federal government alone could save $1.1 trillion over the next decade in areas like fraud and improper payments prevention, big data and analytics, mobile, and cybersecurity.47 For example, the federal government is forecast to make $117 billion in improper payments in FY 2020 and has made over $1 trillion in improper payments since FY 2012.48 Technology CEO Council estimates “the federal government could reduce improper payments by approximately $270 billion over 10 years” by employing techniques like when IBM implemented predictive analytics for New York State, which resulted in the prevention of $1.2 billion in improper tax refunds.49

Cybersecurity is another area where modern technology can save taxpayer money. A study by the Ponemon Institute found the United States to have the highest average cost for a data breach in 2020 at $8.64 million.50 Public-private partnerships can help federal, state and local governments avoid expensive cybersecurity attacks. IT security company Akamai helped the U.S. State Department move to a secure cloud-based web presence that successfully protected the agency from one of the largest Distributed Denial of Service (DDoS) attacks on U.S. government websites to date.51

Once again, public-private-partnership is an essential part of a 21st century cyber defense strategy. A good example is the Treasury/IRS Security Summit and ISAC, which was created by IRS Commissioner Koskinen five years ago, in concert with the private sector. This Treasury/IRS initiative has thus far reduced identity theft tax refund fraud by 80.52 This innovative strategy to defend the tax system against international cyber-attacks should be studied as a model for other government agencies who hold sensitive information and billions in public assets.

Conclusion

The Covid-19 pandemic has shed a light on the obsolete systems used by federal, state and local governments to deliver relief. When time was of the essence, the federal government stumbled in delivering stimulus checks and PPP loans efficiently and accurately. State governments were ill-equipped to process the unprecedented surge in unemployment applications. To be sure, government IT issues predate the pandemic, as federal and state systems have been routinely compromised by data breaches.

The root cause of these IT problems is a decades-long shortfall in government infrastructure investment. For example, the overwhelming share of the federal government’s investment in IT is spent on operating and maintaining outdated legacy systems, some of which are more than half a century old. But the solution isn’t to maintain obsolete systems that aren’t secure and don’t serve their purpose anymore; the solution is for governments to invest in modernization and digitization. Governments should start with pilot projects and partner with the private sector where possible. The HOPE Act would represent a down payment on the $316 billion we estimate federal, state and local governments has fallen behind the private sector. Likewise, modern public-private partnership strategies would enable government to leverage private sector investments and infrastructure to apply them to public purpose.

Methodology Appendix

Data from the Bureau of Economic Analysis enables us to calculate real software investment per full-time equivalent worker for the private sector, the federal nondefense sector, the federal defense sector, and the state and local sector. As shown in Figure 1, the growth rate was substantially faster in the private sector compared to the three government sectors.

We then calculated how much higher software investment in the three government sectors would have needed to be in each year since 1999 to match the growth rate of real software investment per FTE in the private sector. We then translated this increase into nominal dollars and summed over the twenty-year period to get the total shortfall. The 2019 figure gives the current gap reported in Table 2.

This estimate should be regarded as a rough measure of the amount of “software debt” that the government has built up. Ordinarily we might not worry about a lack of spending 10 or 15 years ago because of depreciation, but the government has spent far too much money holding legacy database systems together with scotch tape.

The other issue is hardware. The data published by the BEA for government spending on computers includes “consumption expenditures” as well as investment, so it doesn’t quite correspond with private sector investment in computers. It is generally agreed, however, that even in the era of cloud computing that the government needs to modernize its hardware.

Social distancing is essential to limit the spread of the novel coronavirus, but it also reduces opportunities for millions of Americans to earn a wage or buy goods and services from others. As a result, state and local income and sales taxes that fund education, public safety, and other essential services are drying up. Meanwhile, the rising unemployment rate is causing states to spend more on safety-net programs, such as unemployment insurance and Medicaid. Because most state and local governments are required to balance their budget, this fiscal squeeze is compelling them to cut their budgets right when people and businesses need government support the most.

PPI’s Center for Funding America’s Future has developed a tool to help estimate the additional aid state and local governments will need from the federal government over the next two years to compensate for lost economic activity. Users can input an unemployment rate in each quarter through 2021 (the default values for which are based on the Federal Reserve’s September 17th projections) and set the percent of emergency reserves they are comfortable asking states to draw down.

The results show how much money, beyond what Congress has already appropriated, states will need to fund their aid spending and make up for lost revenues without cutting their budgets or raising taxes. The figures only show the change in revenues or spending from what they were before the crisis, without accounting for the lost economic growth that was previously projected to occur in the coming years before the pandemic hit.

PPI currently estimates that state and local governments will need at least $250 billion in additional federal support between now and the end of 2021.

This estimate is based on the latest labor market data and experiences during past recessions, but it is important to note that the unique nature of the current crisis, as well as changes to state fiscal policy or the economy at-large since those recessions, has already meaningfully altered the expected impact on state and local government finances. In fact, our current baseline estimate is significantly smaller than the $500+ billion estimate produced by our calculator when it was first published in May. The biggest reason for the change is that better-than-expected economic news: the current unemployment rate, as well as the projected unemployment rates for future quarters, are below what they were projected to be four months ago.

Given the demonstrated unpredictability of the current economic crisis, PPI’s estimates should be considered a guideline rather than a concrete policy prescription. We strongly encourage congressional lawmakers to design programs that provide aid to state and local governments based on real economic indicators, rather than appropriating a precise amount of money that could easily be significantly larger or significantly smaller than what is needed.

We have also made some important methodological changes to our calculator. We no longer give users the option of including shortfalls in state unemployment insurance systems that are currently set to be recouped under current law from higher taxes that automatically apply to employers who lay off workers, as the unprecedented nature of this crisis has made it difficult to produce credible predictions based on the experiences of past recessions. Additionally, the calculator now includes the cost of supporting K-12 schools, which joins several other new spending needs beyond covering existing shortfalls, such as election security and creating a national state-led testing program (but still does not account for other costs directly related to addressing the pandemic, such as increased spending through public health insurance programs).

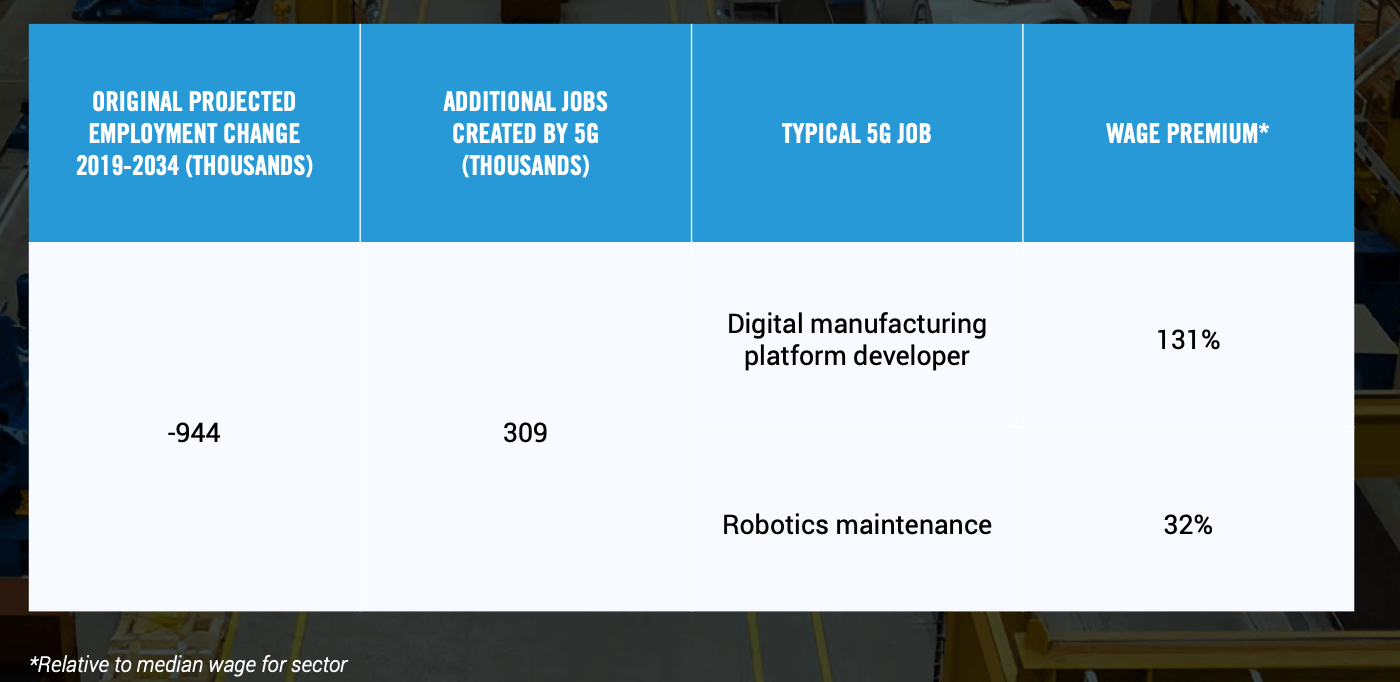

In a new paper, the Progressive Policy Institute, working with the National Spectrum Consortium, projects that applications of 5G will create 309,000 manufacturing jobs in the United States over the next 15 years. That’s only a small part of the 4.6 million jobs that 5G is expected to create over that period, according to the paper, “The Third Wave: How 5G Will Drive Job Growth Over the Next Fifteen Years,” which I co-authored with Elliott Long.

The application of 5G to manufacturing is especially important because the new communications technology has the potential to jumpstart a lagging sector. Yes, it feels funny to call manufacturing a lagging sector, but that’s the only way to describe it. Even before the pandemic, labor productivity decreased in 18 of the 21 NAICS 3-digit manufacturing industries in 2019, according to a recent report from the Bureau of Labor Statistics. Output grew at a crawl.

The benefit of 5G is that it allows a much faster digitization of the physical transformation processes that lie at the heart of manufacturing. A 2019 McKinsey analysis observed that “[f]or decades, factory automation has relied on programmable logic controllers (PLCs) that were physically installed on (or very near) the machines they controlled, and then hard-wired into computer networks to ensure precise, reliable control under extreme conditions. If 5G consistently meets its performance promises, the PLC could be virtualized in the cloud, enabling machines to be controlled wirelessly in real time at a fraction of the current cost.” Not only will costs be lower, but flexibility will be improved.

The Progressive Policy Institute hosted a conversation on how members of the Democratic Party can better protect recent gains made by Black and Brown students while advancing these gains after the 2020 Presidential Election. The conversation surrounded gains made by Black and Brown students, how these gains were made, and more importantly how Democrats can ensure the gains continue under the next Administration.

Speakers:

– U.S. Senator Michael Bennet, (D) Colorado

– David Osborne, Progressive Policy Institute

– Honorable Antonio Villaraigosa, Former Mayor, City of Los Angeles

– Keri Rodrigues, National Parents Union

– Dr. Howard Fuller, Freedom Coalition for Charter Schools

Moderator: Curtis Valentine, Deputy Director of Reinventing America’s Schools Project.

Watch on YouTube here. On the go? Listen to the conversation where you find your podcasts:

5G, because of its low latency and high throughput, won’t just be an evolution in technology, but a revolution. It will open the door to incredible innovation in both the private sector and the government – including augmented and virtual reality, precision agriculture, smart ports, transportation and logistics, autonomous vehicles, connected construction and so much more.

In the United States, it is critically important to understand how this fundamental shift in technology will impact the broader economy, especially at a moment when COVID-19 has caused significant economic disruption and massive job losses nearing Great Depression levels. Key questions include:

How many jobs will be created by the 5G Economy? Will they be focused around traditional technology centers like San Francisco, New York, and Boston, or create new opportunities across the nation? What kinds of jobs will be created?

And for policymakers, what does the U.S. need to do to support efficient allocation of radio spectrum to support this technology development? And should we provide job training to ensure that workers in America can meet the opportunity?

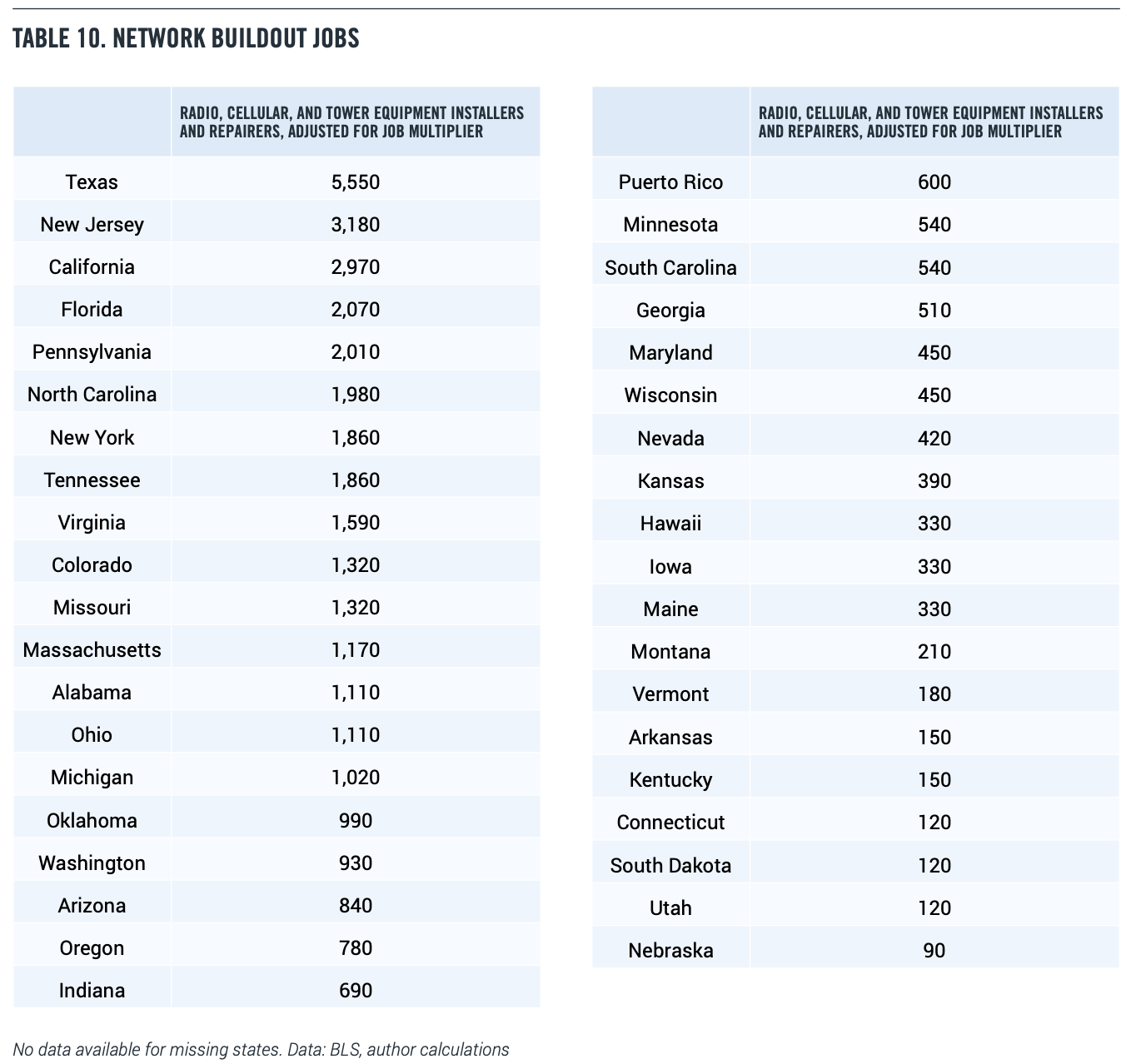

Already the 5G job revolution has begun. Large mobile providers such as AT&T and Verizon are building out new networks across the country. Network companies such as Cisco, CommScope, Mavenir, and L3Harris are hiring 5G system architects, Radio Access Network (RAN) engineers, 5G solution architects, and technical managers in the 5G space.

Technicians and tower climbers are putting up 5G small cells at a rapid pace. This is not the first time that fundamental shifts in networking technologies have created sudden shifts in the economy and job opportunities.

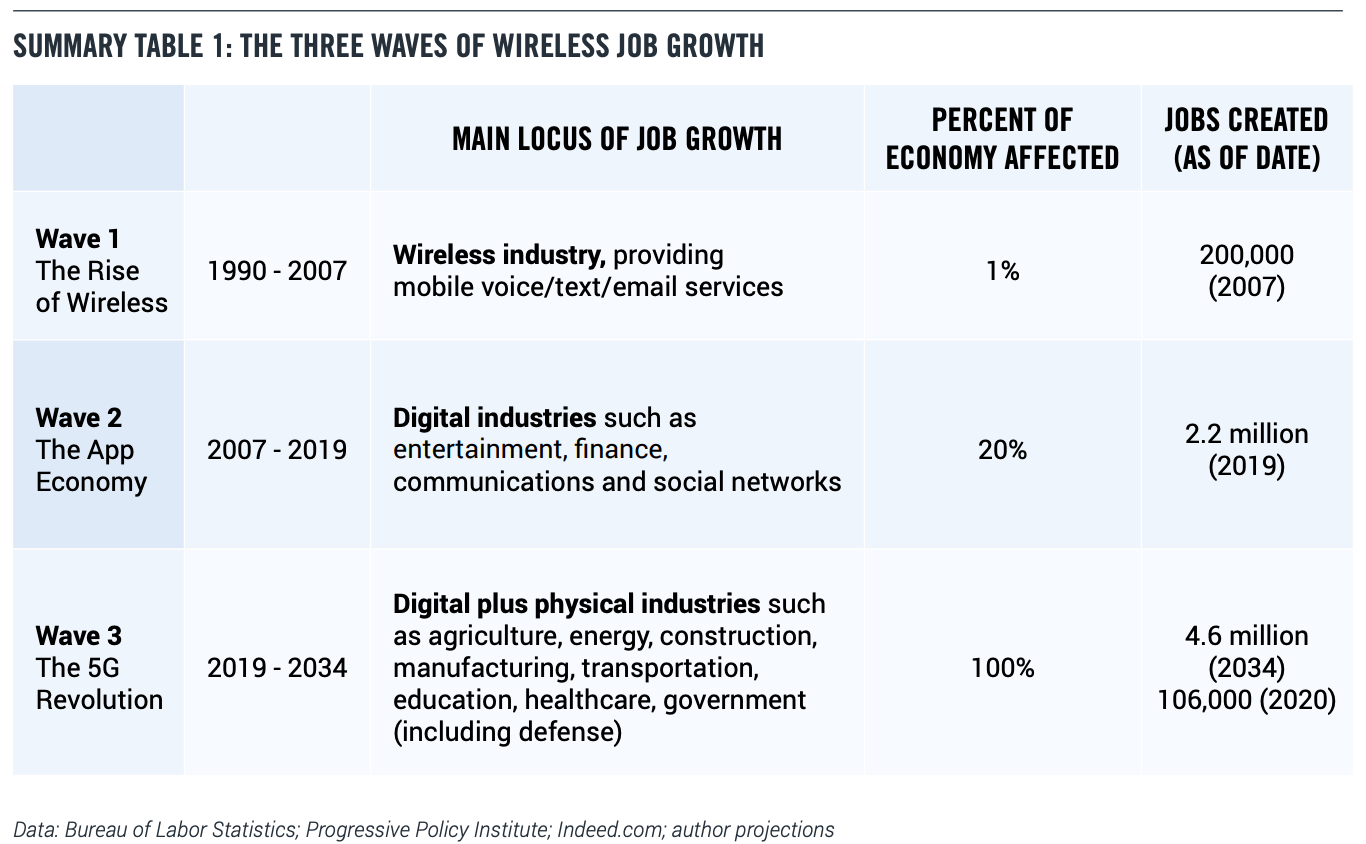

This paper identifies and outlines three waves of wireless-driven job growth (Summary Table 1) in the U.S., and answers major questions about how many jobs will be created, which industries will be affected, where they will be located, and what we can do as a nation to accelerate efforts to meet this challenge.

Wave 1, The Rise of Wireless, covers the period from 1990-2007, as mobile carriers were building out the original wireless networks and cell phones went from a rarity to a necessity. Wave 1 generated roughly 200,000 jobs in the wireless industry.

Wave 2, “The App Economy,” covers the period from 2007 to 2019, which was rooted in the application of wireless to mobile apps via smartphones, rather than in the wireless industry.

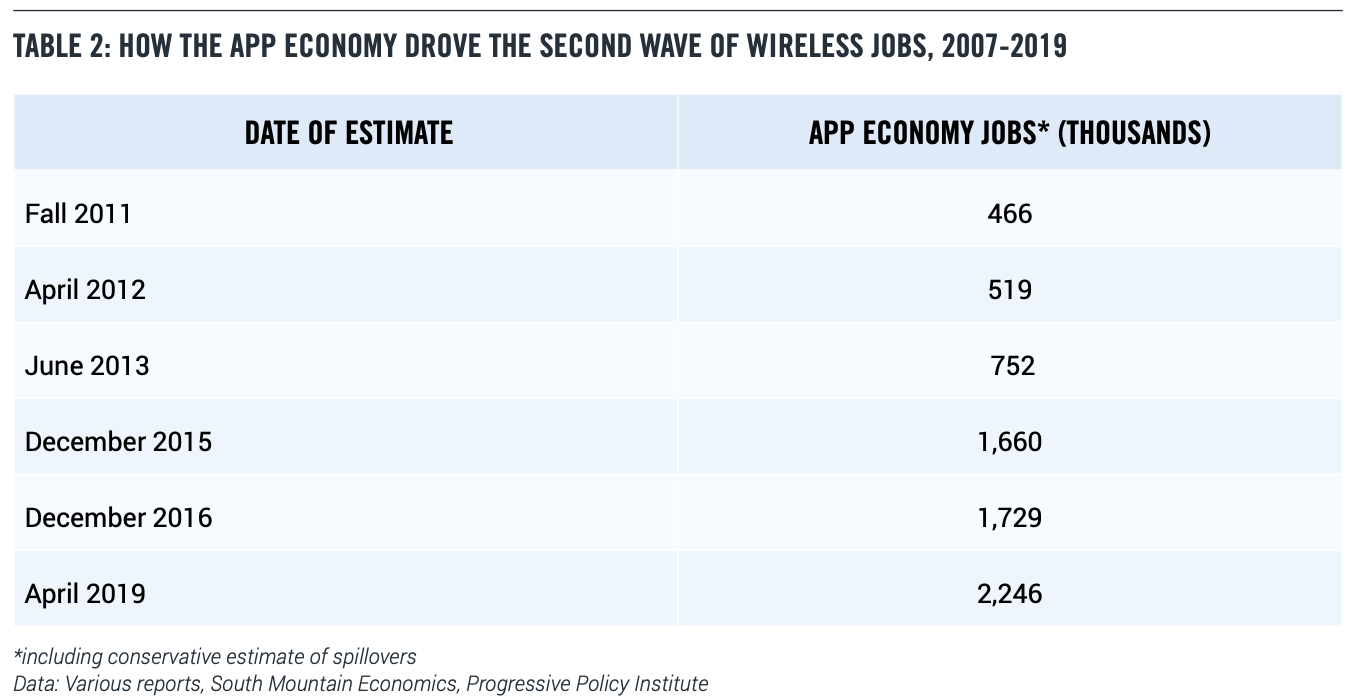

Conventional BLS statistics contained no categories for app developers. But a widely cited study by this report’s author, released in early 2012, analyzed detailed data on job postings and estimated that the U.S. App Economy included 466,000 jobs, including workers developing and maintaining mobile apps and the workers supporting them. (1) Follow-up studies showed continued growth in the U.S. App Economy, with the latest figures from September 2019 reporting more than 2.2 million App Economy jobs. (2) This reflects an average growth rate of more than 20 percent annually. The main locus of Wave 2 job growth has been in industries such as entertainment, finance, communications and social networks, whose output can be easily delivered in a digital form (hence “digital industries”).

Wave 3, “The 5G Revolution,” began in 2019 as mobile carriers expanded their initial 5G networks. Wave 3 is generated by the applications of wireless to challenges in physical industries, such as agriculture, energy, construction, manufacturing, transportation, education, healthcare, and government including defense.

In recent years, most of these physical industries have experienced low or negative productivity growth, as well as low spending on telecommunications services.

5G is reversing both of these trends. Faster, more versatile wireless communications are an essential factor in driving productivity gains and creating jobs. Research shows that industries like manufacturing, construction, and healthcare have lagged in digitization, helping explain why productivity growth has been so slow. To increase productivity, physical industries need the ability to gather information from widely dispersed sensors and to use that data to control activities in real time. That’s not possible without faster and more versatile wireless commnications supplied by 5G. And the COVID-19 pandemic is accelerating the shift to many of these use cases.

How many jobs in the US will The 5G Revolution generate?

Unlike Wave 2, which mostly generated “cognitive” tech jobs which required a college education, Wave 3 is rooted in the physical world.

As a result, Wave 3 will also create mixed ‘cognitive-physical” skilled jobs, many of which fall into the category of installers and maintainers. So while App Economy jobs were focused on software development, Wave 3 jobs will drive job growth in dozens of sectors, across the economy in what we would traditionally consider both white collar and blue collar positions. Simply put, the third wave will benefit a wider set of Americans and regions than the second wave did.

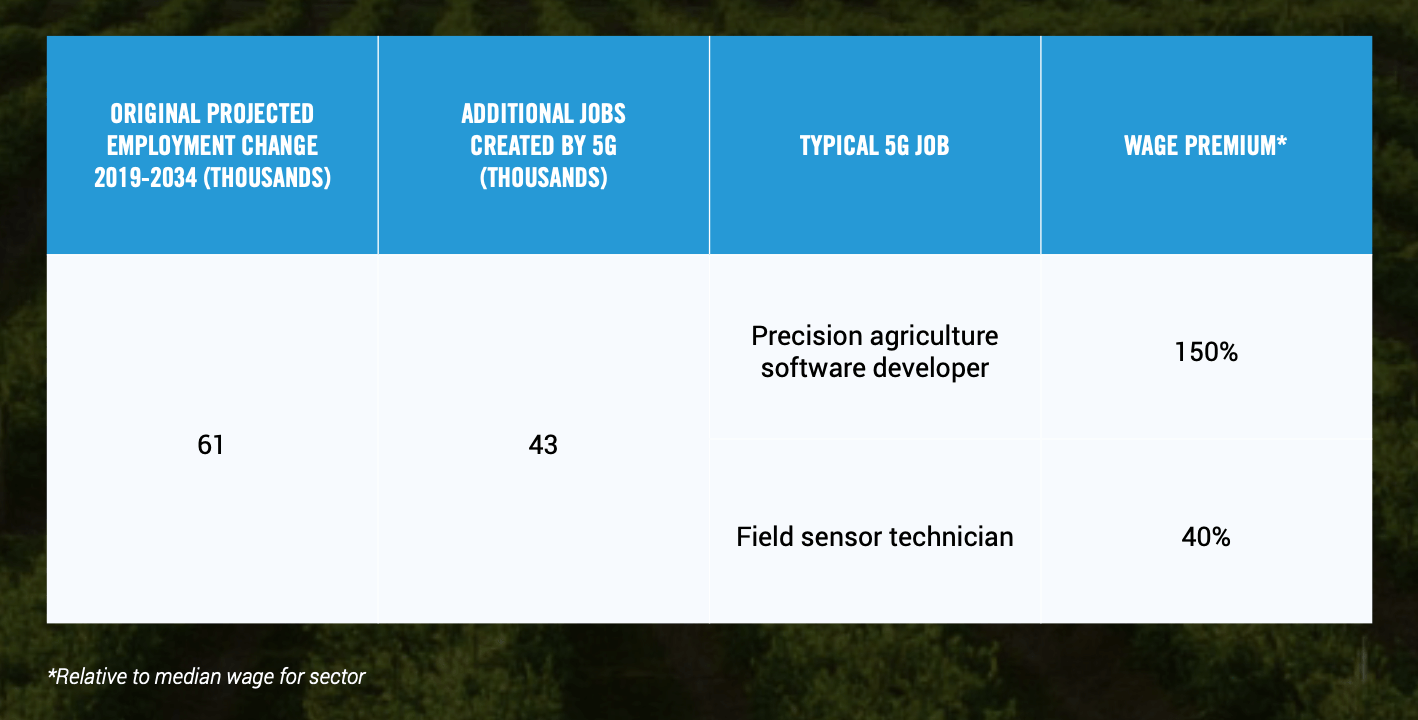

For example, healthcare providers already monitor medical equipment like pacemakers remotely. But with 5G, the set of possible athome diagnostics or even interventions will expand greatly, and telehealth installers and maintainers will be a highly valued occupation. Similarly, precision agriculture will require “field sensor technicians,” autonomous vehicles will need a cadre of mechanics, and ecommerce will need people skilled in robotics maintenance.

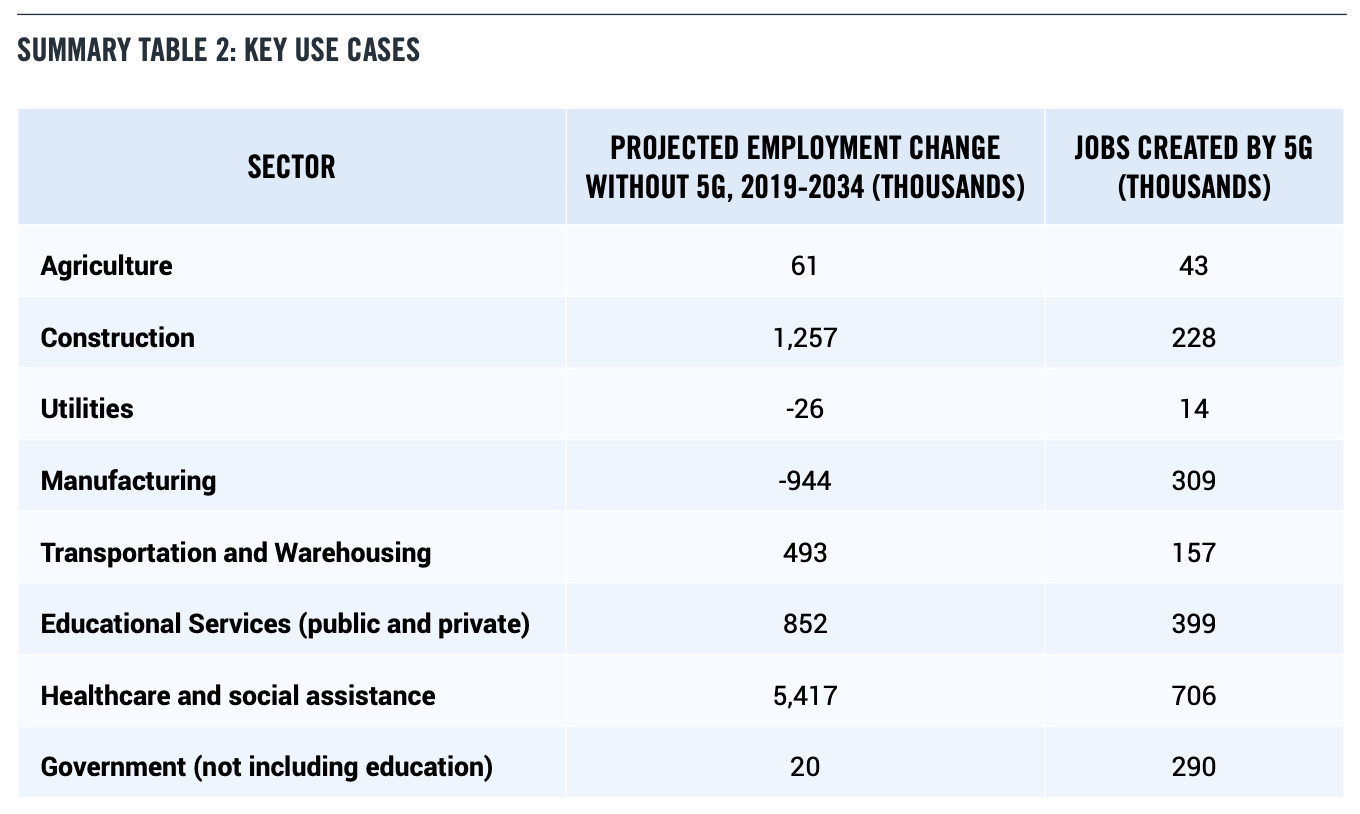

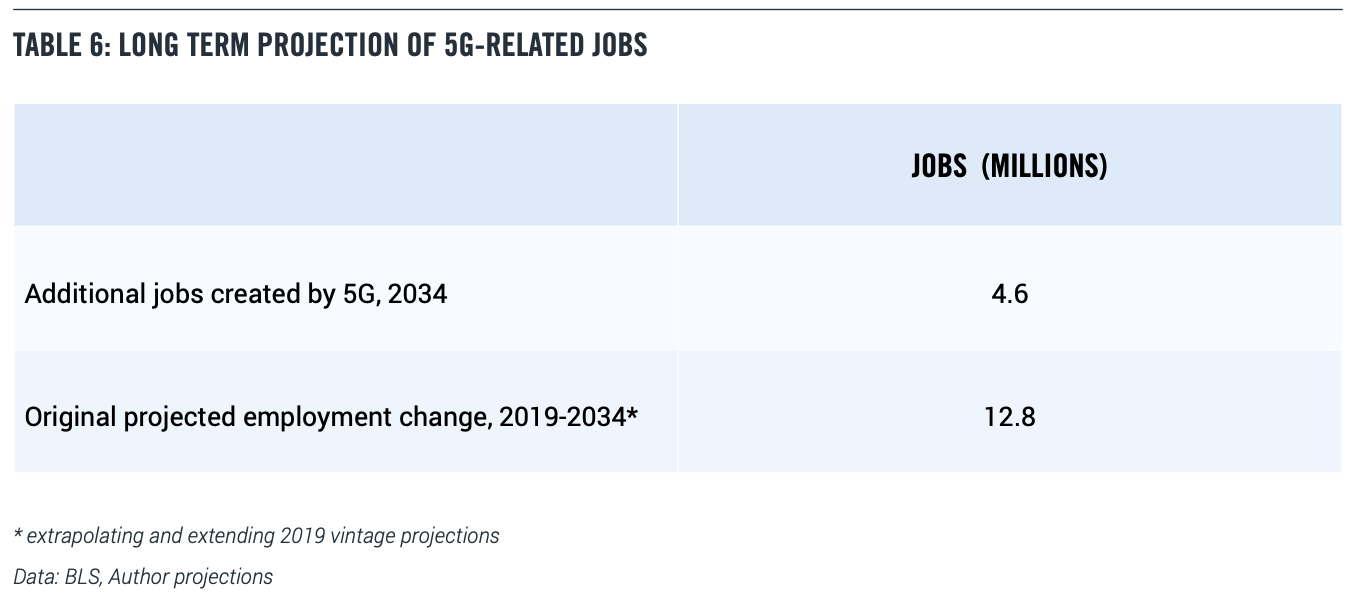

Using the latest BLS projections as a baseline jumping off point, we estimate that 5G and related technologies will create 4.6 million jobs relative to the baseline in 2034, 15 years after the introduction of 5G in 2019 (which is also, not coincidentally, the peak of the most recent business cycle). These are higher paying jobs that will replace jobs that are lost in a wide range of industries and use cases (Summary Table 2).

In an important sense, 5G job creation is a countervailing force to job destruction from automation and globalization, and critically important in the post-COVID world.

During these tough economic times, we also need to be concerned about the short-term job impact and opportunities that 5G is creating as well. This paper also shows that current 5G build-out and engineering activities are creating 106,000 jobs as of April/May 2020. We estimate the location of these jobs by state. To get this estimate, we use a combination of data from real-time job postings and BLS figures.

What Do Policymakers Need to Do?

Finally, this paper identifies four areas where policymakers should focus to harness the full potential of 5G.

First, more spectrum – mmWave, sub-6, and unlicensed – will be needed for broadband and related applications. The U.S. would benefit greatly from a long-range spectrum plan. While the Trump Administration has directed the Department of Commerce to create a National Spectrum Strategy, it has not yet been released.

A long-range spectrum plan would ensure the resource is allocated wisely, provide certainty to 5G stakeholders, and encourage long-term investment in networks for 5G and beyond.

In addition to spectrum, the U.S. also needs a plan for the adoption of 5G across the government, both defense and civilian. The public sector should be a leader, not a follower.

Third, Congress should be willing to invest heavily in the development of 5G and successor technologies. That’s essential if the U.S. is to keep up with global competition.

And finally, the U.S. should make a significant investment in job training. The U.S. needs to double down on traditional STEM fields and encourage more people in America to go into engineering and math. Beyond that, we need a national skills initiative and mentoring programs to ensure that this new generation of workers will have the training needed to support the cognitive-physical jobs that the 5G Revolution is already beginning to create.

I. THE FIRST TWO WAVES OF WIRELESS JOB CREATION

Wireless technologies are generally divided into generations, each one corresponding to higher speed and increased capabilities. 5G is the current technology being rolled out, with 6G on the horizon, promising even faster speeds and satellite-terrestrial integration.

However, for the purposes of this paper we use a different taxonomy, based on the labor market impact of wireless technologies.

Wave 1: The Rise of Wireless

Commercial mobile radio telephony—what is sometimes called “0G”—was available as a niche service since the late 1940s. (3) It had very little economic impact. The first true commercial portable cellphone, the Motorola DynaTAC 8000X, was introduced in 1983, but there were only 5 million cellphone subscribers as of 1990.

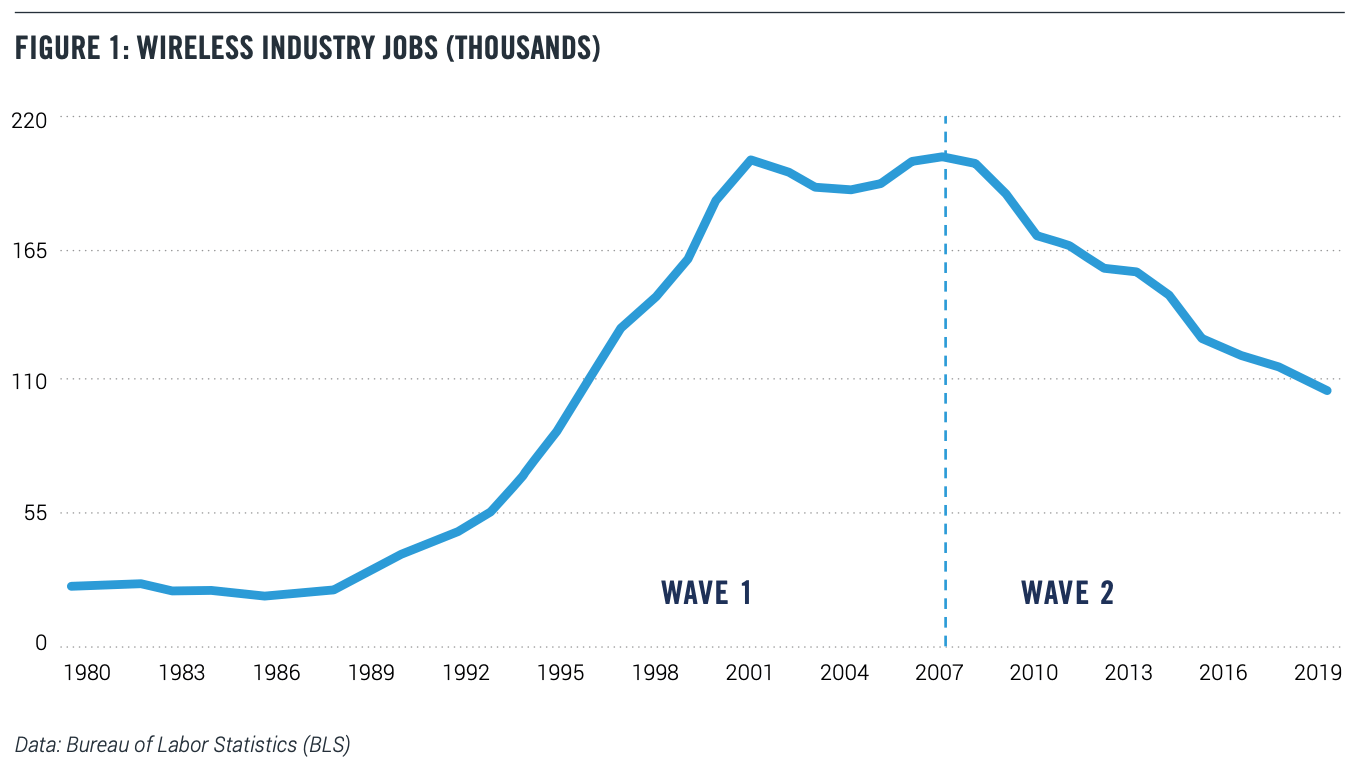

But the use of cellular wireless technology rapidly gathered speed after 1990, giving rise to 109 million subscribers as of 2000 and 233 million subscribers as of 2006. Not surprisingly, the need to build out networks, and handle a soaring customer base generated a large number of jobs. The number of people working in the wireless industry went from 36,000 in 1990 to 200,000 in 2000. (4) Wireless employment remained at roughly that level until 2007 (Fig 1).

The first wave of wireless job growth encompasses 2G in the 1990s and 3G and 3G+ in the first half of the 2000s. With 2G data speeds measured in the kilobits, only low-bandwidth applications such as voice, text messages, and email were viable. Running other applications on top of a slow network was almost impossible.

Mobile internet became possible with 3G and 3G+, but it was still not fast enough to make a significant difference.

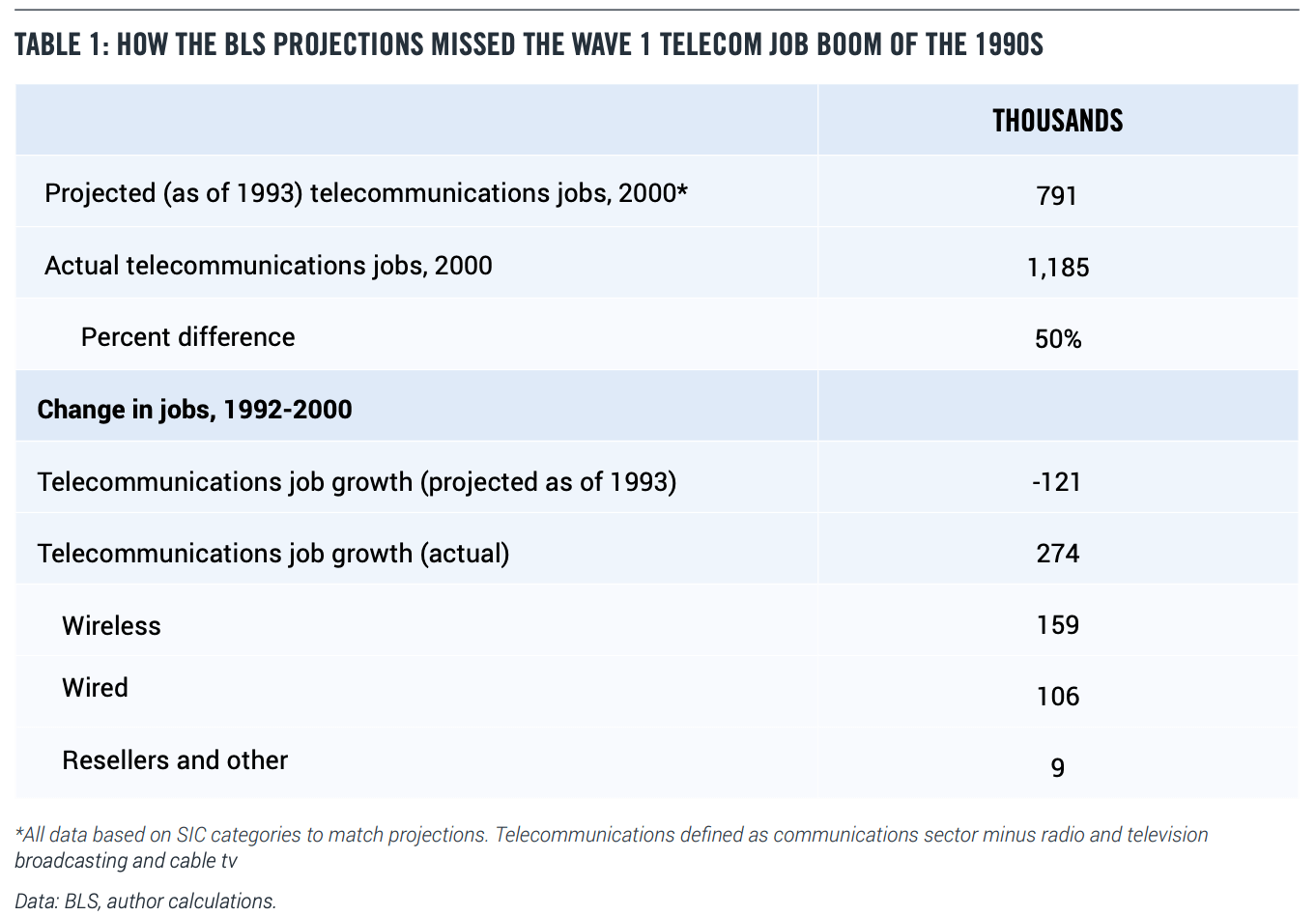

Wave 1, The Rise of Wireless, was not anticipated in any of the long-run employment projections issued by the BLS in the late 1980s and early 1990s. That’s important, because the BLS projections, issued regularly since the 1960s, are the most widely quoted comprehensive long-run occupational and industry forecasts available. The BLS also maintains the most detailed occupation industry matrix available for the United States.

Yet, the BLS projection methodology typically misses the impact of new technologies. For example, the employment projections issued in 1993 anticipated that telecommunications employment would drop from 912,000 in 1992 to 791,000 in 2000. (5) In reality, telecommunications jobs rose to 1,185,000 in 2000, 50 percent above the projected value (Table 1). (6)

Wave 2: The App Economy

The second wave of wireless jobs, The App Economy, began in 2007 with Apple’s introduction of the iPhone, coupled tightly with the opening of the App Store and Android Market (later renamed Google Play) in 2008. Suddenly mobile phone users had a powerful computer in their pockets that could handle a myriad of applications. The demand for mobile broadband soared. Mobile wireless networks moved from faster versions of 3G to 4G and LTE, as the number of broadband subscriptions soared.

But the second wave of wireless jobs also started with a paradox. Despite the central role of mobile, employment in the wireless industry peaked in 2007 and fell by half by 2019. In 2011, the Wall Street Journal ran a piece with the stark title: “Wireless Jobs Vanish.” (7)

In fact, wireless was creating jobs, but not in the wireless industry. (8) More and more IT professionals were involved in either developing mobile apps, maintaining them after they were on the market, or supporting them with users. For banks and other financial institutions, mobile apps became an important way of supplying their services without having expensive real estate or branch workers. Moreover, mobile apps could use the camera on smartphones to provide services like depositing checks at homes.

Beyond utilitarian tasks like banking, shopping, and travel reservations, apps became the major way that people interacted with their smartphones. We watched videos, listened to music or podcasts, messaged friends, played games, and spent time on social networks. One survey found that adult Americans spent almost three hours per day on their smartphones, and 90 percent of that time was spent on apps. (9)

Conventional BLS statistics contained no categories for app developers. But a widely cited study by this report’s author, released in early 2012, analyzed detailed data on job postings and estimated that the U.S. App Economy included 466,000 jobs, including workers developing and maintaining mobile apps and the workers supporting them. (10) Follow-up studies confirmed continued growth in the U.S. App Economy, with the figures from April 2019 reporting more than 2.2 million App Economy jobs. (11) This reflects an average growth rate of more than 20 percent annually (Table 2).

Other studies have found similar or even higher estimates. For example, a 2018 study from Deloitte estimated 5.7 million App Economy jobs in the U.S., using a different methodology and a much bigger assumption of spillover effects. (12)

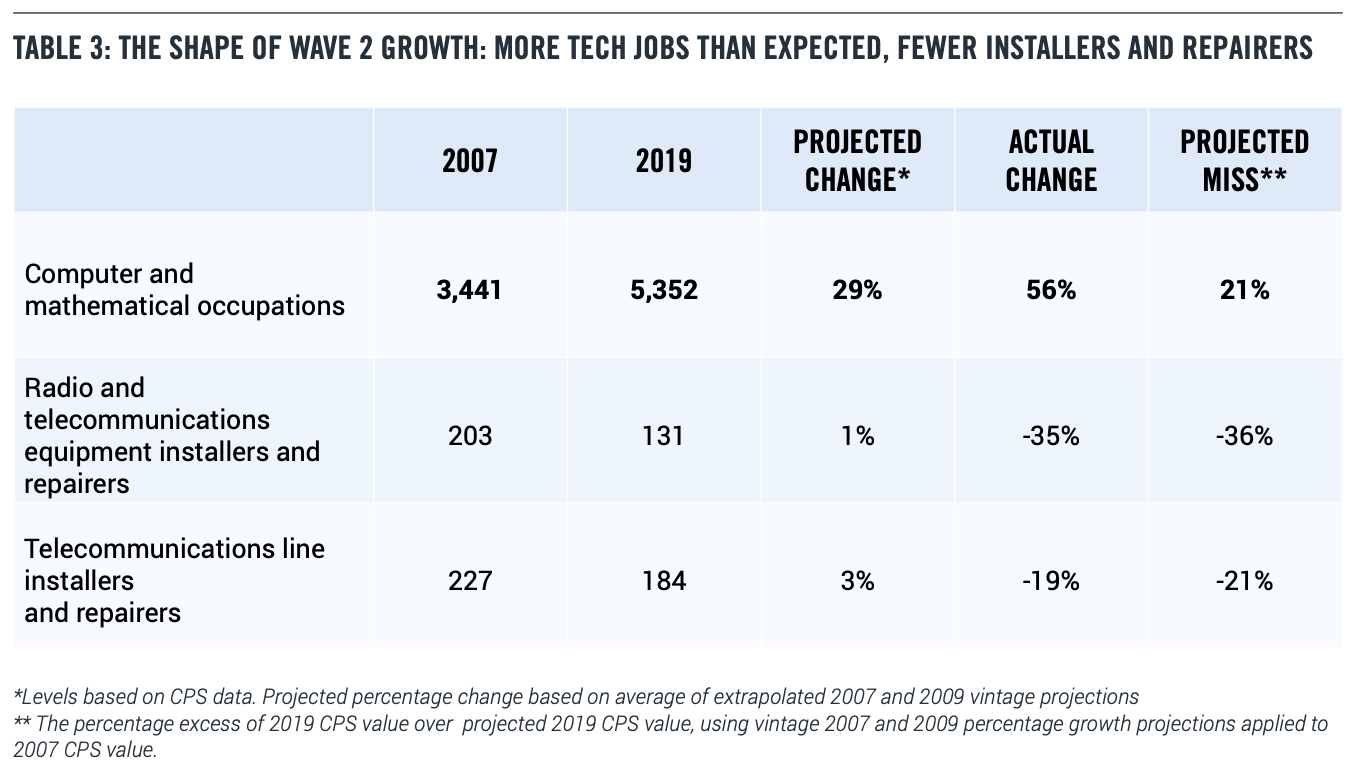

The job impact of mobile broadband and the App Economy did show up in the official numbers in a different way: the unexpectedly rapid growth of people working in “computer and mathematical occupations.” “Computer and mathematical occupations” is a broad category that includes data scientists, software developers and engineers, information security specialists, computer support specialists, and database and network administrators.

By contrast, skilled workers who maintain the telecom networks—the people who lay and fix the fiber-optic lines and put up the cellphone towers—are in the “installation, maintenance, and repair” occupations.

The BLS projections in 2007 and 2009 underestimated the expected size of the computer and mathematical workforce in 2019 by roughly 20 percent, or over 1 million workers. But the relevant categories of skilled installers and maintainers were overestimated in the projections. This tilt towards tech jobs is very important for understanding the third wave (Table 3).

II. WAVE 3: THE 5G REVOLUTION

Wave 3 of wireless-driven job growth, The 5G Revolution, began in 2019 as mobile carriers expanded their initial 5G networks, and then continued into 2020. All major carriers in the U.S. — AT&T, Verizon, and T-Mobile — are heading towards nationwide 5G networks by the end of 2020, according to analysts. (13) The pandemic has made the case for 5G more compelling as many of the use cases for 5G services have been pulled into the present.

Telehealth has become not just optional but a requirement in many medical situations.

Students from kindergarten to graduate school have been forcibly introduced to distance learning. Businesses and governments have been learning how to use virtual meetings, at a much lower cost than flying around the world. Companies have started using robots to help disinfect their stores. (14)

The U.S. military faces its own challenges, as the virus has forced changes in routines to minimize infectiousness and to protect its suppliers. “We believe the COVID-19 pandemic has accelerated society’s transition to broadband and digitization by at least a decade,” said one market analyst in March 2020. (15)

Indeed, in the early days of the pandemic, Verizon announced that it was expecting to allocate $17.5- $18.5 billion on capital expenses in 2020, up from its previous guidance of $17-$18 billion. “This effort will accelerate Verizon’s transition to 5G and help support the economy during this period of disruption,” Verizon said in a press release. So far, the pandemic has caused spectrum auctions in Europe to be pushed back. (16) Meanwhile the FCC has not changed its spectrum auction plans for 2020. (17)

Spending on 5G networks is what is known by economists as “autonomous investment”—that is, investment that is not linked to the immediate ups and downs of GDP. (18)

The Extension of Wireless to Physical Industries

Wave 2 was focused on “digital industries,” where the output can be reduced to bits and bytes. This includes games, music, communications, social networks, news, advertising, financial services, and ecommerce purchases of digital goods such as hotel and plane reservations. These digital industries, while important, make up less than 20 percent of the economy. (19) (Formally defined, the digital sector includes computer and electronics manufacturing; ecommerce; software and other publishing; video and audio content; broadcasting; telecommunications; data processing; internet publishing and search; and computer systems design and programming. Slight changes to the boundary of the digital sector does not affect the analysis here).

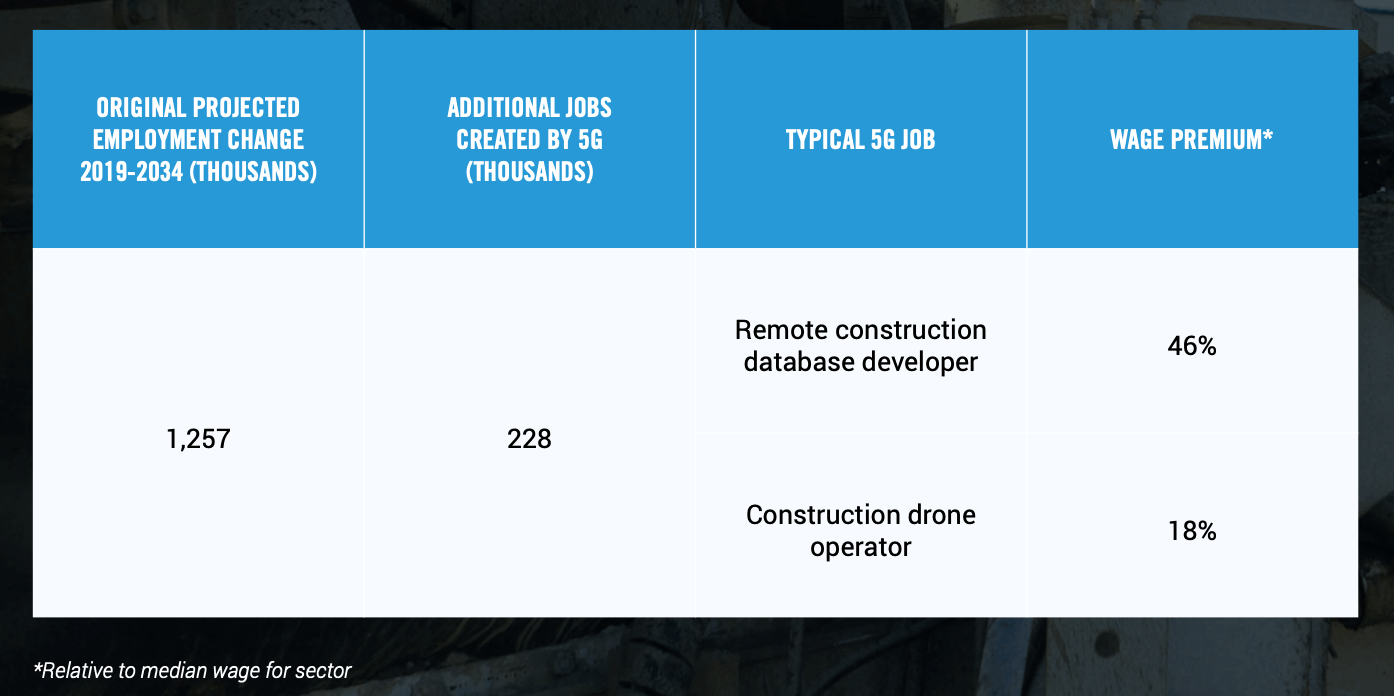

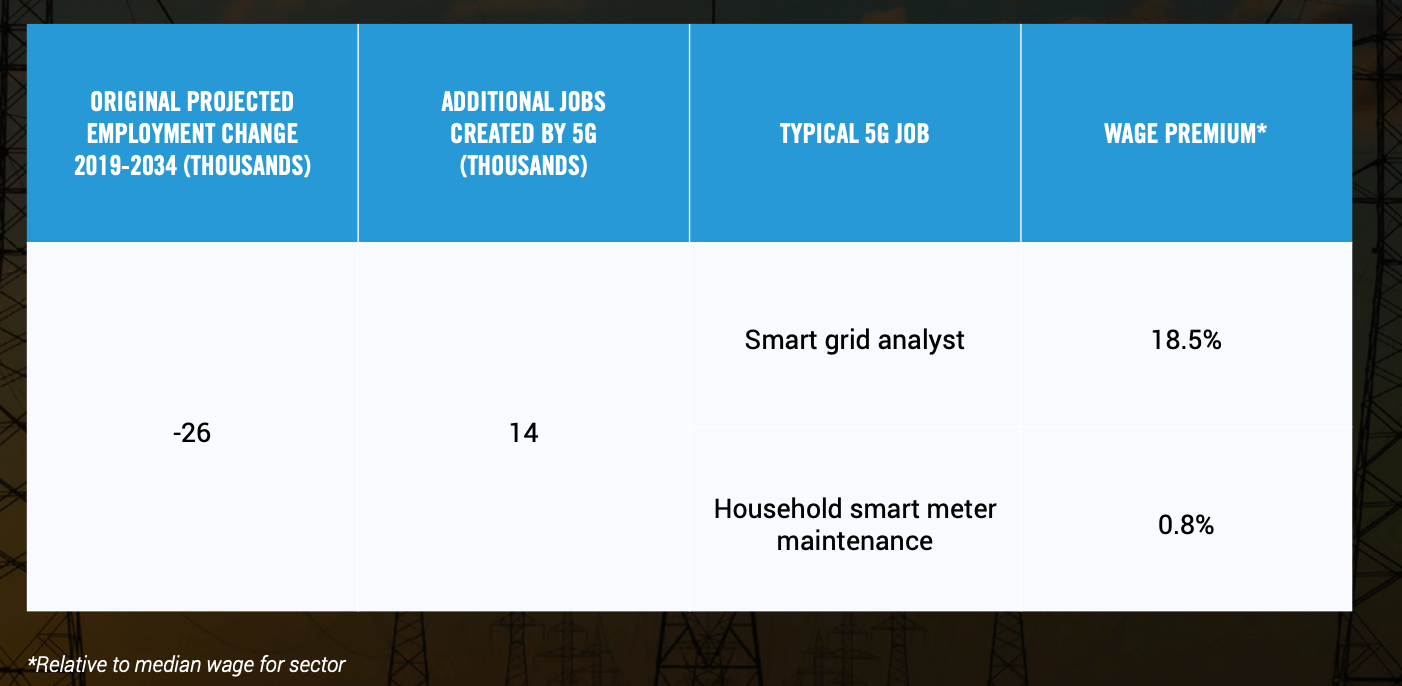

Wave 3, by contrast, is based on the applications of wireless to the challenges and opportunities in physical industries, such as agriculture, energy, construction, manufacturing, transportation, education, healthcare, and government (including defense).

Physical industry use cases include low-power wireless sensors that must operate for long periods in a field, say, without a battery replacement, or a low-latency connection to a drone or autonomous vehicle.

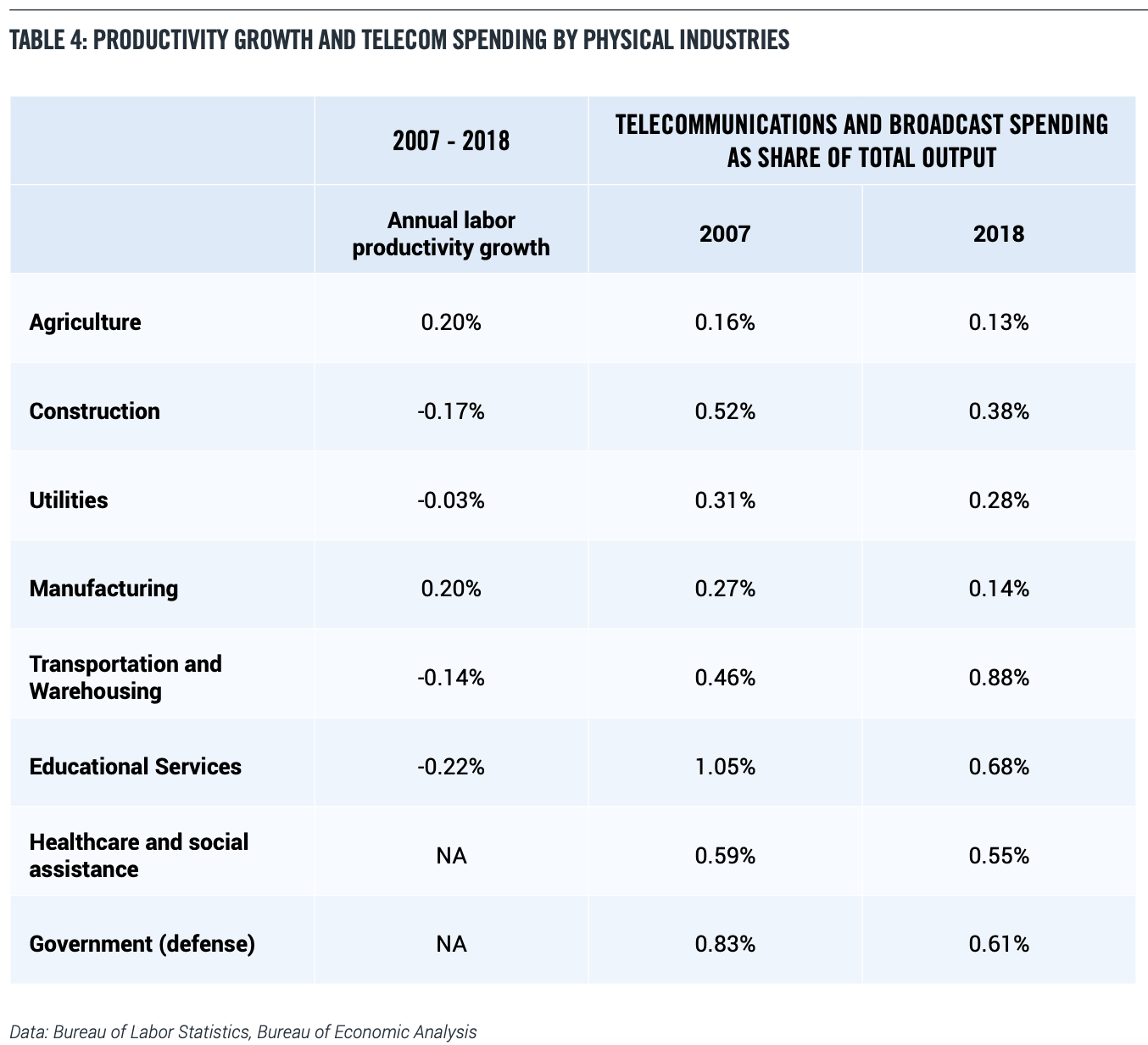

Table 4 shows the key physical sectors had slow or negative productivity growth during the second wave (in general 1 percent annual productivity growth is adequate and 2 percent is good, so none of these industries made the grade). Slow or negative productivity growth means less competitive industries, weaker wage gains, and lesser quality jobs.

Surprisingly, most of these industries had low and falling spending on telecommunications services, as a share of total output (for most industries, total output can be interpreted as revenues. For defense, total output can be interpreted as spending including accounting for depreciation). (20) For example, in agriculture, the amount spent on telecom services went from a very low 0.16 percent in 2007 to an even lower 0.13 percent. (To provide some context, in 2018 the average telecom share for digital industries was 3.5 percent, and the average telecom share for physical industries was 0.7 percent).

5G is likely to reverse both of these trends. Faster, more versatile wireless communications are an essential factor in driving productivity gains. Research shows that industries like manufacturing, construction, and healthcare have lagged in digitization, helping explain why productivity growth has been so slow. To increase productivity, physical industries need the ability to gather information from widely dispersed sensors and to use that data to control activities in real-time. That’s not possible without faster and more versatile wireless communications supplied by 5G.

The ability to rapidly communicate data and information using 5G will increase productivity gains in both the public and private sectors. And these productivity gains, in turn, will lead to higher revenue, faster wage gains, advances in job quality, and increased international competitiveness.

In 2017, a study from the Technology CEO Council examined the impact 5G will have on productivity growth in the “physical industries” and tax revenues over the next 15 years.21 The report estimated that the physical industries will boost annual economic growth by 0.7 percentage points over the next 15 years, generating an additional $2.7 trillion in annual economic output, $8.6 trillion in wage and salary payments, and $3.9 trillion in federal tax revenue.

The 5G Revolution and Job Growth

The impact of 5G on jobs can be summarized as “network meets the cloud.” That means we can push more capabilities out to the edge, including real-time and near-real-time applications of machine learning and artificial intelligence to the physical world. In many cases, new technologies create new tasks and markets that didn’t exist before. (22) For example, healthcare providers already monitor medical equipment like pacemakers remotely. But with 5G, the set of possible at-home diagnostics or interventions will expand greatly, and telehealth installers and maintainers will be a highly valued occupation.

5G will greatly expand the capabilities of drones in a range of applications from agriculture to military to logistics, especially in conjunction with artificial intelligence. That will expand the market for skilled drone operators, sometimes called “remote-pilots-in-command,” earning as much as $100,000 per year.

The other alternative is that productivity gains will lower costs enough to expand the market, which ends up creating new jobs. (23) That’s what happened in ecommerce. The use of robots in ecommerce fulfillment centers, combined with effective use of data, helped drive down costs low enough to offer consumers fast delivery and easy returns. And the combination of fast delivery and easy returns, in turn, made the ecommerce proposition irresistible to many consumers, because now they could avoid the time and trouble of going to the store, getting the product quickly and simply returning it for free if it didn’t work. The result was a massive shift from unpaid household shopping hours to paid ecommerce fulfillment and delivery hours. (24)

Or consider manufacturing. The pandemic has called into question the wisdom of depending on global supply chains for important medical supplies, and by extension, any parts that one might need in a crisis.

The low-latency high-bandwidth services delivered by 5G can help spur the digitization of the factory floor, boosting productivity and increasing flexibility. (25, 26) The result could be a shift to distributed local manufacturing in the U.S. in the post-COVID era, creating jobs and shortening supply chains.

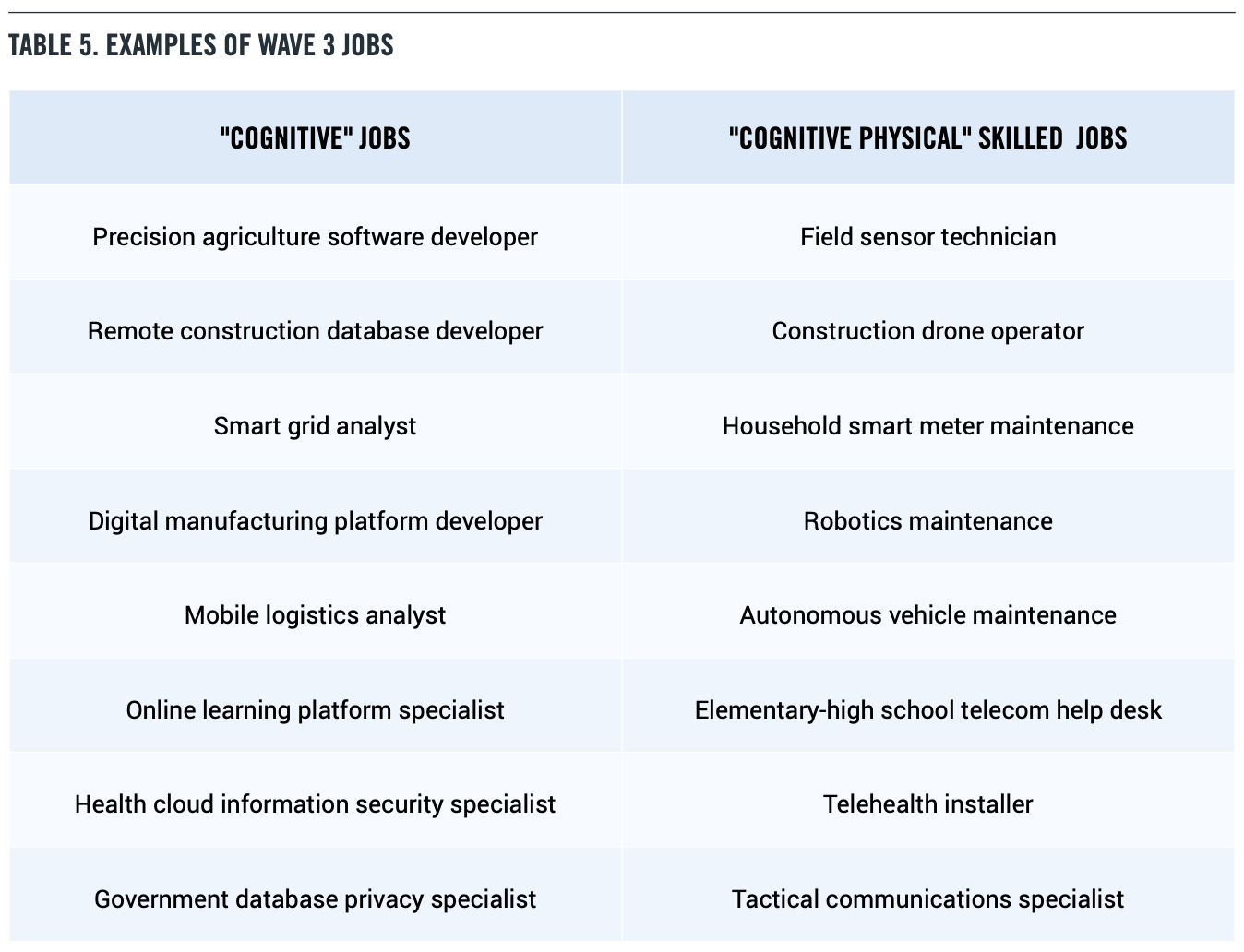

Table 5 identifies examples of Wave 3 jobs. Unlike Wave 2, which mostly generated “cognitive” tech jobs which required a college education, Wave 3 is rooted in the physical world. As a result, Wave 3 will also create mixed ‘cognitive-physical” skilled jobs, many of which fall into the category of installers and maintainers. In addition, people will continue to play an essential role in the supervision loop of advanced robots.

The types of cognitive jobs listed in Table 5 mainly fall into the broad occupational class of “computer and mathematical occupations.” Relative to the median wage for all occupations, these jobs pay a wage premium of 122 percent.

But Wave 3 will also generate blue-collar jobs that use a combination of manual and problem-solving skills—what we call “cognitive-physical” jobs— which are likely to pay a wage premium as well.

Today, the median wage for telecommunications equipment installers and repairers is 45 percent higher than the overall median wage, according to figures from the BLS. As 5G becomes an integral part of business operations, we would expect such jobs to become more valuable rather than less.

III. QUANTIFYING LONG-TERM 5G-RELATED JOBS

Estimates of job growth spurred by a new technology have to be measured against some baseline. As we noted earlier, the BLS projection methodology typically looks backward, not forward, and has a difficult time dealing with ongoing technological changes. BLS projections have consistently understated the job impact of wireless innovation. In the first wireless wave, jobs in the wireless industry came in 50 percent above projections. In the second wireless wave, the rise of the App Economy drove up demand for computer and mathematical jobs 21 percent above BLS projections as of 2019.

Our fundamental assumption is that unlike the second wave—which was mostly focused on digital industries—the third wave will drive demand for both cognitive and cognitivephysical jobs across the whole range of physical and digital industries. The third wave will therefore benefit a wider set of Americans and regions than the second wave did. We therefore adopt a simple and straightforward approach to estimating the impact of 5G on jobs. We start with the latest BLS industry and occupation projections, issued in September 2019, for the 2018-2028 period. We rebase them to 2019 and extend them to 2034 to get a 15-year projection.

Then we assume that the additional jobs produced by 5G in the third wave, relative to the baseline, are the same magnitude as the additional jobs produced by wireless innovation in the second wave. We then allocate these jobs across industries according to their size, rather than focused on only tech. Finally, we then apply a conservative job multiplier.

Based on these assumptions, we estimate that 5G and related technologies will produce an additional 4.6 million jobs in 2034 relative to the baseline original projected growth of 12.8 million.