Today, the Senate Judiciary Committee announced a markup of an antitrust bill aimed at a handful of America’s most successful technology companies, led by Senator Amy Klobuchar (D-MN). The bill will harm American consumers and American middle-class jobs from coast to coast.

Dr. Michael Mandel, Vice President and Chief Economist of the Progressive Policy Institute, released the following statement:

“The digital economy should be a source of pride for Democrats. Digital inflation is low, wage growth in the tech-ecommerce sector is extremely rapid, and digital job creation is strong – especially in pivotal swing states.

“Instead, if this bill is passed, it will undercut the tech and ecommerce industries – which are vital to our 21st century economy – and give China the edge in leadership and the digital economy. The Senate and House bills are unpopular with voters in the battleground congressional districts, and will likely stunt job growth in these pivotal swing states ahead of the 2022 election.

“Senate Democrats should rethink their push to cater toward the extremes of the party and instead focus on pragmatic, pro-growth legislation that makes the digital economy stronger.”

Based on our analysis of BLS data, the tech-ecommerce ecosystem added 1.4 million jobs between September 2017 and September 2021, the most recent data available from the BLS. The previous job creation leader, the health care sector, added 500,000 jobs, roughly one-third of the tech-ecommerce total. And the rest of the economy lost 900,000 jobs.

On the state level, the tech-ecommerce ecosystem took the place of health care as the main job producer in most of the country. From our analysis, 40 states gained more jobs from tech-ecommerce than health care and social assistance from 2017Q1 to 2021Q1 (our analysis requires detailed QCEW data from the BLS, which currently goes through the first quarter of 2021).*

The top of the list, not surprisingly, was California, which added 310,000 tech-ecommerce jobs over the four year stretch. That made a big difference. In a June 2021 blog item, we estimated that tech-ecommerce accounted for roughly 42% of the increase in California personal tax revenues from 2015 to 2020.

The next four states, ranked by tech-ecommerce job creation, are Texas, Florida, Washington, and New York. New York, in particular, added 73,000 tech-ecommerce jobs over that 4-year stretch. Meanwhile, the number of jobs in the crucial New York finance and insurance sector was flat or slightly down.

Other states with strong tech-ecommerce job growth included Ohio (61,000); Arizona (58,000); Georgia (56,000);North Carolina (56,000); Illinois (56,000); and New Jersey (55,000). Note how tech-ecommerce jobs are well-distributed around the country.

Amazon is currently building its second headquarters in northern Virginia, with a total of 25,000 workers expected over the next decade. But even before the Amazon build-out, Virginia has experienced a surge in tech-ecommerce jobs. Between 2017Q1 and 20201Q1, tech-ecommerce jobs rose by 38,000, while jobs in the rest of the economy, including health care, fell by 53,000.

Virginia’s tech-ecommerce jobs are also well-compensated, earning an average of $109,700 per person in 2020. That’s compared to an average wage of $65,100 for all Virginia workers, and $63,900 for Virginia manufacturing workers.

Nevada had a 76 percent increase in tech-ecommerce jobs from 2017Q1 to 2021Q, the biggest percentage gain among states. Arizona had a 49% increase in tech-ecommerce jobs, the third highest percentage gain. Arizona tech-ecommerce jobs paid an annual wage (including bonuses) of $83,300 on average in 2020. That’s comparable to the average pay for Arizona manufacturing wages($82,400), and substantially higher than average pay in Arizona health care and social assistance ($57,600). Tech-ecommerce pay in Arizona is 43% higher than average pay for the Arizona economy as a whole.

The raw numbers are not so impressive for smaller states, but tech-ecommerce is still important for a state like Delaware, which gained 2,000 tech-ecommerce jobs between 2017Q1 and 2021Q1, while finance and insurance employment stagnated. Average pay for the tech-ecommerce sector in 2020 was $73,000 per year, compared to $58,000 for health care and social assistance jobs.

New Hampshire gains 5,000 tech-ecommerce jobs, while health care was flat in terms of hiring and the rest of the state economy lost jobs. In Vermont, tech-ecommerce jobs were flat but employment in the rest of the economy, including health care, shrank by 20,000.

One interesting note: Minnesota is one of the few states where health care jobs grew significantly more than tech-ecommerce jobs. Perhaps coincidentally, Minnesota is also the home state of Senator Amy Klobuchar, who is the lead sponsor for a tech antitrust legislation in the Senate.

*Note that the total lost jobs on the state level, outside of tech-ecommerce and healthcare, is much larger because the most recent detailed state level data available is 2021Q1.

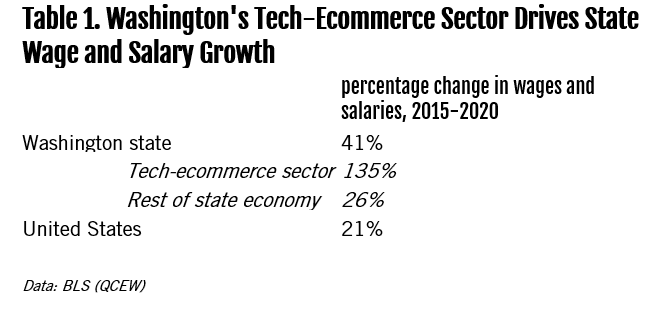

Between 2015 and 2020, total wages and salaries in Washington state rose by 41%, the biggest gain of any state, and almost double the 21% gain for the country as a whole. (See Table 1). This was not simply a pandemic effect, since Washington wage and salary growth was also first in the country in the 2014-2019 period as well.

To a large extent, Washington’s country-leading position in labor income is being driven by job and wage gains in the tech-ecommerce sector. Building on previous research and recent blog posts, we define the tech-ecommerce sector as including five tech industries and three ecommerce industries. The tech industries are computer and electronic production manufacturing (NAICS 334); software publishing (NAICS 5112); data processing and hosting (NAICS 518); Internet publishing and search, and other information services (NAICS 519); and computer systems design and programming (NAICS 5415). The three ecommerce industries are electronic shopping and mail order houses (NAICS 4541); local delivery (NAICS 492); and ecommerce fulfillment and warehousing (NAICS 493). We draw on Bureau of Labor Statistics data from the Quarterly Census of Employment and Wages (QCEW). This dataset reports on all jobs in each industry, as well as wages, salaries, and bonuses, including ordinary income from exercised stock options.

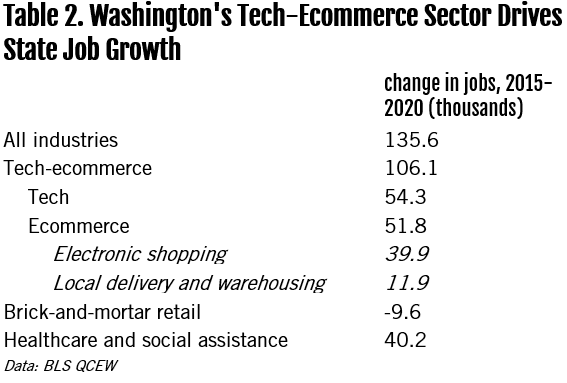

Let’s look at jobs first. From 2015 to 2020, the tech-ecommerce sector added over 100,000 new jobs to the Washington economy. Tech-ecommerce accounted for more than three-quarters of total job creation over that span, far outpacing the contribution of the healthcare and social assistance sector, which has long been the most dependable source of job growth (table 2).

Within the new jobs created by tech-ecommerce, roughly about half of those were in tech industries, and about half were in ecommerce industries (note that the BLS generally assigns establishments to industries according to the type of work being done at that establishment, not the industry of the parent company. So that an ecommerce fulfillment center is typically categorized in warehousing, no matter who owns it).

It’s important to note that the roughly 52,000 jobs being created in ecommerce over the past five years far exceeds the 10,000 jobs lost in brick-and-mortar retail in Washington. Average annual pay in the local delivery and warehousing industries in Washington came to about 30% higher than average annual pay in brick-and-mortar retail in the state. That’s the typical spread we found nationally in past research.

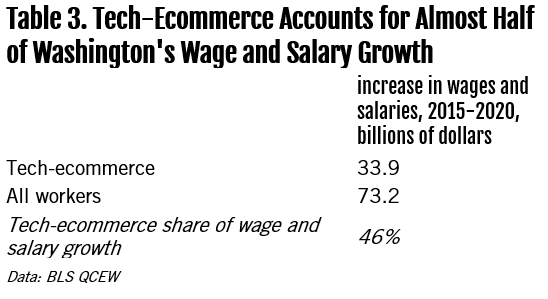

Now consider labor income in the state. Total wage and salary payments in Washington’s tech-ecommerce sector rose by $34 billion from 2015 to 2020, according to BLS data. That’s compared to the $73 billion increase in total wage and salary payments across the state. To put it another way, the tech-ecommerce sector accounted for 46% of the increase in wages and salaries in Washington from 2015 to 2020. (Table 3)

Finally, we turn to the question of the impact of the tech-ecommerce sector on state tax revenues in Washington. Tax collections have come in much stronger than expected, with forecasts repeatedly being raised. In particular, taxes for the 2020-21 fiscal year are currently forecast to come in 13.4% higher than the 2019-2020 fiscal year, and roughly 60% above 2014-2015 levels (See June 2021 Revenue Review from the Washington State Economic and Revenue Forecast Council, page 27).

How much of that gain is accounted for by the tech-ecommerce sector? There are several issues with making this calculation. The state government reports and forecasts tax revenue data on a fiscal year basis, while our data on the tech-ecommerce sector is on a calendar year basis and stops with 2020. In addition, states with a personal income tax have a direct connection between wage and salary payments and state tax revenues Washington, however, has no personal income tax, and relies instead on a variety of other taxes, including a retail sales taxes, a business and occupation tax, a property tax, and a real estate excise tax.

Usually we think of taxes like these as being less immediately responsive to changes in wages and salaries than an income tax would be. Indeed, there was a stretch, around the time of the financial crisis and the years after, when the state’s “General Fund” tax revenues languished, even as the state’s wages and salaries started to rebound.

In recent years, however, the combined and diverse flows of tax revenues into the state’s coffers appear to be rising more or less in parallel with the QCEW wage and salary measure, when adjusted for fiscal years. That makes it plausible that we can use the tech-ecommerce share of wage and salary growth as a proxy for tech-ecommerce share of tax revenue gains.

There are two possible tax revenue measures we can use for our back-of-envelope calculations — either “General Fund” taxes, or a somewhat broader category of state tax revenues, which starts with “General Fund” taxes and then adds in several taxes earmarked for education and training. That broader tax concept has been growing somewhat faster in recent years. Noting that Washington is on two-year budget cycles (also known as “Bienniums”), General Fund tax revenues rose by $17.1 billion from the 2013-15 budget cycle to the 2019-21 budget cycle, while the broader measure of tax revenues rose by $18.9 billion.

We then apply the 46% tech-ecommerce share of wage and salary growth to the increases in the two measures of tax revenues. We estimate that the growth of tech-ecommerce jobs and incomes accounts for $8.0-8.8 billion in higher tax revenues funding the 2019-21 budget cycle compared to the 2013-15 budget cycle. This should be viewed as a roughly estimate and not a final figure.

Conclusion and Implications

The tech-ecommerce sector is a massive positive for jobs, incomes and taxes in the state of Washington. That suggests Washington-headquartered Amazon and Microsoft, rather than “blocking the sunlight” for other companies in the state, play a central role in a thriving ecosystem that benefits workers, raises wages and generates tax revenues. As the saying goes “if it ain’t broke, don’t fix it.”

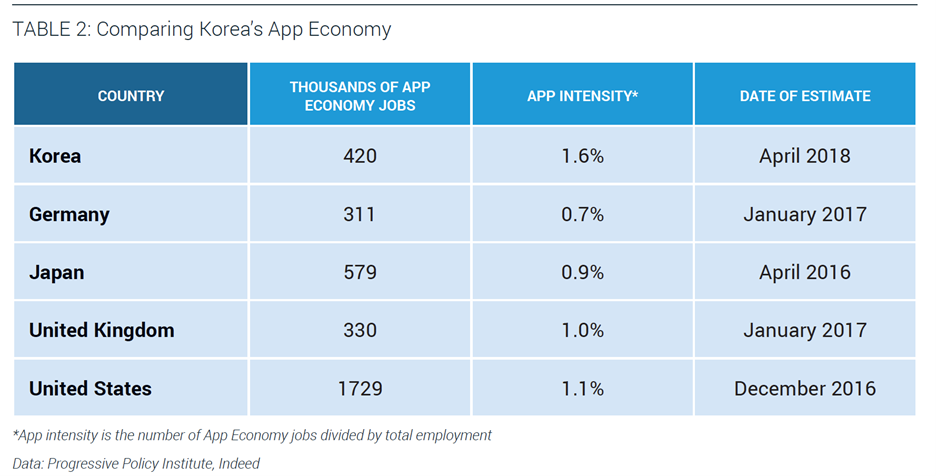

By our analysis, Korea’s “App Economy” is one of the strongest in the world. In our 2018 study, the Progressive Policy Institute (PPI) estimated that Korea had 420,000 App Economy jobs, amounting to 1.6% of the workforce (see reproduced table below). This figure for “app intensity” was considerably higher than Japan, the United Kingdom, Germany, and even the U.S. at the time (though our latest estimate pegs American app intensity at 1.7% as of August 2020).

Moreover, as of 2020, 8 out of the top ten app companies in Korea were Korean-headquartered, according to download estimates from App Annie. By comparison, only 1 out of the top ten app companies in Germany were German-headquartered. Korea has a vibrant domestic App Economy that other countries would be envious of.

But despite this record of success, the Korean government is considering legislation that would dramatically change the app business environment. The legislation—which would amend Korea’s Telecommunications Business Act–would prohibit online app stores from requiring app developers to use the app store’s payment systems for in-app purchases. In effect, this would be equivalent to forcing a brick-and-mortar retailer to allow competitors to set up alternative checkout lanes in their stores.

The first question is: Why try to fix something that isn’t broken? Korean app developers are prospering under the current system and creating well-paying jobs. Why take the risk that a new system will turn out worse?

The second question is: Why undertake measures that would potentially accelerate “decoupling” Korea’s economy from the United States? The legislation under consideration would primarily affect U.S. tech companies, feeding the current American desire to shorten supply chains and build up internal tech production capacities. Korea and the U.S. will always be allies and friends, but in today’s political environment, lawmakers should pay attention to building bridges, not destroying them.

This table is reproduced from “Korea’s App Economy,” May 2018, Progressive Policy Institute. Data for other countries was current in 2018 when table was published. The latest numbers are available on request.

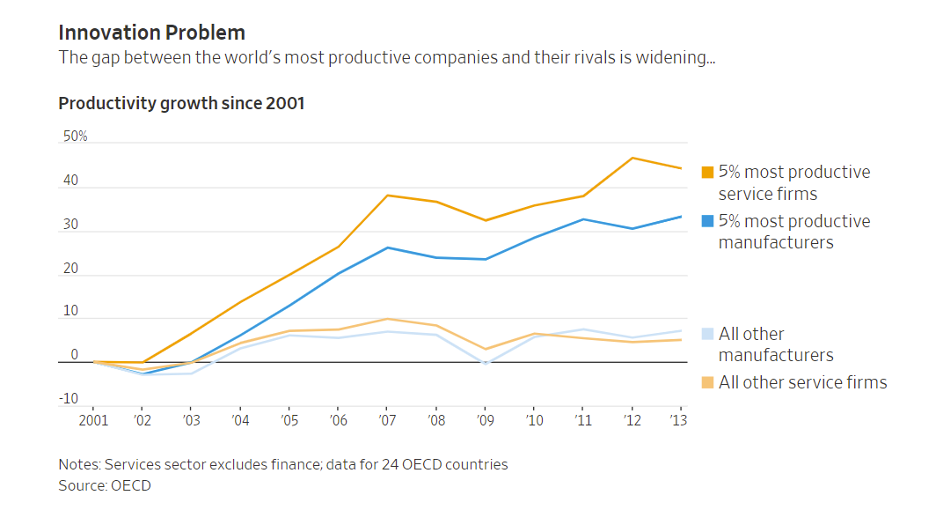

For the firms that adopt them, artificial intelligence (AI) systems can offer revolutionary new products, increase productivity, raise wages, and expand consumer convenience.[1] But there are open questions about how well the ecosystem of small and medium-sized enterprises (SMEs) across the United States is prepared to adopt these new technologies. While AI systems offer some hope of narrowing the recent productivity gap between small and large firms, that can only happen if the technologies actually diffuse throughout the economy.

While some large firms in the U.S. are on the cutting edge of global AI adoption, the challenge for policymakers now is to help these technologies diffuse across the rest of the economy. To realize the full productivity potential of the U.S., AI tools need to be available to 89% of U.S. firms that have fewer than 20 employees and the 98% that have fewer than 100.[2] An AI-enabled productivity boost would be particularly timely as SMEs are recovering from the effects of the ongoing COVID-19 crisis.

The report discusses the promise for AI systems to increase productivity among U.S. SMEs, the current barriers to AI uptake, and policy tools that may be useful in managing the risks of AI while maximizing the benefits. In short: there is a wide range of policy levers that the U.S. can use to proactively provide the underlying digital and data infrastructure that will make it easier for SMEs to take the leap in adopting AI tools. Much of this infrastructure operates as a type of public good that will likely be underprovided by the market without public support.

Benefits of AI adoption:

The central case for AI adoption is that human cognition is limited in a variety of ways, most notably in time and processing power. Software tools can improve decision-making by increasing the speed and consistency with which decisions can be made, while also allowing more decisions to be planned out ahead of time in the event of various contingencies. Under this broad framework, we can think about “AI” as being a broad suite of technologies that are designed to automate or augment aspects of human decision-making.

While many of AI’s most eye-catching use cases will likely remain the preserve of large platforms, the technology also holds tremendous promise for SMEs. The adoption of third-party AI systems will notably enable SMEs to streamline mundane (but often costly) tasks such as marketing, customer relationship management, pre- and post-sales discussions with consumers, and Search Engine Optimization (SEO). These systems can provide a lifeline for SMEs who are overwhelmed by the many challenges of running a business, and they can expand the number of businesses that are eligible for certain financial supports. For example, AI tools can be used to improve the accuracy of credit risk underwriting models and using alternative data sources and a streamlined process, they can make it easier for SMEs to take out loans they otherwise might not qualify for under traditional methods. Along similar lines, research shows that AI-driven robotics have (and will continue) to boost the productivity of SMEs in the manufacturing industry.

Importantly, this upcoming wave of AI technology can help SMEs catch up with larger, international firms because it can democratize the benefits of large information technology (IT) investments that superstar firms have been seeing over the last decade.

The economist James Bessen has argued that the top 5% of firms in many industries have been increasingly pulling away from the rest of the field because they’ve made large investments in proprietary IT systems. Their smaller rivals struggle to develop their own systems because they lack the necessary scale to hire a large stable of in-house technical talent. Amazon, for example, has a team of 10,000 employees working to improve their Alexa and Echo systems.

While AI tools can’t fully reverse this trend, they can help shrink the gap when embedded into Software as a Service (SaaS) platforms that smaller firms can make use of without the same level of investment. Essentially, through general-purpose AI tools, SMEs can have access to a host of productivity enhancements that these proprietary IT systems offer, but at a price point that is economical for SMEs. By shrinking this productivity gap, smaller firms can begin to compete in earnest while differentiating from large firms through improved customer service and greater product diversity. This will give a large leg up to SMEs who adopt these AI systems and help them better compete with large global incumbent firms.

Consider a firm like Keelvar Systems, which uses advanced sourcing automation to help businesses rapidly shift supply chains around the globe in the event of disruptions or delays. Essentially, it replaces or augments the work that a large supply chain and sourcing office would do within a firm. By using their service, or others like it, SMEs have the ability to benefit from similar levels of sophistication in their supply chain management without having employees spend hundreds of hours on tedious tasks or maintaining expensive proprietary IT systems.

There are firms like Legal Robot that have created a series of tools to help small businesses access legal services that would otherwise require a small army of in-house lawyers. With their service, SMEs can use smart contract templates based on their industry, receive instant contract analysis to make sure they are receiving fair terms and can automate certain aspects of compliance with laws like the GDPR.

Likewise, companies like Bold360 have helped SMEs improve their customer service experiences by offering a variety of AI-powered-chatbots and tools. Many basic customer concerns about products or delivery can be handled by these basic chatbots, freeing up human customer representatives to focus their time on the hard or advanced cases. Again, the pattern here is there is a service that large, multinational companies have been investing billions of dollars to create proprietary versions of, and now the customizability of AI is helping this service become more accessible to SMEs.

What are the barriers to AI adoption for SMEs in the U.S. and what can policymakers do to help create a welcoming environment?

Data investment as a public good

Depending on the context, data can often have the same traits as other public goods. First, it is non-rival—the marginal cost of producing a new copy of a piece of data is zero. Stated differently, multiple individuals can use the same dataset at almost no additional cost. The second important trait is that data is hard to exclude. Consider this report. Once it has been posted online, it is difficult to prevent people from accessing and sharing it as they see fit. This is one of the reasons why copyright infringement is so hard to stamp out.

Oversimplifying, these two features can lead to two opposite problems. On the one hand, economic agents might underinvest in public goods, absent government-created appropriability mechanisms (such as patent and copyright protection). Conversely, public goods tend to be underutilized (at least from a static point of view). Any price that enables economic agents to recoup their investments in a public good will be above the good’s “socially optimal” marginal cost of zero. Public good policies thus involve a tradeoff between incentives to create and incentives to disseminate. For example, patents give inventors the exclusive right to make, use and sell their invention; but inventors must disclose their inventions, and these fall into the public domain after twenty years.

What does this mean for data and artificial intelligence? If policymakers think that data is an essential input for cutting-edge AI, then they should question whether obstacles currently prevent firms from investing in data generation or disseminating their data.

While policies in this space involve significant tradeoffs, some offer much higher returns to social welfare. For instance, to the extent policymakers believe existing datasets are being underutilized, purchasing private entities’ data (through voluntary exchanges) and placing it in public data trusts would be a better policy than imposing data sharing obligations (which could undermine firms incentive to produce data in the first place). This is akin to the idea of government patent buyouts.

Of particular interest for policymakers, however, is the fact that some SMEs are sitting on top of data flows that are not being fully utilized because it is expensive to make data usable and these datasets may not be very valuable in isolation. As an example, industry-level manufacturing data might be quite valuable to all firms in a sector, but the dataflows from one SME are much less valuable. The U.S. could align incentives by providing investment funds to quantify various aspects of business flows and then submit them to public data trusts, which could be accessible for use by all firms in the industry. This would essentially be treating valuable dataflows as a type of public infrastructure that needs government investment to be fully realized.

This kind of public investment can happen not only through incentives for private firms but through the public sector as well. Governments at all levels (state, local, and national) have valuable dataflows regarding infrastructure development, the organization of public transportation, and general macro-level economic data that can be turned into open datasets for public and commercial use. Particularly on the national level, the U.S. should consider investment in IT infrastructure that can coordinate the submission of open datasets on the state and local level.

Indeed, if key scientific or commercial datasets do not yet exist, the public sector may be best positioned to create them in the first place as a type of digital infrastructure provision. One notable structure that may help in this regard is the idea of a Focused Research Organization, which would provide a team of researchers with an ambitious budget and a nimble organizational structure with the specific goal of creating new public datasets or toolkits over a set time period.

Provide regulatory certainty

For SMEs deciding whether to invest in adopting AI tools, regulatory and compliance costs can be a significant deterrent. Policymakers should recognize that regulation is often more burdensome for small firms that generally have less ability to shoulder compliance costs. Especially in industries with low marginal costs, such as the tech sector, larger firms can spread fixed compliance costs across more consumers, giving them a competitive edge over smaller rivals. Regulation can thus act as a powerful barrier to entry. For instance, a study found that the European experiment with GDPR led to a 17% increase in industry concentration among technology vendors that provide support services to websites.

This is not to say that additional regulation is, or is not, necessary in the first place. Indeed, there are a host of malicious or unintentional harms that can occur from improperly calibrated AI systems. Regulation can be a powerful tool to prevent these harms and, when well-balanced, can promote greater trust in the overall ecosystem. But potential regulation should follow sound policymaking principles that reduce the regulatory burden imposed on firms, notably by making regulation easy to understand, risk based, and low-cost to comply with.

In the U.S. there is to date no overriding national AI regulation. Instead, each sectoral regulator (i.e. Federal Aviation Administration, Security and Exchange Commission, Federal Trade Commission, etc.) has been steadily increasing their oversight over the use of algorithms and software in their specific area. This is likely an appropriate approach, as the kinds of risks and tradeoffs at play are going to be very different in healthcare or financial decision-making when compared to consumer applications. As this approach develops, it would be prudent to develop a risk-based framework that allows for more scrutiny of algorithmic decision-making in sensitive areas while giving SMEs confidence to invest in low-risk areas with the knowledge they will not later take on large compliance costs.

However, regulation over data protection has been far more segmented and piecemeal. And the state-by-state patchwork of rules that has developed can be a significant deterrent for SMEs when considering whether to invest in the use of certain AI tools. Policymakers should consider an overriding national privacy law that would be able to set standard rules of the road over the protection of data in all 50 states so that U.S. SMEs can invest with confidence.

Finally, U.S. policymakers should consider aggregating all this information through the creation of a dedicated AI regulatory website that provides a toolkit of resources for SMEs about the benefits of AI adoption for their business, the potential obligations and roadblocks that they need to be aware of, and best practices for cybersecurity hygiene and data sharing.

Expand the AI talent pool

A lack of skilled talent is one of the biggest barriers to AI adoption as the technical skills required to build or adapt AI models are in short supply. In the U.S., especially, smaller companies struggle to compete with the high salaries paid out by large tech firms for top-end machine learning engineers and data scientists.

In broad strokes, this skills shortage can be alleviated in two ways: through upskilling the domestic population and by improving immigration pathways for global talent.

To upskill the domestic population, one relatively simple lever would be to pay some portion of the costs of individuals and businesses who wish to upskill. In the U.S., a portion of a worker’s retraining costs may be written off as a business expense so long as the worker is having their productivity improved in a role they currently occupy. But this expense is not tax deductible if the proposed training would enable them to take on a new role or trade.

For example, if a small manufacturing firm has technically competent IT staff who wish to attend a specialized training course on using machine vision systems in a warehouse environment, this expense would not currently be deductible as it would enable them to take on a new role within the company. This inadvertently creates an incentive to spend more on capital productivity investments than labor productivity investments. Addressing this imbalance would incentivize more firms to invest in worker retraining and help speed the creation of an AI workforce in the U.S.

Secondly, the U.S. needs to urgently address the shortcomings in the U.S. immigration system which make it more difficult for startups to compete with large incumbents on the basis of talent. Approximately 79% of the graduate students in computer science (and related subfields) studying in the U.S. are international students, which means a large majority of potential AI workers U.S. firms may look to recruit must operate through the immigration system. The cost, complexity, and length of this process inevitably favors large, incumbent firms who can afford to navigate the regulatory maze of procuring an H-1B or related work visa.

A recent NBER paper showed in detail the myriad ways in which access to international talent is important for startup success. Utilizing the random nature of the H-1B lottery system, the paper compared startups that randomly received a higher percentage of their visa applications approved to those who did not. The random nature of the H-1B lottery makes an ideal policy experiment because it allows for a clean test in which other potentially confounding variables are controlled for. The study found that a one standard deviation increase in the likelihood of successfully sponsoring an H-1B visa correlated with a 10% increase in the likelihood of receiving external funding, a 20% increase in the likelihood of a successful exit, a 23% increase in successful Initial Public Offering, and a 4.8% increase in the number of patents filed by the startup.

Policymakers could begin to counter this effect by waiving immigration fees for firms of a certain size and by streamlining the application process.

Further, policymakers should look to create a statutory startup visa so that international entrepreneurs have a viable pathway into the U.S. to launch firms of their own. According to research by Michael Roacha and John Skrentny, international STEM PhD students are just as likely to report wanting to work for or launch their own firm as native-born students, but the difficulty of our immigration system pushes them towards working at large incumbent firms.

Using these two levers of upskilling and immigration reform, the U.S. should increase the supply of AI talent available to SMEs or to launch SMEs themselves and thereby spur the adoption of AI adoption.

Conclusion

Artificial intelligence systems hold great potential to streamline the costs of doing business in a modern economy, particularly for SMEs. The last 20 years of the information technology revolution have helped large, established firms reach the cutting edge of productivity while smaller firms have been left behind. But general-purpose AI tools now provide an opportunity for SMEs to take advantage of many of these IT advancements at a cost and a scale that is feasible for them. Policymakers should attempt to proactively build out the digital infrastructure that will make it easier for SMEs to take the leap in adapting AI tools.

Summary of policy recommendations:

Data investment as a public good:

Where appropriate, align incentives for the private sector to contribute industry-level SME data to public and private data trusts that could be used by everyone.

Invest in making more government datasets open to the public.

Fund Focused Research Organizations or similar groups with the explicit goal of creating new scientific and commercial public datasets.

Provide regulatory certainty:

Clarify existing regulations and the obligations that SMEs must meet when utilizing a new AI tool.

Encourage the development of a risk-based framework that allows for more stringent regulation of sensitive applications while giving certainty to SMEs on investment in low-risk applications.

Pass an overriding national privacy law so that SMEs aren’t deterred from investing by a patchwork of differing state-by-state laws.

Consider the creation of a new SME regulatory website that provides informational resources to SMEs about the benefits of AI adoption for their business and the potential roadblocks that they need to be aware of.

Expand the AI talent pool

Encourage upskilling of the U.S. population by making worker retraining deductible as a business expense.

Reevaluate U.S. immigration pathways to make them more attractive for international technical talent.

Streamline the immigration application process and waive fees for firms below a certain size to make it easier for SMEs to compete for technical talent.

[1] This report is an adaptation of an earlier paper coauthored with Dirk Auer titled “Encouraging AI Adoption in the EU”.

[2] Annual Survey of Entrepreneurs – Characteristics of Businesses: 2016 Tables, United States Census Bureau

The large tech and ecommerce companies have become massive job generating and income creating machines, hiring hundreds of thousands of workers in the United States. This is one of the great hiring surges in history, providing well-paying jobs for an unprecedented number of workers.

But just looking at hiring by the tech giants themselves does not fully answer the question of their impact on the labor market. It could be that, like tall trees, they block the sunlight and keep other tech companies and ecommerce companies stunted.

This “ecosystem dominance” would manifest as weak job and income growth in the tech-ecommerce sector as a whole. If true, this harm to workers becomes a powerful justification for strong regulatory and antitrust growth against the tech giants. In other words, chopping down the trees would help the rest of the forest grow.

Alternatively, strong job and income growth across all tech and ecommerce industries would show the tech giants–who invested a stunning $65 billion in the United States in 2020—are playing a crucial role in a thriving ecosystem that benefits workers, raises wages and generates tax revenues. Indeed, from 2015 to 2020—a period that includes the pandemic—the tech-ecommerce ecosystem generated 1.7 million net new jobs and added $289 billion in labor income. By comparison, the whole private sector lost 360,000 jobs. In that case, common sense would call for regulatory prudence. As the saying goes “if it ain’t broke, don’t fix it.”

California

For this blog post we will focus on the job, income, and tax impact of the tech-ecommerce sector on California, which is the headquarters of three out of the four tech giants. In addition, in the fourth quarter of 2020, Amazon employed more workers in California (153,000+) than it does in Washington (80,000+).

Our analysis builds on PPI’s April 2021 paper, “Innovative Job Growth in the 21st Century: Has the Tech-Ecommerce Ecosystem Become the New Manufacturing?”. The tech-ecommerce ecosystem includes five tech industries and three ecommerce industries. The tech industries are computer and electronic production manufacturing (NAICS 334); software publishing (NAICS 5112); data processing and hosting (NAICS 518); Internet publishing and search, and other information services (NAICS 519); and computer systems design and programming (NAICS 5415). The three ecommerce industries are electronic shopping and mail order houses (NAICS 4541); local delivery (NAICS 492); and ecommerce fulfillment and warehousing (NAICS 493).

We draw on Bureau of Labor Statistics data from the Quarterly Census of Employment and Wages (QCEW). This dataset reports on all wages, salaries, and bonuses, including ordinary income from exercised stock options. We look at the five-year period from 2015 to 2020, which includes the pandemic year.

Table 1. Strong Job and Labor Income Growth in California’s Tech-Ecommerce Sector

Percentage change, 2015-2020

Tech-ecommerce sector

California

Core tech counties*

Rest of California

United States

Jobs

38%

30%

43%

31%

Total wage and salary income**

76%

77%

74%

56%

*San Francisco, San Mateo, Santa Clara

**Includes exercised stock options

Data: BLS QCEW

Table 1 shows the growth of jobs and labor income in California’s tech-ecommerce sector from 2015 to 2020. Tech-ecommerce jobs rose by 38% over the five-year stretch in California, compared to 31% in the United States as a whole. Meanwhile, private sector jobs rose by 0.3% in California and fell by 0.3% nationally (not shown on table).

Wages and salaries in California’s tech-ecommerce sector rose by an astounding 76% from 2015-2020, compared to 56% nationally. Meanwhile, private sector wages and salaries rose by 31% in California, and 21% nationally.

Table 2 shows the importance of the tech-ecommerce sector for California’s economy. The tech-ecommerce sector added 350,000 jobs between 2015-2020 in the state, and $100 billion in additional wage and salary income. That means the tech-ecommerce sector accounted for 38% of the entire increase in private sector wages in the state over that period.

Table 2. Tech-Ecommerce Sector Powers California Income Growth

Tech-ecommerce sector

California

Core tech counties

Rest of California

United States

Increase in jobs, 2015-2020 (thousands)

350

113

237

1738

Increase in wage income, 2015-2020 (billions of dollars)

$100

$62

$37

$289

Share of private sector wages, 2020 (percent)

21%

45%

11%

11%

Share of private sector wage growth, 2015-2020 (percent)

38%

56%

25%

22%

*San Francisco, San Mateo, Santa Clara

**Includes exercised stock options

Data: BLS QCEW

Note that Table 1 and Table 2 break out the core tech counties, San Francisco, San Mateo, and Santa Clara, from the rest of the state. Taken together, the two tables show that both the core tech counties and the rest of the state have shown roughly equal rates of income growth from the tech-ecommerce sector.

Table 3 looks specifically at ecommerce and retail jobs in California. Obviously, the pandemic forced a dramatic decline of brick-and-mortar retail jobs in the state. At the same time, the number of ecommerce jobs increased by more than enough to counteract the decline of brick-and-mortar retail. Moreover, the ecommerce jobs were substantially better paid on average.

As a result, when we combine brick-and-mortar retail with ecommerce industries in California, the number of net jobs rose by 28,000. Average annual pay rose by 22 percent.

Table 3. California’s Ecommerce Industries Create Net New Jobs and Boost Average Pay

Brick-and mortar retail

Thousands of jobs

Average annual pay

2015

1611

33229

2020

1475

40199

Change, 2015-2020

-136

Ecommerce industries

2015

207

54078

2020

372

55882

Change, 2015-2020

164

Brick-and-mortar retail plus ecommerce

2015

1819

35608

2020

1847

43360

Change, 2015-2020

28

Data: BLS QCEW

Finally, we turn to the question of the impact of the tech-ecommerce sector on personal income taxes in California. Tax collections have come in much stronger than expected, with personal income tax collections in the first nine months of the 2020-21 fiscal year running at 17% or $14 billion above forecast. Personal income tax revenues in the 2020-21 fiscal year are now forecast to be 54% about 2015-2016 levels.

How much of that gain is accounted for by the tech-ecommerce sector? There are several issues with making this calculation. The state government reports and forecasts tax revenue data on a fiscal year basis, while our data on the tech-ecommerce sector is on a calendar year basis and stops with 2020. Second, our definition of the tech-ecommerce sector includes a wide variety of industries, with average annual pay that runs from roughly $50,000 to well over $300,000. Third, much of the surge in personal tax revenues is coming from capital gains, which is directly connected with the success of the tech-ecommerce sector but is not reported in the BLS QCEW data.

Nevertheless, we can make a back-of-the-envelope estimate of the personal tax revenue generated by the tech-ecommerce sector. First, let’s start by looking the increases in personal tax revenues coming from wage and salary income (included ordinary income from exercised stock options) over the 2015-2020 period. By our estimate, the increase in tech-ecommerce wages and salaries accounts for roughly 37% of the increase in personal tax revenues from wages and salaries in the 2015-2020 period.

But of course, there has been a surge in capital gains revenues as well. If we attribute half the unanticipated increase in capital gains in 2020 to the tech-ecommerce sector, then tech-ecommerce accounts for roughly 42% of the increase in California personal tax revenues from 2015 to 2020. This should be viewed as a rough estimate rather than a final number.

On Wednesday, the House Judiciary Committee is going to mark up five tech antitrust bills. Collectively, the bills mark a major departure from the traditional consumer welfare standard that has governed antitrust law over the last few decades. Instead of focusing on consumers, these new laws would single out just five large tech platforms and apply an entirely different set of standards. One bill would effectively ban them from making any future acquisitions, which might have the unintended consequence of reducing startup investment, and therefore reducing competition. Most concerningly, another one of the bills would lead to breakups of all five major tech companies. Vertical integration would effectively be prohibited because, according to the bill’s authors, it presents an irreconcilable conflict of interest.

But what this framing misses is all the consumer benefits that flow from integrated ecosystems. Many digital products are free to access because they are subsidized by ads elsewhere in the ecosystem. A hallmark of a seamless user experience is being able to switch between devices, websites, and apps without needing to re-enter all your information. Crucially, these integrated experiences are also safer for users because fewer players in the market have direct access to user data (which is why most government agencies do not allow federal employees to “jailbreak” their smartphone devices or sideload apps from unapproved app stores). And of course, private label goods on Amazon work just the same as they do in Walmart or CVS — they offer consumers similar quality to name brands at lower prices.

Here’s a more detailed breakdown of the five bills and what they would do to tech platforms (in order from most reasonable to least reasonable):

The budgets for the FTC and DOJ to conduct antitrust enforcement have fallen by 18% between 2010 and 2019, after adjusting for inflation. Over the same period of time, the economy has grown by 22%. To properly enforce the antitrust laws on the books, the DOJ and FTC need resources that match the scope of the problems they face. This bill would increase their enforcement resources by almost 30% and change the merger filing fee structure to fall more heavily on larger deals. There is significant bipartisan support for this bill and it is urgently needed.

For the next four bills, you need to understand what a “covered platform” is. All four bills define them the same way (and these new rules would only apply to covered platforms). A covered platform is a “website, online or mobile application operating system, digital assistant, or online service” that meets all three of the following conditions: (1) 50 million U.S.-based monthly active users or 100,000 U.S.-based monthly active business users; (2) greater than $600 billion in net annual sales or market capitalization; and (3) is a “critical trading partner” that can restrict business users access to customers.

As of today, there are only six companies in the U.S. that meet the $600 billion market capitalization threshold. Every commentator assumes Amazon, Apple, Facebook, and Google will qualify as covered platforms, and most agree that Microsoft will be included as well, considering it operates multiple large-scale platforms, such as Windows, Office, Xbox, and LinkedIn. It remains to be seen whether the “net annual sales” metric will be interpreted to cover financial services companies like Visa, JP Morgan Chase, and PayPal, which process a large volume of payments.

What seems clear, however, is that the subcommittee bills target big tech firms instead of probing economic concentration across the U.S. economy.

The ACCESS Act would require platforms to provide third parties with APIs, software that allows access to platform data. The bill leaves the definition of “data” up to the FTC to determine. Data portability done right can lower switching costs and improve competition in an industry. Consider the enormous success of telephone number portability in the telecom industry. Letting consumers own their telephone number lowers the cost of moving to a new provider. And because telephone numbers are a necessary and discrete piece of data that all carriers must use to operate a network, there was no risk of decreasing the incentive to invest in creating this data.

For tech platforms, there might be similar discrete, static, and critical data sets that should be subject to mandatory portability rules. For example, the social graph — the list of all your friends or connections on a social network — is a very important dataset for new startups to have access to. Users are more likely to use a new app if during the onboarding process they are able to share a social graph from another social network and find all their friends on the new platform with a single click.

However, the problem with this bill is that it is not narrowly tailored to discrete and critical data sets like the social graph. It merely says that “a covered platform shall maintain a set of transparent, third-party-accessible interfaces (including application programing interfaces) to enable the secure transfer of data to a user, or with the affirmative consent of a user, to a business user at the direction of a user, in a structured, commonly used, and machine-readable format.” The bill leaves it to the FTC to define what “data” means for the purpose of the bill. It would be very helpful if Congress offered more guidance on what kinds of data it intends to be covered by these rules.

If data is defined too broadly, then there might be unintended consequences for investment incentives. For example, tech companies are all racing to build the next great computing paradigm. Will it be virtual reality? Blockchain technology? Augmented reality? Smart devices? Or something else no one can predict? Regardless of which paradigm wins out, if the future winner is forced to give every one of its competitors access to all of its data, then that would decrease the incentive to invest in the next big platform today. The most tragic part of the scenario is that these will be unseen costs — we won’t know what we lost out on. The future will just be somewhat dimmer because a well intentioned policy backfired due to poor drafting and a rushed process.

The Platform Competition and Opportunity Act is effectively a ban on all mergers and acquisitions by platform companies. This bill would ban platforms from acquiring companies that:

“compete with the covered platform … for the sale … of any product or service”;

“constitute nascent or potential competition to the covered platform … for the sale … of any product or service”;

“increase the covered platform’s … market position”; or

“increase the covered platform’s … ability to maintain its market position”

Given how broad this language is, the bill would effectively ban all acquisitions by platform companies. Since more than 90% of startups provide a return for their founders, employees, and investors through an acquisition as opposed to going public, this bill has the potential to backfire and decrease investment in startups. A recent study found that “VC activity intensifies after enactment of country-level takeover friendly legislation and decreases following passage of state antitakeover laws in the U.S.” This bill would qualify as an antitakeover law.

This bill is aimed at remedying the perceived conflict of interest by platforms and businesses that leverage those platforms to reach consumers. In essence, this bill bans self-preferencing by requiring platform owners to refrain from any conduct that gives their own products an advantage over competitors’ products. Section 2 of the bill makes it clear how all encompassing this rule aims to be (emphasis added):

“It shall be unlawful for … a covered platform … to engage in any conduct that … advantages [its] own products, services, or lines of business over those of any other business user, excludes or disadvantages the products, services, or lines of business of another business user relative to the covered platform operator’s own products, services, or lines of business, or discriminates among similarly situated business users.

The bill then provides 10 examples of discriminatory conduct, including tying, anti-steering provisions, retaliation, and restrictions on pricing.

But those specific examples aren’t really necessary when the bill includes a blanket ban on any conduct that “advantages” the platform’s products over those of third parties. While this attempt to fix a conflict of interest may seem intuitive at first glance (think of Elizabeth’s Warren’s baseball analogy), the more you think about the idea, the less it makes sense. For example, consider how this rule would apply to Apple. The iPhone runs on Apple’s proprietary iOS operating system. Apple wouldn’t be allowed to “advantage” its App Store in any way, which means it can’t be pre-loaded on devices and it can’t be the default app store unless users select it. This same logic applies to every layer of the tech stack. Apple makes dozens of popular first-party apps, including FaceTime, iMessage, Mail, and Music. As the bill is currently written, Apple would not be allowed to pre-install those apps on iPhone devices because that would “advantage” them over other video conferencing, messaging, mail, and music apps.

Now consider how this law would apply to Google. If a user typed in “restaurants near me” on Google, the search engine wouldn’t be able to directly offer map results at the top of the page from Google Maps because that would give it an “advantage” over other mapping services. Google would be forced to merely provide links to competitive mapping services rather than give consumers the answer to their question. The same rule would apply to Google Shopping if a user searched for sneakers. Instead of showing the user sneakers, Google would have to show users links to shopping websites that sell sneakers. This would represent a huge loss to consumer convenience that makes these products so popular (91% of Americans have a favorable opinion of Amazon, 90% have a favorable opinion of Google, and 81% have a favorable opinion of Apple).

Most concerningly, this bill would break the safety and security of many features of the iPhone. If Apple has access to a piece of hardware, such as a sensor or communications chip, then it has to give equal and fair access to that same hardware function to all third parties. That sounds like a laudable goal if you want more options when it comes to payments (i.e., access to the NFC chip) or location services (i.e., access to GPS) or the microphone (e.g., the way say Siri is always listening for “Hey, Siri”). But the flip side of more competition in this context is that every bad actor with the intent to defraud consumers or invade their privacy now also has access to sensitive data by law.

Lastly, some argue that the affirmative defense section of this bill would allow some pro-consumer conduct by the platforms to continue (such as continuing to pre-install apps on phones). The platforms can “advantage” their own products so long as they “would not result in harm to the competitive process by restricting or impeding legitimate activity by business users; or was narrowly tailored, could not be achieved through less discriminatory means, was nonpretextual, and was necessary to prevent a violation of, or comply with, Federal or State law; or protect user privacy or other non-public data.” But pre-installation and default settings clearly give a leg up to the products controlled by the platform owner and therefore might “result in harm to the competitive process.” If the intent of the drafters is not to ban this type of conduct, they should clarify this section.

The most extreme and economically destructive of the five bills is The Ending Platform Monopolies Act. It tries to address the same problem as the American Innovation and Choice Online Act — conflicts of interest between platform owners and platform competitors. But instead of requiring platform owners to operate their platforms in a neutral fashion as the non-discrimination bill does, this bill bans vertical integration outright and would lead to the break up of every large tech company across multiple dimensions.

Google would have to spin off YouTube, Android, Chrome, the Play Store, and its apps (Gmail, Google Maps, Drive, etc.) into separate businesses. Of course, that would destroy Google’s current business model where revenue from search and display advertising is used to subsidize an ecosystem of free products for consumers. Post-breakup, the newly independent entities would likely need to start charging subscription fees or create their own advertising business from scratch (and add more ad units to their respective products).

Amazon would be forced to spin off its private label goods business (e.g., Amazon Basics) and Amazon Marketplace because those two lines of business compete with the traditional retailing model where Amazon takes inventory of the product from wholesalers and then resells it at a markup. Amazon would also be forced to spin off its Amazon Prime Video streaming service and Amazon Web Services.

It has not yet been properly appreciated that this bill is aimed at addressing the same alleged conflict of interest issue as the American Choice and Innovation Online Act. If they are passed together, this bill would obviate the other one. As independent technology analyst Ben Thompson pointed out, this could mean that Chairman David Cicilline is attempting to make his bill seem reasonable by comparison even though it also has radical implications for tech ecosystems. Legislators shouldn’t fall for this obvious gambit.

The DOJ and FTC desperately need more resources to adequately enforce the antitrust laws on the books, and a narrowly tailored data portability mandate could enhance digital platform competition. But blanket bans on acquisitions, self-preferencing, and vertical integration would destroy many of the consumer benefits that make the tech giants world leaders in their respective markets. Hobbling America’s tech giants without adequate evidence of consumer harm would be a capitulation to the populists on the far left and far right at a time when we need to be focused on economic recovery.

Tomorrow morning, the House Judiciary Committee will mark up a series of antitrust bills that, taken together, would stifle digital innovation and hinder the United States in economic competition with China.

Alec Stapp, Director of Technology Policy at the Progressive Policy Institute (PPI) released the following statement:

“Economic concentration in many sectors of the U.S. economy is a serious issue that demands scrutiny and creative responses from lawmakers. Unfortunately these five bills fail to grapple responsibly with this challenge. Instead, they single out a handful of America’s most innovative and globally competitive tech companies for divestiture and draconian regulation. These bills would be a major blow to job creation and innovation even as our economy struggles to recover from the pandemic recession.

“We hope the Members of the House Judiciary Committee will stand up for American workers, consumers and entrepreneurs by refusing to join in an ideological crusade to dismantle “big tech.” While well-tailored regulation is certainly worth debating, the extreme provisions written into these bills would do more harm than good, and set us back in our fight against foreign dominance in the tech/e-commerce industry.”

Earlier this year, PPI released a new report on job growth in the tech/e-commerce sector, which found that this sector is now the top job creator in the U.S. economy. The sector generated more than 1.2 million net new jobs from 2016 to 2020, including during the pandemic. On average, pay in the tech/e-commerce ecosystem was 44% higher than average pay in the private sector and 21% higher than average pay in manufacturing nationally. The report also found that the growth of tech/e-commerce jobs has expanded beyond the coasts and regions known as tech innovation hot spots, including growth during the pandemic in Arizona, Ohio, Texas, Indiana, and Florida.

TO: Pro-Growth Democrats

FROM: PPI President Will Marshall

RE: How to Lose to China

President Joe Biden says that America is locked in a “strategic competition” with China for global economic and political leadership in the 21st century. Keeping the United States on the leading edge of technological innovation and entrepreneurship is how we win this contest between liberal and autocratic systems.

It’s also the key to generating more good jobs that can help our country close stark income and opportunity gaps at home, as well as demonstrating the strength and resilience of liberal democracy to doubters around the world.

That’s why it’s baffling and dismaying to see some anti-tech Democrats unveil late last week a flurry of bills aimed at breaking up and otherwise handcuffing America’s most innovative and globally competitive companies. These bills narrowly target a handful of large online platforms whose offerings are eagerly sought by people everywhere.

Nonetheless, both right-wing and left-wing populists have drawn a bead on “Big Tech” companies, the former for supposedly muzzling conservatives, the latter for alleged abuses of market power. The bills are based on a tendentious and deeply flawed report by the House Antitrust Subcommittee.

As the Progressive Policy Institute and other analysts have documented, the evidence supporting the report’s claims of systemic antitrust abuses is remarkably flimsy. It mostly consists of misleading anecdotes and alarmism about conjectural rather than actual harms.

In contrast, the benefits Americans get from big internet companies like Google, Amazon, and Apple are tangible and easy to measure. These include lower consumer prices (monopolies typically are supposed to raise them), high capital investment in the U.S. economy, and robust creation of high-wage jobs, a rare bright spot in the pandemic recession. All of these emerge from a hotly competitive and innovative digital ecosystem.

Fresh in the public mind is the essential role the major tech and e-commerce platforms played in keeping the U.S. economy afloat during the pandemic shut-downs. They enabled millions of us to work from home, stay in touch with friends and family, shop online for goods delivered swiftly and safely to our homes, learn and have medical appointments remotely, and entertain ourselves while homebound.

Of course, private companies are run by humans, not saints, and some will make errors or cheat to gain competitive advantage. Large and powerful companies of all kinds certainly merit close scrutiny, as well as government penalties and regulation if they break the law. But on close examination, the populist indictment singling out a few “Big Tech” firms mostly boils down to a vague discomfort with bigness itself.

That’s not enough to justify wrecking the most vibrant part of the still-recovering U.S. economy. We urge pragmatic Democrats to stand firm against these ill-conceived bills and instead craft well-tailored remedies where there is solid evidence of antitrust violations or other public harms arising from market concentration.

In short, as pro-growth progressives we believe there are two compelling reasons why Democrats should not allow themselves to be stampeded into an ideological crusade to break up America’s most dynamic and successful companies:

First, it would be bad for our country. Hobbling America’s most formidable competitors would be tantamount to shooting ourselves in the foot as the race with China for economic and technological primacy intensifies.

Second, it would be a serious political blunder. With razor-thin majorities in Congress, and a challenging midterm election next year, Democrats shouldn’t let the left’s antipathy to competitive markets, private enterprise, and disruptive innovation — aka economic progress — define their party.

It’s important to note that there is no public groundswell for eviscerating the nation’s leading tech companies. On the contrary, they are highly popular with working and middle-class Americans — including swing voters inkey battleground states that helped Biden win in 2020. The pressure to do so comes mainly from right-wing conspiracy theorists and left-wing academics and activists besotted with anti-capitalist and neo-socialist posturing.

China’s Drive for Tech Dominance

China has made no secret of its determination to be first to scale what President Xi Jinping calls the “global peaks of technology.” The Chinese Communist Party’s (CCP) new five-year plan identifies mastery of cutting-edge technologies as a matter of national security, not just economic development, and allocates massive state resources accordingly.

The plan aims to boost spending on research and development by 7% annually, slightly more than budget increases (6.8%) for China’s military. Premier Li Keqiang has offered state support for speeding development of quantum computing, artificial intelligence, advanced semiconductors, and cloud computing.

The government clearly intends to extend its industrial policy model from manufacturing to vanguard technologies like artificial intelligence, robotics, and semiconductors. That means subsidizing national champions and steering government procurement contracts to Chinese companies. The China Development Bank recently announced plans to deploy $60 billion in loans to 1,000 firms developing key innovations.

According to a Brookings Institution report, China sees leadership in 5G technology and other emerging technologies as a way to expand its global power. Stung by the Trump administration’s blacklisting of Huawei and other Chinese tech companies, Beijing has proclaimed a goal of “technology independence.”

Just how realistic that is in a world of intertwined supply chains remains to be seen. But knowledgeable observers believe we are headed for “bifurcated” U.S. and Chinese digital ecosystems over the next decade. In any case, Beijing has set its sights on being the global standard setter for the next generation of high-tech industries.

In addition to its advantages on 5G, China leads the world in electric car sales and is investing heavily in biotech. Then there are the CCP’s chilling efforts to harness high tech to Xi’s totalitarian political aspirations, such as the use of AI surveillance technology to monitor its people’s “social profile” and modify “antisocial” behavior.

Meanwhile, Chinese hackers who apparently are backed by the central government are unrelenting in their attempts to steal intellectual property from U.S. tech companies

(Microsoft has reported recent attacks on its email server), defense contractors, universities, infectious-disease researchers, and U.S. government agencies.

Unlike the backers of the anti-tech bills, the Chinese understand that competing on a global scale requires large-scale companies. In fact, about half the world’s largest tech companies are Chinese, including Huawei (with 197,000 employees, bigger than any U.S. tech company except Amazon), Alibaba (117,000), and Tencent (86,000).

With strong backing by the Chinese government, these companies all are — like America’s tech giants — making big capital investments in future growth. “If we don’t get moving, they are going to eat our lunch,” President Biden has warned, in making the case for his ambitious jobs and families bills.

Now is the time for Democrats to embrace economic patriotism — and optimism. By boosting public investment in science and applied research, encouraging private companies to boost their capital spending, and unleashing the inventive and entrepreneurial genius of a free people, the United States can out-innovate and out-compete an increasingly repressive China.

But the anti-tech bills released last week point in the opposite direction. They are a formula for losing to China. Democrats and true progressives should reject them.

Progressives are supposed to care about jobs. Yet the collection of anti-tech bills just released by members of the House Judiciary Committee go after the companies and industries that have been the most reliable source of job creation in recent years.

Using the methodology developed in our April 2021 paper, Innovative Job Growth in the 21st Century, we calculate that the tech-ecommerce sector has replaced the healthcare sector as the biggest creator of jobs in the U.S. economy. In the five-year stretch from 2015 through 2020, the tech-ecommerce sector added more than 1.7 million jobs. That’s compared to almost 1.2 million jobs for the healthcare sector, including social assistance.

Moreover, these tech-ecommerce jobs are spread over the entire country. Tech-ecommerce job growth from 2015 to 2020 exceeded healthcare job growth in 36 states, including the District of Columbia. The top ten states for tech-ecommerce job growth start with California, Texas and Washington, but also include Florida, Georgia, Ohio, Pennsylvania and Illinois (see table below).

In terms of jobs, the top tech-ecommerce companies compare well to the great manufacturing companies of the past. The top five tech-ecommerce firms—Apple, Alphabet, Microsoft, Facebook, and Amazon—employed 1.8 million workers globally as of early 2021. By comparison, the top five industrial firms by stock market value in the peak manufacturing employment year of 1979—GM, GE, IBM, Kodak, and Dupont—had a total global employment of 1.9 million, just slightly more.

What about pay? The average annual pay in the tech-ecommerce sector is higher than average annual pay in healthcare in every state except for one (Oklahoma). This includes all positions and roles, across the whole universe of tech-ecommerce jobs, from fulfillment center workers to software developers. Average tech-ecommerce pay is higher than average manufacturing pay for 43 states, including the District of Columbia.

Note that these figures include a large number of non-college workers. Our analysis of government data shows that roughly 40% of workers in tech-ecommerce industries have less than a bachelor’s degree. On average, they are earning at least as much or more as they would be making in manufacturing, with the big difference that tech and e-commerce firms are hiring non-college workers without experience at a much faster rate than manufacturers are.

As the saying goes, if it ain’t broke, don’t fix it. Progressives should appreciate the job creation record of the tech-ecommerce companies rather than trying to break them up.

Top states for tech-ecommerce job creation

Job change, thousands, 2015-2020

Tech-ecommerce

Healthcare and social assistance

California

331.8

267.7

Texas

170.7

109.8

Washington

107.1

40.2

Florida

100.8

95.1

New York

85.4

142.6

Georgia

63.9

39.4

New Jersey

61.7

5.9

Ohio

60.4

6.0

Pennsylvania

57.2

56.6

Illinois

57.0

6.3

North Carolina

51.3

16.7

Arizona

46.8

56.8

Colorado

41.9

22.6

Virginia

40.4

16.7

Tennessee

37.1

16.5

Maryland

35.9

3.4

Massachusetts

34.6

2.6

Indiana

33.8

25.7

Michigan

29.3

-2.5

Nevada

26.3

20.3

Missouri

24.3

18.2

Oregon

24.2

42.8

Utah

24.1

20.2

Kentucky

20.9

11.7

South Carolina

17.8

14.8

Note: The tech-ecommerce sector includes four tech industries and three ecommerce industries. The four tech industries are software publishing (NAICS 5112); data processing and hosting (NAICS 518); Internet publishing and search, and other information services (NAICS 519); and computer systems design and programming (NAICS 5415). The three ecommerce industries are electronic shopping and mail order houses (NAICS 4541); local delivery (NAICS 492); and ecommerce fulfillment and warehousing (NAICS 493).

New legislative package would be a devastating blow to American technological leadership

Today, Members of the House of Representatives introduced a new package of bills aimed at stifling digital innovation through extreme antitrust legislation.

Alec Stapp, Director of Technology Policy at the Progressive Policy Institute (PPI) released the following statement:

“The package of bills proposed by Members of the Judiciary Committee would be a devastating blow to American technological leadership at a time when that leadership is more necessary — and more at risk — than ever. While the current system isn’t perfect — the FTC and DOJ urgently need more resources, for example — our antitrust institutions are part of the overall pro-innovation ecosystem that has enabled the United States to produce technology companies that are the envy of the world. These companies create good jobs for American workers — both directly and indirectly — as well as provide innovative products for consumers around the world.

“It makes no sense to apply a drastically different set of rules to a small handful of companies without clear evidence of consumer harms, and a compelling story for how these new rules would remedy those harms. On the contrary, radical measures such as line of business restrictions and bans on self-preferencing would destroy many of the integrated products consumers currently enjoy.

“Apple would no longer be allowed to make its own apps (the iPhone would arrive out of the box with an empty home screen). Google would no longer be allowed to offer Google Maps on Android devices or use it to show map results in search. Amazon would no longer be allowed to offer generic goods at lower prices (just as Walmart, Costco, and every other large retailer do). It’s hard to see how these rules would benefit anyone other than the small handful of competitors that have been trying to use regulation to kneecap America’s most successful companies.

“Lastly, the bill related to mergers is written so broadly that it would effectively ban all future acquisitions by large tech companies. This might have the unintended consequence of decreasing investment in startups because acquisitions are by far the most common way that founders, investors, and employees earn a return on their equity. Reforms are certainly necessary, especially on issues related to privacy, misinformation, and election interference, but these bills would do nothing to address those concerns and would cause more harm in the process.”

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

While other companies cut back on spending as the coronavirus pandemic took hold last year, e-commerce giant Amazon boosted its domestic capital investments by 75% to nearly $34 billion—and helped set the stage for a robust economic recovery, according to a new report from the Progressive Policy Institute.

KEY FACTS

Capital investment by Amazon and its peers in the e-commerce, broadband and tech industries helps spur job creation, boosts production and distribution capacity and combats inflation by shoring up supply, the report’s authors argue.

In Amazon’s case, the extra investment on property and equipment last year was driven by the need to meet an enormous surge of demand during the pandemic, the report notes.

Those investments put the firm in PPI’s top slot on its list of “Investment Heroes.”

Verizon was second on PPI’s list with $16.1 billion in domestic capital investment last year, AT&T was third on the list with $15.6 billion invested, and Alphabet and Intel rounded out the top five with $14 billion and $12.5 billion invested, respectively.

BIG NUMBER

500,000. That’s how many workers Amazon added in 2020, according to the report.

CRUCIAL QUOTE

“The willingness of these companies to keep spending essentially made it possible for large chunks of the economy to move forward, despite the pandemic,” the report states.

KEY BACKGROUND

Despite its major investments in the U.S. economy last year, Amazon’s business practices have also been the target of criticism. The firm was recently sued by the attorney general of the District of Columbia over allegations that it engaged in anticompetitive practices that “have raised prices for consumers and stifled innovation and choice across the entire online retail market.” Rep. David Cicilline (D-R.I.) said Amazon’s recent purchase of film studio MGM is a sign that the company is “laser-focused on expanding and entrenching their monopoly power.” And that’s not to mention criticism over the way the company handled safety protocols for workers and drivers during the pandemic.

Amazon’s $34 Billion Makes It an ‘Investment Hero,’ Study Says

The e-commerce giant was far and away the leader in U.S. capital spending in 2020, according to a Progressive Policy Institute analysis.

By Peter Coy

Democratic and Republican politicians alike are dumping on Amazon.com Inc. over its ceaseless expansion—marked most recently by its agreement to buy the movie studio with the roaring lion logo, Metro-Goldwyn-Mayer. Representative David Cicilline, a Rhode Island Democrat, says “they are laser-focused on expanding and entrenching their monopoly power,” while Senator Josh Hawley, a Missouri Republican, tweets that Amazon “shouldn’t be able to buy anything else. Period.”

But not everybody is mad at Amazon. A new study from the Progressive Policy Institute, which was founded in 1989 as a centrist Democratic think tank and promises “radically pragmatic thinking,” calls Amazon its No. 1 “investment hero.” It estimates that Amazon boosted its U.S. capital spending by 75% in 2020, to $33.8 billion, from the year earlier, which was more than twice that of any other company.

The study names 25 investment heroes based on their U.S. capital spending. The rest of the top five for 2020 are Verizon Communications, $16.1 billion; AT&T, $15.6 billion; Google’s parent Alphabet, $14 billion; and Intel, $12.5 billion.

“The willingness of these companies to keep spending essentially made it possible for large chunks of the economy to move forward despite the pandemic,” says the report. “Investment by broadband and tech companies kept people connected at home during the shock of the lockdown; and the investment by e-commerce firms helped keep essential goods flowing while many Americans could not go out shopping.”

The report is by Michael Mandel, the institute’s chief economic strategist, and Elliott Long, a senior economic policy analyst. Mandel was chief economist of BusinessWeek, the predecessor to Bloomberg Businessweek (making him my former boss). He is also a senior fellow at the Mack Institute for Innovation Management of the Wharton School at the University of Pennsylvania.

Critics of Amazon say it costs jobs by putting smaller retailers out of business. But in an email exchange, Mandel wrote that “the number of workers added by e-commerce exceeds jobs lost by brick and mortar.” The main reason, he wrote, is that e-commerce customers are creating jobs for drivers, warehouse workers, and others, who are freeing them from having to shop in person. “Investment in e-commerce is job-creating because it replaces unpaid household shopping hours, which have fallen dramatically,” Mandel wrote.

This is the 10th annual edition of the investment heroes report by the Progressive Policy Institute. It’s based on gross investment—i.e., before accounting for the effects of depreciation. The numbers come from company reports. The authors made estimates when the companies didn’t break out U.S. investment separately. Most financial companies, excluding health insurance companies, were excluded. For Amazon, which relies heavily on finance leases, the report included principal repayment on those leases as a form of investment.

The report takes a shot at critics in the camp of Cicilline and Hawley, without naming names. “It seems odd that Congress seems more interested in sharply questioning companies that are investing heavily in America, rather than those that have reduced investment or actually disinvested in this country,” it says.

The Progressive Policy Institute gets general funding from some of the companies on the heroes list, Mandel wrote in an email. But he says “the methodology only uses publicly available data and a consistent procedure that can be replicated.”

The MGM deal was announced after the report was completed. (Acquisitions don’t count toward companies’ capital spending numbers in the report.) In an email, Mandel wrote, “This deal potentially increases the level of competition in the growing market for streaming content. The key is to watch Amazon’s investment behavior. If Amazon invests in producing more content based on MGM intellectual property, as seems likely, that means lower prices for consumers and more content production jobs.”

In announcing the deal on May 26, the company stated, “Amazon will help preserve MGM’s heritage and catalog of films, and provide customers with greater access to these existing works.” Amazon didn’t immediately respond to a request for comment on this story.