Washington, DC – The House Subcommittee on Antitrust released its long-awaited report today on competition in digital markets. The recommendations include a call to break up tech companies so they can no longer own platforms and offer products and services on them at the same time, something that almost all other retail leaders do and do well.

“The radical proposals set forth in the report would hinder America’s most innovative and globally competitive companies, simply because they are big, and ultimately would harm consumers,” noted Alec Stapp, Director of Technology at the Progressive Policy Institute. “The real problem with antitrust enforcement is that our agencies are underfunded and haven’t addressed the real competition issues in the healthcare and other consumer-facing industries”

“The report just skips over the statistical evidence that these companies lead the sector which has performed better than the rest of the economy in terms of prices, productivity, wages, investment and job growth,” said Dr. Michael Mandel, Chief Economic Strategist at the Progressive Policy Institute. “If you have a car that’s running smoothly, why disassemble it for parts?”

Experts Alec Stapp, Director of Technology Policy and Dr. Michael Mandel, Chief Economic Strategist at the Progressive Policy Institute are available for commentary. For more information or to speak with Alec or Michael, please contact Ryan@RokkSolutions.com.

The Covid-19 crisis has put a spotlight on how archaic government systems are failing to keep up with the times and handle an unexpected surge of applications for public assistance programs. Cybersecurity threats have demonstrated vulnerability in aging government IT systems. New missions and requirements for government technology capability have shown the limitations of 20th century technology systems and resources for addressing 21st century needs.

The scale of the problem is massive. According to our estimates, federal, state and local governments would have needed to spend an accumulated $316 billion more over the past 20 years to have kept up with the growth of software investment per worker in the private sector. This should be viewed as a lower bound on the shortfall in government IT investment, as this figure excludes hardware investments that also should have been made.

Washington needs to build incentives inside government for a technology culture of continuous improvement and innovation to keep up with external technology developments and changes. Absent such a major modernization strategy, government will become less and less functional in our everyday lives. We need a big push to modernize government, using new digital tools not only to deliver services more efficiently, but to reengineer public services to make them more citizen-friendly and empowering.

To meet public expectations for the kind of speed, versatility, accuracy and efficiency that Americans experience in the non-governmental aspects of modern daily life, we must once again reinvent government just as we did 25 years ago at the beginning of the internet age.

Congress has tried to provide critical relief to Americans during the Covid-19 pandemic — passing three phases of disaster relief totaling 13.6 percent of GDP — but the rollout of support has been marred by obsolete IT and bureaucratic culture.1 In June, the House Ways and Means Committee estimated between 30 to 35 million stimulus checks had yet to be issued.2

The initial rounds of the Paycheck Protection Program (PPP) also were plagued by institutional delays, internal IT system crashes and incomplete, inaccurate and lagging databases. An April 2020 survey by the National Federation of Independent Business found that 28 percent of small business owners were unsuccessful in submitting an application for funds.3 The Small Business Administration’s loan processing system, known as E-Tran, crashed twice in April, frustrating lenders and small business owners seeking relief.45

State governments have also stumbled. For example, unemployment offices have been stretched thin as roughly 58 million Americans have filed claims since March.6 In Washington State, only 41 percent of claims had been paid as of July 30.7 Florida’s unemployment website has crashed repeatedly, with phone calls to the office going unanswered8, and citizens complaining of lengthy delays. Frustrated workers in Oklahoma and Kentucky have camped out overnight in front of unemployment offices for answers.9

Government IT Woes Predate COVID

The COVID-19 crisis is just the latest example of a chronic issue plaguing government programs at the state and federal levels. Poor information technology infrastructure and practices, antiquated and siloed systems, and outdated databases, have led to three main issues: security vulnerabilities, poor user experience and lengthy delays for citizens interacting with their government.

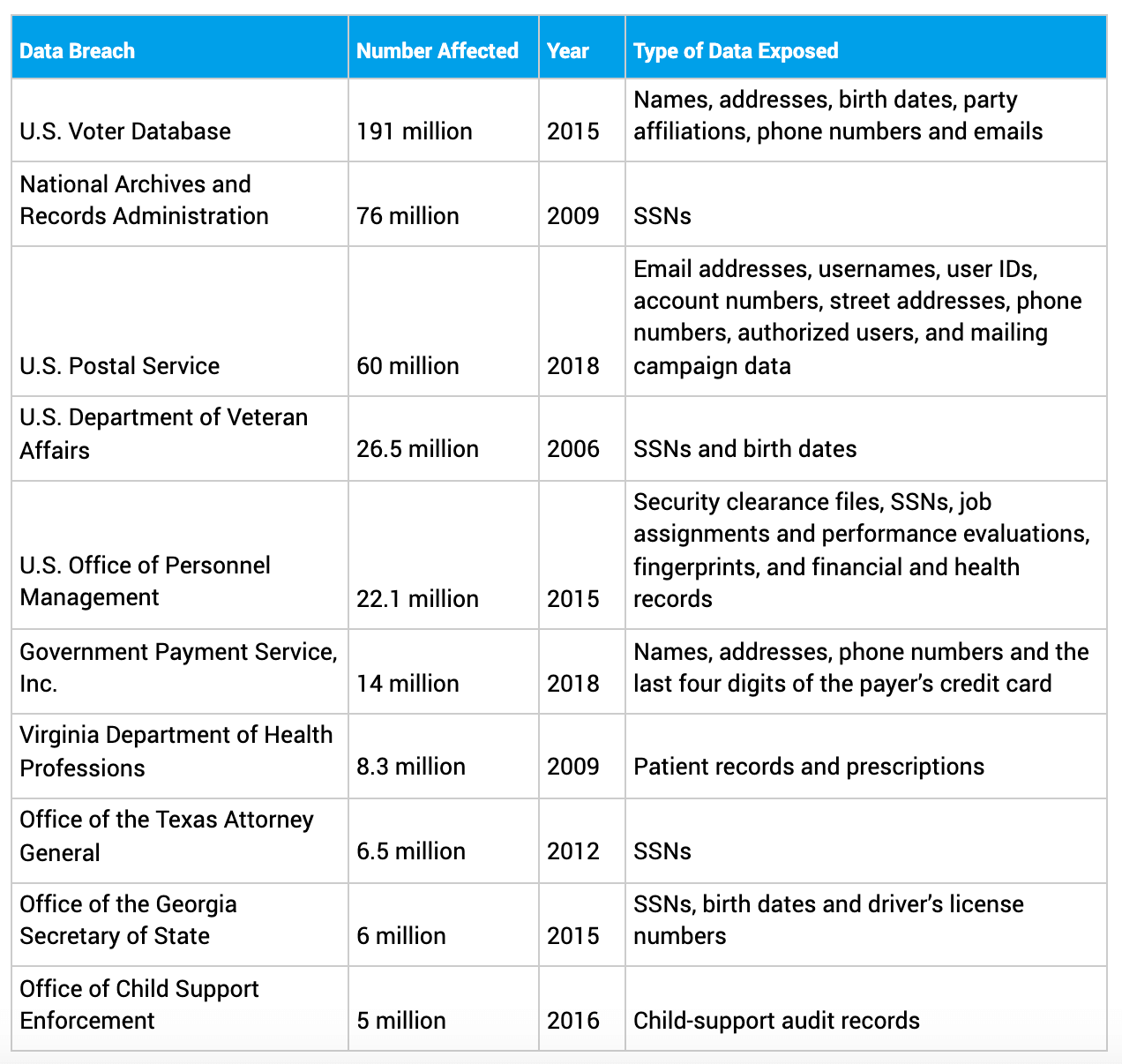

On the question of data security, perhaps the most infamous case is the data breach of the U.S. Office of Personnel and Management (OPM) in 2015 by hackers working for the Chinese military.10 The incident affected 22.1 million Americans and included data on security clearance files, Social Security numbers (SSNs), job assignments, performance evaluations, fingerprints, and financial and health records.

Most disturbingly, data missing from the OPM database could potentially be used by foreign spy services to uncover CIA operatives working under diplomatic cover, as Ellen Nakashima reported for TheWashington Post: “Names that appear on rosters of U.S. embassies but are missing from the OPM records might, through a process of elimination, reveal the identities of CIA operatives serving under diplomatic cover.”11

But while the OPM hack may have attracted the most attention in recent years, it wasn’t even the largest hack of U.S. government data in terms of the number of people affected. As shown in the table below, data breaches of the U.S. Voter Database, the National Archives and Records Administration (NARA), and the U.S. Postal Service (USPS) each affected more than 50 million Americans.

Table 1: Largest Government Data Breaches

Source: Government Accountability Office

15 In addition to data breaches, government databases are often inaccurate and out of date, leading to ineffective performance. For example, the IRS taxpayer database contains incomplete and aging data, which resulted in improper payments in PPP benefits to large numbers of dead taxpayers, returned payments that were misdirected, and even funds sent abroad to foreign citizens of other countries. 1213

Currently, the U.S. government spends the vast majority of its IT budget on maintaining and operating older legacy systems rather than upgrading and modernizing them. A 2019 Government Accountability Office report found that 80 percent of the $90 billion the federal government planned to spend on IT in 2019 would be used to operate and maintain existing systems.14 As shown in the table below, the report concludes that there are 10 legacy systems most in need of modernization, a few of which are more than 45 years old. One system at the Department of Education still runs on Common Business Oriented Language (COBOL), a programming language first introduced in 1959.

COBOL was originally designed for mainframe computers. While it has mostly died out in the private sector as businesses have transitioned from owning on-premise mainframe computers to renting cloud computing services from Amazon, Microsoft, or Google, COBOL has been in the news recently as government relief programs struggle to cope with surging demand.16

Government systems still rely on this outdated technology for essential services. At the state level, COBOL has been used to keep unemployment insurance programs running continuously for 40 years (34 state unemployment systems still depend on it today).1718 And during the current crisis, New Jersey’s governor put out a call for volunteers fluent in COBOL to help fix the state’s computer systems.19 Data from Indeed, a job listings search engine, showed a massive increase in search interest for “COBOL” in April.20 But there is a real risk these calls for help will go unanswered. COBOL is only the 43rd most popular programming language as of this year and the average age of a COBOL programmer is about 55-years-old.2122

Why haven’t millions of people received their economic impact payments from the IRS yet? COBOL seems to be the culprit there, too. Many Americans encountered error messages (“Payment Status Not Available”) when they tried to find out why they hadn’t received their stimulus check yet.23 The solution? Using only uppercase letters in the form (and if that didn’t solve the issue, people were advised to try abbreviating words like “Street” and “Avenue”).

But the problems are not just limited to outdated programming languages. The IRS has a profoundly outdated and inaccurate taxpayer database and its systems are unable to talk to each other. John Koskinen, the Commissioner of the IRS from 2013 to 2017, testified on multiple occasions in Congress, and made other public statements, about the dangerously outmoded condition of the agency’s IT infrastructure, even citing existing systems that date back to the Kennedy Administration.24

Other government processes are also antiquated. In New York, newly unemployed workers are required to fax in documentation.25 In some states, people can file for unemployment online, but only from a desktop or laptop computer.26 The state websites, it turns out, aren’t mobile-friendly — a significant barrier for the millions of people whose only internet access is via their smartphones.27 And some states, such as Illinois, even shut down their websites for multiple hours every day.28

A Decades-Long Investment Shortfall

These problems with the government’s digital infrastructure didn’t arise overnight. Technical failures of this nature are the inevitable result of an accumulating investment deficit over recent decades. According to a Progressive Policy Institute analysis of Bureau of Economic Analysis data, federal and state government investment in software per worker significantly lags behind private sector investment.2930

As the pandemic recession grinds on, the federal and state governments must invest more in digitizing their operations if they are going to deliver aid faster and more accurately. U.S. officials should study the example of Estonia, which has digitized 99 percent of government services, including online voting, an e-residency platform that allows businesses across the European Union to establish and manage a business online, and a nationwide system of digitally-kept health records.31323334 Estonian officials estimate that digitizing these processes saves the country two percent of its Gross Domestic Product a year in salaries and expenses, roughly what it pays to meet its military obligations to NATO.35

The federal government has a Technology Modernization Fund, but it’s only been allocated $125 million since 2017 when it was created.3637 In its big relief bills (such as the Paycheck Protection Program and the CARES Act), Congress included funds for agencies to upgrade their technology systems. For example, the bills allocated nearly $3 billion to the Small Business Administration that could be used to upgrade and modernize its IT systems. But much of the money has gone to hire outside contractors rather than to acquire new technology. For instance, the Small Business Administration awarded RER Solutions $500 million for data analysis and loan recommendations as part of Covid-19 relief.38 Sufficient in-house technology systems would both limit the potential for breaches to occur and be a more prudent use of taxpayer money rather than continuously “renting” delivery systems.

For too long, the U.S. public sector has been a laggard in adopting the modern digital technologies that the rest of society have. That’s mainly been the result of underinvestment. To close this public-private technology gap, the federal and state governments need to invest more in software and systems improvements to ensure aid is rapidly delivered during the next crisis.

Government IT Needs Both Incremental Modernization and End-to-End Modernization

All of these issues might make it seem like the best approach is to tear everything out root-and-branch and start over. And while end-to-end modernization strategies might make sense in some cases, for the most essential government systems, an incremental strategy is actually best because it minimizes risks to essential services and limits downtime for users. As Alasdair Allan, a computer scientist at the Raspberry Pi Foundation, pointed out, legacy software systems have accumulated decades of solutions to corner cases and bug fixes. Starting from scratch would be a mistake:39

You should (almost) never rewrite from scratch, and (almost) never throw the legacy system away, it is your institutional knowledge. A legacy software system is years of undocumented corner cases, bug fixes, codified procedures, all wrapped inside software.

If you start from scratch you will miss things. There is no guarantee that you will end up in a better situation, just a different one. I have yet to speak to anyone that has been involved with a project to reimplement a large legacy code base from scratch that has anything good to say about the idea. Document, improve the build system, modernise the infrastructure around it. Write tests. But do not throw it away.

Modern programming languages can be used to deliver social services on modern devices (e.g., smartphones) while sitting on top of the existing mainframe servers. This approach would drastically improve the user experience while preserving the accumulated knowledge. But what might this look like in practice and where should the government start?

Start Small: Public-Private Partnerships and Pilot Projects

One area the federal government can look to improve incrementally in terms of delivery via information technology is anti-poverty programs. Low-income families spend inordinate amounts of time and energy running from one social service agency to the next to apply for public assistance. Now, with many offices shut down, social distancing, and intermittent mass transit, that job is harder than ever. The opportunity costs of simply applying for and receiving public support have risen dramatically. We need to use new digital tools to reduce those costs by empowering low income people to apply once online and receive benefits on an ongoing basis.

Over time, government IT systems have accrued a lot of technical debt — the cost of future work caused by choosing an easy, short-term fix.40 Solving these problems won’t be easy. But a step in the right direction would be passing the Health, Opportunity, and Personal Empowerment (HOPE) Act.41

As Joel Berg detailed in a white paper for PPI in 2016, the HOPE Act would jumpstart the modernization of social services with pilot projects and innovation contracts.42

“Currently, low-income families need to navigate a morass of bureaucracy to receive the benefits they need and deserve, including SNAP, WIC, and UI benefits. Filling out the requisite forms often requires waiting in long lines and traveling to far flung offices. For example, for residents of Panola, Alabama, the closest location to get a driver’s license is a 70-minute drive away.For more complicated processes, recipients often need to hire professionals to help them secure financial assistance from the government.

A 2016 PPI study found that low-income workers paid an average of about $400 each to national tax preparation storefront chains in low income neighborhoods.43 A better alternative would be to move all these services online and make them accessible from a single smartphone app.”

Nevertheless, the government — at both the federal and state and local levels — does not have a good track record of building large scale transactional systems. Moreover, poor customer experiences have too often resulted from government attempts to mimic the online transactional processes and consumer interfaces the public has come to expect from their daily experiences with private sector innovations. And as we’ve shown, the government has a big task ahead in fixing its current systems, in terms of financial resources, managerial resources, and tech talent resources.

However, the needs of the country also cannot wait for notoriously lengthy public procurement cycles to solve these problems. Just getting through the phases of systems design, specifications, and competitive procurement for major systems would take 5-10 years, while implementation of awarded contacts would take 5-10 years more, with high risk of obsolescence by the time of deployment. Successful government reinvention will therefore require reinvention of processes and strategies for service delivery in order to rapidly meet public expectations for performance. Innovative public-private partnerships, with appropriate public safeguards, should be a cornerstone methodology for government reinvention in the 21st century.

With all of that in mind, new online service delivery platforms could be provided via multi-sourced public-private partnerships – including those at no cost to either the public treasury or individual users — which would allow the government to harness the private sector’s technology capabilities and IT infrastructure, with a declared objective of creating an environment of continuous innovation and improvement. The government could then create supporting national public communications campaigns, down to the community level, to inform the public about the availability of these service platforms, so the working poor can know there is are free online, government-sponsored and regulated alternatives available to them.

According to Berg, the HOPE Act can help make this better alternative a reality:44

“Here’s how HOPE would work: The President and Congress would need to work together to enact a law that would authorize the federal Departments of Health and Human Services (HHS), Housing and Urban Development, (HUD), Treasury, and Agriculture (USDA) to work together – and to form public/private partnerships with banks, credit unions, and technology companies – to create HOPE accounts and action plans that combine improved technology, streamlined case management, and coordinated access to multiple federal, state, city, and nonprofit programs that already exist. States and localities would initially be asked to participate in pilot projects implementing the accounts and plans, and, if they work, would be required over time to implement them universally.”

The program would only cost $35 million in its initial stages and would go a long way to showing the potential benefits of bringing government tech into the 21st century. As Berg says, “In America, trying to get out of poverty can be a full-time job.”45 In normal times, this is a tragedy. In a pandemic, when tens of millions are at risk of becoming impoverished for the first time in their lives, this is a national emergency.

The HOPE Act can serve as the first step in a radically pragmatic approach to modernizing government IT. Senator Kirsten Gillibrand and Representative Joe Morelle have been leading the effort to include this bill in the Phase 4 relief package for the COVID crisis and low-income Americans need this change now more than ever.46

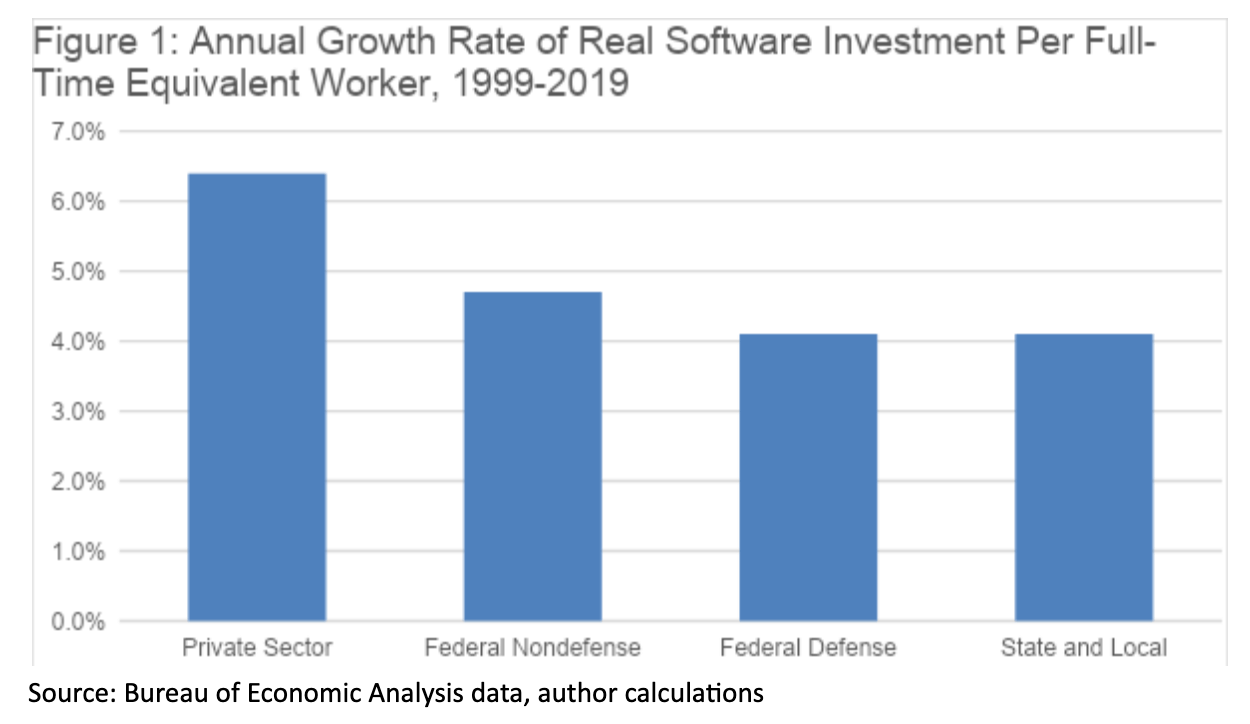

A big part of the problem is that government investment in software has not kept pace with the private sector. As Figure 1 shows, real private sector investment in software per full-time equivalent (FTE) worker increased at an annual growth rate of 6.4 percent over the last 20 years. Meanwhile real investment in software per FTE worker grew at a noticeably slower rate of 4.7 percent for federal nondefense, 4.1 percent for federal defense, and 4.1 percent for state and local governments.

If the federal nondefense sector had kept pace with the private sector, software investment in 2019 would be 38 percent, or $10.7 billion higher (Table 2). Software investment in the federal defense sector would be 55 percent higher, and state and local government software investment would be 54 percent higher.

Table 2: The 2019 Software Gap (billions)

Actual software investment

Necessary software investment*

Size of the gap

Federal Nondefense

28.3

39.0

38%

Federal Defense

12.6

19.5

55%

State and Local

20.1

31.0

54%

*assuming that real software investment per FTE had kept up with private sector

Data: BEA, PPI

But that’s not the worst of it. This gap has accumulated over time, as year after year the government has spent less than it should have. According to our estimates, the accumulated shortfall in government software investment since 1999 has totaled $316 billion. As Table 3 shows, federal nondefense, federal defense and state and local governments would have invested an additional $123.6 billion, $89.5 billion, and $102.5 billion, respectively, to match the private sector’s pace over the last 20 years. This should be viewed as a lower bound on the shortfall in government IT investment, as this figure excludes hardware investments that will also need to be made.

Table 3: Accumulated Shortfall in Software Investment, 1999-2019 (Billions)

Federal Nondefense

$123.6

Federal Defense

$89.5

State and Local

$102.5

Total

$315.6

Source: Bureau of Economic Analysis data, author calculations

*See Methodology Appendix

While the task of modernizing government technological capabilities may seem immense, it pales in comparison to the opportunity cost of not acting at all. A Technology CEO Council report highlighting opportunities for innovation in government use of technology estimated the federal government alone could save $1.1 trillion over the next decade in areas like fraud and improper payments prevention, big data and analytics, mobile, and cybersecurity.47 For example, the federal government is forecast to make $117 billion in improper payments in FY 2020 and has made over $1 trillion in improper payments since FY 2012.48 Technology CEO Council estimates “the federal government could reduce improper payments by approximately $270 billion over 10 years” by employing techniques like when IBM implemented predictive analytics for New York State, which resulted in the prevention of $1.2 billion in improper tax refunds.49

Cybersecurity is another area where modern technology can save taxpayer money. A study by the Ponemon Institute found the United States to have the highest average cost for a data breach in 2020 at $8.64 million.50 Public-private partnerships can help federal, state and local governments avoid expensive cybersecurity attacks. IT security company Akamai helped the U.S. State Department move to a secure cloud-based web presence that successfully protected the agency from one of the largest Distributed Denial of Service (DDoS) attacks on U.S. government websites to date.51

Once again, public-private-partnership is an essential part of a 21st century cyber defense strategy. A good example is the Treasury/IRS Security Summit and ISAC, which was created by IRS Commissioner Koskinen five years ago, in concert with the private sector. This Treasury/IRS initiative has thus far reduced identity theft tax refund fraud by 80.52 This innovative strategy to defend the tax system against international cyber-attacks should be studied as a model for other government agencies who hold sensitive information and billions in public assets.

Conclusion

The Covid-19 pandemic has shed a light on the obsolete systems used by federal, state and local governments to deliver relief. When time was of the essence, the federal government stumbled in delivering stimulus checks and PPP loans efficiently and accurately. State governments were ill-equipped to process the unprecedented surge in unemployment applications. To be sure, government IT issues predate the pandemic, as federal and state systems have been routinely compromised by data breaches.

The root cause of these IT problems is a decades-long shortfall in government infrastructure investment. For example, the overwhelming share of the federal government’s investment in IT is spent on operating and maintaining outdated legacy systems, some of which are more than half a century old. But the solution isn’t to maintain obsolete systems that aren’t secure and don’t serve their purpose anymore; the solution is for governments to invest in modernization and digitization. Governments should start with pilot projects and partner with the private sector where possible. The HOPE Act would represent a down payment on the $316 billion we estimate federal, state and local governments has fallen behind the private sector. Likewise, modern public-private partnership strategies would enable government to leverage private sector investments and infrastructure to apply them to public purpose.

Methodology Appendix

Data from the Bureau of Economic Analysis enables us to calculate real software investment per full-time equivalent worker for the private sector, the federal nondefense sector, the federal defense sector, and the state and local sector. As shown in Figure 1, the growth rate was substantially faster in the private sector compared to the three government sectors.

We then calculated how much higher software investment in the three government sectors would have needed to be in each year since 1999 to match the growth rate of real software investment per FTE in the private sector. We then translated this increase into nominal dollars and summed over the twenty-year period to get the total shortfall. The 2019 figure gives the current gap reported in Table 2.

This estimate should be regarded as a rough measure of the amount of “software debt” that the government has built up. Ordinarily we might not worry about a lack of spending 10 or 15 years ago because of depreciation, but the government has spent far too much money holding legacy database systems together with scotch tape.

The other issue is hardware. The data published by the BEA for government spending on computers includes “consumption expenditures” as well as investment, so it doesn’t quite correspond with private sector investment in computers. It is generally agreed, however, that even in the era of cloud computing that the government needs to modernize its hardware.

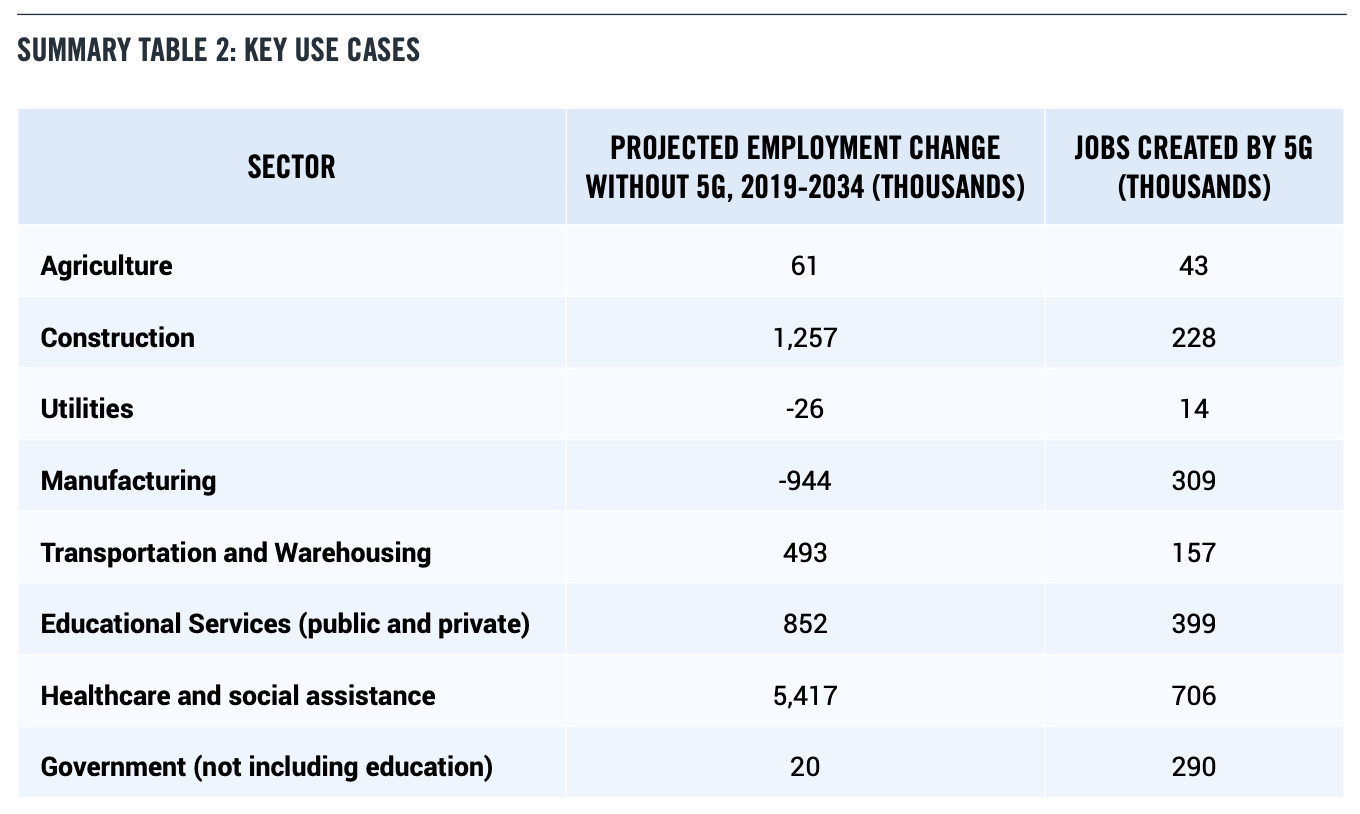

In a new paper, the Progressive Policy Institute, working with the National Spectrum Consortium, projects that applications of 5G will create 309,000 manufacturing jobs in the United States over the next 15 years. That’s only a small part of the 4.6 million jobs that 5G is expected to create over that period, according to the paper, “The Third Wave: How 5G Will Drive Job Growth Over the Next Fifteen Years,” which I co-authored with Elliott Long.

The application of 5G to manufacturing is especially important because the new communications technology has the potential to jumpstart a lagging sector. Yes, it feels funny to call manufacturing a lagging sector, but that’s the only way to describe it. Even before the pandemic, labor productivity decreased in 18 of the 21 NAICS 3-digit manufacturing industries in 2019, according to a recent report from the Bureau of Labor Statistics. Output grew at a crawl.

The benefit of 5G is that it allows a much faster digitization of the physical transformation processes that lie at the heart of manufacturing. A 2019 McKinsey analysis observed that “[f]or decades, factory automation has relied on programmable logic controllers (PLCs) that were physically installed on (or very near) the machines they controlled, and then hard-wired into computer networks to ensure precise, reliable control under extreme conditions. If 5G consistently meets its performance promises, the PLC could be virtualized in the cloud, enabling machines to be controlled wirelessly in real time at a fraction of the current cost.” Not only will costs be lower, but flexibility will be improved.

5G, because of its low latency and high throughput, won’t just be an evolution in technology, but a revolution. It will open the door to incredible innovation in both the private sector and the government – including augmented and virtual reality, precision agriculture, smart ports, transportation and logistics, autonomous vehicles, connected construction and so much more.

In the United States, it is critically important to understand how this fundamental shift in technology will impact the broader economy, especially at a moment when COVID-19 has caused significant economic disruption and massive job losses nearing Great Depression levels. Key questions include:

How many jobs will be created by the 5G Economy? Will they be focused around traditional technology centers like San Francisco, New York, and Boston, or create new opportunities across the nation? What kinds of jobs will be created?

And for policymakers, what does the U.S. need to do to support efficient allocation of radio spectrum to support this technology development? And should we provide job training to ensure that workers in America can meet the opportunity?

Already the 5G job revolution has begun. Large mobile providers such as AT&T and Verizon are building out new networks across the country. Network companies such as Cisco, CommScope, Mavenir, and L3Harris are hiring 5G system architects, Radio Access Network (RAN) engineers, 5G solution architects, and technical managers in the 5G space.

Technicians and tower climbers are putting up 5G small cells at a rapid pace. This is not the first time that fundamental shifts in networking technologies have created sudden shifts in the economy and job opportunities.

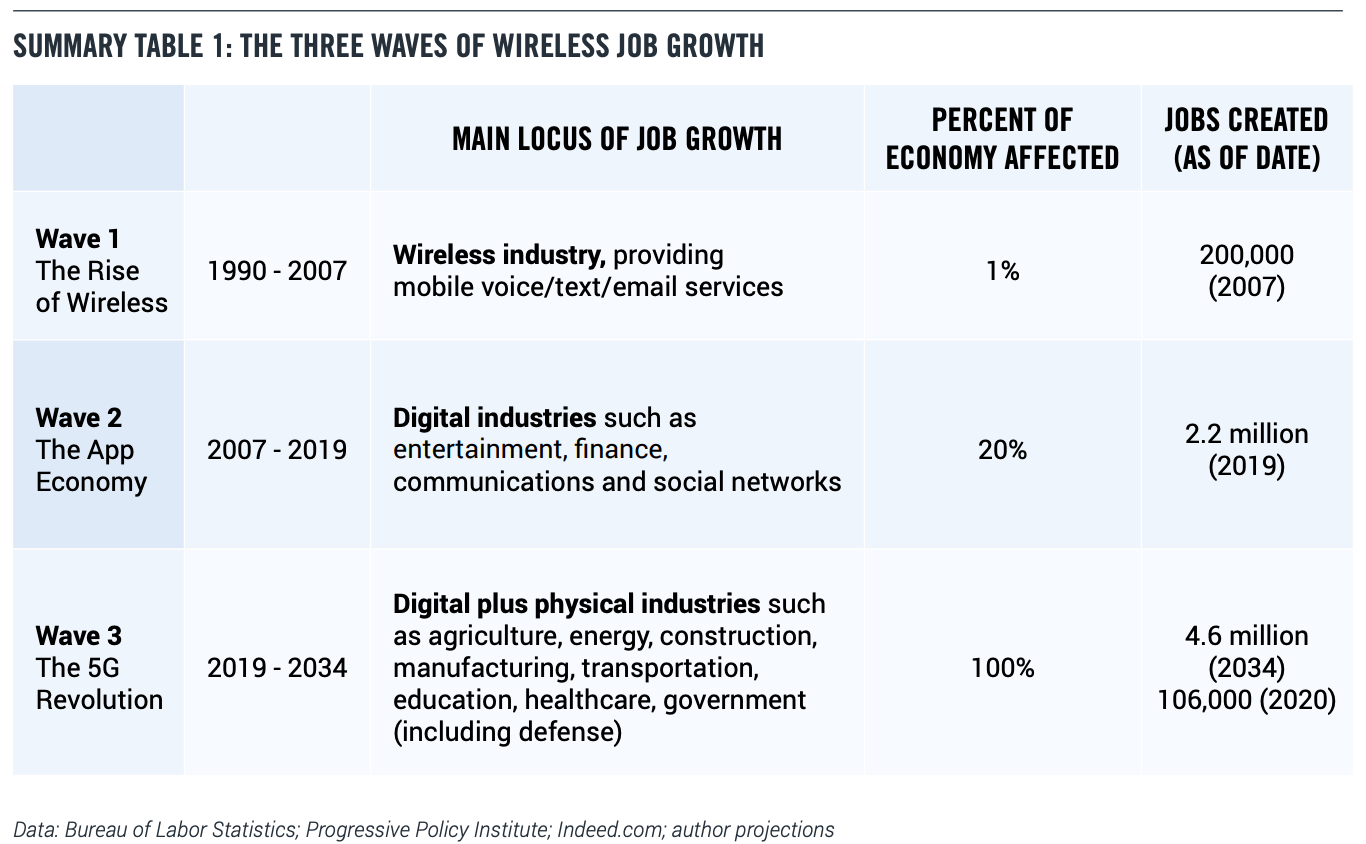

This paper identifies and outlines three waves of wireless-driven job growth (Summary Table 1) in the U.S., and answers major questions about how many jobs will be created, which industries will be affected, where they will be located, and what we can do as a nation to accelerate efforts to meet this challenge.

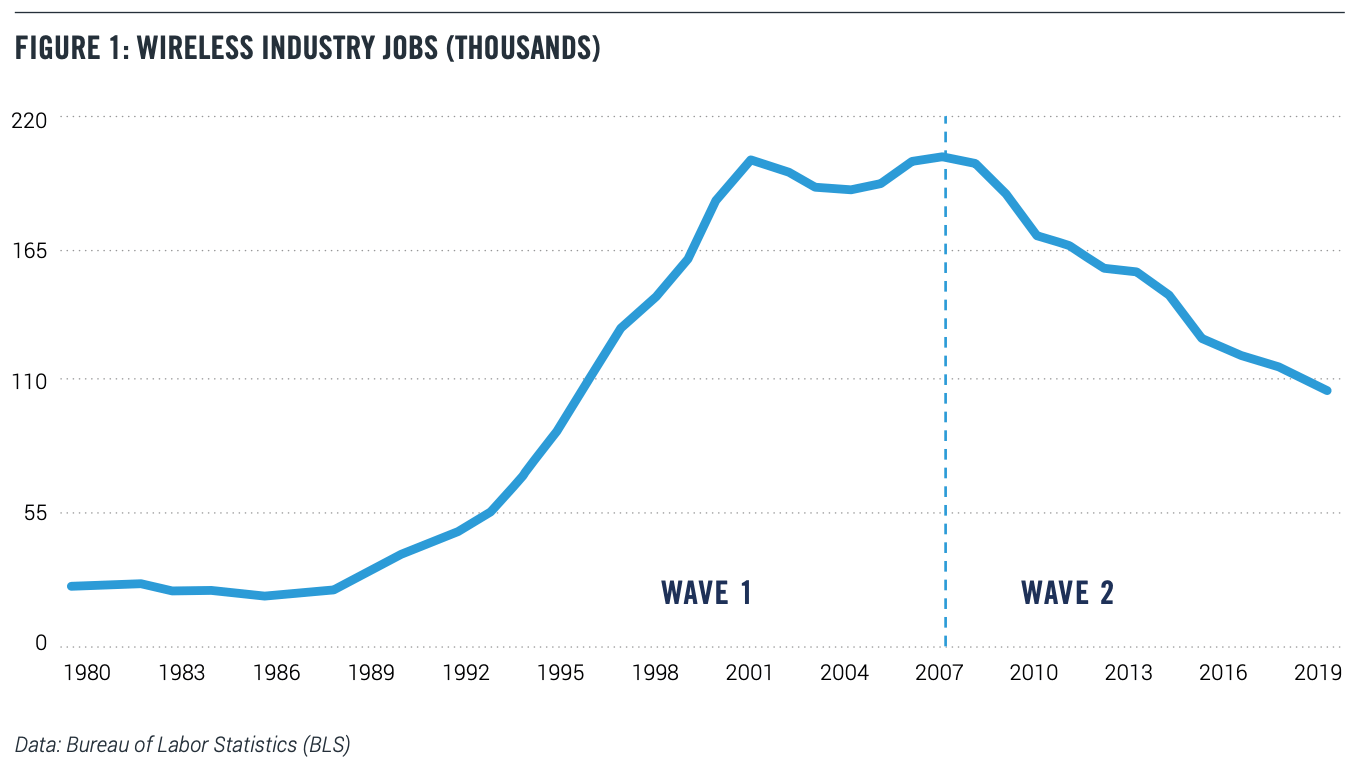

Wave 1, The Rise of Wireless, covers the period from 1990-2007, as mobile carriers were building out the original wireless networks and cell phones went from a rarity to a necessity. Wave 1 generated roughly 200,000 jobs in the wireless industry.

Wave 2, “The App Economy,” covers the period from 2007 to 2019, which was rooted in the application of wireless to mobile apps via smartphones, rather than in the wireless industry.

Conventional BLS statistics contained no categories for app developers. But a widely cited study by this report’s author, released in early 2012, analyzed detailed data on job postings and estimated that the U.S. App Economy included 466,000 jobs, including workers developing and maintaining mobile apps and the workers supporting them. (1) Follow-up studies showed continued growth in the U.S. App Economy, with the latest figures from September 2019 reporting more than 2.2 million App Economy jobs. (2) This reflects an average growth rate of more than 20 percent annually. The main locus of Wave 2 job growth has been in industries such as entertainment, finance, communications and social networks, whose output can be easily delivered in a digital form (hence “digital industries”).

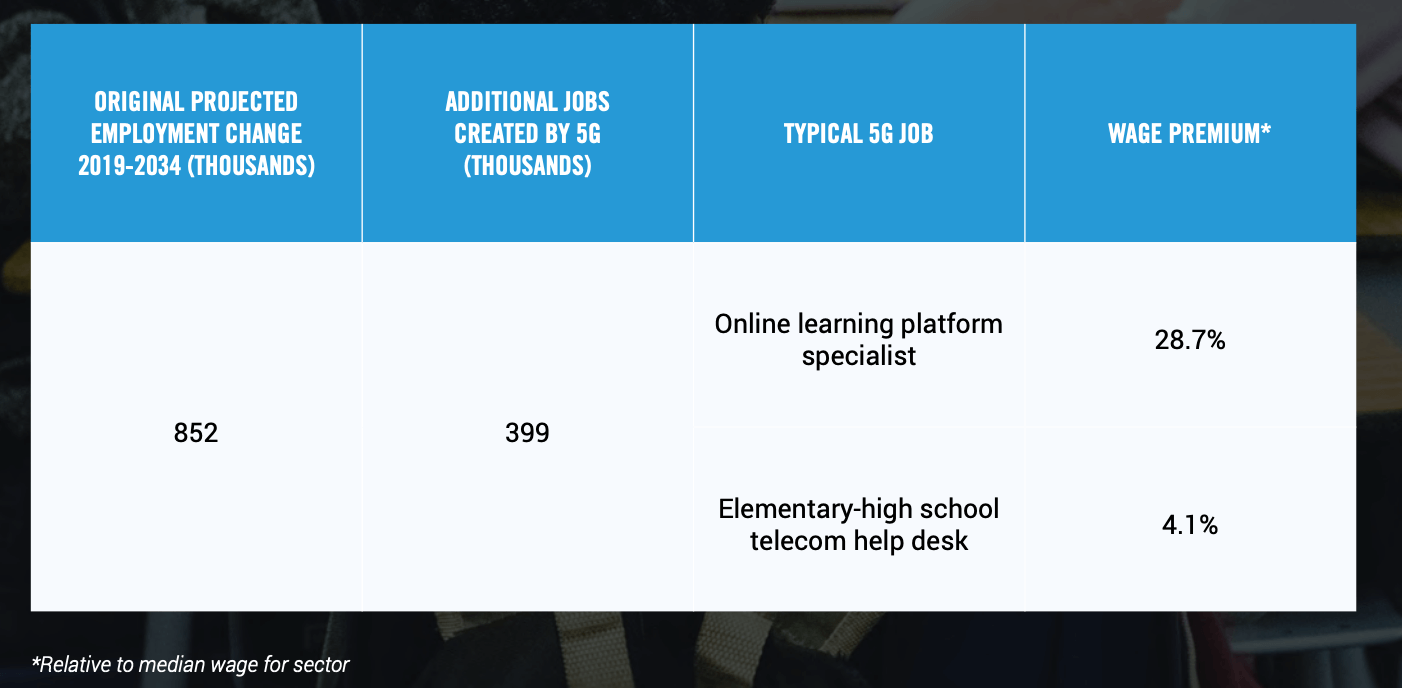

Wave 3, “The 5G Revolution,” began in 2019 as mobile carriers expanded their initial 5G networks. Wave 3 is generated by the applications of wireless to challenges in physical industries, such as agriculture, energy, construction, manufacturing, transportation, education, healthcare, and government including defense.

In recent years, most of these physical industries have experienced low or negative productivity growth, as well as low spending on telecommunications services.

5G is reversing both of these trends. Faster, more versatile wireless communications are an essential factor in driving productivity gains and creating jobs. Research shows that industries like manufacturing, construction, and healthcare have lagged in digitization, helping explain why productivity growth has been so slow. To increase productivity, physical industries need the ability to gather information from widely dispersed sensors and to use that data to control activities in real time. That’s not possible without faster and more versatile wireless commnications supplied by 5G. And the COVID-19 pandemic is accelerating the shift to many of these use cases.

How many jobs in the US will The 5G Revolution generate?

Unlike Wave 2, which mostly generated “cognitive” tech jobs which required a college education, Wave 3 is rooted in the physical world.

As a result, Wave 3 will also create mixed ‘cognitive-physical” skilled jobs, many of which fall into the category of installers and maintainers. So while App Economy jobs were focused on software development, Wave 3 jobs will drive job growth in dozens of sectors, across the economy in what we would traditionally consider both white collar and blue collar positions. Simply put, the third wave will benefit a wider set of Americans and regions than the second wave did.

For example, healthcare providers already monitor medical equipment like pacemakers remotely. But with 5G, the set of possible athome diagnostics or even interventions will expand greatly, and telehealth installers and maintainers will be a highly valued occupation. Similarly, precision agriculture will require “field sensor technicians,” autonomous vehicles will need a cadre of mechanics, and ecommerce will need people skilled in robotics maintenance.

Using the latest BLS projections as a baseline jumping off point, we estimate that 5G and related technologies will create 4.6 million jobs relative to the baseline in 2034, 15 years after the introduction of 5G in 2019 (which is also, not coincidentally, the peak of the most recent business cycle). These are higher paying jobs that will replace jobs that are lost in a wide range of industries and use cases (Summary Table 2).

In an important sense, 5G job creation is a countervailing force to job destruction from automation and globalization, and critically important in the post-COVID world.

During these tough economic times, we also need to be concerned about the short-term job impact and opportunities that 5G is creating as well. This paper also shows that current 5G build-out and engineering activities are creating 106,000 jobs as of April/May 2020. We estimate the location of these jobs by state. To get this estimate, we use a combination of data from real-time job postings and BLS figures.

What Do Policymakers Need to Do?

Finally, this paper identifies four areas where policymakers should focus to harness the full potential of 5G.

First, more spectrum – mmWave, sub-6, and unlicensed – will be needed for broadband and related applications. The U.S. would benefit greatly from a long-range spectrum plan. While the Trump Administration has directed the Department of Commerce to create a National Spectrum Strategy, it has not yet been released.

A long-range spectrum plan would ensure the resource is allocated wisely, provide certainty to 5G stakeholders, and encourage long-term investment in networks for 5G and beyond.

In addition to spectrum, the U.S. also needs a plan for the adoption of 5G across the government, both defense and civilian. The public sector should be a leader, not a follower.

Third, Congress should be willing to invest heavily in the development of 5G and successor technologies. That’s essential if the U.S. is to keep up with global competition.

And finally, the U.S. should make a significant investment in job training. The U.S. needs to double down on traditional STEM fields and encourage more people in America to go into engineering and math. Beyond that, we need a national skills initiative and mentoring programs to ensure that this new generation of workers will have the training needed to support the cognitive-physical jobs that the 5G Revolution is already beginning to create.

I. THE FIRST TWO WAVES OF WIRELESS JOB CREATION

Wireless technologies are generally divided into generations, each one corresponding to higher speed and increased capabilities. 5G is the current technology being rolled out, with 6G on the horizon, promising even faster speeds and satellite-terrestrial integration.

However, for the purposes of this paper we use a different taxonomy, based on the labor market impact of wireless technologies.

Wave 1: The Rise of Wireless

Commercial mobile radio telephony—what is sometimes called “0G”—was available as a niche service since the late 1940s. (3) It had very little economic impact. The first true commercial portable cellphone, the Motorola DynaTAC 8000X, was introduced in 1983, but there were only 5 million cellphone subscribers as of 1990.

But the use of cellular wireless technology rapidly gathered speed after 1990, giving rise to 109 million subscribers as of 2000 and 233 million subscribers as of 2006. Not surprisingly, the need to build out networks, and handle a soaring customer base generated a large number of jobs. The number of people working in the wireless industry went from 36,000 in 1990 to 200,000 in 2000. (4) Wireless employment remained at roughly that level until 2007 (Fig 1).

The first wave of wireless job growth encompasses 2G in the 1990s and 3G and 3G+ in the first half of the 2000s. With 2G data speeds measured in the kilobits, only low-bandwidth applications such as voice, text messages, and email were viable. Running other applications on top of a slow network was almost impossible.

Mobile internet became possible with 3G and 3G+, but it was still not fast enough to make a significant difference.

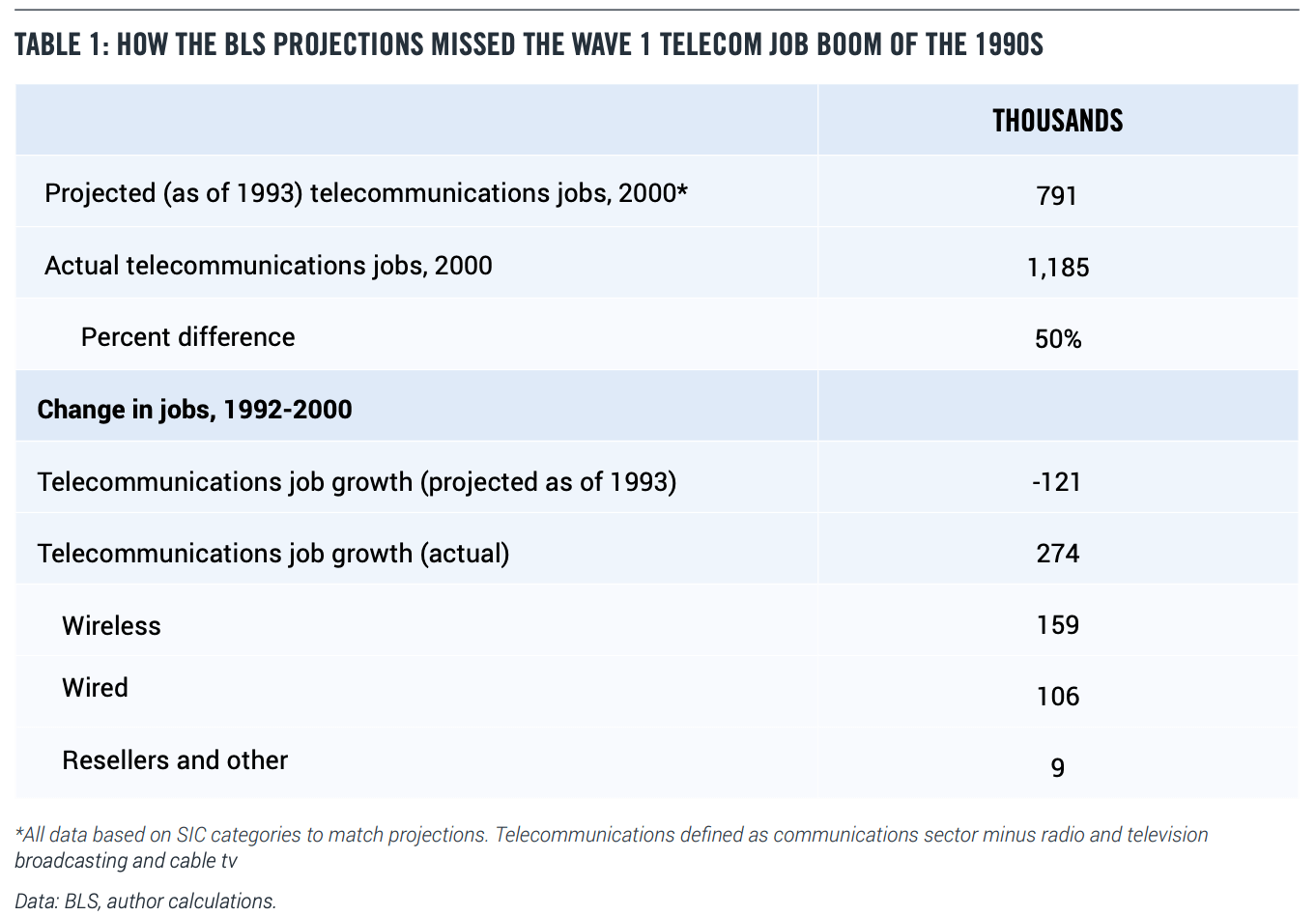

Wave 1, The Rise of Wireless, was not anticipated in any of the long-run employment projections issued by the BLS in the late 1980s and early 1990s. That’s important, because the BLS projections, issued regularly since the 1960s, are the most widely quoted comprehensive long-run occupational and industry forecasts available. The BLS also maintains the most detailed occupation industry matrix available for the United States.

Yet, the BLS projection methodology typically misses the impact of new technologies. For example, the employment projections issued in 1993 anticipated that telecommunications employment would drop from 912,000 in 1992 to 791,000 in 2000. (5) In reality, telecommunications jobs rose to 1,185,000 in 2000, 50 percent above the projected value (Table 1). (6)

Wave 2: The App Economy

The second wave of wireless jobs, The App Economy, began in 2007 with Apple’s introduction of the iPhone, coupled tightly with the opening of the App Store and Android Market (later renamed Google Play) in 2008. Suddenly mobile phone users had a powerful computer in their pockets that could handle a myriad of applications. The demand for mobile broadband soared. Mobile wireless networks moved from faster versions of 3G to 4G and LTE, as the number of broadband subscriptions soared.

But the second wave of wireless jobs also started with a paradox. Despite the central role of mobile, employment in the wireless industry peaked in 2007 and fell by half by 2019. In 2011, the Wall Street Journal ran a piece with the stark title: “Wireless Jobs Vanish.” (7)

In fact, wireless was creating jobs, but not in the wireless industry. (8) More and more IT professionals were involved in either developing mobile apps, maintaining them after they were on the market, or supporting them with users. For banks and other financial institutions, mobile apps became an important way of supplying their services without having expensive real estate or branch workers. Moreover, mobile apps could use the camera on smartphones to provide services like depositing checks at homes.

Beyond utilitarian tasks like banking, shopping, and travel reservations, apps became the major way that people interacted with their smartphones. We watched videos, listened to music or podcasts, messaged friends, played games, and spent time on social networks. One survey found that adult Americans spent almost three hours per day on their smartphones, and 90 percent of that time was spent on apps. (9)

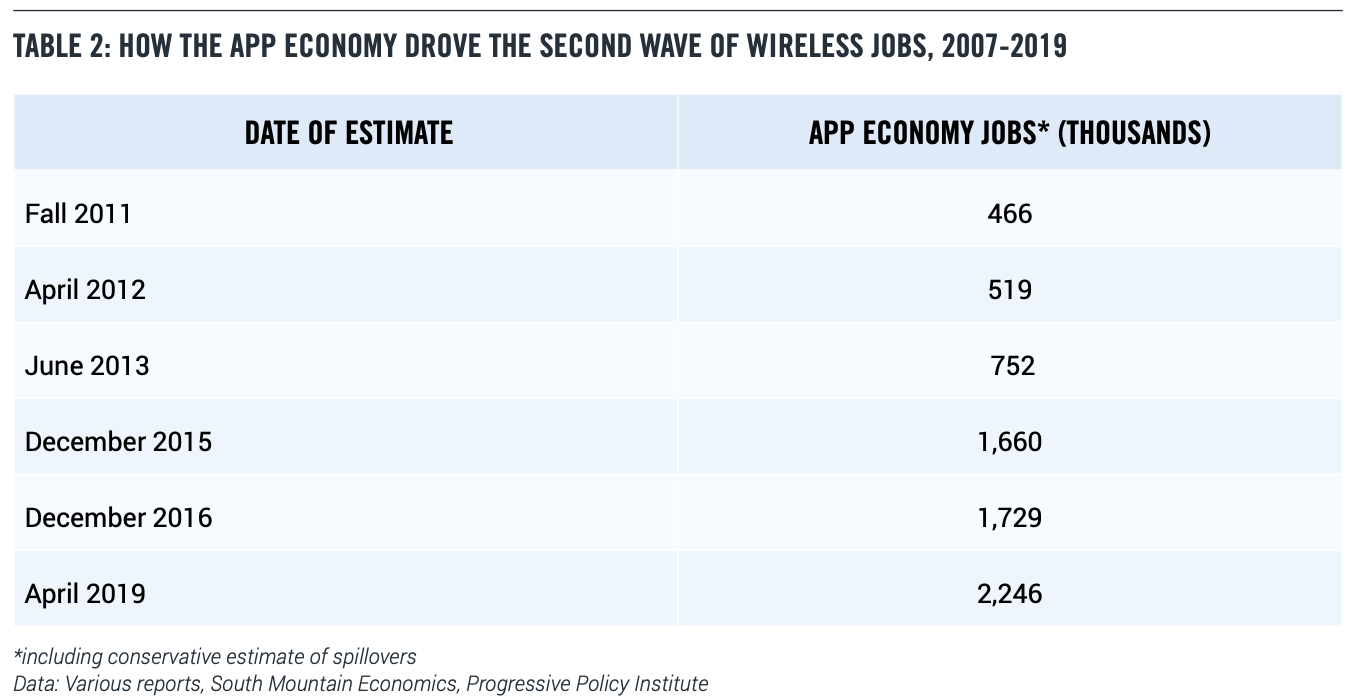

Conventional BLS statistics contained no categories for app developers. But a widely cited study by this report’s author, released in early 2012, analyzed detailed data on job postings and estimated that the U.S. App Economy included 466,000 jobs, including workers developing and maintaining mobile apps and the workers supporting them. (10) Follow-up studies confirmed continued growth in the U.S. App Economy, with the figures from April 2019 reporting more than 2.2 million App Economy jobs. (11) This reflects an average growth rate of more than 20 percent annually (Table 2).

Other studies have found similar or even higher estimates. For example, a 2018 study from Deloitte estimated 5.7 million App Economy jobs in the U.S., using a different methodology and a much bigger assumption of spillover effects. (12)

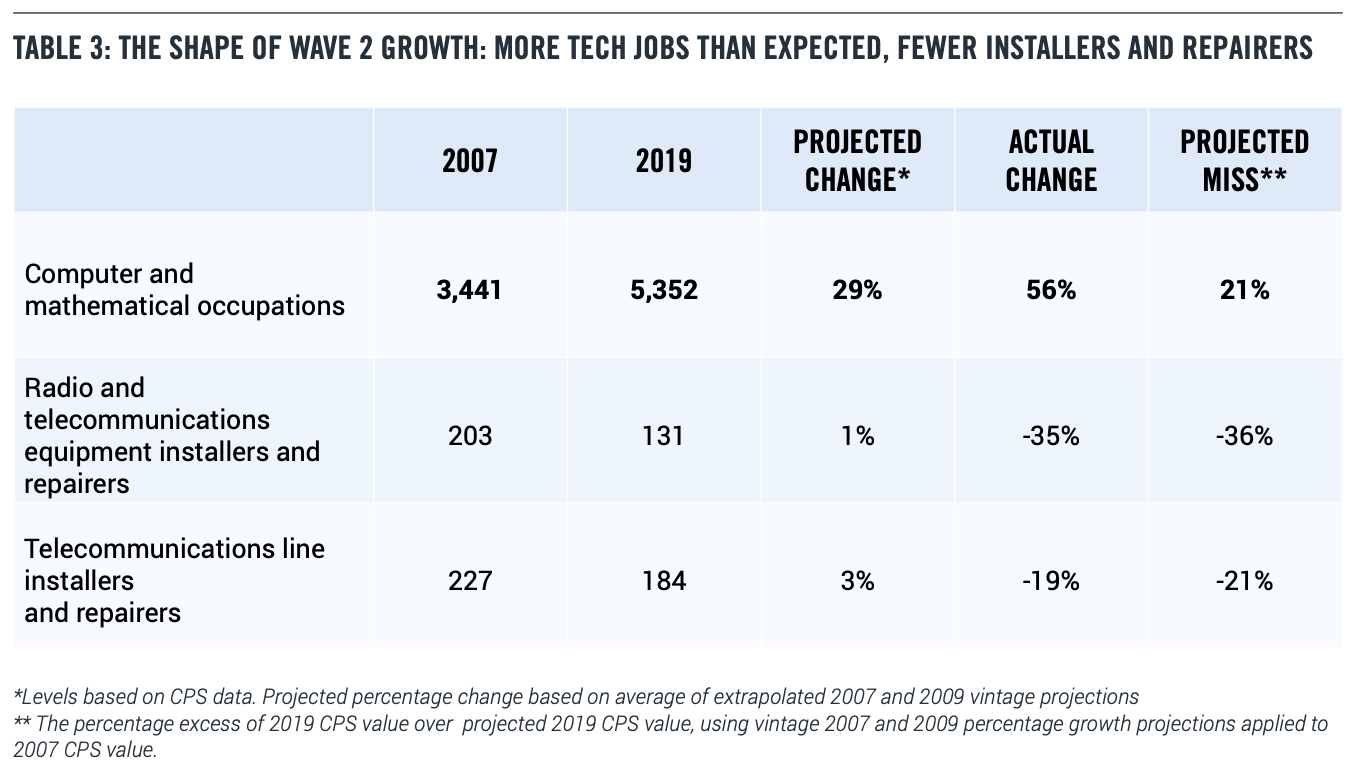

The job impact of mobile broadband and the App Economy did show up in the official numbers in a different way: the unexpectedly rapid growth of people working in “computer and mathematical occupations.” “Computer and mathematical occupations” is a broad category that includes data scientists, software developers and engineers, information security specialists, computer support specialists, and database and network administrators.

By contrast, skilled workers who maintain the telecom networks—the people who lay and fix the fiber-optic lines and put up the cellphone towers—are in the “installation, maintenance, and repair” occupations.

The BLS projections in 2007 and 2009 underestimated the expected size of the computer and mathematical workforce in 2019 by roughly 20 percent, or over 1 million workers. But the relevant categories of skilled installers and maintainers were overestimated in the projections. This tilt towards tech jobs is very important for understanding the third wave (Table 3).

II. WAVE 3: THE 5G REVOLUTION

Wave 3 of wireless-driven job growth, The 5G Revolution, began in 2019 as mobile carriers expanded their initial 5G networks, and then continued into 2020. All major carriers in the U.S. — AT&T, Verizon, and T-Mobile — are heading towards nationwide 5G networks by the end of 2020, according to analysts. (13) The pandemic has made the case for 5G more compelling as many of the use cases for 5G services have been pulled into the present.

Telehealth has become not just optional but a requirement in many medical situations.

Students from kindergarten to graduate school have been forcibly introduced to distance learning. Businesses and governments have been learning how to use virtual meetings, at a much lower cost than flying around the world. Companies have started using robots to help disinfect their stores. (14)

The U.S. military faces its own challenges, as the virus has forced changes in routines to minimize infectiousness and to protect its suppliers. “We believe the COVID-19 pandemic has accelerated society’s transition to broadband and digitization by at least a decade,” said one market analyst in March 2020. (15)

Indeed, in the early days of the pandemic, Verizon announced that it was expecting to allocate $17.5- $18.5 billion on capital expenses in 2020, up from its previous guidance of $17-$18 billion. “This effort will accelerate Verizon’s transition to 5G and help support the economy during this period of disruption,” Verizon said in a press release. So far, the pandemic has caused spectrum auctions in Europe to be pushed back. (16) Meanwhile the FCC has not changed its spectrum auction plans for 2020. (17)

Spending on 5G networks is what is known by economists as “autonomous investment”—that is, investment that is not linked to the immediate ups and downs of GDP. (18)

The Extension of Wireless to Physical Industries

Wave 2 was focused on “digital industries,” where the output can be reduced to bits and bytes. This includes games, music, communications, social networks, news, advertising, financial services, and ecommerce purchases of digital goods such as hotel and plane reservations. These digital industries, while important, make up less than 20 percent of the economy. (19) (Formally defined, the digital sector includes computer and electronics manufacturing; ecommerce; software and other publishing; video and audio content; broadcasting; telecommunications; data processing; internet publishing and search; and computer systems design and programming. Slight changes to the boundary of the digital sector does not affect the analysis here).

Wave 3, by contrast, is based on the applications of wireless to the challenges and opportunities in physical industries, such as agriculture, energy, construction, manufacturing, transportation, education, healthcare, and government (including defense).

Physical industry use cases include low-power wireless sensors that must operate for long periods in a field, say, without a battery replacement, or a low-latency connection to a drone or autonomous vehicle.

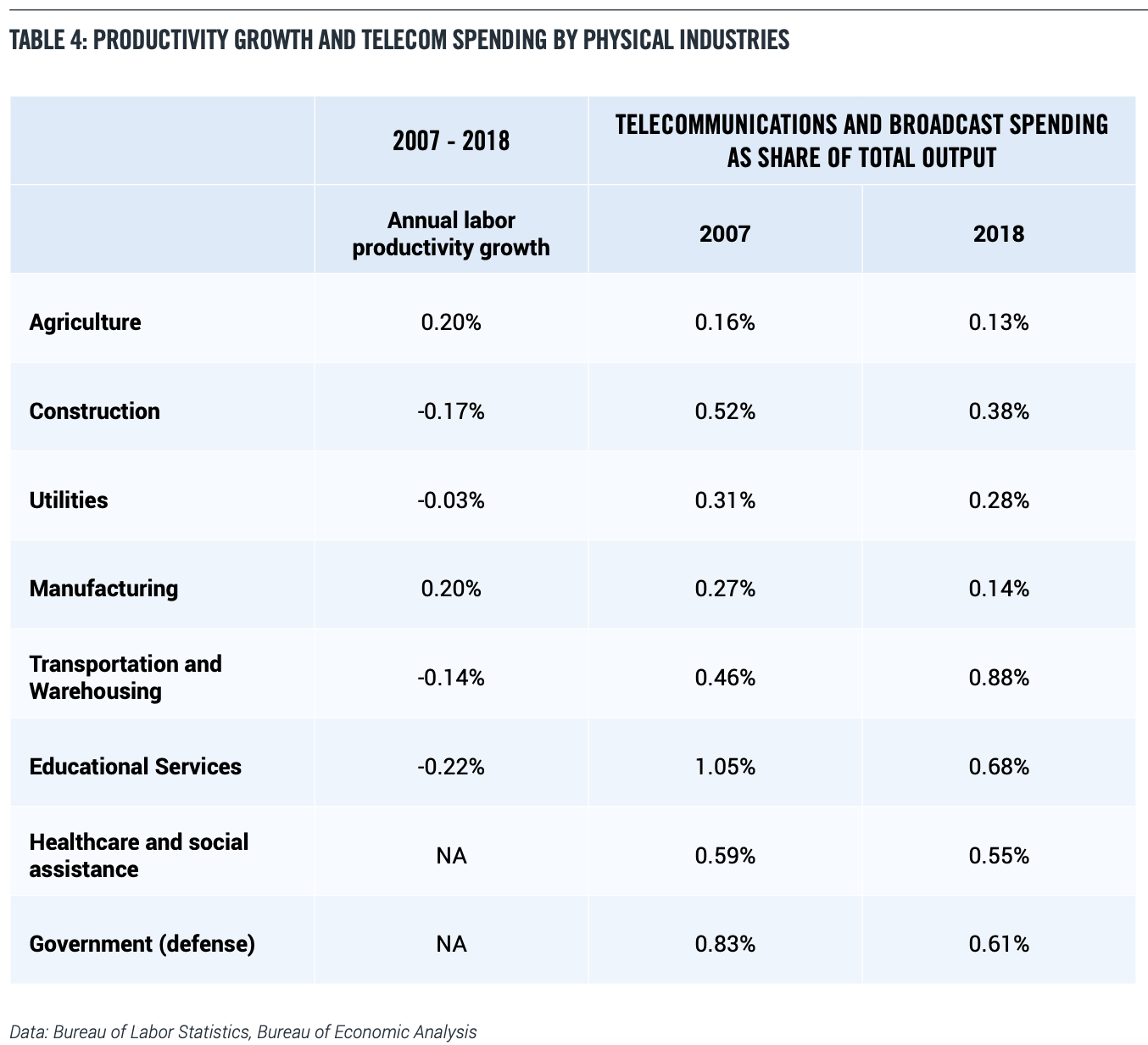

Table 4 shows the key physical sectors had slow or negative productivity growth during the second wave (in general 1 percent annual productivity growth is adequate and 2 percent is good, so none of these industries made the grade). Slow or negative productivity growth means less competitive industries, weaker wage gains, and lesser quality jobs.

Surprisingly, most of these industries had low and falling spending on telecommunications services, as a share of total output (for most industries, total output can be interpreted as revenues. For defense, total output can be interpreted as spending including accounting for depreciation). (20) For example, in agriculture, the amount spent on telecom services went from a very low 0.16 percent in 2007 to an even lower 0.13 percent. (To provide some context, in 2018 the average telecom share for digital industries was 3.5 percent, and the average telecom share for physical industries was 0.7 percent).

5G is likely to reverse both of these trends. Faster, more versatile wireless communications are an essential factor in driving productivity gains. Research shows that industries like manufacturing, construction, and healthcare have lagged in digitization, helping explain why productivity growth has been so slow. To increase productivity, physical industries need the ability to gather information from widely dispersed sensors and to use that data to control activities in real-time. That’s not possible without faster and more versatile wireless communications supplied by 5G.

The ability to rapidly communicate data and information using 5G will increase productivity gains in both the public and private sectors. And these productivity gains, in turn, will lead to higher revenue, faster wage gains, advances in job quality, and increased international competitiveness.

In 2017, a study from the Technology CEO Council examined the impact 5G will have on productivity growth in the “physical industries” and tax revenues over the next 15 years.21 The report estimated that the physical industries will boost annual economic growth by 0.7 percentage points over the next 15 years, generating an additional $2.7 trillion in annual economic output, $8.6 trillion in wage and salary payments, and $3.9 trillion in federal tax revenue.

The 5G Revolution and Job Growth

The impact of 5G on jobs can be summarized as “network meets the cloud.” That means we can push more capabilities out to the edge, including real-time and near-real-time applications of machine learning and artificial intelligence to the physical world. In many cases, new technologies create new tasks and markets that didn’t exist before. (22) For example, healthcare providers already monitor medical equipment like pacemakers remotely. But with 5G, the set of possible at-home diagnostics or interventions will expand greatly, and telehealth installers and maintainers will be a highly valued occupation.

5G will greatly expand the capabilities of drones in a range of applications from agriculture to military to logistics, especially in conjunction with artificial intelligence. That will expand the market for skilled drone operators, sometimes called “remote-pilots-in-command,” earning as much as $100,000 per year.

The other alternative is that productivity gains will lower costs enough to expand the market, which ends up creating new jobs. (23) That’s what happened in ecommerce. The use of robots in ecommerce fulfillment centers, combined with effective use of data, helped drive down costs low enough to offer consumers fast delivery and easy returns. And the combination of fast delivery and easy returns, in turn, made the ecommerce proposition irresistible to many consumers, because now they could avoid the time and trouble of going to the store, getting the product quickly and simply returning it for free if it didn’t work. The result was a massive shift from unpaid household shopping hours to paid ecommerce fulfillment and delivery hours. (24)

Or consider manufacturing. The pandemic has called into question the wisdom of depending on global supply chains for important medical supplies, and by extension, any parts that one might need in a crisis.

The low-latency high-bandwidth services delivered by 5G can help spur the digitization of the factory floor, boosting productivity and increasing flexibility. (25, 26) The result could be a shift to distributed local manufacturing in the U.S. in the post-COVID era, creating jobs and shortening supply chains.

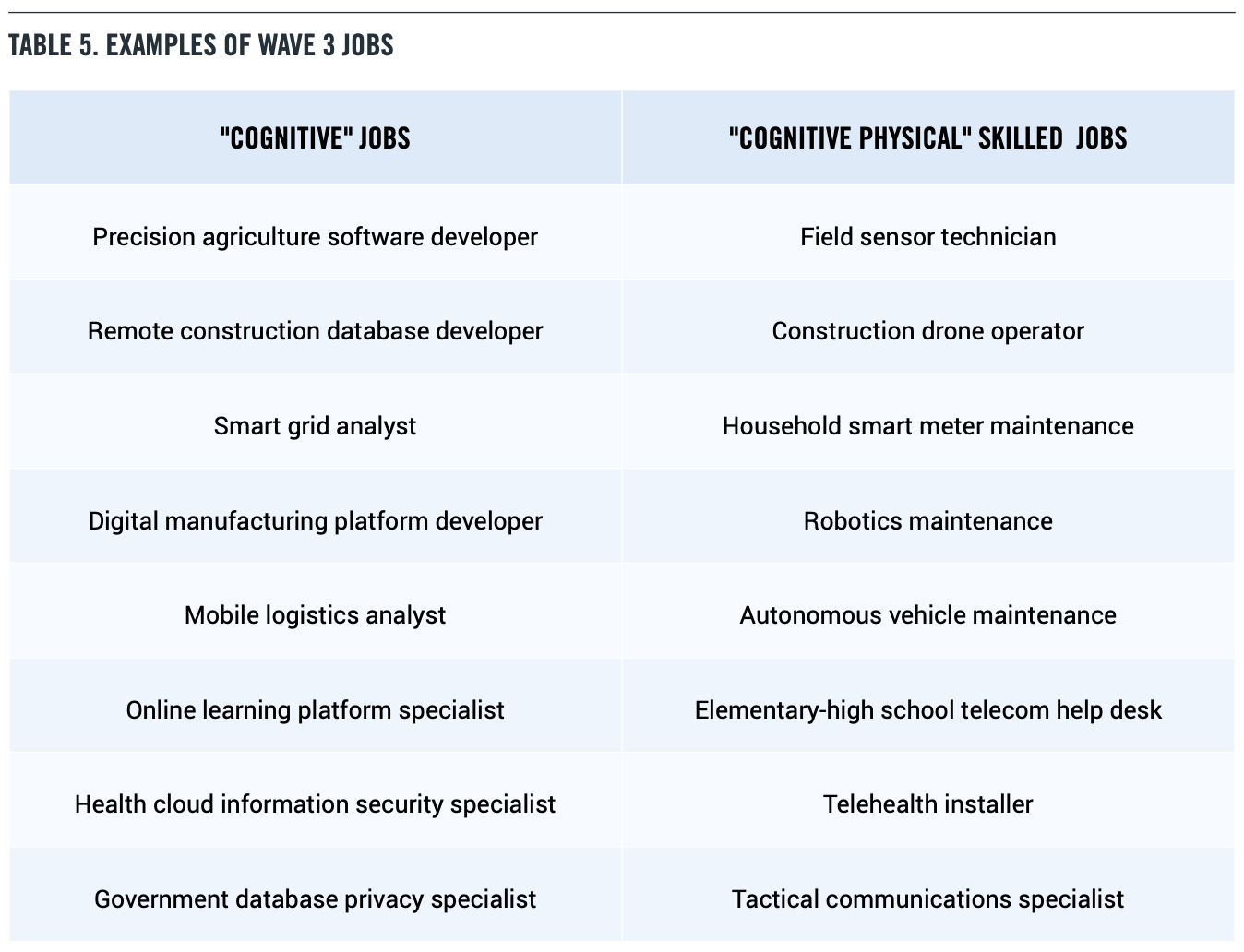

Table 5 identifies examples of Wave 3 jobs. Unlike Wave 2, which mostly generated “cognitive” tech jobs which required a college education, Wave 3 is rooted in the physical world. As a result, Wave 3 will also create mixed ‘cognitive-physical” skilled jobs, many of which fall into the category of installers and maintainers. In addition, people will continue to play an essential role in the supervision loop of advanced robots.

The types of cognitive jobs listed in Table 5 mainly fall into the broad occupational class of “computer and mathematical occupations.” Relative to the median wage for all occupations, these jobs pay a wage premium of 122 percent.

But Wave 3 will also generate blue-collar jobs that use a combination of manual and problem-solving skills—what we call “cognitive-physical” jobs— which are likely to pay a wage premium as well.

Today, the median wage for telecommunications equipment installers and repairers is 45 percent higher than the overall median wage, according to figures from the BLS. As 5G becomes an integral part of business operations, we would expect such jobs to become more valuable rather than less.

III. QUANTIFYING LONG-TERM 5G-RELATED JOBS

Estimates of job growth spurred by a new technology have to be measured against some baseline. As we noted earlier, the BLS projection methodology typically looks backward, not forward, and has a difficult time dealing with ongoing technological changes. BLS projections have consistently understated the job impact of wireless innovation. In the first wireless wave, jobs in the wireless industry came in 50 percent above projections. In the second wireless wave, the rise of the App Economy drove up demand for computer and mathematical jobs 21 percent above BLS projections as of 2019.

Our fundamental assumption is that unlike the second wave—which was mostly focused on digital industries—the third wave will drive demand for both cognitive and cognitivephysical jobs across the whole range of physical and digital industries. The third wave will therefore benefit a wider set of Americans and regions than the second wave did. We therefore adopt a simple and straightforward approach to estimating the impact of 5G on jobs. We start with the latest BLS industry and occupation projections, issued in September 2019, for the 2018-2028 period. We rebase them to 2019 and extend them to 2034 to get a 15-year projection.

Then we assume that the additional jobs produced by 5G in the third wave, relative to the baseline, are the same magnitude as the additional jobs produced by wireless innovation in the second wave. We then allocate these jobs across industries according to their size, rather than focused on only tech. Finally, we then apply a conservative job multiplier.

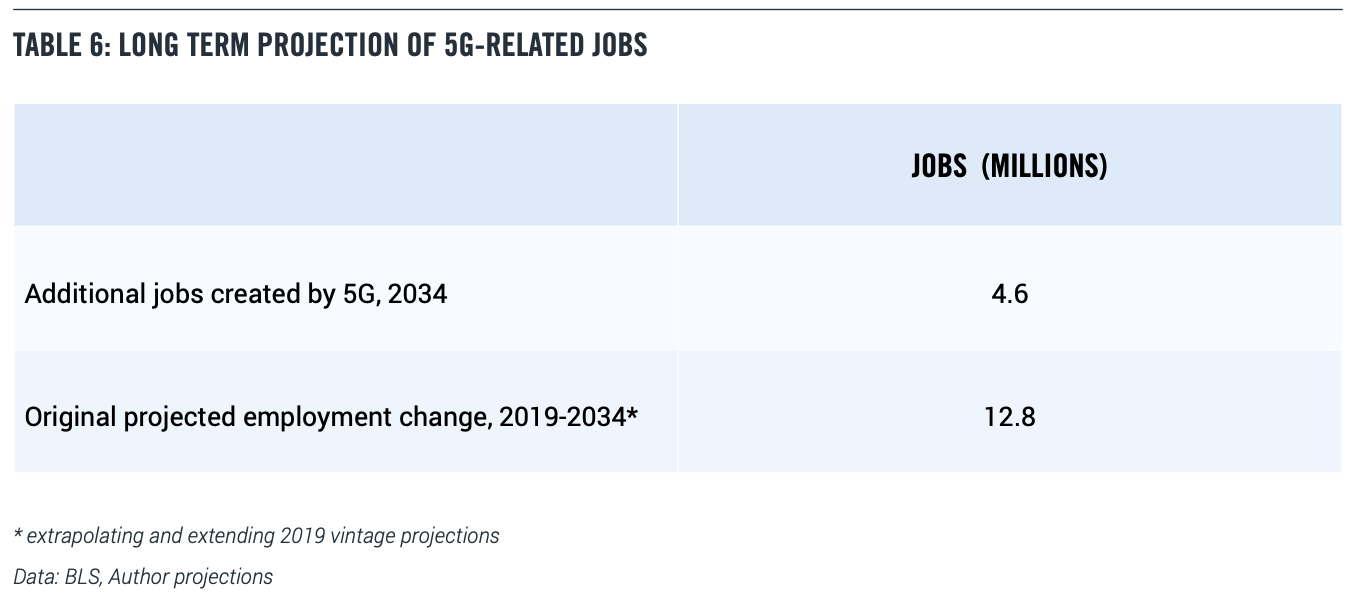

Based on these assumptions, we estimate that 5G and related technologies will produce an additional 4.6 million jobs in 2034 relative to the baseline original projected growth of 12.8 million.

When we say ‘additional’ we mean that 5G-driven job growth is an additional factor that the conventional projections do not take into account. In an important sense, 5G job creation is a countervailing force to job destruction from automation and globalization. These are higher paying jobs that will replace jobs that are lost.

Past Reports Projecting 5G impact On Jobs

In 2017, Accenture released a report estimating wireless operators will directly invest $275 billion between 2017 and 2024 in 5G infrastructure, creating up to 3 million jobs and boosting GDP by $500 billion.27 Of the $275 billion investment, $93 billion was estimated to be spent on construction, with the remainder being allocated to network equipment, engineering, and planning. Importantly, the report recognized this growth will be spread across communities of all sizes. “Small to medium-sized cities with a population of 30,000 to 100,000 could see 300 to 1,000 jobs created. In larger cities like Chicago, we could see as many as 90,000 jobs created,” the authors wrote.

More recently, a report on the global economic impact of 5G was released in November 2019 by IHS Markit, updating a 2017 study. (28) This report looked at several measures of 5G impact. First, the report forecast that between 2020 and 2035, global real GDP would grow at an average annual rate of 2.5 percent, with 5G contributing almost 0.2 percent of that growth. Second, the report looked at the seven leading countries for 5G—the United States, China, Japan, Germany, South Korea, the United Kingdom, and France—and found that the collective investment in R&D and capital expenditures by firms that are part of the 5G “value chain” within these countries will average over $235 billion annually, measured in 2016 dollars. The U.S. and China each accounted for about one-quarter of global spending on 5G R&D and capital expenditures. Third, the IHS Markit report estimated that 22 million jobs would be supported by the 5G value chain globally in 2035, with 2.8 million of those jobs in the United States.

Most recently, two economists at NERA Economic Consulting, Jeffrey A. Eisenach and Robert Kulick, estimated the potential job impact of 5G. (29) They found that if 5G adoption followed the path of 4G adoption, then, “at its peak, 5G will contribute approximately 3 million jobs and $635 billion in GDP to the U.S. economy in the fifth year following its introduction.” This employment effect is smaller but faster than the one reported here.

IV. KEY 5G USE CASES

As previously noted, The 5G Revolution will create job opportunities across many sectors and regions in the U.S. In this next section, we identify eight of the most likely use cases that have significant potential for job growth.

1. AGRICULTURE

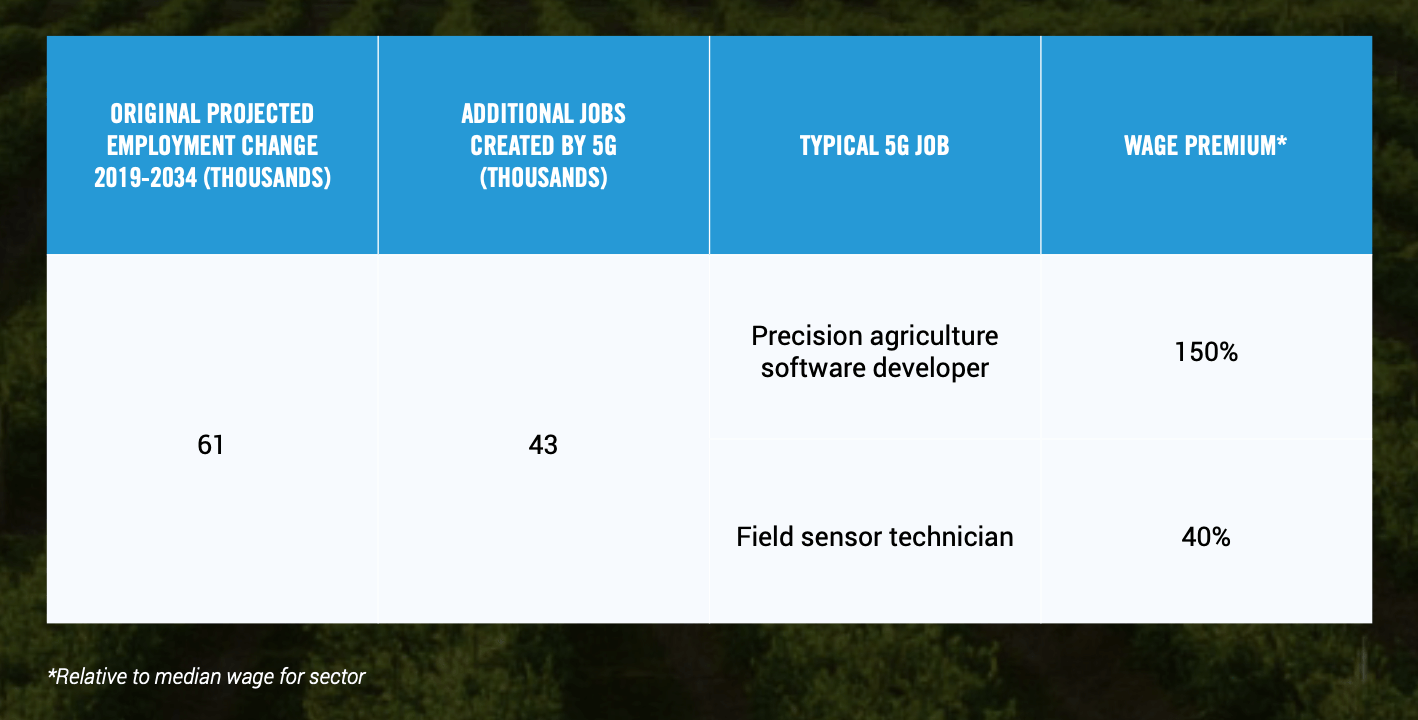

Agriculture is an industry ripe for transformation. In many areas of the country, it is still heavily dependent on low-cost labor, which may be discouraged because of the pandemic. And as of 2018, only 0.1 percent of agriculture revenues were being spent on telecommunications, a percentage that had dropped slightly since 2007.

Faced with an evolving environment with increasing temperatures and diverging precipitation levels in wet and dry areas, precision agriculture will rely on an interconnected system of low power sensors, integrated equipment, and data—all powered by 5G—to monitor field conditions and maximize yields while efficiently allocating scarce resources such as water. (30)

To best utilize the new technologies, agriculture will have to build and maintain a new tech and telecom infrastructure and the workforce is only now starting to come into existence. This requires both software developers and people to install and maintain the equipment.

For example, as of March 2020, agriculture technology company Farmers Edge was looking for a precision technology specialist to install equipment and software at its growers’ farms in Madison, Wisconsin.

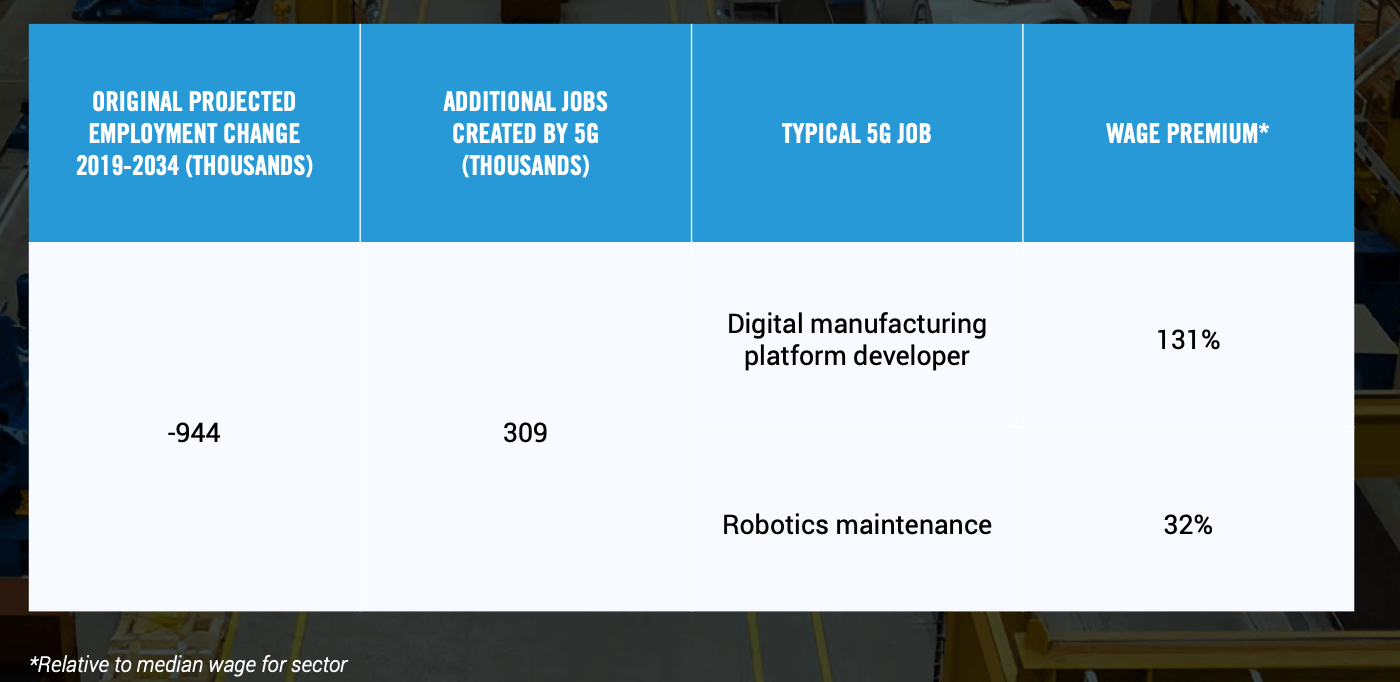

2. CONSTRUCTION

5G plays an essential role in digitizing construction, a key sector which has been plagued by high costs and low productivity in recent decades, especially in public infrastructure. (31) Perhaps not coincidentally, construction is one of the least digitized sectors of the economy. (32)

Since 2000, the cost of construction has risen 118 percent according to the Bureau of Economic Analysis. (33) Highways and streets have become 126 percent more expensive for state and local governments to invest in. (34) By comparison, overall prices in the economy have only risen 41 percent over the same time span. (35)

This increase in the relative price of construction helps explain why U.S. infrastructure seems shoddier and worn-out these days.

A 5G communication grid will allow the seamless and flexible integration of automated equipment and skilled workers on a construction site. Structures will go up faster with fewer dangerous errors, and worksites will be safer. Meanwhile, as 5G helps bring down the cost of construction, demand will rise. Both renovation and new building will be cheaper and faster.

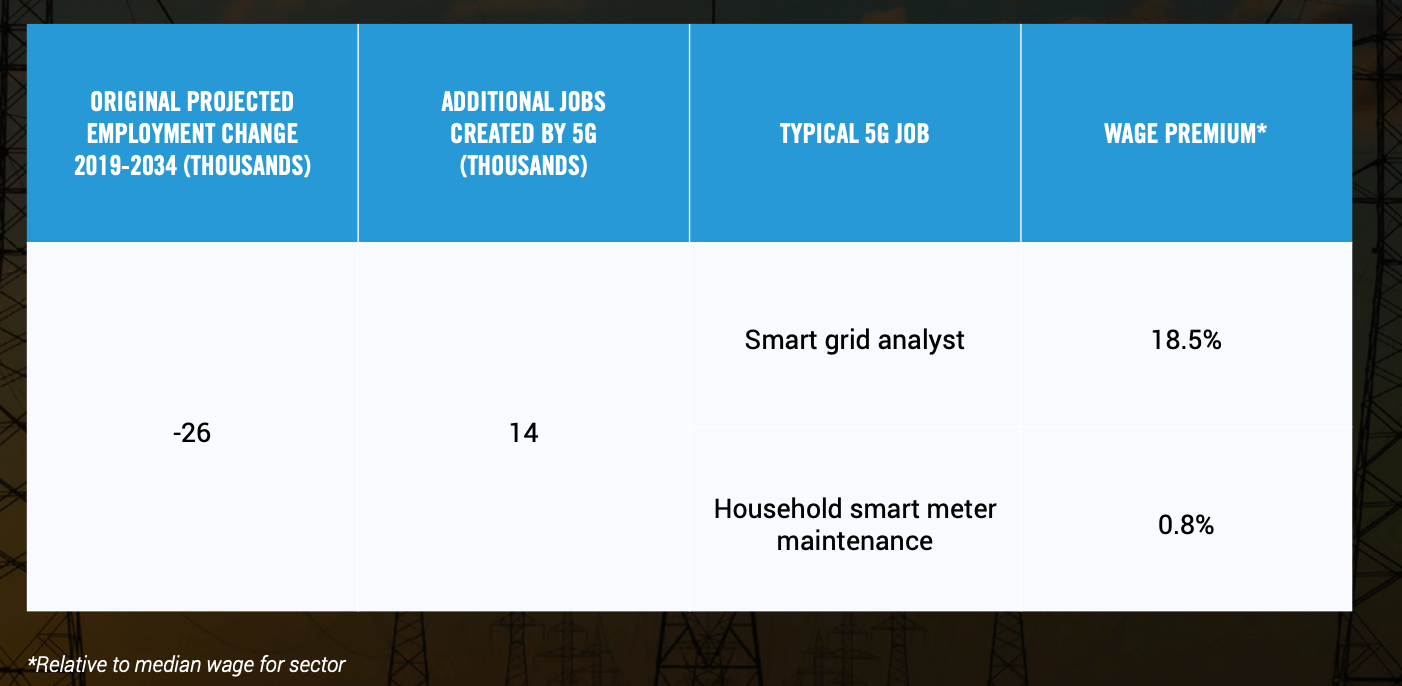

3. UTILITIES

Energy use management is an essential use case for 5G. Utilities are already extensive users of information technology within their own operations to monitor power production and distribution. But 5G makes it much easier to connect up smart meters to the grid to give people and businesses better incentives to control their electric use.

This is one sector where our projection methodology may underestimate the number of new 5G-related jobs. If the energy infrastructure shifts over the next 15 years from fossil fuels to low-carbon energy sources, the opportunities for 5G-enabled workers may be very strong.

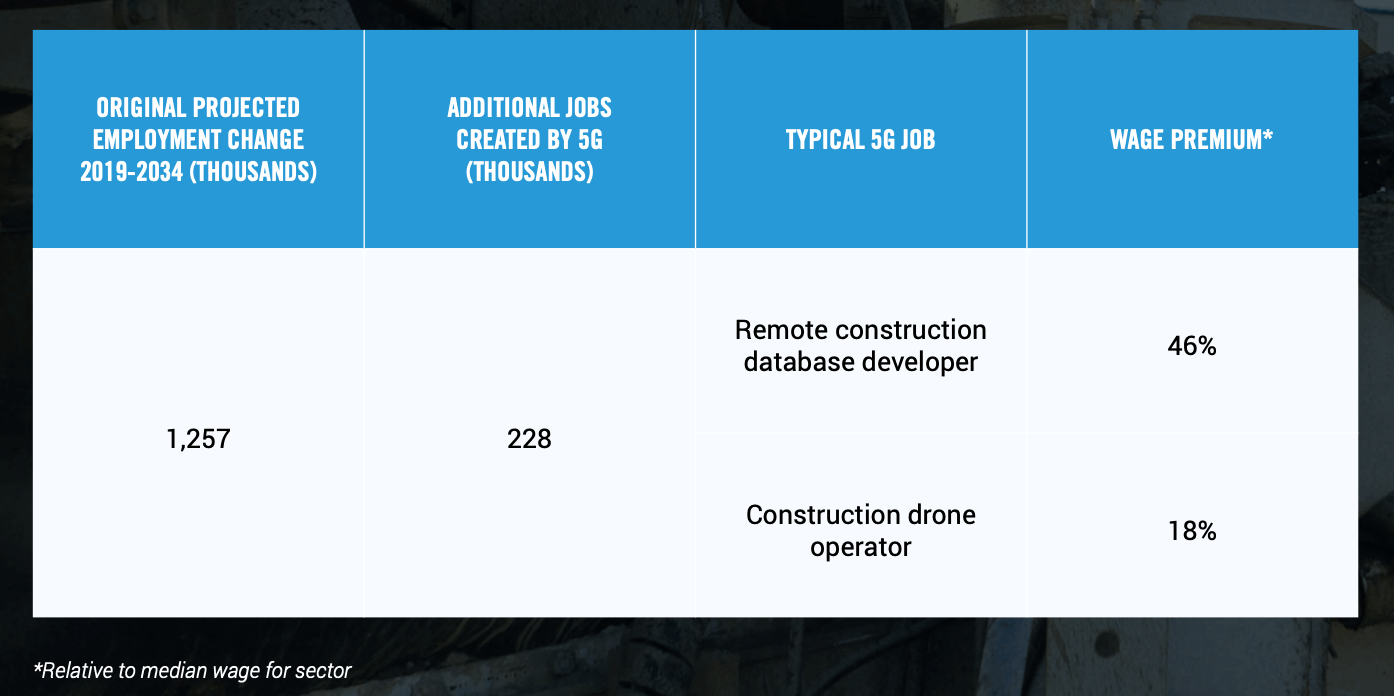

4. MANUFACTURING

In manufacturing, 5G and digitization will help reduce costs, making domestic manufacturing more competitive. Many manufacturing industries have weak or even negative multifactor productivity growth over the past 20 years. (36) Multifactor productivity growth takes into account the usage of purchased services, energy, capital, and intermediate inputs and is a key measurement of competitiveness. Investment in information technology such as 5G, which manufacturing has lagged in since the early 1990s, will enable new business models that expand markets and enhance domestic competitiveness.

New markets and reinvigorated domestic competitiveness means more jobs in the U.S. Through a combination of digitized distribution, digitized production, and new manufacturing platforms – coined by PPI as the Internet of Goods – a new network of smallbatch and custom goods factories will likely arise. Importantly, these industrial startups will fuel job creation in low-density areas and former industrial hubs like the Midwest and upstate New York, as physical industries like manufacturing dominate these economies. That means more domestic production and less imports. (37)

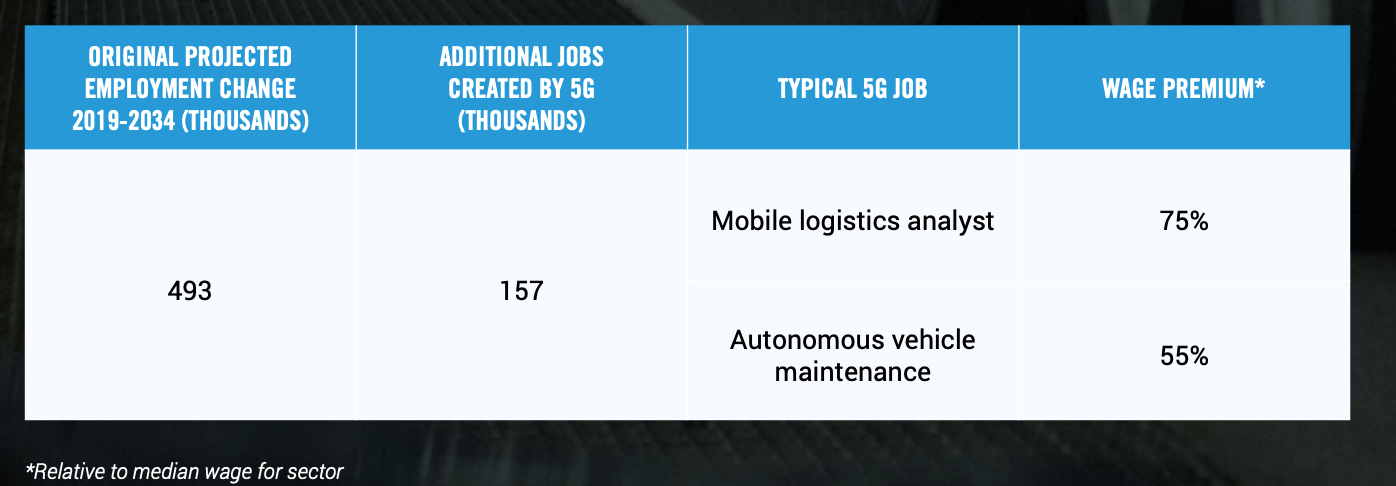

5. TRANSPORTATION AND WAREHOUSING

5G will transform how people and goods move from point to point and how cities manage traffic. This has major implications for industries ranging from defense and transportation to logistics and delivery.

Low-latency 5G connections will accelerate the roll-out of fully autonomous trucks and cars. But the flip side is that these vehicles will have to be maintained to a very high standard to keep them safe, creating more jobs for skilled technicians, and compensating for the loss of truck driver jobs.

These capabilities depend on the speed of 5G to rapidly relay data. In trucking, a report by McKinsey recognizes, “sixty-five percent of the nation’s consumable goods are trucked to market. With full autonomy, operating costs would decline by about 45 percent, saving the US for-hire trucking industry between $85 billion and $125 billion.” (38) This savings from automated trucking could be passed onto consumers in the form of lower prices. Delivery drones stand to further disrupt how goods are delivered.

And in traffic management, traffic signals will be based on real-time traffic flow rather than timed stoplights. Pittsburgh recently introduced smart traffic lights and saw travel times cut by 25 percent. (39) These innovations reduce the need for drivers and increase the need for maintenance and road workers as driving and delivery become less physically intensive and goods can be moved around the clock.

The creation of new types of jobs is already starting. As of March 2020, transportation services company Transdev Services was hiring a self-driving vehicle operator in San Francisco, California. Technology platform Argo AI was seeking an autonomous vehicle system test specialist responsible for operating its autonomous test platforms in Miami, Florida. And transportation services firm MV Transportation was searching for an autonomous vehicle attendant tasked with ensuring the safe operation of the Autonomous Vehicle in Corpus Christi, Texas.

6. EDUCATION (PUBLIC AND PRIVATE)

Students and teachers at all levels were forced to adopt virtual learning in 2020 because of the pandemic. Reports from the field have been mixed. The technology in many cases was not up to the task, and many students, especially in low-income neighborhoods, were caught on the wrong side of the digital divide. If schools want to engage in virtual learning, they will need a technology like 5G with the bandwidth for students and teachers to fully engage.

A related issue is training of workers on new equipment and processes. As 5G moves into the workplace, it will transform the way that physical industries such as manufacturing and healthcare do business. In order for workers to stay relevant, the training technology has to become 5G-enabled as well.

7. HEALTHCARE

As with education, the pandemic forced healthcare providers to adopt ad hoc telehealth practices without the proper technology. 5G will provide the framework in which providers can truly practice healthcare at a distance. Moreover, 5G is essential to unlocking quality healthcare for rural, low-density areas because of its ability to support real-time high-quality video, transmit large medical images, and enable real-time remote monitoring.

Maintaining the telehealth infrastructure will be a core function at hospitals, which will employ skilled telehealth technicians, just like they have lab technicians and nurses. Clinical information will flow wirelessly into electronic health records, requiring specialized database specialists who are trained in the medical and privacy requirements of these types of data. As of late April, Beth Israel Lahey Health of Beverly, Massachusetts was looking for a “telehealth installer.”

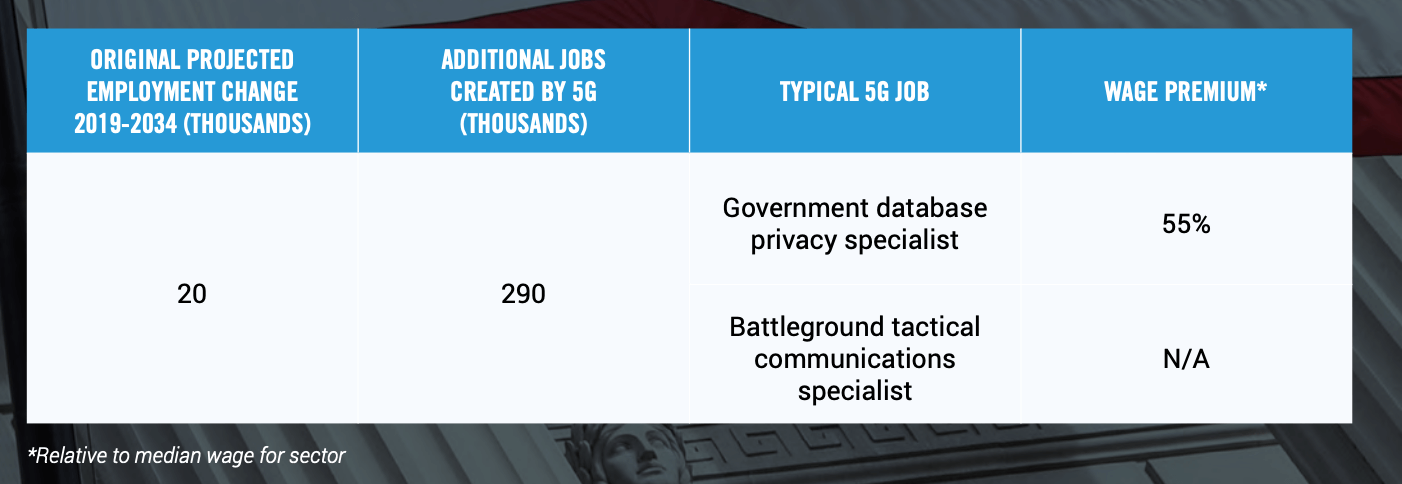

8. GOVERNMENT (EXCEPT EDUCATION)

We can divide the impact of 5G on government into military and civilian uses. On the military side, a March 2020 report from the Congressional Research Service noted: “5G technologies could have a number of potential military applications, particularly for autonomous vehicles, command and control (C2), logistics, maintenance, augmented and virtual reality, and intelligence, surveillance, and reconnaissance (ISR) systems—all of which would benefit from improved data rates and lower latency (time delay).” (40)

In fact, the USDOD has already released several Requests for Prototype Proposals for test beds focusing on AR/VR for training, smart warehouses and dynamic spectrum sharing. All of these potential applications generate new human resource demands as well. As the capabilities of 5G evolve, it becomes more important than ever to best make use of resources, both in terms of equipment and people. For example, as of summer 2020, The Aerospace Corporation was looking for a “5G and Internet of Space Things Wireless Network Engineer” with the ability to obtain a U.S. security clearance.

On the civilian side, “smart cities” development will mean that state and local governments will have to transform all of their services to 5G, from waste collection to police to property tax assessment. And that will, in turn, mean a workforce much more heavily oriented towards maintaining and repairing the necessary telecom equipment.

Where Will Wave 3 Jobs be Located?

Both the first and second wave of wireless jobs were concentrated in dense digital cities like San Francisco, New York and Boston.

Table 7 shows examples of top “digital” areas, as ranked by the share of local GDP coming from the information sector, the financial services sector, and the professional services sector (which includes law, engineering, and accounting, as well as computer programming).

Not surprisingly, the list of the top digital metro areas is headed by New York and San Francisco. There’s one important caveat: for confidentiality reasons, the Bureau of Economic Analysis suppresses some data, so we can’t calculate the digital share for all metro areas.

EXAMPLES OF TOP DIGITAL METRO AREAS

1. Boston-Cambridge-Newton, MA-NH

2. Boulder, CO

3. New York-Newark-Jersey City, NY-NJ-PA

4. San Francisco-Oakland-Berkeley, CA

5. Seattle-Tacoma-Bellevue, WA

*Listed alphabetically. Inclusion based on digital share, which measures the share of the information, financial services, and professional services sectors in overall metro GDP Data: BEA

By contrast, Wave 3 will benefit those areas which are more balanced in terms of digital and physical industries. Table 9 shows some examples of such areas. These areas are not tech deserts, for sure, but they are well-positioned to take advantage of the opportunities offered by 5G.

EXAMPLES OF BALANCED DIGITAL/PHYSICAL METRO AREAS

1. Albany-Schenectady-Troy, NY

2. Ann Arbor, MI

3. Baltimore-Columbia-Towson, MD

4. Buffalo-Cheektowaga, NY

5. Cleveland-Elyria, OH

6. Colorado Springs, CO

7. Detroit-Warren-Dearborn, MI

8. Harrisburg-Carlisle, PA

9. Huntsville, AL

10. Jacksonville, FL

11. Kansas City, MO-KS

12. Lincoln, NE

13. Pittsburgh, PA

14. San Antonio-New Braunfels, TX

*Listed alphabetically. Inclusion based on digital share, which measures the share of the information, financial services, and professional services sectors in overall metro GDP Data: BEA

V. SHORT-TERM SNAPSHOT: THE IMMEDIATE IMPACT OF 5G

So far, we have been discussing the longterm job impact of 5G. But in the wake of the COVID-19 pandemic, we need to be concerned about the short-term job impact as well. In this section, we show that current 5G build-out and engineering activities has already created 106,000 jobs as of April/May 2020 (Table 9).

Estimating 5G Network Build-out Jobs

Network build-out activities, of course, consist of installing 5G small cells around the country, including their backhaul connections. In some cases, the technicians and installers are employed directly by the carriers, while in other cases they are contractors. These are cognitive physical jobs, in the sense that we discussed earlier in the rep

ort. We get data on this employment from two different sources. First, the BLS track

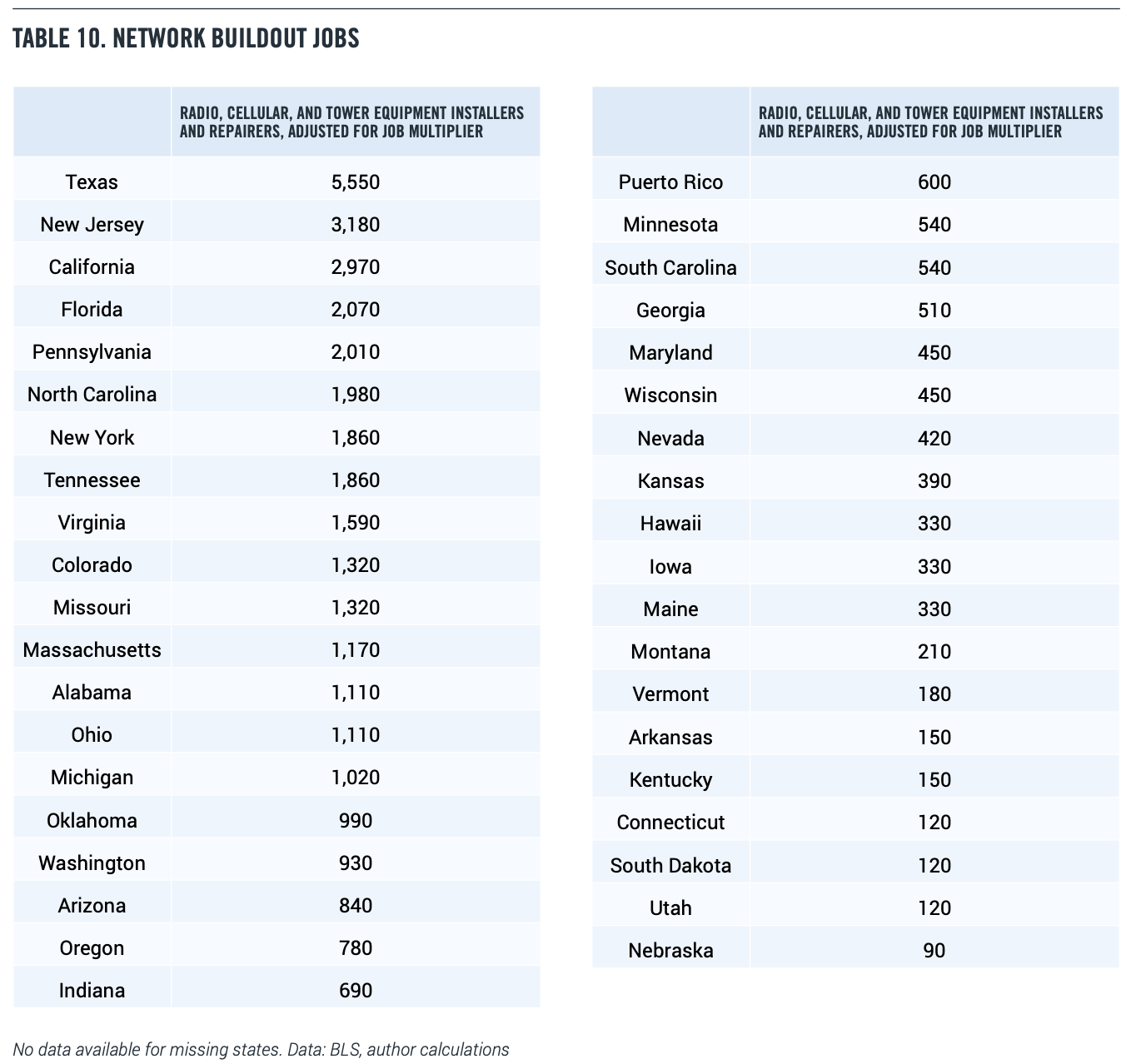

s the number of “Radio, Cellular, and Tower Equipment Installers and Repairers” in its Occupational Employment Statistics (OES). (41) As the name suggests, this category includes the workers who install 5G access points. As of May 2019, the last data available, there were 14,370 workers in this occupational category, with a relative standard error of 5.8 percent. Factoring in a conservative job multiplier, that gives us a net job impact of 43,000.

How are those jobs distributed? The top state according to the BLS data is Texas, followed by New Jersey, California, and Florida. These figures were as of May 2019 and based on several years of rolling surveys (Table 9).

Of course, the location of build-out activity changes over time as providers finish with one area for now and shift their construction activities to other area. To understand current 5G construction activity, we turn to another data source: publicly available job postings. These job postings contain information on the location of jobs and also the skills needed. For example, one company is advertising for a “Tower Top Hand” with 5G experience in the Baltimore area.

The database of job postings that we use comes from Indeed.com, which identifies itself as “the #1 job site in the world.”(42) Indeed’s real-time database of job postings is full-text Booleansearchable, including by title, location and by age of job posting.

We searched for job postings with the terms “tower” or “technician” in the title, and 5G in the body of the posting. This allowed us to identify “hot spots”—metro areas where there was current hiring activity for workers installing 5G networks (Table 11).

As of early May, companies are hiring for tower technicians in areas such as Allentown, Pennsylvania and the Baltimore metro area, as telecom providers extend their 5G networks outside of the densest high-income urban areas. Indeed, local news publications in these areas show evidence of discussions about ongoing deployments. (43)

Current 5G Engineering and Software Jobs

Making 5G a reality will also require hiring in engineering and software development. But unlike cell and tower installers and repairers, there is no obvious BLS occupational category that matches up well to 5G engineers and software developers.

To understand the prevalence and location of 5G engineers and developers, we further analyze the universe of online job postings, using a methodology that was developed to estimate the number and distribution of App Economy jobs.

These job postings contain information on the location of jobs and also the skills needed. For example, in late April and early May 2020, Commscope was advertising for an “Engineer, Principal 5G Systems” in Richardson, Texas. Epsilon Solutions was advertising for a contract “Wireless Core Engineer” to “test, deploy and debug DISH’S standalone 5G network” in Denver, Colorado. And KaRDS Cyber Solutions in Annapolis Junction, Maryland was advertising for a “5G Wireless SME / Senior Systems Engineer Level 6.” This position required a “TS/ SCI clearance with polygraph.

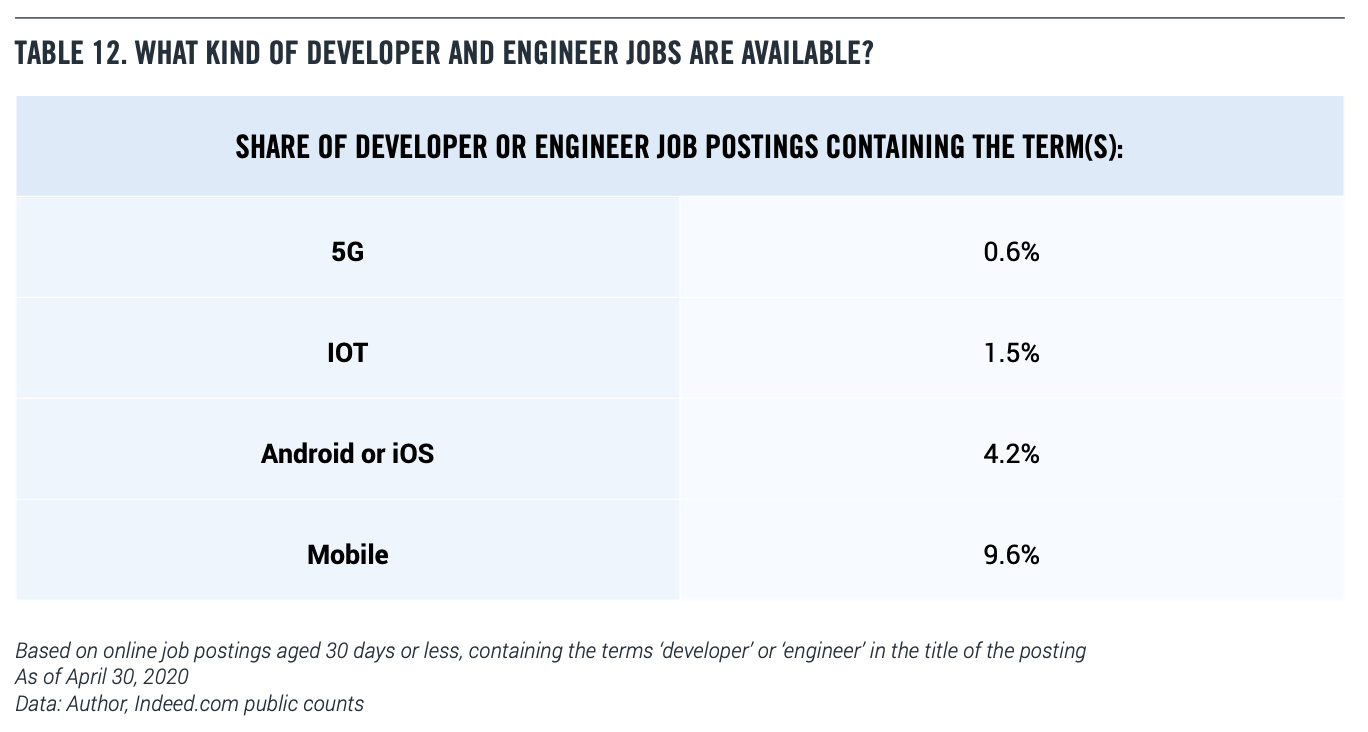

We started by searching for job postings with the words “engineer” or “developer” in the title, with postings aged 30 days or less. This gave us our initial pool of roughly 50,000 postings nationally as of the end of April. Generally speaking, our past research has suggested that searches with no age limit work better, but because of the pandemic-related shutdowns, we decided to focus on the more recent job posts.

Within that pool, roughly 0.6 percent contain the term 5G. By contrast, job postings containing the terms IoT, Android or iOS, or mobile are far more common (Table 12). We then use this share of job postings to estimate the share of jobs (see Appendix). There are roughly 1.75 million engineers, and an equal number of software developers, according to BLS. Taking 0.6 percent of that total comes to roughly 21,000 jobs, and then accounting for the multiplier gives us 63,000 5G-related engineering related jobs.

A First Look at China

We gain some insights into the Chinese 5G labor market through analysis of online job postings in both English and Chinese, as collected by Indeed.com. This approach is limited because of the lack of visibility into hiring by key 5G companies such as Huawei, China Telecom, and Tencent, so we cannot arrive at an overall number. Nevertheless, even a preliminary analysis may be useful.

We consider job postings which include ‘5G’ in the title and were released 30 or fewer days ago. For example, in the U.S., CommScope posted an opening for a 5G Systems Architect. As of August 17, 2020, the U.S. had 85 such new postings, compared with 125 for China. As noted, the China sample is significantly incomplete.

To put these numbers into some context, over the same period, the U.S. had 14370 new postings with ‘software’ in the title, while China had 4137 new postings with ‘software’ in the title (in either Chinese or English). That suggests the intensity of Chinese hiring of 5G personnel, relative to hiring of software personnel overall, is higher than in the U.S.

These jobs are very heavily concentrated in a relatively small number of states. California and Texas by themselves account for almost 50 percent of 5G engineering job postings. This makes sense given the location of the leading companies in the 5G space.

VI. THE KEY INPUT TO 5G JOBS: CAPITAL INVESTMENT AND SPECTRUM ACCESS

5G is a capital-intensive investment by its nature. To realize its benefits, wireless operators must invest in R&D and capital expenditures in engineering and network buildout. In a 2017 study, Accenture estimated wireless operators will invest $275 billion from 2017 to 2024, $93 billion of which will be spent on construction. (44) Indeed, via its Investment Heroes series, PPI estimates the major wireless operators have invested more than $150 billion in the United States since 2016, much of which has gone towards 5G R&D and deployment. (45, 46)

The portion of spectrum to be most used for 5G is divided into two categories: millimeter wave (above 24 GHz) and sub-6 (6 GHz and below). (47, 48) Each of these spectrum ranges will play a vital role in bringing 5G products and services online. While mmWave has the fastest speeds, it has limited range and is not able to tolerate much interference like walls or rain. (49) In the sub-6 spectrum, the range is better than that of the mmWave, but speeds are reduced. While mmWave will be utilized in dense population areas such as downtown areas and stadiums to transmit data, sub-6 will be critical to providing access to IoT products in suburban and rural areas.

Spectrum for commercial use is controlled by the Federal Communications Commission (FCC). One of the ways the FCC distributes spectrum is by auctioning licenses, with the proceeds going to the Treasury Department. Since 1994, the U.S. government has raised over $100 billion in revenue from wireless companies participating in FCC spectrum auctions. (50) The FCC’s first 5G spectrum auction, the mmWave of 28 GHz, was conducted in November 2018.51 The FCC followed by auctioning the 24 GHz band in March 2019, and the 37, 39, and 47 GHz bands in December 2019. (52, 53)

Much of the spectrum used by mobile networks to date have been concentrated in the sub-6 bands of 600 MHz to 2.6 GHz. These mid- to low-bands are likely to be used for 5G as well to achieve wider geographical coverage. As of April 2019, the FCC had awarded 716 MHz of spectrum below 3 GHz. (54) Additionally, the FCC has designated the 2.5 GHz band to “be available for commercial use via competitive bidding”. (55) The FCC ran an auction the 3.5 GHz band in July and August 2020. (56) And in February, the FCC ordered satellite operators in the 3.7- 4 GHz range to relocate, freeing the space for reallocation by December 2023. (57)

The other mechanism by which the FCC distributes spectrum is by allowing unlicensed use of certain spectrum – for purposes such as Wi-Fi. Under this regime, operators can use designated airwaves to transmit data without getting permission from the FCC. (58) However, the lack of exclusivity in unlicensed bands means an increased risk of interference. In March 2019, the FCC freed up the 116-123 GHz, 174.8-182 GHz, 185-190 GHz, and the 244-246 GHz bands for unlicensed use. (59) And in April 2020, the FCC proposed rules to make the entire 6 GHz band available for unlicensed use. (60)

International Comparisons of Spectrum Allocations

In April 2019, Analyses Mason released a report summarizing certain countries’ spectrum allocations. (61) The countries had comparable amounts of spectrum below 3 GHz awarded, with the U.S. coming in first at 716 MHz, Australia in second at 690 MHz, Germany at third with 689 MHz, Canada fourth with 648 MHz, and the United Kingdom rounding out the top five with 647 MHz. Asian countries have allocated similar amounts of spectrum below 3 GHz, with Japan at 601 MHz, Hong Kong at 583 MHz, China at 582 MHz, and South Korea at 477 MHz.

Awarded spectrum from 3-24 GHz had greater variation among countries. “Whilst many countries have now awarded over 100MHz of (exclusive nationwide) spectrum to mobile, several countries (China, Italy, and Spain) have awarded 300MHz or more,” the authors write. Following those three countries were South Korea, the U.K., Australia, Japan and Qatar – all with 200 MHz or more allocated. Notably, the U.S., Canada, France, Germany, and Hong Kong had not awarded any of this spectrum as of April 2019. As previously mentioned, sub-6 spectrum is a critical component to delivering new 5G products and services outside of high population density areas because of its ability to travel long distances while still providing 5G speed.

In the mmWave range, only the U.S., South Korea, and Italy had awarded spectrum. The U.S. had awarded 2,500 MHz, South Korea 2,400 MHz, and Italy 1,000 MHz as of April 2019. Other countries in the analysis had mmWave allocations planned, ranging from the second half of 2019 to 2021. The U.S. leads in the total amount auctioned or planned to be auctioned at about 7 GHz, followed closely by China at 6 GHz, and Canada at nearly 5 GHz. Australia, France, Germany, Spain, Sweden and the U.K. all planned to assign around 3 GHz.

A broader February 2020 analysis of countries conducted by Global Mobile Suppliers Association found 40 countries have completed allocations of 5G suitable spectrum since 2015. (62) “A total of 54 countries have announced plans and approximate dates for allocating 5G-suitable frequencies with timelines for completion between now and end-2022,” the authors note.