FACT: Height of papers needed to qualify T-shirt as ‘CAFTA duty-free’: ~ four inches.

THE NUMBERS: U.S. clothing import growth, 2005-2022* –

World

+$30.2 billion

Vietnam

+$15.7 billion

Bangladesh

+$7.3 billion

China

+$4.0 billion

Cambodia

+$2.8 billion

India

+$2.8 billion

Indonesia

+$2.8 billion

Pakistan

+$1.6 billion

CAFTA/DR**

+$1.4 billion

Jordan

+$0.9 billion

Egypt

+$0.8 billion

Italy

+$0.8 billion

Haiti

+$0.6 billion

Kenya

+$0.3 billion

Ethiopia

+$0.3 billion

Peru

+$0.2 billion

Colombia

-$0.3 billion

Korea

-$1.0 billion

Mexico

-$2.6 billion

Hong Kong

-$3.5 billion

* * Counting from completion of CAFTA/DR. See below for a more recent count of change 2012-2022.

** Guatemala, El Salvador, Honduras, Nicaragua, Costa Rica, and the Dominican Republic as a group. More detail: Nicaragua +$2.0 billion, Honduras +$0.6 billion, El Salvador +$0.3 billion, Guatemala +$0.1 billion, Costa Rica -$0.5 billion, Dominican Republic -$1.2 billion.

WHAT THEY MEAN:

CBP’s “border encounter” statistics show about 34,000 Central Americans reaching the U.S.’ southern border each month so far this year. Ten years ago, following their trek north in his book The Beast* (2010) Salvadoran journalist Oscar Martinez recounts stories of gang kidnappings and extortion, rape and sexual abuse, fatal falls from the roofs of trains along the way, and likely arrest at the end. Asking himself in closing why anyone would make such a trip, Martinez decides that the largest cause is simple:

“They’re unable to accept that miserable routine of waking up at five in the morning to travel two hours on a dangerous public transit system to get to a fast-food restaurant or a market or a warehouse in San Salvador, or Tegucigalpa, or Guatemala City, where they spend the whole day toiling away at undignified work only to return to their small homes, dog-tired, making a measly minimum wage that barely lets them afford beans and tortillas for their children.”

Vice President Kamala Harris makes a similar comment in a February conference on the “Northern Triangle” (Guatemala, Honduras, and El Salvador):

“[P]eople generally do not want to leave home. And when they do, it is because they are either fleeing some harm or because staying home will mean that they cannot satisfy the basic needs of their family and themselves.”

The conclusion drawn from their comments — that if the U.S. has a particular interest easing political stress and migration pressure in Central America, American policy should encourage investment and higher-quality employment — has a forty-year history. Four decades ago, the Ronald Reagan/Tip O’Neill “Caribbean Basin Initiative” aimed to encourage clothing-making in Central America by waiving U.S. tariffs under a complex legal formula known as “Section 807,” which offered buyers of Central American-made clothes duty-free treatment so long as the shirts, blouses, etc. were made of U.S.-produced fabric. The hope was that a growing garment industry would create many jobs, dampen the economic volatility arising from heavy reliance on fruit and coffee exports, reduce the social temperature, and so ease peace-making. A decade later, Central American maquiladora factories — long lines of sewing machines operated by young women; complementary male employment in factory repair, and transport — provided $4.8 billion of America’s $39.4 billion in clothing imports, or about eighth (by value) of the total.

After 20 years, the “CAFTA-DR” – the full and permanent Free Trade Agreement now joining the U.S. with Guatemala, El Salvador, Honduras, Nicaragua, Costa Rica, and the Dominican Republic – replaced the CBI in phases from 2005 through 2009. Its hope was that a permanent agreement would make the region more competitive and build buyer confidence. But in practice, this hasn’t exactly happened. Though Central America’s clothing trade has grown a bit in dollar terms, despite its tariff advantage the region’s share of U.S. imports has dropped from 12.3% in 2005 to 10.1% in 2022. Though CAFTA-DR clothes have no tariff, while as of 2022 Asian clothes were taxed at an average of 18.8%,** most new clothing imports in the last two decades have come from Asia. (China in the 2000s, Vietnam and Bangladesh in the 2010s and 2020s). Also a bit striking: imports from FTA partner Jordan and ‘preference’ beneficiary Haiti (which operates under another upgrade of CBI rather than a free trade agreement), though smaller overall, have grown much faster than imports from the CAFTA-DR countries.

Why? A plausible explanation is the complexity and costliness of the CAFTA/DR agreement. Like its CBI predecessor, CAFTA-DR retains a clause — known as a “yarn-forward rule” in apparel-trade jargon — requiring nearly all of (say) a T-shirt’s cloth and yarn*** to be made in the U.S. or a CAFTA country to qualify it for duty-free status. This means very restricted supply options for garment factories — to cite FTA partners only, no high-quality Peruvian cotton, no Colombian cloth, no Korean yarn or thread. Furthermore, CAFTA/DR includes a 143-page list of “product-specific rules of origin” writing special provisions for individual products meant to suit the very specific business models of many individual U.S. firms as of 2005. As a case in point, the agreement’s denim rules were meant to guide Central American manufacturers to fabric from a particular U.S. mill in North Carolina. As a sample of the daunting legal language this entails, here’s a passage drawn from the 2007 “textile amendment” requiring users to monitor the width of wool in the lining of jackets and skirts down to the half-micron:

“Chapter Rule 1 Except for fabrics classified in tariff item 5408.22.aa, 5408.23.aa, 5408.23.bb, or 5408.24.aa, the fabrics identified in the following headings and subheadings, when used as visible lining material in certain men’s and women’s suits, suit-type jackets, skirts, overcoats, carcoats, anoraks, windbreakers, and similar articles, other than men’s and boys’ and women’s and girls’ suits, trousers, suit-type jackets and blazers, vests, and women’s and girls’ skirts of wool fabric, of subheadings 6203.11, 6203.31, 6203.41, 6204.11, 6204.31, 6204.51, 6204.61, 6211.39, or 6211.41, provided that such goods are not made of carded wool fabric or made from wool yarn having an average fiber diameter of less than or equal to 18.5 microns, must be both formed from yarn and finished in the territory of one or more of the Parties: 51.11 through 51.12, 5208.31 through 5208.59, 5209.31 through 5209.59, 5210.31 through 5210.59, 5211.31 through 5211.59, 5212.13 through 5212.15, 5212.23 through 5212.25, 5407.42 through 5407.44, 5407.52 through 5407.54, 5407.61, 5407.72 through 5407.74, 5407.82 through 5407.84, 5407.92 through 5407.94, 5408.22 through 5408.24, 5408.32 through 5408.34, 5512.19, 5512.29, 5512.99, 5513.21 through 5513.49, 5514.21 through 5515.99, 5516.12 through 5516.14, 5516.22 through 5516.24, 5516.32 through 5516.34, 5516.42 through 5516.44, 5516.92 through 5516.94, 6001.10, 6001.92, 6005.31 through 6005.44, or 6006.10 through 6006.44.

Compliance with these rules requires 31 classes of documents ranging from bills of lading and employee time-cards to contracts with dyers and finishers, invoices, proofs of payment and so on; the resulting sheaf of paper is said typically to be about four inches high. Apart from the cost and lawyer-hours involved in verifying all this, rules designed for specific products from particular factories tend to lose relevance over time. In the denim case, the plant in question closed after a chemical accident in 2017, and since then Guatemala, El Salvador, and Honduras have stopped selling jeans to the U.S.

Thus CAFTA producers have been treading water as full-tariff competitors in Southeast Asia boomed. The Jordan agreement and the Haiti programs, simpler as they require only a showing of local added value rather than requiring detailed sourcing, appear much more successful.

Turning back now to Martinez’ journalism and Vice President Harris’ observation, the main point – to lower social temperatures and reduce migration pressure — still seems like a strong one. With it in mind, can we do better? Could individual pieces of the CAFTA/DR that are no longer relevant – perhaps the denim piece — be scrapped? Could Congress allow Central American factories to use cloth and yarn from FTA partners, or Latin America generally? Or perhaps the whole thing might be redone, merged with the “USMCA” and the string of smaller FTAs going south from Panama to Colombia, Peru, and Chile?

* A bit dated as a description of the migrant route around 2010, but still relevant. ‘The Beast’, La Bestia, is a migrant nickname for southern Mexican freight trains.

** Counting Chinese products, many of which are subject to the Trump administration’s additional “301” tariffs. The 2022 rate for Asian clothes excluding Chinese-made goods was 16.6%.

*** Using a cotton T-shirt because this (HTS 61091000) is the top import from the CAFTA/DR countries, at $2.8 billion of the U.S.’ $35 billion in total imports (everything, clothes, coffee, oil, mangoes, etc.) from these countries last year.

Clothing and textile import data in various forms from the Commerce Department’s Office of Textiles and Apparel.

The CAFTA/DR:

Full agreement text for CAFTA/DR; see Chapter 4, Annex 4.1 and “Textiles Amendment” for clothing rules.

An alternative clothing-import table:

The chart at the top counts from the signature of CAFTA/DR in 2005. A more recent count, looking at the decade 2012 to 2022 would be somewhat different, with China down rather than up, Vietnam and Bangladesh getting almost 2/3 of all new imports, and slightly higher growth for the CAFTA/DR countries. Same table, though a bit shorter:

World

+$23.6 billion

Vietnam

+$11.3 billion

Bangladesh

+$5.3 billion

India

+$2.8 billion

CAFTA/DR

+$2.7 billion*

Cambodia

+$2.0 billion

Pakistan

+$1.4 billion

Jordan

+$1.0 billion

Italy

+$1.0 billion

Sri Lanka

+$0.7 billion

Indonesia

+$0.7 billion

Turkey

+$0.7 billion

Egypt

+$0.5 billion

Haiti

+$0.6 billion

Peru

+$0.4 billion

Madagascar

+$0.4 billion

Burma

+$0.4 billion

Kenya

+$0.3 billion

Ethiopia

+$0.3 billion

Colombia

+$0.1 billion

Mexico

-$0.2 billion

China

-$8.4 billion

*Within CAFTA/DR, totals are Nicaragua +$1.4 billion, Guatemala +$0.7 billion, Honduras +$0.6 billion, El Salvador +$0.1billion, Dominican Republic unchanged, Costa Rica -$0.2 billion.

ABOUT ED

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

National Security Advisor Jake Sullivan’s April 27 speech at the Brookings Institution, explaining the Biden administration’s global-economy policies, is an odd piece at an important time. Mr. Sullivan covers a lot of ground in a lengthy (4,981-word) speech: “industrial strategy” and subsidies; trade and tariffs; the U.S. relationship with China; brief excursions into finance, aid, and infrastructure, and so on. Parts of it work well, in particular his passage on China policy. Some other parts less so. That on trade especially is a sort of study in breezy mis-summarization of history, muddy elucidation of current choices, and unclear future direction.

Most important, when taken as a whole and given its timing just as the 2024 presidential campaign begins, the speech seems to be politically out of tune and picking the wrong targets. It is vigorous if defensive in rebuking the Biden administration’s liberal-internationalist friends for their worries that it may be overreaching in industrial strategy and under-reaching in trade policy. It is premature at best in positing that the administration’s global-economy agenda has achieved consensus status as the “project of the 2020s and 2030s,” and does not recognize — despite warnings from allies as important and close to the subject as Japan — the strength of the Chinese counter-“project.” And while spending lots of time in an argument with the 1990s, it elides not only the recent Trump administration record but the domestic political challenge from the administration’s Trumpist/isolationist enemies — which, in a few months, will seek to end the Biden administration, and with it not only Sullivan’s version of international economics but the 80-year liberal-internationalist legacy the speech rightly praises.

“Industrial” 517,000 Electronics 136,000

Automotive 121,000

All other 260,000

Specialized services 121,000

“Consumer” 19 million

* International Federation of Robotics, 11/22

WHAT THEY MEAN:

Reporting from Guangzhou last November, Reuters finds Chinese workers losing interest in manufacturing work:

“More than 80% of Chinese manufacturers faced labor shortages ranging from hundreds to thousands of workers this year, equivalent to 10% to 30% of their workforce, a survey by CIIC Consulting showed. China’s Ministry of Education forecasts a shortage of nearly 30 million manufacturing workers by 2025.”

The article’s young blue-collar Chinese interlocutors now prefer additional education or finding jobs in services (and a startlingly large number, Reuters also says, are “adopting a minimal lifestyle known as ‘lying flat,’ doing just enough to get by and rejecting the rat race of China Inc.”) China’s factories seem, however, to be adapting – in part by trying to offer higher wages, but also by hiring metal and plastic stand-ins. The International Federation of Robotics’ annual snapshot of the robot universe, World Robotics 2022, reports that over half of last year’s 517,385 newly employed industrial robots last year went to work in China, and that Chinese factories are now more robot-heavy than America’s:

“Every other robot globally installed in 2021 ended up in China: Installations surged by 51% to 268,195 units.”

On a broader scale, IFR’s report divides the new-robot picture into three parts:

Industrial robots: Last year’s Chinese robot surge was unusually large, but also reflects a trend sustained over the past decade. China is now by far the world’s top industrial-robot employer, home to 1.22 million working factory robots, or over a third of the world’s 3.48 million total. A contributor to this is the shifting industry-sector balance of robot use: auto plants (especially in the U.S., Japan, Korea, and Germany) were the first and historically the largest employers of robots, but have been surpassed at least in raw numbers by the electronics industry.

By this total count, China is the world’s robot metropolis. A different perspective — the ratio of robots to human workers — finds neighboring Korea easily eclipsing even China’s mighty robot army. The Korean government reports exactly 1,000 robots for every 10,000 Korean factory workers, far ahead of second-place Singapore’s 670 robots per 10,000 factory workers. After them comes Japan at 399 and Germany at 397; China is sixth at 322; and Taiwan and the U.S. essentially tie for eighth at 276 and 274 respectively. (The world average is 141.) Japan, finally, is likely the industrial-robot production center; though this year’s report doesn’t have a figure, last year’s cited Japan as producing 45% of industrial robots.

Specialized services robots: Robot services professionals are fewer in numbers than their proletarian factory cousins — 121,000 new ones last year, about a quarter of the 517,000 new industrials — and (like the human “services sector”) are very diverse. The largest group, 49,500, went to work in logistics, carrying packages in warehouses and delivery centers, and moving industrial components through factories. Another 20,000 took “hospitality” jobs, such as ferrying food from kitchen to table in large restaurants* or greeting customers; 14,800 went to work in hospitals, clinics, or emergency medical services, 12,600 in industrial cleaning work, and about 8,000 in farms, dairy, and ranching. IFR’s report regrettably doesn’t have figures on the countries in which these high-skill robots are lighting up, but notes that (in some contrast to the industrial-robot world, where Japan is the largest producer and neighbors Korea and China the leading users), the U.S. is the largest services-robot manufacturer.

Homes: Finally, 19 million humble domestic robots went to work in homes, mainly for interior cleaning and vacuuming, but also for lawn-mowing.

* The Trade Fact series editor encountered two attentive and polite restaurant robots at a restaurant in Chiang Rai in the northern reaches of Thailand in February. Thai industrial-robot installation rose by 36% last year, to about 4,000.

FURTHER READING:

Chinese workers not so interested in factory jobs.

… but no worries, here are the metal and plastic replacements. Global highlights from the International Federation of Robotics’ World Robotics 2021.

… and IFR’s closer looks at industrial and services robots.

The New York-based Institute of Electrical and Electronics Engineers has a weekly new-robot video. Try the prototype seabed-cleaning jellyfish-robot.

A few looks ahead, and one look back, from robot arts and lit:

Capek’s R.U.R. (1921) invented the word “robot,” and the classic “robot uprising” plot. The title acronym stands for a fictional “Rossum’s Universal Robots” company, with “Rossum” a slightly modified version of the Czech word for “reason,” and “robot” likewise an adapted term for “worker.” A Penn State robotics academic looks at R.U.R. a century later.

In robot-friendly Japan, by contrast, Astro-Boy (said to be the first anime character) is a helpful friend to humanity.

Stanislaw Lem’s “Mortal Engines” collection speculates about machine intelligence. In “The Hunt”, a well-meaning human pilot volunteers to destroy a supposedly mad robot; next, in “Mask,” a troubled, self-aware female robot-assassin tracks down a political dissident.

Philip K. Dick thought humans and robots would lose the ability to distinguish themselves from one another.

And Adrienne Mayer’s Gods and Robots: Myths, Machines, and Ancient Dreams of Technology takes the long look back, at visions of androids, flying cars, computers, and other semi-inventions in classical Greece, with comparators from India, Babylon, and the mechanical men of the Qin Dynasty court.

ABOUT ED

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

FACT: U.S. Customs seizes 75 shipments of counterfeit goods imports each day.

THE NUMBERS: Counterfeit goods seizures by U.S. Customs* –

FY2021 value $3.3 billion

Number of seizures 27,115

FY2016 value $1.4 billion

Number of seizures 31,560

FY 2011 value $1.1 billion

Number of seizures 24,792

* CBP data; “value” is at the “Manufacturers Suggested Retail Price” of an authentic item.

WHAT THEY MEAN:

Here’s fashion magazine Allure with a closeup on the criminal fringe of the global manufacturing economy, through the lens of a 2016 seizure of counterfeit perfume in New York:

“Five men have been arrested in New York by U.S. Immigration and Customs (ICE) for knowingly selling counterfeit designer perfumes made with ingredients including antifreeze and urine across at least seven states … The authorities reportedly recovered approximately 10,000 boxes of the faux scents, whose ingredients included the aforementioned urine and antifreeze along with ‘other unpleasant, flammable, or dangerous chemicals that burn when applied to the skin.’ ”

Background: The most recent big-picture study of trade in counterfeits, a 2021 report from the OECD, estimated an upper limit of $464 billion worth of counterfeit goods flowing across borders in 2019. This would have been 2.5% of that year’s $19.8 trillion in goods exports — not much different from the 3.3% counterfeit share they estimated for 2016 and the same as their 2.5% estimate for 2013. By the OECD’s account, 90% of counterfeit goods come from five places — China, Hong Kong, Singapore, Turkey, and the United Arab Emirates — and the most frequently counterfeited products include shoes, clothes, perfumes and cosmetics (making Allure‘s New York arrest story a pretty representative case), along with watches and leather products like luggage and handbags.

U.S. counterfeit seizure statistics likewise seem to show a fairly stable level of counterfeit trade (or at least of interdictions of counterfeit goods) over the past decade, after a sharp rise in the 2000s. CBP’s FY2011 report tallied 24,792 seizures of counterfeit shipments (about 70 each day), and the 2016 report noted a higher total, at nearly 32,000. The 2021 total, at 27,115 seizures, was in between. Three ways to look at these totals:

(a) Number and kind of products: The 27,115 seizures in 2021 in turn brought in over 115,000 different “lines” of products, which reflect OECD’s report on the most frequently counterfeited goods fairly well: 73,367 seizures of counterfeit designer clothes, shoes, and luggage; 3,155 of personal products like the counterfeit perfumes, medicines, and medical products (including, in that troubled year, 35 million substandard masks and 38,154 useless or dangerous faux-COVID test kits); 5,380 sets of consumer electronics items, and 1,083 shipments of aircraft and auto parts.

(b) Origins: Here the U.S. statistics slightly differ from those of the OECD. As with OECD, they report China and Hong Kong as the top sources, accounting for 51,787 of the 115,000 “lines” of counterfeit goods, and also have Turkey in third with 10,781 lines. The remaining two are the Philippines with 6,416, and Colombia with 5,912.

(c) Transport methods: Counterfeit goods most frequently travel to the U.S. (assuming that CBP’s seizure statistics more or less accurately reflect the counterfeiting industry’s logistics choices) by express deliveries and mail shipments. CBP’s figures show 16,926 of the seized shipments arriving via express delivery, while 7,293 arrived by mail, 2,274 by maritime cargo, and 622 by unspecified other methods. The maritime cargo seizures, however, were apparently very large and valuable; weighted towards consumer electronics counterfeits, they accounted for $1.5 billion or half the total value of all seizures.

The amount of counterfeit goods which get all the way to consumers is by nature uncertain. The CDC, looking closely at medicine, says that “in high-income countries, such as the United States, less than 1% of medicines sold are counterfeit.” Medicines, though, are presumably an area where providers are especially cautious and law enforcement especially vigilant. CBP’s advice to consumers (and the message implicit in Allure’s graphic description of counterfeit perfume ingredients), though, is to be careful with what you buy: “Counterfeit products are low quality and can cause injuries or even death when used.”

FURTHER READING:

Ewww – Allure (2016) on the gross ingredients and nasty side-effects of counterfeit perfume.

… and a similar report this week from CBP, on a seizure of 150 parcels containing 744 counterfeit Botox shipments this Monday in Louisville.

CBP’s one-page, three-point guide for consumer awareness.

… and from the U.S. Trade Representative Office, this morning’s “Special 301” report on intellectual property reviews counterfeiting law and enforcement on pp. 16-20.

U.S. seizure data:

The Customs Service’s annual reports on counterfeit seizures, by country and type of good, back to FY2003. Seizure counts rise steadily from the 5,973 of FY2003 to 14,675 in FY2007 and 19,959 in FY 2010, peak at above 31,000 in FYs 2016, 2017, and 2018, and then drop back a bit to the 27,115 of FY2002. Next update likely in September.

And the World Health Organization’s home-page for counterfeit medicine.

And beyond the borders:

Wealthy countries with sophisticated and efficient customs enforcement record most seizures of counterfeit goods; in lower-income regions, seizures are less systematic and counterfeits are much more likely to reach consumers. As an example, the UN’s Office of Crime and Drug Control reports that substandard or counterfeit medicine rates are above 40% in eight countries — Venezuela, Suriname, Mali, Ghana, Malawi, Nepal, Bhutan, and Vietnam — and between 20% and 39% in 15 more. They published estimates this spring that these counterfeits contribute to as many as 267,000 annual deaths from malaria, and 169,000 deaths from childhood pneumonia. UNODC’s examination of counterfeit medicine in Africa, with a closeup on especially vulnerable low-income Sahelian states.

ABOUT ED

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

FACT: Natural disaster death rates fell by over 90% in the last century.

THE NUMBERS: Annual deaths to natural disasters* –

2020s 13,000 (world population 8 billion)

1970s 99,000 (world population 4 billion)

1920s 524,000 (world population 2 billion)

* Our World in Data

WHAT THEY MEAN:

Each year brings about the same count of floods, earthquakes and tsunamis, droughts, hurricanes and cyclones, and other tragedies and disasters of geology and weather. But the toll these events take on life, society, and the economy seems to lessen over time. Website Our World in Data, using a simultaneously gloomy and hopeful database developed by the University of Louvain, summarizes:

“[O]ver the course of the 20th century there was a significant decline in global deaths from natural disasters. In the early 1900s, the annual average was often in the range of 400,000 to 500,000 deaths. In the second half of the century and into the early 2000s, we have seen a significant decline to less than 100,000 — at least five times lower than these peaks. This decline is even more impressive when we consider the rate of population growth over this period. When we correct for population — showing this data in terms of death rates (measured per 100,000 people) — then we see a more than 10-fold decline over the past century.”

Why? Gingerly comparing two sets of historical tragedies and disasters:

Japan and Earthquakes: This September marks the centennial of the Great Kanto Earthquake, the deadliest in Japanese history, which struck Taisho-era Tokyo in 1923. Believed to have reached 7.8 on the Richter Scale,* the quake killed over 105,000 of the city’s then-2.2 million residents through building collapses and fires. (Based on the Japanese government’s most recent estimates; earlier estimates were closer to 150,000.) The vastly larger Great Tohoku Earthquake of 2011 — 9.1 on the Richter scale, 20 times more powerful than the 1923 event — is thought by geologists the fourth-largest earthquake ever measured anywhere. It nonetheless took many fewer lives, because of the efficiency of Japan’s urban building codes, sea walls able to absorb at least some of the tsunami impact, immediate electronic warnings to bullet trains and motorists, and rapid-response civil defense bureaucracy.

Bangladesh and Cyclones: The Bhola Cyclone which struck Bangladesh in 1970, during which winds reached 145 mph, may have killed half a million people. More recent cyclones, though sometimes comparably powerful, are less deadly. The 2020 “super-Cyclone Amphan” and its 150 mph winds, for example, took 26 lives in Bangladesh, 98 in India’s neighboring West Bengal province, and 4 in Sri Lanka. Drawn from a least-developed country rather than Japan’s high-income, high-tech economy, Bangladesh’s post-Bhola experience is an equally powerful illustration of the ways in which weather service, evacuation drills, cultivated coastal mangrove forests to absorb storm impact, and evacuation drills are, though unable to prevent disasters, can make them far less dangerous.

More generally, the Our World in Data figures suggest that the level of annual disaster deaths is quite variable, and not precisely comparable across time since large individual events often affect not only annual totals but decade-long averages. Nonetheless, the broad trend seems clear. The 1920s featured the highest number of annual disaster deaths on average in OWiD‘s table, at over half a million per year. In the 1970s, a half-century later, the average was just below 100,000 disaster deaths per year. For the 2010s, it was 45,000 per year; and for the incomplete 2020s, the lowest of all at 13,000 per year.

The scale of this decline varies for different kinds of events. The sharpest reductions are in deaths to droughts and consequent famines, which are down 99.8% from the 472,400 per year average of the 1920s to 2,012 per year in the 2010s and 837 per year so far in the 2020s. (Famines remained significant causes of death in South Asia through the 1940s and in China to the early 1960s, and in the Horn of Africa until the last such event in anarchic Somalia 30 years ago. Better infrastructure, emergency relief, globalization, and multiple sources of food can ensure that people don’t starve when local or individual international sources go down, people no longer starve.) Losses to inland river floods have dropped almost as sharply. Those to earthquakes and tsunamis seem more uneven, with the recent averages much affected by the 2007 Port-au-Prince earthquake and the Indian Ocean tsunami which struck Indonesia, Thailand, and Sri Lanka in 2004. Hurricane and cyclone mortality, finally, is down about 90%, from 12,000 to 14,000 per year in the mid-20th century to about 1,600 per year so far in the 2020s, with Bangladesh’s post-Bhola experience striking evidence for the success of preparation and disaster relief in vulnerable least-developed countries. Last word to Our World in Data:

“This trend does not mean that disasters have become less frequent, or less intense. It means the world today is much better at preventing deaths from disasters than in the past.”

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

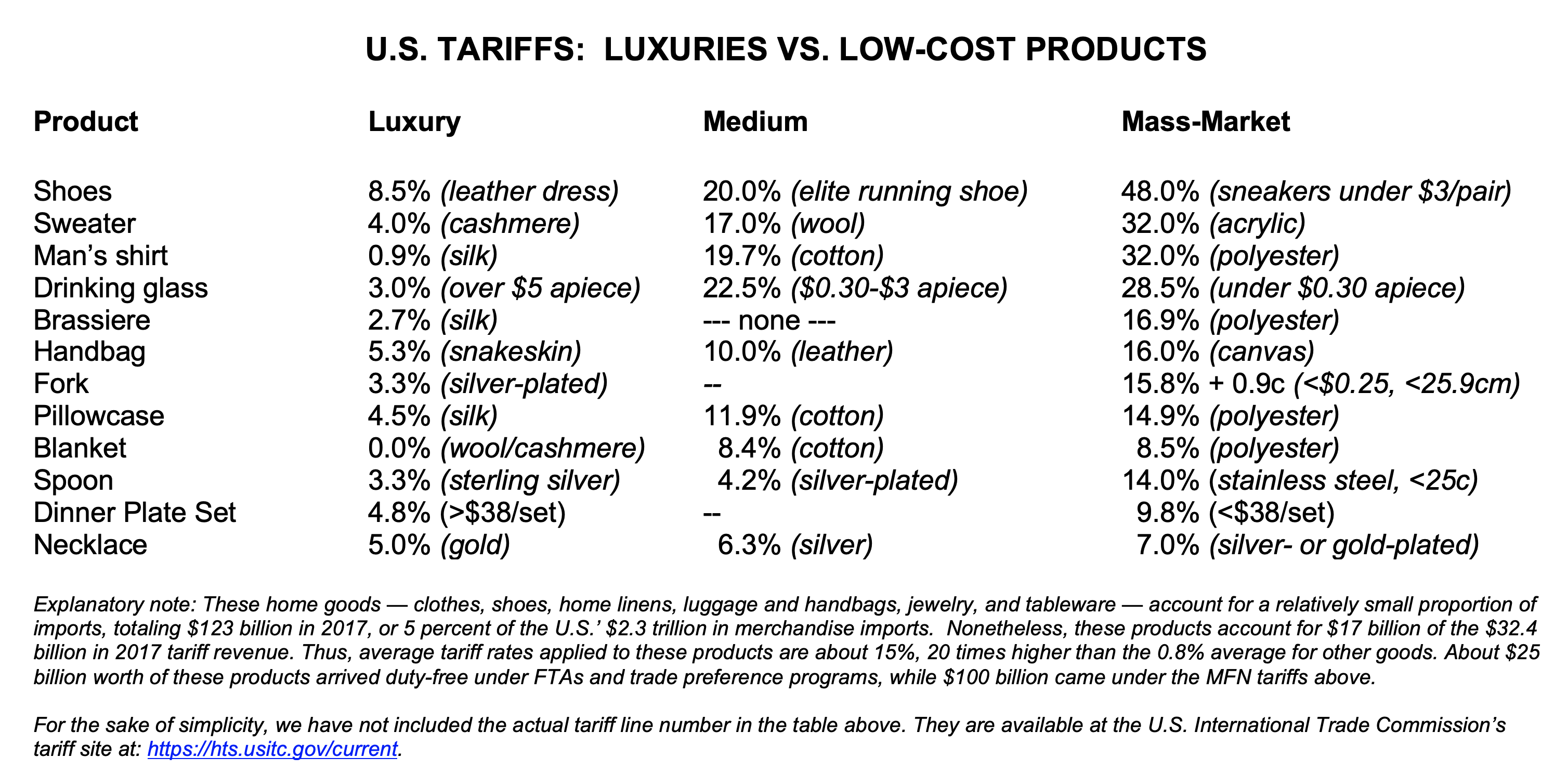

* About 20% for a spoon valued at 25 cents on imports; 25% for a spoon costing 10 cents or less. Tariff lines are 71141130 for sterling silver, 82159930 for stainless steel spoons costing less than 25 cents each, and 82159935 for spoons at or above 25 cents each.

WHAT THEY MEAN:

How is it that cheap spoons are taxed more heavily than sterling silver?

In his 1832 essay on the U.S.’ tariff law, the former Treasury Secretary Albert Gallatin — then a 70-year-old observer and occasional commentator on policy; in earlier life a teenage immigrant from Geneva in the 1780s, a Jeffersonian-Republican politician and founder of the Ways and Means Committee in the 1790s, and Treasury Sec. for the Jefferson and Madison administrations from 1801-1814 — makes a cautious case for progressive taxation:

“Higher duties on luxuries than on articles generally, and in some cases exclusively, used by the less wealthy classes of society are justified by the propriety of laying a heavier burden on those who are the best able to bear it.”

He then glumly notes that, tariffs being an especially opaque way to raise money, and businesses and wealthy people being more able to investigate and complain about their “burdens” than the public in general and the poor in particular, the tariff laws of 1816 and 1828 had done the opposite.

“The principal commodities which have been selected for special protection, iron and all the coarser woollen articles of clothing, are as well as salt, coal, and sugar, essentially necessary to all classes of society. The duties laid on such commodities fall therefore much more heavily, in proportion to their means, on the less wealthy classes; and it has already been seen with what singular ingenuity that on woollens has been so arranged, as to make the poor pay, in every instance, considerably more than the rich. This your memorialists consider to be one of the most obnoxious features of the restrictive system.”

Income and payroll taxes now far exceed the $90 billion tariff system as a U.S. revenue source. But 190 years after Gallatin’s essay, the case of spoons raises some strikingly similar questions. Buyers of cheap stainless steel spoons pay about four times the tax on wealthy neighbors buying sterling, to wit:

(1) Mass-market: Low-priced stainless steel spoons, imported at prices below 25 cents each, get a 14% tariff. For readers familiar with the D.C. metro area, think middle-class and low-income families in Rockville or P.G. County, or the Salvadoran and Ethiopian restaurants along Georgia Avenue just north of the District. No such spoons seem to be made in the U.S. at all.

(2) Luxury: The tariff on sterling silver spoons is 3.3%, a bit less than a quarter of the cheap-stainless rate. Say, McLean and Georgetown, the Mayflower and the Four Seasons, downtown law firms, etc. In this sector, American companies and individuals do make sterling silver spoons, sometimes in batches and sometimes as artisanal pieces, but the prices are high enough to make tariff rates irrelevant.

(3) Mid-tier: More expensive stainless steel falls in the middle, with a 6.8% tariff. One company in upstate New York, Sherill Industries, makes high-priced stainless steel silverware, whose prices seem to average around $4.00 per piece.

Gallatin’s term “obnoxious” is subjective, but doesn’t seem unreasonable here. Neither the cheap-spoon line (“82159930”) nor the sterling line (71141130”) appear to affect trade flows much, so in this case the tariff system is acting much more in its ‘tax’ role than its ‘trade’ role. There’s little doubt that in this case the poor are taxed considerably more than the rich, and the spoons case is more a typical case than a weird anomaly. An illustrative table of 12 products, drawn from PPI testimony to the International Trade Commission last year:

In this perspective, Gallatin seems to identify a structural challenge that remains powerful despite the passage of nineteen decades. Perhaps especially in tariffs as opposed to more transparent income or sales taxes, low-income people often don’t know when they are being taxed and aren’t in a position to ask for lighter burdens. And in the political system, most tariff analysis relates to trade policy rather than the role of tariffs in taxation; Gallatin’s Ways and Means Committee, in fact, appears not to have held a hearing on the tax implications of tariff policy since 1974. So with little knowledge about strange phenomena like the differential rates on stainless steel and sterling even among policymakers, policies rarely get critical examination and “the less wealthy classes” seem to wind up carrying the heavier burdens.

FURTHER READING:

Analysis then and now:

Frederick Taussig’s State Papers and Speeches on the Tariff collection (1892), featuring Gallatin’s 1832 essay along with other 18th- and 19th-century trade policy luminaries (Alexander Hamilton, Daniel Webster, and the now-obscure Robert Walker, who was James K. Polk’s Treasury Secretary in the 1840s).

The Harmonized Tariff Schedule; see Chapter 71, heading 7114 for sterling silver and other precious-metal “silverware,” and Chapter 81, heading 8215 for “base metal.”

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

FACT: Multinationals employ three out of every 10 American workers.

THE NUMBERS: Employees of multinational firms (U.S.- and foreign-based) as a share of total U.S. private-sector employment –

2020 31%

2019 29%

2012 26%

2002 26%

1992 25%

WHAT THEY MEAN:

Here is J.M. Keynes, looking back from 1919 at the “globalized” world of the 1910s, from the perspective of a wealthy (male) Londoner:

“[For] the middle and upper classes, life offered, at a low cost and with the least trouble, conveniences, comforts, and amenities beyond the compass of the richest and most powerful monarchs of other ages. The inhabitant of London could order by telephone, sipping his morning tea in bed, the various products of the whole earth, in such quantity as he might see fit, and reasonably expect their early delivery upon his doorstep; he could at the same moment and by the same means adventure his wealth in the natural resources and new enterprises of any quarter of the world, and share, without exertion or even trouble, in their prospective fruits and advantages; or he could decide to couple the security of his fortunes with the good faith of the townspeople of any substantial municipality in any continent that fancy or information might recommend.”

Taking up his themes of easy and uninterrupted flows of investment and trade a century later, with some employment focus as against Keynes’ investor-and-consumer viewpoint–

The U.N. Conference on Trade and Development’s annual “World Investment Report”, reports that annual cross-border “foreign direct investment” flows have varied between $1 trillion and $2 trillion over the last decade, with the U.S. in most years both the largest source and recipient. Last year was a typical example, with the U.S. receiving $367 billion of the worldwide $1.6 trillion in total inbound FDI flows, and sending out $404 billion.

Reporting each year on these flows’ real-world manifestations, the Commerce Department’s Bureau of Economic Analysis publishes figures on international businesses’ employment, investment stocks, employment, R&D, payrolls, and so forth in the United States and abroad. Their most recent editions cover the year 2020 and find U.S. “affiliates” of foreign-based firms employing 8.6 million workers, and U.S.-based firms with overseas operations employing 28.4 million people in the U.S. (along with 14 million overseas). Together, then, internationally operating businesses employed 37 million private-sector workers, or 31% of the COVID-depressed 120 million total. Two bits of perspective on this:

(1) Economic role: The “multinational’ firms — both U.S. “parents” and foreign “affiliates” — are particularly employers in manufacturing (10 million of 12.2 million), retail (10 million of 17 million, and information industry (2.0 million of 2.7 million). They are also very prominent in private-sector science, together accounting for $430 billion of 2020’s $717 billion in U.S. R&D spending. (U.S.-based firms did most of this at $361 billion, not counting $59 billion in overseas R&D; U.S.-based affiliates of foreign firms contributed $73 billion in U.S.-based R&D. And they account for about two-thirds of U.S. goods trade, including $1.08 trillion of 2020’s $1.66 trillion in exports, and $1.43 trillion of the $2.35 trillion in imports.

(2) Over time: At least with respect to employment, multinationals’ role in U.S. economic life has been pretty stable over the last generation. The 31% share of employment in 2020 is at the high end of BEA’s records, but this is mainly because, before COVID vaccines, employment was especially depressed in industries with fewer multinationals, such as restaurants, hotels, beauty shops, and other small services businesses. Over the last 30 years, the “multinational” share of U.S. employment has varied between 25% and 29% of private-sector workers – or, to cite a few specific years, 26% of the 121 million private-sector workers in 2012, 26% of the 108 million in 2002, and 25% of the 90 million in 1992. Over this time, U.S.-based multinationals have added about 11 million employees in the U.S. (17.5 million then, 28.4 million in 2020), while simultaneously adding 10 million overseas. International firm employment in the U.S. has grown at a slightly faster pace in percentage terms but less sharply in total numbers, rising by about 80% from 4.8 million in 1992 to 8.6 million in 2020.

Lots of money and research, the various products of the world freely available, employment rising at typically modest but positive gradations each year. All this may feel a bit reassuring, as “geopolitics” grows steadily more menacing, and international institutions fray at the edges — but it also makes Keynes’s close, as he reflects on how fragile the apparent calm and stability of his own recent past were, especially unsettling:

“[H]e [the hypothetical upper-middle class Londoner, probably referring to himself] regarded this state of affairs as normal, certain, and permanent, except in the direction of further improvement, and any deviation from it as aberrant, scandalous, and avoidable. The projects and politics of militarism and imperialism, of racial and cultural rivalries, of monopolies, restrictions, and exclusion, which were to play the serpent to this paradise, were little more than the amusements of his daily newspaper, and appeared to exercise almost no influence at all on the ordinary course of social and economic life.”

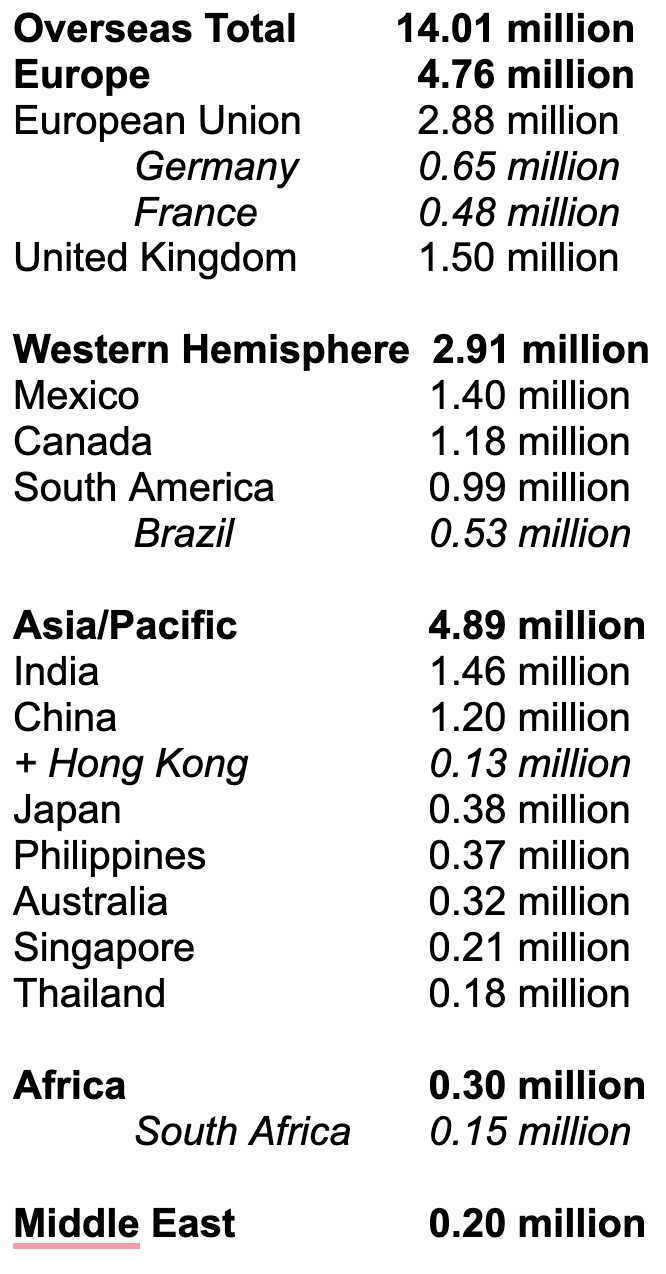

BEA’s figures look at U.S. private-sector investment abroad as well as multinationals operating here, with some detail on destinations for U.S. investment and the ownership of investment here. As both a destination and a source, Europe is the main partner and Canada is disproportionately large. By value (“investment stock”), Europe is home to $4 trillion of $6.5 trillion in U.S. FDI abroad (2020), with the U.K. at $1.0 trillion, EU members $2.7 trillion, and Switzerland, Norway, Iceland, and Turkey together $0.25 trillion. Latin American countries are at $0.25 trillion, led by Mexico at $110 billion; Asia and the Pacific are at $960 billion, topped by Singapore at $294 billion, Australia at $167 billion, and Japan and China both around $118 billion. Measured by jobs, though, U.S. firms employ about as many people in Asia as in Europe. A table of U.S. overseas employment by region:

Looking the other way, European firms are likewise the main international employers in the United States, at 5 million jobs or about 60% of the 8.6 million total. By country, U.K. firms led at 1.2 million, followed by Japanese at just above 1 million, Canadians just below, Germans at 885,000, French at 740,000, and Dutch at 569,000. Japanese firms employed a bit more than 1 million Americans, second only to the Brits; Canadians just a bit less at 940,000. Chinese firms, though receiving much attention and publicity, were modest employers of Americans at 153,000; Mexicans were at 89,000, and Indians 73,000.

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

The venerable International Telecommunications Union (ITU), the world’s oldest “international organization,” has been printing, telegraphing, broadcasting, and posting telecom data since its launch in 1865.* Its most recent look at the digital world, out last September, finds 5.3 billion people, or two-thirds of the world’s 8 billion population, now have internet access. Two observations on this:

(1) This year’s 5.3 billion internet users are nearly three times the 2.0 billion ITU counted in 2010; over ten times the 0.4 billion it found in 2000; and about 1,000 times the roughly 3 million comp sci students, telecom enthusiasts, and government officials using the pre-WWW, copper-cable-based networks of 1990. In high-income countries, more than 90% of people are now online, with the exceptions (if the U.S. is a good sample) mostly infants and elderly people who don’t want service. Many of the newer users — 600 million have logged on since the COVID pandemic — are now in lower-income regions: Least-developed country use has jumped from 89 million to 407 million since 2015, and 40% of sub-Saharan African households are now online, as against 11% in 2015.

(2) Information exchange is rising faster than user count. ITU estimated 1,230 terabits of bandwidth in use every second (Tbps) in 2022, up from 979 Tbps in 2021, and four times the 292 Tbps it found in 2017. About 40% of data exchange goes on in Asia, which accounted for 542 of the 1,230 TBps last year. Europe added 242 TBps, the Western Hemisphere (including the U.S., Canada, the Caribbean, and Latin America) 224, and the rest of the world 220.

Intellectual and cultural assessments of the rising user counts and accelerating data exchanges are always pretty subjective. Economic measurements are also often murky, but there are some useful gauges, especially with respect to the U.S.. The OECD, for example, estimates that the $25 trillion U.S. economy now includes $112 billion in annual sales of data and data-related advertising, and that data stocks are worth about $421 billion in national “wealth.” With respect to trade, the Commerce Department’s Bureau of Economic Analysis reports $89 billion in U.S. exports of information and communications services and $594 billion in digitally deliverable services in 2021 — together, more than a quarter of the $2.26 trillion in total U.S. exports.

In purely physical terms, the growth in user counts will have to slow down by the late 2020s. But the scale of information exchange can easily keep rising, since the physical capacity to carry data continues to grow both under the oceans and above the atmosphere. The glass-watchers at TeleGeography, for example, see 552 submarine cables operating in 2023, with 33 new ones scheduled to go live this year and 19 more so far in 2024. Meanwhile, satellites are handling larger shares of data flow, and 1,000 to 1,500 new ones go into orbit each year.

In ‘governance’ terms, however, questions about fraying policies and thickening cyber-borders seem to be intensifying even as the Internet accommodates more users and carries more information. Examples: steady interest among lots of governments in digital service taxation; last year’s efforts, especially from India, to end the WTO’s 24-year-old “moratorium” on tariffs for digital transmissions; and the quiet but intense ideological tug-of-war between the “internet sovereignty” concepts proposed by authoritarian governments and the “multi-stakeholder”/free flow of data views held traditionally by the U.S. and most liberal democracies, and elaborated in last year’s 61-country Declaration for the Future of the (“open, free, global, interoperable, reliable, and secure”) Internet.

* Created to deal with the questions raised by the deployment of the first telegraph cables; converted into a League of Nations organization in 1919, and a U.N.-specialized agency more recently.

FURTHER READING:

ITU’s 2023 “Facts and Figures” report on internet populations, data exchange, smartphone use, and more worldwide and by region.

… and the 61-country Declaration for the Future of the Internet, including 39 in Europe, five in the Pacific, three in Africa, one in the Middle East, and 9 in the Western Hemisphere (of which two are Caribbean, two North American, one Central American, and four South American).

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

THE NUMBERS: World ozone-depleting substance consumption* – 19891.32 million tons 20050.25 million tons 2010 0.10 million tons 20150.01 million tons?

* Includes chlorofluorocarbons, hydrochlorofluorocarbons, methyl bromide, carbon tetrachloride, halons, and methyl chloroform. (Our World in Data)

WHAT THEY MEAN:

Here is a success story:

Chlorofluorocarbons, known for pronunciation’s sake as “CFCs,” are strings of carbon atoms joined with the halide elements fluorine and chlorine rather than their more common hydrogen-ion partners. First synthesized in 1928 by American refrigerator-makers, they were used worldwide as coolants and industrial solvents from the 1930s to the 1990s by manufacturers, building superintendents, food-service professionals, and home-owners, all of them unaware that CFCs react easily with ozone, and that this, in turn, could have large consequences.

Via eleventh-grade chemistry, meanwhile, ozone is a pungent form of oxygen arranged chemically as “O3,” as distinct from breathable oxygen “O2.” Floating in a “layer” 15-35 kilometers above the earth, ozone absorbs ultraviolet light and in doing so reduces the risk of skin cancer to people, cools lower-atmosphere temperatures, and facilitates photosynthesis in land plants and oceanic phytoplankton. CFCs are fairly stable molecules that float around for a long time — depending on the particular molecule, they can last from 100 to 200 years before breaking up and raining down out of the sky — and react quickly with ozone. Thus their release from buildings and refrigerators began an era of high-atmosphere chemical reactions, which scientists predicted in the 1970s and then detected as a fall in the atmosphere’s “total column ozone” count by 1985. This eased ultraviolet light passage to the earth, with especially large effects over Antarctica where a large “hole” of missing ozone appeared in the early 1980s, first at about 5 million square km and reaching 28 million square km by 2000.

How to respond? The Montreal Protocol, a monument of Reagan-administration and international environmental diplomacy, banned the production and use of CFCs in 1987, and has since been ratified and implemented by 196 countries and territories. Over the ensuing 35 years, production and industrial consumption of CFCs has dropped by about 100%, from 1.1 million tons in 1986 to 43,000 tons in 2005, then to a tiny 63 tons in 2010, and since then oscillating around zero. (“About 100%” and “oscillating” because sometimes discovery and destruction of unused CFC stocks create a negative output; alternatively, sometimes destruction of old buildings inadvertently releases old “banks” of CFC-containing insulation for a small positive output.)

The “Kigali Amendment” negotiated under the Obama administration in 2016 added a ban on hydrofluorocarbons — a temporary replacement for CFCs which are less potent ozone-depleters but have strong greenhouse effects — and made the sale of the next generation of chemicals conditional on participation. This went into effect in 2019, with Senate ratification last fall. The HFCs are supposed to be gone by 2030.

Two results of all this:

(1) CFC atmospheric concentration down: Near zero in 1920, the level of chlorine in the Antarctic stratosphere hit 2.2 parts per billion in 1980 and peaked at 4.7 parts per billion in the mid-1990s. Since then it has been falling by 0.4% to 0.8% per year, with NOAA charts showing “CFC-11” down from 540 points per trillion to 490 ppt since the late 1990s, “CFC-12” from 270 ppt to 220 ppt, and “CFC-113” from 84 ppt to 68 ppt. The current CFC level is about 3.5 parts per billion, and though CFCs degrade only slowly, NOAA’s projections show a return to 1980 levels by the 2070s.

(2) Ozone layer slowly recovering: As CFC levels drop, ozone levels have stabilized. UNEP believes “total column ozone” is rising by about 1% to 3% per year, and the “ozone hole” above Antarctica now oscillates in a range between 16 million square km in 2019 and 24.5 million square km in 2022. The UN Environmental Programme’s 2022 ozone assessment tentatively projects that atmospheric ozone will return to its 1980 levels sometime around the year 2040 worldwide, and in the 2060s for the Antarctic. The reduced emissions of CFC and related gases, meanwhile, appear to have averted a rise of 0.5 to 1 degree Celsius in average global temperatures; and the Kigali Amendment is likely to prevent another 0.5-degree rise.

So altogether: With good scientific evidence, commitment by governments of quite different political outlooks, implementation by bureaucracies and businesses, and some modest temporary sacrifice for the common good, policy can achieve a lot.

FURTHER READING:

Then –

From Ronald Reagan’s enthusiastic comments on the Montreal Protocol in April 1988:

“The Montreal protocol is a model of cooperation. It is a product of the recognition and international consensus that ozone depletion is a global problem, both in terms of its causes and its effects. The protocol is the result of an extraordinary process of scientific study, negotiations among representatives of the business and environmental communities, and of international diplomacy. It is a monumental achievement.”

And NASA’s ‘ozone watch’ tracks ozone density (as measured in Dobson Units) over the South Pole

ABOUT ED

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

* Our World in Data. Note that data (a) is available for 70 countries in 2017 and fewer in earlier years, (b) covers “non-agricultural workers,” so is less dependable for countries with large rural/farming populations, and (c) applies to formal-sector workers for whom data is reported and available, and misses sometimes very large informal-sector workforces.

WHAT THEY MEAN:

The Washington Post reports on an unusual proposal from the Korean Labor Ministry:

“South Korea’s conservative government has proposed increasing the legal cap on weekly work hours from 52 to 69 … South Koreans already toil more than many of their overseas counterparts. They work an average of 1,915 hours a year, compared with 1,791 hours for Americans and 1,490 hours for the French, who have a 35-hour workweek, according to figures from the Organization for Economic Cooperation and Development. The OECD average is 1,716 hours.”

Comparisons like these are a bit fraught. The OECD, whose data covers 44 middle- and upper-income countries plus averages for the EU and the OECD membership, very responsibly warns that its “data are intended for comparisons of trends over time; they are unsuitable for comparisons of the level of average annual hours of work for a given year, because of differences in their sources and method of calculation.” Broader attempts to add low-income country data (for example the 70-country table published by Our World in Data) are even riskier, (a) low-income country statistical agencies may be less accurate; (b) coverage of informal-sector workers in low- and middle-income countries will be either much spottier than formal-sector work or nonexistent; and these surveys typically exclude farm labor, whose share of total jobs is low in high-income regions but often high in low-income countries. All these cautions noted, the available figures do suggest a couple of conclusions:

1. Southeast Asians spend the most time on the job. Our World in Data, whose figures go through 2017, reports that Cambodians — garment-workers in Phnom Penh, hotel maids and concierges around Siem Reap, truckers, and crane operators on the Phnom Penh-Sihanoukville run – spent an average of 2,456 hours on the job that year.* Also in Our World’s top six: Myanmar at 2,438 hours per year, Malaysia and Singapore at 2,238 hours each, and Bangladesh (“South Asian” by geographic convention but in the same neighborhood) at 2,232 hours. The non-Asian representative in the longest-hour tier is Mexico, at 2,255 hours per year. ASEAN generally is a long-hour region: Thai workers rank 10th in the Our World table with 2,185 hours per year, Vietnam and the Philippines 12th and 13th, and Indonesia 19th with 2,024. To the west and north, India and Pakistan clock in at about 2,100 hours each, with China at a slightly higher 2,174 hours.

2. Europeans spend the least time on the job: Relaxed but efficient Europeans show up at the bottom-hour tiers of all three surveys. Defying all stereotypes, Germans work the fewest hours, at 1,354 per year in Our World’s 2017 table, and 1,349 hours in OECD’s 2021 figures. This is the equivalent of 38 five-day weeks, assuming 8-hour days, with 14 weeks off. Just above the Germans come Danes, Luxembourgers, Dutch, Norwegians, Icelanders, Austrians, Swedes, and French, all working less than 1,500 hours per year. EU workers score well on productivity figures, though, so they get a lot done in their limited office/plant/lab/shop time. Americans are pretty near a hypothetical world average (1,757 working hours by Our World’s count and 1,791 hours according to the OECD) with Japan’s 1,738 hours and Australia’s 1,731 about the same. The longest high-income work years turn up in the Baltic states and Taiwan at nearly 2,000 hours each — 30 8-hour days more than Americans — with Hong Kong’s 2,186 hours and Singapore’s 2,238 hours the high-income world’s longest working years.

3. Over time, people work less: In the very big picture, even the world’s highest work-hour totals look modest when matched against those of earlier times. The Our World database includes 11 countries whose labor ministries were able to estimate annual work hours in 1870. All reported over 3,000 hours a year on the job, with Belgium’s 3,455 hours — essentially a ten-hour day, every day with a couple of holidays and no weekends off — looking like the longest year ever measured. The U.K.’s 2,755 hours, the lowest in the 1870 records, is still 300 hours more than Cambodia’s modern estimate. National holidays, 8-hour-day laws, overtime pay rules, and similar legal and regulatory changes brought these remarkable totals down through much of the 20th century. In the U.S.’ case, the 3,096-hour work year of 1870 fell to 2,605 hours by 1913. In 1950, 15 years after the Fair Labor Standards Act, the work year was just above 2,000 hours.

4. No clear recent pattern: Using a more relatable time frame — say, the last generation’s experience since 1990 or 2000 — no clear pattern appears. The U.S.’ total hasn’t changed much — 1,796 hours in 1990, a bump up to 1,845 in 2000, and 1,796 in 2021. On the other hand, work years have lengthened in much of Asia and parts of Latin America — up by 30 to 84 hours in India, Colombia, Cambodia, the Philippines, China, and Indonesia. Elsewhere, though, Thai workers have cut their 2500-hour year by 310 hours since 2000, Taiwanese by 190 hours, Irish by 187 hours, and Chileans and Costa Ricans by 289 and 155. And as the Korean economy has evolved from a heavy-industry center to a services-and-tech “Hallyu Wave” [link: https://www.progressivepolicy.org/blogs/ppis-trade-fact-of-the-week-squid-game-outdrew-the-world-series-this-year-nov-17-2021/], its working year has fallen by a full 600 hours: 2,677 hours in 1990, 2,509 in 2000, 2,063 in 2017, and most recently 1,909 in 2021. This is still a bit long by high-income country standards, but represents a drop of 600 hours, or 75 8-hour days, in a single generation. Perhaps this suggests why senior Labor Ministry bureaucrats, remembering their weekend-less youth, may feel that 69 hours a week isn’t too much to ask?

* As an example, the 2,456-hour average may reflect the experience of a very limited fraction of Cambodian workers, as ILO figures show 92% of Cambodians are in informal work, and World Bank data report that 75% of Cambodians live in rural areas.

The U.S. Geological Survey’s mineral commodity statistics, covering steel, aluminum, and 130 other substantives from abrasives, aggregates, and aluminum to yttrium and zirconium, with salt, pumice through steel, aluminum, rare earth elements, cement, gold, iridium/osmium/platinum, gemstones, tin, and more.

… and Cambodia’s Better Factories program, an ILO-launched system operating since 1999, offers independent inspection for hours, union rights, sexual harassment, and other labor rights standards for garment workers in 557 factories

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.

Ed began his career on Capitol Hill before serving USTR as Policy Advisor to USTR Charlene Barshefsky from 1998 to 2001. He then led PPI’s Trade and Global Markets Project from 2001 to 2011. After PPI, he co-founded and directed the independent think tank Progressive Economy until rejoining USTR in 2015. In 2013, the Washington International Trade Association presented him with its Lighthouse Award, awarded annually to an individual or group for significant contributions to trade policy.

Ed is the author of Freedom from Want: American Liberalism and the Global Economy (2007). He has published in a variety of journals and newspapers, and his research has been cited by leading academics and international organizations including the WTO, World Bank, and International Monetary Fund. He is a graduate of Stanford University and holds a Master’s Degree in International Affairs from Columbia Universities and a certificate from the Averell Harriman Institute for Advanced Study of the Soviet Union.

FACT: U.S. steel and aluminum output have changed little since 2017.

THE NUMBERS: Steel production in the United States –

2000 102 million tons 2001-2010 average 95 million tons 2011-2017 average 84 million tons 2017 total81.6 million tons 2018-2022 average 83 million tons 2022 total82 million tons (first estimate)

WHAT THEY MEAN:

A passage from the Commerce Department’s January 2018 “Section 232” report on the national security implications of steel trade argues for a tariff or global quota, on the grounds that this would (a) reduce imports, (b) thus allow U.S. mills to run at 80% capacity instead of the 74% measured in 2017, and so finally (c) secure a U.S. national security need for long-term sources of locally cast metal. Note in particular the leap of faith in the third sentence: “If a reduction in imports can be combined with an increase in domestic steel demand, as can be reasonably expected …”:

“By reducing import penetration rates to approximately 21 percent, U.S. industry would be able to operate at 80 percent of their capacity utilization. Achieving this level of capacity utilization based on the projected 2017 import levels will require reducing imports from 36 million metric tons to about 23 million metric tons. If a reduction in imports can be combined with an increase in domestic steel demand, as can be reasonably expected [with] rising economic growth rates combined with the increased military spending and infrastructure proposals that the Trump Administration has planned, then U.S. steel mills can be expected to reach a capacity utilization level of 80 percent or greater. This increase in U.S. capacity utilization will enable U.S. steel mills to increase operations significantly in the short-term and improve the financial viability of the industry over the long-term.”

The Department eventually recommended a 25% tariff on most imported steel, and a similar 10% tariff on most imported aluminum, and received these in March 2018. The tariffs are mostly still in place (along with intense controversies between the U.S. and its allies, and at the WTO), though modified by Biden administration agreements with the U.K., EU, and Japan for duty-free imports up to a particular annual quota level.

How do the results look five years later, when compared with the report’s 2018 predictions? Useful figures come from the U.S. Geological Survey, which each year produces concise 2-page reports on mining, smelting, proven reserves, shares of world production, and other stats for 138 metals and minerals, from abrasives and aggregates to yttrium and zirconium, with salt, talc, tin, crushed rocks, gemstones, gold, rare earth elements, platinum group metals, steel, and aluminum in between. This year’s steel section, out January 31, reports the following:

(1) Output: U.S. raw steel production, at 82 million tons in 2022, was about the same as the 81.6 million tons in pre-tariff 2017, after ticking up to 87.8 million tons in 2019 and then dropped during and since the COVID pandemic. The total is more or less the same as the average output over the last decade or in the five pre-232 years.

(2) Capacity utilization: The Federal Reserve’s “FRED” database reports U.S. steel capacity utilization at 72.6% in December 2022, slightly below the 74.0% reported in December 2017. Full-year average figures were 73.5% in 2017 and 74.7% in 2022.

(3) Domestic demand: USGS’ calculates U.S. ‘apparent consumption’ of steel at 96 million tons in 2022, down a bit from 99 million tons in 2017. The 2022 figure is essentially equal to the 2007-2017 average of 95.5 million tons per year (and far below the 104 million-ton average from 1996-2006).

By these measures, the U.S. steel industry looks about the same in 2022 as it did in 2017. Thus the Commerce Department’s prediction that growth plus public policy would create “an increase in domestic demand” for steel, and long-term higher capacity utilization despite the higher prices tariffs would create, didn’t pan out. Two other measures, though, do show some changes:

(4) Trade: U.S. imports of steel were 30 million tons in 2022, well below the 42.4 million tons reported for 2017 and slightly below the 32 million-ton average from 2008 to 2017. U.S. steel exports are also down, though, from 9.6 million tons in 2017 to 8.0 million tons. In effect, since the tariffs U.S. producers have gained some market share within the United States, but lost a bit worldwide.

(5) Employment: USGS finds blast furnaces and steel mill employment down from 80,600 in 2017 to 75,000 in 2022, and foundry employment from 65,000 to 50,000. (More recent Bureau of Labor Statistics shows smaller declines, from 82,000 to 80,000 in mills and from 117,000 to 108,000 in foundries.) Either way, this isn’t a great industrial measure, since lower employment with identical output can easily reflect investment in technologies and higher productivity.

The aluminum story seems pretty similar. USGS’ aluminum survey reports 741,000 tons of primary aluminum output in 2017, rising to 1.09 million tons in 2019 and then falling back to 860,000 tons in 2022. As with steel, 2022 aluminum imports and exports were both below their 2017 levels, with imports down from 6.2 million tons in 2017 to 5.9 million tons in 2022, and exports from 1.3 million tons to 1.0 million tons. Their figure for aluminum import market share has oscillated more violently than that for steel, having risen from 33% in 2014 to 59% in pre-tariff 2017, falling to 38% in 2020 during the COVID pandemic and 41% in 2021, and then jumping back up to 54% in 2022.

In sum, imports of both metals did in fact drop after the tariffs; but the Commerce Department’s anticipation of higher output and higher capacity utilization rates didn’t materialize, and its expectation that tariffs would be consistent with rising domestic use of these metals looks a bit optimistic.

FURTHER READING:

The “Section 232” site for the Commerce Department’s Bureau of Industry and Security, with links to the 2018 reports on steel and aluminum.

The U.S. Geological Survey’s mineral commodity statistics, covering 132 substantives from abrasives, aggregates, and aluminum to yttrium and zirconium, with salt, pumice through steel, aluminum, rare earth elements, cement, gold, iridium/osmium/platinum, gemstones, tin, and more in between.

ABOUT ED

Ed Gresser is Vice President and Director for Trade and Global Markets at PPI.

Ed returns to PPI after working for the think tank from 2001-2011. He most recently served as the Assistant U.S. Trade Representative for Trade Policy and Economics at the Office of the United States Trade Representative (USTR). In this position, he led USTR’s economic research unit from 2015-2021, and chaired the 21-agency Trade Policy Staff Committee.