Kudos for recognizing that the Federal Energy Regulatory Commission is the agency best equipped to consider and approve proposals to build long-distance interstate electric transmission needed to deliver affordable but remote renewable energy to where it is needed. Otherwise, America will not be able to decarbonize our grid or our economy.

“Most homeowners’ insurance policies do not include flood insurance,” says state Insurance Commissioner David Altmaier. Flood insurance can easily add another $1,500 to the bill. All of these costs help make inflation higher in Florida than the national average. By 2100, if greenhouse gas emissions are not dramatically reduced, Florida could face sea levels rise by up to 6 feet, with more than 900,000 properties at risk of being underwater. Welcome to the world of increasingly brutal climate disasters that will make the lives of average Americans, especially the elderly, far more insecure and expensive, if emissions are allowed to continue rising, as they will if Trump or DeSantis becomes president after the next election.

America could have cleaner, cheaper energy if only we could agree to get out of our own way. The obstacle we have created is a thicket of federal and state regulations requiring energy projects to undergo lengthy, expensive, one-by-one government studies, in theory, to determine their environmental impact. But as Earth Day approaches, it’s time we align these regulations with the need to rapidly build clean energy infrastructure to both address the climate crisis and reduce consumer energy costs.

This regulatory process is termed “permitting” because of more than 60 types of federal government permits that can be required for projects, and it stems primarily from the 1969 National Environmental Policy Act (NEPA). Initially conceived as a quick and simple examination for most routine projects, the combination of project siting, NEPA review and issuing permits has morphed into a many-years-long process rife with opportunities for narrow interests to block projects even where they demonstrably serve consumer and public interests and cut emissions. Perversely, clean energy projects, especially low-cost solar power, are most often the projects facing the longest delays.

A major question facing American energy and climate policymakers today is what role abundant U.S. natural gas should play in the global clean energy transition. Some environmental activists oppose all gas use. But a new report from the Progressive Policy Institute (PPI) finds that expanding U.S. liquefied natural gas exports can lower global greenhouse gas emissions significantly, especially if fugitive emissions of methane are deeply reduced.

The climate benefits of America’s shale gas revolution have been evident domestically for years. More than three-fifths of total U.S. carbon dioxide emissions reductions over the period 2005 to 2020 were due to coal-fired power plants being replaced by natural gas plants.

In the last year, since Russia’s invasion of Ukraine, the U.S. has also become the world’s largest liquefied natural gas (LNG) exporter, more than doubling deliveries to Europe. This has helped the EU’s economy withstand the cutoff of most Russian gas, with clear geopolitical and economic benefits. Less appreciated are the emissions reductions achieved, since American LNG has limited the growth in the EU’s coal and also reduced use of higher methane-leaking Russian gas.

President Joe Biden has achieved remarkable success for U.S. climate policy halfway through his term, and his first State of the Union after the midterms should reflect the accomplishments that Democrats have made in passing the Inflation Reduction Act and Democrats and Republicans both for their roles in the IIJA, CHIPS and Science Act, and the ratification of the Kigali Amendment. But what PPI’s Energy and Climate team wants to see most is what comes next: What are President Biden’s climate plans for the next two years of a divided Congress, for 2024, and beyond? And how will Biden position U.S. energy policy amidst continued turbulence in global markets as Russia’s war in Ukraine drags on?

As hundreds of billions in spending and loans flow out of these new federal programs to firms, households, and state and local governments, President Biden and both parties in Congress should look to finally strike a deal reforming federal and other barriers to the deployment of crucial new clean energy technologies held back by the permitting process, environmental review delays, and inter-jurisdictional conflicts. Biden should also call on Congress to fully fund the energy-related provisions of the CHIPS and Science Act authorizing roughly $54 billion for R&D over the next 5 years through programs at ARPA-E, the NSF, and elsewhere. The 2023 Omnibus bill only included partial funding for these investments in basic science and early-stage energy technologies and only for the coming year; fully funding them for the next 5 years will help the U.S. maintain its position at the cutting edge of the energy transition.

Lastly, Biden’s biggest climate challenge is not domestic but international. As my PPI’s Paul Bledsoe has noted, emissions from China alone are greater than all developed countries combined and still growing. The administration must work with our allies to find more effective means of compelling developing nations to reduce their emissions. Simultaneously, working more closely with allies like the EU, U.K., Japan, and South Korea that lack trade agreements with the U.S. will allow closer cooperation on provisions in the IRA that grant bonuses to countries with existing agreements, like Canada and Mexico. And with Russia’s war against Ukraine ongoing, American LNG exports continue to play a vital role in European and global energy markets by maintaining energy security, offering especially low-methane supplies, and displacing coal-fired generation.

Let’s hope 2023 is a year of continued success for America’s clean energy leadership.

This post is part of a series from PPI’s policy experts ahead of President Biden’s State of the Union address. Read more here.

Today, the Progressive Policy Institute’s Innovation Frontier Project (IFP) released a new paper urging United States policymakers to establish a new framework on domestic rare earth element production, including streamlined permitting, tax reform, and high-impact R&D. Report author Daniel Oberhaus argues this new framework is critical for America’s future economic prosperity and the fight for innovation and economic leadership with China.

“When it comes to establishing a robust American rare earths industry, time is of the essence,” writes Daniel Oberhaus in the report. “…China’s dominance of this sector has been wielded for political leverage in the past with disastrous economic consequences that were felt across the globe. This may very well happen again in the future, but the stakes will be even higher given the increasingly central role that rare earths play in our daily lives.”

The report outlines four policy recommendations for a Rare Earths Elements strategy in the U.S., including:

Introducing tax incentives for domestic rare earth elements producers

Establishing a federal coordinating body for rare earths elements mine permitting

Establishing a federal rare earths elements recycling program; and

Prioritizing federal support for rare earths elements alternatives

Daniel Oberhaus is a science writer based in Brooklyn, New York. He was previously a staff writer at Wired magazine covering space exploration and the future of energy. His first book, Extraterrestrial Languages, is about the art and science of interstellar communication and was published by MIT Press in 2019.

Based in Washington, D.C., and housed in the Progressive Policy Institute, the Innovation Frontier Project explores the role of public policy in science, technology and innovation. The project is managed by Jordan Shapiro. Learn more by visiting innovationfrontier.org.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Urges Deep Cuts in U.S. Methane from Gas to Maximize Climate Benefit

A new issue brief authored by the Progressive Policy Institute’s Paul Bledsoe argues the United States can help become a clean energy superpower by leveraging both green innovations and exports of low-emitting U.S.-made natural gas. The issue brief is the first of a series authored by Mr. Bledsoe on the role of U.S. natural gas in the ongoing domestic and global clean energy transition, and is titled “The Climate Case for Expanding U.S. Natural Gas Exports.”

“The policy question for America is: Can and should the U.S. systemically produce and export more gas to reduce domestic and global emissions? This study suggests the answer is emphatically: Yes,” writes report author Paul Bledsoe. “But achieving large security, economic, and climate benefits from increased gas production will require additional actions by the U.S., the industry, our allies, and even coal-consuming nations, especially major reductions of methane emissions.”

Key policy recommendations from the issue brief include:

Increase Domestic Gas Production

Double U.S. Gas Exports

Cut Life Cycle Methane Emissions from Oil and Gas to 0.3%

Retire Coal Plants More Quickly

Improve Gas Infrastructure

Set Goal of Zero-Net Emissions from Gas by 2040

Establish Accurate Global Methane Emissions Data Center; and

Urge Gas-Importing Nations to Establish Methane Emissions Content Standards

The Progressive Policy Institute will be releasing a series of issue briefs on key topics supporting the policy recommendations outlined in this report in the coming weeks, including briefs on how the entrenchment of global coal power locks in record global emissions; Europe’s continuing need for U.S. LNG to displace the use of coal and Russian-exported gas; the actions needed to increase U.S. natural gas production and exports; and how reducing methane and CO2 from U.S. natural gas will maximize climate benefits.

Paul Bledsoe is a strategic adviser at the Progressive Policy Institute and a professorial lecturer at American University’s Center for Environmental Policy. He served on the White House Climate Change Task Force under President Clinton, at the U.S. Department of the Interior, as a staff member at the Senate Finance Committee and for several members of the U.S. House of Representatives. Read his full biography here.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C., with offices in Brussels and Berlin. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

A key question for current American climate, energy, and security policy is what role abundant U.S. natural gas should play in the ongoing domestic and global clean energy transition. This report finds that expanding U.S. natural gas production and exports can cut coal use, lowering domestic and global greenhouse gas emissions, along with other policies to increase renewable power and other forms of clean energy.

Studies consistently show that coal-to-liquefied natural gas (LNG) switching provides net greenhouse gas emissions reductions, usually between 40-50%, meaning the extent of global emissions reductions from coal displacement will be in part determined by how much U.S. liquefied natural gas reaches overseas coal-using nations. In China, for example, coal emissions have grown by 15% over the last decade due to new coal-fired power plants, and data shows gas power plants have the potential to reduce Chinese emissions by up to 35%.

Large reductions in coal emissions are urgently needed for climate protection. Last year, global coal consumption reached an all-time high, fueled by record coal output in China, India, and Indonesia, the world’s three largest producers. Europe, facing sharp reductions in Russian natural gas, also increased coal consumption for the second year in a row, and the U.S. still uses coal for 22% of its electricity. Global coal-fired generation reached an all-time high in 2021, pushing CO₂ emissions from coal power plants to record levels. These increases in coal use drove worldwide greenhouse gas emissions to record highs in 2022, belying any notion that current climate policies alone have been effective in rapidly reducing coal emissions.

In addition, recent investigations by Bloomberg News have found that Chinese coal mines emit massive plumes of methane so large that they accounted for roughly a fifth of total global methane emissions from all oil, gas, coal, and biomass combined. Such huge methane emissions from coal mining suggest that the overall greenhouse gas emissions footprint from China’s coal industry is larger than previously understood, making the case for coal-to-gas switching in China and other coal-producing nations around the world even more compelling.

But to maximize the climate change benefits of American gas displacing coal at home and abroad, the U.S. must also pursue increasingly aggressive reductions of fugitive emissions of methane. Not only is methane a greenhouse gas 86 times more powerful than carbon dioxide in causing warming over the next two decades, but mitigation of methane is uniquely important for limiting near-term global temperature increases that are causing dangerous and expensive climate impacts.

The good news is that ambitious new U.S. methane mitigation regulations from the Biden Administration, methane emission taxes, mitigation funding in recent legislation, and renewed efforts by industry can drive down fugitive emissions of methane from U.S. gas rapidly and far below recent levels. Moreover, three-quarters of methane emissions can be mitigated with current technology, and half can be eliminated at zero net costs to the oil and gas industry. In contrast, estimates of methane emissions from Russian gas are at least 2.8% of total gas volume, and likely much higher, since Kremlin estimates are unreliable and deliberately misleading, and are not subject to any serious new mitigation efforts, making Russian gas worse than coal for the climate.

The climate value of the U.S. shale gas revolution has been evident for many years. According to EIA data, coal to gas switching accounted for as much as 61% of the U.S. emissions reductions over the period 2005-2020. More than 100 U.S. coal plants were converted to natural gas plants from 2011 to 2020.

Meanwhile, abundant U.S. gas has lowered energy and heating prices for U.S. consumers and benefited American manufacturing, not to mention the large balance of payments benefits of revenue flowing into the U.S. from gas exports. If the geopolitical value of U.S. gas was not already evident, Russia’s war on Ukraine has dramatically illustrated its vital importance to America’s allies. U.S. gas exports to Europe over eight months of 2022 tripled, as detailed recently by PPI’s Elan Sykes, rapidly helping Europe move toward its new goal of shaking free of Vladimir Putin’s energy blackmail, while keeping EU natural gas prices far lower than expected in the last several months.Indeed, U.S. gas supplies have now been credited with lowering overall European inflation, boosting the EU economy at a crucial moment.

But Russia’s war on Ukraine shows no signs of resolution, so increased U.S. LNG exports will continue to be crucial to Europe’s emissions reductions for many years to come, helping the EU further reduce its reliance on high-methane-leaking Russian natural gas while also limiting EU coal use.

Leading analysts like Kaushal Ramesh at Rystad Energy expect large growth in EU LNG demand from about 72mn tons a year in 2021, to more than 110mn tons each year from now until at least 2030. Trevor Sikorski of Energy Aspects anticipates tight EU and global gas supply through 2025, and says that gas will play an EU role until 2040.

Similarly, expanding U.S. gas exports to fast-growing Asian nations and others around the world now primarily reliant on coal consumption can cut emissions and help prevent Russia from dominating new global gas export markets. Economic growth in the region, particularly in China and India, is expected to drive demand for a wide range of energy sources, including natural gas. Due to low lifecycle emissions of methane, U.S. liquefied natural gas delivered to China has, on average, at least 30% lower lifecycle greenhouse gas emissions than Chinese coal does, and according to many measures, U.S. LNG has about 50% less or even lower lifecycle emissions than older Chinese coal-fired plants. A similar industry study finds a 48% emissions reduction.

A private study by a leading environmental organization finds that net reductions from existing coal-fired power plants in Vietnam switching to U.S. LNG would be about 40%. Research by EQT, a leading U.S. gas supplier, finds that replacing older coal plants in Vietnam with Northeastern Pennsylvania gas would result between 53% and 58% life-cycle net emissions reductions. The EQT analysis finds that U.S. LNG is currently replacing ~900,000 tons of international coal per day. As noted, IEA finds in general that coal-to-gas switching reduces emissions by 50%.

On this basis, we argue that Asia should not only increase its use of natural gas to displace coal, but do so particularly by purchasing LNG imports from the United States and other lower methane-emitting sources, rather than sourcing natural gas from Russia. We find that lower methane emissions gas systems give the United States a significant competitive advantage versus other sources of gas, an advantage that is likely to grow as the U.S. institutes ever more stringent methane regulations.

U.S. proven natural gas reserves are massive and can accommodate large increases in domestic and global use for several decades, to help reduce coal domestically and globally. But as a practical matter, large increases of U.S. LNG exports will require even larger domestic production increases so that domestic gas prices stay low and popular political support for exports continues. Studies show that the U.S. can dramatically increase gas exports and production for more than two decades during the clean energy transition while keeping domestic prices low, at roughly $3 per million British thermal unit (MMBtu), which is likely to be the benchmark for cost-effective production in the long term. Additional U.S. gas production will be needed to meet growing EU demand of perhaps 7 billion and 8 billion cubic feet per day (bcfd) demand in the next three to five years, but can offer export prices of less than $8/MMBtu, compared to recent peak European gas prices of $40 to $70/MMBtu.

But this will require expanding U.S. natural gas infrastructure, including gas pipelines, LNG export terminals, and other facilities as part of an overall energy deployment policy based on permitting reform, which will provide even greater benefits to renewable energy. In particular, the U.S. should prioritize efforts to provide pipelines and other infrastructure to bring low-cost Appalachian gas to domestic and international markets, helping to limit inflation. All of this suggests that along with unprecedented U.S. incentives for other forms of cleaner energy passed in major bills over the last two years, American policymakers should now add the climate change benefits of expanding U.S. gas production and exports to the already strong geopolitical and domestic economic case for greater gas production in the near-term.

Indeed, the combination of a huge build-out of American clean energy technologies and low-emitting natural gas puts the U.S. in a uniquely enviable position to both dramatically reduce its domestic greenhouse gas emissions and help catalyze major global greenhouse gas reductions, in effect becoming a clean energy superpower. The U.S. will increasingly export not only natural gas, but also key technologies like carbon capture and storage (CCS) and electricity storage, and others. CCS, in particular, will be necessary for economies around the world to not just limit emissions from natural gas power plants, but to decarbonize heavy industries like steel, cement, aluminum, and other sectors that make up roughly 20% of U.S. and global carbon dioxide emissions. Advances in using CCS in natural gas plants can play a role in this process, especially if industrial use brings down costs. Overall, one can imagine a sustainable U.S. system in which renewable energy, electric vehicles, electricity storage, nuclear power, hydropower, and natural gas with carbon capture create a near-or-net-zero emissions energy economy well before 2050.

Yet, ironically, some left-leaning climate advocates oppose coal-to-natural gas fuel switching, even as worldwide coal consumption has continued to grow. These doctrinaire advocates insist on grouping coal and natural gas together as sources that must be immediately curtailed, despite the fact that gas displaced roughly half of U.S. coal in the last 15 years, and coal-to-gas switching was responsible for more than 60% of U.S. emissions cuts during that period. It’s time honest climate advocates faced a fundamental fact: Natural gas production can have a crucial role in a successful global climate and clean energy transition, especially in the near-term. Indeed, it seems clear that as a practical economic and geopolitical matter, the greatest extent of near-term climate progress cannot be made without gas (along with renewable power) helping to balance electricity grids and rapidly phase out coal, in the West, in Asia, and elsewhere.

At the same time, small but vocal elements on the political right are in denial about the need to deeply and quickly cut methane emissions from natural gas (and, over time, CO₂) so that gas can reduce emissions to the greatest extent possible. But analysis consistently finds that both coal-to-gas switching and deep methane cuts must take place to maximize the economic, geopolitical and climate value of overall U.S. energy approaches. Policymakers should ignore these ideological, not factual, appeals emanating from both fringes of the political debate.

In the next two decades, much more electric power will be needed in America and globally. Electricity demand will grow significantly, in part due to the electrification of transportation through the adoption of electric vehicles, which could raise U.S. electric power demand alone by as much as 38%. One underappreciated advantage of natural gas power plants is their ability to provide rapid onset baseload power to balance electric grids increasingly dependent on intermittent renewable energy, with gas plants able to cycle up to full power within five or 10 minutes, providing synchronicity with renewable energy. In contrast, other forms of baseload power like nuclear and coal plants take far longer to deliver power to the grid when the sun stops shining and the wind stops blowing. Natural gas-fired plants that operate in a combined-cycle configuration are more efficient than coal-fired plants, producing electricity with significantly less energy input than coal, helping to further lower CO₂ emissions.

But U.S. gas must continue to dramatically reduce emissions of both methane and carbon dioxide. As new methane detection technologies are deployed, the U.S. gas industry will be able to prove that American natural gas can achieve among the lowest emissions of methane of any gas exports in the world, gaining a competitive advantage over higher-leaking systems and rival exports like those from Russia. Currently, many

gas-importing nations, especially in Europe, are skeptical of large methane emissions reductions achieved by the U.S. in recent years. Such a competitive advantage of proving low fugitive emissions of methane from U.S. gas should also jumpstart global efforts by other major gas exports to limit methane leaks from their gas exports, as importers favor lower methane-leaking gas.

This “race to cut methane” can greatly increase the climate benefits of using gas to displace higher-emitting coal globally, and has already begun as evidenced by methane emissions reductions programs by major gas exports like Qatar. More rapid adoption of carbon capture technologies on gas fired power plants will be needed to cut overall GHG emissions from gas.

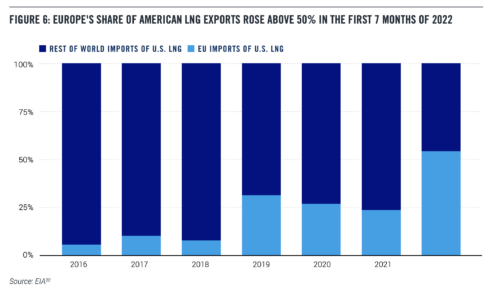

Total U.S. LNG exports increased only slightly in the first eight months of 2022, since short-term capacity is largely fixed, so the main way that gas shipments to the EU increased involved exporters redirecting shipments away from other destinations, mainly Asia. Europe received 23% of U.S. LNG in 2021, but 54% through August of 2022.

Of course, a main reason U.S. LNG was redirected to Europe was the higher price, with European spot natural gas prices often running several times those in other markets, including Asia. But for now, thanks in part to U.S. LNG, European prices have moderated.

In 2022, U.S. exports of natural gas as LNG rose 8% to 10.6 bcfd, just behind Australia’s 10.7 bcfd. The United States remained ahead of Qatar, which in third place shipped 10.5 bcfd., though the U.S. is set to take the global lead on LNG exports early in 2023.

Overall, the U.S. gas industry is forecast to produce approximately 100 bcfd in 2023, so exports are likely to be somewhat more than 10% of national production.

Total U.S. LNG exports are expected to rise in 2023, although by how much is uncertain, as major new export facilities are not expected to reach full output until 2025.

The long-term role of gas beyond this decade is less clear. It may turn out that over the coming years renewable energy will continue to see dramatic price reductions making it far cheaper than other sources, although renewable energy would still need to be built more quickly and at tremendous scale. And other technologies like electricity storage may see advances that allow for electric grids to absorb greater amounts of intermittent renewable energy. But these developments are also uncertain. What is clear is that both the U.S. and EU have used gas to displace coal in large amounts, and to stabilize their electric grids to use more renewable energy, while much of the rest of the world has not. That presents a near-term opportunity for U.S. LNG exports to reduce global coal use significantly, limiting emissions in the process.

The policy question for America is: Can and should the U.S. systemically produce and export more gas to reduce domestic and global emissions? This study suggests the answer is emphatically: Yes. But achieving the security, economic, and climate benefits from increased gas production will require additional actions by the U.S., the industry, our allies, and even coal-consuming nations. To gain these benefits from increased gas production and exports, this report recommends the following policy actions.

POLICY RECOMMENDATIONS

Increase Domestic Gas Production

The United States should increase natural gas production substantially to allow for expansion of exports to Europe, Asia, and other markets through this decade, while at the same time keeping domestic natural gas prices low to help U.S. consumers, America’s industrial economy, and further phasing out of domestic coal. The precise size of U.S. gas production and export increases will be dependent on a range of market, gas price, regulatory, and investment factors, but a national goal of increasing overall gas production from 2022 levels by 2028 is achievable and in U.S. economic, security, and climate interests. For example, to account for a doubling of new LNG exports, U.S. overall gas production would expand by about 10%.

Double U.S. Gas Exports

Internationally, the U.S. should increase LNG export levels as an explicit goal of U.S. policy, as articulated by President Joe Biden in 2021, specifically to help Europe end its dependence on Russian gas and help the EU reduce their dependence on high-emitting coal. The U.S. should also increase LNG exports to many other coal-dependent nations, including China, to encourage

coal-to-gas switching as a critical element in reducing overall global greenhouse gas emissions. The total size of U.S. LNG export growth will be in part dependent on natural gas prices in Europe, Asia, and elsewhere. But given new LNG export facility construction, we propose an overall U.S. goal of doubling LNG exports over 2022 levels by 2028, in keeping with increases in total U.S. gas production with some of that increase going to phase out domestic coal more quickly. Today the U.S. has six major LNG export terminals. Three new U.S. LNG export facilities now under construction will be at full output by 2025, and provide about half the LNG needed to meet the doubling goal. But several additional export facilities would still need to be built or existing exports expanded. The U.S. Energy Information Agency expects U.S. LNG exports to increase 65% by 2033.

Retire Coal Plants More Quickly

The U.S. should increase the pace of unabated coal-fired power plant retirements (coal still provides 22% of U.S. electricity) as a climate policy priority, using all available methods, including new power plant emissions regulations, increased energy efficiency, renewable energy, nuclear and hydropower, and coal-to-natural gas switching; the latter which has been responsible for well over half of U.S. emissions reductions since 2005.

Improve Gas Infrastructure

Meeting these objectives will require significant new investments in and permitting of U.S. natural gas pipelines and export facilities, as well as broader energy permitting reforms that will benefit renewable energy, gas, long-distance, high voltage electric power lines, and other elements of America’s clean energy infrastructure. U.S. policy should encourage all of these investments consistent with broader U.S. decarbonization and clean energy goals.

Cut Life Cycle Methane Emissions from Oil and Gas to 0.3%

The U.S. should adopt a national goal of driving down lifecycle methane emissions from domestically-produced gas to less than 0.3% of overall gas volume by 2030, from about 1.7% in recent years, so that U.S. gas has demonstrably the lowest methane emissions in the world. New methane detection technologies in the U.S. can help prove these reductions. Overall, the net cost of such mitigation is low, and will be more than made up for on a national level by revenue from increased LNG exports.

Set Goal of Zero-Net Emissions from Gas by 2040

The U.S. should also embrace a goal of near-zero methane emissions by 2040, as well as net-zero carbon dioxide emissions from U.S. natural gas power plants by 2040, through carbon capture and storage, hydrogen, direct air capture, and other technologies.

Establish Accurate Global Methane Emissions Data Center

OECD nations should within two years establish a definitive, accurate inventory of methane emissions from major natural gas producing and exporting countries, to improve on the current situation in which wildly differing methane data are offered by governments, industry, and NGOs, each with their own agendas and methods. It is in the interest of the U.S. that such definitive and accurate methane emissions data numbers be derived, since U.S. methane emissions are far lower than many other global exporters, specifically Russia, and falling rapidly. New satellite, drone, and other methane detectiontechnologies should allow the accumulation of accurate statistics regarding methane emissions in the next year or two if needed investments are made. The International Energy Agency could be one organization considered to act as a clearinghouse for such accurate methane emissions data.

Urge Gas-Importing Nations to Establish Methane Emissions Content Standards

As accurate methane data is established, major gas-importing regions like the EU should establish methane emissions regulations for all gas imports, driving the global system toward stringent methane standards to make gas even more beneficial to the climate while freezing out Russia’s antiquated, leaky system, and in the long-run forcing it to reform.

NOTE TO READERS

PPI will be releasing additional Issue Briefs on key topics supporting these recommendations in the next few weeks, including on:

Entrenchment of Global Coal Power Locks in Record Global Emissions

Europe’s Continuing Need for U.S. LNG to Displace Coal and Russian Gas

Asia’s Growing Opportunity for Coal-to-Gas Switching

Actions Needed to Increase U.S. Natural Gas Production and Exports

Reducing Methane and CO₂ from U.S. Natural Gas to Maximize Climate Benefits

Taken together, today’s recommendations and these upcoming briefs will compromise a comprehensive report on the topic.

The stunning protests by average Chinese citizens against Xi Jinping’s disastrous Covid lockdowns may open the door not just to less restrictive Covid approaches, but to global outrage over an even more cataclysmic threat—China’s out of control greenhouse gas emissions that are destabilizing the global climate.

The latest protests in China are reminiscent not just of Tiananmen Square demonstrations in 1989, but also of the public outcry from 2013-2017 against China’s crippling air pollution. Those protests proved politically powerful enough to force at least some improvements in Beijing’s air quality, prompting new investments in clean energy and slight changes to China’s intensely polluting industrial economy.

Yet these mostly cosmetic actions have done little to slow planet-endangering greenhouse gas growth presided over by Xi. China’s yearly emissions are now more than 31% of the global total. That’s more than all emissions from the U.S. and every other developed country on earth combined. And unlike the U.S., EU and our allies who are spending hundreds of billions of dollars to deeply cut our greenhouse gases, China’s emissions are still rising.

The current Democratic trifecta is coming to a close, and Republicans will be taking back power in the House this January. The lame-duck Congress looks to be productive, but one item that fell shortmay come back to haunt Democrats.

Permitting reform — a push by Sen. Joe Manchin (D-WV) to change the way big infrastructure projects that involve federal dollars are approved — was a notably divisive proposal that supporters had hoped would pass in the lame duck. On December 15, the Senate, in a 47-47 vote, rejected a bid to add the measure as an amendment to a must-pass defense bill. It was a personal loss for Manchin but a potentially bigger one for a key Democratic priority: building out a clean energy infrastructure, and fast.

Today, the Progressive Policy Institute (PPI) released a new policy brief examining Europe’s energy supplies before and after Russia’s invasion of Ukraine, and the role the U.S. has played in expanding exports to the EU in the wake of the war. The policy brief is titled “Russian Shutoffs and American Exports: Explaining the European Natural Gas Shortage,” and is authored by Elan Sykes, Energy Policy Analyst at the Progressive Policy Institute.

“The United States is uniquely positioned to help our allies in Europe whether the energy crisis caused by Putin’s war, and one tool we have is ramping up exports of LNG during the EU’s time of great need. We can’t stand idle as Europe considers burning more coal to get through the winter,” said policy brief author Elan Sykes.

As outlined in the brief, U.S. Liquefied Natural Gas (LNG) exports increased by nearly three times from January to August in 2022, compared to the same period in 2021. Policy brief author Elan Sykes argues the U.S. should continue to boost exports of LNG to Europe to avoid a forced transition to dirtier energy sources like coal — or even more painful energy shortages, factory shutdowns, and skyrocketing household energy costs. He also urges the U.S., the EU, and other allies with ambitious climate agendas to seize on the crisis as an opportunity to expand and speed up deployment of clean energy and energy efficiency technologies to the greatest extent possible.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

Russia invaded Ukraine in February 2022, placing the European Union in a bind and forcing a choice between supporting Ukraine with aid, arms sales, and sanctions on Russia on the one hand, or withholding support to maintain Russian natural gas supplies. Before the invasion, Russia served as the largest supplier of natural gas to the EU through multiple pipeline systems and as Liquified Natural Gas (LNG). Europe chose support for Ukraine, and two key pipelines were shut off following the invasion.

The EU has sought to increase LNG imports from around the world to make up the gap as best as possible, and global gas prices skyrocketed as a consequence. The U.S. has stepped in as a key LNG supplier, sending nearly triple the quantity of LNG to the EU through August 2022 compared to the first eight months of 2021. The U.S., EU, and other allies with ambitious climate agendas should also seize on the crisis as an opportunity to expand and speed up deployment of clean energy and efficiency technologies to the greatest extent possible.

American exports are limited by the available capacity of liquefaction terminals, so the increase in shipments to Europe has come at the expense of other global customers for U.S. natural gas. The EU has spent the past several months purchasing as much LNG as possible to hit storage targets, along with a raft of policies aimed at expanding alternative sources of energy, encouraging conservation, and supporting households with subsidies.

The squeeze on supplies has loosened since September, as storage tanks across Europe have reached their capacity, and warm fall weather lessened seasonal demand. Through a combination of luck with the weather, curtailed industrial output, and expensive inventory buildup through LNG import growth, the European Union has made it nearly to the end of 2022 without a disaster. But the limits of LNG import and storage capacity, the vagaries of winter weather, and success in deploying clean energy and efficiency technologies will each continue to affect the EU, its energy markets, and its climate ambitions for the foreseeable future.

EU ENERGY SUPPLIES BEFORE AND AFTER RUSSIA’S INVASION

In terms of overall supply, the EU imported 58% of its energy in 2020, down slightly from the pre-pandemic figure of 60% in 2019. Natural gas makes up 24% of all the primary energy consumed in the EU, with import dependency and share of natural gas in overall energy supply varying by country.

In 2019, a “normal” pre-pandemic year, the EU’s total energy supply added up to 16.5 Petawatthours, of which 24% or 3.9 PWh came from natural gas. In that year, the EU imported a total of 440 bcm of natural gas, of which 38% came from Russia through the Nord Stream, Yamal, Turkstream, and Ukrainian pipeline systems and via LNG tanker. The remaining share was supplied by Norwegian, North African, and Turkish-Azerbaijani pipelines and by LNG tankers from around the world. After Russia, the largest exporters of LNG in 2019 were Qatar, Nigeria, and the United States (which supplied 3% of EU gas imports in 2019).

This picture of Europe’s pre-war energy reliance underscores the importance of Russia’s decision to weaponize its energy resources since its invasion of Ukraine. The Yamal Pipeline, running through Belarus to Poland, has been shut off since July. Now, the Nord Stream pipeline in the Baltic, which was running below capacity for several months while Gazprom claimed maintenance issues but is now offline due to suspected sabotage, is permanently out of commission as well. Prior to the invasion and shutoffs, these pipelines would be supplying roughly 800 mcm and 1,200 mcm respectively per week around this time of year.

The set of pipelines running through Ukraine supplied more variable quantities of natural gas in pre-invasion years, but has been supplying between 260-280 mcm of natural gas per week, or roughly 10-20% below prewar maximums ranging from 1550-2250 mcm per week. Unlike the other three main pipeline systems sending Russian gas to the EU, the Turkstream pipeline has not been severely curtailed, but it supplies smaller, variable amounts with a range this year of 34 to 323 mcm per week.

Cumulative Russian gas exports through midOctober to the EU and the U.K., as measured by Bruegel and ENTSOG, dropped by 74.5 bcm compared to the average for the same length of time for the years 2015-2020. That leaves a huge hole in Europe’s energy supply, equivalent to 4.8% of total energy supply for the EU in 2019. If Russian exports continue at 500 mcm per week, roughly continuing the trend since August, the total loss will reach 6.8%.

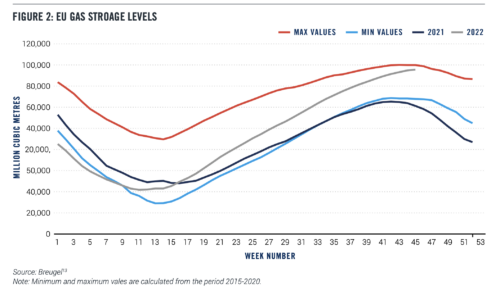

Imports and storage have helped make up part of this gap, but due to their relatively fixed capacity can only contribute as much as the EU’s present energy infrastructure allows. Data from the EU’s gas transmission system shared by Breugel show that European storage has filled to nearly the all-time maximum as importers rushed to replace cut off Russian supplies even after prices spiked:

While the Breugel data for 2021 and for previous years show that gas stocks usually started drawing down at this time of year, that’s happening more slowly this year as Europe attempts to store the absolute most it can for the winter. But since storage is nearly full and LNG imports do not necessarily have a place to go in the EU, LNG future prices have dropped back to a point comparable to post-invasion, preshutoff levels:

Looking ahead, future markets expect prices to stay elevated for the coming year at least and major uncertainties remain. In the meantime, painful tradeoffs are being made. The EU agreed to union-wide targets for storage, which they have since exceeded, and for reductions in gas demand of 15% through this coming March.

While good weather so far this fall kept building heat demand for gas low, the elevated price of natural gas has still hit consumers in heating, electricity, and especially industry. Industrial gas consumption dropped by 25% in the third quarter of this year, and continued high costs have come to threaten the viability of European plants in energy-intensive industries like chemicals, basic metals, and mineral producers. High gas costs also are passed through electricity prices to other energy-intensive industries that do not consume significant quantities of gas directly, and to households.

In France, where a nuclear-heavy grid might have been expected to lessen the blow to the power system, a set of prolonged maintenance issues have kept reactors from providing a crucial backstop. The EU and its member states are exploring and adopting various policy tools to subsidize households, diversify supplies of gas, and speed deployment of efficiency upgrades, renewables, and electrified end-use technologies like heat pumps that can help replace gas combustion where possible.

Many of these initiatives will take time to bear fruit, and in the meantime nobody in the financial markets or elsewhere can fully predict the most important immediate factor in Europe’s energy shortage: the weather this winter. A cold winter means higher demand for heating and electricity, and fixed import and storage capacity might not be able to keep up without painful tradeoffs for the EU.

AMERICAN LNG TO THE RESCUE

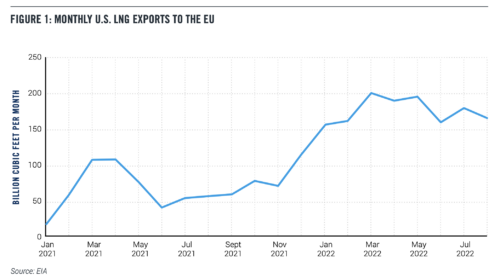

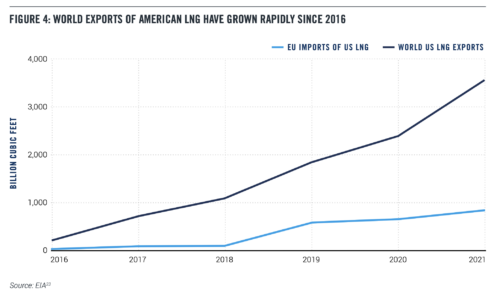

Into the Russia-sized hole in European energy budgets step the United States, Qatar, and Nigeria. A major global producer and now exporter of oil and natural gas, America is host to the largest LNG export capacity of any country in the world, with seven liquefaction terminals together averaging 11.1 bcf in exports per day in the first half of this year.

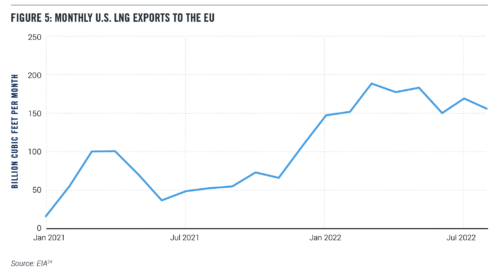

U.S. exports to the EU were already growing for years before the invasion, as the graph above shows. But U.S. firms have stepped up shipments to the EU massively since Russia’s invasion:

U.S. LNG exports to Europe increased by 2.8 times in the first eight months of 2022 compared to the same period in 2021, up from 512 bcf to 1,413 bcf. EU neighbors Turkey and the U.K. also roughly doubled their imports of American LNG over these periods, up by 67 bcf and 123 bcf, respectively. Global US LNG exports increased slightly in that time, to 2.6 trillion cubic feet through August of this year from 2.3 tcf in the first eight months of 2021, but capacity is fixed in the short run (absent maintenance problems like the May 2022 fire at the Freeport terminal, which is expected to resume exports soon).

While the “size of the pie” of overall U.S. gas exports grew ever so slightly, the main way that gas shipments to the EU have increased is by taking a larger slice of it from other would-be importers of U.S. LNG around the world, from 23% last year to 54% through August of this year.

For example, big customers of U.S. LNG in South America and Asia have seen sharp drops in American imports in 2022 so far. Brazil, Argentina, and Chile together imported 213 bcf less in 2022 than the same period in 2021. In East Asia, a slight increase in shipments to Taiwan was dwarfed by the huge drop in aggregate imports of China, India, Japan, and South Korea for a net decrease of 541 bcf. Smaller importers around the globe lost out too, as these decreases among big importers outside of Europe did not entirely offset the ravenous EU. As noted above, the share of overall American LNG exports going to Europe shot up from 23% last year to 54% so far this year.

Diverting shipments to the EU has the benefit of easing Russia-induced shortages across the Atlantic, but this strategy creates tradeoffs. Trading a concentrated, acute shortage in Europe for a diffuse shortage around the world means that the losers of a natural gas bidding war must contend with higher prices and foregone economic activity. Some will take the option of burning more coal instead, releasing more carbon dioxide and air pollution into the atmosphere.

CONCLUSION

Since the Nord Stream pipeline has now been not only shut off but damaged in a probable sabotage, global LNG suppliers have shipped nearly as much gas as storage can hold. Meanwhile, the war shows no signs of abating as Ukraine continues to claw back territories supposedly “annexed” by Russia. Europe thus could face a prolonged energy shortage and will continue importing significant volumes of LNG for the foreseeable future.

The United States must continue to boost exports of its relatively cleaner natural gas to Europe and the world. Otherwise, EU countries and other would-be gas importers could be forced to burn more coal to keep the lights on, or endure painful energy shortages.

Entering winter with nearly full storage capacity in the EU, global prices are higher than preinvasion benchmarks but dropping from their end-of-summer/fall peak. With futures prices high for the coming years, planned expansions to U.S. export capacity will help as they come online, but will take years. Expansions underway at three more liquefaction facilities are not expected to increase peak capacity from 13.9 bcf per day to 19.6 bcf per day until the end of 2025. With demand dependent on the uncontrollable factor of winter weather and short-run capacity for U.S. exports fixed, there remains much to do outside of direct increases in U.S. exports.

In Europe, supply-side policies to boost alternatives to natural gas such as expanding renewables generation and keeping older nuclear plants online will help keep the kilowatts flowing, emissions down, and energy costs from spiraling. Support on the demand side for electrified appliances to replace gas heaters and stoves and efficiency upgrades like insulation will ease the pressure on limited gas inventories and household finances.

These recommendations apply in equal measure to the U.S., where electrification and climate tech deployment can help add to the suite of available options for American consumers increasingly exposed to fickle international gas markets.

Planned expansions of LNG export capacity, and the pipeline systems required to feed them, should be acknowledged as a means to reduce global power-system emissions wherever they replace marginal coal combustion or natural gas produced in countries with higher leakage rates. As the methane mitigation policies in the Inflation Reduction Act and other potential policies like the new U.S. pledge at COP27 help reduce the impact of U.S. gas extraction upstream, the carbon advantage and climate benefits of globally abundant American LNG will grow.

Finally, as PPI has noted elsewhere, if American natural gas is to help Europe meet its carbon reduction targets, reducing upstream leaks and providing support to complementary energy technologies that speed decarbonization need to be part of the policy package.

The big news out of COP 27, the UN climate negotiations, according to most media was a global agreement to create a fund to provide developing nations more aid to explicitly address rising climate change impacts. Yet, this action, while justified, is at best a thin, temporary band aid. Because without deep cuts in greenhouse gases from huge polluters like China, the cost of climate impacts will soon skyrocket into the trillions, overwhelming the ability of rich and poor countries alike to address it.

So, what was done in Egypt to actually limit emissions and control global temperature increases, which after all is the central goal of the 2015 Paris climate agreement? Precious little. Instead, a perverse sort of political correctness on the global left overtook the needed focus on solving the climate crisis, much of which is now inarguably caused by autocratic nations like China, Russia, Turkey, Iran and Saudi Arabia, who were barely mentioned during these talks.

China’s annual emissions alone are nearly one-third of the global total, more than all the developed countries combined, and still rising. Global greenhouse emissions cannot decline — and climate protection cannot be achieved — until and unless China begins to cut its emissions. Yet, China was never under any intense pressure from developing nations to act at these negotiations. China’s President Xi Jinping, fresh from gaining a third consecutive five-year term as the leader of the Communist Party Conference, didn’t even bother to show up. Never mind, that China consumes nearly 60 percent of the world’s coal each year!

Election seasons always feature exaggerated divisions, with candidates drawing bright lines between themselves and opponents. But lasting problems come when discourse devolves into false choices between important shared goals. Improving U.S. energy security and preventing catastrophic climate change are issues sometimes falsely opposed during election cycles, when there is little reason that they should be in competition.

For the last decade, during a period of relatively stable energy prices, public discussion has focused primarily on climate risk, for good reason. But as Americans deal with higher energy prices and Europe faces a full-blown energy supply crisis, it’s clear that sustainability and security are intertwined goals. Russia’s weaponization of energy and its impacts on EU climate ambitions provide the starkest example of the interdependency of climate, costs and security.

A timely new report, published today by the Progressive Policy Institute’s Paul Bledsoe and Elan Sykes, argues the Biden Administration and the Democratic-controlled Congress’s historic clean energy and climate projects, passed in the Infrastructure Investment and Jobs Act, the CHIPs and Science Act and the Inflation Reduction Act, face major roadblocks that could threaten delivering on the promises of green innovation in the United States. The report authors find that America’s clean energy transition is dependent on permitting reform.

“If these reforms are not adopted, chances are we will face trillions of dollars in annual climate change impact costs in the U.S. and globally, and climate change impacts increasingly undermining domestic and global economic growth and security. The U.S. has made the initial policy investments to set the stage for clean energy and climate change success — now we must help ourselves, and the world, finish the job. No policy actions are more important,” write authors Paul Bledsoe, Strategic Adviser for the Progressive Policy Institute and Elan Sykes, Energy Policy Analyst at the Progressive Policy Institute in the report.

The report comes as Sen. Joe Manchin’s push for permitting reform has met pressure from far-left environmental groups, progressive activists, and members of the House Progressive Caucus. These concerns, which are overwrought, ignore the consensus among environmental analysts that slow regulatory review is creating more environmental and economic costs as we act to fight climate change.

Key policy recommendations from the report include:

Passing the Permitting Proposal led by Sen. Manchin and Sen. Majority Leader Schumer

Authorizing the study of successful permitting reforms – including the FCC’s ‘shot clock’ for cell tower siting

Passing the SITE Act, which would empower the Federal Energy Regulatory Commission as the siting authority for transmission projects that are currently forced to go through lengthy and fragmented approval processes and improve eminent domain procedures.

Maximizing Green Categorical Exclusions and Programmatic Reviews

Making reforms at the State and Local levels; and

Preventing new regulations from hindering new technologies.

Paul Bledsoe is a strategic adviser at the Progressive Policy Institute and a professorial lecturer at American University’s Center for Environmental Policy. He served on the White House Climate Change Task Force under President Clinton, at the U.S. Department of the Interior, as a staff member at the Senate Finance Committee and for several members of the U.S. House of Representatives. Read his full biography here.

Elan Sykes is an Energy Policy Analyst at PPI. Elan works on energy deployment, innovation, and decarbonization. Prior to joining PPI, Elan served as a researcher at the Climate Leadership Council where he focused on carbon pricing, global climate policy, and the intersection of climate and trade policies.

The Progressive Policy Institute (PPI) is a catalyst for policy innovation and political reform based in Washington, D.C., with offices in Brussels and Berlin. Its mission is to create radically pragmatic ideas for moving America beyond ideological and partisan deadlock. Learn more about PPI by visiting progressivepolicy.org.

The Biden Administration and the Democratic-controlled Congress have earned plaudits for enacting unprecedented funding for clean energy incentives and climate protection. These include provisions in the bipartisan infrastructure law (IIJA), the U.S. competitiveness legislation (CHIPS), sections of the Inflation Reduction Act (IRA), and other legislation, totaling approximately $514 billion in new spending on clean energy and climate, not including other related infrastructure funding.[1] Taken together, these new laws represent the greatest investment in new U.S. energy infrastructure in nearly a century.

And yet, because of regulatory roadblocks and nuisance litigation, it is unclear that this new funding will deliver on its two policy goals:

1) Rapid, low-cost build out of a powerhouse, world-leading U.S. clean energy sector.

2) Large reductions in domestic greenhouse gas emissions (GHG) necessary to put the U.S. in a vanguard position to force emissions reductions by other key emitting nations globally.[2]

America must lead the world as a whole toward a rapid clean energy revolution and decarbonization. But a big obstacle stands in our way:

A broken domestic U.S. energy permitting system that imposes tremendously high costs in time and money to build clean energy infrastructure projects, if they get built at all.

Ironically, in the name of environmental protection, a perverse process has set in whereby often unnecessary and duplicative government reviews and nuisance lawsuits have pushed average time for permitting to 4.3 years for transmission, 3.5 years for pipelines, and 2.7 years for renewable energy generation projects. Notably, these numbers don’t include those many hundreds of projects that are abandoned and never built because costs — often in the millions or tens of millions — and delays have become too burdensome for developers. These long, costly delays and false starts are simply not consistent with a rapid and cost-effective build out of U.S. clean energy generation and transmission, new hydrogen and carbon management infrastructure, or deep reductions in domestic GHG emissions in keeping with U.S. policy goals and climate science. In fact, initial studies note that without permitting and regulatory reforms, projectedclimate and economic benefits of these recent laws wouldbe artificially limited and fail to meet policy goals.[3],[4]

Equally, the potential economic and climate upsides for the U.S. of the actions recommended in this report are tremendous. Multiple studies[5],[6] show the IIJA, CHIPS and especially IRA new laws hold remarkable U.S. economic promise, including:

Growing the overall U.S. economy and new clean energy sector worth trillions each year;[7] creating millions of good, new jobs;[8] reducing consumer and business energy costs by 4% or $50 billion by 2050, while saving the average households hundreds of dollars each year;[9] and expanding U.S. technology and energy exports.

Reducing U.S. greenhouse gas emissions approximately 40% by 2030 below 2005 levels;[10],[11] the IRA bill alone would enable the U.S. to close 50% to 66% of the emissions gap between business-as-usual emissions and the Biden goal of 50% emissions reduction by 2030.[12] Together, the three new laws will help cut the near and long-term costs of climate change impacts and lower threats to public safety; protect worker productivity; improve public health and reducing health care costs;[13] enhance national and global security; and increase long-term U.S. competitiveness in the fast-growing global clean energy economy that will be worth tens of trillions of dollars during the 21st century.

But major studies that find large economic, clean energy, and climate benefits all assume significant improvements in clean energy project permitting and regulatory streamlining. Respected analysis also finds that to ensure these major benefits occur, and to maximize all potential economic and climate benefits[14] will require additional actions by the Administration and Congress.

When Senators Joe Manchin, D-W.Va., and Chuck Schumer, D-N.Y., announced that they had come to an agreement to pass the investments in energy and healthcare that became the Inflation Reduction Act, they also agreed to push for reforms aimed at speeding up the lengthy federal environmental review and permitting process. A draft summary of the deal proposes a prioritization process for strategically important projects, changes to review timelines and litigation rules, and reforms for certain projects and project-types.

The Manchin-Schumer proposal offers a path forward for the crucial reforms amid a narrowing window of opportunity for action this Congress. Leading Democratic climate hawks in the Senate, including Senators Brian Schatz, D-Hawaii, Martin Heinrich, D-N.M., and Ron Wyden, D-Ore., who helped designed the clean energy tax credit package that formed the core of the IRA’s climate component, have endorsed the call for swifter regulatory review and permitting of clean energy projects.

Unfortunately, however, the proposal has drawn fire from some far-left environmental groups and progressive activists. In the House, 77 members, most members of the left-wing Progressive Caucus, signed a letter arguing that permitting reform should not be included as part of a must-pass government funding bill, and may undermine efforts to improve environmental justice. Several senators, including Senators Ed Markey, D-Mass., and Bernie Sanders, I-Vt., have leveled similar concerns. Such fears are overwrought. There’s a growing consensus among environment analysts that slow regulatory review in fact creates environmental as well as other costs, and that slowing climate change is the most crucial goal of environmental justice.[15] Many of the key Manchin-Schumer proposals regarding NEPA administration, electric transmission, and hydrogen merely extend the benefits of existing law on infrastructure permitting, widening the scope of FAST-41 support through the Permitting Council to cover more energy projects and provide additional resources to coordinate and complete their reviews efficiently at a time where timely energy infrastructure deployment is of the utmost economic, political, and climate importance.[16]

The Manchin-Schumer proposals would not eviscerate environmental protections. Rather, in most cases, it will simply codify existing NEPA and other provisions, like those allowing simultaneous agency reviews, and greater use of the categorical exclusion process, already allowed under current law, as noted by leading Democratic siting expert Daniel Adamson.[17]

The proposal would also bring the U.S. in line with other advanced countries, notably the EU and Canada, which have high levels of environmental protection while maintaining firm deadlines for environmental reviews.[18],[19]

For years, most Republicans have advocated reforms not dissimilar to Manchin-Schumer, but Congressional Republicans are so far withholding support for the pending proposal, appearing wary of giving Democrats an additional legislative accomplishment. Now Senate Republicans, led by Senator Shelley Moore Capito, R-W.Va., have unveiled a new permitting reform blueprint, supported by 38 GOP senators. Their approach gives states “sole authority” over regulations on fracking on federal land and would allow states the right to “develop energy resources” on federal land within their boundaries. In general, the Republican approach only indirectly and insufficiently improves problems with renewables or transmission siting while taking a much more aggressive stance on oil and gas development on public lands, banning the Biden administration’s interim Social Cost of Carbon estimate, and codifying many of the Trump administration’s attempted changes to undermine environmental regulation.[20] These provisions are therefore not serious attempts to further the U.S. clean energy transition or limit greenhouse gas emissions in keeping with needed climate protection.

Our report describes in depth the ways in which our current regulatory systems are fundamentally broken, and concludes with the following recommendations to Congress for accelerating government reviews and permitting, including:

Pass the Manchin-Schumer Permitting Proposal:

The quickest and best step available to speed up permitting immediately and unleash the investments made in the IIJA, CHIPS, and IRA package is to pass the Manchin-Schumer proposal. This must include Reforming Energy Project Permitting and Streamlining Regulatory Hurdles, including under the National Environmental Policy Act (NEPA), as envisioned in pending legislation, specifically for major high voltage electric power lines to carry renewable energy from remote areas of generation to regions of strong demand; Natural gas and CO2 pipelines; Electricity Storage projects; Electric and other advanced vehicle charging and fuel infrastructure; Carbon Capture and Storage and Direct Air Capture technologies; Advanced Nuclear Power; Advanced Geothermal, and many other new technologies.

Study and Consider Adopting Successful Permitting Reforms — including 2-Year “Shot Clock” — from Other Sectors:

Congress should authorize the study of successful permitting reform in other parts of the economy, including the Federal Communications Commission’s adoption of time limiting “shot clocks” for the siting of cell phone and communications towers, with an eye toward adopting this time limit for appropriate energy projects. Applying these procedures to key green projects like grid-scale solar, wind turbines, battery storage, and transmission lines on public lands will ensure developers of rapid government decision-making that can increase certainty, reduce costly delays, and help speed up deployment. With all of the new resources available to agencies for permitting in the IRA, quick decisions will not undercut thorough examination of any localized impacts from these well-understood and environmentally critical projects.

Pass the SITE Act:

This bill, written by Senator Sheldon Whitehouse, D-R.I., and cosponsored by leading climate advocates Senators John Hickenlooper, D-Colo., and Martin Heinrich, D-N.M., and others in the House, would empower Federal Energy Regulatory Commission as the siting authority for transmission projects that are currently forced to go through lengthy and fragmented approval processes and improve eminent domain procedures. Ideally, these provisions would be included in reform legislation passing Congress this year.

Maximize Exclusions and Programmatic Reviews:

A Categorical Exclusion (CE) is a group of actions that a federal agency has determined, after review by White House Council on Environmental Quality, do not individually or cumulatively have a significant effect on the human environment and for which, therefore, neither an environmental assessment nor an environmental impact statement is normally required. Legislation should seek to expand the use of CE whenever possible, requiring use of the fasted possible review process available under law.

Reforms at the State and Local Levels:

At the state and local levels, policymakers should look for parallel opportunities to reform slow or outdated review, siting, and permitting procedures that in many cases are just as onerous, costly, and counterproductive as federal regulations. State and local jurisdictions are host to many crucial opportunities for clean energy deployment that will not rise to the federal level, including distributed renewable generation, local transportation networks, and denser forms of housing development. In New York, a new Office of Renewable Energy Siting established in 2020 has already improved on the older, more arduous approval process by consolidating and expediting siting and review requirements and empowering the State to override local restrictions on renewable energy that are “unreasonably burdensome”; this model should be emulated more widely by other states, especially California, whose California Environmental Quality Act is notoriously for many years of delaying needed energy infrastructure.

Prevent New Regulations from Hindering New Technology:

New permitting hurdles or regulatory bottlenecks may also emerge as innovative technologies like direct air capture, carbon capture, utilization and storage, CO2 pipelines, hydrogen hubs, advanced nuclear, and advanced geothermal wells scale up. These and other new clean energy technologies may require additional regulatory actions as they are more widely commercialized; however, federal policy makers in Congress and the Executive Branch must guard against the imposition of new unnecessary regulatory burdens especially those that delay needed infrastructure buildout.

A Broken Permitting System and Regulatory Gridlock

With the incentives to deploy clean energy technologies in place following the passage of IIJA, IRA, and partially-funded CHIPS, these permitting reforms are crucial for ensuring maximum economic and climate benefits. In fact, initial studies find that without permitting and regulatory reforms, projected climate and economic benefits of these new law would be severely limited and fail to meet policy goals.[21],[22] Congress should work quickly to pass them as proposed and continue to search for additional ways to speed up deployment.

The federal environmental review, siting, and permitting process (hereafter summarized as “permitting”) is a complex collection of requirements that oblige project sponsors to submit lengthy documents outlining the project’s impact on the environment and analyzing potential alternative projects. Depending on the type of project, federal law may require analysis under the 1969 National Environmental Policy Act, or NEPA, which can take several forms depending on the type of project and its expected impact. NEPA review can take one of three forms, increasing in stringency from Categorical Exclusions, which are intended to exempt unimpactful projects from unnecessary scrutiny, Environmental Assessments, or EAs, a sort of intermediate review after which a project can be declared to have no significant impact (FONSI), submit a “mitigated FONSI” that lays out steps taken to reduce the project’s impact and ensure that it stays below the threshold for further review, or sent up to the highest level of review, an Environmental Impact Statement, or EIS.[23],[24] Large projects with expected significant impacts go straight to the EIS stage. Only after the Final EIS is issued can federal agencies make final decisions regarding the project, including determinations made along the way on 64 different types of permit that might be required depending on the nature of a project.[25]

While initial NEPA reviews were generally brief documents produced quickly, the intervening decades have seen a marked increase in the completion time and page counts of NEPA review documents. In 2020 the CEQ released a report finding that recently published EISs took 4.5 years to complete from formal Notice of Intent to final Record of Decision and ran for an average of 661 pages — not counting the average 1,042 pages of appendices.[26] And while Categorical Exclusions and Environmental Assessments are quicker and shorter, the federal government is responsible for issuing many more of them, somewhere on the order of 10,000 EAs and 100,000 CEs per year, and so while a comprehensive assessment of their time and financial cost to the government does not exist, the cumulative resources dedicated to them are significant.[27]

Permitting Council data for a representative sample of energy sector projects from 2010 to 2017 bears out the finding that permitting adds years to these crucial projects: the average time from formal start to final decision averaged 4.3 years for transmission, 3.5 for pipelines, and 2.7 years for renewable energy generation projects.[28],[29] These reports are costly to produce for both the government and for private developers, not just in staff and consultant salaries, but also by adding years of delay where investment is tied up but cannot be deployed productively.[30]

These average review times obscure the occasionally devastating impact that NEPA review and equivalent requirements from state governments can have on clean energy infrastructure and other pro-environment projects. Cape Wind, an offshore project that would have been the first of its kind in the U.S., was caught up in litigation for 16 years; another Massachusetts project, Vineyard Wind, is finally going ahead after years of NEPA review and Trump administration-imposed delays.[31],[32],[33] On land, a wind project in Wyoming took 11 years for approval.[34] New York City’s congestion pricing program, a valuable attempt to incentivize cleaner alternative transport modes and disincentivize traffic that clogs Manhattan’s streets, is being put off for NEPA review as well.[35] At a time when climate change is exacerbating extreme weather phenomena and brutal wildfires rage in the Western U.S., NEPA delays USFS wildfire prevention by an average of 3.6 to 7.2 years depending on the project type.[36] Recent analysis finds that U.S. coal fired power plants that have been scheduled to close are staying open, in many cases in order to stabilize regional electricity grids, which are running into regulatory and permitting roadblocks in expanding intermittent wind and solar power.[37]

Sadly, the problem of environmental review bogging down environmentally critical projects is not exclusive to federal law. At the state level, regulations, such as California’s CEQA, have proved a similar barrier to green projects like high-speed rail between San Francisco and LA and to San Francisco’s bike lanes.[38],[39],[40] Climate-beneficial projects in other states have also encountered this problem, such as the rezoning of Minneapolis to allow denser and more climate-efficient forms of housing which was successfully sued under MERA, Minnesota’s state-level NEPA equivalent.[41] In Iowa, one analysis has found that local ordinances restricting wind turbines may obstruct more than half of future wind power development needed in the state for U.S. net-zero 2050 goals.[42] While this paper is focused on federal reforms, many of the issues discussed here also apply to this patchwork of varied and occasionally stifling state permitting processes that require reform as well.

Energy Permitting and the Deployment Challenge

The ability of the new programs laid out in the IIJA, CHIPS, and IRA to achieve their goals and maximize the public benefit depends on our ability to build the infrastructure and technologies they fund. This means rapid buildout of vast new low-carbon electricity generation, which in turn will require significant changes to our electricity grids in the form of long-distance transmission, large-scale storage, and resilience upgrades, along with new technologies to turn this clean energy into useful applications for industry, transportation, and buildings. Now, the funding is in place to make significant progress on this buildout, but the fraction of costs spent on bureaucratic paperwork and time spent waiting with NEPA review, siting decisions, and permits pending remain to be determined.

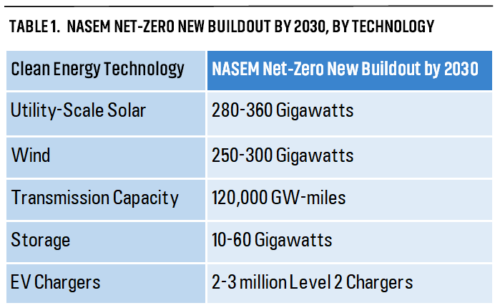

Just how much new energy infrastructure will be required? The National Academies report, Accelerating Decarbonization of the U.S. Energy System, lays out the scientific consensus on what the U.S. will need to deploy to reach net-zero emissions: far more than is currently in operation.[43] And all of this new deployment must happen at an accelerating pace.

Expert energy systems modelers have estimated that the IRA will accelerate renewable deployment significantly: The REPEAT Project at Princeton University’s ZERO Lab has projected that, absent permitting and siting obstacles, the IRA could spur 39 GW of wind and 49 GW of grid-scale solar per year by 2025 and 2026.[44] Energy Innovation, another modeling group, projects that the cumulative wind and solar generation on the grid could reach between 795-1053 GW by 2030 thanks to the IRA funding.[45] Both modeling reports, however, explicitly call out permitting and transmission capacity as potential bottlenecks that could limit this deployment.

Compared against historical renewable deployment rates, achieving this acceleration and ambitious net-zero targets will be a huge lift. For the last two decades, wind and solar generation have grown rapidly in the U.S. as technology improved, costs declined, and public policy support generally expanded. Between 2001 and 2021, the U.S. installed a total of 130 GW of wind and 95 GW of solar (including distributed and thermal solar — utility-scale PV generation is smaller, and in 2020 nameplate capacity for all of the U.S. was only 46.6 GW).[46],[47] Annual net capacity additions for the last 10 years in the same data averaged 9 GW each of wind and solar.

In that time, projects as small as 0.1 GW (10 MW) of solar and as large as 3 GW of wind were subject to NEPA reviews counted in the FPISC review, where renewable project permitting times stretched for an average of 2.7 years each. If each fraction of a gigawatt takes almost 3 years to secure federal permits, and the transmission upgrades needed to carry that power to consumers takes over 4 years per project, the modeled effects of the IIJA and IRA will never come to pass. Instead of rapid progress on clean energy, the funding appropriated in these laws will pay for slow-moving projects and countless person-hours of duplicative, unnecessarily burdensome reviews.

And for newer clean energy projects on the cutting edge of technology, like new advanced nuclear power, advanced geothermal, hydrogen hubs, and carbon management infrastructure in the form of capture and storage, direct air capture, and CO2 pipelines will struggle even harder. Because these technologies are newer, they may present novel environmental impact questions that take longer to sort out at first. All the more reason, then, to ensure that permitting staff are able to focus on these new technologies rather than clogging up their agenda with well-understood and environmentally vital renewable energy and transmission projects.

Passage of the Infrastructure Investment and Jobs Act and the Inflation Reduction Act’s clean energy provisions has committed the nation to deploy renewable generation capacity and battery storage at several times the historic pace. Permitting reform can help us step up the tempo of installing new solar panels, wind turbines, and other clean generation; upgrading aging transmission grids and ensuring reliable supplies; millions of new EV charging stations funded with $7.5 billion in the IIJA, improving energy efficiency in mass transit and buildings; and launching innovative new carbon management and clean hydrogen regional hubs. We should demand the highest possible public benefits from these investments.

Modest Steps Forward

The permitting problem is not new and several previous attempts to speed up approvals have helped incrementally improve the process.